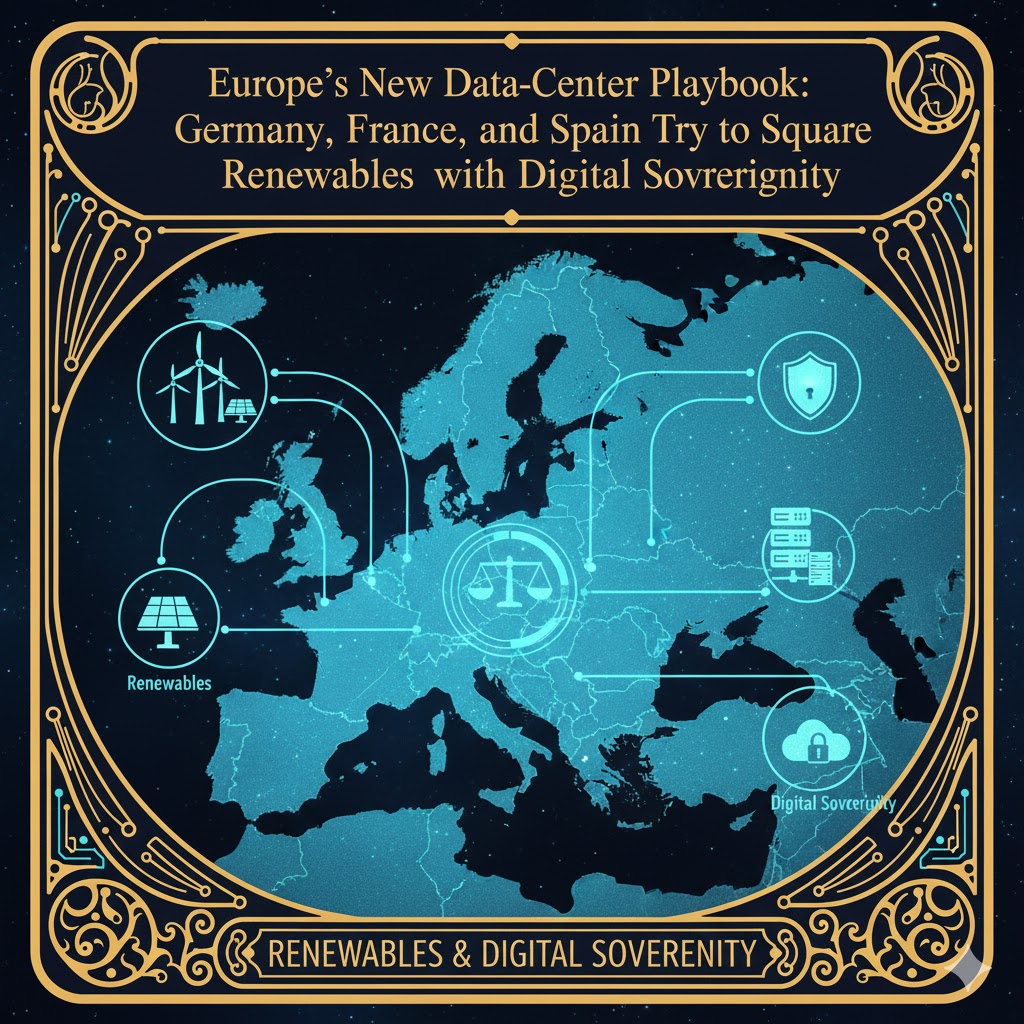

TL;DR:

- Germany has turned its Energy Efficiency Act (EnEfG) into one of the world’s toughest data-center mandates: 50% renewable electricity from Jan 1, 2024, moving to 100% by Jan 1, 2027, plus binding reporting and waste-heat reuse obligations. White & Case+2MHP Management- und IT-Beratung+2

- France is leaning on its low-carbon nuclear-heavy grid and a massive AI build-out, pairing sovereign-compute rhetoric with €109B in AI-linked investments and utility-driven site provisioning for multi-GW campuses. Sifted+2Reuters+2

- Spain has proposed a Royal Decree that would hard-wire efficiency, transparency, and sustainability into new builds (≥1 MW), pushing beyond EU baselines—public consultation closed Sept 15, 2025. Ashurst+1

The strategic tension: Europe’s regulatory lead could deliver greener, more sovereign compute—but also slower, costlier capacity versus U.S. hyperscalers and unconstrained markets. For AI-scale power (hundreds of MW to multi-GW), grid connection, build-speed, and cost of capital will decide winners.

Why this matters now

Generative-AI has collapsed infrastructure roadmaps from years to quarters. Europe is racing to anchor sovereign computing capacity while making sustainability non-negotiable. The result is a three-country microcosm of Europe’s wager: mandate first, scale fast later—and hope policy accelerators can offset project risk and timing.

Advanced Concepts for Renewable Energy Supply of Data Centres

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Germany: Mandates with teeth

Berlin’s Energy Efficiency Act (EnEfG) sets hard rails for operators:

- Renewables ramp: 50% renewable electricity from 2024; 100% by 2027. This is not a “best effort”—it’s a compliance requirement. White & Case

- Scope & timing: Applies to DCs ≥300 kW connection power, with detailed metering, monitoring, and publication of energy and waste-heat data. MHP Management- und IT-Beratung+1

- Waste-heat reuse: Facilities must plan for recovery and reuse; policymakers explicitly want campuses sited where heat can be monetized (district heating, industrial loads). germandatacenters.com+1

Strategic read: Germany has chosen regulatory certainty over optionality. For AI-ready campuses, 100% renewable from 2027 means procuring firmed clean power (PPAs plus storage, hydro/nuclear imports, or grid guarantees). Expect higher near-term LCOE and time-to-power risk, but also durable ESG and procurement advantages for enterprise and public workloads. White & Case+1

waste heat recovery data center equipment

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

France: Low-carbon baseload + national ambition

France is positioning itself as Europe’s clean-power outlier:

- Power advantage: Around 95% low-carbon electricity (nuclear + renewables) with lifecycle intensity ~21 g CO₂e/kWh (2024)—orders of magnitude lower than EU average. elysee.fr

- Scale narrative: The Élysée tied France’s AI strategy to a €109 billion investment wave, skewed to data-center capacity; EDF has identified ~2 GW across four owned sites and is scouting more, explicitly courting 1 GW-class AI projects. Sifted+2Reuters+2

- Global tie-ups: A France–UAE framework targets a 1 GW AI data center with tens of billions in capital—geopolitics meeting grid reality. Reuters

Strategic read: France’s bet is speed-by-utility and brand-by-carbon. If EDF can de-risk land, power, and interconnect for hyperscalers and sovereign operators, France may out-deploy neighbors despite France’s own permitting debates. The question is grid connection timing and local acceptance around water, heat, and land—even in a nuclear-friendly nation. Reuters+1

nuclear-powered data center cooling systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Spain: From hot market to hard rules

Madrid has moved from growth to guardrails:

- Draft Royal Decree (Aug 2025): Would bind new DCs ≥1 MW to stringent efficiency, sustainability, and disclosure requirements; consultation ran to Sept 15, 2025. Ashurst+1

- Policy intent: Goes beyond EU minimums (EED/Delegated Regulation) on transparency and performance—in line with Spain’s push to manage a demand boom (triple-digit MW growth) without grid stress blowback. Jones Day

Strategic read: Spain is codifying what fast growers learn the hard way: make efficiency and transparency table stakes before megaprojects stack up in a few metros. Expect location-shaping effects (sites near renewables, desalination, or district-heat off-takers) and more front-loaded capex for measurement and heat-integration.

AI Data Center Infrastructure Engineering: Power Distribution, Liquid Cooling, High-Density Networking, and Energy Efficiency for GPU Training … Hardware & Compiler Engineering Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What this means for operators, hyperscalers, and policymakers

1) The cost of “green by mandate” is moving on-balance-sheet.

Germany’s 2027 line forces real procurement: 24/7-matched PPAs, storage contracts, or nuclear-backed imports. France’s nuclear base lowers the premium, but developers still face connection and reinforcement timelines. Spain will tilt toward renewables + grid-friendly siting through decree. All three models push developers into energy-market sophistication—or into closer utility partnerships. White & Case+1

2) Waste-heat is becoming an offtake, not a footnote.

With EnEfG and local planning rules, German metros will increasingly expect heat recovery into district networks. This influences cooling tech choices (liquid, rear-door, immersion) and campus topologies. Spain’s decree logic and French municipal politics point the same way—even if not statutory everywhere, it’s becoming a social license issue. germandatacenters.com

3) Sovereign stacks need sovereign timelines.

Public buyers (ministries, health, defense, education) want EU jurisdictional control and carbon-credible compute. But AI build cycles are measured in quarters. France’s EDF-led land-and-power packaging is an attempt to close that gap; Germany and Spain will need analogous one-stop corridors or risk losing AI training to faster-moving grids. Reuters

4) Expect a two-tier Europe.

Core metros that can prove firm low-carbon power and heat-reuse pathways will command premium rents and longer-dated commitments. Secondary markets lacking grid headroom or municipal support will see delayed or downsized builds—despite land availability.

Risks to watch

- Grid connection queues: Even with EDF’s sites, connection timing is the pacing item for GW-scale AI campuses in France; similar constraints apply in Germany’s industrial corridors and Spain’s solar belts. Reuters

- Policy drift or judicial review: EnEfG amendments and Spain’s decree could evolve in implementation; operators must plan for compliance volatility across federal/municipal layers. eco+1

- Capex inflation from 24/7 matching: True hourly-matched clean power costs more than annual REC balancing; storage and curtailment deals add complexity that not every developer can underwrite. White & Case

My take: Europe’s “regulatory edge” vs. the speed trap

Europe is proving you can legislate greener compute and anchor sovereignty. Germany sets the high-water mark on legally binding renewables and heat-reuse; France shows how a utility-backed, nuclear-enabled grid can court AI megaprojects; Spain is moving fast to lock in standards before the next capacity wave arrives. White & Case+2Reuters+2

But the global race isn’t grading on ESG alone. The U.S. (and parts of the Middle East) are moving at a speed Europe will struggle to match. If permitting, transmission, and interconnects can’t be compressed, Europe risks offshoring the heaviest AI training while importing models and renting inference. The fix is not to loosen climate ambition—it’s to industrialize delivery:

- Package land + power + interconnect the way France is trying with EDF. Reuters

- Standardize district-heat integration so it’s an engineering pattern, not a bespoke negotiation. germandatacenters.com

- Use contracts-for-difference and sovereign guarantees to de-risk 24/7 PPAs for operators who can’t price energy markets like a utility. (Inference based on renewable-matching mandates and utility-site programs cited above.) White & Case+1

If Europe can execute that playbook, it keeps its regulatory edge without conceding scale—and that’s how you compete with U.S. hyperscalers without abandoning the climate bar you just set.

Sources

Germany: EnEfG mandates and obligations (renewables 50%→100%, scope, reporting), and waste-heat reuse direction. Watson Farley & Williams+4White & Case+4MHP Management- und IT-Beratung+4

France: Low-carbon grid metrics (Élysée brief), EDF site program (~2 GW), and AI investment wave (€109B incl. foreign partners). Le Monde.fr+3elysee.fr+3Reuters+3

Spain: Draft Royal Decree on energy efficiency & sustainability for data centers, consultation timeline, and alignment beyond EU minimums. Ashurst+1