Thorsten Meyer | ThorstenMeyerAI.com | February 2026

Executive Summary

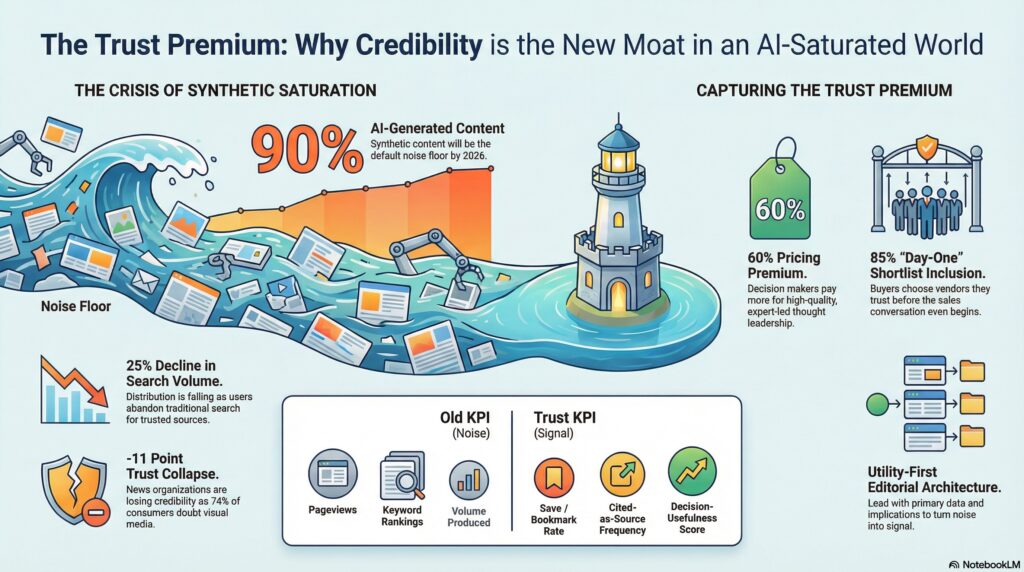

90% of online content will be AI-generated by 2026 (Gartner/Europol). 74% of new web pages already contain detectable AI content (Ahrefs, April 2025). Traditional search engine volume is dropping 25% (Gartner). And major news organizations just lost 11 net trust points (Edelman 2026).

The math is simple: content supply is exploding while trust is collapsing. The scarce asset is no longer distribution — it’s credibility. Organizations that treat content as a production problem will drown in the noise they helped create. Organizations that treat content as a trust architecture will own the attention that drives decisions.

This article is about the structural shift from content volume to content credibility — and the editorial operating model that captures the trust premium.

| Metric | Value |

|---|---|

| Online content AI-generated by 2026 (Gartner) | 90% |

| New web pages with AI content (Ahrefs, Apr 2025) | 74.2% |

| New articles primarily AI-written by late 2024 (Graphite) | 50%+ |

| Online content AI-generated/translated (AWS) | 57% |

| Search engine volume decline by 2026 (Gartner) | 25% |

| U.S. organic click-through rate (Mar 2025) | 40.3% (down from 44.2%) |

| No-click searches, U.S. (Mar 2025) | 27.2% (up from 24.4%) |

| Major news orgs: net trust change (Edelman 2026) | –11 points |

| Readers comfortable with AI-generated news | 12% |

| Americans wanting AI disclosure in news | 90% |

| Consumers doubting photos/videos from trusted outlets | 74% |

| Online deepfakes: 2023 vs. 2025 | ~500K → ~8 million |

| Deepfake annual growth rate | ~900% |

| Adults confident identifying deepfakes | 9% |

| B2B buyers choosing from day-one shortlist | 85% |

| Buyers selecting previously known brands | 78% (enterprise: 86%) |

| Decision-makers willing to pay premium for good thought leadership | ~60% |

| Hidden buyers: thought leadership more effective than marketing materials | 71% |

| Hidden buyers trusting thought leadership over product sheets | 64% |

| Thought leadership consumption: 1+ hour/week | 63% |

| Marketers: original research more valuable than AI content | 67% |

| B2B buying journey in dark funnel | 70% |

| Content pieces consumed before purchase decision | Up to 15 |

| B2B marketers using AI for content | 89% |

| Market saturation: top marketer concern (2026) | #1 |

| GenAI use growing: prevalence affecting trust (Edelman) | 37% cite it |

| Worried about foreign actors injecting falsehoods | 65% |

| Get news from ideologically different sources weekly | 39% |

Trust.: Responsible AI, Innovation, Privacy and Data Leadership

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

1. The Saturation Arithmetic

The numbers describe a structural break, not a trend. When 74% of new web pages contain AI-generated content and more than half of new English-language articles are primarily AI-written, the default state of published content is synthetic. The internet’s signal-to-noise ratio is inverting.

Volume Explosion

| Metric | Value | Source |

|---|---|---|

| Online content AI-generated by 2026 | 90% | Gartner/Europol |

| New web pages with AI content (Apr 2025) | 74.2% | Ahrefs |

| New articles primarily AI-written (late 2024) | 50%+ | Graphite |

| Online content AI-generated/translated | 57% | AWS |

| Active web page text from AI sources | 30–40% | Academic estimates |

| Online deepfakes (2023 → 2025) | ~500K → ~8M | Industry data |

| Deepfake annual growth | ~900% | Industry data |

This is not about AI being bad at writing. AI writes competent prose at scale. The problem is that competent prose at scale makes competent prose worthless. When everyone can produce B+ content instantly, B+ content becomes the noise floor.

Distribution Collapse

| Distribution Metric | Value |

|---|---|

| Search engine volume decline by 2026 (Gartner) | 25% |

| U.S. organic click-through (Mar 2025) | 40.3% (↓ from 44.2%) |

| EU/UK organic click-through (Mar 2025) | 43.5% (↓ from 47.1%) |

| No-click U.S. searches (Mar 2025) | 27.2% (↑ from 24.4%) |

| Clicks to Google-owned properties | 14.3% |

| B2B buying journey in dark funnel | 70% |

Search — the dominant content distribution mechanism for two decades — is fragmenting. Gartner predicts a 25% decline in traditional search volume by 2026 as AI chatbots and virtual agents become substitute answer engines. Organic click-through rates are already falling. No-click searches are rising. 70% of the B2B buying journey happens in the dark funnel before a vendor is contacted.

The implication: content that exists only to rank in search is losing its distribution advantage. Content that is sought by name — because the source is trusted — retains it.

![Express Schedule Free Employee Scheduling Software [PC/Mac Download]](https://m.media-amazon.com/images/I/41yvuCFIVfS._SL500_.jpg)

Express Schedule Free Employee Scheduling Software [PC/Mac Download]

- User-friendly drag & drop planning: Simple shift scheduling interface

- Manage time-off and holidays: Add sick leave, breaks, holidays

- Email schedules to staff: Send schedules directly via email

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

2. The Trust Collapse

Content saturation doesn’t just reduce attention. It degrades trust in the entire information ecosystem.

Institutional Trust Erosion

| Trust Metric | Value | Source |

|---|---|---|

| Major news orgs: net trust loss | –11 points | Edelman 2026 |

| Readers comfortable with AI-generated news | 12% | Media surveys |

| Americans demanding AI disclosure | 90% | Media surveys |

| Consumers doubting photos/videos from trusted outlets | 74% | Consumer research |

| Worried about foreign actors injecting falsehoods | 65% | Edelman 2026 |

| Get news from ideologically different sources weekly | 39% | Edelman 2026 |

| GenAI prevalence affecting institutional trust | 37% cite it | Edelman 2026 |

| Adults confident identifying deepfakes | 9% | iProov 2025 |

| Correct identification of all fakes (iProov test) | 0.1% | iProov 2025 |

The 2026 Edelman Trust Barometer captures a structural shift: trust is retreating from institutions into “closer and more homogeneous spaces.” Major news organizations lost 11 net trust points. Only 39% consume news from ideologically different sources weekly. 37% cite the growing use of generative AI platforms as a factor eroding trust.

The trust crisis is not about any single deepfake or misinformation campaign. It’s about the cumulative effect of an information environment where synthetic content is the default, detection is nearly impossible (0.1% correct identification rate), and audiences have adapted by trusting less broadly.

The Audience Response: Harder Filtering

Audiences are not passive receivers. They are filtering harder for:

| Filter | What Audiences Look For |

|---|---|

| Known editorial standards | Consistent quality track record, recognizable voice |

| Transparent sourcing | Primary data, named sources, linked evidence |

| Explicit uncertainty | Acknowledgment of what’s not known |

| Actionable framing | “So what?” answered clearly |

| Human attribution | Named authors with verifiable expertise |

Only 12% of readers are comfortable with AI-generated news. 90% want disclosure when AI creates content. 74% doubt photos or videos even from trusted outlets. The audience has internalized what the technology created: an environment where the default assumption is synthetic until proven otherwise.

Hidden Camera Detectors,GPS Tracker Detector and Bug Detection Device

- Multi-function Detection: Camera, GPS, and bug detection combined

- Wide Frequency Range: Detects signals from 1MHz to 6.5GHz

- Adjustable Sensitivity: Six levels for precise detection

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

3. The Trust Premium: What It Is and How It Works

The trust premium is the measurable advantage that credible content producers hold over volume content producers in attention, influence, and commercial outcomes.

Evidence of the Premium

| Trust Premium Indicator | Value | Source |

|---|---|---|

| Decision-makers willing to pay premium for good thought leadership | ~60% | Edelman-LinkedIn |

| Hidden buyers: thought leadership more effective than marketing | 71% | Edelman-LinkedIn 2025 |

| Hidden buyers trusting thought leadership over product sheets | 64% | Edelman-LinkedIn 2025 |

| Buyers choosing from day-one shortlist | 85% | B2B research |

| Buyers selecting previously known brands | 78% (enterprise: 86%) | B2B research |

| Content consumed before purchase decision | Up to 15 pieces | B2B research |

| Thought leadership consumption: 1+ hour/week | 63% | Edelman-LinkedIn |

| Hidden buyers: more receptive to outreach after strong TL | 95% | Edelman-LinkedIn 2025 |

| Original research more valuable than AI content | 67% of marketers | Industry surveys |

The data is unambiguous: 60% of decision-makers will pay a premium to suppliers who produce strong thought leadership. 71% of hidden buyers — the internal stakeholders who influence decisions behind the scenes — say thought leadership is more effective than marketing materials. 85% of buyers choose from their day-one shortlist, and 78% select brands they knew before research began.

This is the trust premium in action: credibility compounds into commercial advantage before the sales conversation starts. In an AI-saturated environment where anyone can produce generic content, the organizations that produce trusted synthesis own the shortlist.

Why the Premium Is Growing

| Driver | Mechanism |

|---|---|

| Content supply explosion | More content → harder to differentiate → trusted sources stand out more |

| Distribution fragmentation | Search declining → direct audience relationships matter more |

| Detection fatigue | Audiences can’t verify → they default to sources with track records |

| Dark funnel dominance | 70% of buying journey invisible → brand credibility formed by content, not sales |

| AI homogenization | AI produces converging outputs → distinctive point of view becomes rare |

The trust premium grows as saturation increases. When all content sounds similar — because it’s generated from similar models trained on similar data — the content that sounds different (because it reflects genuine expertise, original research, and a clear point of view) captures disproportionate attention.

The AI Entrepreneur: How to Make Money with AI: From Idea to Launch — Build, Fund, Market, and Scale Your AI Business in 90 Days or Less

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

4. The Trust Premium Framework

Credibility is not a vibe. It’s an editorial architecture. Four components turn content from noise into signal.

Component 1: Evidence Labeling

Tag every significant claim by confidence level.

| Confidence Level | Definition | Example |

|---|---|---|

| High | Primary data, audited reports, regulatory filings | “95% of GenAI pilots fail (MIT, 2025)” |

| Medium | Credible surveys, expert consensus, directional data | “Market expected to reach $X by 2028 (analyst estimate)” |

| Low / Directional | Early signals, limited data, informed inference | “Early indicators suggest… (N=small, single study)” |

Most content treats all claims equally. “Gartner predicts” and “one blog says” get the same assertive tone. Evidence labeling makes the confidence structure visible — and audiences respond by trusting the overall output more because they can see where the certainty is and isn’t.

Component 2: Source Quality Hierarchy

Not all sources are equal. The hierarchy:

| Source Tier | Examples | Trust Weight |

|---|---|---|

| Primary data | SEC filings, regulatory documents, court records, APIs | Highest |

| Audited research | Peer-reviewed studies, major analyst reports (Gartner, McKinsey, MIT) | High |

| Named expert attribution | Identified professionals with verifiable domain expertise | Medium-High |

| Industry surveys | Named methodology, disclosed sample size, published firm | Medium |

| Unnamed aggregation | “Sources say,” “reports indicate,” “experts believe” | Low |

| AI-generated synthesis | No attribution, no methodology, no confidence markers | Lowest |

67% of marketers say original research is more valuable than AI-generated content for trust and credibility. The source hierarchy operationalizes why: original research carries the friction of methodology, the accountability of named researchers, and the specificity of disclosed data. AI synthesis carries none of those trust signals.

Component 3: Point-of-View Discipline

The most common failure in AI-saturated content is the absence of interpretation. AI produces competent summaries. It rarely produces clear positions.

| Generic Summary (Noise) | Point-of-View (Signal) |

|---|---|

| “AI adoption is accelerating across industries” | “78% of organizations use AI in at least one function — but 60% generate no material value. Adoption without structure is the norm.” |

| “Companies should consider AI governance” | “80%+ of unauthorized AI transactions come from internal policy violations. Governance isn’t optional — it’s the primary risk vector.” |

| “The content marketing landscape is evolving” | “74% of new web pages contain AI content. The noise floor just rose. Competing on volume is now competing to lose.” |

Point-of-view discipline means every piece takes a position, states it clearly, and supports it with evidence. Not opinion without data. Not data without interpretation. The combination.

Component 4: Utility-First Structure

Every piece must answer two questions: So what? and What now?

| Structure Element | Purpose |

|---|---|

| Lead with the data point | Establish the evidence before the argument |

| State the implication | What does this mean for the reader’s decisions? |

| Define the action | What should the reader do differently? |

| Name the trade-off | What are the costs, risks, or alternatives? |

| Set the decision criteria | How should the reader decide? |

Content that informs without directing is noise. Content that directs without evidence is opinion. The trust premium is captured by content that does both: evidence-backed, implication-clear, action-ready.

5. Editorial Operating Rules for the AI-Saturated Era

The trust premium framework requires operational discipline. These are the editorial rules that prevent credibility erosion.

Rule 1: Publish Fewer, Sharper Pieces

Market saturation is the #1 concern for marketers in 2026. The response is not “produce more, better content.” The response is produce less content with higher evidence density, clearer positioning, and more actionable structure.

| Volume Strategy (Old) | Trust Strategy (New) |

|---|---|

| 4 blog posts/week | 1 substantive briefing/week |

| Optimize for keywords | Optimize for decision utility |

| Maximize impressions | Maximize save/share/forward |

| Cover every trending topic | Own specific decision domains |

| Repurpose across channels | Originate for the primary audience |

89% of B2B marketers use AI for content creation. When everyone publishes more, publishing more is the one strategy guaranteed to not differentiate.

Rule 2: Separate Confirmed Facts from Directional Signals

| Label | Usage |

|---|---|

| Confirmed | Audited data, regulatory filings, peer-reviewed research |

| Estimated | Major analyst projections, survey data with disclosed methodology |

| Directional | Early signals, limited sample sizes, expert inference |

| Unknown | Openly stated gaps in available evidence |

This is evidence labeling in practice. The “Unknown” category is the most valuable: stating what you don’t know builds more credibility than pretending certainty where none exists.

Rule 3: Include Explicit Assumptions and Open Questions

Every analysis rests on assumptions. Making them explicit — “This analysis assumes current regulatory trajectory continues” or “This estimate depends on enterprise adoption rates that are currently directional” — transforms the content from assertion into reasoning that the reader can evaluate.

Rule 4: Build Repeatable Templates for Executive Readers

The trust premium compounds when the format itself becomes trusted. Readers who know the structure — data first, implication second, action third, trade-off fourth — can extract value faster. Faster extraction means more consumption, which reinforces the trust signal.

| Template Element | Function |

|---|---|

| Executive summary with key metrics | Scan value in 30 seconds |

| Comparison tables | Side-by-side evaluation without narrative bias |

| Pull quotes with key takeaways | Shareable, referenceable insights |

| Action items with decision criteria | Direct operational application |

| Sources section with linked references | Verifiability without interrupting flow |

Rule 5: Audit Content Monthly for Claim Quality

| Audit Dimension | What to Check |

|---|---|

| Claim accuracy | Has the data been updated, corrected, or contradicted? |

| Source freshness | Are referenced studies still the most current? |

| Confidence calibration | Were “high confidence” claims actually borne out? |

| Correction discipline | Were errors corrected publicly and promptly? |

| Action validity | Do the recommendations still hold given new evidence? |

The correction discipline is the highest-leverage trust signal in content. Organizations that correct publicly — “In our February analysis, we cited X. Updated data from March shows Y. Our revised assessment is Z.” — build more credibility than organizations that never admit error.

6. Metrics That Matter: From Volume to Decision-Usefulness

The traditional content KPI stack — pageviews, time on site, social shares — measures attention, not trust. The trust premium requires different instrumentation.

| Old KPI | Trust KPI | What It Measures |

|---|---|---|

| Pageviews | Save/bookmark rate | Content worth keeping |

| Time on site | Forward-to-team rate | Content worth sharing with decision-makers |

| Social shares | Direct return visits | Audience comes back by name, not by search |

| MQLs from content | Day-one shortlist inclusion | Content created pre-sale credibility |

| Keyword rankings | Cited-as-source rate | Content referenced by others as evidence |

| Content volume produced | Decision-usefulness score | Content changed a decision or action |

85% of buyers choose from their day-one shortlist. 70% of the buying journey happens in the dark funnel. The metrics that matter are the ones that measure whether content is building the trust that forms shortlists and influences decisions before vendors are ever contacted.

7. Practical Implications and Actions

Action 1: Adopt an Evidence-and-Confidence Standard for All Flagship Outputs

Every claim tagged high, medium, low, or directional. Every source categorized by tier. This is not bureaucracy — it’s the editorial equivalent of audited financials. When 74% of web content is AI-generated, the organizations that show their evidence work stand out by default.

Action 2: Shift KPIs from Volume to Decision-Usefulness

Stop measuring pageviews as a success metric. Measure save rate, forward-to-team rate, direct return visits, and cited-as-source frequency. These are the indicators that content is building the trust premium — not just capturing attention, but influencing decisions.

Action 3: Add a Recurring “What to Do Next” Section in Every Piece

Decision-usefulness is the dividing line between content that informs and content that matters. Every piece should end with specific, evidence-backed actions that the reader can take. Not “consider implementing AI governance.” Instead: “Define four autonomy tiers per workflow before deployment. Pre-define stop criteria quantified in the pilot charter.”

Action 4: Audit Top Content Monthly for Claim Quality and Correction Discipline

Review the top 10 pieces monthly. Check: Are the claims still accurate? Have sources been updated? Were predictions borne out? Publish corrections prominently. The 67% of marketers who say original research beats AI content are right — but only if the original research stays current and self-correcting.

Action 5: Build Signature Frameworks Readers Can Reuse Operationally

The highest-value trust content creates frameworks — repeatable structures that readers apply to their own decisions. A 6-week pilot blueprint. A five-layer trust stack. A decision-tiering model. These frameworks become intellectual property that the audience associates with the source, building the trust premium with every reuse.

8. What to Watch

Platforms and buyers rewarding source transparency over content frequency. Search algorithms are already shifting toward quality signals over volume signals. The next evolution: platforms explicitly surfacing provenance metadata — who created this, with what methodology, based on what data. Content with verifiable provenance will receive distribution advantages. Content without it will be treated as noise.

More demand for operator-grade briefings over general trend commentary. The market is bifurcating: generic AI-generated trend summaries (free, abundant, low trust) versus operator-grade briefings with original data, clear positions, and actionable frameworks (premium, scarce, high trust). The decision-maker audience — the 63% consuming 1+ hour of thought leadership weekly — is migrating toward the second category.

Emerging premium for trusted niche publishers with strong editorial governance. Individual journalists’ newsletters, podcasts, and LinkedIn followings increasingly rival institutional outlets. The trust premium doesn’t require scale. It requires consistency, evidence quality, and point-of-view clarity. A niche publisher with 5,000 deeply engaged decision-maker subscribers captures more commercial value than a mass publisher with 5 million casual readers.

The Bottom Line

90% of online content will be AI-generated by 2026. 74% already is. Search is declining 25%. Major news organizations lost 11 trust points. Only 12% of readers are comfortable with AI-generated news. And 85% of B2B buyers choose from their day-one shortlist — a shortlist formed by trust, not by volume.

The trust premium is not a branding exercise. It’s a structural advantage in an information market where supply is infinite and credibility is scarce. The organizations that build editorial architectures — evidence labeling, source hierarchies, point-of-view discipline, utility-first structure — will own the attention that drives decisions. The organizations that optimize for content volume will compete with every AI model that writes faster and cheaper than they do.

In an information market where AI produces infinite supply, the only moat is the trust your audience grants you — and trust is earned by evidence, not by volume.

Thorsten Meyer is an AI strategy advisor who has noticed that the organizations producing the least content in 2026 are often capturing the most trust — and the most revenue. More at ThorstenMeyerAI.com.

Sources

- Gartner/Europol — 90% Online Content AI-Generated by 2026

- Ahrefs — 74.2% New Web Pages Contain AI Content (April 2025)

- Graphite — 50%+ New Articles Primarily AI-Written (Late 2024)

- AWS — 57% Online Content AI-Generated/Translated

- Gartner — 25% Search Engine Volume Decline by 2026

- Gartner — Traditional Search Losing Share to AI Chatbots

- Edelman — 2026 Trust Barometer: –11 Net Trust Points for Major News Orgs

- Edelman — 37% Cite GenAI Growth as Trust Factor; 65% Worried About Foreign Falsehoods

- Edelman-LinkedIn — 2025 B2B Thought Leadership Impact Report: Hidden Buyers

- Edelman-LinkedIn — 60% Willing to Pay Premium; 71% TL More Effective Than Marketing

- iProov — 0.1% Correct Identification of All Fakes (2025)

- iProov — Only 9% of Adults Confident Identifying Deepfakes

- Industry Data — Deepfakes ~500K (2023) to ~8M (2025), ~900% Growth

- Media Surveys — 12% Comfortable with AI News; 90% Want Disclosure

- Consumer Research — 74% Doubt Photos/Videos from Trusted Outlets

- B2B Research — 85% Choose from Day-One Shortlist; 78% Select Known Brands

- B2B Research — Up to 15 Content Pieces Before Purchase; 70% Dark Funnel

- Industry Surveys — 67% Say Original Research More Valuable Than AI Content

- Content Marketing Institute — Market Saturation #1 Concern (2026)

- Ahrefs/Digital Elevator — U.S. Organic CTR 40.3%, No-Click 27.2% (March 2025)

- B2B Research — 89% Using AI for Content; 95% B2B Marketers Use AI Apps

- Fortune — Deepfake Voice Cloning Crossed Indistinguishable Threshold (2026)

- Search Engine Journal — B2B Trust Deficit: 80% Post-Purchase Dissatisfaction

- Mediaforta — AI Authenticity: Trust Defines SEO and GEO in 2026

- UNESCO — Deepfakes and the Crisis of Knowing

© 2026 Thorsten Meyer. All rights reserved. ThorstenMeyerAI.com