By Thorsten Meyer — April 2026

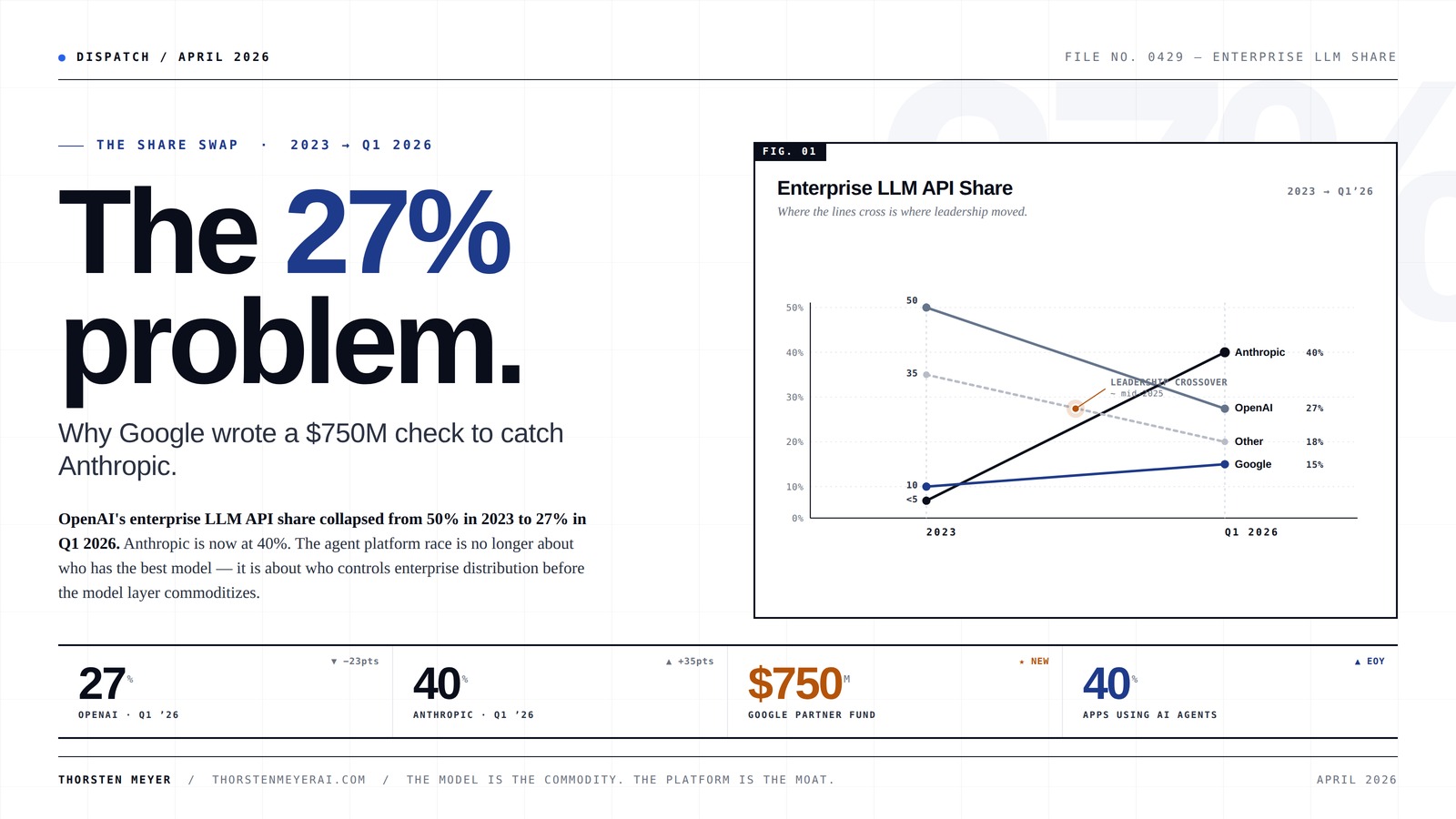

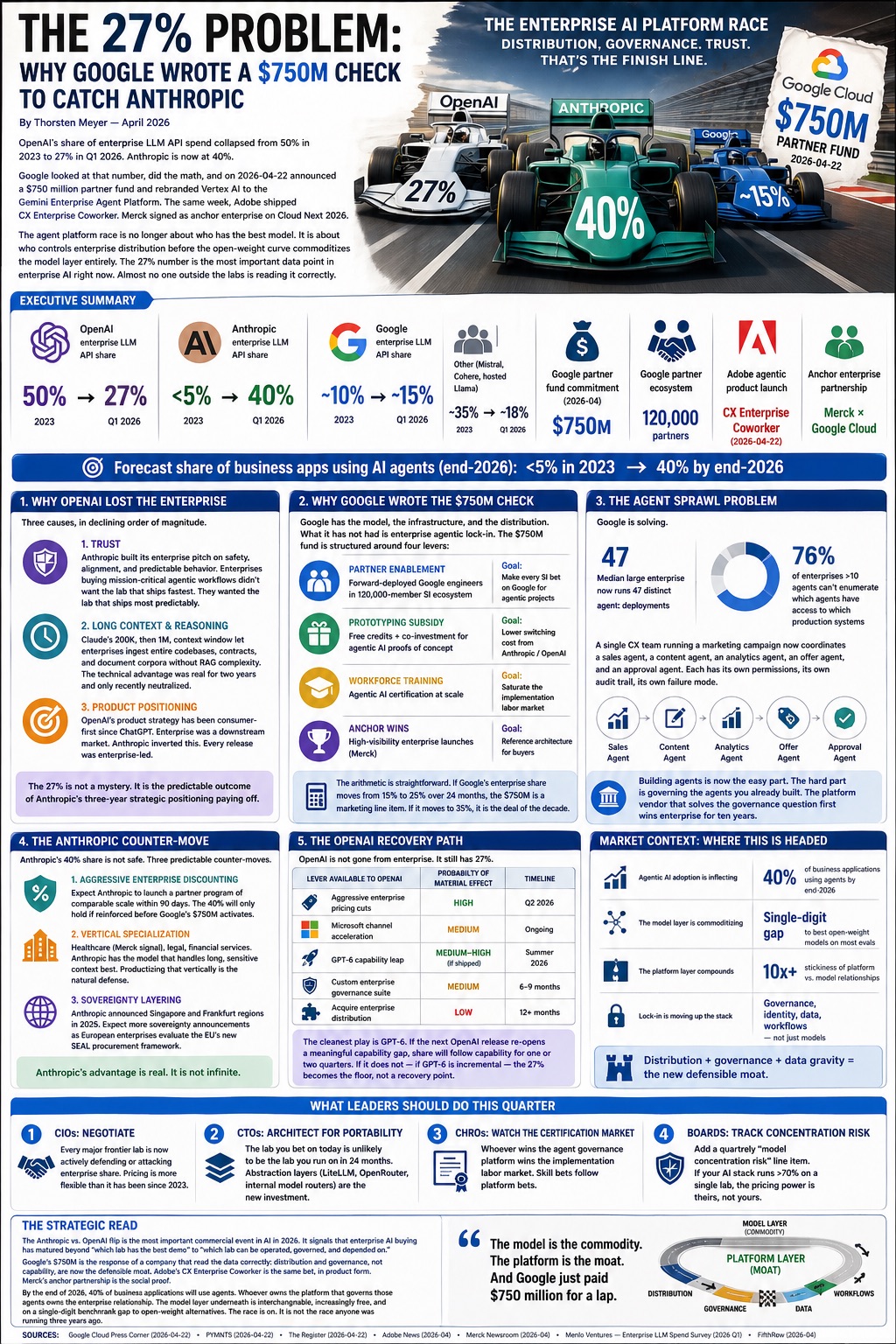

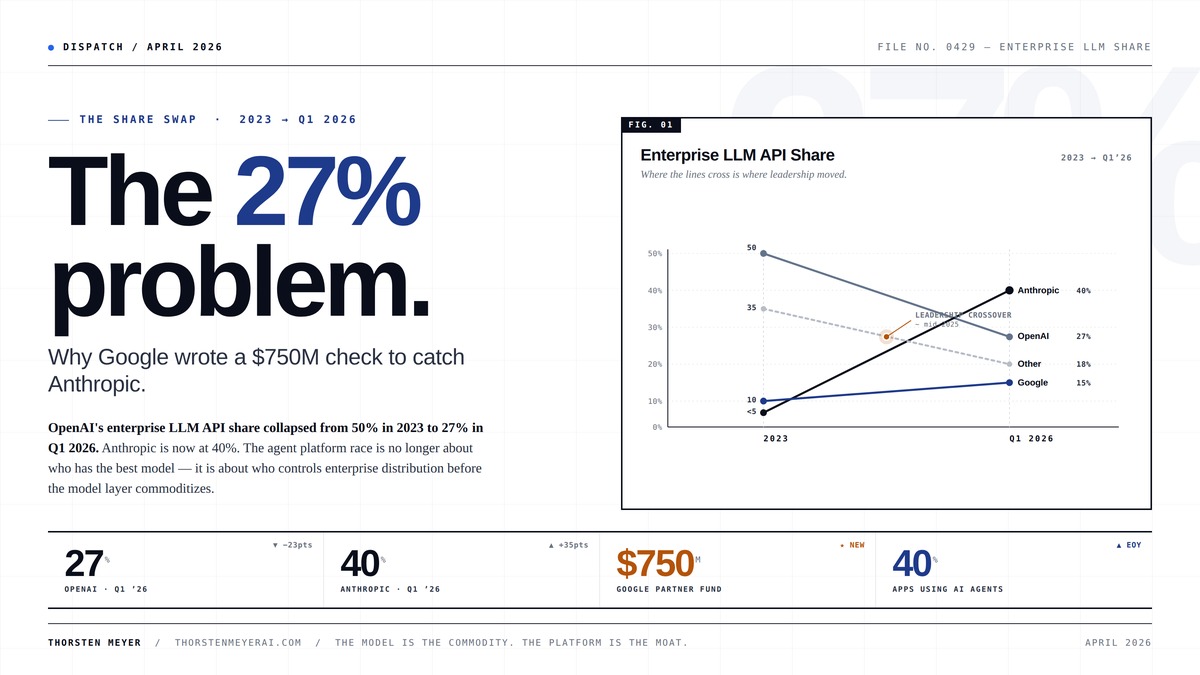

OpenAI’s share of enterprise LLM API spend collapsed from 50% in 2023 to 27% in Q1 2026. Anthropic is now at 40%.

Google looked at that number, did the math, and on 2026-04-22 announced a $750 million partner fund and rebranded Vertex AI to the Gemini Enterprise Agent Platform. The same week, Adobe shipped CX Enterprise Coworker. Merck signed as anchor enterprise on Cloud Next 2026.

The agent platform race is no longer about who has the best model. It is about who controls enterprise distribution before the open-weight curve commoditizes the model layer entirely.

The 27% problem.

Why Google wrote a $750M check to catch Anthropic.

OpenAI’s share of enterprise LLM API spend collapsed from 50% in 2023 to 27% in Q1 2026. Anthropic is now at 40%. Google looked at that number, did the math, and on 2026-04-22 announced a $750 million partner fund and rebranded Vertex AI to the Gemini Enterprise Agent Platform. The agent platform race is no longer about who has the best model. It is about who controls enterprise distribution before the model layer commoditizes entirely.

Three years. The lead has moved twice.

Each line is an enterprise LLM API vendor. The slope is the share trajectory from 2023 to Q1 2026. Where the lines cross is where leadership moved.

Designing Large Language Model Applications: A Holistic Approach to LLMs

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three causes, in declining order of magnitude.

The lab that ships most predictably.

Anthropic’s pitch was safety, alignment, and predictable behavior. Enterprises buying mission-critical agentic workflows did not want the lab that ships fastest. The preference compounded across renewal cycles.

200K, then 1M tokens — without RAG.

Claude let enterprises ingest entire codebases, contracts, and document corpora without retrieval-pipeline complexity. The technical advantage was real for two years and only recently neutralized.

Enterprise-led every release.

OpenAI’s product strategy has been consumer-first since ChatGPT. Enterprise was the downstream market. Anthropic inverted this — and the inversion paid out.

Google ADK and Gemini Enterprise Agent Platform: Build, Deploy, Govern, and Scale Production-Ready AI Agents for Enterprise Workflows

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

If 15% becomes 25%, this is a marketing line item. If it becomes 35%, it is the deal of the decade.

Google’s fund is structured around four mechanisms. Each one targets a different bottleneck in enterprise agentic adoption.

Forward-deployed engineers, embedded.

Google engineers placed inside the 120,000-member system-integrator ecosystem.

Free credits + co-investment for PoCs.

Buyers test agentic workloads on Gemini before committing budget — at low or no cost.

Agentic AI certification at scale.

Programs that flood the implementation labor market with Google-trained talent.

High-visibility enterprise launches.

Merck × Google Cloud, signed at Cloud Next 2026, becomes the regulated-industry reference architecture.

The model is the commodity. The platform is the moat. And Google just paid $750 million for a lap.

Generative AI for Software Development: Building Software Faster and More Effectively

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Anthropic has 40%. OpenAI has 27%. Both are now playing for Q3.

Three predictable counter-moves.

Aggressive enterprise discounting.

Match Google’s $750M with a partner program of comparable scale within 90 days — or watch the 40% erode before defenders activate.

Vertical specialization.

Healthcare (the Merck signal), legal, financial services. The model that handles long sensitive context best is a vertical product waiting to be packaged.

Sovereignty layering.

Singapore + Frankfurt regions in 2025. Expect more under the EU’s new SEAL procurement framework.

Five levers · one cleanest play.

Aggressive pricing cuts.

Highest-probability lever, immediately deployable. Defend the 27% floor while waiting on capability.

GPT-6 capability leap.

The cleanest play. If GPT-6 re-opens a meaningful gap, share follows capability for one or two quarters. If it is incremental, 27% becomes the floor.

Custom enterprise governance suite.

The agent-sprawl problem is the moat. OpenAI is late but not absent — a credible governance product still has time.

Platform Engineering for Artificial Intelligence: Designing scalable infrastructure, data pipelines, and model lifecycle management for generative AI and agentic protocols (English Edition)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Negotiate. Now.

Every major frontier lab is actively defending or attacking enterprise share. Pricing is more flexible than at any time since 2023. Renewals signed this quarter will be cheaper than renewals signed in Q3.

Architect for portability.

The lab you bet on today is unlikely to be the lab you run on in 24 months. Abstraction layers — LiteLLM, OpenRouter, internal model routers — are the new investment, not optional infrastructure.

Watch the certification market.

Whoever wins the agent governance platform wins the implementation labor market. Skill bets follow platform bets — usually with a 12-month lag.

Quarterly: model concentration risk.

If your AI stack runs >70% on a single lab, you have lock-in. The pricing power is theirs, not yours. Add the line item to the quarterly review or wait for it to surface during a 2027 renewal you cannot escape.

The 27% number is the most important data point in enterprise AI right now. Almost no one outside the labs is reading it correctly.

Executive Summary

| Metric | 2023 | Q1 2026 |

|---|---|---|

| OpenAI enterprise LLM API share | 50% | 27% |

| Anthropic enterprise LLM API share | <5% | 40% |

| Google enterprise LLM API share | ~10% | ~15% |

| Other (Mistral, Cohere, hosted Llama) | ~35% | ~18% |

| Google partner fund commitment (2026-04) | — | $750M |

| Google partner ecosystem | — | 120,000 partners |

| Adobe agentic product launch | — | CX Enterprise Coworker (2026-04-22) |

| Anchor enterprise partnership | — | Merck × Google Cloud |

| Forecast share of business apps using AI agents (end-2026) | <5% | 40% |

The lead in enterprise has moved twice in three years. It is now Anthropic’s to lose. Google has just declared that it is no longer willing to lose it.

1. Why OpenAI Lost the Enterprise

OpenAI’s drop from 50% to 27% has three causes, in declining order of magnitude.

Cause 1: Trust. Anthropic built its enterprise pitch on safety, alignment, and predictable behavior. Enterprises buying mission-critical agentic workflows did not want the lab that ships fastest. They wanted the lab that ships most predictably. That preference compounded across renewal cycles.

Cause 2: Long context and reasoning. Claude’s 200K, then 1M, context window let enterprises ingest entire codebases, contracts, and document corpora without RAG complexity. The technical advantage was real for two years and only recently neutralized.

Cause 3: Product positioning. OpenAI’s product strategy has been consumer-first since ChatGPT. Enterprise was a downstream market. Anthropic inverted this. Every release was enterprise-led.

The 27% is not a mystery. It is the predictable outcome of Anthropic’s three-year strategic positioning paying off.

2. Why Google Wrote the $750M Check

Google has the model (Gemini 2.5+), the infrastructure (TPU v6), and the distribution (Workspace, Cloud, Android). What it has not had is enterprise agentic lock-in. The April 22 announcement is an attempt to fix that in one quarter.

The $750M fund is structured around four levers:

| Lever | Mechanism | Strategic Goal |

|---|---|---|

| Partner enablement | Forward-deployed Google engineers embedded in 120,000-member SI ecosystem | Make every system integrator bet on Google for agentic projects |

| Prototyping subsidy | Free credits + co-investment for agentic AI proofs of concept | Lower switching cost from Anthropic / OpenAI |

| Workforce training | Agentic AI certification at scale | Saturate the implementation labor market with Google-trained talent |

| Anchor wins | High-visibility enterprise launches (Merck) | Reference architecture for buyers |

The arithmetic is straightforward. If Google’s enterprise share moves from 15% to 25% over 24 months, the $750M is a marketing line item. If it moves to 35%, it is the deal of the decade.

Anthropic has 40% share and a five-year head start. Google is betting that distribution beats accumulation.

3. The Agent Sprawl Problem Google Is Solving

The Gemini Enterprise Agent Platform (the rebranded Vertex AI) is not a new product. It is a new framing: the central control plane for organizations now running not one agent, but hundreds.

Adobe’s CX Enterprise Coworker, announced the same week, illustrates the problem. A single CX team running a marketing campaign now coordinates a sales agent, a content agent, an analytics agent, an offer agent, and an approval agent. Each has its own permissions, its own audit trail, its own failure mode.

Median large enterprise now runs 47 distinct agent deployments. Median enterprise running >10 agents reports they cannot enumerate which agents have access to which production systems.

The platform race is, fundamentally, the race to be the one place where this sprawl is governed.

“Building agents is now the easy part. The hard part is governing the agents you already built. The platform vendor that solves the governance question first wins enterprise for ten years.”

4. The Anthropic Counter-Move

Anthropic’s 40% share is not safe. Three predictable counter-moves are coming.

Counter-move 1: Aggressive enterprise discounting. Expect Anthropic to launch a partner program of comparable scale within 90 days. The 40% will only hold if reinforced before Google’s $750M activates.

Counter-move 2: Vertical specialization. Healthcare (Merck signal), legal, financial services. Anthropic has the model that handles long, sensitive context best. Productizing that vertically is the natural defense.

Counter-move 3: Sovereignty layering. Anthropic announced Singapore and Frankfurt regions in 2025. Expect more sovereignty announcements as European enterprises evaluate the EU’s new SEAL procurement framework.

Anthropic’s advantage is real. It is not infinite.

5. The OpenAI Recovery Path

OpenAI is not gone from enterprise. It still has 27% — a substantial book — and a brand that consumers know best. But the pivot required is structural.

| Lever Available to OpenAI | Probability of Material Effect | Timeline |

|---|---|---|

| Aggressive enterprise pricing cuts | High | Q2 2026 |

| Microsoft channel acceleration | Medium | Ongoing |

| GPT-6 capability leap | Medium-High if shipped | Summer 2026 |

| Custom enterprise governance suite | Medium | 6–9 months |

| Acquire enterprise distribution | Low | 12+ months |

The cleanest play is GPT-6. If the next OpenAI release re-opens a meaningful capability gap, share will follow capability for one or two quarters. If it does not — if GPT-6 is incremental — the 27% becomes the floor, not a recovery point.

What Leaders Should Do This Quarter

1. CIOs: Negotiate. Every major frontier lab is now actively defending or attacking enterprise share. Pricing is more flexible than it has been since 2023.

2. CTOs: Architect for portability. The lab you bet on today is unlikely to be the lab you run on in 24 months. Abstraction layers (LiteLLM, OpenRouter, internal model routers) are the new investment.

3. CHROs: Watch the certification market. Whoever wins the agent governance platform wins the implementation labor market. Skill bets follow platform bets.

4. Boards: Add a quarterly “model concentration risk” line item. If your AI stack runs >70% on a single lab, you have lock-in. The pricing power is theirs, not yours.

The Strategic Read

The Anthropic vs. OpenAI flip is the most important commercial event in AI in 2026. It signals that enterprise AI buying has matured beyond “which lab has the best demo” to “which lab can be operated, governed, and depended on.”

Google’s $750M is the response of a company that read the data correctly: distribution and governance, not capability, are now the defensible moat. Adobe’s CX Enterprise Coworker is the same bet, in product form. Merck’s anchor partnership is the social proof.

By the end of 2026, 40% of business applications will use agents. Whoever owns the platform that governs those agents owns the enterprise relationship. The model layer underneath is interchangeable, increasingly free, and on a single-digit benchmark gap to open-weight alternatives.

The race is on. It is not the race anyone was running three years ago.

The model is the commodity. The platform is the moat. And Google just paid $750 million for a lap.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Sources

- Google Cloud Press Corner, Google Cloud Commits $750M to Accelerate Partners’ Agentic AI Development (2026-04-22)

- PYMNTS, Google Accelerates Agentic AI Shift With New Enterprise Platform (2026-04-22)

- The Register, Google says it has all the answers for AI agent sprawl (2026-04-22)

- Adobe News, Adobe Unveils CX Enterprise Coworker (2026-04)

- Merck Newsroom, Merck and Google Cloud Partner to Accelerate Agentic AI Enterprise Transformation (2026-04)

- Menlo Ventures, Enterprise LLM Spend Survey (2026 Q1)

- FifthRow, AI Agent Orchestration Goes Enterprise: The April 2026 Playbook (2026-04)