€10 billion 2021-2027 European supercomputing investment through EuroHPC JU. 19 AI Factories selected across 21 European countries plus 13 AI Factory Antennas. €20 billion InvestAI Facility to create up to 5 AI Gigafactories with 100,000+ advanced AI processors each. JUPITER at #4 worldwide, LUMI at #9, Leonardo at #10 in the global TOP500. Alice Recoque deploying 2026 as Europe’s second exascale. The EuroHPC Federation Platform first release shipped April 15, 2026. 76 expressions of interest submitted to host AI Gigafactories. Council Regulation (EU) 2026/150 expanded the JU’s mandate. The compute substrate underlying every project in the seven-essay European sovereign-LLM framework — and the three structural complications the framework didn’t address directly.

By Thorsten Meyer — May 2026

This is the eighth standalone essay in the European sovereign-LLM track and the first Tier 2 expansion piece. The prior seven essays documented six distinct institutional answers (AMÁLIA, Minerva, OpenEuroLLM, Mistral, Aleph Alpha, Apertus) plus the integrative synthesis framework. Every one of those projects depends operationally on the EuroHPC compute substrate or a national-equivalent. Minerva trained on Leonardo. Apertus on Alps. OpenEuroLLM allocated millions of GPU hours across EuroHPC systems. AMÁLIA on Portuguese Deucalion. Mistral on commercial cloud plus the ASML strategic-investor partnership. Aleph Alpha historically on alpha ONE and now Schwarz Group’s STACKIT plus €11B Berlin data center. The compute substrate is the unifying infrastructure question the seven-essay framework didn’t address directly.

The structural argument I want to make in this piece: the EuroHPC infrastructure framework is the operational substrate for the European sovereign-AI movement, but it surfaces three structurally distinct complications that the seven-essay framework didn’t address directly. First, the AI Factory vs. AI Gigafactory bifurcation explicitly acknowledges that current AI Factory infrastructure is insufficient for frontier-class model training — this is the operational confirmation of Finding 1 from the synthesis essay (the structural capability gap is real). Second, the heterogeneity hidden cost (CUDA / ROCm / multi-generation hardware fragmentation) produces software complexity and optimization overhead that European AI developers absorb individually. Third, the hub-and-spoke geographical concentration of flagship systems in wealthier member states (Germany JUPITER, Italy Leonardo, Spain MareNostrum 5, France Alice Recoque) creates structural inequality that the AI Gigafactory Member State firm commitment model may exacerbate rather than resolve.

The headline integrative finding for this piece: the European sovereign-AI movement’s compute substrate is operationally credible at the AI Factory tier for mid-sized model training (Apertus 70B on Alps demonstrates this empirically) but structurally insufficient for frontier-class training, which is what the €20 billion AI Gigafactory framework is meant to address. The AI Gigafactory framework is the European AI policy framework’s response to Finding 1 of the synthesis essay — and it operationally confirms that single AI Factory tier is not enough. The June 2026 AI Gigafactory selection timeline and the August 2 EU AI Act enforcement window make summer 2026 the operational deadline against which the compute substrate’s strategic positioning should be evaluated.

This piece walks the EuroHPC infrastructure landscape forensically — the existing 19 AI Factories + flagship systems, the AI Gigafactory framework as the structural response to scale insufficiency, the heterogeneity and concentration complications the seven-essay framework didn’t surface, and what the compute substrate analysis implies for the synthesis essay’s strategic recommendations. The standard caveat applies: the EuroHPC landscape is moving fast (Federation Platform first release April 15, 2026 · AI Gigafactory selection process ongoing through 2026), and the strategic assessment may shift as specific procurement decisions ship through summer 2026 and beyond.

EuroHPC.

The compute

substrate.

€10 billion AI Factories + €20 billion AI Gigafactories. 19 AI Factories + 13 Antennas. JUPITER #4, LUMI #9, Leonardo #10. Federation Platform shipped April 15. The compute substrate underlying every project in the seven-essay framework — and the three structural complications the framework didn’t address directly.

This is the eighth standalone essay in the European sovereign-LLM track and the first Tier 2 expansion piece. The prior seven essays documented six institutional answers plus the integrative synthesis framework. Every one of those projects depends operationally on the EuroHPC compute substrate or a national-equivalent. Apertus trained on Alps (10,752 GH200 superchips, 4,096 GPUs). OpenEuroLLM allocated millions of GPU hours across multiple EuroHPC systems. Minerva trained on Leonardo. AMÁLIA on Deucalion. Mistral on commercial cloud + ASML strategic-investor partnership. Aleph Alpha historically on alpha ONE + now Schwarz Group STACKIT + €11B Berlin DC. The compute substrate is the unifying infrastructure question the seven-essay framework didn’t address directly. Summer 2026 is the operational moment when the substrate’s strategic positioning is determined.

Two tiers. One scale gap.

The EU policy framework operates two structurally distinct programmatic tiers. The bifurcation explicitly acknowledges that current AI Factory tier infrastructure is insufficient for frontier-class model training. The AI Gigafactory framework is the EU policy framework’s operational response to the structural capability gap Finding 1 from the synthesis essay surfaces empirically.

High-Performance AI Systems Engineering: Techniques for Faster Model Training, Efficient GPU Workloads, Distributed Computing, and Reliable AI Deployment across Modern Infrastructure

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

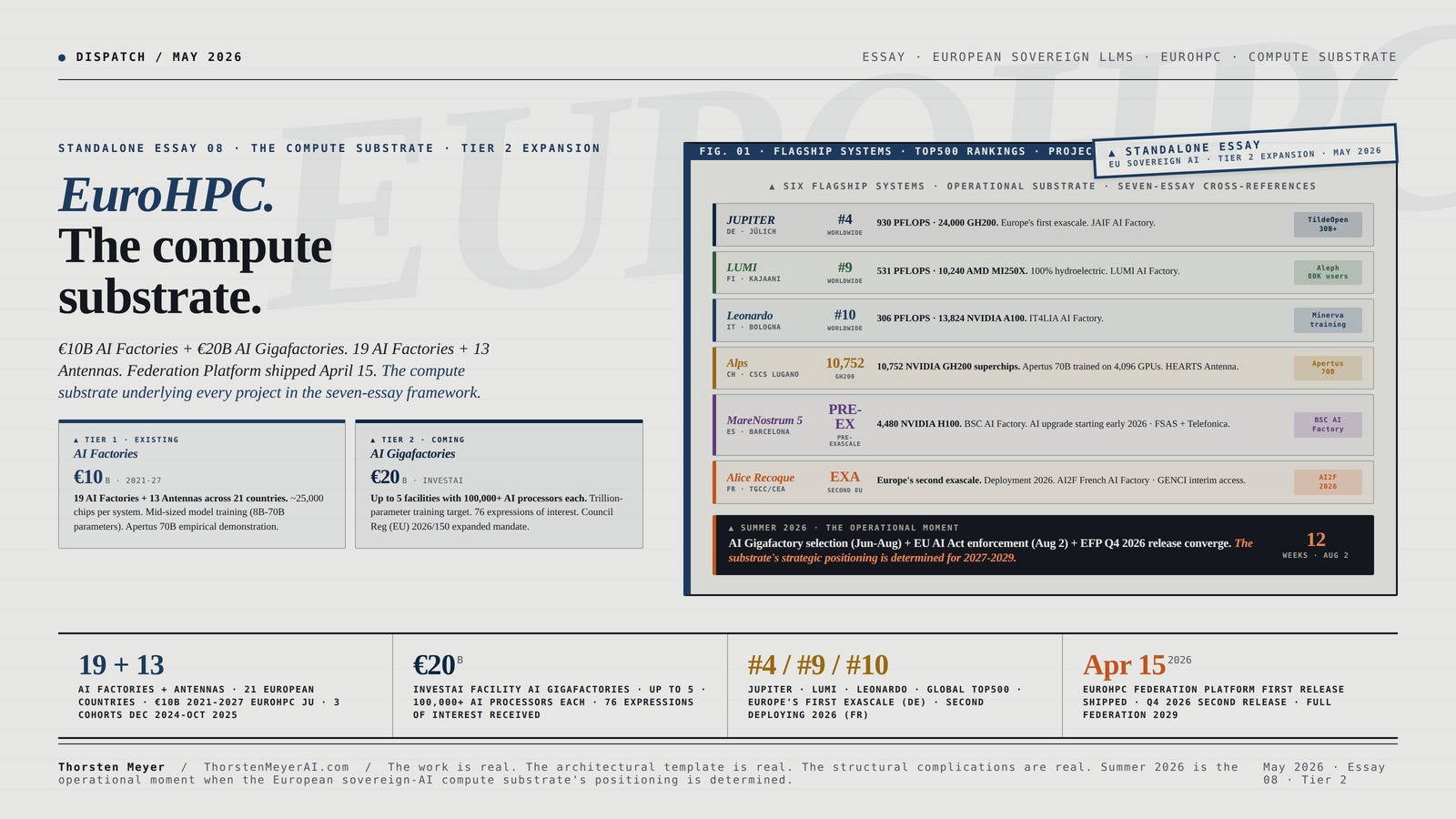

Six flagships. Six chromatic cross-references.

The flagship EuroHPC systems crystallize the substrate underlying the seven-essay framework. Three rank in the global TOP500 top 10. Two are exascale (one operational, one deploying 2026). All six are project-cross-referenced in the seven-essay framework. The chromatic register of each system maps to its project cross-reference.

30B+ trained

LUMI users

training

Factory

2026

70B

As an affiliate, we earn on qualifying purchases.

Three cohorts. 21 European countries.

The AI Factory selection has expanded rapidly through December 2024 – October 2025 across three cohorts. 13 AI Factory Antennas in 7 EU Member States plus 6 partner countries complete the framework. The Antennas are the institutional infrastructure connecting Apertus (Switzerland) and other partner-country projects to the EuroHPC framework.

RackChoice MATX/Mini-ITX 2U Rackmount Server Chassis hotswap 12bays 12Gbps SFF-8643 Backplane Include Sliding Rail and SFF-8643 Minisas to SATA Cables

- 2U server chassis support M/B size: Micro-ATX 9.6 x 9.6 /…

- Drive Bays: 12x 3.5" / 2.5" SATA/SAS…

- PSU: Supports standard ATX power supply…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three complications. Three policy gaps.

The compute substrate analysis surfaces three structurally distinct complications. These are not criticisms of EuroHPC — they are the operational realities the strategic discourse should integrate. The Federation Platform partially addresses the first; the AI Factory Antennas framework partially addresses the second; the AI Gigafactory framework explicitly addresses the third.

Software for Exascale Computing – SPPEXA 2016-2019 (Lecture Notes in Computational Science and Engineering Book 136)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Summer 2026. Three deadlines simultaneously.

The June 2026 AI Gigafactory selection process, the August 2 EU AI Act enforcement window, and the Q4 2026 EuroHPC Federation Platform second release all converge in summer 2026. This is the operational moment when the European sovereign-AI compute substrate’s strategic positioning is determined for the 2027-2029 horizon.

4 weeks ago

from now

moment

from now

from now

months

from now

The work is real across the EuroHPC framework. Substantial infrastructure built. 19 AI Factories operational or in deployment. 13 Antennas connecting smaller member states. EuroHPC Federation Platform shipped April 15, 2026. Apertus 70B operationally demonstrates Alps-tier training. The structural complications are also real. Heterogeneity hidden cost. Geographical concentration. Scale-tier bifurcation. Both can be true at once. Summer 2026 is the operational moment when the European sovereign-AI compute substrate’s strategic positioning is determined.

I · The institutional and infrastructure baseline

The factual baseline before the structural argument. From the European Commission AI Factories policy framework, the EuroHPC JU AI Factories Systems documentation, the EuroHPC JU five-year review, the Interface EU policy brief on AI Factories, and the October 2025 HPC User Forum EuroHPC presentation.

EuroHPC JU · the institutional structure

The European High Performance Computing Joint Undertaking is the legal and funding entity that coordinates European supercomputing. Created in 2018, reviewed in 2021 under Council Regulation (EU) 2021/1173, and expanded under Council Regulation (EU) 2026/150 to include AI Gigafactories and quantum technologies. The JU brings together the European Union and participating countries to coordinate efforts and pool resources with the objective of making Europe a world leader in supercomputing.

The 2021-2027 investment scope: €10 billion in supercomputing infrastructure and AI Factories through the EuroHPC JU — Commission contribution plus Member States’ and Associated Countries’ matching investments. This is the public-good infrastructure framework underlying every project in the seven-essay European sovereign-LLM track.

The institutional architecture has three distinct programmatic tiers:

- AI Factories · regional ecosystems built around AI-optimized supercomputers + data services + talent support + priority access for startups and SMEs · 19 selected total

- AI Factory Antennas · national gateways connected to AI Factories · 13 selected in 7 Member States and 6 partner countries · €55 million EU investment matched by participating states

- AI Gigafactories · large-scale facilities for trillion-parameter model training · €20 billion InvestAI Facility · up to 5 facilities · 100,000+ advanced AI processors each

The programmatic tiering is structurally important. It explicitly acknowledges three distinct operational scales: AI Factories serve research and mid-sized model training; AI Factory Antennas serve regional access; AI Gigafactories serve frontier-class training at scales comparable to private AI labs and cloud providers. The bifurcation between AI Factories and AI Gigafactories is the EU policy framework’s operational acknowledgment that current AI Factory tier infrastructure is insufficient for frontier model training.

The 19 AI Factories · selected across three cohorts

The selection timeline crystallizes the EuroHPC AI Factory framework’s rapid expansion through 2024-2025:

- December 2024 cohort (7 sites) · Finland (LUMI), Germany (JUPITER), Greece (Daedalus), Italy (IT4LIA · Leonardo), Luxembourg (MeluXina), Spain (BSC · MareNostrum 5), Sweden (Arrhenius)

- March 2025 cohort (6 sites) · Austria, Bulgaria, France (AI2F · Alice Recoque + GENCI national systems), Germany (additional · Jülich experimental platform), Poland, Slovenia (SLAIF · Vega + IZUM)

- October 2025 cohort (6 sites) · Czech Republic (CZAI · KarolAIna + Karolina), Lithuania, Netherlands, Poland (additional), Romania, Spain (experimental platform)

The 19 AI Factories involve 21 European countries and operate under a federated framework that the EuroHPC Federation Platform (EFP) is progressively integrating. Each AI Factory acts as a one-stop shop nationally, offering European AI startups, SMEs, and researchers comprehensive support to develop AI-ready data, access AI-optimised HPC resources, training, and expert guidance.

The 13 AI Factory Antennas complement this network with regional access points: Belgium, Cyprus, Hungary, Ireland, Latvia, Malta, Slovakia (EU Member States) plus Iceland, Moldova, North Macedonia, Serbia, Switzerland (HEARTS Antenna for Apertus’s Alps infrastructure), and the United Kingdom (partner countries). This is the institutional infrastructure connecting Apertus operationally to the EuroHPC framework despite Switzerland being outside the EU.

The flagship supercomputing systems · TOP500 rankings

Three EuroHPC systems rank in the global TOP500 top 10 as of mid-2025 per the Interface EU policy brief:

- JUPITER (Germany · Jülich) · #4 worldwide · 930 PFLOPS peak · 24,000 NVIDIA GH200 Grace Hopper superchips in booster module · Europe’s first exascale supercomputer · fully online since late 2025

- LUMI (Finland · Kajaani) · #9 worldwide · 531.51 PFLOPS · 10,240 AMD Instinct MI250X GPUs · ranked among the greenest supercomputers globally · 100% hydroelectric power

- Leonardo (Italy · Bologna) · #10 worldwide · 306.31 PFLOPS · 3,456 compute nodes × 4 NVIDIA A100 = 13,824 A100 accelerators in the Booster Module

Other flagship systems crystallized across the seven-essay framework:

- MareNostrum 5 (Spain · Barcelona Supercomputing Center) · 1,120 nodes × 4 NVIDIA H100 = 4,480 H100 GPUs in accelerated partition · AI upgrade signed January 2026 with FSAS Technologies + Telefonica consortium · installation starting early 2026

- Alice Recoque (France · TGCC/CEA) · Europe’s second exascale supercomputer · deployment starting 2026 · AI2F French AI Factory committed to interim access via GENCI national systems (Jean Zay at IDRIS/CNRS, Adastra at CINES/France Universités, Joliot-Curie at TGCC/CEA)

- Alps (Switzerland · CSCS Lugano) · 10,752 NVIDIA GH200 Grace Hopper superchips · trained Apertus 70B on up to 4,096 GPUs with 10M+ GPU hours invested · HEARTS Antenna links Switzerland to EuroHPC framework

- Deucalion (Portugal) · petascale · supports Portuguese AMÁLIA national project

- Karolina (Czech Republic) · petascale · KarolAIna AI-optimized successor under Czech AI Factory framework

For temporal context on the seven-essay framework: the AMÁLIA, Minerva, OpenEuroLLM, and Apertus projects all access this institutional infrastructure operationally. Mistral and Aleph Alpha use commercial cloud + strategic-investor compute (ASML for Mistral · Schwarz Group STACKIT and €11B Berlin DC for Aleph Alpha post-merger) plus selective EuroHPC allocations through specific research projects.

Documented training runs on EuroHPC infrastructure

Per the Interface EU policy brief, specific training runs that have been operationally documented on EuroHPC systems:

- Apertus 70B trained on Alps (Switzerland) · 10,752 NVIDIA GH200 superchips infrastructure · 4,096 GPUs used · 15T tokens

- TildeOpen LLM (30B+ parameters) trained on LUMI and JUPITER · multilingual European model

- Minerva-7B trained on Leonardo (Italy) · 128 GPUs · Sapienza + FAIR consortium

- AMÁLIA derivatives on Deucalion (Portugal) · Portuguese pt-PT specialization

This is the operational evidence that EuroHPC infrastructure supports up to 70B parameter model training at current scale. It also crystallizes the structural ceiling: no European frontier-class training run (200B+ dense parameters or trillion-parameter MoE) has been operationally documented on EuroHPC infrastructure. This is the empirical gap the AI Gigafactory framework is meant to address.

II · The AI Gigafactory framework · the structural response to scale insufficiency

The most structurally significant European AI infrastructure policy development of 2025-2026. From the European Commission AI Factories policy page, the EuroHPC JU AI Gigafactories framework, and the EuroHPC JU AI Gigafactories FAQ documentation.

The InvestAI Facility · €20 billion

The InvestAI Facility is the EU’s €20 billion investment vehicle to create up to 5 AI Gigafactories. It operates as a public-private partnership framework intended to “guarantee a secure investment landscape and nurture a competitive and innovative AI ecosystem within Europe.” This is the structurally distinct infrastructure framework from AI Factories — different scale, different funding model, different operational objective.

AI Gigafactories are large-scale facilities dedicated to the development and training of next-generation AI models containing trillions of parameters. To achieve this, AI Gigafactories will bring together:

- Computing power — over 100,000 advanced AI processors

- Strong emphasis on power capacity

- Reliable supply chains

- Advanced networking

- Energy efficiency

- AI-driven automation

For scale context: 100,000+ AI processors is approximately 4× the scale of JUPITER’s booster module (24,000 GH200 superchips). This is frontier-class training infrastructure at scales comparable to private AI lab and cloud provider compute.

The procurement and selection framework

Per the EuroHPC JU AI Gigafactories FAQ documentation, the AI Gigafactory selection process operates through a distinctive joint procurement framework:

- Joint Procurement Agreement (JPA) between EuroHPC JU and Participating States — signature expected February 2026 ahead of Call for Tenders launch

- Member State firm commitment required before Call for Expression of Interest launches — committing to fund the AI Gigafactory’s share within their territory

- Independent expert panel + accredited financial institution evaluate submissions — Governing Board selects

- Two financial models available: CAPEX (capital expenditure) or Off-take (capacity purchase commitments)

- Member States have no role in evaluation or selection process — fairness and “non-imputability of the State”

Per the Interface EU policy brief, 76 expressions of interest have been submitted to host AI Gigafactories. This is structurally significant — it indicates substantial European competition to host the new infrastructure. The Member State firm commitment model means hosting an AI Gigafactory requires substantial national budget allocation, which structurally favors wealthier member states (a complication surfaced in Section III below).

The strategic-positioning implications

Three structural observations about the AI Gigafactory framework worth surfacing:

Observation 1 · The AI Gigafactory framework is the EU policy framework’s operational acknowledgment that AI Factories are insufficient for frontier training. The Interface EU policy brief makes this explicit: “AI factories are suited to supporting research in training medium-sized AI models, the factories are not sufficient to boost commercial AI innovation across the EU at scale.” The AI Gigafactory tier explicitly addresses this gap. This is the policy-level confirmation of Finding 1 from the synthesis essay (the structural capability gap is real and consistent across all six institutional models).

Observation 2 · The €20B AI Gigafactory commitment is structurally meaningful at European investment scales but still modest at US frontier-developer scales. OpenAI’s Stargate project commitments operate in the hundreds of billions of dollars; Microsoft, Google, and Meta combined AI infrastructure capex through 2026 exceeds $400B. The EU’s €20B AI Gigafactory commitment is approximately one-twentieth of US private-sector AI infrastructure commitment. This is not a criticism — it is the operational scale honest acknowledgment. The AI Gigafactory framework is structurally credible at European public-finance scales; it is not structurally credible as a frontier-match commitment at US scales.

Observation 3 · The June 2026 AI Gigafactory selection timeline aligns with the August 2, 2026 EU AI Act enforcement window. The two operational deadlines arrive nearly simultaneously. This crystallizes summer 2026 as the operational moment for the European sovereign-AI movement. AI Gigafactory selection decisions and EU AI Act enforcement decisions will both ship through summer 2026 — both shape the operational substrate for the strategic-positioning recommendations from Essay 07 (the synthesis framework).

III · The three structural complications · what the seven-essay framework didn’t address

The compute substrate analysis surfaces three structurally distinct complications that the seven-essay framework didn’t address directly. These are not criticisms of EuroHPC — they are the operational realities the strategic discourse should integrate.

Complication 1 · Hardware heterogeneity · the hidden software cost

The EuroHPC fleet is structurally heterogeneous across multiple dimensions. Per Segler Consulting’s analysis, the fleet is “a diverse mix of accelerator architectures (NVIDIA’s CUDA-based GPUs and AMD’s ROCm-based GPUs) and multiple generations of hardware (NVIDIA’s V100, A100, H100, and GH200; AMD’s MI250X).”

The operational implication is structurally significant. A European AI developer building a model on LUMI must use the AMD ROCm software stack. To run or scale that same model on Leonardo or MareNostrum 5, they would need to port their code to NVIDIA’s CUDA platform — “a non-trivial engineering task,” per Segler. Even within the NVIDIA ecosystem, optimizing code for the different tensor core capabilities, memory hierarchies, and interconnects of the A100, H100, and GH200 architectures requires specialized work.

The empirical evidence from Apertus crystallizes this. Per the Apertus engineering experience report, the Apertus project team discovered that “for specific container-image versions, the Python reference implementation of xIELU was incompatible with torch.compile, causing JIT compilation to fail, preventing execution. CSCS engineers supported the users by diagnosing the issue within the lower layers of the software stack and developing a custom CUDA kernel that restored compatibility with the compilation pipeline.” The kernel optimization work achieved approximately 20% kernel execution speedup but required specialized systems and performance-engineering expertise from CSCS engineers.

The structural implication for European sovereign-AI strategy: the heterogeneity cost is real and absorbed individually by each European AI project. This is the hidden tax on European sovereign-AI development that does not exist at the same magnitude for US frontier developers using homogeneous NVIDIA infrastructure. The EuroHPC Federation Platform is meant to address some of this, but full federation isn’t operational until 2029. In the interim, every European AI project pays the heterogeneity cost.

Complication 2 · Hub-and-spoke geographical concentration

The flagship system distribution crystallizes the second structural complication. JUPITER is in Germany. Leonardo is in Italy. MareNostrum 5 is in Spain. Alice Recoque is in France. Per Segler Consulting, this creates “a hub-and-spoke model where smaller or less wealthy nations are relegated to hosting less powerful petascale systems or establishing ‘Antennas’ — national gateways that provide access to the larger factories on the continent.”

The structural cause is the co-funding model. Hosting entities are required to match the EU’s substantial financial contributions for top-tier systems. Only nations with significant domestic science and technology budgets can afford to host the most powerful exascale machines. The AI Gigafactory framework structurally amplifies this dynamic — Member State firm commitment is required before Call for Expression of Interest, and the financial commitment scales with AI Gigafactory scope.

The empirical pattern from the seven-essay framework crystallizes this. Mistral (France) operates from the country with the second exascale system and the largest national-funding capacity. Aleph Alpha (Germany) is anchored in the country hosting Europe’s first exascale system and the strongest industrial-capital ecosystem (Schwarz Group €500M+ + $600M Cohere Series E + €11B Berlin DC). Apertus (Switzerland) operates outside the EU but on the second-largest GH200 deployment globally (Alps · 10,752 GH200). AMÁLIA (Portugal) and Minerva (Italy) operate at smaller national infrastructure scales — AMÁLIA on Deucalion (petascale Portuguese system), Minerva on 128 GPUs of Leonardo (Italy’s larger flagship).

The strategic-positioning implication: the EuroHPC framework’s geographical concentration creates structural inequality that the seven-essay framework’s partnership-architecture finding partially addresses but doesn’t resolve. The portfolio approach (Recommendation 5 from Essay 07) is the policy framework’s response to this complication — different institutional structures for different operational requirements, with the AI Factory Antennas providing regional access points for smaller member states.

Complication 3 · The AI Factory tier scale gap

The Interface EU policy brief crystallizes the third complication explicitly: “Although the EU’s AI factories host highly performing supercomputers, their AI-specific capacities are lower scale than many of leading supercomputers privately owned by leading AI labs and cloud providers. They do allow for training and deploying mid-sized AI models.”

Quantitatively: JUPITER’s 24,000 GH200 booster module is approximately 1/4 the scale of the AI Gigafactory target (100,000+ advanced AI processors). MareNostrum 5’s 4,480 H100 GPUs is approximately 1/22 the AI Gigafactory target. Leonardo’s 13,824 A100 accelerators is approximately 1/7 the target. LUMI’s 10,240 AMD MI250X GPUs is approximately 1/10 the target. The current EuroHPC AI Factory tier operates at scales appropriate for training models up to ~70B parameters but structurally insufficient for trillion-parameter frontier training.

The empirical training-run evidence confirms this scale ceiling. Apertus-70B trained on 4,096 GPUs of Alps. TildeOpen LLM (30B+ parameters) trained on LUMI and JUPITER. Minerva-7B trained on 128 GPUs of Leonardo. No frontier-class European training run (200B+ dense parameters or trillion-parameter MoE) has been operationally documented on EuroHPC infrastructure. This is the empirical confirmation of the AI Factory tier’s structural scale ceiling.

The strategic implication: the AI Gigafactory framework is the EU policy framework’s response to this scale gap. The June 2026 AI Gigafactory selection timeline determines whether Europe will have frontier-class training infrastructure operational by 2027-2028. This is the timeline against which Recommendation 3 from Essay 07 (industrial-anchor investment model at scale) should be evaluated. The Schwarz Group industrial-anchor model and the AI Gigafactory framework are complementary structural responses to the same scale gap.

IV · The EuroHPC Federation Platform · the operational integration framework

The architectural framework attempting to address the heterogeneity hidden cost. From the October 2025 HPC User Forum presentation and the LUMI AI Factory access calls documentation.

The Federation Platform timeline

The EuroHPC Federation Platform (EFP) project started January 2025 with contract signed December 2024. The deployment timeline:

- Phase 1 (2025-2026) · Development of a Minimum Viable (Federation) Platform (MVP) covering six key areas including federated AAI, resource allocations, and complex workflow manager with smart scheduler

- Q1 2026 first release · Integration with currently online EuroHPC HPC and AI systems · shipped April 15, 2026

- Q4 2026 second release · Additional EFP components and capabilities

- 2026-2029 · Progressive inclusion of PoIs (Points of Interface)

- 2029 · Fully hyperconnected ecosystem in operation

The April 15, 2026 first release shipped four weeks before this essay’s publication. It is the operational evidence that the federation framework is moving from policy to production. However, the full federation timeline (2029) means the heterogeneity hidden cost remains operationally significant through at least 2027-2028 — the same window during which AI Gigafactory selection decisions and EU AI Act enforcement determine the European sovereign-AI movement’s structural positioning.

The federation architecture · what it solves and what it doesn’t

The EuroHPC Federation Platform addresses six key areas:

- Federated Authentication and Authorization Infrastructure (AAI) · unified login/access across EuroHPC systems

- Resource allocations · cross-system compute booking and management

- Complex workflow manager · multi-system pipeline orchestration

- Smart scheduler · workload placement optimization across federated systems

- Data management · cross-system data accessibility

- User experience harmonization · common service standards

What the Federation Platform addresses: the operational friction of accessing multiple EuroHPC systems through unified interfaces. It does not address the underlying hardware heterogeneity (CUDA vs ROCm fragmentation). It does not address the geographical concentration of flagship systems. It does not address the scale gap relative to AI Gigafactory or US frontier-developer infrastructure.

The structural implication: the Federation Platform is necessary but not sufficient. It improves the operational user experience for European AI developers accessing EuroHPC infrastructure, but it does not eliminate the three structural complications surfaced in Section III. The structural complications remain operationally significant through 2027-2028 even after full Federation Platform deployment in 2029.

The April 2026 HORIZON-JU-EUROHPC-2026-COAIF-03 call

Per the EuroHPC JU April 28, 2026 announcement, the EuroHPC JU launched a new call for proposals with €25 million indicative budget targeting three specific challenges:

- Coordinating and networking of AI Factories and Antennas · building common service standards and harmonized user experience

- Networking of AIF Data Labs · supporting connection across Europe via shared Simpl platform · secure and efficient data and tools sharing compliant with European regulations

- Strengthening AI Factories network · improved coordination + expanded high-quality data + boosted global competitiveness

The €25M call has a 3-year duration with €12.5M EU contribution and deadline June 23, 2026. This is the operational follow-up to the Federation Platform first release — the harmonization framework that bridges the gap between technical federation (EFP) and institutional federation (AI Factories network coordination).

The strategic implication: the April 2026 call signals that the EuroHPC framework is moving from infrastructure deployment to operational federation as the priority programmatic work through 2026-2028. This is the institutional evidence that the policy framework is integrating the heterogeneity-cost complication structurally — not just through hardware procurement but through service-standards harmonization.

V · The compute substrate analysis · what it implies for the seven-essay framework

The integrative observations the EuroHPC infrastructure analysis produces for the synthesis essay’s strategic recommendations.

Implication 1 · The synthesis essay’s Finding 1 is operationally confirmed by the AI Gigafactory framework

The synthesis essay’s first structural finding — “the structural capability gap is real and consistent across all six institutional models” — is operationally confirmed by the EU policy framework’s bifurcation between AI Factories (€10B 2021-2027) and AI Gigafactories (€20B InvestAI Facility). The EU policy framework explicitly acknowledges that current AI Factory tier infrastructure is insufficient for frontier-class training. This is the institutional evidence that the synthesis essay’s strategic-positioning recommendation (stop pursuing Position 1 at AI Factory tier scale) is operationally grounded.

The strategic implication: the AI Gigafactory framework is the EU policy framework’s attempt to address Finding 1 by changing the operational substrate’s scale. The June 2026 AI Gigafactory selection decisions will determine whether Europe builds frontier-class infrastructure capable of supporting Position 1-grade training runs by 2027-2028. This does not invalidate Recommendation 4 from Essay 07 (stop pursuing Position 1 as strategic objective) — it modifies the timeline. Until AI Gigafactory infrastructure ships operationally, Position 1 remains empirically unsupported at European scales. After AI Gigafactory infrastructure ships, the strategic-positioning question becomes whether to pursue Position 1 with frontier-grade infrastructure or to remain on the Position 2 + Position 4 framework with frontier-grade infrastructure deployed for sovereignty + vertical specialization objectives.

Implication 2 · The compute substrate validates the partnership-architecture finding

The synthesis essay’s Finding 3 — “partnership architecture is the operational structure that scales” — is structurally validated by the EuroHPC framework itself. EuroHPC is operationally a 21-country partnership architecture — the consortium-partnership model from Essay 03 (OpenEuroLLM) operating at infrastructure scale rather than project scale. The 19 AI Factories + 13 Antennas + 5 planned AI Gigafactories all operate through partnership consortia.

The empirical evidence from the seven-essay framework crystallizes this. The AI2F French AI Factory consortium includes GENCI + AMIAD + CEA + Cines + CNRS + France Universités + Inria + French Tech + Station F + HubFranceIA. The SLAIF Slovenian AI Factory includes IZUM + Jožef Stefan Institute + ARNES + five universities. The CZAI Czech AI Factory includes VSB Technical University Ostrava + Brno University of Technology + Charles University + Czech Technical University + INDRA + IOCB. Every AI Factory operates as a partnership consortium. The single-firm competitive frame is empirically unsupported at infrastructure scale, just as it is unsupported at project scale.

The strategic implication: Recommendation 1 from Essay 07 (recognize partnership architectures explicitly in European AI policy) is structurally validated by the EuroHPC framework’s own institutional architecture. European AI policy is already partially operationalizing this recommendation through the EuroHPC consortium model — but the recognition could be more explicit in funding criteria, procurement requirements, and regulatory frameworks beyond infrastructure deployment.

Implication 3 · The Apertus case is the architectural-template for EuroHPC integration

The synthesis essay’s Finding 4 — “compliance can be architectural, not policy-layer” — combines with the EuroHPC infrastructure context to produce a sharper strategic argument. Apertus’s training on Alps (Switzerland) operationally demonstrates that architectural-compliance European AI projects can scale to 70B parameters on EuroHPC-tier infrastructure. The retroactive opt-out compliance + Goldfish loss + memorization avoidance framework is buildable at 70B scale on 4,096 GPUs.

The strategic implication: Recommendation 2 from Essay 07 (adopt Apertus-style architectural compliance as reference standard) is operationally validated at EuroHPC infrastructure scale. European AI projects that adopt the Apertus architectural-compliance template can train at 70B+ scale on EuroHPC infrastructure without requiring AI Gigafactory-tier resources. This is the empirical evidence that Position 2 + Position 4 strategic positioning is operationally credible at current EuroHPC AI Factory scale — independent of whether AI Gigafactory infrastructure ships by 2027-2028.

Implication 4 · The heterogeneity cost and concentration complications need explicit policy responses

The three structural complications surfaced in Section III are not addressed adequately by the EuroHPC Federation Platform alone. Recommendation 5 from Essay 07 (build a portfolio approach that supports all six institutional structures) should explicitly integrate the heterogeneity-cost mitigation and geographical-concentration redistribution dimensions.

Concrete policy implications:

- Heterogeneity cost mitigation · European AI policy should support open-source software stacks (PyTorch ROCm, NVIDIA Megatron) and porting toolkits that reduce the CUDA/ROCm fragmentation cost individually absorbed by each European AI project. The April 2026 HORIZON-JU-EUROHPC-2026-COAIF-03 call partially addresses this through service-standards harmonization, but explicit software-stack support would accelerate the integration timeline before 2029.

- Geographical concentration redistribution · the AI Factory Antennas framework (€55M EU + matching state investment) is the policy response to flagship-system concentration. Strengthening Antenna funding and access guarantees would reduce the structural inequality that the AI Gigafactory Member State firm commitment model may exacerbate.

- AI Gigafactory geographical distribution · the AI Gigafactory selection process should explicitly weight geographical distribution alongside technical and financial criteria, ensuring that the 5 planned facilities are not all hosted in the four largest member states.

VI · The closing argument · the compute substrate and the August 2 enforcement window

The integrative observation the compute substrate analysis produces for the seven-essay framework’s strategic positioning. The EuroHPC infrastructure framework is operationally credible at the AI Factory tier for current European sovereign-AI requirements — but the structural complications and the AI Gigafactory framework’s June 2026 selection timeline make summer 2026 the operational moment when the substrate’s strategic positioning is determined for the 2027-2029 horizon.

Summary of the eight-essay framework as of mid-May 2026:

The European sovereign-LLM essay track now operates as a complete strategic framework with infrastructure substrate analysis:

- Essay 01 · AMÁLIA · Portuguese national continuation · operates on Deucalion (petascale)

- Essay 02 · Minerva · Italian national from-scratch · operates on Leonardo (#10 globally, 13,824 A100)

- Essay 03 · OpenEuroLLM · pan-European consortium · operates across multiple EuroHPC systems

- Essay 04 · Mistral · French commercial-frontier · operates on commercial cloud + ASML strategic-investor compute

- Essay 05 · Aleph Alpha · German enterprise-sovereignty pivot · historically alpha ONE + now Schwarz Group STACKIT + €11B Berlin DC

- Essay 06 · Apertus · Swiss federal-research-institution · operates on Alps (10,752 GH200) · the empirical EuroHPC-tier training demonstration

- Essay 07 · Portfolio · the synthesis framework · seven structural findings + five strategic recommendations

- Essay 08 (this piece) · EuroHPC · the compute substrate analysis · three structural complications + AI Gigafactory framework + Federation Platform timeline

The integrative finding crystallized: the European sovereign-AI compute substrate is operationally credible at the AI Factory tier for mid-sized model training (up to 70B parameters demonstrated empirically), structurally insufficient for frontier-class training (the AI Gigafactory framework is the policy-level response), and structurally complicated by hardware heterogeneity, geographical concentration, and scale-tier bifurcation. All three of these are operational realities the strategic discourse should integrate.

The August 2 enforcement window remains twelve weeks away. The June 2026 AI Gigafactory selection process runs in parallel. Summer 2026 is the operational moment when the European sovereign-AI movement’s compute substrate, regulatory framework, and strategic positioning are all simultaneously determined. The eight-essay framework is what the discourse should integrate before the windows close.

For the European AI policymaker specifically, the compute substrate analysis adds five concrete operational implications to the synthesis essay’s strategic recommendations:

- The AI Gigafactory framework operationally confirms Finding 1 — current AI Factory tier is insufficient for frontier-class training. The €20B InvestAI Facility is the policy response.

- The EuroHPC partnership architecture validates Finding 3 — partnership consortia operate at infrastructure scale, not just project scale. European AI policy should integrate this empirical pattern explicitly.

- Apertus’s Alps training operationally validates Recommendation 2 — architectural-compliance European AI projects can scale to 70B parameters on EuroHPC-tier infrastructure independent of AI Gigafactory deployment.

- The heterogeneity hidden cost and geographical concentration require explicit policy responses — the Federation Platform (full deployment 2029) and Antennas framework partially address these but additional software-stack support and AI Gigafactory geographical distribution criteria would accelerate integration.

- The June 2026 AI Gigafactory selection timeline + August 2 EU AI Act enforcement window make summer 2026 operationally significant. The five strategic recommendations from Essay 07 should be evaluated against these specific deadlines.

That’s the read on the EuroHPC compute substrate as of mid-May 2026 — twelve weeks before the August 2 enforcement window opens and approximately six weeks before the AI Gigafactory selection decisions begin shipping. The work is real across the EuroHPC framework. Substantial infrastructure built. 19 AI Factories operational or in deployment. 13 Antennas connecting smaller member states. EuroHPC Federation Platform shipped April 15, 2026. The structural complications are also real. Heterogeneity hidden cost, geographical concentration, scale-tier bifurcation. Both can be true at once.

The European AI strategic discourse should be ready for whatever the empirical data shows across the AI Gigafactory selection, the August 2 enforcement window, and the seven-essay-plus-substrate framework simultaneously, including findings that complicate any single-framework narrative. The compute substrate analysis is the operational grounding the synthesis essay’s strategic recommendations needed. Different tiers of infrastructure. Different institutional partnerships. Different operational requirements. One coherent European sovereign-AI compute substrate — operationally credible at AI Factory tier, structurally insufficient at frontier-tier without AI Gigafactory deployment, complicated by heterogeneity and concentration through at least 2027-2028.

The August 2 enforcement window is twelve weeks away. The AI Gigafactory selection timeline is operationally active. The discourse should integrate the eight-essay framework before both deadlines arrive.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Reading · the European sovereign-LLM essay track

- AMÁLIA · The Three Hard Questions — Standalone Essay 01 · Portuguese national continuation answer · operates on Deucalion

- Minerva · The Opposite Path — Standalone Essay 02 · Italian national from-scratch answer · operates on Leonardo

- OpenEuroLLM · The Third Path — Standalone Essay 03 · pan-European consortium answer · multi-system EuroHPC

- Mistral · The Fourth Path — Standalone Essay 04 · commercial-frontier answer · commercial cloud + ASML

- Aleph Alpha · The Retrospective Case — Standalone Essay 05 · enterprise-sovereignty pivot answer · Schwarz Group STACKIT

- Apertus · The Architectural Template — Standalone Essay 06 · federal-research-institution answer · operates on Alps · 10,752 GH200

- Portfolio · The Synthesis — Standalone Essay 07 · synthesis framework · seven structural findings + five strategic recommendations

- This piece — Standalone Essay 08 · EuroHPC · the compute substrate analysis · three structural complications + AI Gigafactory framework + Federation Platform

Sources

EuroHPC institutional and infrastructure framework

- European Commission · Shaping Europe’s digital future · AI Factories policy · €10B 2021-2027 investment · 19 AI Factories + 13 Antennas + €20B InvestAI Facility

- EuroHPC JU · AI Factories Systems · IT4LIA Italy / BSC Spain / LUMI Finland / Discoverer Bulgaria

- EuroHPC JU · AI Factories overview · framework architecture

- EuroHPC JU · AI Gigafactories framework · 100,000+ advanced AI processors target

- EuroHPC JU · AI Gigafactories FAQ · JPA · CAPEX vs Off-take · Member State commitment framework

- EuroHPC JU · AI Factories Access Modes · Industrial Innovation track

- EuroHPC JU · Five Years review · December 17, 2025 · 145M+ node hours awarded · 2,334 projects

- EuroHPC JU · MareNostrum 5 AI upgrade contract · January 26, 2026 · FSAS Technologies + Telefonica consortium

- EuroHPC JU · Six additional AI Factories selected · October 10, 2025 · Czechia · Lithuania · Netherlands · Poland · Romania · Spain

- EuroHPC JU · Additional AI Factories March 12, 2025 · Austria · Bulgaria · France (AI2F) · Germany (Jülich) · Poland · Slovenia (SLAIF)

- EuroHPC JU · HORIZON-JU-EUROHPC-2026-COAIF-03 call · April 28, 2026 · €25M coordination + networking call

- EuroHPC JU · AI Factory Antennas selection · LUMI AI Factory documentation · 13 Antennas · €55M EU funding

- LUMI supercomputer · EuroHPC Access Calls for AI Factories · April 15, 2026 EFP first release · Industrial Innovation track

Independent analysis

- Interface EU · The European Union’s AI Factories · policy brief on AI Factories framework · TildeOpen 30B+ training on LUMI and JUPITER · 76 expressions of interest for AI Gigafactories

- Segler Consulting · Europe’s AI Gambit: An In-Depth Analysis of the EuroHPC AI Factories and the Quest for Digital Sovereignty · heterogeneity hidden cost analysis · hub-and-spoke concentration analysis · CUDA vs ROCm fragmentation

- HPC User Forum · Josephine Wood · The European High Performance Computing Joint Undertaking · October 2025 · Federation Platform timeline · system distribution

- Magazyn Rekruter · Europe’s Sovereign AI Factories: The Top 5 You Need to Know in 2026 · February 13, 2026 · JAIF / LUMI / IT4LIA / BSC / SLAIF

- HPCwire · EuroHPC Launches Call for Proposals · May 2026 coverage

Key reference figures and quantitative facts

- EuroHPC JU 2021-2027 total investment · €10 billion across infrastructure and AI Factories

- InvestAI Facility AI Gigafactory commitment · €20 billion for up to 5 facilities

- AI Factory Antennas budget · €55M EU + matching state investment

- AI Gigafactory chip target · 100,000+ advanced AI processors per facility

- AI Gigafactory model training target · trillion-parameter models

- AI Gigafactory expressions of interest received · 76 European cities/consortia

- Council Regulation (EU) 2026/150 · expanded EuroHPC JU mandate to include AI Gigafactories + quantum

- JUPITER (Germany Jülich) · #4 worldwide · 930 PFLOPS · 24,000 NVIDIA GH200 superchips · Europe’s first exascale

- LUMI (Finland Kajaani) · #9 worldwide · 531.51 PFLOPS · 10,240 AMD Instinct MI250X · 100% hydroelectric

- Leonardo (Italy Bologna) · #10 worldwide · 306.31 PFLOPS · 13,824 NVIDIA A100 accelerators · 3,456 nodes × 4

- MareNostrum 5 (Spain Barcelona) · 4,480 NVIDIA H100 · AI upgrade starting early 2026 · FSAS + Telefonica

- Alice Recoque (France TGCC/CEA) · Europe’s second exascale · deployment 2026

- Alps (Switzerland CSCS Lugano) · 10,752 NVIDIA GH200 superchips · trained Apertus on 4,096 GPUs

- Deucalion (Portugal) · petascale · supports AMÁLIA

- Karolina (Czech Republic) · petascale · KarolAIna AI-optimized successor

- AI Factory cohort 1 (December 2024) · 7 sites · Finland · Germany · Greece · Italy · Luxembourg · Spain · Sweden

- AI Factory cohort 2 (March 2025) · 6 sites · Austria · Bulgaria · France · Germany (additional Jülich experimental) · Poland · Slovenia

- AI Factory cohort 3 (October 2025) · 6 sites · Czechia · Lithuania · Netherlands · Poland (additional) · Romania · Spain (experimental)

- AI Factory Antennas (13) · EU Member States: Belgium · Cyprus · Hungary · Ireland · Latvia · Malta · Slovakia · Partner countries: Iceland · Moldova · North Macedonia · Serbia · Switzerland · UK

- EuroHPC Federation Platform Q1 2026 first release · shipped April 15, 2026

- EuroHPC Federation Platform Q4 2026 second release · additional components

- EuroHPC Federation Platform full deployment · 2029

- HORIZON-JU-EUROHPC-2026-COAIF-03 call · €25M indicative budget · €12.5M EU contribution · 3-year duration · June 23, 2026 deadline

- AMÁLIA · Minerva · OpenEuroLLM · Mistral · Aleph Alpha · Apertus · Portfolio synthesis · seven-essay framework cross-references