The runway.

Two of the largest initial public offerings in history are being assembled at the same time, by two companies that did not meaningfully sell to enterprises three years ago. OpenAI is preparing a listing targeted at up to a $1 trillion valuation, with an S-1 filing widely expected in the fourth quarter of 2026. Anthropic is in talks to raise at a valuation above $900 billion, with bankers floating a public listing as early as October 2026. Goldman Sachs, JPMorgan, and Morgan Stanley are circling both.

The numbers underneath are extraordinary and moving weekly. OpenAI is generating roughly $2 billion a month — about $25 billion annualized — with 900 million weekly active users and enterprise now above 40% of revenue, on track for parity with consumer by the end of 2026. Anthropic crossed a $30 billion annualized run rate by April 2026, up from roughly $9 billion at the end of 2025, with enterprise customers contributing about 80% of revenue and more than 1,000 of them spending over $1 million a year.

But the same disclosures carry the other half of the story. OpenAI is projected to lose around $14 billion in 2026, with cash burn estimates running far higher and profitability not expected before roughly 2030; its gross margin sits near 33%. Anthropic’s gross margin is reported around 40%, with a forecast — internal, and aggressive — of reaching 77% by 2028. Both companies are sitting on compute commitments measured in the hundreds of billions of dollars.

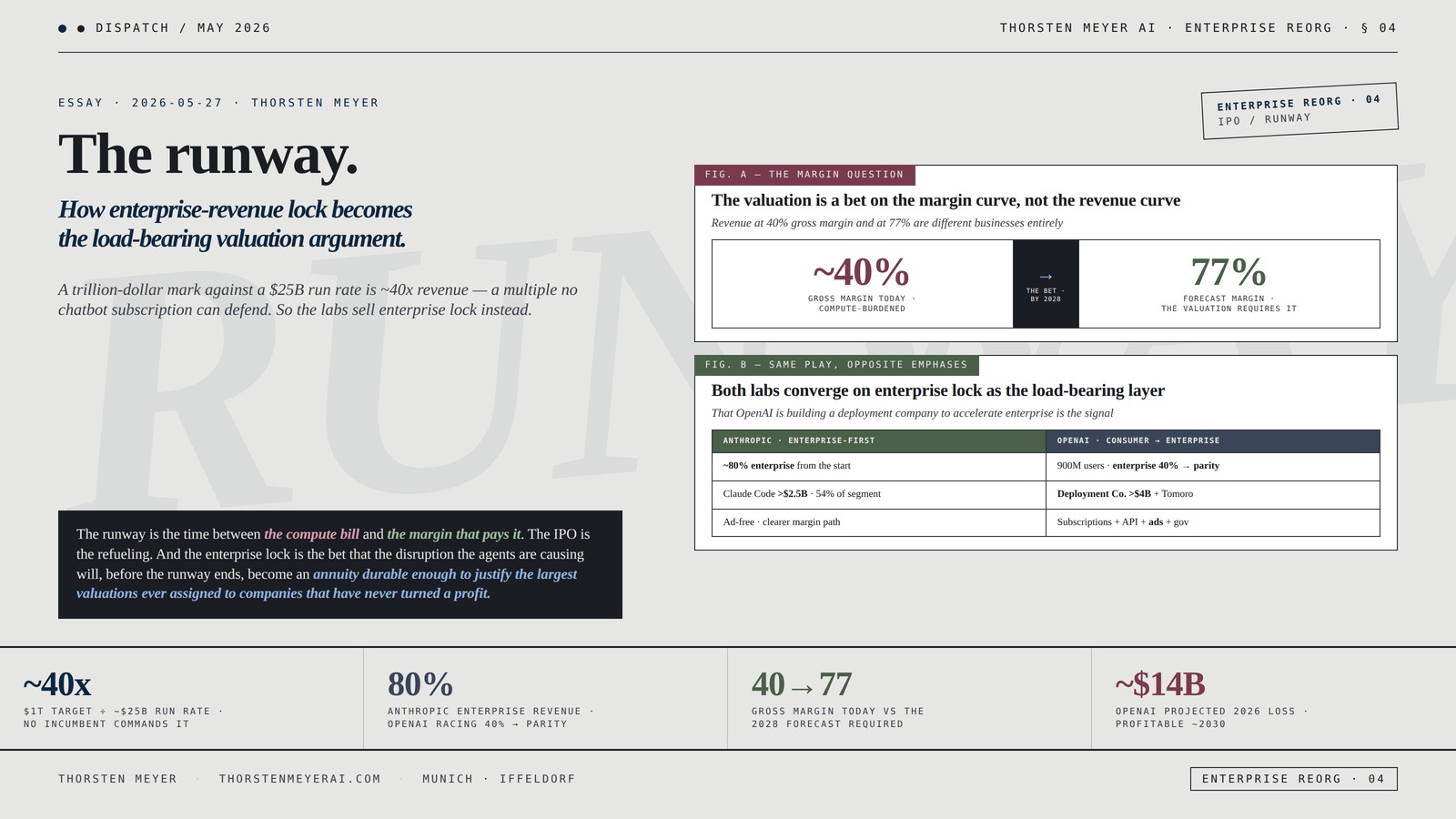

So the valuation cannot rest on the consumer story. A trillion-dollar mark against a $25 billion run rate is roughly 40x revenue; even at a $40 billion run rate it is 25x — multiples no public software incumbent currently commands, and ones a chatbot-subscription business cannot plausibly defend on its own. Bridgewater’s Greg Jensen reportedly told clients the implied multiple is “priced for a monopoly outcome that does not yet exist.”

That is why the load-bearing argument in both IPO stories is the same word: enterprise. Enterprise revenue is the thing being offered to public markets as the justification for the multiple — durable, contracted, expanding, embedded in workflows — and it is, not coincidentally, the exact revenue generated by the agents that are compressing the software and services industries this track has been documenting.

The structural argument I want to make: the AI labs are racing to convert enterprise-revenue lock into the load-bearing valuation argument before public markets demand audited proof — and that argument is reflexive, because the agents producing the enterprise revenue are the same agents whose disruption funds the multiple that funds the compute that builds the agents. The IPO is not just a financing event. It is the moment the enterprise-disruption thesis gets priced — and tested.

The headline integrative finding: The two labs are running the same play with opposite emphases. Anthropic is selling an enterprise-first story — 80% enterprise, a clearer margin path, ad-free, a coding wedge into the software economy — as the cleaner public-market comparable. OpenAI is selling a consumer-scale-plus-enterprise-acceleration story — 900 million users, enterprise racing to parity, an ads pilot, a new deployment company. Both are betting that enterprise lock is what converts a speculative model-quality bet into a defensible revenue annuity. And both face the same skeptic’s question: whether the margins that make enterprise revenue valuable will ever arrive, or whether the compute bill swallows the annuity before the runway ends.

This essay walks why the consumer story cannot carry the multiple, the enterprise lock being offered as the answer, the reflexive loop connecting the disruption to the valuation, the two labs’ opposite-emphasis strategies, the margin question that decides everything, the disclosure reckoning the S-1 will force, and the structural reading of an IPO that prices the enterprise-disruption thesis itself.

The runway.

How enterprise-revenue

lock becomes the load-

bearing valuation

argument.

a multiple no incumbent commands

OpenAI racing 40% → parity

forecast the valuation requires

not cash-flow positive before ~2030

$1T target ÷ ~$25B

run-rate revenue

>$900B reported ÷

~$30B run rate

OpenAI gross margin ·

95% of users are free

- ~80% enterprise revenue from the start

- Claude Code >$2.5B, 54% of the coding-tool segment

- ~40% margin today, 77% forecast by 2028

- Ad-free · PBC + Long-Term Benefit Trust

- Risk: a single-product (Claude Code) concentration

- 900M weekly users · enterprise 40% → parity

- Subscriptions + API + ads pilot + government

- Deployment Company >$4B + Tomoro acqui-hire

- The brand name for AI · broadest distribution

- Drag: consumer margin it is racing to offset

compute-burdened

by 2028 ·

inference cost

must fall

the valuation requires it

The runway is the time between the compute bill and the margin that pays it. The IPO is the refueling. And the enterprise lock is the bet that the disruption the agents are causing will, before the runway ends, become an annuity durable enough to justify the largest valuations ever assigned to companies that have never turned a profit.Thorsten Meyer · The Runway · Enterprise Reorg 04

By Thorsten Meyer — May 2026

This is the fourth dispatch in the AI Enterprise Reorganization track. Earlier pieces walked the CFO’s new operating system, the consulting pyramid’s compression, and the agents absorbing finance and professional-services work. This one closes the loop: the same enterprise disruption those pieces documented is now the central exhibit in the largest IPO stories in history — the revenue the labs are offering public markets as proof that the disruption is real, durable, and theirs to monetize.

The structural argument I want to make: enterprise-revenue lock is being asked to do something a consumer-subscription business cannot do — justify a mega-cap multiple on a company that loses billions and has never been profitable. The labs need the enterprise story precisely because the consumer story, however large, is a usage business with thin margins and uncertain retention, while the enterprise story is a contracted, embedded, expanding-seat business that looks like the software annuities public markets know how to value. The IPO is the moment that substitution gets tested: can enterprise lock carry a valuation the consumer business cannot?

The headline integrative finding: The reflexivity is the core of it. The agents are compressing software and services (the prior pieces in this track); that compression is the labs’ enterprise revenue; that revenue is the valuation argument; that valuation funds the compute; that compute builds the next agents. It is a self-referential loop in which the disruption and the financing are the same phenomenon viewed from two ends — and the loop holds only as long as the margins arrive and the revenue proves durable. The IPO prices the loop. The first audited quarter tests it.

This essay walks the consumer-multiple problem (Section I), the enterprise lock offered as the answer (Section II), the reflexive loop (Section III), the two labs’ opposite strategies (Section IV), the margin question (Section V), the S-1 disclosure reckoning (Section VI), and the structural reading of pricing the disruption thesis (Section VII).

I · The consumer-multiple problem · why scale is not enough

The valuation-gap crystallization. Start with the number that does not work. The consumer business, however large, cannot justify the valuation on its own — and everyone pricing these deals knows it.

The multiples

OpenAI: a $1 trillion target against roughly $25 billion annualized revenue is about 40x run-rate revenue; even if revenue reaches $40 billion by year-end, that compresses to roughly 25x. These are run-rate, not audited-trailing, multiples — but they are multiples no public software incumbent currently commands.

Anthropic: a $380 billion Series G mark (February 2026) against then-$14 billion run rate was about 27x; a reported new round above $900 billion against a ~$30 billion run rate is roughly 30x. For context, ServiceNow — a profitable, decades-mature enterprise-software incumbent — traded at a materially lower market cap than Anthropic’s private mark.

Why consumer scale does not close the gap

Consumer is a usage business with thin margins: ChatGPT’s 900 million weekly active users and 50 million-plus subscribers are a genuinely historic consumer franchise. But consumer AI is a high-churn, usage-metered, compute-heavy business — 95% of users are free, inference is expensive, and the gross margin (around 33% for OpenAI) reflects it. Consumer scale produces revenue, but not the margin profile or the retention durability that justifies a software multiple.

The ads pivot is a tell: OpenAI’s ads pilot — reportedly past $100 million in run-rate ARR within weeks — is evidence that the consumer business is being pushed to monetize beyond subscriptions. Introducing ads into a premium product is what you do when subscription revenue alone does not carry the model. It is rational; it is also a signal that consumer subscriptions are not enough.

Comparison to consumer platforms is fraught: ChatGPT is the brand name for AI the way Google is for search, and brand dominance is real pricing power. But consumer-platform comparisons (to social networks, to search) mislead, because those platforms monetized through advertising at very high margins, which a compute-metered AI product does not — at least not yet.

The skeptic’s framing

“Priced for a monopoly that does not yet exist”: the Bridgewater critique names the problem precisely. At 25-40x run-rate revenue, the valuation assumes a durable, monopoly-like outcome — sustained hypergrowth, margin expansion, and competitive insulation — that the current business has not demonstrated. The consumer business, priced honestly, does not get you to the valuation. Something else has to.

The consumer-multiple observation

The consumer business is large, historic, and insufficient. It produces revenue at a margin and durability that cannot defend a 25-40x multiple, and the ads pivot signals the labs know it. The valuation gap between what the consumer business can justify and what the private markets have marked is the gap the enterprise story is being asked to fill. Everything in the IPO narrative that is not consumer scale is, in effect, an argument about enterprise.

Enterprise AI Solutions Architecture: The Practitioner’s Handbook for Designing, Delivering, and Scaling Production AI Systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The enterprise lock · the answer being offered

The annuity crystallization. The thing being offered to close the valuation gap is enterprise-revenue lock — and it is offered because it looks like the one thing public markets reliably pay mega-cap multiples for: a contracted, embedded, expanding software annuity.

What enterprise lock looks like

Anthropic’s enterprise base: roughly 80% of revenue from enterprise; more than 1,000 customers spending over $1 million annually (doubled from ~500 in under two months); eight of the Fortune 10 as customers; over 300,000 business customers; customers spending over $100,000 a year grown sevenfold. Claude Code — the agentic coding wedge — passed $2.5 billion in run-rate revenue, with enterprise more than half of it.

OpenAI’s enterprise acceleration: enterprise above 40% of revenue and on track for parity with consumer by end-2026; more than 9 million paying business users; a new OpenAI Deployment Company capitalized at over $4 billion and an acqui-hire of consulting group Tomoro (≈150 deployment engineers) — an explicit move to build the forward-deployment muscle that converts model access into embedded enterprise revenue.

Why enterprise revenue is worth more per dollar

Contracted and embedded: enterprise revenue comes through multi-year agreements, seat expansions, and workflow integration (Claude in coding pipelines, finance workflows, document production). Embedded revenue has switching costs; switching costs produce retention; retention is what justifies a software multiple. A dollar of embedded enterprise revenue is worth more than a dollar of churning consumer subscription, because it is more durable and more predictable.

Expanding by design: the “land and expand” motion — a team adopts Claude Code, then the department, then the enterprise — produces net revenue retention above 100%, the metric public software investors prize most. The 7x growth in $100k+ customers and the doubling of $1M+ customers in two months are exactly this dynamic.

It looks like software, not usage: enterprise AI revenue, sold through contracts and seats and embedded in workflows, resembles the SaaS annuities public markets know how to value — which is precisely why it is the story being told.

The substitution being attempted

Enterprise lock substitutes for the missing margin and durability: the labs are, in effect, asking public markets to value them on the enterprise revenue’s quality (contracted, embedded, expanding) rather than the consumer revenue’s quantity (large, but thin and churning). The enterprise story is the bridge from “speculative model-quality bet” to “defensible revenue annuity” — and the annuity framing is what supports a mega-cap multiple.

The enterprise-lock observation

Enterprise-revenue lock is offered as the answer to the consumer-multiple problem because it has the one property the consumer business lacks: it looks like a durable software annuity. Contracted, embedded, expanding, enterprise revenue is worth more per dollar than consumer usage, and it is the part of the story that justifies the multiple. The labs are not selling the chatbot to public markets. They are selling the enterprise lock — and the chatbot is the funnel that feeds it.

Beyond Vibe Coding: From Coder to AI-Era Developer

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The reflexive loop · the disruption is the revenue is the valuation

The reflexivity crystallization. Here is the structural heart of it, and the thing that makes these IPOs different from any prior technology listing: the enterprise revenue being offered as the valuation justification is the same revenue generated by the agents disrupting the industries the prior pieces in this track documented. The disruption and the financing are the same phenomenon.

The loop

Step 1 — the agents compress: Claude Code and its peers compress software engineering; the finance agents compress the CFO’s office; the deployment work compresses consulting. (These are the prior dispatches in this track.)

Step 2 — the compression is the revenue: that compression is the labs’ enterprise revenue. Claude Code’s $2.5 billion is the monetization of software-engineering compression. The finance agents’ adoption is the monetization of finance-function compression. The enterprise revenue and the enterprise disruption are the same dollars.

Step 3 — the revenue is the valuation argument: that enterprise revenue is the load-bearing argument for the 25-40x multiple (Section II).

Step 4 — the valuation funds the compute: the IPO and the private rounds fund the hundreds of billions in compute commitments — Stargate, the Azure/Oracle/AWS arrangements, the TPU and GPU capacity.

Step 5 — the compute builds the next agents: which compress the next tranche of industries, producing the next tranche of enterprise revenue.

Why the loop is the story

Self-reference: the valuation is justified by revenue that is produced by disruption that is funded by the valuation. It is not circular in the fallacious sense — the revenue is real — but it is reflexive: each element depends on the others holding. The multiple assumes the disruption continues; the disruption requires the compute; the compute requires the capital; the capital requires the multiple.

The market-cap evidence: the loop is visible in the public markets’ reaction. The software sell-off that accompanied the agentic-tool launches — the trillions in cumulative market-cap pressure on incumbent software and services names — is the market pricing the other side of the same loop. The value the agents destroy in incumbent software is, in the labs’ story, the value they capture as enterprise revenue. The disruption and the revenue are two readings of one event.

The fragility

The loop holds only while each link holds: if the disruption slows (better incumbent defense, commoditization), enterprise revenue growth decelerates, the multiple compresses, the capital gets more expensive, and the compute buildout strains. The reflexive loop that makes the story powerful on the way up makes it fragile on the way down — because each element depends on the others, a crack in one propagates. Friar’s reported warning that compute spending could outpace revenue if growth does not accelerate is a warning about exactly this.

The reflexive-loop observation

The enterprise revenue offered as the valuation justification is the monetization of the very disruption the prior pieces documented — making the IPO a security whose value derives from the continuation of the enterprise compression it finances. This is what makes these listings unlike any prior tech IPO: the company is selling public markets a stake in a disruption that the company’s own products are causing and the IPO’s proceeds will accelerate. The loop is real, it is powerful, and it is fragile in exactly the way reflexive systems are: it holds until one link doesn’t.

The Definitive Guide to Conversational AI with Dialogflow and Google Cloud: Build Advanced Enterprise Chatbots, Voice, and Telephony Agents on Google Cloud

The Definitive Guide to Conversational AI with Dialogflow and Google Cloud: Build Advanced Enterprise Chatbots, Voice, and Telephony…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The two strategies · enterprise-first versus consumer-scale

The divergence crystallization. The two labs are running the same enterprise-lock play with opposite emphases, and the difference is the cleanest way to see what public markets are actually being asked to value.

Anthropic · enterprise-first

The mix: roughly 80% enterprise revenue. The story is built around the enterprise annuity from the start — API usage, Claude Code, Claude for Work — with consumer as a smaller component.

The margin claim: gross margin reported around 40% today, with an internal forecast of 77% by 2028 and a claimed efficiency edge (≈$2.10 revenue per compute dollar by 2028 vs. OpenAI’s projected ≈$1.60). The pitch is a clearer, faster path to profitability.

The positioning: ad-free (an explicit contrast with OpenAI’s ads pilot), safety-forward, PBC-with-a-Long-Term-Benefit-Trust governance. The enterprise-first mix is presented as the cleaner public-market comparable — the AI company that most resembles a durable enterprise-software business.

The concentration risk: the enterprise-first story is, to a remarkable degree, a single-product story — Claude Code is the dominant growth driver. Concentration in one product (and in the coding vertical) is the flip side of the clean enterprise narrative.

OpenAI · consumer-scale-plus-enterprise-acceleration

The mix: enterprise above 40% and racing to parity with consumer by end-2026. The story leads with consumer scale (900 million weekly users, the brand-name-for-AI position) and adds enterprise acceleration as the margin-and-durability layer.

The monetization breadth: subscriptions, API, an ads pilot, a government vertical (the Pentagon reference contract), and the new Deployment Company plus Tomoro acqui-hire to build forward-deployment capacity. The pitch is breadth — multiple monetization surfaces, with enterprise the fastest-growing.

The positioning: the default consumer surface and the broadest distribution, converting consumer dominance into enterprise entry. The Deployment Company is the explicit move to build the embedded-revenue muscle Anthropic has through Claude Code.

What the divergence reveals

Both converge on enterprise as the load-bearing layer: Anthropic starts there; OpenAI is racing there. The fact that the consumer-scale leader is building a deployment company and acqui-hiring consultants to accelerate enterprise revenue is the strongest possible evidence that enterprise lock — not consumer scale — is what carries the valuation. OpenAI has the larger consumer franchise and is still rushing to build the enterprise annuity, because the consumer franchise alone does not justify the mark.

The two-strategies observation

The two labs run the same enterprise-lock play from opposite starting points — Anthropic enterprise-first, OpenAI consumer-first-racing-to-enterprise — and both converge on enterprise revenue as the valuation’s load-bearing layer. Anthropic offers the cleaner enterprise comparable with concentration risk; OpenAI offers broader monetization with a consumer-margin drag it is racing to offset. That both are sprinting toward enterprise lock — one defending its lead, one building from scale — is the clearest signal of what public markets are actually being asked to buy.

The AI Data Center Race: No-Constraints Thinking for the Age of Compute

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The margin question · what decides everything

The unit-economics crystallization. The entire structure — the enterprise lock, the reflexive loop, the multiple — rests on one unresolved question: whether the margins that make enterprise revenue valuable will actually arrive. This is where the bull and bear cases meet.

The current margins

Thin, for now: OpenAI’s gross margin is reported near 33%; Anthropic’s near 40%. These are not software margins — they are compute-burdened margins, weighed down by inference costs, free-user load, and the price of frontier training. At these margins, revenue growth does not automatically produce profit; it can produce larger losses.

The expansion assumption

The 77% bet: Anthropic’s internal forecast of 77% gross margin by 2028 (from ~40% today) is one of the most aggressive margin-expansion assumptions ever embedded in a private technology valuation. It assumes inference costs fall sharply (more efficient models, better hardware utilization), the revenue mix shifts toward higher-margin enterprise, and scale produces leverage. The valuation does not work at 40%; it works at something approaching 77%. The multiple is a bet on the margin curve, not the revenue curve.

The efficiency claim: the ≈$2.10-per-compute-dollar-by-2028 figure is the same bet stated as a ratio. It is plausible — model efficiency has compounded, each generation doing more with less compute — but it is a forecast, not a result, and the distance from here to there is the risk.

The losses and the burn

Billions, ongoing: OpenAI is projected to lose ~$14 billion in 2026, with cash-burn estimates running materially higher (some estimates near $27 billion in 2026 and far more in 2027 under the renegotiated Microsoft terms), and is not expected to be cash-flow positive before ~2030. The compute commitments — hundreds of billions across Stargate, Azure, Oracle, AWS — are contractual and largely non-recallable. The runway is the gap between when the compute must be paid for and when the margins arrive to pay for it.

Where bull and bear meet

The bull case: enterprise revenue compounds, mix shifts, inference costs fall, margins expand toward software levels, and the annuity becomes profitable at scale — vindicating the multiple.

The bear case: compute spending outpaces revenue (Friar’s warning), margin expansion slips, the 77% assumption proves optimistic, competition commoditizes model quality, and the labs are left with large contracted compute bills against revenue that grows but never reaches the margin that justifies the mark. Revenue at 40% gross margin and revenue at 77% gross margin are different businesses entirely — and the valuation is priced for the second while the company operates as the first.

The margin-question observation

The margin question decides everything, because the valuation is a bet on the margin curve, not the revenue curve. Enterprise revenue is only worth a software multiple if it carries software margins, and the labs operate today at roughly half the margin the valuation assumes. The runway is the time between now and the arrival of those margins; the burn is the cost of staying on it; and the IPO is the refueling. Whether the margins arrive before the runway ends is the entire bet.

VI · The S-1 reckoning · what disclosure will force

The disclosure crystallization. Everything above is built on private marks, selective disclosures, and run-rate figures. The S-1 changes that — it forces audited numbers into public view, and the gap between the narrative and the audited reality is the reckoning the IPO will bring.

What the S-1 will force into the open

Audited revenue and the gross/net question: run-rate figures will become audited GAAP revenue. A specific scrutiny point: Anthropic reports cloud-reseller revenue on a gross basis (counting total end-customer spend, booking partner payouts as expenses), which inflates top-line relative to net-reporting peers — a treatment the S-1 and any restatement risk will surface.

Gross margin after compute: the audited gross margin — the number that determines whether enterprise revenue is a software annuity or a compute pass-through — becomes public, against the 77% forecast.

Contract obligations: the hundreds of billions in compute commitments become disclosed liabilities, with their timing and recallability spelled out. The market will see the runway’s length and the burn’s slope.

Governance rights: who controls the company, what the nonprofit/PBC structures actually bind, what insiders and late investors can sell at lock-up expiry (the prior governance pieces in the adjacent track bear directly here).

Why this is the reckoning

The narrative meets the audit: the IPO narrative is enterprise lock, hypergrowth, and a margin curve bending toward software economics. The S-1 forces that narrative against audited revenue, audited margin, disclosed obligations, and disclosed governance. The gap between the run-rate story and the audited reality — if there is one — surfaces in the prospectus, not the press release.

The first quarter as a public company: the lock-up expires ~90-180 days after listing; the first audited quarterly report sets the durable public valuation. The private markets priced the narrative; the public markets, with audited numbers, price the reality. The IPO is where those two prices meet.

The reckoning observation

The S-1 is where the enterprise-lock narrative meets the audit, and the audit is less forgiving than the private round. Audited revenue, gross margin after compute, disclosed compute obligations, and governance rights all become public — and the reflexive loop, the margin assumption, and the multiple all get tested against numbers that have been examined rather than asserted. The private valuation prices the story; the S-1 prices the proof; and the distance between them is what the IPO actually reveals.

What this is not

It is not a prediction that the IPOs fail. The revenue is real and historic; the enterprise lock is genuine; the margin curve may well bend as forecast. The reckoning is a test, not a verdict.

It is not a claim that the two labs are equivalent. Anthropic’s enterprise-first mix and reported margin path differ structurally from OpenAI’s consumer-first-with-ads profile, and the S-1s will read differently. The shared structure is the enterprise-lock argument, not the financials.

It is not a claim that the disruption is fake. The prior pieces documented real compression in software and services. The question is not whether the disruption is real but whether the labs can monetize it at margins that justify the mark.

The synthesis observation

The AI labs are racing to convert enterprise-revenue lock into the load-bearing valuation argument before the S-1 forces audited proof — and that argument is reflexive, because the enterprise revenue is the monetization of the disruption the IPO finances. The consumer business, however historic, cannot carry a 25-40x multiple; the enterprise annuity is offered to close the gap; the annuity’s value depends on a margin curve the companies have not yet climbed; and the whole structure is a loop in which the disruption, the revenue, the valuation, and the compute each depend on the others holding.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that these are not ordinary technology IPOs. They are the moment the enterprise-disruption thesis — the one this entire track has documented — gets priced and tested in public, by markets that will demand audited margins where private rounds accepted run-rate narratives. The runway is the time between the compute bill and the margin that pays it. The IPO is the refueling. And the enterprise lock is the bet that the disruption the agents are causing will, before the runway ends, become an annuity durable enough to justify the largest valuations ever assigned to companies that have never turned a profit.

That is the structural editorial question the runway sits on top of. It is a consumer business that cannot carry its own multiple, an enterprise annuity offered to close the gap, a reflexive loop binding the disruption to the financing, and a margin assumption that decides whether any of it works. And it is the layer where the entire enterprise-reorganization thesis gets its verdict — not in whether the agents can compress the industries, but in whether compressing them produces a business durable and profitable enough to justify the price the markets have already, privately, agreed to pay.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Enterprise Reorganization track

This dispatch

- This piece · The runway · how enterprise-revenue lock becomes the load-bearing valuation argument for the labs whose agents are doing the compressing — and why the IPO prices the enterprise-disruption thesis itself · synthesis-deep dominant, structural-slate and labor-rose balance

The track

- The CFO’s new operating system · Enterprise Reorg 01 · the finance-function compression that is part of the enterprise revenue this piece prices

- The pyramid cracks · Enterprise Reorg 02 · the consulting compression that is the other half of the enterprise-disruption annuity

- Forthcoming · The Palantir model at scale · the forward-deployed-engineering economics that OpenAI’s new Deployment Company and Anthropic’s enterprise motion are both adopting · empirical-clay register

Adjacent tracks

- The clause · AI Governance 03 · the governance terms the S-1 will force into public view

- The cleaner cap table · AI Governance 02 · Anthropic’s PBC-and-Long-Term-Benefit-Trust structure as it heads toward a listing

- The calendar technicality · AI Governance 01 · the litigation backdrop to the OpenAI restructuring that cleared the IPO path

Sources

The IPO setups

- Technerdo · OpenAI’s $1 Trillion IPO — Q4 2026 IPO window (likely Oct/Nov), reported ~$60B raise at up to $1T · S-1 amendments and roadshow in Q3 2026 · ~$25B annualized revenue (Feb 2026), up from ~$20B end-2025 · $280B revenue target by 2030 · lock-up 90-180 days · technerdo.com

- AI IPO Tracker 2026 · aifundingtracker — OpenAI ~$25B annualized at $852B, CFO Friar flagging late-2026/2027 listing window, projected ~$14B 2026 loss, profitability ~2029-2030 · Anthropic >$30B annualized on ~1,400% YoY growth, talks to raise $50B at $900B, IPO as early as October · SpaceX confidential S-1 April 1 targeting $1.75T+ · aifundingtracker.com

- TECHi · OpenAI IPO — no filed S-1 as of May 6 2026 · $122B round at $852B post-money · $2B/month revenue · enterprise >40% of revenue, on track for parity with consumer by end-2026 · 900M weekly users, 50M+ subscribers, 9M+ paying business users · five things public investors cannot yet see (audited revenue, gross margin after compute, contract obligations, governance, insider selling) · techi.com

- Tech-Insider · OpenAI’s $122B Raise — S-1 filing predicted by Q4 2026; Goldman drafting disclosure language; NYSE “AI”/”OAI” working assumption · secondary-market premium (12-18% on Hiive/Forge) could reset implied valuation above $1T pre-IPO · FT “valuation gap”; Bridgewater’s Greg Jensen: implied ~35x forward revenue “priced for a monopoly outcome that does not yet exist” · Friar warned compute spending could outpace revenue · tech-insider.org

OpenAI’s enterprise build and burn

- OpenAI · $122B raise blog — primary source: 900M+ weekly active users, 50M+ subscribers, ChatGPT 6x next AI app’s web/mobile sessions, ads pilot >$100M ARR in under six weeks, enterprise >40% of revenue and on track for parity with consumer by end-2026 · openai.com

- Sacra · OpenAI — IPO groundwork (Cynthia Gaylor as first head of IR), filing H2 2026 / 2027 listing, up to $1T · refocusing on coding and enterprise, cutting side projects · $600B disclosed compute, projected burn ~$27B 2026 / ~$63B 2027, not cash-flow positive before 2030 · government vertical (Pentagon reference contract) · sacra.com

- TS2 · OpenAI valuation test — Anthropic’s $30B-at-$900B terms pressuring OpenAI’s $852B mark · Microsoft revenue-share cap reported at $38B · OpenAI Deployment Company capitalized at >$4B, acqui-hiring consulting group Tomoro (~150 engineers/deployment staff) targeting the same enterprise customers as Anthropic · ts2.tech

- Motley Fool · 5 Things to Know — $1T target, $852B latest round, $122B raised · $280B revenue target by 2030 from enterprise + commercial · $13.1B sales in 2025; nearly half of 2026 sales from enterprise · $600B total compute spend by 2030 (down from $1.4T in commitments) · fool.com

Anthropic’s enterprise-first story and margins

- VentureBeat · Anthropic $30B run rate — Dario Amodei’s “80x” Q1 2026 annualized growth (with the caveat that annualized rates overstate); run-rate trajectory $87M (Jan 2024) → $1B (Dec 2024) → $9B (end-2025) → $14B (Feb) → $19B (Mar) → $30B (Apr 2026); Salesforce took ~20 years to reach $30B; the “single agents → multiple agents → organizational intelligence / country of geniuses in a datacenter” thesis · venturebeat.com

- Sacra · Anthropic — ~$43B annualized April 2026 (up from $9B end-2025); 300,000+ business customers ≈80% of revenue; >1,000 customers >$1M/yr (doubled from 500+ in under two months); $100k+ customers grown 7x; gross-basis cloud-reseller revenue reporting (inflates top line vs net peers); Claude Code GA May 2025, $1B Nov 2025, $2.5B Feb 2026; Wilson Sonsini engaged for IPO prep · sacra.com

- TechMarketBriefs · Anthropic IPO — 27x revenue at the $380B Series G ($14B run rate); ServiceNow (~$93B, down 41% YTD) trades below Anthropic’s private mark; ~80% enterprise vs OpenAI consumer-heavy; PBC + Long-Term Benefit Trust; ad-free pledge vs OpenAI ads; internal projections ~$70B 2028 revenue / $17B cash flow, gross margin ~40%→77% by 2028; OpenAI internal models ~$74B operating losses 2028, profitability ~2030; Pentagon contract collapse · techmarketbriefs.com

- TradingKey · Anthropic IPO comparison — ~80% enterprise, gross margins ~40% (≈on par with OpenAI), improved from -94% in 2024; enterprise LLM API share Anthropic 32% vs OpenAI 25%; Claude Code 54% of AI coding-tool segment, >$2.5B revenue; 95% free users a “profit black hole”; public-market investors favor the enterprise-oriented, clearer-profitability model · tradingkey.com

- Shanaka Anslem Perera · The Growth Miracle and the Six Fractures — the bear frame: 27x revenue encodes a derivative on AGI’s arrival date; 40% vs 77% gross margins are “different businesses entirely”; the margin-expansion assumption is “one of the most aggressive ever embedded in a private technology valuation”; customer/product concentration (Claude Code) as a paradox · shanakaanslemperera.substack.com

- DeepResearchGlobal · Anthropic outlook — 2028 gross-margin forecast 77%; projected $2.10 revenue per compute dollar by 2028 vs OpenAI’s $1.60; model-efficiency compounding (comparable quality at 3-4x less compute per generation); 2027 ARR scenarios $12B (base) to $34.5B (bull) · deepresearchglobal.com

The enterprise-disruption backbone (this track)

- The CFO’s new operating system / The pyramid cracks · Thorsten Meyer · Enterprise Reorg 01-02 · the finance-function and consulting compression that is the enterprise revenue this piece prices · the agentic disruption whose monetization is the IPO’s load-bearing valuation argument · the $2T+ software/services market-cap pressure that is the other side of the reflexive loop

Key reference figures crystallized

- OpenAI: ~$25B annualized (~$2B/mo) · 900M weekly users, 50M+ subscribers, 9M+ business users · enterprise >40% → parity by end-2026 · ads pilot >$100M ARR · ~33% gross margin · ~$14B 2026 loss (burn est. higher), profitability ~2030 · $122B round at $852B; $1T IPO target, S-1 expected Q4 2026; ~$600B compute commitments · Deployment Company >$4B + Tomoro acqui-hire

- Anthropic: ~$30B+ annualized (from ~$9B end-2025) · ~80% enterprise · 1,000+ customers >$1M/yr · 8 of Fortune 10 · Claude Code >$2.5B (54% of coding-tool segment) · ~40% gross margin, 77% forecast by 2028, ~$2.10/compute-$ by 2028 · $380B Series G (Feb 2026); reported new round >$900B; IPO as early as Oct 2026; Wilson Sonsini engaged · PBC + LTBT, ad-free

- The multiples: $1T / $25B ≈ 40x run-rate (≈25x at $40B); $900B / $30B ≈ 30x; $380B / $14B ≈ 27x · ServiceNow (profitable incumbent) below Anthropic’s private mark · Bridgewater: “priced for a monopoly that does not yet exist”

- The reflexive loop: agents compress → compression is enterprise revenue → revenue is the valuation argument → valuation funds compute → compute builds next agents · the $2T+ software/services sell-off is the other side

- The margin question: ~33-40% today vs 77% forecast · “revenue at 40% and revenue at 77% are different businesses” · Friar: compute could outpace revenue · the runway = time between the compute bill and the margin that pays it

- The S-1 reckoning: audited revenue (gross vs net reporting), gross margin after compute, contract obligations, governance rights, insider lock-up selling — the narrative meets the audit