Part 6 of a five-day series on the 2026 memory crunch. Part 5 followed the tax onto the workbench; this one follows it into the place most people assume is safe.

If you’ve watched RAM and SSD prices double and thought good thing I’m in the cloud — I don’t buy the memory, I rent it, this one’s for you. The logic feels airtight. It isn’t. You’re still paying for every gigabyte of that DRAM; you’ve just stopped being able to see the bill.

The memory squeeze reaches the cloud through a cost cascade as reliable as gravity — and the cloud’s particular cruelty is that it arrives disguised. There’s no line item that says “memory surcharge.” There’s just a number that creeps, on instances you’ve run for years, for reasons your invoice never explains.

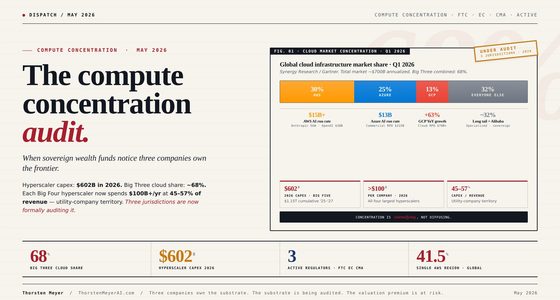

Cloud’s hidden memory bill

Thought the cloud lets you dodge the squeeze — you rent the RAM, you don’t buy it? You’re still paying for every gigabyte. You’ve just stopped being able to see the bill.

No escape from the shortage anywhere — on-prem servers also cost +15–25%. But providers hedge scarce hardware better than you can, and you can’t buy half a cluster for two weeks.

8×H200 ≈ $15–20/hr owned (3-yr amortized) vs $39.80 rented — roughly half. 83% of CIOs plan to repatriate some workloads. Hybrid is the new default.

The cloud doesn’t make the memory tax disappear — it launders it, turning a violent fab shortage into a few innocuous percentage points scattered across a bill you can’t easily audit. “I’m in the cloud, I’m safe” is the most expensive misconception in this series. Refuse to pay for idle RAM, sort each workload to its cheapest venue, and lock pricing before the Q2–Q3 adjustment. The escape hatch was never cloud-vs-on-prem — it’s discipline-vs-drift. Next: the local-inference rig.

The cascade nobody itemizes

The path from a fab in Korea to your monthly bill has four steps, and each one passes the cost down.

It starts where the whole series started: the wafer, where Samsung, SK Hynix, and Micron raised server DRAM prices on the order of 60–70% versus late 2025. That flows into OEM servers — Dell, Lenovo, and HP, who build the machines the cloud runs on, and who announced server price increases of 15–25%, with Dell adding another 17% in March 2026. Those servers become the cloud providers’ infrastructure cost. And that, finally, becomes your instance price.

The math is worth internalizing because it explains why the increase looks small while being anything but. Memory is roughly 20–30% of a server’s bill of materials. So even a brutal 60–200% jump in DRAM, diluted across CPUs, storage, networking, and chassis that didn’t spike, works out to a 15–25% rise in server cost — which providers, protecting their margins, pass through as roughly 5–10% on your bill. A modest-looking 7% increase on your invoice is a savage memory shortage, three layers of dilution later. It looks survivable precisely because the cascade hides its size.

Kingston Server Premier 32GB 3200MT/s DDR4 ECC CL22 DIMM 2Rx8 Hynix D Server Memory – KSM32ED8/32HD

Server Premier memory modules are designed to target the specific requirements of Data Centre & Cloud customers, System…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

AWS broke a twenty-year promise

For two decades, the cloud sold itself on a single, quiet assurance: prices only ever go down. Migrate, accept the lock-in, and your costs will fall over time. That assumption just died.

On January 4, 2026, AWS raised prices for the first time in its history — a roughly 15% hike on GPU capacity, with its eight-H200 instance jumping from $34.61 to $39.80 an hour. OVHcloud’s CEO became the only major provider to say the quiet part out loud, forecasting 5–10% increases between April and September 2026. AWS, Azure, and Google Cloud have otherwise stayed publicly silent — but they buy their servers from the same OEMs facing the same memory bills, and providers typically lag procurement by three to six months, which points every one of them at a Q2–Q3 2026 adjustment. As one prominent cloud-cost analyst observed, once the door to price increases is open, it doesn’t close again. The precedent is the story.

Gigastone 【NAS Certified】 1TB High Endurance SSD (2-Pack) Up to 550MB/s TLC Flash with SLC Caching 24/7 Reliable for Gaming/PC/NAS SSD 5-Year Warranty 2.5" SATA Internal Solid State Drives RAID Disk

[High Endurance Grade] : No.1 NAS SSD choice in heavy workloads NAS systems|24/7 superior NAS Cache with reliable…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why it’s hidden

Here’s what makes the cloud bill insidious rather than merely higher: it almost never appears as one honest, fightable charge.

Cloud price increases surface as gradual adjustments scattered across the bill — a few percent on this instance family, a quiet bump on that storage tier, a region that’s suddenly pricier, a free-tier allowance that shrank. The hit lands hardest on memory-optimized instances — AWS’s r-series, Azure’s E-series, GCP’s highmem — and on memory-hungry managed services like Redis, ElastiCache, and in-memory databases, which are mostly DRAM by cost and therefore most exposed. Compute-optimized instances rise more gently (3–7%); the memory-heavy ones lead.

And the trap most teams miss: your discounts don’t protect you. A reserved instance or enterprise discount is a fixed percentage, so when the underlying on-demand price rises, your absolute cost rises with it. A $100,000-a-month spend at a 15% discount was $85,000; after a hike it’s $115,000 list, $97,750 discounted — you’re paying $12,750 more for the identical workload, and the discount you negotiated did nothing to stop it. Reserved capacity bought at last year’s baseline can quietly become a worse deal than it looked, because the math of reserved-versus-on-demand shifts the moment the baseline moves.

A-Tech 256GB Kit (8x32GB) DDR4 2666MHz PC4-21300 ECC RDIMM 2Rx4 Dual Rank 1.2V ECC Registered DIMM 288-Pin Server & Workstation RAM Memory Upgrade Modules (A-Tech Enterprise Series)

A-Tech RAM Memory compatible for select DDR4 Servers & Workstation systems only; (*WILL NOT WORK with Desktop Computers,…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Renting isn’t the escape hatch — but neither is fleeing it

The tempting conclusion is to pull everything back on-premises. Resist the clean version of that, because the honest picture is more nuanced.

There is no escape from the shortage itself. Whether you run in AWS or your own data center, the servers cost 15–25% more — the tax is levied at the fab, and everyone downstream pays it. In fact, for elastic and unpredictable workloads, the cloud is still the right answer, and arguably a better one in a shortage: providers have the OEM relationships and the scale to secure scarce hardware that an individual buyer simply can’t, and you can’t buy half a GPU cluster for two weeks.

But the balance tips hard for steady, high-utilization work. Owning eight H200s runs roughly $240,000–$320,000 up front — about $15–20 per hour amortized over three years, against AWS’s post-hike $39.80. For a cluster you’ll run flat-out for years, owning is roughly half the cost of renting, and the shortage widened that gap by pushing the cloud price up. This is why 83% of CIOs report plans to repatriate at least some workloads — not a stampede out of the cloud (only a sliver plan a full exit), but a sober re-sorting of which workload belongs where. The emerging default isn’t cloud or on-prem; it’s hybrid: predictable baselines where ownership amortizes, bursts and experiments in the cloud where elasticity pays. For anyone running steady inference, that math is the whole argument for keeping it local — a thread Part 7 picks up directly.

Kingston Server Premier 8GB 3200MT/s DDR4 ECC Reg CL22 DIMM 1Rx8 Server Memory Hynix D Rambus – KSM32RS8/8HDR

Server Premier memory modules are designed to target the specific requirements of Data Centre & Cloud customers, System…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What to actually do

The shortage rewards exactly the discipline most teams defer:

- Audit your memory footprint — total the RAM across prod, staging, and dev, and separate what’s used from what’s merely provisioned. Idle RAM was a rounding error a year ago; now it’s the most expensive waste on your bill.

- Right-size aggressively — a 128GB instance using 40GB was always wasteful; in 2026 it’s bleeding money. This is the single highest-return lever you have.

- Lock pricing before the increases land — negotiate renewals and commit to Savings Plans or reserved terms before the Q2–Q3 2026 adjustments, not against a risen market.

- Match each workload to its cheapest venue — steady and high-utilization tends to favor owning; spiky and uncertain favors the cloud. Sorting this honestly is worth more than any single discount.

- Treat cost as continuous — the days of a quarterly review catching everything are over; a price change can land on a Saturday. FinOps monitoring exists because the bill now moves like a market.

The take

The cloud doesn’t make the memory tax disappear. It launders it — taking a violent shortage at the fab and metabolizing it into a few innocuous percentage points scattered across a bill you can’t easily audit, on instances you assumed were a fixed cost of doing business. The “I’m in the cloud, I’m safe” instinct is the most expensive misconception in this whole series, because it stops you from looking for a charge that’s absolutely there.

You can’t dodge the tax in any venue. What you can do is refuse to pay for idle RAM, sort your workloads to the cheapest place to run each, and lock your pricing before the next adjustment. The escape hatch was never cloud-versus-on-prem. It was discipline-versus-drift.

Which brings the series to the build that brought many of us into this in the first place. Next: The Real Cost of a Local-Inference Rig in 2026.

Sources: SoftwareSeni (cost-passthrough cascade, 20–30% memory share of server BOM, provider-lag timing); Hostkey and Worldstream (server DRAM increases, OVH forecast, memory-optimized instance exposure, right-sizing guidance); byteiota (AWS January 2026 GPU price hike, p5e.48xlarge pricing, repatriation and own-vs-rent economics); IDC (CIO repatriation survey). Figures reflect reporting as of late June 2026 and are fast-moving; prices are point-in-time. Analysis and recommendations are the author’s and not financial advice.