By Thorsten Meyer | ThorstenMeyerAI.com | February 2026

Executive Summary

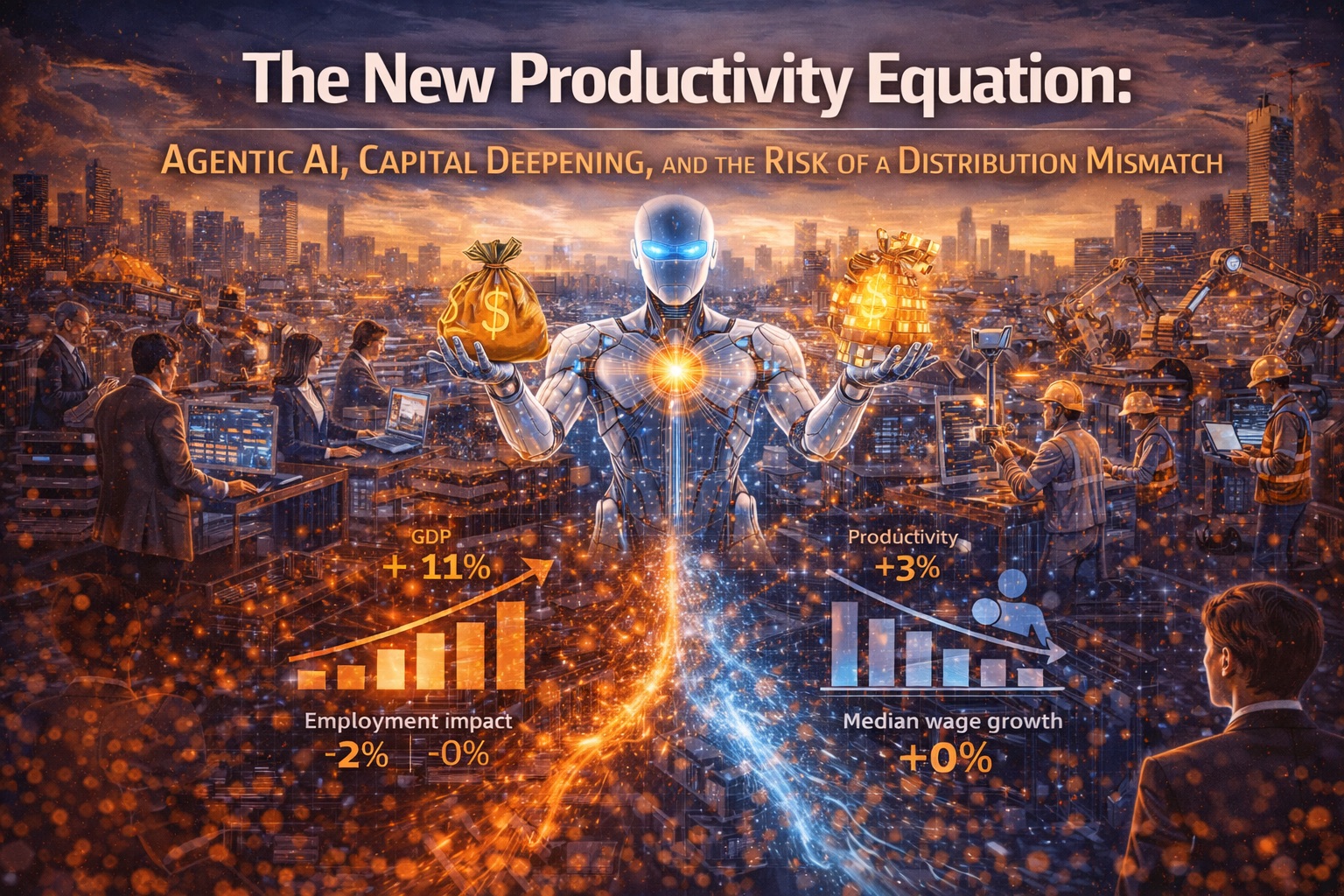

Hyperscaler capital expenditure will exceed $600 billion in 2026 — a 36% increase over 2025 — with roughly 75% tied directly to AI infrastructure. Alphabet alone plans $175–185 billion in 2026 capex, more than doubling its 2025 spend. Total global AI spending is projected to hit $2 trillion in 2026. The capital is flowing. The question is what it buys.

The productivity evidence is less impressive than the investment figures. AI’s measurable impact on total factor productivity remains approximately 0.01 percentage points in 2025 — functionally invisible in macroeconomic data. Only ~6% of enterprises report AI-driven EBIT impact of 5% or more. The OECD’s 2023 data shows the US recorded 1.6% labor productivity growth while the euro area fell −0.9%, the steepest drop since 2009. Average OECD productivity sits at roughly $70 per hour worked.

The strategic question isn’t whether AI can generate outputs. It’s whether organizations can convert capability into sustained productivity growth without widening the distributional strain that already separates a US Gini of 0.394 from Germany’s 0.309. Capital deepening without governance deepening creates fragility. Investment without diffusion creates concentration. And concentration without distribution management creates political risk that eventually constrains the investment itself.

| Metric | Value |

|---|---|

| Hyperscaler capex (2026 forecast) | >$600 billion |

| AI share of hyperscaler capex | ~75% ($450B) |

| Alphabet 2026 capex plan | $175–185 billion |

| Total global AI spending (2026 est.) | $2 trillion |

| Capital intensity (% of revenue) | 45–57% |

| OECD avg productivity (2023) | ~$70/hour worked |

| US labor productivity growth (2023) | +1.6% |

| Euro area productivity growth (2023) | −0.9% |

| AI TFP impact (2025, Penn Wharton) | 0.01 pp |

| Firms reporting 5%+ AI EBIT impact | ~6% |

| US Gini (disposable income, 2023) | 0.394 |

| Germany Gini (2022) | 0.309 |

Plaud Note Pro AI Voice Recorder Transcribe & Summarize for Meetings Calls

- High-Accuracy Transcription: Supports 112 languages with speaker labels

- Instant Structured Summaries: Creates mind maps, To-Do lists, proposals

- Multimodal Input Capture: Record audio, add images, type notes

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

1. Productivity Upside Exists, but Diffusion Is the Bottleneck

The productivity data tells two stories simultaneously. At the individual level, professionals using AI tools become approximately 26% more productive within weeks. Workers with AI skills command a 56% wage premium, up from 25% the prior year. The share of firms using AI rose from 20% in 2017 to 78% in 2025. By December 2025, 35.9% of workers reported using generative AI tools.

At the macroeconomic level, almost none of this shows up yet. Penn Wharton’s projected AI impact on total factor productivity growth: 0.01 percentage points in 2025. The OECD Compendium of Productivity Indicators 2025 documents a widening gap between the US and the euro area — 1.6% growth versus −0.9% — but attributes this to structural factors, not AI diffusion.

The Frontier-Median Gap

| Metric | Frontier (95th %ile) | Median | Gap |

|---|---|---|---|

| AI message volume per worker | 6× median | Baseline | 6:1 |

| AI messages per seat (firms) | 2× median | Baseline | 2:1 |

| EBIT impact ≥5% from AI | ~6% of firms | Unmeasurable for most | Concentration |

| AI adoption (firms, 2025) | 78% using AI | But depth varies radically | Adoption ≠ impact |

| Worker AI tool usage (Dec 2025) | 35.9% | Concentrated: young, educated, higher-earning | Skewed |

The pattern is familiar from every major technology wave: early adopters capture disproportionate gains while the median firm achieves “measurable ROI with some efficiency gains” that “don’t add up to transformation.” This isn’t a technology problem. It’s a diffusion problem — and diffusion stalls when organizations fail at the complementary changes that actually convert AI spend into productivity lift.

What Diffusion Requires

| Complementary Change | Why It Matters | Who Typically Fails |

|---|---|---|

| Process simplification | AI automates complexity; it doesn’t eliminate it | Orgs that layer AI onto broken processes |

| Data governance modernization | Models need clean, accessible, governed data | Orgs with siloed, undocumented data estates |

| Decision-rights redesign | Who approves what when AI recommends? | Orgs that haven’t updated authority structures |

| Capability-building (managers) | Frontline leaders must manage human-AI work | Orgs that train only technical staff |

AI spend alone does not create productivity lift. Organizational rewiring does. And organizational rewiring is slow, expensive, and politically difficult — which is why the productivity data lags the investment data by years, not months.

“The gap between AI investment and AI productivity isn’t a technology lag. It’s an organizational design debt that most firms haven’t started repaying.”

The AI Prompt Playbook: Master AI Prompt Engineering with 140 Ready-to-Use Templates for ChatGPT, Claude, Gemini & Copilot

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

2. Capital Deepening Without Governance Deepening Creates Fragility

The scale of AI infrastructure investment in 2026 is historically unprecedented. Hyperscaler capital intensity now reaches 45–57% of revenue — levels that would have been unthinkable five years ago. The Big Five (Amazon, Alphabet, Microsoft, Meta, Oracle) are increasingly using debt markets to bridge the gap between rising capex and internal free cash flow, transforming historically cash-funded models into leveraged ones.

The Investment Concentration

| Company | 2026 Capex (Est.) | vs. 2025 | Primary Allocation |

|---|---|---|---|

| Alphabet | $175–185B | >2× ($91.4B) | Data centers, TPUs, AI infrastructure |

| Meta | $115–135B | ~2× ($72.2B) | AI compute, data centers |

| Amazon | ~$146.6B | +18% ($124.5B) | AWS, AI infrastructure |

| Microsoft | ~$80B+ | Continued increase | Azure AI, data centers |

| Total Big Five | >$600B | +36% over 2025 | 75% AI-specific |

This is capital deepening at a pace that has no modern precedent in technology markets. But capital deepening without governance deepening creates two distinct risks:

Risk 1: False Productivity

Higher activity throughput does not equal better outcomes. Organizations that measure AI productivity by volume — queries processed, documents generated, tickets resolved — may be generating more output with degraded quality, trust, or compliance outcomes. The insurance market is beginning to price this: AI governance evidence is increasingly required for coverage, and “we automated it” is not the same as “we governed it.”

Risk 2: Value Capture Asymmetry

Gains from AI infrastructure investment accrue disproportionately to infrastructure owners, platform operators, and early-adopting firms. Labor, consumers, and the broader economy absorb transition costs. This isn’t speculation — it’s the pattern that PwC’s 56% wage premium data already demonstrates. The workers who know how to use AI tools capture outsized compensation. The workers who don’t face stagnation or displacement.

Morningstar’s 2026 analysis frames this as an “AI arms race” reshaping investment landscapes. The Atlantic Council identifies geopolitical fragmentation forcing multinationals to operate separate AI stacks across regions — adding governance complexity that most capital plans don’t budget for.

“$600 billion in AI infrastructure investment is a bet on capability. Whether it becomes a bet on productivity depends entirely on the governance, process, and human-capital investments that don’t appear in the capex line.”

Capital deepening creates potential. Governance deepening converts it into value. Most organizations are investing heavily in the first and underinvesting catastrophically in the second.

![Claude AI for Beginners Bible: [5 in 1] The Ultimate Guide to Automate Your Work, Save Hours Every Week, and Use AI for Real-World Results](https://m.media-amazon.com/images/I/415+fSJacsL._SL500_.jpg)

Claude AI for Beginners Bible: [5 in 1] The Ultimate Guide to Automate Your Work, Save Hours Every Week, and Use AI for Real-World Results

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

3. Distribution Mismatch as a First-Order Business Risk

Using OECD inequality data as directional anchors — US Gini at 0.394 versus Germany at 0.309 — leaders should assume fundamentally different political and market responses to AI-led restructuring in different contexts.

How Distribution Baselines Shape AI Response

| Context | Gini Range | Political Response to AI Restructuring | Corporate Risk |

|---|---|---|---|

| Low inequality (Nordics) | 0.25–0.28 | High trust; transition programs funded | Lower; social compact holds |

| Moderate inequality (Germany) | 0.30–0.32 | Structured negotiation; works councils | Moderate; predictable |

| High inequality (US, UK) | 0.35–0.40 | Populist backlash; regulatory volatility | High; narrative risk |

| Very high inequality (emerging) | 0.40+ | Instability risk; unpredictable policy | Very high; operational |

The distribution mismatch problem is straightforward: AI gains concentrate before they diffuse, and the political tolerance for concentration depends on the starting distribution. A market where the top decile already captures a disproportionate share has structurally less capacity to absorb another round of technology-driven concentration without backlash.

CEO Sentiment Shift

The EY CEO Confidence Index reveals a notable correction: the proportion of CEOs expecting AI to reduce headcount dropped from 46% in January 2025 to 24% in December 2025. Meanwhile, 69% of CEOs now believe AI investments will maintain or grow employment. This is either a genuine recalibration or a public-positioning adjustment in response to reputational risk. Either way, it signals that the “efficiency through elimination” narrative has become politically costly.

For Multinationals: One Global Labor Narrative Will Fail

A company announcing the same AI-driven restructuring in Stockholm, Stuttgart, and St. Louis will face three different reactions. The Gini differential isn’t an abstraction — it determines the political surface area of your AI deployment. Workforce and social compacts need country-specific calibration, not global templates.

“Distribution isn’t an externality anymore. It’s a constraint that determines whether your AI investment generates returns or generates regulation.”

The Enterprise Integration Architect Designing Secure, Resilient, and AI-Ready Digital Platforms

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

4. Why “Post-Labor” Needs Measurement Architecture Now

Many post-labor discussions remain conceptual — interesting in seminars, useless in board rooms. The gap between post-labor theory and post-labor governance is a measurement gap. Boards can’t manage what they can’t measure, and most organizations can’t measure the distributional dynamics of their own AI deployments.

The Measurement Spine

| Construct | What to Measure | Current State |

|---|---|---|

| Autonomous value share | % of value created by autonomous vs. human-supervised systems | Most firms can’t distinguish |

| Productivity gain distribution | How gains split across wages, prices, margins, tax base | Rarely tracked beyond P&L |

| Retraining access by cohort | Which workers get transition pathways, by demographics | Ad hoc where it exists |

| Non-market value impacts | Public service quality, access, equity effects | Almost never measured |

| Exception-management capacity | Human oversight capacity relative to automation scope | Not a standard metric |

Without this measurement spine, post-labor strategy becomes ideology rather than management. A board that approves an AI transformation without knowing how productivity gains distribute across stakeholders is making a bet without understanding the odds.

The Policy Infrastructure Gap

The US has proposed an AI Workforce Research Hub for scenario planning and recurring analysis. Congress has the Investing in American Workers Act — a 20% tax credit for increases in qualified training spending. These are directional. They are not operational. The gap between policy proposals and functional transition infrastructure remains vast.

The WEF’s January 2026 analysis puts it starkly: AI’s $15 trillion prize will be won by learning, not just technology. But “learning” at the scale required — 59% of the global workforce needing reskilling by 2030 — demands institutional infrastructure that doesn’t exist in most countries.

The organizations that build measurement architecture now will have strategic options that those relying on conceptual frameworks won’t. When regulators ask “who benefited from your AI deployment?” — and they will — the measured answer beats the narrative one.

5. Strategic Portfolio: Where to Place Bets in 2026

Not all AI investments carry the same confidence level. The distinction between high-confidence productivity gains and speculative transformation claims is the difference between capital allocation and capital speculation.

The Confidence Matrix

| Confidence Level | Investment Area | Evidence Base | Expected Payback |

|---|---|---|---|

| High | Process reliability / downtime reduction | Operational data; measurable before-after | 6–18 months |

| High | Compliance automation (repetitive, control-heavy) | Regulatory requirements create clear scope | 12–24 months |

| High | Human-AI teaming in diagnostics/monitoring | Clinical, industrial, and IT evidence | 12–24 months |

| Medium | Multi-agent orchestration across BUs | Growing (1,445% inquiry surge); limited production data | 18–36 months |

| Medium | Autonomous optimization (procurement/logistics) | Constrained environments show results | 18–36 months |

| Low / high-uncertainty | Broad autonomous strategic planning | Minimal evidence; high complexity | Unknown |

| Low / high-uncertainty | Rapid institutional knowledge replacement | No transition architecture = failure mode | High risk |

The multi-agent AI market is projected to reach $11.78 billion in 2026, growing to $251.38 billion by 2034. Gartner reports a 1,445% surge in multi-agent system inquiries from Q1 2024 to Q2 2025. Deloitte projects the autonomous agent market at $8.5 billion by 2026, potentially $35–45 billion by 2030 with better orchestration.

But market size projections are not evidence of operational readiness. The gap between inquiry volume and production deployment is the space where most AI investment risk lives.

“The high-confidence bets are boring. The low-confidence bets are exciting. Boards that can’t tell the difference will discover the distinction in their write-off schedule.”

6. Practical Implications and Actions

For Enterprise Leaders

1. Treat productivity and distribution as a coupled system. Require board-level review of both in every AI business case. A productivity gain that concentrates in the top quintile while externalizing transition costs is not a net gain — it’s a deferred liability.

2. Implement gain-sharing principles early. Link a defined share of AI productivity gains to workforce transition and capability investment. The 56% wage premium for AI-skilled workers is an opportunity to fund transition — if the gain-sharing mechanism exists.

3. Use scenario planning with inequality sensitivity. Run separate operating plans for high- and low-inequality contexts. The same AI deployment requires different workforce communication, transition investment, and public engagement in markets with different Gini baselines.

4. Classify AI investments by confidence level. Separate high-confidence operational improvements from speculative transformation bets. Allocate governance resources accordingly — the speculative bets need more oversight, not less.

5. Set an evidence threshold for scaling. No scale decision based solely on vendor benchmarks. Require internal causal evidence that the AI deployment produces the claimed productivity effect in your operating environment.

For Public-Sector Leaders

6. Build public-value KPIs in social-mandate sectors. Health, education, and administrative justice require quality-access metrics, not just cost metrics. AI that reduces cost while degrading access is a net negative for public institutions.

7. Require distributional impact assessment for major AI procurements. Who benefits, who bears transition costs, and what measurement confirms both. Make this a procurement requirement, not a policy aspiration.

8. Fund transition infrastructure at the scale of the investment. If AI capex is hitting $600 billion globally, transition investment should be proportionate — not the afterthought it currently is.

For Boards and Investors

9. Ask about governance depth, not just capital depth. The capital-to-governance ratio in most AI investments is dangerously skewed. Organizations spending billions on infrastructure and millions on governance are building on a foundation designed to fail.

10. Explicitly classify uncertain trend claims. Mark where forecasts rely on sparse evidence or advocacy-driven sources. The difference between “$2 trillion in AI spending” (measurable) and “$15 trillion in AI value” (projected) is the difference between a fact and a hope.

What to Watch Next

- Evidence of real diffusion: productivity gains at median firms, not only digital leaders

- Policy moves tying AI deployment to social contribution or transition obligations

- Market differentiation between “automation at any cost” firms and “resilient transition” firms

- Hyperscaler debt levels as capex-to-cash-flow gaps widen

- Whether the 6% of firms with measurable AI EBIT impact becomes 15% or stays at 6%

- Regulatory responses to AI-driven value concentration in high-inequality markets

The Bottom Line

Six hundred billion dollars in hyperscaler capex. Two trillion dollars in global AI spending. And a productivity impact that, at the macroeconomic level, rounds to zero. The investment thesis is clear. The productivity thesis is not.

The gap between capital deployed and value captured isn’t a timing issue — it’s a design issue. Organizations that treat AI as an infrastructure problem will get infrastructure. Organizations that treat it as a productivity problem will invest in the complementary changes — process redesign, data governance, decision-rights restructuring, capability-building — that actually convert capability into outcomes.

The distribution dimension makes this harder. A US Gini of 0.394 means every productivity gain lands in a political environment where concentration is already contested. Ignoring distribution doesn’t make it irrelevant — it makes it someone else’s problem until it becomes yours.

The new productivity equation isn’t AI investment = productivity gain. It’s AI investment × organizational readiness × governance depth ÷ distributional strain = sustainable value. Most organizations are solving for one variable and ignoring the other three.

Capital without governance is speculation. Productivity without distribution is instability. And instability, eventually, reprices everything.

Thorsten Meyer is an AI strategy advisor who reads hyperscaler earnings calls and OECD productivity reports with equal enthusiasm — and equal skepticism. More at ThorstenMeyerAI.com.

Sources:

- IEEE ComSoc — Hyperscaler Capex >$600B in 2026 (December 2025)

- Goldman Sachs — Why AI Companies May Invest >$500B in 2026 (2026)

- CNBC — Alphabet Resets the Bar for AI Infrastructure Spending (February 2026)

- Introl — Hyperscaler CapEx Hits $600B: The AI Infrastructure Debt Wave (January 2026)

- OECD — Compendium of Productivity Indicators 2025 (June 2025)

- OECD — Tracking Productivity Trends Amid Economic Headwinds (September 2025)

- Penn Wharton Budget Model — Projected Impact of GenAI on Productivity Growth (September 2025)

- OpenAI — The State of Enterprise AI 2025 Report (2025)

- McKinsey — The State of AI in 2025 (2025)

- St. Louis Fed — State of Generative AI Adoption in 2025 (November 2025)

- PwC — Global AI Jobs Barometer 2025 (2025)

- WEF — AI’s $15 Trillion Prize: Won by Learning (January 2026)

- Deloitte — Unlocking Exponential Value with AI Agent Orchestration (2026)

- Gartner — 40% of Enterprise Apps to Feature AI Agents by 2026 (August 2025)

- Fortune Business Insights — AI Agents Market Size and Forecast (2026)

- Morningstar — AI Arms Race: How Tech’s Capital Surge Reshapes Investment (2026)

- Atlantic Council — Eight Ways AI Will Shape Geopolitics in 2026 (2026)

- EY — CEO Confidence Index (January 2026)

- OECD — Income Inequality Indicators / Gini Coefficients (2024)

- OECD — Policy Approaches to Reduce Inequalities While Boosting Productivity (2024)