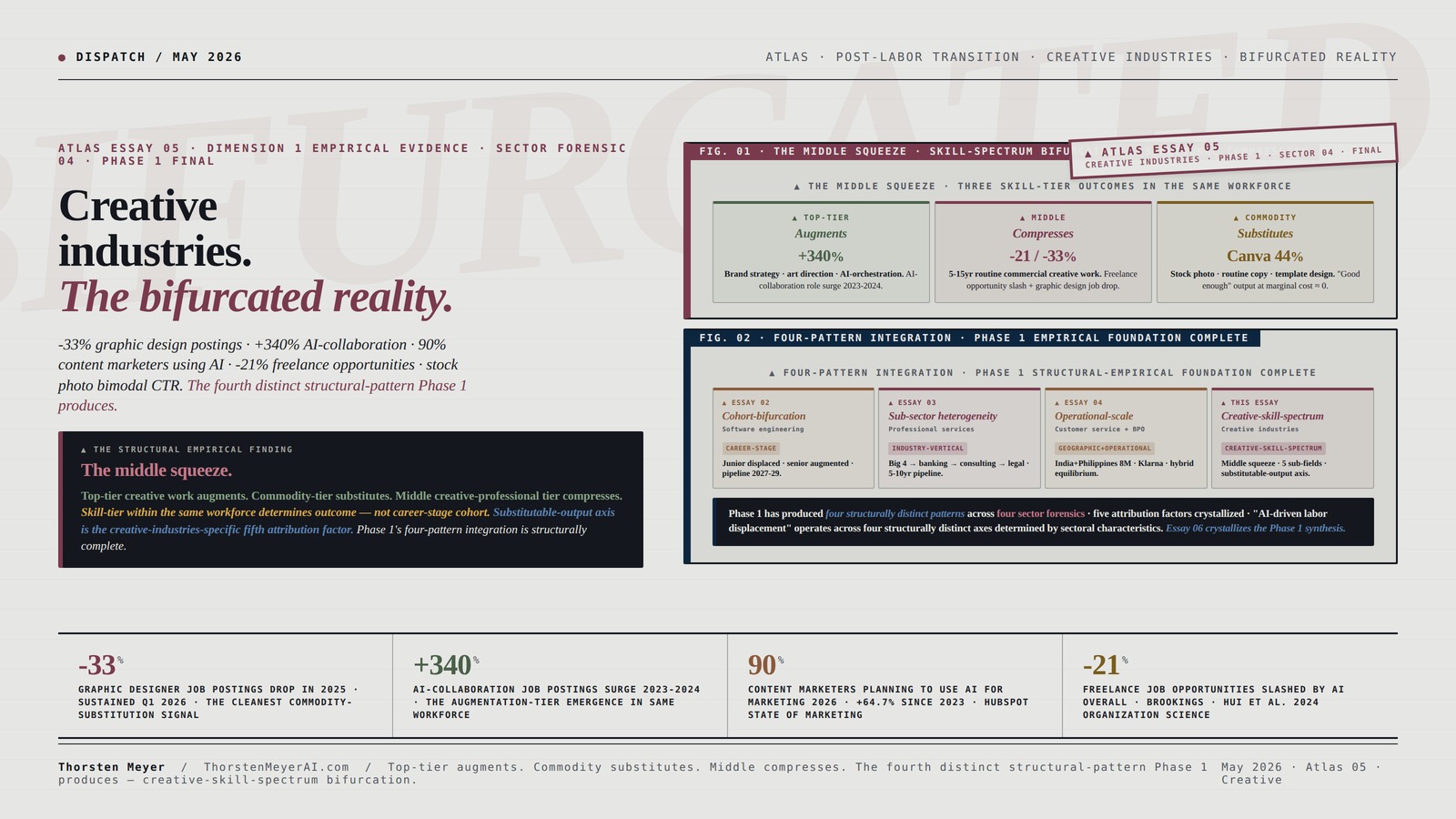

Graphic designer job postings dropped 33% in 2025. AI-collaboration job postings surged 340% between 2023 and 2024 in the same workforce. Content production roles dropped 28% same period. Only 31% of designers use AI for core work versus 59% of developers. Canva commands 44% of creative AI tool usage; Midjourney 13%; Jasper 12%; Runway 12%. 90% of content marketers plan to use AI for marketing in 2026 — a 64.7% rise since 2023. 73% of marketing professionals use AI for content creation, but only 12% rely fully on AI without human review. AI-generated advertising imagery is rated more aesthetically appealing than comparable human-created content while quality, creativity, purchase intention, and brand engagement remain statistically indistinguishable. About half of AI-generated stock photos outperform human-made ones in click-through rates by up to 50%, while the other half underperform by up to 25% — a bimodal distribution. The Brookings-cited Hui et al. Organization Science 2024 research on Upwork finds pronounced displacement effect in submarkets where required skills closely align with core LLM functionalities. Demand for translation, writing, and graphic design services has fallen on freelance platforms. AI just slashed freelance job opportunities by 21%. The structural-pattern crystallized: top-tier creative work augments, routine commercial creative work substitutes, middle creative-professional tier faces compression. This is the “middle squeeze” — creative-skill-spectrum bifurcation. The fourth distinct structural-pattern Phase 1 of the Atlas produces.

By Thorsten Meyer — May 2026

This is Atlas Essay 05 — the fourth and final Dimension 1 empirical-evidence sector forensic in the Post-Labor Transition Atlas, completing Phase 1’s sector-forensic foundation before the Phase 1 synthesis essay. Essay 02 crystallized the cohort-bifurcation pattern in software engineering. Essay 03 extended it through sub-sector heterogeneity in white-collar professional services. Essay 04 introduced the operational-scale displacement pattern in customer service + BPO. Essay 05 tests whether creative industries produces a fourth distinct structural-pattern — and the empirical evidence supports a “middle squeeze” pattern that is structurally distinct from all three prior findings.

The structural argument I want to make: creative industries produces the fourth distinct structural-pattern Phase 1 of the Atlas produces — creative-skill-spectrum bifurcation, a.k.a. the “middle squeeze.” The displacement is not cohort-specific (juniors vs. seniors) and not sub-sector-fragmented and not operational-scale (geographic + workforce-wide horizontal). It is skill-tier bifurcated within the same workforce: top-tier signature creative professionals augment, routine commercial creative work substitutes, and the middle creative-professional tier faces structural compression. The middle squeeze is the empirical signature.

The headline empirical finding: creative industries displacement operates on a skill-spectrum axis rather than a cohort axis or an operational-scale axis. The same workforce contains professionals at both ends of the displacement spectrum simultaneously: high-end art directors and brand strategists augmenting with Midjourney/Runway/Adobe Firefly to deliver work that previously required teams; commodity-tier stock illustration and routine copywriting and template design collapsing under Canva/ChatGPT/Sora; and the middle-tier commercial designer/copywriter/translator/photographer facing the structural compression that produces the 33% job-posting drop in graphic design and the 21% freelance-opportunity slash overall. The “middle squeeze” pattern is the empirical signature of Interpretation 2 from Essay 01’s framework, but operating on a structurally different axis than the three prior sectors.

This essay walks the empirical evidence base (the multi-source convergence on graphic design, copywriting, translation, stock photography, and adjacent creative sub-fields), the bifurcation mechanism (commodity substitution vs. strategic augmentation), the “middle squeeze” structural pattern (the compressed mid-tier), the attribution-rigor framework specific to creative industries (the substitutable-output axis), and the integrative observations producing the four-pattern integration that Essay 06’s Phase 1 synthesis will crystallize.

Creative industries.

The bifurcated reality.

Graphic designer postings -33% · AI-collaboration roles +340% · content production -28% · 90% content marketers using AI · stock photo bimodal click-through distribution · 21% freelance opportunity slash. The fourth distinct structural-pattern Phase 1 produces — creative-skill-spectrum bifurcation.

This is Atlas Essay 05 — the fourth and final Dimension 1 sector forensic in Phase 1. Creative industries produces the fourth distinct structural-pattern: creative-skill-spectrum bifurcation, a.k.a. the “middle squeeze.” Top-tier creative work augments — brand strategy, art direction, AI-orchestration · AI-collaboration job postings +340% 2023-2024. Commodity-tier creative work substitutes — stock photography, routine copy, template design · graphic designer postings -33% in 2025 · content production roles -28%. Middle creative-professional tier faces structural compression — the squeeze that makes the bifurcation pattern empirically distinct from cohort-bifurcation (Essay 02), sub-sector heterogeneity (Essay 03), and operational-scale displacement (Essay 04). Multi-source convergence: Brookings · Hui et al. Organization Science · Envato 2026 (1,780 creatives) · Figma 2025 · HubSpot · European Parliament study · Hartmann et al. 2025. Phase 1’s four-pattern integration is structurally complete.

Five sub-fields. One pattern.

Creative industries has the most empirically-fragmented evidence base across sub-fields of any Phase 1 sector. The consistent across-sub-field finding is the bifurcation pattern itself — top-tier augments, commodity substitutes, middle compresses, in every sub-field documented.

signal

vs quality

vs specialized

distribution

cutting

Luminar AI Photo Editing Software – Skylum Software Photo Editor – You Bring the Creative Vision – Powerful AI Brings it to Life – Get the Graphic Design Software for Mac and Windows 10 Pro – 2 seats

- Fast, Stunning Photo Enhancements: Create breathtaking photos quickly with AI

- Advanced AI Features: Includes SkyAI, FaceAI, SkinAI, BodyAI, AtmosphereAI

- User-Friendly Interface: Simple, intuitive design for easy editing

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three tiers. The middle squeeze.

The structural-empirical pattern across the five sub-fields. Creative industries displacement operates on a substitutable-output axis distinct from cohort, sub-sector, and operational-scale axes of the prior sectors. Top-tier augments, commodity substitutes, middle compresses.

stock photo click-through rate optimization tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five factors. Substitutable-output.

The analytical decomposition extended to creative industries. Creative industries operates on a fifth attribution factor — the substitutable-output axis — that is structurally distinct from cohort-specific, pyramid-model, and operational-scale dynamics of the prior three sectors.

here

specific

Successful AI Product Creation: A 9-Step Framework

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four patterns. Phase 1 complete.

The integrative observation Essay 05 produces. Phase 1 has now produced empirical evidence for four structurally distinct displacement patterns — operating across four structurally distinct axes determined by sectoral characteristics. “AI-driven labor displacement” is a family of patterns, not a single phenomenon.

axis

axis

operational axis

spectrum axis

Creative industries is the bifurcated reality empirically confirmed. Top-tier creative work augments — brand strategy, art direction, AI-orchestration · AI-collaboration roles +340%. Commodity-tier creative work substitutes — stock photography, routine copy, template design · graphic-design job postings -33%. Middle creative-professional tier faces structural compression — the “middle squeeze” pattern. This is the fourth distinct structural-pattern Phase 1 produces — creative-skill-spectrum bifurcation operating on a skill-tier axis rather than cohort, sub-sector, or operational axes. The Atlas framework’s Phase 1 empirical-evidence foundation is structurally complete. Four sector forensics. Four distinct structural-patterns. Five attribution factors. Essay 06 crystallizes the integrative synthesis.

![Adobe Photoshop Elements 2026 | Software Download | Photo Editing | 3-year term license | Activation Required [PC/Mac Online Code]](https://m.media-amazon.com/images/I/41xELXBHllL._SL500_.jpg)

Adobe Photoshop Elements 2026 | Software Download | Photo Editing | 3-year term license | Activation Required [PC/Mac Online Code]

- AI-Generated Image Creation: Create images and backgrounds with AI

- Photo Enhancement Tools: Erase distractions, replace backgrounds, touch up faces

- User-Friendly Editing Modes: Quick, Guided, and Advanced editing options

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

I · The empirical evidence base · five creative sub-fields documented

The factual baseline before the structural-pattern argument. Creative industries has the most empirically-fragmented evidence base across sub-fields of any Phase 1 sector — and the consistent across-sub-field finding is the bifurcation pattern itself.

Sub-field 1 · Graphic design + illustration · the canonical bifurcation case

Per the Risk Quiz · “Will AI Replace Graphic Designers? 2026 Risk Analysis” (April 9, 2026), the Upwork · “Will AI Replace Graphic Designers? What To Know in 2026” analysis, and the We and The Color · “The Collapse of the Mid-Level Freelance Market Due to AI” coverage:

The graphic design empirical signature is the cleanest evidence for creative-skill-spectrum bifurcation:

- Graphic designer job postings dropped 33% in 2025 · sustained through Q1 2026

- Only 31% of designers use AI for core work (Figma 2025 AI Report) versus 59% of developers · the adoption gap is itself structurally significant

- AI-collaboration job postings surged 340% between 2023 and 2024 · the augmentation-tier emergence

- Content production roles dropped 28% same period

- Q1 2026 tech layoffs: 55,911 workers · 736/day · 20.4% explicitly cited AI/automation

- Canva commands 44% of creative AI tool usage · Midjourney 13% · Jasper 12% · Runway 12%

The “Canva dominance” finding is structurally significant. Canva is the platform that lets non-designers produce designer-acceptable output — the empirical evidence that the barrier to “good enough” visual content has collapsed. This is the commodity-substitution axis of the bifurcation. The structural mechanism: clients who previously paid mid-tier designers $500-$2,000 for routine commercial work now generate equivalent output via Canva ($20/month) and pay designers $50 to “polish” the AI output.

The “race to the bottom” qualitative evidence (per We and The Color community sourcing from Reddit, Dribbble, LinkedIn comment threads): “Clients keep asking me to just ‘tweak the AI output.’ This is the new race to the bottom. Instead of hiring a designer to create, clients generate something mediocre with AI, then want to pay a designer $50 to polish it. The creative work becomes a correction service. Compensation and creative authority both collapse simultaneously. ‘My rates haven’t moved in two years, but my pipeline has halved.'”

The Envato State of AI in Creative Work 2026 report surveying 1,780 creative professionals confirms the bifurcation pattern across the wider creative workforce.

Sub-field 2 · Copywriting · the volume-vs-quality split

Per Filthy Rich Writer · “Is AI Taking Over Copywriting in 2026?” (February 3, 2026), Click Forest · “AI copywriting versus human creativity”, SEOwind · “Will AI Replace Copywriters”, and Mustard and Moxie · “Why AI Can’t Replace Your Copywriter (Yet)”:

The copywriting empirical signature shows the bifurcation operating on the volume-vs-quality axis:

- 90% of content marketers plan to use AI for marketing in 2026 · rise of 64.7% since 2023

- 73% of marketing professionals use AI for content creation · only 12% rely fully on AI without human review (HubSpot State of Marketing Report)

- 94.5% of content creators worldwide use AI tools for editing, image generation, writing captions

- HubSpot’s 2024 AI Trends for Marketers: AI adoption in marketing jumped from 21% in 2022 to 74% in 2023 · rapid shift in content production methods

- 47% of marketers already use AI tools to generate content · 28% use them to generate design elements (Siege Media research)

- JPMorgan Chase + Persado · five-year deal for AI-generated ad copy · the canonical enterprise reference deployment

- Coca-Cola custom GPT-based platform · 40% concept-to-campaign time reduction · 25% engagement increase

The structural interpretation: the 12% “rely fully on AI without human review” figure is structurally significant — it crystallizes the bifurcation pattern in copywriting specifically. AI handles the volume tier (routine commercial copy, social media posts, ad variants, SEO content, email drafts) at near-total adoption. Humans handle the quality tier (brand voice development, long-form thought leadership, regulated/compliance-sensitive copy, high-stakes campaign concepts, copy requiring deep audience insight). The middle commercial-copywriter tier faces compression — neither at the top (signature brand work) nor the bottom (commodity AI-generated output).

The “AI is detectable and Google penalizes it” structural argument from Mustard and Moxie is part of the operational equilibrium: search-engine quality signals are emerging as the structural anchor for human-authored content in SEO-driven copywriting submarkets.

Sub-field 3 · Translation · the routine-vs-specialized split

The translation sub-field shows the bifurcation pattern operating most cleanly along a routine vs. specialized axis:

- DeepL + Google Translate + GPT-4 displacement of routine commercial translation (product descriptions, customer service responses, basic UI strings, social media content)

- Literary translation augmenting rather than substituting · the literary craft requirements + cultural-fluency depth + voice-preservation requirements remain structurally non-substitutable

- Legal translation augmenting rather than substituting · the certified-translator requirement + regulatory compliance + liability framework keeps human translators in the operational loop

- Medical translation similar pattern · the patient-safety requirement + specialized terminology + regulatory framework

- Demand for translation services has fallen on freelance platforms (Demirci et al. 2025)

The structural mechanism: translation is the sub-field where the substitutable-output axis is most operationally clear. Routine translation produces commodity output (functional-acceptable rendering between languages); specialized translation produces craft output (legally-defensible translation, literarily-meaningful translation, medically-accurate translation). The volume-tier routine translation collapses under AI substitution; the quality-tier specialized translation augments.

Sub-field 4 · Stock photography + advertising imagery · the bimodal distribution

Per the European Parliament study citing Hartmann et al. (2025) on advertising AI imagery:

The stock photography and advertising imagery empirical signature is structurally distinct:

- AI-generated advertising imagery is rated more aesthetically appealing than comparable human-created content

- Quality, creativity, purchase intention, and brand engagement remain statistically indistinguishable between AI-generated and human-created

- In real-world campaigns: ~50% of AI-generated stock photos outperform human-made ones in click-through rates by up to 50%

- The other ~50% underperform by up to 25% · bimodal distribution

- Stock photography long-tail dominance by AI-generated images · the structural collapse of the long-tail commodity stock photography market

The structural interpretation: stock photography is the sub-field where AI substitution is most operationally complete in the commodity tier. The bimodal click-through distribution is the structural signature — AI either dramatically outperforms (the half of cases where AI hits the target audience) or significantly underperforms (the half of cases where AI misses on context, emotional resonance, brand fit). The high-end advertising photography augments through art direction; the commodity stock photography collapses under direct substitution. The bimodal distribution itself is the bifurcation signature.

Sub-field 5 · Freelance creative platform demand · the cross-cutting empirical evidence

Per the Brookings analysis citing Hui et al. (2024 · Organization Science), the arXiv “Generate the Future of Work through AI” paper, and Medium · “Why AI Disruption Will End Freelancing as We Know It”:

The freelance creative platform evidence is the most analytically rigorous empirical base:

- Hui et al. 2024 (Organization Science · Brookings-cited): pronounced displacement effect in Upwork submarkets where required skills closely align with core LLM functionalities

- Demand for translation, writing, and graphic design services has fallen on freelance platforms (Demirci et al. 2025 · Hui et al. 2024 · Yilmaz et al. 2023)

- AI slashed freelance job opportunities by 21% (fxis.ai July 2025)

- Stack Overflow user engagement declined markedly following ChatGPT release (Quinn and Gutt 2025 · Burtch et al. 2024 · del Rio-Chanona et al. 2023 · Yilmaz et al. 2023)

- Goldberg and Lam 2025 art platform study: GenAI substitutes for non-GenAI content, crowding out lower-quality non-GenAI creators · entry of GenAI producers increases variety, quality, sales · consumers and platforms benefit, non-GenAI creators disadvantaged

- Brookings framing: “High-skill workers with access to complementary tools may benefit, while mid-skill workers, whose tasks are more easily replicated by AI, may be displaced or pushed into lower-paying jobs.”

The structural finding from freelance platform empirical research crystallizes the “middle squeeze”: displacement is concentrated in the mid-skill freelance workforce. High-skill freelancers benefit from AI complementarity. Low-skill commodity-tier work substitutes. The middle tier compresses.

II · The bifurcation mechanism · commodity substitution vs. strategic augmentation

The structural-empirical pattern across the five sub-fields. The creative industries displacement operates on a substitutable-output axis distinct from the cohort, sub-sector, and operational-scale axes of the prior sectors.

The commodity-tier substitution

The empirical evidence is clear across the five sub-fields documented:

- Routine commercial graphic design · Canva-tier production · template-based work · stock-element compositions · routine social media graphics · simple ad variants

- Routine commercial copywriting · social media posts · email drafts · SEO content variants · standard ad copy · product descriptions

- Routine translation · product descriptions · customer service responses · UI strings · social media content

- Stock photography long-tail · commodity stock photography · template-able imagery · routine product photography

- Stock illustration + routine animation · template-based illustration · routine explainer animation · generic motion graphics

The structural mechanism: AI tools produce “good enough” output at marginal cost approaching zero for the commodity tier. Clients who previously paid mid-tier creative professionals for this work now produce equivalent output via subscription AI tools at $20-$50/month. The economic floor for commodity creative work has structurally collapsed.

The strategic-tier augmentation

The empirical evidence is equally clear on the augmentation side:

- Brand strategy + art direction · creative professionals directing AI tools across larger work portfolios · taking on projects that previously required full teams

- High-end creative concepts · Coca-Cola GPT-platform pattern · concept-to-campaign acceleration · localized campaigns in multiple markets within days

- Signature creative work · the “human-made design becomes the new sought-after thing” pattern from designer community discourse

- AI-collaboration roles · 340% surge in postings 2023-2024 · prompt engineering · art-directing AI output · integrating AI into production workflows

- The “AI-orchestrating creative director” emerging role · structurally similar to software engineering’s “AI-orchestrating architect” but operating on creative-output rather than codebase-output dimensions

The structural mechanism: AI tools function as productivity multipliers for top-tier creative professionals. The Goldberg and Lam art-platform finding crystallizes the dynamic: entry of GenAI producers increases variety, quality, sales · consumers and platforms benefit · non-GenAI creators are disadvantaged (in the commodity tier) but high-end art direction benefits.

The “middle squeeze” · the structural compression of the mid-tier

The middle creative-professional tier — neither at the top (signature work) nor the bottom (substitutable commodity) — faces the structural compression that produces the 33% graphic-design-job-posting drop and the 21% freelance-opportunity slash.

The mid-tier creative professional profile:

- 5-15 years of experience

- Solid execution skills in their specific creative craft

- Mid-market client base (small businesses, agencies serving mid-market clients)

- Routine commercial creative work as their core revenue base

- Limited brand-strategic or art-directional positioning

- Limited AI-fluency / prompt-engineering expertise

This profile is structurally squeezed from both directions simultaneously:

- Below: AI tools enable non-designers to produce commodity-tier output their clients accept

- Above: AI-augmented top-tier creative professionals take on more projects per professional, capturing market share that previously fed the mid-tier

The middle squeeze is the empirical signature of creative-skill-spectrum bifurcation. It is structurally distinct from the cohort-bifurcation pattern (where juniors at the bottom face displacement and seniors at the top augment) because the displacement axis here is skill-tier within the same workforce rather than career-stage cohort within a stratified pyramid. A graphic designer with 12 years of experience and routine-commercial-work specialization faces the squeeze; a graphic designer with 12 years of experience and brand-strategy / AI-orchestration specialization augments. The years of experience are equal; the position on the creative-skill-spectrum determines the outcome.

III · The attribution-rigor framework · the substitutable-output axis

The analytical decomposition Essays 02-04 introduced extended to creative industries. Creative industries operates on a fifth attribution factor (the substitutable-output axis) that is structurally distinct from cohort-specific, pyramid-model, and operational-scale dynamics.

Factor 1 · Macroeconomic · same baseline

The same 2023-2024 macroeconomic environment affecting all prior sectors operates here. Cost-cutting pressure across marketing budgets, freelance budget compression, agency consolidation, and client efficiency demands.

Factor 2 · AI-tool maturation · creative-specific tools

The AI-tool maturation factor is structurally similar to prior sectors but with creative-specific tools:

- Image generation: Midjourney · DALL-E · Adobe Firefly · Stable Diffusion · Leonardo · Ideogram

- Design: Canva (44% market share) · Figma AI · Adobe Express AI · Microsoft Designer

- Copywriting: ChatGPT · Claude · Jasper · Copy.ai · Writer · custom enterprise LLMs

- Video: Sora · Runway · Pika · Hailuo · Kling

- Music: Suno · Udio · ElevenLabs (voice)

- Translation: DeepL · GPT-4 · Claude · Google Translate Neural

The tools have crossed the operational-substitutability threshold for commodity-tier creative output in 2023-2025.

Factor 3 · Cohort-specific compounding · structurally weaker here

The cohort-specific factor that drove software engineering and professional services displacement is structurally weaker in creative industries. Mid-career creative professionals (5-15 years experience) face displacement alongside junior creative professionals if both occupy the routine-commercial-work tier. Seniors with strategic positioning augment regardless of cohort. The cohort axis is largely replaced by the skill-tier axis as the structural dimension.

Factor 4 · Pyramid-model pressure · not present

The professional-services-specific pyramid-model factor is not structurally present in creative industries. Creative work is generally not delivered through a traditional pyramid hierarchy of junior-to-senior progression with associated training-and-billing economics. The displacement mechanism operates on different structural lines.

Factor 5 · Substitutable-output axis · the creative-industries-specific factor

The fifth attribution factor is structurally specific to creative industries: the substitutable-output axis. Creative work outputs have a specific quality threshold (“good enough for purpose”) that varies dramatically across the creative-output spectrum:

- Low-threshold commodity work (stock photo for blog post, routine social media graphic, basic translation) · “good enough” threshold easily achievable by AI · commodity-tier substitution operates here

- High-threshold signature work (brand identity, signature campaign, literary translation, art-directed photography) · “good enough” threshold requires specific creative judgment that AI cannot reliably reproduce · augmentation tier operates here

- Middle-threshold commercial work (custom illustrations for mid-market client, custom brand-aligned copy, commercial photography requiring specific direction) · “good enough” threshold technically achievable by AI with sufficient prompt-engineering effort but with reliability gaps · the middle squeeze tier

The substitutable-output axis is the creative-industries-specific factor. It compounds with macroeconomic and AI-tool factors to produce the bifurcation pattern. The Atlas operates on attribution rigor: naming each factor by sector rather than conflating them.

IV · The integrative observations · the four-pattern Phase 1 framework

The structural-pattern findings the creative industries forensic produces for the Atlas framework. Phase 1 has now produced empirical evidence for four structurally distinct displacement patterns within the same broad phenomenon of “AI-driven labor displacement.”

Pattern 1 · Cohort-bifurcation (Essay 02 · software engineering)

Junior cohort displaced · senior cohort augmented · pipeline collapsing 2027-2029. Within-sector cohort stratification operates on career-stage axis.

Pattern 2 · Sub-sector heterogeneity (Essay 03 · white-collar professional services)

Cohort-bifurcation fragmented across sub-sectors · intensity gradient · pipeline 5-10 year horizon. Within-sector sub-sector fragmentation operates on industry-vertical axis.

Pattern 3 · Operational-scale displacement (Essay 04 · customer service + BPO)

Geographic concentration · workforce-wide horizontal pressure · hybrid-model emergence as operational equilibrium. Within-sector operational-scale dynamics operate on geographic-and-operational axis.

Pattern 4 · Creative-skill-spectrum bifurcation (this essay · creative industries)

The “middle squeeze” · top-tier augments · commodity substitutes · middle compresses. Within-sector skill-tier bifurcation operates on creative-skill-spectrum axis.

The four-pattern integration

The Atlas framework’s Phase 1 has produced empirical evidence that “AI-driven labor displacement” operates across four structurally distinct axes:

- Career-stage axis (cohort-bifurcation) · software engineering canonical case

- Industry-vertical axis (sub-sector heterogeneity) · white-collar professional services canonical case

- Geographic-and-operational axis (operational-scale displacement) · customer service + BPO canonical case

- Creative-skill-spectrum axis (middle squeeze) · creative industries canonical case

The analytical-discipline finding: the structural-empirical pattern is that sectoral characteristics determine which axis dominates. Sectors with stratified training pyramids (software engineering, professional services) produce cohort-bifurcation patterns. Sectors with operational-scale workforces (BPO) produce geographic-concentration patterns. Sectors with substitutable-output spectrums (creative industries) produce skill-spectrum bifurcation patterns.

The four-interpretations revisited

Linking back to Essay 01’s four structural interpretations:

- Interpretation 1 (transition not arriving at scale) · weak fit for creative industries · 33% job-posting drop + 21% freelance-opportunity slash are substantial empirical displacement signals

- Interpretation 2 (transition arriving slowly with heterogeneous effects) · empirically dominant · the middle squeeze IS the heterogeneity signature on a skill-tier axis

- Interpretation 3 (transition arriving fast with structural alternatives unrecognized) · partial fit · the displacement is observably fast in commodity-tier creative work

- Interpretation 4 (transition arriving fast with structural alternatives operationally available) · partially supported · creative-platform cooperatives (Stocksy United) operationally tested but not at scale

The four-pattern integration confirms Interpretation 2 as empirically dominant across the four sector forensics, with each sector producing a structurally distinct manifestation of the same underlying interpretation. This is the structural finding Essay 06’s Phase 1 synthesis will crystallize.

Phase 1 progress · structural-empirical foundation complete

Four of six Phase 1 essays shipped. Four distinct structural-patterns identified. The empirical-evidence foundation for the Post-Labor Transition Atlas is structurally complete. Essay 06 (the Phase 1 synthesis) will integrate the four patterns into the cross-sector framework before Phase 2 (jurisdictional policy responses, July-August 2026) begins.

V · The closing argument · what the bifurcated reality crystallizes

The integrative observation Essay 05 produces for the Atlas framework. Creative industries is the bifurcated reality empirically confirmed — and the fourth distinct structural-pattern Phase 1 of the Atlas produces.

The empirical evidence crystallized:

- Graphic designer job postings -33% in 2025 · sustained through Q1 2026

- AI-collaboration job postings +340% 2023-2024 · the augmentation-tier emergence

- Content production roles -28% same period · the commodity-tier substitution

- 31% of designers use AI for core work (Figma) vs 59% of developers · the adoption gap is structurally significant

- Canva 44% creative AI tool market share · the commodity-substitution platform anchor

- Q1 2026 tech layoffs: 55,911 workers · 20.4% explicitly cite AI/automation

- Envato 2026 report: 1,780 creative professionals surveyed · bifurcation pattern confirmed

- 90% of content marketers plan to use AI for marketing in 2026 (+64.7% since 2023)

- 73% of marketing professionals use AI for content · only 12% rely fully on AI without human review

- JPMorgan + Persado 5-year deal · Coca-Cola custom GPT platform · canonical enterprise references

- Hartmann et al. 2025: AI advertising imagery rated more aesthetically appealing · quality/creativity/purchase-intention statistically indistinguishable

- Stock photo bimodal distribution: ~50% outperform humans by up to 50% CTR · ~50% underperform by up to 25%

- Hui et al. 2024 Organization Science (Brookings-cited): pronounced displacement effect on Upwork submarkets where required skills closely align with LLM functionalities

- AI slashed freelance job opportunities by 21% overall

- Goldberg and Lam 2025: GenAI substitutes for non-GenAI content, crowding out lower-quality creators · variety/quality/sales increase

The bifurcated reality finding:

- Top-tier creative work augments · brand strategy · art direction · AI-orchestration · signature work · 340% surge in AI-collaboration job postings

- Commodity-tier creative work substitutes · stock photography · routine copy · template design · routine translation · 33% graphic-design job-posting collapse

- Middle creative-professional tier faces structural compression · the “middle squeeze” pattern · 5-15 year experienced designers in routine commercial work face displacement that 5-15 year experienced designers in strategic positioning do not

The fifth attribution factor crystallized:

- Macroeconomic · same as prior sectors

- AI-tool maturation · Midjourney + Canva + Sora + Suno + DeepL + ChatGPT operationally substitutable in 2023-2025

- Cohort-specific compounding · structurally weaker here · skill-tier axis dominates over cohort axis

- Pyramid-model pressure · not structurally present

- Substitutable-output axis · the creative-industries-specific fifth factor · “good enough” threshold spectrum determines bifurcation

The four-pattern Phase 1 integration:

- Pattern 1 · cohort-bifurcation (Essay 02 · software engineering) · career-stage axis

- Pattern 2 · sub-sector heterogeneity (Essay 03 · white-collar professional services) · industry-vertical axis

- Pattern 3 · operational-scale displacement (Essay 04 · customer service + BPO) · geographic-and-operational axis

- Pattern 4 · creative-skill-spectrum bifurcation (this essay · creative industries) · creative-skill-spectrum axis

For the Atlas framework specifically:

- Creative industries produces the fourth distinct structural-pattern Phase 1 of the Atlas produces. The “middle squeeze” is empirically robust across five sub-fields documented (graphic design · copywriting · translation · stock photography · cross-cutting freelance platform evidence).

- The substitutable-output axis is the creative-industries-specific fifth attribution factor. The Atlas operates on sector-specific attribution rigor. Phase 1 has now produced five attribution factors across four sectors (three universal + pyramid-model in professional services + substitutable-output in creative industries).

- The four-pattern integration is the structural-empirical finding Phase 1 produces. “AI-driven labor displacement” is not a single phenomenon — it operates across four structurally distinct axes determined by sectoral characteristics. This is the analytical-discipline finding Essay 06 will crystallize.

- Interpretation 2 from Essay 01 (transition arriving slowly with heterogeneous effects) is empirically dominant across all four sector forensics, with each sector producing a structurally distinct manifestation. The heterogeneity itself is the structural signature of the post-labor transition as of mid-2026.

- Phase 1 is structurally complete after Essay 06. The empirical-evidence foundation for the Post-Labor Transition Atlas is established. Phase 2 (July-August 2026 · jurisdictional policy responses) operates on this foundation.

That’s the read on creative industries as the bifurcated reality empirically confirmed as of mid-May 2026. The work is real across creative industries. The displacement is substantial in commodity-tier creative work. The augmentation is substantial in strategic-tier creative work. The middle squeeze is the structural compression of the mid-tier. The “middle squeeze” is the fourth distinct structural-pattern Phase 1 of the Atlas produces — and the empirical signature of Interpretation 2 operating on a creative-skill-spectrum axis.

The Atlas framework’s Phase 1 empirical-evidence foundation is structurally complete. Four sector forensics have produced four distinct structural-patterns. The cohort-bifurcation hypothesis from Essays 02-03 is empirically important but not universal — Essays 04 and 05 produce structurally distinct patterns that the framework holds simultaneously. Essay 06 will crystallize the four-pattern integration as Phase 1’s synthesis finding before Phase 2’s jurisdictional policy responses begin in July 2026.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Reading · the Post-Labor Transition Atlas

- Atlas Essay 01 · The Atlas opening · what the framework is · four-dimension architecture · six chromatic registers · four structural interpretations

- Atlas Essay 02 · Software engineering · the canonical case · cohort-bifurcation Pattern 1 · empirical-clay register

- Atlas Essay 03 · White-collar professional services · the Tier 1 displacement · sub-sector heterogeneity Pattern 2 · labor-rose register

- Atlas Essay 04 · Customer service + BPO · the operational-scale displacement · operational-scale Pattern 3 · empirical-clay register

- This piece · Atlas Essay 05 · Creative industries · the bifurcated reality · Pattern 4 · labor-rose register

- Forthcoming · Atlas Essay 06 · Phase 1 synthesis · what the four sectors crystallize · synthesis-deep register

Sources

Graphic design + illustration empirical base

- Risk Quiz · Will AI Replace Graphic Designers? 2026 Risk Analysis · April 9, 2026 · graphic designer job postings -33% in 2025 · 31% designers use AI vs 59% developers · AI-collaboration postings +340% 2023-2024 · content production roles -28% · Canva 44% market share · Q1 2026 tech layoffs 55,911 workers · 20.4% cite AI/automation

- Upwork · Will AI Replace Graphic Designers? What To Know in 2026 · designer community perspective · “AI replaces mediocre designers” framing · human-made design as sought-after

- We and The Color · The Collapse of the Mid-Level Freelance Market Due to AI · Envato State of AI in Creative Work 2026 report (1,780 creative professionals) · “race to the bottom” qualitative evidence · “tweak the AI output” pattern · “rates haven’t moved · pipeline halved”

Copywriting empirical base

- Filthy Rich Writer · Is AI Taking Over Copywriting in 2026? · February 3, 2026 · JPMorgan + Persado 5-year deal · “AI is a support, not a solution” practitioner framing

- Click Forest · AI copywriting versus human creativity · 90% content marketers plan to use AI in 2026 (+64.7% since 2023) · 73% use AI for content · 12% rely fully on AI without human review (HubSpot)

- SEOwind · Will AI Replace Copywriters · Coca-Cola custom GPT platform · 40% concept-to-campaign reduction · 25% engagement increase · HubSpot 2024 AI Trends: 21% → 74% AI marketing adoption 2022-2023

- Mustard and Moxie · Why AI Can’t Replace Your Copywriter (Yet) · Google penalty on AI-generated content · search-engine quality signal as structural anchor

Stock photography + advertising imagery empirical base

- European Parliament study · The Economics of Copyright and AI · Hartmann et al. 2025 · AI advertising imagery rated more aesthetically appealing · quality/creativity/purchase-intention statistically indistinguishable · bimodal CTR distribution (50% outperform up to 50% · 50% underperform up to 25%)

Cross-cutting freelance platform empirical base

- Brookings · Is generative AI a job killer? Evidence from the freelance market · Hui et al. 2024 Organization Science paper · “High-skill workers with access to complementary tools may benefit, while mid-skill workers may be displaced or pushed into lower-paying jobs”

- arXiv · Generate the Future of Work through AI: Empirical Evidence from Online Labor Markets · Upwork dataset analysis · pronounced displacement effect in LLM-aligned submarkets · skill-transition effects · high-skilled freelancers disproportionately contribute to skill transitions

- Medium · Why AI Disruption Will End Freelancing as We Know It · July 2025 · AI slashed freelance job opportunities by 21%

- European Parliament study · Goldberg and Lam 2025 art platform finding · GenAI substitutes for non-GenAI content · crowding out lower-quality creators · variety/quality/sales increase

Key reference figures crystallized

- Graphic designer job postings · -33% in 2025

- AI-collaboration job postings · +340% between 2023 and 2024

- Content production roles · -28% same period

- Designer AI adoption · 31% (vs 59% developers) — Figma 2025 AI Report

- Creative AI tool market share · Canva 44% · Midjourney 13% · Jasper 12% · Runway 12%

- Q1 2026 tech layoffs · 55,911 workers · 736/day · 20.4% cite AI/automation

- Envato 2026 report · 1,780 creative professionals surveyed

- Content marketers AI plans 2026 · 90% (+64.7% since 2023)

- Marketing professionals AI usage · 73% for content · 12% rely fully on AI without human review (HubSpot)

- Content creators using AI · 94.5% worldwide

- HubSpot 2024 AI marketing adoption · 21% (2022) → 74% (2023)

- JPMorgan + Persado · 5-year deal for AI ad copy

- Coca-Cola custom GPT platform · 40% concept-to-campaign time reduction · 25% engagement increase

- Hartmann et al. 2025 · AI advertising imagery more aesthetically appealing · quality statistically indistinguishable

- Stock photo bimodal distribution · ~50% AI outperform humans by up to 50% CTR · ~50% underperform by up to 25%

- Hui et al. 2024 Organization Science · pronounced displacement effect in LLM-aligned Upwork submarkets

- AI freelance opportunity slash · 21% overall

- Goldberg and Lam 2025 art platform · GenAI substitutes for non-GenAI · crowds out lower-quality creators

- The “middle squeeze” pattern · top-tier augments · commodity substitutes · middle compresses

- Creative-skill-spectrum bifurcation · skill-tier axis distinct from cohort/sub-sector/operational axes

- Five attribution factors · macroeconomic + AI-tool + cohort-specific + pyramid (sector-specific) + substitutable-output (sector-specific to creative)

- Four-pattern Phase 1 integration · cohort-bifurcation + sub-sector heterogeneity + operational-scale + creative-skill-spectrum

- Interpretation 2 empirically dominant · across all four Phase 1 sector forensics