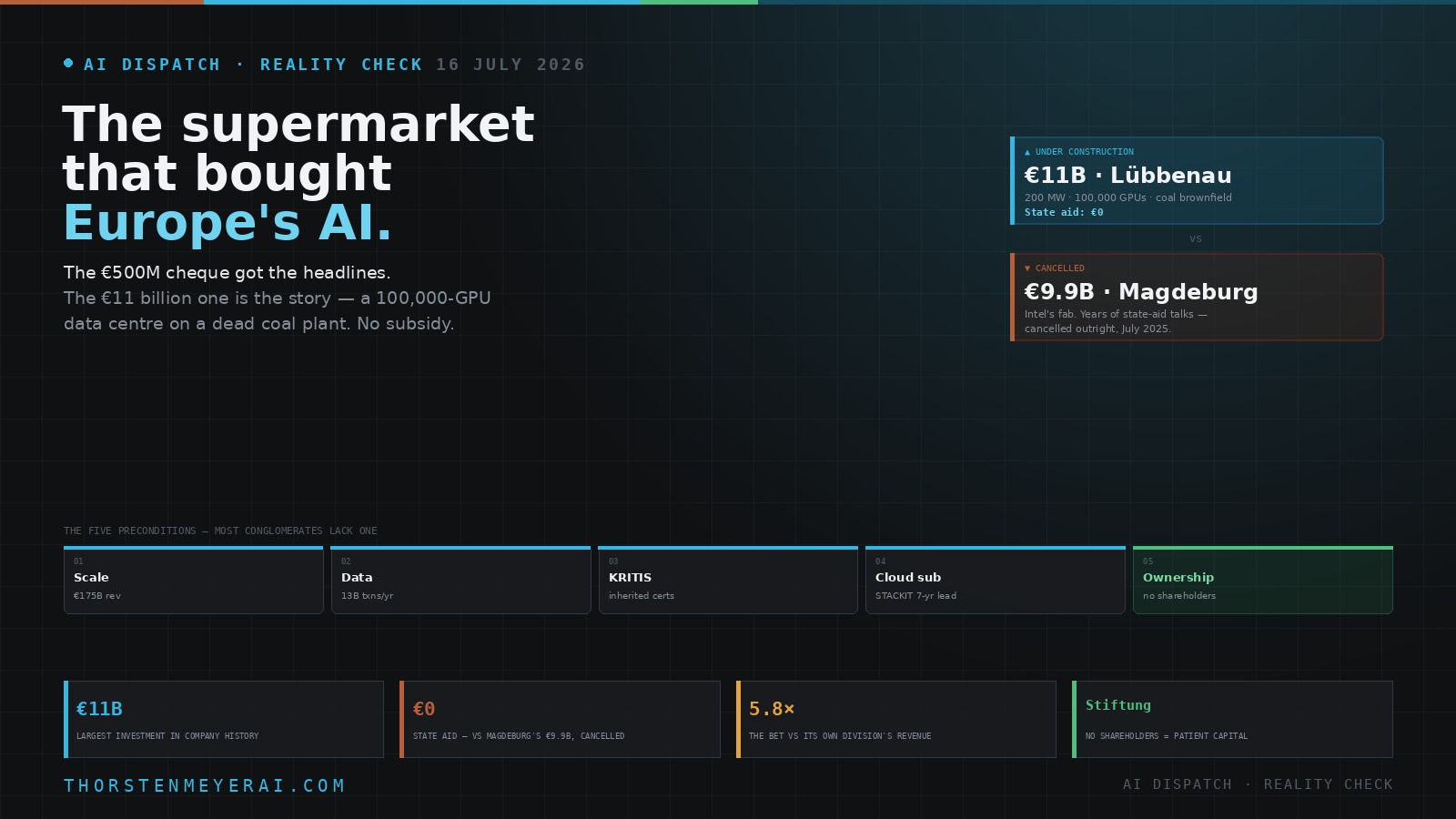

The €500 million cheque got the headlines. The €11 billion one is the story.

While everyone was parsing the Cohere–Aleph Alpha merger, the company that actually underwrote it was doing something far more consequential in a corner of Brandenburg. On the site of a dead coal-fired power plant near Lübbenau, the owner of Lidl and Kaufland is building a 200-megawatt AI data centre designed to hold up to 100,000 GPUs.

It is the largest single investment in Schwarz Group’s history. It is more than five times the annual revenue of the division making it. And — this is the part that should stop you — it is taking no government subsidy at all.

Compare that to Intel’s Magdeburg fab, which spent years negotiating €9.9 billion in German state aid before being cancelled outright in July 2025. One of these projects is under construction. The other is a hole in the ground and a lesson.

That contrast is the thesis: Europe’s most credible AI sovereignty play isn’t coming from Brussels or Berlin. It’s coming from industrial balance sheets — and the reason it works is a boring German legal structure nobody talks about.

The supermarket that bought Europe’s AI: why industrial capital beats government money

The €500M cheque got the headlines. The €11 billion one is the story. On a dead coal plant in Brandenburg, the owner of Lidl is building a 200 MW, 100,000-GPU AI data centre — with no government subsidy at all.

Europe looked for its AI advantage in regulation, talent and Brussels programmes. Magdeburg is what that produces. The real advantage was sitting in the Mittelstand: enormous, foundation-owned industrials with recession-proof cash, decades of proprietary data, inherited KRITIS compliance — and nobody to answer to. Patient capital is the one thing American AI structurally cannot buy. But be precise: Europe’s sovereignty didn’t get nationalised — it got privatised. The answer to American corporate power over European AI is turning out to be German corporate power, with a toll booth attached. That may be the better trade. Just don’t call it independence — call it a change of landlord, and read the lease.

What Schwarz actually is

Most people outside Germany know Lidl. Almost nobody grasps the scale behind it.

Schwarz Group is Europe’s largest retailer: roughly €175 billion in annual revenue, 575,000 employees, operations in 32 countries, and north of 13 billion transactions a year. Five divisions — Lidl, Kaufland, Schwarz Produktion, PreZero (waste management), and, since September 2023, Schwarz Digits.

Schwarz Digits is the IT arm: about 7,500 people at launch, around €1.9 billion in annual sales, co-led by Christian Müller and Rolf Schumann. It bundles STACKIT (the cloud platform, built internally from 2018 and opened to external customers around 2022–23), XM Cyber (the Israeli cybersecurity firm Schwarz bought for ~$700M in 2021), and the group’s e-commerce and AI work.

The stated ambition, in the co-CEOs’ own words to the FAZ, is to become Europe’s first sovereign hyperscaler. STACKIT currently runs four data centres across Germany and Austria; Lübbenau is the fifth. And the operational pedigree is real, not aspirational — this is infrastructure that has been running Europe’s largest retail estate at critical-infrastructure scale since 2018, carrying BSI C5, ISO 27001, SOC 2, and DORA certifications, because German food supply is KRITIS.

That last point matters more than it sounds. Schwarz didn’t build a compliance story for the AI market. It inherited one from selling groceries.

RackChoice 3U rackmount Server Chassis Support Liquid Cooling Compatibility up to Elevated 360mm Radiator Support SFX PSU/ATX/MicroATX/Mini-ITX MB

- Pre-installed 120mm Fans: Includes 3 fans or supports 360mm radiator

- Motherboard Compatibility: Supports ATX, MicroATX, Mini-ITX

- Drive Bays: 2×3.5-inch and 1×2.5-inch internal bays

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The Lübbenau bet

The numbers deserve to be laid out properly, because they’re what make this different from a press release.

€11 billion total — roughly €2.5 billion of construction and €8.5 billion of technology. A 13-hectare brownfield site on a former coal plant. 200 MW connected load in the first phase, modular expansion after. Capacity for up to 100,000 GPUs. First construction module targeted for end of 2027. Entirely green electricity, liquid-cooled, with waste heat piped into the local district heating network. It already meets the specification for the EU’s planned AI Gigafactories, and Lübbenau is positioned as one of them.

Now hold two numbers next to each other. Schwarz Digits’ annual revenue: ~€1.9 billion. The Lübbenau commitment: €11 billion. The division is betting more than five times its own top line on a single site. For comparison, Tesla’s Grünheide Gigafactory came in around €6 billion.

Germany’s Digital Minister Karsten Wildberger has been effusive — Germany needs computing power to play in AI’s premier league — and the political support is genuine. But note what it isn’t: money. No subsidy. No state aid negotiation. No Magdeburg.

The Data Center Engineering Handbook: A Practical Guide to Infrastructure Design, Power Systems, Cooling, Security, Compliance, and Operational Excellence

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The pattern nobody named

Here’s what the Cohere coverage missed by treating Schwarz as a funding source. Schwarz is the second instance of a pattern, and the pattern is the actual news.

Look at who anchors Europe’s two AI champions:

Cohere–Aleph Alpha ← Schwarz Group. Co-led Aleph Alpha’s ~$500M Series B in 2023 via an investor consortium, took a stake reported above 20%, then committed €500 million leading Cohere’s Series E — structured as preferred equity plus convertible debt, with STACKIT as Cohere’s primary European cloud provider under a reported five-year exclusivity, against committed compute capacity. Reported target: 1.5 GW of contracted data-centre power across Germany, Austria and Poland by 2028.

Mistral ← ASML. The Dutch lithography monopolist led Mistral’s €1.7 billion Series C with €1.3 billion, taking roughly 10% fully diluted and a strategic committee seat — becoming Mistral’s largest shareholder.

Neither of Europe’s frontier AI companies is anchored by a venture fund or a government. Both are anchored by industrial corporates. One makes the machines that make chips. The other sells groceries. And around the edges the same thing is happening: Bosch and SAP were both in Aleph Alpha’s cap table; SAP, Deutsche Telekom, Ionos and Siemens have been negotiating joint bids for EU-funded AI data centres.

European industry has quietly decided that domestic AI capability is strategic infrastructure, not discretionary procurement. That’s a category change, and it happened without a single Brussels programme causing it.

ENTERPRISE AI INFRASTRUCTURE: Modern MLOps, Vector Databases, GPU Clusters, and Scalable Data Architecture for LLMs (The Enterprise AI Architect’s Handbook)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why industrial money beats government money

Four reasons, and they’re structural rather than sentimental.

It doesn’t change with elections. A five-year sovereign-AI programme funded by a coalition survives exactly as long as the coalition does. Schwarz’s commitment survives as long as Schwarz does, which — given it sells food in 32 countries — is a considerably longer horizon. As one framing of the deal put it, corporate sovereign capital is commercially motivated rather than politically motivated, and that makes it more durable, not less.

It arrives bundled with infrastructure. Government money buys GPUs. Schwarz money buys GPUs and the cloud they sit in and the certifications and the operational track record. Cohere didn’t just get €500 million; it got a European cloud it didn’t have to build.

It arrives bundled with a customer. This is the underrated part. Schwarz is itself an enormous enterprise AI customer — 575,000 employees, 13 billion transactions, the world’s largest SAP retail estate. The combined entity has a guaranteed anchor workload on day one. Government funding gives you runway. Industrial funding gives you revenue.

And the decisive move isn’t the cheque — it’s the substrate. Making STACKIT the cloud the merged company runs on means Schwarz becomes a beneficiary of every enterprise and government deployment the entity ever wins. The €500 million buys a stake. The exclusivity buys a toll booth.

Large-Scale AI Engineering: Design, Train, and Optimize Foundation Models on NVIDIA GPU Clusters

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The five preconditions — why this isn’t a template

Before anyone concludes that every European conglomerate should now buy an AI lab: the Schwarz model requires five things simultaneously, and most candidates lack at least one. (This framework comes from the industrial-anchor analysis published on StrongMocha, which is worth reading in full if you want the detailed version.)

1. Scale — €175B revenue and operationally stable cash flow. The blunt formulation from that analysis: “We always eat.” Recession-resistant cash is what makes an €11B multi-year commitment thinkable.

2. Data — 13 billion transactions a year across 32 countries. Not a pilot dataset; an economy’s worth of operational telemetry.

3. KRITIS status — classification as critical infrastructure (German food supply), which drags BSI C5, ISO 27001, SOC 2 and DORA architecture along with it. This is what makes regulated procurement credible without a decade of retrofitting. Comparable KRITIS sectors: financial services, telco, energy.

4. An existing sovereign-cloud subsidiary — STACKIT’s roughly seven-year production head start: 20,000 servers, 22.5 PB of storage, 1.4 million network ports, the world’s largest SAP retail systems, all production-tested. A greenfield effort started in 2026 cannot match that by 2028. The only comparable existing operators are Deutsche Telekom’s T-Systems, OVHcloud, Orange Bleu, and Telefónica Tech.

5. Long-term ownership — and this is the one that decides everything.

Europe’s hidden advantage is a legal structure

Schwarz Group is controlled personally by Dieter Schwarz and the Dieter Schwarz Foundation. No public shareholders. No quarterly earnings calls. No activist investor asking why €11 billion is going into a data centre instead of a buyback.

Sit with the implication, because I think it’s the most underrated fact in European tech. The thing that lets Schwarz make a decade-long, €11 billion, unsubsidised bet on sovereign infrastructure is not German engineering or EU regulation. It’s the absence of public shareholders.

That’s a structural advantage the United States cannot replicate. Its industrial giants are publicly traded and shareholder-disciplined; a US retailer announcing an $11 billion AI data centre with no clear five-year return would be punished within a quarter. China does patient capital differently — through the state, with the political strings that implies. Germany has a third model: the Stiftung — foundation ownership — which produces private capital on a public-institution time horizon.

And Schwarz is not alone in having it. Robert Bosch Stiftung holds roughly 94% of Bosch. The Carl-Zeiss-Stiftung owns Zeiss. Bertelsmann sits under the Bertelsmann Stiftung. Würth, Miele, Trumpf — the German Mittelstand is full of enormous, foundation-owned, quarterly-pressure-free industrial companies sitting on decades of proprietary data.

Europe has spent three years wondering how to compete with American capital. The answer may be that it can’t compete on volume — and doesn’t need to, if it can compete on patience.

Who’s next — the honest shortlist

Run the five preconditions and the field narrows fast. Most conglomerates fail at least one, and the realistic candidate list is four to six names, not fifty:

Bosch is the strongest structural fit: ~€90B revenue, foundation-owned (no quarterly pressure), deep industrial and automotive data, KRITIS-adjacent, and already an Aleph Alpha investor. What it lacks is a cloud subsidiary at STACKIT’s maturity — the precondition you can’t buy quickly.

Deutsche Telekom / T-Systems has the mirror-image problem: a real sovereign-cloud operation and genuine telco KRITIS status, but it’s publicly traded with the German state as a large shareholder — failing the ownership precondition while satisfying the infrastructure one.

SAP, Siemens and Ionos are already circling EU-funded AI data-centre bids. All publicly traded; all have data and scale; none has Schwarz’s combination.

ASML has already done a version of this — but from the opposite direction: strategic equity in Mistral, without a cloud subsidiary or a captive workload. That’s the investor model, not the anchor model.

Zeiss, Bertelsmann, Würth have the ownership structure and the patience, but not the cloud infrastructure or, in most cases, the scale.

The honest conclusion is the uncomfortable one: Schwarz is a special case, not a template. The pattern is real and worth naming. The replication is genuinely hard, and anyone who tells a minister that “we just need five more Schwarz Groups” is selling something.

The critique — a new landlord is not freedom

Now the part that should temper the enthusiasm, because there’s a version of this story that’s pure boosterism and it isn’t true.

Swapping AWS dependency for Schwarz dependency is still dependency. If STACKIT holds five-year exclusivity as the European cloud for the company Europe just designated its sovereign AI champion, then a single privately-held German conglomerate becomes a chokepoint in European AI. That’s not no risk. It’s a different risk — domestic rather than foreign, which feels better and isn’t automatically better.

The thing that makes it durable also makes it opaque. No public shareholders means no public accountability, no mandatory disclosure, no quarterly scrutiny. Europe is concentrating strategic national capability inside a structure specifically designed to answer to nobody but its owner. There’s a German critical tradition on exactly this — Golem published a piece last August calling the sovereign cloud a fairy tale and questioning the BSI’s role in blessing it. That criticism deserves airtime, not dismissal.

Founder control carries succession risk. Everything above rests on one family’s continuity of intent.

And there’s a paradox sitting inside the sovereignty story: Schwarz signed a long-term partnership with Google in November 2024 to migrate its ~575,000 employees to Google Workspace — hosted in Schwarz’s own data centres via STACKIT, yes, but the sovereign-cloud champion is nonetheless one of Google’s larger European customers. Sovereignty, again, turns out to be a spectrum rather than a status.

Finally, the bet is genuinely enormous. €11 billion against a €1.9 billion division. If STACKIT can’t win external customers at hyperscaler scale — against AWS, Azure and Google, who are not standing still and have their own EU sovereign-cloud offerings — this becomes the most expensive lesson in German corporate history. That is a real possibility, not a rhetorical hedge.

The take

The Cohere–Aleph Alpha merger will be remembered as the deal. It shouldn’t be. The story is who paid for it, and why they could.

Europe has been looking for its AI advantage in the wrong places — in regulation, in talent, in Brussels programmes, in the hope that a subsidy could conjure a champion. Magdeburg is what that produces. Meanwhile the actual advantage was sitting in plain sight in the German Mittelstand: enormous, foundation-owned industrial companies with recession-proof cash flow, decades of proprietary data, inherited critical-infrastructure compliance, and — decisively — no shareholders to answer to. That is patient capital, and patient capital is the one thing American AI structurally cannot buy.

But be precise about what just happened. Europe’s sovereignty didn’t get nationalised. It got privatised. The answer to American corporate power over European AI is turning out to be German corporate power over European AI — with a toll booth attached, an ownership structure accountable to one family, and a five-year exclusivity clause on the champion’s cloud.

That may well be the better trade. On jurisdiction, on durability, on operational competence, it probably is. Just don’t call it independence. Call it a change of landlord — and read the lease.

Sources: Schwarz Digits / STACKIT figures, the €11B Lübbenau campus (200 MW, ~100,000 GPUs, €2.5B construction + €8.5B technology, first module end-2027, brownfield coal site, green power, district heating) via Data Center Dynamics, ESM Magazine, Smart Country Convention, Silicon Saxony and Xpert.digital; Schwarz Digits structure, STACKIT history, XM Cyber, the BSI cooperation (March 2025) and the Google Workspace partnership (November 2024) via Wikipedia and FAZ/Handelsblatt reporting; Schwarz Group scale (~€175B revenue, 575,000 employees, 32 countries) and the five-preconditions framework (scale · data · KRITIS · sovereign-cloud subsidiary · long-term ownership) via the industrial-anchor analysis published on StrongMocha; Cohere Series E terms, STACKIT exclusivity and the 1.5 GW/2028 target as reported; ASML–Mistral Series C (€1.3B, ~10%, strategic committee seat) via TechCrunch and Penchan; Intel Magdeburg cancellation (July 2025, €9.9B state aid) via trade coverage; Golem.de (August 2025) for the sovereign-cloud critique. Several deal terms are reported rather than confirmed by the parties, and the Cohere–Aleph Alpha transaction remains subject to regulatory approval. Not investment advice. Analysis and framing are the author’s.