By Thorsten Meyer — May 2026

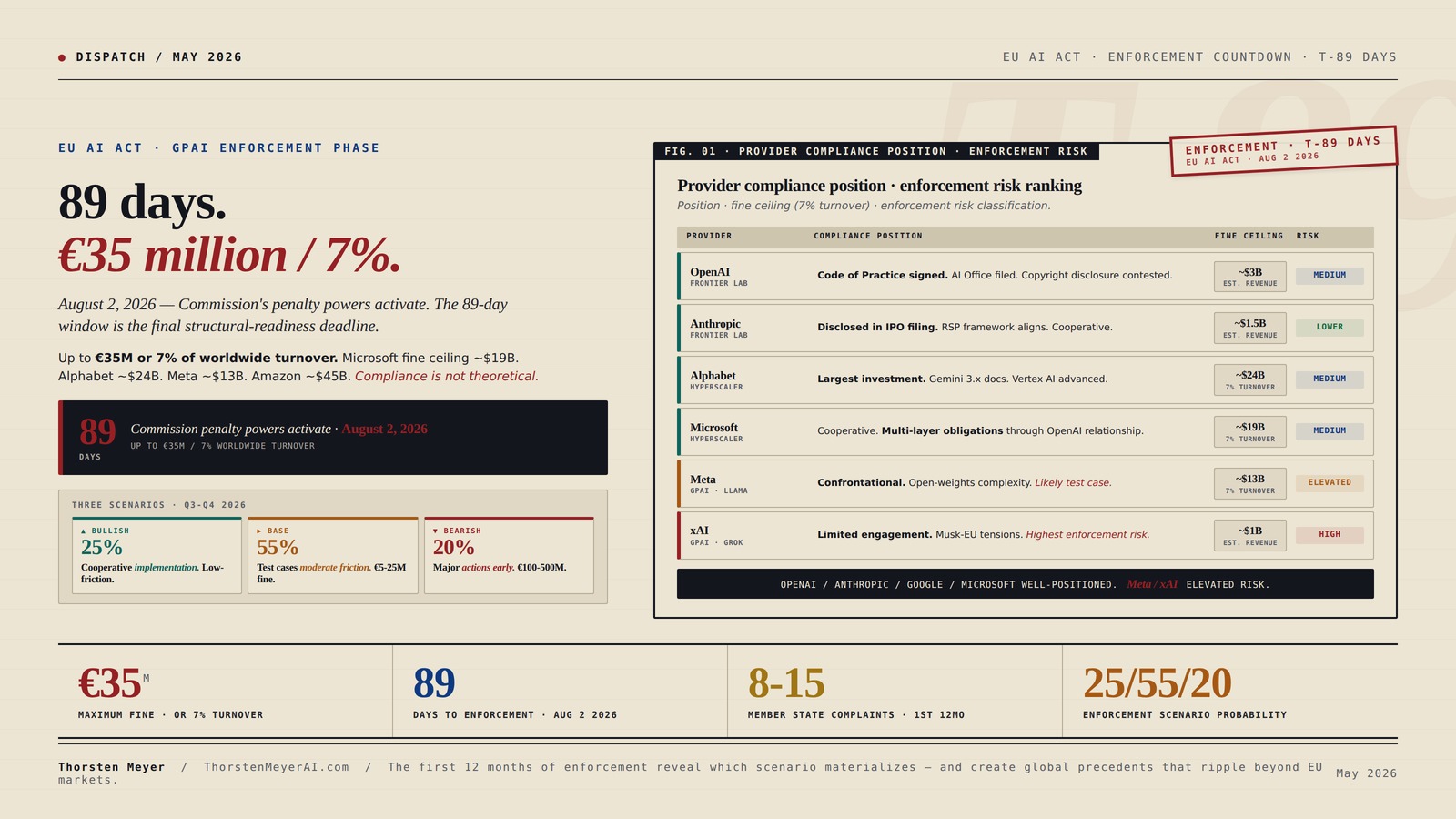

August 2, 2026 — exactly eighty-nine days from publication of this dispatch — the European Commission’s enforcement powers under the EU AI Act enter into application against providers of general-purpose AI (GPAI) models. The Commission gains the power to request documentation and information, conduct evaluations, request compliance and risk-mitigation measures, request market restriction, recall, or withdrawal, and impose fines. The maximum fine is €35 million or 7 percent of annual worldwide turnover, whichever is higher. For Microsoft, the upside-of-fine bound is approximately $19 billion. For Alphabet, ~$24 billion. For Meta, ~$13 billion. For Amazon, ~$45 billion. For OpenAI as a private company, scaled to revenue, $1.5-3 billion. For Anthropic, $0.8-1.5 billion. The numbers are not theoretical — they are the structural ceiling on penalties starting August 2.

Most analysis of the EU AI Act has focused on the regulation’s substantive content. The structural reality through Q3-Q4 2026 is different: enforcement infrastructure has been operating since August 2025 (AI Office established, GPAI obligations in force), but the Commission’s penalty powers come online August 2, 2026. The 89-day window between now and then is the structural compliance-readiness deadline for every AI lab, hyperscaler, and downstream deployer with EU exposure. The companies that have been treating EU compliance as a forward priority versus those treating it as an immediate enforcement risk are about to be sorted into different cohorts.

This dispatch is the structural read on enforcement Q3-Q4 2026. The compliance position of major providers as of May 2026. What enforcement actions are most likely in the first 6-12 months of penalty authority. The strategic implications for AI labs, hyperscalers, downstream deployers, and customers in EU markets. How the enforcement window connects to the broader threads from this dispatch series.

The dispatch on the EU AI Sovereignty dispatch covered the policy framework and the geographic positioning. The dispatch on the Anthropic IPO disclosure covered explicit margin-compression risk from EU compliance. The dispatch on the bubble question covered the specific frontier-lab valuation considerations that EU enforcement could affect. Q3-Q4 2026 EU enforcement is the empirical test of how regulatory risk converts to operational reality.

89 days.

€35 million / 7%.

August 2, 2026 — Commission’s penalty powers activate. The 89-day window is the final structural-readiness deadline.

Up to €35M or 7% of worldwide turnover — whichever is higher. Microsoft fine ceiling ~$19B. Alphabet ~$24B. Meta ~$13B. Amazon ~$45B. Compliance is not theoretical. OpenAI signed Code of Practice. Anthropic disclosed in IPO filing. Meta + xAI face elevated risk. The 89-day window is the structural compliance deadline.

worldwide turnover

Nine phases. One structural threshold.

Substantive obligations have been progressively activating through 2025-2026. August 2, 2026 is the structural shift from “EU AI Act exists” to “EU AI Act enforcement is active.”

EU AI Act for Non-EU Companies: A Practical Market-Access Guide for US, UK, Canadian, and Global Businesses Selling AI Products, Software, or Services … (EU AI Act Practical Compliance Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Eight providers. Non-uniform exposure.

Compliance positions are non-uniform across major providers. The first 12 months of enforcement reveal which providers face the deepest scrutiny.

AI Prompts for Medical Device Compliance: A Practical Handbook for Regulatory Affairs, Quality Systems, and Risk Management Professionals

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios. One year of enforcement.

25/55/20 probability. Base scenario most likely because AI Office signaled cooperative intent, providers invested in compliance, and first year of authority typically produces moderate enforcement.

- Documentation phase onlyFew high-profile actions.

- No early finesCompliance commitments resolve.

- Cooperative classificationAnnex III ambiguity worked through.

- Limited margin impactEU compliance ~3-5% overhead.

- Outcome: EU AI Act operational but doesn’t materially affect economics.

- 1-3 doc-driven actions5-10 Member State complaints.

- First fine €5-25MxAI most likely · Meta secondary.

- Annex III disputeFormal proceedings, resolved.

- 5-10% EU overheadMaterial but absorbable.

- Outcome: Modest valuation compression. Frontier-lab base case.

- Major fine €100-500MTop-tier provider.

- Market restrictionFrontier-tier model.

- 15-25% EU overheadMaterial cost cascade.

- Frontier-lab valuation hitEU-specific compression.

- Outcome: Multi-year recovery. Bubble bear case gains evidence.

EU enforcement activation is not a discrete regulatory event. It is the operational reality that determines whether the AI cycle’s structural risks compound or remain bounded. The first 12 months of enforcement reveal which scenario materializes — and create global precedents that ripple beyond EU markets.

AI Compliance Checklist: Self-Assessment Tool for EU AI Act, ISO 42001 & NIST AI RMF — Ready-to-Use Frameworks (AI Compliance Toolkit Book 1)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Complete substantive compliance now.

Documentation, AI Office collaboration channels active, required notifications filed. Treat 89-day window as final readiness deadline before active enforcement authority begins. The structural goal: avoid being the high-profile enforcement test case in the first 12 months. OpenAI / Anthropic / Google / Microsoft well-positioned; Meta / xAI face elevated risk.

Invest in downstream compliance support.

Compliance through cloud-AI services (Azure OpenAI, Vertex AI, Bedrock) is multi-layer complex. The provider that makes EU compliance easiest for enterprise customers captures durable share. Compliance support investment is structural competitive moat — not just cost center.

Plan deployment timing strategically.

August 2, 2026 changes regulatory calculus for new deployments. Pre-August deployments get more favorable carve-outs in many cases. Pre-position accordingly. Multi-vendor sourcing reduces single-vendor compliance failure exposure. The 89-day window is structural deployment-timing optimization opportunity.

Update forward-risk models.

Differentiate on compliance investment quality. xAI / Meta-Llama-deployers face highest enforcement risk; OpenAI / Anthropic / Google / Microsoft face manageable risk. Anthropic IPO disclosure framework provides useful precedent — explicit risk acknowledgment combined with active compliance investment positions favorably.

AI Engineering: Building Applications with Foundation Models

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive Summary · The Enforcement Picture in One Table

| Date | Event | Status today | Enforcement implication |

|---|---|---|---|

| Feb 2, 2025 | Prohibited practices + AI literacy | In force | Already actionable; some compliance gaps remain |

| Aug 2, 2025 | GPAI model obligations | In force | Substantive compliance required; no penalties yet |

| Aug 2, 2025 | AI Office operational | Active | Documentation requests possible; informal collaboration |

| Aug 2, 2025 | Member State penalty rules deadline | Largely complete | National frameworks exist for non-GPAI |

| May 6, 2026 | T-89 days to Commission enforcement | Today | Final compliance window opens |

| Aug 2, 2026 | Commission enforcement powers / GPAI fines | 89 days | Up to €35M / 7% turnover penalty authority active |

| Aug 2, 2026 | Annex III high-risk system obligations | 89 days | Articles 8-15 compliance for new deployments |

| Aug 2, 2027 | Pre-existing GPAI compliance deadline | +1 year | Models on market before Aug 2025 must comply |

| Dec 31, 2030 | Large-scale IT systems compliance | +4 years | Annex X systems compliance deadline |

The structural reality is that enforcement is not a future event. Substantive obligations have been actionable since February 2025 and August 2025. What changes August 2, 2026 is the Commission’s ability to impose penalties for GPAI provider non-compliance and the activation of compliance-intensive Annex III high-risk requirements. The 89-day window is the structural compliance-readiness deadline. After that, every major AI provider with EU exposure is operating under active penalty authority for the first time.

1. What August 2, 2026 actually changes

The substantive provisions of the EU AI Act have been progressively activating through 2025-2026. August 2, 2026 changes the enforcement landscape in three structural ways.

Change 1 · Commission penalty powers activate for GPAI providers. Since August 2, 2025, providers of GPAI models have been subject to substantive obligations under Chapter V of the AI Act. Documentation, risk assessment, copyright compliance, transparency obligations, technical documentation. Compliance has been required, but the Commission’s ability to impose penalties for non-compliance has been suspended for a one-year adjustment period. August 2, 2026 ends the adjustment period. Penalties up to €35M or 7 percent of worldwide turnover become available. The structural significance: providers that have been deferring full compliance can no longer do so without penalty exposure.

Change 2 · Annex III high-risk system obligations become enforceable. Articles 8-15 of the AI Act establish requirements for high-risk AI systems: risk management, data governance, technical documentation, automatic logging, transparency, human oversight, accuracy and robustness. These obligations apply broadly across systems used in employment, education, essential services, law enforcement, migration, justice, biometric categorization, and other Annex III categories. August 2, 2026 is the date these obligations apply to systems placed on the market after that date. Existing systems get a carve-out unless they undergo “significant design changes,” which is a broad definition that effectively forces compliance for any meaningfully updated system.

Change 3 · Article 50 transparency obligations broaden. Article 50 requires transparency for AI-generated or AI-manipulated content. Synthetic content must be labeled in a machine-readable and detectable way where technically feasible. Deepfakes and public-interest text require user notification. Emotion recognition and biometric categorization require informed-user notice. The transparency provisions apply to providers and deployers, creating a multi-layer compliance obligation. August 2, 2026 is the structural enforcement date.

The combined effect: a structural shift from “EU AI Act exists and creates obligations” to “EU AI Act enforcement is active and penalties are real.” The behavior change in Q3-Q4 2026 will be observable. Compliance investment that had been treated as “important but not urgent” through 2025 becomes “urgent and material” in the 89-day window.

2. Where each major provider stands on compliance

The compliance position of major AI providers as of May 2026 is non-uniform.

OpenAI. Has signed the EU AI Act Code of Practice, signaling cooperative engagement with the AI Office. Substantive compliance documentation is partially complete. Notification to the AI Office for systemic-risk models has been filed. Public commitments to ongoing collaboration. OpenAI’s structural position: relatively well-prepared on documentation and procedural compliance; substantive risk remains around copyright training-data disclosure (the most contested compliance area) and around model evaluation methodologies that satisfy the AI Office’s interpretation of “systemic risk.” The structural risk: copyright disclosure could trigger enforcement action if implementation falls short of regulatory interpretation.

Anthropic. Has filed required notifications. Public commitments to compliance. Structural position: similar to OpenAI on documentation, with the additional structural advantage of constitutional AI / Responsible Scaling Policy framework that aligns with several AI Act compliance themes (transparency, risk management, human oversight). The Anthropic IPO disclosure explicitly flagged EU regulatory risk as forward-risk factor — Anthropic has been treating compliance as material from the disclosure perspective.

Google (Alphabet). Has the largest substantive compliance investment among hyperscalers given European market exposure. Gemini 3.x compliance documentation appears comprehensive based on public signals. Vertex AI / Google Cloud compliance for downstream deployers appears advanced. Structural position: well-prepared, but exposure is broader given multi-product surface area and biometric categorization adjacencies (Photos, YouTube, advertising) that may trigger Annex III high-risk classifications.

Microsoft. Compliance through Azure OpenAI Service is the binding question. Microsoft has substantial enterprise customer relationships in EU markets, which makes downstream-provider compliance obligations material. Public commitment to collaborate with AI Office. Structural position: well-resourced for compliance investment but faces compliance complexity through the OpenAI relationship (which models are licensed, how downstream deployment works, how the joint Azure OpenAI Service satisfies dual-provider obligations).

Meta. Has been more confrontational with EU regulation historically. Llama (open-source model) compliance question is structurally complex — open-source GPAI providers face specific obligations that interact with the open-weights distribution model. Structural position: less aligned with EU regulatory framework than other providers, larger probability of becoming an early enforcement test case if compliance gaps emerge.

xAI. Limited public engagement with EU compliance framework. Grok deployment in EU markets is relatively new. Structural position: highest enforcement risk among major providers given limited apparent compliance investment and the political backdrop of Elon Musk’s broader European tensions.

Mistral / Aleph Alpha / Stability / European players. Sovereign positioning provides political cover but does not exempt from compliance. European players have been more visibly cooperative with the AI Office. Structural position: lower enforcement risk through political alignment plus substantive compliance investment, though resource constraints relative to US peers create different operational challenges.

Chinese providers (DeepSeek, Alibaba Cloud, Tencent). EU access is constrained but not prohibited. Structural position: enforcement is implausible against providers with limited EU presence; market access is the binding question rather than penalty exposure.

The non-uniform compliance landscape implies non-uniform enforcement risk. Providers with strong compliance investment and cooperative engagement (OpenAI signed, Anthropic disclosed, Google/Alphabet resourced) face lower enforcement probability. Providers with limited engagement (xAI most acute, Meta secondary) face higher probability of becoming early enforcement test cases.

3. The first 6-12 months · what enforcement actually looks like

Predicting specific enforcement actions in 2026-2027 requires understanding the AI Office’s likely operational pattern.

Pattern 1 · Documentation requests precede penalties. The first wave of enforcement activity will likely be Article 91 documentation requests. The Commission asks providers for technical documentation, risk assessments, copyright disclosure, evaluation methodologies. Failure to provide adequate documentation can trigger Commission compliance demands; persistent failure triggers fines. Expect documentation requests to begin in the first 60-120 days after August 2, 2026 against multiple providers. The volume and granularity of requests will reveal which providers face the deepest scrutiny.

Pattern 2 · Test cases through Article 92 / Article 93 evaluations. Commission evaluations of GPAI models for compliance — including model evaluations that test claimed capabilities, safety measures, and risk-mitigation effectiveness — will likely begin in the first 6 months. Some models will pass; others will be flagged for additional compliance measures. Expect 1-3 high-profile evaluations in the first 12 months, with at least one finding of material compliance gap that triggers public Commission action.

Pattern 3 · Member State complaints from downstream providers. Article 89 allows downstream providers (companies that deploy GPAI models in their products) to lodge complaints against GPAI model providers for failure to provide required documentation or compliance support. Expect 5-15 such complaints in the first 12 months, with material concentration on the providers least cooperative with downstream documentation requests. The complaint pattern reveals which providers are creating downstream compliance friction.

Pattern 4 · Scientific Panel alerts. Article 90 establishes a Scientific Panel that can alert the AI Office to systemic or specific identifiable risks. The Panel was established through 2025-2026 and will begin substantive work in 2026-2027. Expect 2-4 Scientific Panel alerts in the first 18 months, focused on systemic-risk models (frontier-tier models with capabilities meeting the FLOPs threshold or other criteria for systemic-risk classification).

Pattern 5 · The first major fine. A specific fine against a GPAI provider in the €5-25M range is plausible within the first 12 months of enforcement authority. The candidates: a provider with public compliance gaps that the AI Office has documented through Article 91 requests; a provider that has refused to engage cooperatively with the AI Office; a provider that has been the subject of Member State complaints. Probability ordering by current compliance position: xAI (highest), Meta (second), Other Western providers including OpenAI, Anthropic, Google (lower). The first major fine is structurally important because it sets the precedent for how enforcement scales subsequently.

Pattern 6 · Indirect enforcement through downstream restrictions. A potentially more impactful enforcement vector than fines: Commission can require market restriction, recall, or withdrawal of non-compliant GPAI models. This is functionally equivalent to denying EU market access. The structural effect is more material than a fine — fines are absorbable, but denial of EU market access is a 20-30 percent revenue hit for major providers. Expect at least one preliminary market-restriction action in the first 18 months, even if it is later resolved through compliance commitments rather than full restriction.

The cumulative pattern: enforcement starts with documentation (lower-friction), escalates through evaluations and complaints (medium-friction), and eventually reaches penalties and market restrictions (high-friction). The 89-day window from May 2026 to August 2026 is the final structural-readiness deadline before this enforcement cascade activates.

4. The downstream provider compliance question

The compliance obligation is not limited to GPAI model providers. Downstream providers — companies that deploy GPAI models in their products — face substantial compliance obligations of their own.

The cascading obligation structure. GPAI providers must provide documentation and compliance support to downstream providers. Downstream providers must integrate that compliance into their own products. End-deployers must ensure their use of the products complies with use-case-specific obligations (high-risk classifications, transparency, human oversight). Failure at any layer creates exposure for that layer; failure at upstream layers creates additional exposure for downstream layers that relied on incomplete upstream compliance.

The Microsoft-OpenAI question as a structural example. Microsoft licenses OpenAI models and offers them through Azure OpenAI Service. Microsoft is functionally a downstream provider for the model layer but a GPAI provider for the integrated service. Whether OpenAI’s compliance work is sufficient for Microsoft’s downstream obligations or whether Microsoft must do additional substantive compliance is a structural ambiguity the AI Office will need to resolve. Similar dynamics apply to: Microsoft Copilot (downstream of OpenAI), Google Workspace (downstream of Gemini), Amazon Bedrock (downstream of Anthropic, Meta, others), Salesforce Einstein (downstream of multiple labs).

The enterprise customer cascade. Enterprise customers using AI products in EU markets face deployer obligations. A bank using an AI product for credit decisions: deployer obligations under Annex III. A hospital using an AI product for diagnostic support: deployer obligations. A government agency using AI for migration decisions: deployer obligations plus prohibited-practice considerations. The cascade implies that the AI compliance burden does not stay at the model layer — it propagates through the entire value chain, including end customers.

The compliance documentation chain. Every layer must maintain compliance documentation that supports the layer above. GPAI provider documentation feeds downstream provider compliance documentation feeds enterprise deployer compliance documentation feeds end-user transparency. Breaks in the chain create liability exposure at every layer above the break. The implication: GPAI provider compliance quality determines downstream compliance feasibility. Cooperative GPAI providers enable downstream compliance; uncooperative ones create downstream liability cascades.

The structural strategic implication. GPAI providers that invest heavily in downstream compliance support (clear documentation, technical assistance, ongoing collaboration) gain durable customer-relationship advantage. Providers that minimize compliance support force downstream providers to assume the regulatory risk — which over time pushes downstream providers toward better-supported alternatives. Compliance quality becomes a structural competitive variable, not just a cost center.

5. The five strategic risks for EU-exposed AI businesses

Five structural risks are visible for businesses with EU AI exposure as of May 2026.

Risk 1 · Documentation completeness gap. Compliance is documentation-intensive. Risk management, data governance, technical documentation, automatic logging, transparency, human oversight, accuracy and robustness — Articles 8-15 plus the GPAI documentation requirements. Most AI providers have partial documentation but not complete documentation that would withstand an Article 91 request. The gap is bigger for providers that haven’t been treating compliance as material. Closing the gap in the 89-day window is challenging.

Risk 2 · Training data copyright disclosure. The most contested compliance area. GPAI providers must publish a sufficiently detailed summary of training data, with specific attention to copyrighted content. The substantive question of how much detail is “sufficiently detailed” remains contested between regulators and providers. Providers that have been minimizing disclosure face enforcement risk; providers that have been comprehensively disclosing face competitive disadvantage from revealing training data. Either approach creates exposure.

Risk 3 · Annex III high-risk classification ambiguity. Many AI products sit ambiguously near the high-risk threshold. AI in employment screening: high-risk. AI in education assessment: high-risk. AI in essential service provision: high-risk. AI in adjacent areas — productivity tools used by HR, educational chatbots, customer service for essential services — may or may not be high-risk depending on use-case interpretation. Providers face a binary choice: classify conservatively as high-risk (incurring substantial compliance cost), or classify as lower-risk (incurring enforcement risk if Commission disagrees).

Risk 4 · Multi-jurisdiction compliance complexity. Providers operating in EU + US + UK + APAC face overlapping but non-identical regulatory frameworks. EU AI Act, US Executive Orders + state-level AI legislation, UK AI Safety Institute framework, China generative AI rules, Japan / Korea / Singapore AI policy frameworks. Compliance for one jurisdiction does not automatically satisfy others. The compliance overhead grows multiplicatively, not additively.

Risk 5 · Enforcement asymmetry between domestic and foreign providers. EU enforcement against US providers is structurally easier than enforcement against Chinese providers. A €1 billion fine against Alphabet is collectible through EU operations; a €1 billion fine against ByteDance is more difficult to collect. The asymmetry creates competitive distortion: US providers face higher real enforcement risk than nominal regulatory parity would suggest. The structural implication: EU enforcement may inadvertently favor Chinese providers that are less collectible while constraining US providers that are more collectible.

The five risks are structural and not specific to compliance failures. Even providers that achieve full substantive compliance face the documentation, classification, multi-jurisdiction, and asymmetry risks. Risk management requires both substantive compliance and structural strategy.

6. The connections to other dispatches

EU AI Act Q3-Q4 2026 enforcement connects to multiple structural threads from this dispatch series.

Connection 1 · The bubble question disentanglement. The dispatch flagged frontier-lab valuations as one of three contested middle categories. EU enforcement risk is one of the structural factors that could compress those valuations through 2026-2028 — either through direct fines, through market access restrictions, or through downstream compliance costs that compress margins. The bear case in the bubble question gains material support if EU enforcement produces high-profile actions in 2026-2027.

Connection 2 · The Anthropic IPO disclosure. The dispatch covered explicit margin-compression risk factors. EU regulatory risk was named specifically. Q3-Q4 2026 enforcement is the empirical test of how that named risk converts to operational reality. Anthropic IPO investor positioning should incorporate the 89-day enforcement deadline as material.

Connection 3 · The EU AI Sovereignty dispatch. The dispatch covered the European policy framework and geographic positioning for sovereign AI. Enforcement is the operational arm of the sovereignty framework. The first 12 months of enforcement reveal whether sovereignty rhetoric translates to actual market protection for European players or remains primarily symbolic.

Connection 4 · The China Sphere capability gap. The dispatch covered the Chinese sphere positioning. The enforcement asymmetry between Western and Chinese providers (covered in Risk 5 above) is structurally relevant. EU enforcement may inadvertently widen the China sphere price gap by raising compliance costs for Western providers operating in EU markets.

Connection 5 · The hyperscaler capex thesis. The dispatch covered the $725B 2026 commitment. EU compliance costs add to operating costs across the hyperscaler stack. Compliance investment for Microsoft (Azure OpenAI Service), Alphabet (Vertex AI), Amazon (Bedrock) is meaningful but absorbable at hyperscaler scale. The compliance cost is more material for downstream enterprise customers and pure-play AI labs.

Connection 6 · The power bottleneck. The dispatch covered the constraint compounding capex deployment timing. EU regulatory uncertainty adds to deployment-region selection complexity. Some hyperscalers may shift more deployment toward UAE / Norway / Iceland / Texas precisely because power-rich regions also offer lighter regulatory environments. The geographic relocation thesis interacts with the regulatory thesis.

The cumulative picture: EU AI Act enforcement is not a standalone regulatory event. It compounds with multiple structural threads to shape the AI cycle’s evolution through 2026-2028. The 89-day window matters because it triggers the operational reality that prior dispatches identified as forward risk.

7. Three scenarios for Q3-Q4 2026 enforcement

The August 2, 2026 enforcement activation resolves into one of three structural patterns through Q3-Q4 2026.

Bullish scenario · 25% probability · “Cooperative implementation, low-friction enforcement.” First 6 months produce documentation requests but few high-profile enforcement actions. Providers with strong compliance investment (OpenAI, Anthropic, Google, Microsoft) navigate documentation phase smoothly. Few or no early fines. Member State complaints largely resolved through compliance commitments rather than penalties. Annex III high-risk classifications resolved through cooperative interpretation rather than enforcement disputes. The structural read: EU AI Act becomes operational reality but does not materially affect AI lab economics or market structure through 2026-2027.

Base scenario · 55% probability · “Test cases produce moderate friction.” First 6-12 months produce 1-3 documentation-driven Commission actions and 5-10 Member State complaints. At least one preliminary fine in the €5-25M range against a provider with documented compliance gaps (xAI most likely candidate, Meta secondary). At least one Annex III high-risk classification dispute that goes through formal proceedings. Substantive enforcement activity, but limited high-profile actions against the major providers. EU compliance becomes material operating cost (5-10 percent overhead on EU revenue) but does not fundamentally restructure market access. Bubble question dispatch’s middle-case frontier-lab valuation impact materializes modestly.

Bearish scenario · 20% probability · “Major enforcement actions early.” First 6-12 months produce a major fine (€100-500M range) against a top-tier provider, or a market restriction action against a frontier-tier model, or both. Cascading downstream effects: enterprise customers reduce EU AI deployment investments. Compliance costs rise materially (15-25 percent overhead on EU operations). Frontier-lab valuations face EU-specific compression. The bear case in the bubble question dispatch gains specific evidence. Multi-year recovery / adjustment cycle for AI providers operating in EU markets.

The 25/55/20 probability allocation reflects the genuine uncertainty in enforcement execution. The base scenario is most likely because the AI Office has signaled cooperative engagement intent, providers have invested in compliance, and the first year of enforcement authority typically produces moderate rather than maximal enforcement activity. The bullish scenario requires near-perfect compliance + cooperative AI Office orientation. The bearish scenario requires either a high-profile enforcement target or multiple cascading compliance failures.

8. The strategic implications by stakeholder

The 89-day enforcement countdown has direct consequences for five distinct stakeholder groups.

For AI labs (frontier-tier). Complete substantive compliance documentation in the 89-day window. Engage cooperatively with AI Office through informal collaboration channels. File any required notifications immediately. Anthropic’s IPO investor disclosure framework provides a useful precedent — explicit risk acknowledgment combined with active compliance investment. The structural goal: avoid being the high-profile enforcement test case in the first 12 months.

For hyperscalers. Compliance through cloud-AI services (Azure OpenAI, Vertex AI, Bedrock) is structurally complex due to the multi-layer provider relationship. Invest in downstream compliance support that reduces enterprise customer friction. The compliance support investment is structural competitive moat — the hyperscaler that makes EU compliance easiest for enterprise customers captures durable share.

For enterprise EU AI customers. August 2, 2026 deployment decisions become structurally different from pre-August 2026 decisions. Annex III high-risk classifications apply to deployments after this date; pre-existing deployments get carve-outs unless significantly changed. The structural implication: deployment decisions in the 89-day window before August 2 may be lower-friction than deployment decisions after. Plan deployment timing accordingly.

For investors in EU-exposed AI businesses. The 89-day enforcement countdown is material to forward-risk modeling. Companies with strong compliance investment should be positioned more favorably than companies with limited investment. xAI, Meta-Llama-deployers-in-EU face highest enforcement risk among major providers; OpenAI, Anthropic, Google, Microsoft face manageable risk. Differentiate accordingly.

For policymakers and downstream regulators. The first 12 months of enforcement set precedents that ripple globally. US, UK, Japan, and other jurisdictions will observe EU enforcement patterns and adapt their own regulatory frameworks accordingly. The first major fine, the first market restriction action, the first successful downstream complaint — each becomes a reference point for global AI regulation. EU enforcement quality during this window has implications beyond EU markets.

What to Do This Quarter (89 Days to August 2, 2026)

1. Frontier AI labs. Complete substantive compliance documentation now. Ensure AI Office collaboration channels are active. File required notifications. Treat the 89-day window as the final readiness deadline before active enforcement authority begins.

2. Hyperscalers. Invest in downstream compliance support that enables enterprise customer compliance. The compliance-support investment is competitive moat. EU enterprise customers will gravitate toward providers that minimize their compliance friction.

3. Enterprise EU AI customers. Plan deployment timing strategically. August 2, 2026 changes the regulatory calculus for new deployments. Pre-August deployments get more favorable carve-outs in many cases. Pre-position accordingly. Multi-vendor sourcing reduces single-vendor compliance failure exposure.

4. Investors in AI-exposed businesses. Update forward-risk models to incorporate Q3-Q4 2026 enforcement scenario. Differentiate companies on compliance investment quality. Companies with strong compliance position are durably advantaged; companies with limited engagement face elevated enforcement risk.

The Strategic Read

August 2, 2026 — eighty-nine days from publication — Commission enforcement powers under the EU AI Act activate against GPAI providers. Penalties up to €35M or 7 percent of worldwide turnover. The structural shift is from “EU AI Act exists” to “EU AI Act enforcement is active.” Substantive obligations have been progressively activating through 2025-2026; the penalty phase changes the operational risk profile materially.

Compliance positions are non-uniform across major providers. OpenAI signed Code of Practice, Anthropic disclosed in IPO documentation, Google/Alphabet has resourced compliance heavily, Microsoft has cooperative engagement plus complex multi-layer obligations. Meta is more confrontational with EU regulation; xAI has limited apparent compliance investment. The compliance position translates to enforcement-risk position. Providers most aligned with cooperative AI Office engagement face lower enforcement risk; providers least aligned face higher probability of becoming early test cases.

The first 6-12 months of enforcement produce a cascade. Documentation requests in the first 60-120 days. Article 92 / 93 evaluations in months 3-6. Member State complaints accumulating through months 6-12. Scientific Panel alerts in months 12-18. The first major fine in the €5-25M range plausible within the first 12 months, with concentration on providers with documented compliance gaps. Market restriction actions are structurally more impactful than fines and probable within the first 18 months for at least one frontier-tier model.

The downstream provider cascade matters. GPAI provider compliance quality determines downstream provider compliance feasibility. Microsoft-OpenAI, Google-Gemini-Vertex, Amazon-Bedrock-multi-lab relationships create multi-layer compliance complexity. Hyperscalers that invest heavily in downstream compliance support gain durable customer-relationship advantage. Compliance quality becomes a structural competitive variable.

Five structural risks face EU-exposed AI businesses: documentation completeness, training data copyright disclosure, Annex III high-risk classification ambiguity, multi-jurisdiction compliance complexity, enforcement asymmetry between domestic and foreign providers. Even providers that achieve full substantive compliance face the structural risks. Risk management requires both substantive compliance and structural strategy.

Three scenarios resolve through Q3-Q4 2026. Bullish (25%): cooperative implementation, low-friction enforcement, no major early actions. Base (55%): test cases produce moderate friction, 1-3 documentation actions, at least one preliminary fine in €5-25M range, EU compliance becomes 5-10 percent operating-cost overhead. Bearish (20%): major enforcement actions early, €100-500M fine against top-tier provider or market restriction action against frontier-tier model, cascading downstream effects, EU-specific frontier-lab valuation compression.

The strategic implications run by stakeholder. AI labs should complete substantive compliance now. Hyperscalers should invest in downstream compliance support as competitive moat. Enterprise customers should plan deployment timing strategically around August 2, 2026. Investors should update forward-risk models to differentiate companies on compliance investment quality.

The deeper signal: EU enforcement activation is not a discrete regulatory event. It is the operational reality that determines whether the AI cycle’s structural risks (covered in the bubble question dispatch, the Anthropic IPO disclosure dispatch, the EU AI Sovereignty dispatch) compound or remain bounded. The first 12 months of enforcement reveal which scenario materializes. The 89-day window before activation is the final structural-readiness deadline.

The honest assessment: the most likely scenario is the base case — moderate friction, some test cases, manageable economic impact, durable structural changes that compound over multi-year horizons. The probability of either tail outcome (bullish soft enforcement or bearish major actions) is meaningful but lower. The structural insight is that enforcement quality during the first 12 months creates global precedents that ripple beyond EU markets. Other jurisdictions are watching.

T-89 days to EU AI Act enforcement activation. €35M / 7% turnover penalty authority. Compliance positions non-uniform: OpenAI / Anthropic / Google / Microsoft well-positioned; Meta / xAI elevated risk. Enforcement cascade through documentation → evaluations → complaints → fines → market restrictions. Three scenarios with 25/55/20 probability allocation. Base case is moderate friction with structural durable changes.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The EU AI Sovereignty Dispatch

- The Anthropic IPO Disclosure Document

- The Bubble Question, Disentangled

- The China Sphere Capability Gap Q2 Update

- The $725B Hyperscaler Capex Question

- The Power Bottleneck — Grid Cliff 2027-2028

Sources

- artificialintelligenceact.eu · Enforcement of Chapter V under the EU AI Act · April 2026

- DLA Piper · Latest wave of obligations under the EU AI Act · August 2025

- European Commission · Guidelines for providers of general-purpose AI models

- Augment Code · The 2026 EU AI Act and AI-Generated Code · April 2026

- Legal Nodes · EU AI Act 2026 Updates: Compliance Requirements and Business Risks · April 2026

- Dataguard · EU AI Act Timeline: Key Compliance Dates

- artificialintelligenceact.eu · Implementation Timeline

- euaiact.com · EU AI Act Implementation Timeline

- EU AI Act articles 8-15, 50, 88-93, 99 (penalty regime), Articles relating to AI Office and Scientific Panel

- AI Office establishment per Commission decision January 24, 2024 / operational August 2, 2025

- GPAI Code of Practice signatories (OpenAI confirmed; broader signatory list)