Thorsten Meyer | ThorstenMeyerAI.com | March 2026

Executive Summary

The largest debt-funded infrastructure buildout in history has an unpriced dependency on a noble gas.

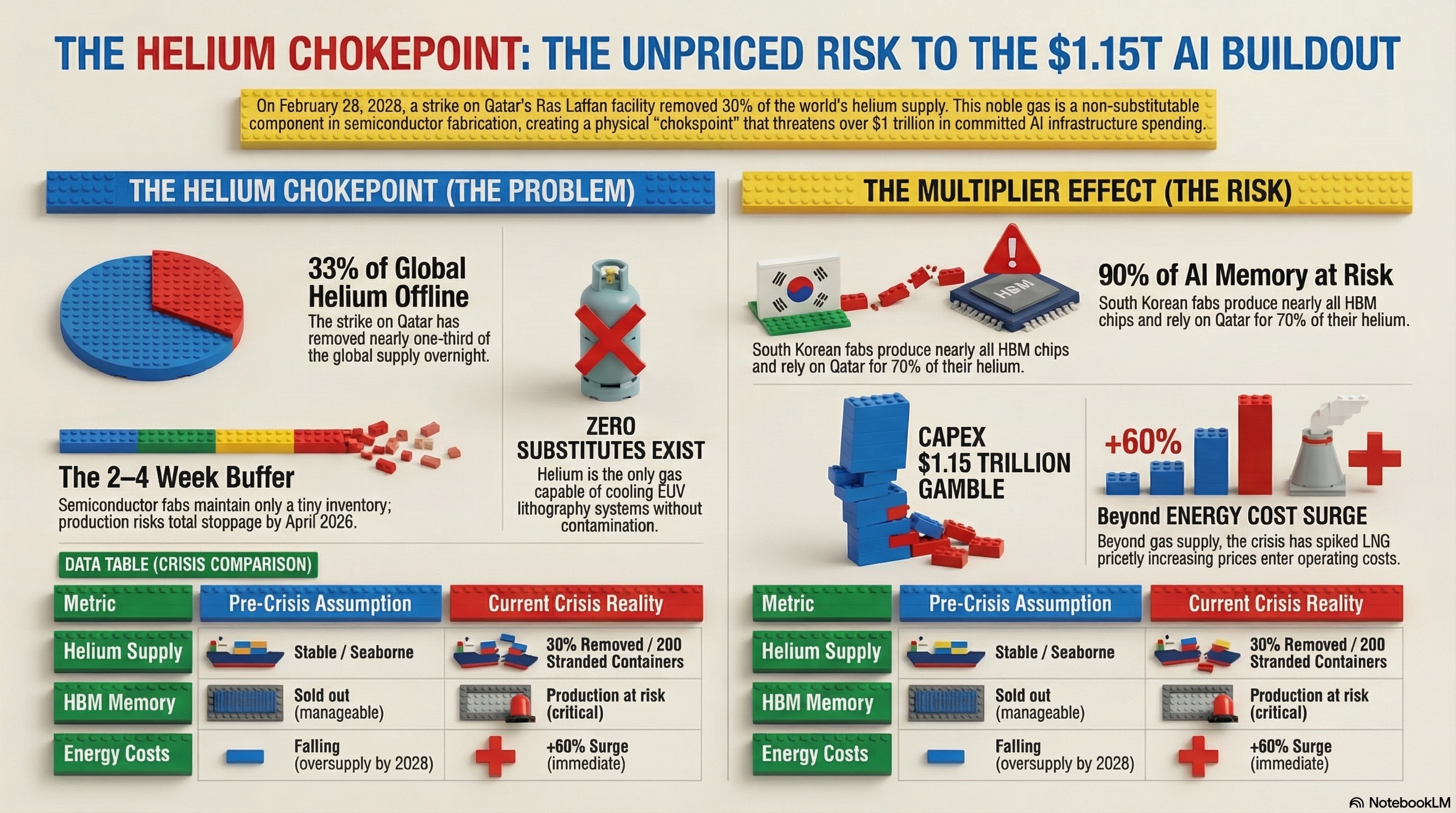

On February 28, 2026, Iranian drone strikes hit Qatar’s Ras Laffan industrial complex — the world’s largest liquefied natural gas facility and the source of over a third of the world’s helium. QatarGas declared force majeure. The Strait of Hormuz is effectively closed to Western commercial shipping. An estimated 27-30% of global helium supply has been removed from the market in weeks, not months. Spot helium prices surged 40-100% depending on the market. European LNG rose 60%.

The five largest US cloud and AI infrastructure providers have committed to spending between $500 billion and $602 billion on capital expenditure in 2026 alone. Seventy-five percent of it is AI infrastructure — approximately $450 billion in AI-specific spending. Goldman Sachs projects total hyperscaler capex from 2025 through 2027 will reach $1.15 trillion. Google’s co-founders Larry Page and Sergey Brin have reportedly said they would rather go bankrupt than lose the AI race.

Every dollar of that spending assumes the chips arrive on schedule. The chips come from fabs in South Korea and Taiwan. Those fabs require helium to operate their lithography machines, cool their wafers, and detect leaks in their vacuum chambers. There is no substitute for helium in any of these processes. Helium’s thermal conductivity is six times higher than nitrogen’s, and because it is inert, it will not react with anything inside the chamber. It is the only gas that can cool these systems without contaminating the process.

South Korea relies on Qatar for over 70% of its helium. Samsung and SK Hynix produce 90% of global High Bandwidth Memory — the component that has already been sold out through 2026. SK Hynix’s CFO stated the company has “already sold out our entire 2026 HBM supply.” DRAM prices have surged 50% year to date. DDR5 contract pricing has risen more than 100%. And now the helium that these fabs need to maintain production is disappearing from the market.

The specialized containers that carry liquid helium — ISO containers cooled to -269 degrees Celsius — vaporize their contents within 48 days. Two hundred of them are stranded near the Strait of Hormuz. The clock is already running.

| Metric | Value |

|---|---|

| Qatar helium share (global) | 33% (27-30% removed) |

| Ras Laffan strike date | February 28, 2026 |

| Strait of Hormuz | Closed to Western shipping |

| Spot helium price surge | 40-100% |

| European LNG surge | 60% |

| Helium containers stranded | ~200 near Hormuz |

| Container vaporization window | 48 days |

| Hyperscaler capex (2026) | $500-602 billion |

| AI-specific capex | ~$450 billion (75%) |

| Hyperscaler capex (2025-2027) | $1.15 trillion (Goldman) |

| Capital intensity | 45-57% of revenue |

| S. Korea helium from Qatar | >70% |

| Taiwan helium from Qatar | ~30% |

| Samsung + SK Hynix HBM share | 90% global |

| HBM supply (2026) | Sold out (SK Hynix CFO) |

| DRAM price surge (YTD) | +50% |

| DDR5 contract price surge | +100% |

| Samsung 32GB DDR5 price | $149 → $239 (+60%) |

| Semiconductor helium use | 24% of global (→30% by 2030) |

| Fab helium inventory buffer | 2-4 weeks |

| AI data center power (US) | 176 TWh (4.4% of total) |

| Russian pipeline gas vs. LNG | ~33% cheaper |

| OECD unemployment | 5.0% (stable) |

| OECD broadband (advanced) | 98.9% |

Bonvoisin 3L Liquid Nitrogen Container, LN2 Tank Cryogenic Dewar, Aluminum Alloy Semen Tank with 6 Canisters Carry Bag

- Multi-purpose Storage: Stores semen, embryos, cells, and dry ice

- Durable & Safe Construction: Made from high-grade aeronautical aluminum with vacuum insulation

- Includes 6 Canisters: 6 stainless steel canisters for sample storage and retrieval

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

1. The Three Channels: How a Missile Strike Reaches a GPU Cluster

A missile strike on a gas facility in Qatar reaches the GPU clusters training the next generation of AI models through three distinct channels — each reinforcing the others.

Channel 1: Helium Supply

| Element | Data | Timeline |

|---|---|---|

| Qatar helium share | 33% of global supply | Offline since Feb 28 |

| Supply removed | 27-30% of global market | Immediate |

| Price surge | 40-100% spot | Within weeks |

| S. Korea dependence | >70% from Qatar | Critical exposure |

| Taiwan dependence | ~30% from Qatar | Moderate exposure |

| Fab inventory buffer | 2-4 weeks | Clock running |

| Stranded containers | ~200 near Hormuz | 48-day vaporization |

| Alternative sources | US (BLM reserves depleted), Algeria, Russia, Australia | Months to ramp |

| Substitute gas | None for EUV cooling, leak detection | No mitigation path |

When helium supply tightens at the fab level, defect rates rise, cost per good die increases, and output falls. The semiconductor industry accounts for 24% of global helium consumption — projected to reach 30% by 2030. Fabs maintain only 2-4 week inventory buffers for helium, compared to 8-12 weeks for other bulk gases. The buffer window is already closing.

Channel 2: LNG Energy Costs

| Element | Data | Timeline |

|---|---|---|

| European LNG price | +60% since Hormuz closure | Immediate |

| Qatar LNG share | World’s 2nd largest exporter | Offline |

| AI data center power (US) | 176 TWh / 4.4% of national | Growing |

| Data center demand growth | Doubling 2022-2026 | Accelerating |

| Energy cost lag to data centers | 4-8 weeks | April-May 2026 |

| LNG expansion (pre-conflict) | Expected to lower costs by 2028 | Now delayed |

Qatar is the world’s second-largest LNG exporter. Its shutdown removes supply from a market that was already tight due to AI data center demand. The LNG expansion wave that was expected to bring energy costs down by 2028 is now facing delays. Data centers running on gas-fired power will see energy cost increases materialize in April to May 2026.

Channel 3: Geopolitical Restructuring

| Element | Data | Implication |

|---|---|---|

| Russian pipeline gas to China | ~33% cheaper than LNG | Structural energy advantage |

| Power of Siberia 2 | Central route in China 2026-2030 plan | Decade-long cheap energy |

| China domestic helium | Investing in extraction capacity | Reducing external dependency |

| US helium reserves (BLM) | Depleted / privatized | Cannot backfill Qatar loss |

| South Korea/Taiwan fabs | Dependent on seaborne helium | Vulnerable to maritime disruption |

Russia-to-China pipeline gas is approximately one-third the cost of contracted LNG and less than half the cost of spot LNG. China’s 2026-2030 development blueprint explicitly advances Power of Siberia 2 pipeline preparatory work. If China secures discounted Russian pipeline energy while Western-allied fabs face LNG cost surges and helium shortages, Chinese semiconductor manufacturing gains a structural cost advantage that could persist for a decade.

“The missile did not hit a chip factory. It hit the gas facility that supplies the gas that the chip factories cannot operate without. Three channels — helium supply, LNG energy costs, and geopolitical restructuring — converge on a single point: the physical substrate of AI.”

Pipe Leak Detection He/Helium Gas Detector Alarm, Gas Analyzer with Gooseneck Probe and Curve Display S311

- Detection Method: Pump suction or natural diffusion

- Detected Gases: Combustible, toxic, harmful gases

- Detection Principle: Electrochemistry, Semiconductor, Catalysis

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

2. The Memory Compounding Effect

The helium disruption arrives at the worst possible moment — into a semiconductor supply chain already in the grip of the most severe memory shortage in industry history.

The Memory Crisis Before Helium

| Signal | Data | Source |

|---|---|---|

| HBM supply (2026) | Sold out | SK Hynix CFO |

| Samsung + SK Hynix HBM share | 90% of global | TrendForce |

| HBM3E price hike | +20% for 2026 | Samsung/SK Hynix |

| DRAM price surge (YTD) | +50% | Market data |

| DDR5 contract price | +100% | Industry reports |

| Samsung 32GB DDR5 | $149 → $239 (+60%) | Samsung |

| NVIDIA RTX 50 production | -30-40% (GDDR7 shortage) | Industry reports |

| HBM TAM by 2028 | $100 billion | Industry projections |

| Memory shortage duration | Through 2026, possibly 2027 | IDC |

The Compounding Mechanism

| Layer | Pre-Helium Crisis | Post-Helium Crisis |

|---|---|---|

| HBM supply | Sold out through 2026 | Production at risk if helium tightens |

| DRAM pricing | +50% YTD, +100% DDR5 | Further price pressure from supply disruption |

| Fab operations | Running at capacity | Defect rates rise; yield drops with helium scarcity |

| GPU production | NVIDIA cutting 30-40% | Additional constraint on memory-intensive AI chips |

| AI infrastructure | $450B committed spending | Chips may not arrive on schedule |

| Delivery timeline | Tight but manageable | 2-4 week helium buffer = hard constraint |

Samsung and SK Hynix have been pivoting limited cleanroom space and capex toward higher-margin HBM for hyperscalers — Microsoft, Google, Meta, Amazon. This pivot already created shortages for consumer DRAM and GDDR7. Now the helium constraint threatens the HBM production itself. The fabs that are sole-source for 90% of global HBM are also the fabs most dependent on Qatari helium.

What Air Liquide Is Doing

Air Liquide has opened a new facility in Taiwan for helium purification and recycling — a sign that the industry recognizes the structural vulnerability. But recycling recovers only a fraction of helium used in fab processes, and new purification capacity takes months to ramp.

“HBM is sold out. DRAM is up 50%. DDR5 is up 100%. And now the helium that these fabs need to maintain production is disappearing. The compounding effect is not additive. It is multiplicative.”

Miller Electric Silverline Series High Purity Gas Regulator 0 to 15 psi, 2", Inert Argon, Helium, Nitrogen (220-4109)

- Regulator Type: Two-stage, high purity, high pressure

- Series: Silver Line

- Gas Compatibility: Argon, Helium, Nitrogen

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

3. The Energy Asymmetry

The countries that fabricate the chips are not the countries that run the data centers. This creates an energy asymmetry that the Qatar crisis has made acute.

The Asymmetry Map

| Function | Location | Energy Source | Qatar Exposure |

|---|---|---|---|

| Chip fabrication | South Korea, Taiwan | Imported LNG + nuclear + renewables | High (helium + LNG) |

| AI model training | US (primarily) | Natural gas + renewables + nuclear | Moderate (LNG price) |

| AI inference | US, EU, Asia | Mixed | Varies |

| Helium production | Qatar (offline), US, Algeria, Russia | Byproduct of gas processing | Direct |

| Russian pipeline gas | Russia → China | Pipeline (not seaborne) | Zero (landlocked) |

The LNG Oversupply That Evaporated

Before the Qatar crisis, analysts projected an LNG supply glut by 2028 as new export terminals in the US, Mozambique, and Qatar came online. Qatar’s own North Field expansion was the largest single LNG project in history. That expansion is now indefinitely paused. The oversupply thesis — which was supposed to make energy cheap for data centers — has collapsed.

| Pre-Crisis Assumption | Post-Crisis Reality |

|---|---|

| LNG oversupply by 2028 | Qatar expansion paused; timeline unknown |

| Falling energy costs for data centers | European LNG +60%; costs rising |

| Energy as minor input cost | Energy becoming strategic constraint |

| Seaborne LNG as reliable supply | Hormuz closure demonstrated fragility |

| Pipeline gas as Russian weapon | Pipeline gas as Chinese advantage |

The China Energy Advantage

| Factor | Western Fabs | Chinese Fabs |

|---|---|---|

| Energy source | Seaborne LNG (spot market) | Pipeline gas (contracted, discounted) |

| Energy cost | +60% and rising | Stable or declining |

| Supply security | Vulnerable to maritime disruption | Landlocked pipeline (not interruptible) |

| Helium access | Seaborne (Hormuz-dependent) | Domestic investment + Russian supply |

| Duration of advantage | Until Hormuz reopens + LNG normalizes | Structural (pipeline = permanent infra) |

“The LNG expansion that was supposed to make energy cheap by 2028 is not coming on time. The countries that fabricate the chips run on imported LNG. The country that could benefit most runs on pipeline gas. The asymmetry is structural.”

As an affiliate, we earn on qualifying purchases.

4. OECD Context: The Physical Substrate of Digital Infrastructure

OECD data on digital infrastructure readiness — 98.9% broadband penetration, 5.0% unemployment, universal connectivity — assumes the physical substrate of computation remains available. The Qatar crisis reveals that this assumption is fragile.

Where the Physical Constraints Are

| Factor | Data | Implication |

|---|---|---|

| Broadband | 98.9% (advanced) | Digital infra ready; physical substrate at risk |

| Unemployment | 5.0% (stable) | Labour market healthy; compute supply uncertain |

| Youth | 11.2% | AI adoption dependent on chip availability |

| Helium removed | 27-30% of global | Fab operations at risk within weeks |

| S. Korea dependence | >70% from Qatar | Highest-risk OECD member for fab disruption |

| HBM sold out | Through 2026 | Memory cannot absorb any production loss |

| Hyperscaler capex | $500-602B (2026) | $1.15T committed without helium risk pricing |

| DRAM surge | +50% YTD | Cost pressure already acute before helium |

| LNG surge | +60% EU | Energy costs compounding chip costs |

| Fab buffer | 2-4 weeks helium | Hard constraint approaching |

The Unpriced Risk

| Risk | Who Bears It | Current Pricing |

|---|---|---|

| Helium supply disruption | Fabs (Samsung, SK Hynix, TSMC) | Not in chip contracts |

| LNG price surge | Data center operators | 4-8 week lag to cost recognition |

| HBM production loss | Hyperscalers (MSFT, GOOG, META, AMZN) | Not in capex forecasts |

| Maritime chokepoint | All seaborne supply chains | Assumed open in planning |

| Geopolitical restructuring | Western tech ecosystem | Not modeled in AI buildout projections |

Transparency note: OECD does not directly measure helium supply chain dependencies, semiconductor fab gas inventories, or LNG-to-compute cost transmission. The indicators combine OECD infrastructure data with commodity market analyses, semiconductor industry reports, and geopolitical assessments.

5. Practical Actions for Leaders

1. Map your AI infrastructure plan’s physical substrate dependencies. Every chip in your data center roadmap passed through a fab that requires helium. Identify which chip suppliers depend on South Korean or Taiwanese fabs, what their helium inventory buffers are, and what your contractual exposure is if delivery timelines slip. If your infrastructure plan does not include a helium risk line item, add one.

2. Scenario-model a 3-6 month chip delivery delay. If helium constraints reduce fab output by even 5-10%, the ripple effect through an already sold-out HBM supply chain could delay AI infrastructure deployment by quarters, not weeks. Model what happens to your AI roadmap if GPU and memory deliveries slip by 3 months, 6 months, or longer. Price the delay.

3. Evaluate energy cost exposure from LNG disruption. If your data centers run on gas-fired power, the 60% LNG price surge will reach your operating costs in April-May 2026. Model the impact on inference costs, training budgets, and total cost of ownership. Consider whether power purchase agreements or renewable energy contracts provide insulation.

4. Track the geopolitical restructuring as a competitive intelligence issue. Russia-to-China pipeline gas creates a structural energy cost advantage for Chinese semiconductor and AI infrastructure. This is not a temporary disruption — it is a decade-long competitive asymmetry. Factor this into strategic planning for compute sourcing, chip supply diversification, and AI infrastructure geography.

5. Diversify helium and memory supply chain exposure. Engage directly with chip suppliers on their helium sourcing. Evaluate Air Liquide’s Taiwan recycling capacity, US helium sources (declining), and Australian/Algerian alternatives. For memory, explore whether Micron (US-based) offers partial hedge against South Korean helium dependency.

| Action | Owner | Timeline |

|---|---|---|

| Physical substrate audit | CTO + Supply Chain | Immediate |

| Chip delay scenario modeling | CFO + CTO | Q2 2026 |

| Energy cost exposure analysis | CFO + Ops | April 2026 |

| Geopolitical competitive intelligence | Strategy + Gov Rel | Q2 2026 |

| Supply chain diversification | CTO + Procurement | Q2 2026 |

The Honest Pushback

Five counterarguments to this thesis, addressed directly.

| Counterargument | Response |

|---|---|

| “Helium recycling can fill the gap” | Recycling recovers only a fraction. Air Liquide’s Taiwan facility is a start, not a solution. Scaling takes months. The buffer is 2-4 weeks. |

| “US helium reserves can backfill” | BLM helium reserves have been depleted and privatized. US production is declining, not expanding. It cannot replace 30% of global supply. |

| “SEMI says no chip shortage yet” | SEMI’s March 19 statement noted existing pipelines are adequate — for now. The 2-4 week buffer means the constraint hits in April if not resolved. |

| “China also needs helium for its fabs” | True, but China is investing in domestic helium extraction and has access to Russian supply. The asymmetry is in trajectory, not current state. |

| “The conflict will resolve quickly” | Even if Hormuz reopens tomorrow, the 200 stranded containers have been vaporizing for weeks. Ras Laffan is partially destroyed. Rebuild timelines are measured in months to years. |

What to Watch

The April buffer window. Asian fabs have approximately 2-4 weeks of helium inventory. By early-to-mid April, if no alternative supply is secured, production disruptions become visible. Watch for Samsung and SK Hynix announcements on production adjustments, yield impacts, or allocation changes.

HBM allocation decisions under helium constraint. If fabs must ration helium, they will prioritize their highest-margin products — HBM for hyperscalers. This means consumer DRAM, GDDR7 for gaming GPUs, and lower-margin enterprise memory face the deepest cuts. The triage decisions made in April-May will determine who gets AI chips and who does not.

The Hormuz reopening timeline as a macro signal. If the Strait of Hormuz remains closed through Q2 2026, the helium crisis becomes a semiconductor production crisis. If it reopens, the immediate pressure eases — but the stranded containers, destroyed infrastructure, and demonstrated fragility permanently reprice the risk.

The Bottom Line

33% of helium supply offline. 27-30% removed from market. 40-100% price surge. 200 containers stranded. 48-day vaporization window. >70% South Korean dependence on Qatar. 90% of HBM from South Korea. Sold out through 2026. +50% DRAM YTD. +100% DDR5. +60% European LNG. $500-602B hyperscaler capex. $1.15T three-year commitment. 2-4 week fab buffer. Zero substitutes for helium in EUV lithography.

The $1.15 trillion AI infrastructure buildout did not price in a noble gas dependency. The noble gas just went offline. The specialized containers are vaporizing. The fabs have 2-4 weeks of buffer. The memory is already sold out. The energy costs are already rising. And the geopolitical restructuring favors the competitor.

Every AI infrastructure plan in the world just acquired an unplanned dependency on a gas that most planners did not know existed in their supply chain. That gap between assumption and reality is where the next quarter’s earnings surprises — and the next year’s competitive restructuring — will live.

Your AI infrastructure plan assumes the chips arrive on schedule. The chips require helium. The helium is offline. The containers are vaporizing. The clock is running. Update your plan.

Thorsten Meyer is an AI strategy advisor who notes that “no substitute for helium in EUV lithography” is the kind of sentence that sounds like a chemistry fact until it becomes a $1.15 trillion infrastructure risk — and that the phrase “force majeure” has never been more literally about force. More at ThorstenMeyerAI.com.

Sources

- Qatar / Ras Laffan — Iranian Drone Strike Feb 28, 2026; Force Majeure Declared

- Fortune — “Iran War Cuts Off Helium From Qatar; Shortages Will Bite in Weeks” (Mar 2026)

- Tom’s Hardware — “Qatar Helium Shutdown Puts Chip Supply on 2-Week Clock” (Mar 2026)

- CNBC — “Tech Stocks: Qatar Attack, Semiconductor Supply Chain, LNG, Helium” (Mar 2026)

- TrendForce — “Helium Crunch Hits South Korea Harder: Samsung, SK Hynix, TSMC” (Mar 2026)

- HPCwire — “Global Helium Shortage Constrains High-Density Compute” (Mar 2026)

- J2 Sourcing — “Global Helium Crisis: Semiconductor Manufacturing Impact” (2026)

- Frost & Sullivan — “Helium as New Chokepoint in Semiconductor Supply Chain” (2026)

- Air Liquide — Taiwan Helium Purification/Recycling Facility Opening (Mar 2026)

- Goldman Sachs — Hyperscaler Capex: $1.15T (2025-2027); $500B+ in 2026

- IDC — Global Memory Shortage Crisis: Impact on AI, Smartphone, PC Markets (2026)

- Samsung — DDR5 Price Surge: $149→$239; Memory Shortage Warning

- SK Hynix — “Entire 2026 HBM Supply Sold Out” (CFO Statement)

- AGBI — “Qatari LNG Shutdown Puts 11% of Global Helium at Risk” (Mar 2026)

- Caixin Global — “Qatar Helium Shutdown Adds Risk to Chip Supply Chain” (Mar 2026)

- Abhishek Gautam — “Hormuz Closure: LNG +60%, AI Compute More Expensive” (2026)

- Atlantic Council / China 2026-2030 — Power of Siberia 2 Pipeline; Russian Gas 33% Cheaper

- OECD — 5.0% Unemployment, 11.2% Youth, 98.9% Broadband

© 2026 Thorsten Meyer. All rights reserved. ThorstenMeyerAI.com