This week it emerged that Apple is lobbying Washington for permission to buy memory chips from the Chinese manufacturer CXMT — a company on the Pentagon’s blacklist.

The move came two days after Apple raised prices on Macs and iPads, blaming the global memory shortage. When the best-funded hardware company on earth can no longer push the cost through quietly, that’s a story in itself.

But here’s the part that matters for Europe: Apple has options at all. It has a domestic supplier in Micron. It can lobby in Washington. And it can — if it must — reach for China.

Europe has none of that. No memory champion of its own, no seat at the table, no leverage on the one variable that counts. The shortage that’s becoming uncomfortable for Apple exposes Europe’s blind spot far more brutally.

Apple is reaching for Chinese memory. Europe doesn’t even have that option.

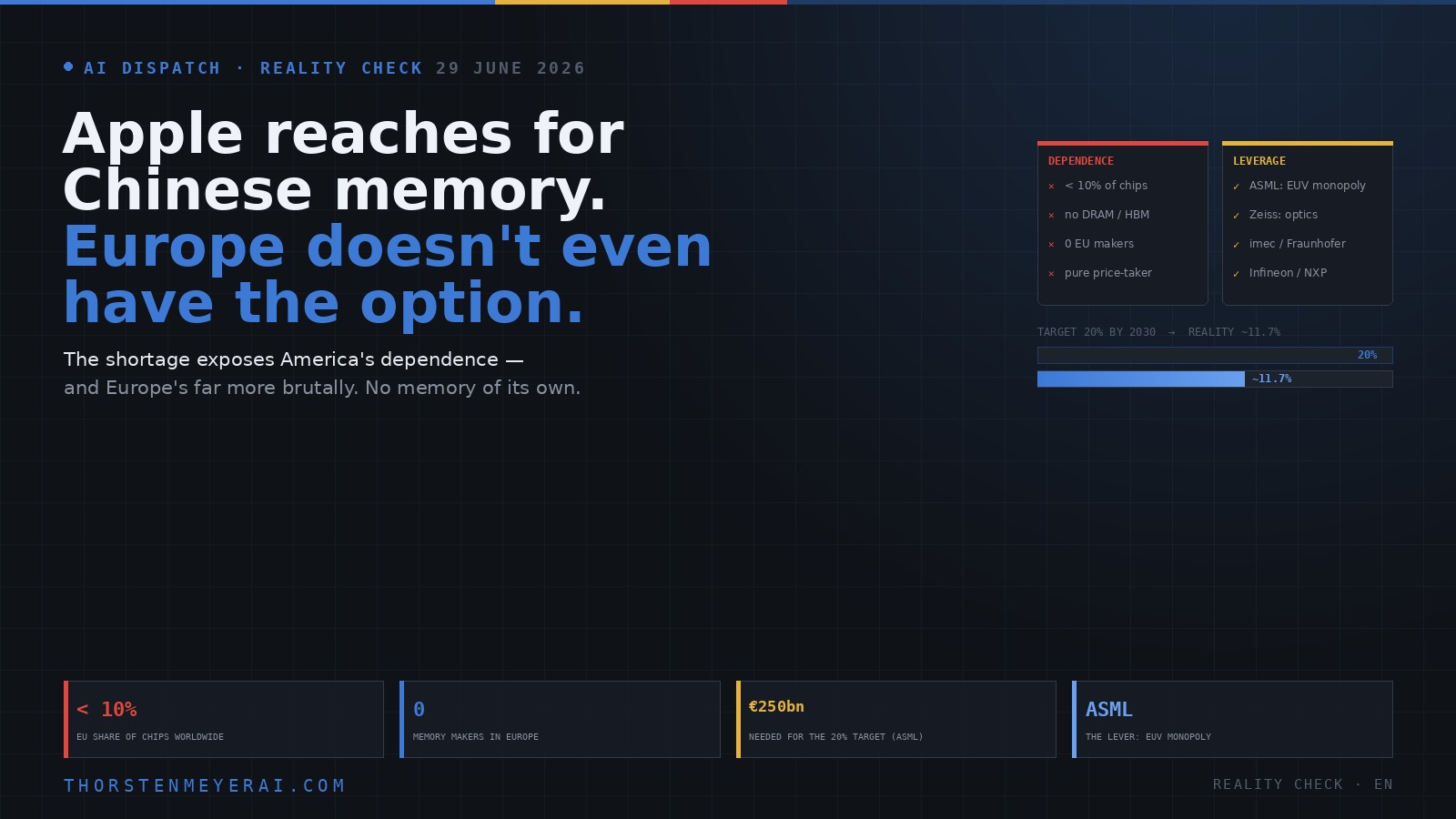

The shortage exposes America’s dependence — and Europe’s far more brutally. Apple has a domestic supplier, political weight, and the China option. Europe has no memory of its own, no seat at the table, no leverage on what counts.

- EU makes < 10% of the world’s semiconductors

- Effectively no DRAM, no HBM from Europe

- 3–4 memory makers worldwide — none European

- Pure price-taker: memory ~4× in 3 quarters

- ASML: EUV monopoly — no leading-edge chip without it

- Zeiss: precision optics, unrivalled worldwide

- imec · CEA-Leti · Fraunhofer: world-class research

- Infineon, NXP, STMicro: automotive · power · SiC

The shortage is a sovereignty test — Europe fails on supply but still holds the leverage in its hand. If even Apple can’t buy its way out, Europe’s answer isn’t to buy its way in, but to run two tracks: press the unique chokepoints as real leverage — and cut dependence wherever it can without Brussels: local-first, open weights, quantization, right-sized hardware. Bury the 20% dream, defend what’s yours, need less.

What Europe makes in memory: almost nothing

Start with the uncomfortable number. The EU manufactures less than 10 percent of the world’s semiconductors by value, and is, in the European Commission’s own words, “almost entirely dependent” on the United States and Asia.

In memory it’s starker still. The number of meaningful DRAM makers has shrunk from more than twenty in the mid-1990s to three or four today: Samsung, SK Hynix, Micron, and a small fringe. Not one of them is European. Commodity DRAM — the working memory in every machine — and above all HBM, the stacked high-performance memory that feeds AI accelerators, are made essentially entirely outside Europe. Fabrication sits in East Asia; design sits in the US.

And the prices? Memory has roughly quadrupled over three quarters by Counterpoint’s reckoning; in some segments the year-over-year rise is closer to sixfold. Europe pays those prices — as a pure price-taker, with no influence over them whatsoever.

European DRAM memory modules

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The levers Brussels cannot pull

The real problem isn’t a lack of will to invest. It’s that Europe’s standard tools — subsidies, regulation, certification — run into a wall they were never built to move.

No funding program on earth conjures TSMC cleanroom capacity on a useful timetable, improves HBM4 yield at SK Hynix, or secures Europe an allocation at Nvidia. Yet that’s exactly what would be required. Scarce HBM output is already booked out by US hyperscalers and AI labs — reportedly OpenAI alone has locked up roughly 40 percent of global DRAM wafer production through 2029. These are not levers the Commission can pull, however much it might want to.

What Brussels can do is real but secondary: electricity prices, permitting, demand aggregation, public procurement, EU-located capacity. The recently unveiled “tech sovereignty package” even goes so far as to give the Commission emergency powers to redirect chip production by priority order in a crisis — overriding existing contracts if necessary. The trouble is, you cannot order into existence what physically isn’t there.

CORSAIR Vengeance LPX DDR4 RAM 32GB (2x16GB) Up to 3200MHz CL16-20-20-38 1.35V Intel XMP AMD EXPO Computer Memory – Black (CMK32GX4M2E3200C16)

Disclaimer: Maximum Speed requires overclocking/PC BIOS adjustments. Maximum speed and performance depend on system components, including motherboard and…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The 20-percent dream is dead

The 2023 EU Chips Act had a clear goal: double Europe’s global market share to 20 percent by 2030, mobilizing some €43 billion.

Reality overtook that long ago. By the Commission’s own figures, Europe reaches only about 11.7 percent by 2030. The European Court of Auditors in December 2025 called the 20-percent target simply “very unlikely.” By ASML’s estimate, hitting it would cost over €250 billion — far more than is available. Flagship projects are stalling or collapsing: Intel’s Magdeburg plant, the STMicro/GlobalFoundries fab in Crolles. The Auditors’ bitter verdict: Europe “exports its brilliance” to be manufactured elsewhere.

Put plainly: autarky in leading-edge fabrication isn’t available on any realistic horizon — not for lack of money alone, but because the dense supplier ecosystem and the tacit process knowledge that Taiwan and Korea built over decades cannot be subsidized into existence by statute.

Training Gaps 1: Semiconductor Equipment Manufacturing, Engineering, Research, Development, and Management

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What Europe has instead: chokepoints no one can route around

None of which leaves Europe powerless — and here is the honest other side of the ledger. Europe controls several chokepoints that no one else can get past.

The most important is ASML in the Netherlands: the world monopoly on EUV lithography, the machines without which no leading-edge chip exists at all. The US export controls against China only function with Dutch cooperation. Add Zeiss and its precision optics, world-class research at imec in Belgium, CEA-Leti in France and Fraunhofer in Germany, plus strong players like Infineon, NXP, and STMicroelectronics in automotive, power, and silicon-carbide chips. Europe doesn’t sit at the final-assembly line of the AI era — but it sits at several of its indispensable upstream stages.

KornaDoz 16 Piece SIM Card Removal Tool Set, Stainless Steel Ejector Pins & Keys, Universal SIM Tray Eject & SD Card Tool Compatible with iPhone, All Smartphones & Tablets, Essential Portable Tech Kit

[Universal Compatibility] A universal sim ejector tool compatible with most smartphones and tablets. This sim card pin is…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Sovereignty through indispensability

From this position follows a strategy that is gaining adherents in Brussels — and the one I consider realistic: not autarky, but indispensability.

The idea, argued by Bruegel and the Centre for Future Generations among others, is simple: if Europe can’t make everything itself, it should build out the chokepoints it does control so that partners and rivals have a hard self-interest in keeping Europe supplied and integrated. Anyone dependent on ASML’s machines and Zeiss’s optics thinks twice before turning off Europe’s memory or chip tap. That is mutual dependence as insurance.

In fairness, the autarky camp counters that only domestic fabrication creates real security, and that a sliver of home capacity is priceless in a crisis. Both arguments have merit. The Chips Act 2.0 attempts the straddle — emphasizing advanced packaging and new memory architectures, faster permitting, and the “lab-to-fab” RESOLVE initiative. But no one should be fooled: even the best plan does not close the fabrication gap by 2027.

The lesson from Apple’s China move

That’s precisely why the Apple episode is so instructive for Europe. Apple shows what dependence looks like under pressure — and Apple is the best conceivable case: a domestic supplier, political weight, the China option as an emergency exit. Europe is the worst case: no memory industry of its own, no emergency exit, no lobby in Seoul or Hsinchu.

If even Apple can’t buy its way out, then Europe’s answer is not to buy its way in — that doesn’t work on this timeline. The answer has to run on two tracks: use the unique chokepoints as genuine political leverage — and at the same time reduce dependence by needing less. For anyone running AI in Europe, that means concretely what this shortage already rewards: local-first instead of cloud dependence, open weights, efficient models, quantization, right-sized hardware. Brussels can’t close the fab gap. Companies and developers can lower their own exposure here and now.

The bottom line

The memory shortage is a sovereignty test, and Europe fails one half of it — supply — while it still holds the other half, leverage, in its hand. The honest conclusion is uncomfortable but clear: bury the 20-percent dream, defend and extend the chokepoints, and cut your own dependence wherever you can do so without Brussels.

Apple is reaching for Chinese memory because it can. Europe’s strength lies not in copying that reach — but in needing less, and in pressing what only Europe has. Anything else means waiting for cheap memory that, on the fab calendar, isn’t coming back any time soon.

Sources: European Commission and EUR-Lex (EU Chips Act, <10% global share, 20% target); Centre for Future Generations and Bruegel (indispensability strategy, ~11.7% by 2030, ASML’s €250bn estimate); European Court of Auditors (December 2025, “very unlikely”); TechPolicy.press (EU tech-sovereignty package, emergency powers); International Center for Law & Economics (HBM allocation, the limits of Brussels’ levers, memory prices); Financial Times via 9to5Mac/Engadget (Apple–CXMT report); Counterpoint Research (memory-price increase). As of late June 2026; figures are point-in-time and fast-moving. Analysis and opinions are the author’s and not investment advice.