What happens to template libraries, legal forms vendors, and document generation tools?

This is the part of the market where the disruption is most complete and the defence options are most limited. Template and forms vendors are not facing margin pressure or a restructured delivery model. They are facing a question about whether their core product continues to exist as a distinct category — and the honest answer, for a significant portion of the market, is that it does not.

ThorstenmeyerAI.com · Analysis · April 2026

The file was never the product

What legal template vendors were actually selling — and why Claude for Word just made the delivery mechanism obsolete. The encoded knowledge has been absorbed into the model. What remains is a question of what else these businesses built.

The market reality in numbers

Three distinct businesses inside “template and forms”

What the viable business looks like on the other side

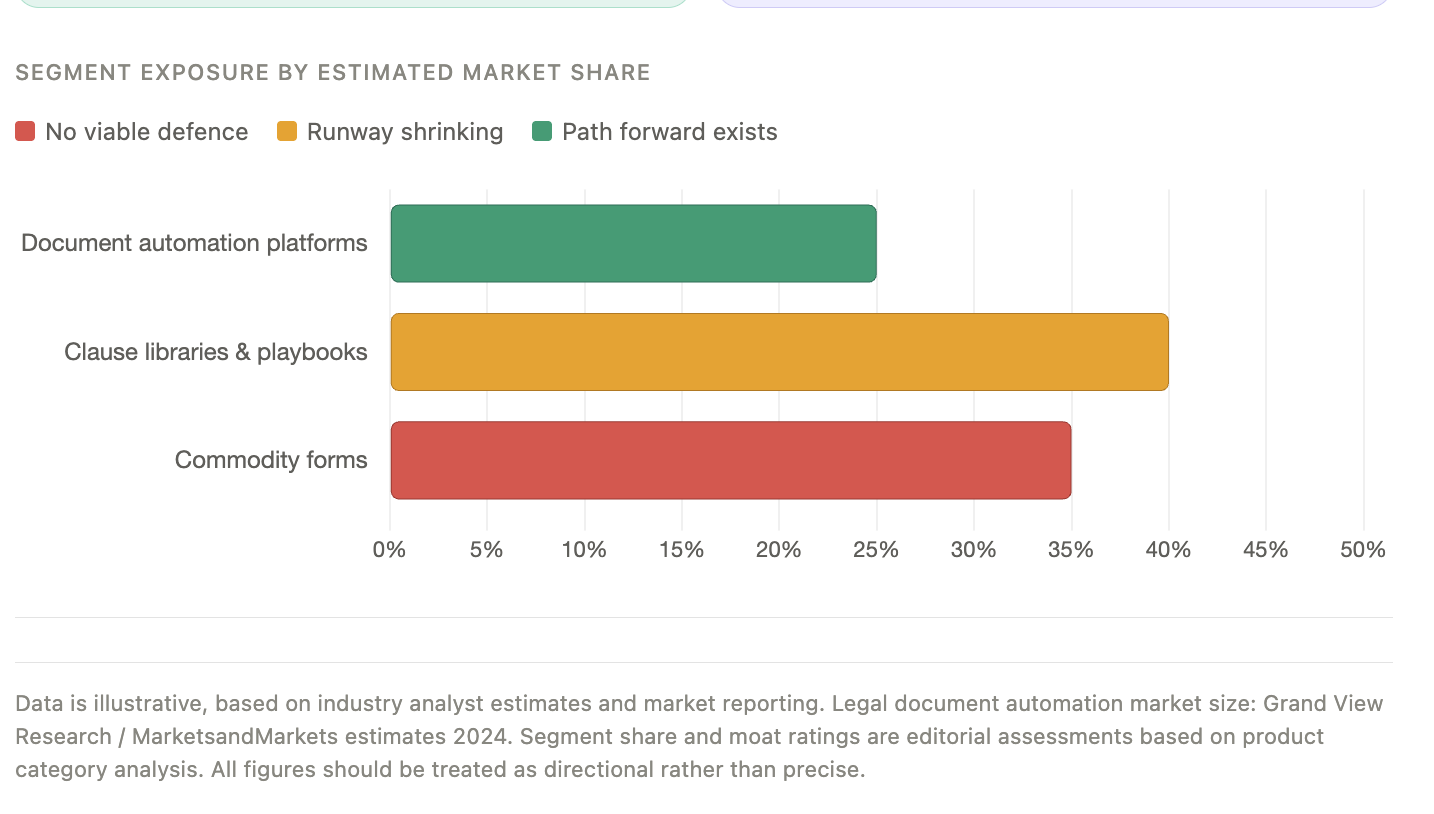

Segment exposure by estimated market share

Data is illustrative, based on industry analyst estimates and market reporting. Legal document automation market size: Grand View Research / MarketsandMarkets estimates 2024. Segment share and moat ratings are editorial assessments based on product category analysis. All figures should be treated as directional rather than precise.

What the template business has always actually been selling

To understand why, you have to be precise about what a template library or legal forms vendor was selling in the first place. On the surface: documents. Pre-written contracts, pre-structured forms, boilerplate clauses organised by jurisdiction and document type. But underneath that: encoded legal knowledge. The value of a well-drafted NDA template from a reputable vendor was not the Word file. It was that a lawyer had already thought through the issues, written language that held up under scrutiny, balanced the interests in a way that reflected market practice, and saved the purchaser from having to do that thinking themselves.

That encoded knowledge is now available through a different channel. When a lawyer can open Word, describe what they need, and receive a first draft that inherits the document’s styles, reflects current market practice, and can be immediately refined through tracked-change iteration — the template file has been disintermediated. The knowledge it contained has been absorbed into the model. The file itself was always just a delivery mechanism, and the delivery mechanism has been replaced.

The three distinct businesses inside “template and forms”

The category is not monolithic, and the exposure varies significantly depending on which version of the business you are in.

The first is commodity forms — standard documents available for low cost or free, covering routine transactions and common legal situations. LLC operating agreements, basic NDAs, simple employment offer letters, residential lease agreements. This segment was already under pressure before Claude for Word existed. LegalZoom, Rocket Lawyer, and their equivalents had already commoditised the low end. AI-assisted drafting finishes that job. A user who previously paid fifteen dollars for a template file now gets a drafted document tailored to their specific situation for the cost of their Claude subscription, which they were paying anyway. There is no meaningful defence available at this end of the market. The product is gone.

The second is professional-grade clause libraries and playbooks — the tools sold to law firms and legal departments as practice management infrastructure. Standard form M&A agreements with alternative provisions, negotiating guides with market data, clause-by-clause commentary explaining why the language is drafted the way it is. This is a more sophisticated product serving more sophisticated buyers, and it has more runway. But the runway is shorter than the vendors would like to believe, for reasons discussed below.

The third is document automation platforms — tools that go beyond static templates to generate customised documents from structured questionnaire inputs, often integrated into broader workflow systems. Contract lifecycle management integrations, self-service portals for routine legal requests, automated lease generation for real estate portfolios. This segment is in the most interesting position: it is the one that most clearly has a path through the disruption, but only if it moves quickly and in the right direction.

Why the clause library model is more fragile than it looks

Professional clause libraries command real prices from sophisticated buyers, and they have relationships, brand reputation, and accumulated content depth that a general-purpose model cannot immediately replicate. But the value proposition rests on a specific assumption: that the encoded legal knowledge in the library is more reliable, more current, and more jurisdiction-specific than what the lawyer could produce or obtain otherwise.

That assumption is eroding. The models are trained on vast quantities of legal text. They have seen more contracts than any clause library contains. Their understanding of market practice across document types is broad, if imperfect. More importantly, they improve continuously and asymmetrically — each model generation narrows the gap between what the library offers and what the model can produce on demand, without any corresponding improvement in the library’s competitive position.

The clause library vendor’s response has historically been to invest in commentary and guidance — the “why” behind the language, not just the language itself. That is the right instinct. Explanatory content that helps a lawyer understand the issues well enough to exercise judgment is harder to replicate than the clause text itself. But it is not immune. Models that can explain as well as draft are already here, and the explanation quality is improving faster than most vendors anticipated.

The jurisdiction-specific and regulatory-specific depth is the strongest remaining moat. A clause library built around the specific requirements of Delaware corporate law, or English law finance documentation, or German employment contracts, reflects accumulated specialisation that general-purpose models handle unevenly. Vendors who have genuinely deep jurisdictional content — not just translated standard forms, but documents that reflect how lawyers actually practice in that jurisdiction — have a differentiation that remains real for now.

Document automation faces a fork in the road

Document automation platforms are in a structurally different position because they were never just about the content — they were about the workflow. A platform that lets a business unit submit a routine contract request through a self-service portal, routes it through an approval workflow, populates a template from the request inputs, stores the executed agreement in a repository, and triggers renewal alerts is doing something more than delivering a document. It is running a process.

Claude for Word, at its current stage, is not a process platform. It is a document intelligence layer inside a single application. It does not manage contract repositories, it does not integrate with procurement systems, it does not track counterparty relationships, it does not trigger workflow approvals, and it does not provide audit trails for compliance purposes. The document automation vendors who have built genuine process infrastructure around their generation capabilities have a real argument that they are offering something the add-in does not.

The fork is this: automation platforms that invested primarily in template quality and generation capability are exposed, because that layer is commoditising. Platforms that invested in workflow, integration, repository management, and the operational infrastructure around the document are in a different conversation — they are selling process management, and the generation layer that Claude for Word provides could actually complement rather than replace them.

The smartest move available to document automation vendors right now is to stop selling the generation capability as a differentiator and start selling it as infrastructure — ideally by integrating Claude or equivalent models directly into their platforms and competing on the workflow and integration layer where they have genuine depth. The vendors that make this pivot early will find that the model commoditising their generation capability also improves their product, because they can use it. The vendors that try to compete on generation quality against a foundation model will lose that argument over a fairly short horizon.

The market positioning problem

There is a specific commercial problem that template and forms vendors face that is worth naming directly: their buyers are increasingly the same people who have access to Claude for Word.

When a legal department buys a clause library subscription, the lawyers using it now also have AI drafting capability in the same tool they draft in. The comparison is immediate and concrete. A lawyer who opens a clause library to find standard force majeure language, then opens Claude for Word and asks it to draft force majeure language appropriate for a software services agreement governed by English law, can evaluate the outputs side by side. That comparison will not always favour the model. But it will often be close enough to raise the question of whether the subscription is justified, and that question is being asked in renewal conversations right now.

The vendors who will survive those renewal conversations are the ones who can point to something in their product that the comparison exercise does not capture: the commentary explaining regulatory context, the jurisdiction-specific annotations, the integration with the firm’s existing precedent management system, the training and support infrastructure. The ones selling primarily on the quality of the document text are in a difficult position, because the document text comparison is now easy to run.

What the viable business looks like on the other side

The template and forms businesses that come through this disruption intact will look quite different from the ones that entered it. They will be selling one of three things.

The first is deeply specialised jurisdictional and regulatory content with genuine expert curation — not just documents, but the explanatory architecture around them. Who wrote this, what qualifications they hold, when it was last reviewed against current law, what the significant issues are that a practitioner needs to understand before using it. This is closer to a legal research product than a forms library, and it commands a different kind of buyer relationship.

The second is process and workflow infrastructure that uses AI-generated documents as a component rather than a product. The generation is table stakes. The contract request portal, the approval routing, the repository, the integration with the ERP system, the renewal management, the reporting — these are the product. Vendors who have built this layer have a path.

The third is AI-assisted document intelligence built on top of the vendor’s proprietary content — a system where the firm’s accumulated clause library, market data, and jurisdictional expertise trains or fine-tunes the generation capability in ways that general-purpose models cannot replicate. This is technically and commercially the hardest path, but it is the one that preserves the most competitive differentiation. A clause library that makes the model better, rather than competing with it, is a different business with a different value proposition.

The category that does not survive

There is a segment of this market that has no viable path and should acknowledge it clearly: the undifferentiated general-purpose template library competing on price and breadth of document coverage.

If you are selling a library of five thousand standard business documents spanning multiple jurisdictions, with no specialised expertise, no workflow integration, no commentary layer, and no proprietary insight that the model does not have — you are selling the training data. The model has read those documents. It has read more documents like them than your library contains. The file format and the delivery mechanism were never the value. The encoded knowledge was. And the encoded knowledge, at the general-purpose level, now lives in the model.

That is not a transition challenge. It is a product discontinuation. The honest response is not to look for a repositioning strategy but to decide whether there is a specialised, expert-curated, jurisdiction-specific version of the business worth building — and whether the existing customer relationships and content assets provide a foundation for it.

For the vendors who built real depth, real expertise, and real workflow infrastructure: the disruption is manageable, the path is visible, and the pivot is available. For the ones who built breadth and volume at the general-purpose end of the market, the category is being absorbed into the model, and the time to have that conversation honestly is before the renewal numbers make it unavoidable.

Legal Engineering: Building AI-Powered Legal Workflows with Multi-Agent Architectures

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

contract workflow management platform

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Claude for Lawyers: AI-Powered Legal Research, Drafting & Document Review — Contracts, Motions, Discovery, Compliance & Ethics

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

No Tools, Just Contracts: How to Win Government Contracts and Subcontract the Work for Profit—Without Ever Picking Up a Tool

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.