By Thorsten Meyer — May 2026

May 19, 2026 — thirteen days from publication of this dispatch — Google opens I/O 2026 at Shoreline Amphitheatre. Google Keynote 10:00-11:45am PT, Developer Keynote 1:30-2:45pm PT, sessions continuing into May 20. A consumer-focused Android Show I/O Edition runs May 12, seven days from now. The framing across pre-event commentary is uniform: this is “the year of the agent.” If 2024 was chatbots and 2025 was integration, 2026 is the deployment-phase test of whether agentic AI converts from demo to production at scale.

The pre-I/O context matters for reading the announcements. Cloud Next 2026 in April already shipped what would historically have been I/O-tier announcements: the Gemini Enterprise Agent Platform (Google’s “operating system for agents”), eighth-generation TPUs (v8t for training, v8i for inference with 80 percent better performance-per-dollar), the Agentic Data Cloud with cross-cloud lakehouse, and Memory Bank for persistent context. Sundar Pichai’s Cloud Next keynote disclosed that first-party Gemini API processing reached 16 billion tokens per minute (up from 10 billion the prior quarter), Gemini Enterprise paid monthly active users grew 40 percent quarter-over-quarter in Q1, and just over half of Google’s overall machine-learning compute investment in 2026 will go toward Cloud customer workloads. The infrastructure foundation is in place. I/O is the consumer-facing demonstration.

The competitive backdrop intensifies the stakes. OpenAI is reportedly building an agentic-OS phone with Jony Ive’s design firm. Apple Project Iris smart glasses leaks suggest a 2026-2027 timeline. Meta acquired ARI for humanoid robotics. Sierra (Bret Taylor’s enterprise AI agent company) closed at $15B valuation. Software-engineering job openings surged 30 percent in 2026 to 67K+ per TrueUp data — the labor market is repricing around agent-augmented productivity. Google enters I/O with the strongest infrastructure position but the question of whether its consumer-product demonstrations match the back-end capability.

This dispatch is the framework for reading May 19-20. The expected announcements with probability weighting. The variables that signal whether the agentic deployment thesis is real or rhetorical. The strategic implications by stakeholder. The connections to broader threads from the dispatch series.

The dispatch on agentic loop failure modes covered the taxonomy of agent failures that production deployment must solve. The dispatch on the bubble question flagged frontier-lab valuations as one of three contested middle categories — Google’s I/O announcements directly affect the Gemini ecosystem positioning. The dispatch on the $725B hyperscaler capex question covered the demand-pull thesis that justifies Alphabet’s $185B 2026 commitment. I/O 2026 is the demand-side validation event for that thesis.

Demo or deployment.

Cloud Next 2026 already shipped the infrastructure. May 19-20 reveals whether consumer-product demonstrations match back-end capability.

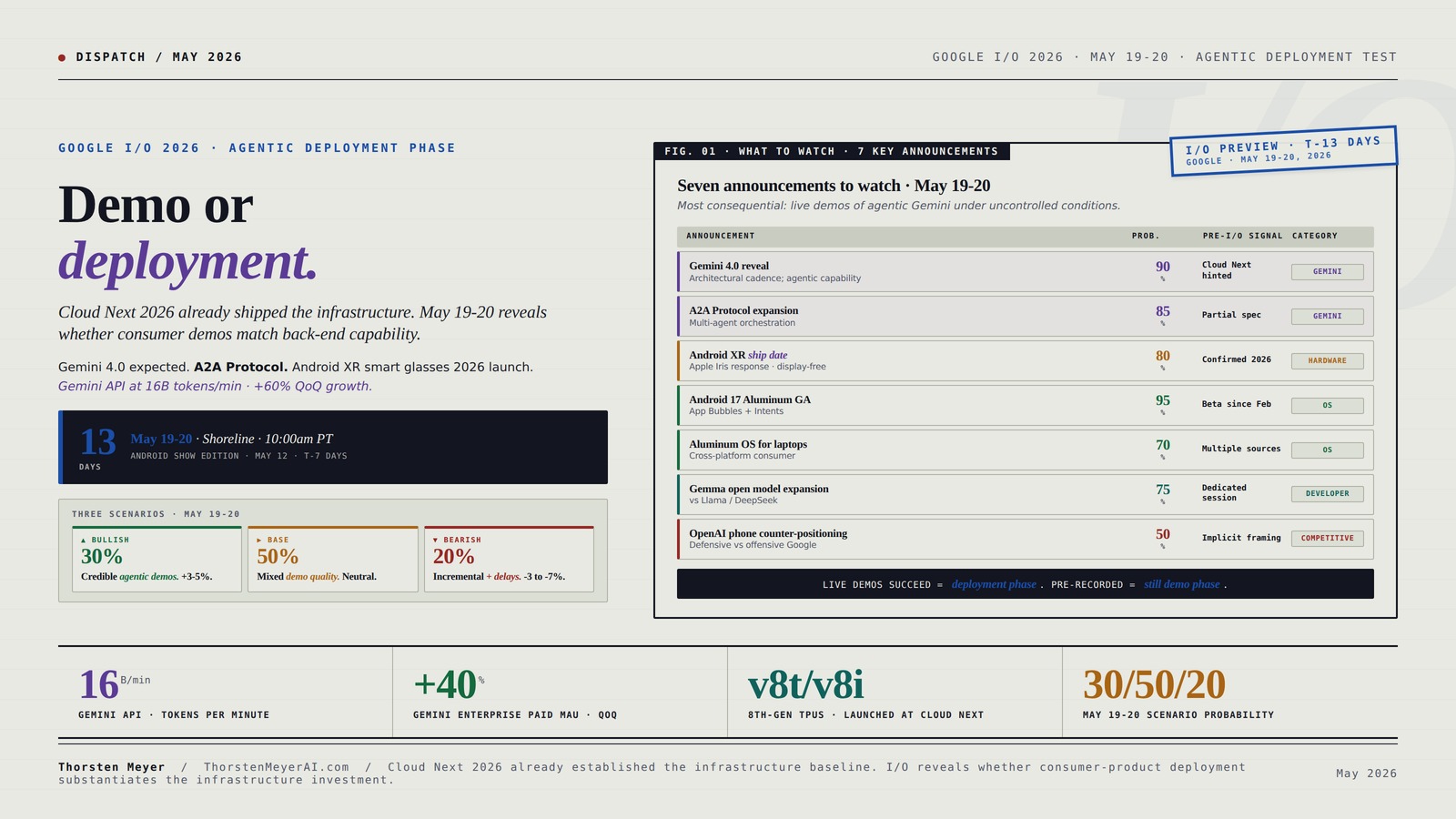

Gemini 4.0 expected centerpiece. A2A (Agent-to-Agent) Protocol. Android XR display-free smart glasses confirmed for 2026 launch. Android 17 (Aluminum) general release. Gemini API at 16B tokens/min · 60% QoQ growth · Gemini Enterprise paid MAU +40% QoQ. Five variables reveal deployment-phase thesis credibility.

May 12 · T-7 days

Ten announcements. Five variables.

The most consequential variable: live demonstrations of agentic Gemini completing real multi-step tasks under uncontrolled conditions. The credibility gap between “agent demos” and “production agent deployment” is wide.

The Complete Google Agent ADK Blueprint: Build 150+ Multimodal AI Agents with Google's Agent Development Kit, Gemini and Google Cloud (The Complete AI Blueprint)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios. One event.

30/50/20 probability allocation. Base case represents normal-execution outcome where some announcements deliver and others slip. Cloud Next infrastructure foundation is locked in regardless.

- Live demos succeedRealistic multi-step tasks complete.

- Smart glasses ship Q3-Q4Display version early 2027.

- Aluminum OS concreteSpecific launch timeline.

- Revenue numbers disclosedSpecific Gemini Enterprise scale.

- Outcome: Stock +3-5%. Capex thesis demand-pull validated.

- Some demos succeedSome scenarios pre-recorded.

- Display-free shipsDisplay version unconfirmed.

- Aluminum directionalNo specific launch date.

- Growth-rate disclosureContinued QoQ%, not absolute.

- Outcome: Stock neutral. Continuation trajectory.

- Gemini 4.0 delayedOr scoped down to 3.5.

- Demos pre-recordedConspicuously controlled.

- Smart glasses pushed 2027Apple wins the timing.

- Aluminum stays conceptualNo launch path.

- Outcome: Stock -3 to -7%. Bubble bear case gains evidence.

I/O 2026 either confirms or undermines the agentic deployment thesis at consumer scale. Cloud Next 2026 already established the infrastructure baseline. I/O reveals whether consumer-product deployment substantiates the infrastructure investment.

AI Smart Glasses with Camera, 4K HD Video & Photo Capture, Real-Time Translation, Recording Glasses with AI Assistant, Open-Ear Audio, Object Recognition, Bluetooth, for Travel (Transparent Lens)

【AI Real-Time Translation & ChatGPT Assistant】AI glasses break language barriers instantly with AI real-time translation. The built-in ChatGPT…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Position based on demonstration quality.

Headline announcements primarily affect long-term product positioning rather than near-term financials. Position based on demonstration-quality variables (live demos, revenue disclosure, case studies). The deeper read: I/O provides forward signal on Q3-Q4 2026 Cloud revenue growth trajectory and the hyperscaler capex thesis demand-pull validation.

Watch Firebase / Antigravity / Flutter GenUI.

Developer-toolchain announcements determine ecosystem stickiness. Specific pricing transparency, production deployment patterns, and security guarantees are the criteria. Production-ready announcements vs framework-with-future-shipping signal different competitive trajectories. Gemma open-model expansion vs Llama / DeepSeek positioning matters.

Read announcements for positioning effects.

Strong I/O demonstrations compress addressable space for non-Google players (Anthropic, OpenAI). Weak demonstrations create competitive opening. The Anthropic IPO positioning particularly affected — strong Google announcements raise the bar for enterprise messaging; weak announcements give Anthropic competitive opening into Q3-Q4 2026.

Integrate I/O signal into multi-vendor sourcing.

Cloud Next infrastructure announcements established platform readiness; I/O announcements about consumer/SMB agent deployment establish ecosystem viability beyond enterprise-only positioning. Multi-vendor sourcing strategies should incorporate I/O signal alongside the bubble question dispatch framework for differentiating durable-value from frothy providers.

Building Solutions with the Microsoft Power Platform: Solving Everyday Problems in the Enterprise

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive Summary · The Watch List in One Table

| Announcement | Probability | Pre-I/O signal | What confirmation reveals |

|---|---|---|---|

| Gemini 4.0 (or 3.5 named differently) | 90% | Cloud Next April 2026 hinted | Architectural cadence; agentic capability advances |

| A2A (Agent-to-Agent) Protocol expansion | 85% | Already partial spec exists | Multi-agent orchestration deployment-readiness |

| Android XR display-free smart glasses ship date | 80% | Confirmed for 2026 launch | Hardware execution; Apple Project Iris response |

| Android 17 (Aluminum) general release | 95% | Beta since Feb 2026 | “App Bubbles” + Intents architecture |

| Aluminum OS for laptops | 70% | Multiple sources confirmed concept | Cross-platform consumer ambition |

| Project Astra production deployment | 65% | Demo-stage at I/O 2024-2025 | Persistent multimodal assistant readiness |

| Veo 4 / video generation update | 60% | Speculative but plausible | YouTube integration, Sora competition |

| Gemma open model family expansion | 75% | Dedicated session confirmed | Open-source positioning vs Llama / DeepSeek |

| Display-equipped XR glasses launch date | 30% | Not confirmed for 2026 | Apple Project Iris timeline pressure |

| OpenAI phone counter-positioning | 50% | Implicit through Aluminum OS framing | Defensive vs offensive Google strategy |

The most likely outcome is a Gemini 4.0 announcement paired with A2A Protocol expansion and Android XR display-free smart glasses with confirmed 2026 ship date. The most consequential variable is whether Google demonstrates agentic Gemini completing real multi-step tasks live on stage — the difference between “demo” and “shipped agent” is the entire deployment-phase thesis. Whether Aluminum OS for laptops gets a real launch timeline (vs continuing as concept) reveals Google’s cross-platform consumer ambition.

Developing AI, IoT and Cloud Computing-based Tools and Applications for Women’s Safety

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

1. The Cloud Next 2026 precedent · what’s already locked in

Reading I/O 2026 correctly requires understanding that Cloud Next 2026 (April 2026) already shipped the enterprise infrastructure foundation. I/O is the consumer-facing layer on top.

The Gemini Enterprise Agent Platform. Cloud Next launched what Thomas Kurian framed as “an operating system for AI agents” — a unified environment for building, scaling, governing, and optimizing AI agents at enterprise scale. Combines Vertex AI capabilities with new tools for orchestration, governance, observability, and agent identity management. The governance layer specifically addresses the question every legal, compliance, and IT team has been asking: how to control thousands of agents. The platform shipped with Agent Identity, Agent Gateway, and Agent Anomaly Detection components — the same governance rigor applied to mission-critical infrastructure.

The eighth-generation TPUs. TPU v8t optimized for training; TPU v8i optimized for inference with 1,152 TPUs in a single pod, 3× more on-chip SRAM, 80 percent better performance-per-dollar versus prior generation. Designed specifically for high-concurrency agentic workloads where millions of agents need to run cost-effectively. The Cloud Next disclosure that just over half of 2026 ML compute investment goes toward Cloud workloads confirms the structural reality: Google is positioning TPU v8 as the economic foundation for agentic deployment at scale. The infrastructure positioning compares directly to NVIDIA’s Rubin platform (covered in the NVIDIA Q1 FY27 dispatch) — both are betting on agentic inference economics through 2027-2028.

The Agentic Data Cloud. Cross-cloud lakehouse with zero-copy access across AWS and Azure, Knowledge Catalog for grounding agents in enterprise-wide semantic context, Deep Research Agent for autonomous intelligence. The multi-cloud framing matters — Google is acknowledging that vendor lock-in is a non-starter for serious AI deployments, which is a meaningful strategic concession from the company most identified with proprietary cloud lock-in historically.

Memory Bank. Persistent context that allows Gemini to remember user preferences across weeks rather than sessions. Ships at Cloud Next; expected to extend to consumer Gemini at I/O. The persistence dimension is structurally important — the agentic deployment thesis requires agents that maintain state across interactions, not just complete-and-reset chat sessions.

Production momentum. Sundar Pichai disclosed at Cloud Next that 75 percent of Google Cloud customers are now using AI products. First-party Gemini API processes 16 billion tokens per minute (up from 10 billion the prior quarter) — 60 percent quarterly growth in API traffic. Gemini Enterprise paid monthly active users up 40 percent quarter-over-quarter. The numbers are real; they substantiate the platform momentum that I/O is positioned to extend to consumer surface area.

The cumulative picture: I/O 2026 doesn’t need to ship the infrastructure (Cloud Next did that). It needs to ship the consumer-facing demonstration that the infrastructure produces credible agentic experience for non-enterprise users. That’s the harder problem.

2. The Gemini 4.0 question · architectural cadence and capability advances

The Gemini 4.0 announcement is the most-watched expectation. The framing matters more than the version number.

The cadence positioning. Gemini 1.0 launched December 2023. Gemini 1.5 February 2024. Gemini 2.0 December 2024. Gemini 2.5 March 2025. Gemini 3.0 fall 2025. Gemini 3.x updates through Q1-Q2 2026. A Gemini 4.0 announcement at I/O 2026 would maintain approximately annual cadence — comparable to NVIDIA’s annual hardware cadence (Hopper → Blackwell → Rubin) and to OpenAI’s GPT-4 → GPT-4.5 → GPT-5 progression. Architectural cadence at the 12-month interval is structurally important because it signals continuous capability advance rather than plateau. Plateau would invalidate the bull case in the bubble question dispatch for frontier-lab valuations.

The capability advances expected. Gemini 3.0 brought “Deepthink” reasoning. Gemini 4.0 is reportedly built on the A2A (Agent-to-Agent) Protocol, which would represent a structural shift from single-model to multi-agent architecture. The capability claim: agents can independently plan and execute multi-step tasks across different applications. The verification question: does Google demonstrate this live on stage with real applications, or does the demonstration depend on simplified scenarios? The credibility gap between “agent demos” and “production agent deployment” is wide; live demonstrations under uncontrolled conditions are the most informative signal.

The Deep Research agent integration. Cloud Next launched the Deep Research Agent for autonomous intelligence work. Consumer Gemini is expected to integrate this capability for individual users. The scope: research synthesis across multiple sources, autonomous operation over hours rather than seconds, structured deliverables (reports, comparisons, decision frameworks). The competitive context: Anthropic’s Claude has been emphasizing similar autonomous research capabilities, and OpenAI’s deep research feature has been a competitive differentiator. The I/O announcement reveals whether Google’s version meaningfully advances the category or matches existing capability.

The Project Astra question. Project Astra has been Google’s persistent multimodal assistant project — running across screen, camera, voice, with shared context. Demo-stage at I/O 2024 and 2025; production-readiness signal at I/O 2026 is plausible. If Astra ships as production feature integrated into Gemini app and/or smart glasses, the multimodal-deployment thesis becomes concrete. If Astra remains demo-stage for a third consecutive year, the credibility of the demo-to-production transition declines materially.

The Gemini Enterprise momentum. 40 percent QoQ paid MAU growth is the strongest single number Google can cite at I/O. The structural question for I/O: does Google announce specific revenue numbers for Gemini Enterprise (it hasn’t disclosed specifics historically), or does it continue to disclose only growth rates? Specific revenue disclosure would signal confidence in the absolute scale. Continued growth-rate-only disclosure signals that the absolute number is still small relative to incumbent enterprise software (Microsoft 365 at ~$50B, Salesforce at ~$35B, etc.).

3. The hardware demonstration · Android XR smart glasses

Android XR smart glasses are the most consumer-tangible hardware demonstration expected at I/O.

The two-product strategy. Google has been developing two distinct Android XR products. The display-free version — camera, speakers, microphones for hands-free Gemini interaction — is confirmed for 2026 launch. The display-equipped version with private in-lens information has not been confirmed for 2026 release. Hardware partners include Samsung, Gentle Monster, and Warby Parker, suggesting a range of styles and price points. The bifurcated approach (simpler product first, more capable product later) is a hedge against execution risk on the display version.

The Apple Project Iris pressure. Apple’s smart glasses leaks have intensified through Q1-Q2 2026. The competitive timing is real — both companies are trying to define the smart glasses category before the other. Google’s structural advantages: Gemini’s multimodal capability, Android’s installed base, partnerships with eyewear brands. Google’s structural disadvantages: hardware execution track record (multiple Pixel hardware delays), brand premium for wearables (Apple has it; Google has been building it). The I/O announcement reveals which pressure point Google emphasizes — software / AI capability or hardware / brand integration.

The Visual Search 2.0 use case. The most concrete demonstrated use case: real-time visual intelligence to identify products and provide instant price comparisons or DIY instructions. The use case is consumer-tangible (e.g., “what is this thing in front of me, where can I buy it cheaper”) and developer-meaningful (e.g., agent integration with shopping APIs, e-commerce, retail). If Google demonstrates a credible end-to-end flow on stage, the smart glasses category gets meaningful product validation.

The display version timeline question. The most consequential variable for Google’s hardware strategy. Confirming a 2026 ship date for the display version would close the timing gap with Apple Project Iris and establish category leadership. Pushing the display version to 2027 maintains current ambiguity and creates space for Apple to define the category first. The I/O announcement on display-version timeline is the structural signal for Google’s hardware strategy through 2026-2027.

4. Android 17 / Aluminum · the OS architecture shift

The Android 17 announcement and the Aluminum OS positioning collectively signal Google’s longer-term OS strategy.

Android 17 (codename Aluminum). Beta since February 2026 with general release expected mid-year (around June-July 2026, ahead of the August Pixel hardware event). The headline feature so far: “App Bubbles” — floating windows that allow AI agents to “peek” into apps (WhatsApp, Gmail, others) to pull information without screen-switching. The deeper architectural shift: Android moving from “Apps” to “Intents” — meaning the OS organizes interactions around what users want to accomplish rather than which app they want to use. The intent-based architecture is the OS-layer enabler for agentic deployment; users describe tasks, agents orchestrate apps in the background.

Aluminum OS for laptops. Multiple sources have confirmed the cross-platform concept — Aluminum OS as an Android-derivative for laptops, parallel to ChromeOS rather than replacing it. Sameer Samat (Google’s Android Ecosystem President) confirmed to Android Authority that Aluminum OS is on track for 2026 debut, pushing back against court documents from the Google antitrust trial that suggested 2028 timeline. The strategic logic: position Android-derivative laptops to compete with macOS in the broader consumer category that ChromeOS doesn’t address. The I/O announcement reveals whether Aluminum OS gets a concrete consumer launch timeline or remains conceptual.

The Apps-to-Intents architecture. The shift from app-centric to intent-centric computing is structurally important. The current paradigm: users open Spotify to play music, Gmail to send email, Chrome to browse. The intent paradigm: users say “play something energetic for my run” or “draft a follow-up to that contractor”; the system orchestrates across apps to fulfill the intent. The architectural shift is enabled by agentic AI capability and by the developer-facing infrastructure that Google has been building (Firebase as “agent-native platform”, Antigravity tool for full-stack applications, Flutter GenUI for AI-generated interfaces). The I/O developer sessions reveal whether the architectural shift is real and developer-ready or marketing positioning.

The competitive context with iOS. Apple has been adapting iOS toward similar intent-based capabilities through Siri intelligence and App Intents framework. The categorical question: does Android 17 / Aluminum get to credible intent-based experience faster than iOS, or does Apple’s more controlled platform and tighter app integration produce a smoother user experience? I/O 2026 demonstrations are the data point on Google’s execution.

5. The developer toolchain · Firebase, Antigravity, agent-native platform

The developer-facing announcements may matter more for long-term ecosystem positioning than the consumer announcements.

Firebase as agent-native platform. Session copy describes Firebase’s evolution into an “agent-native platform” with confirmed path from AI prototyping through production deployment on Google Cloud. Integrations with AI Studio plus Antigravity tool for building full-stack applications. The structural significance: Firebase has been Google’s primary mobile developer platform with substantial installed base. Repositioning Firebase around agent development gives Google a developer-onboarding ramp that competitors lack. The I/O question: does Firebase agent development show clear pricing, security guarantees, and production deployment patterns that developers can act on, or does it remain framework-without-shipping-path?

Antigravity. A tool referenced in session copy as part of the Firebase agent-native platform stack. Limited public information available. The naming (anti-gravity) suggests Google is positioning it as something that removes friction from agent development. The I/O reveal will fill in the actual capability.

Android Studio + Gemini integration. Sessions confirmed for Gemini capabilities integrated directly into Android development workflow. Code completion, agent-based debugging, design-to-code generation. The competitive context: GitHub Copilot at 1.8M+ paid seats, Cursor with strong developer adoption, Anthropic Claude Code expanding. Google’s Android Studio has structural distribution advantage with Android developers but historically limited share among broader developer population. The I/O announcement reveals whether Android Studio + Gemini becomes a credible competitor in the broader IDE category.

Flutter GenUI. Confirmed in session list — capability for building adaptive, AI-generated interfaces dynamically. The use case: developers build skeleton structure; Flutter GenUI generates interface elements based on context and user intent. The structural shift: from designer-built static interfaces to developer-described adaptive interfaces. The I/O demonstration reveals whether the capability ships in production-ready form or remains beta.

Gemma open model family. Dedicated session covering new additions and deployment paths across cloud, desktop, and mobile. Google’s framing positions open model distribution as part of the same platform strategy, not a side track. The competitive context: Llama 4 from Meta, DeepSeek-V3 / V4, Qwen 3, Mistral models all compete for open-source developer mindshare. Google’s structural advantage with Gemma: integration with Vertex AI, Cloud distribution, mobile deployment via Android. The I/O announcement reveals Google’s commitment level to the open-source developer category.

6. The strategic theme · agentic AI deployment-phase test

The over-arching theme of I/O 2026 is whether agentic AI converts from demo-phase to deployment-phase. Multiple variables collectively reveal the answer.

Variable 1 · Live demonstrations under realistic conditions. Pre-recorded demos with controlled scenarios are insufficient. Live demonstrations where Google representatives ask Gemini agents to complete real-world multi-step tasks (book travel with specific constraints, manage calendars with conflicts, handle complex enterprise workflows) are the credibility test. If demonstrations succeed, deployment-phase thesis advances. If demonstrations fail or get conspicuously simplified, the credibility gap widens.

Variable 2 · Specific revenue disclosure for agentic products. Gemini Enterprise 40 percent QoQ growth is impressive but doesn’t disclose absolute scale. Revenue disclosure for specific agentic products (Gemini Enterprise Agent Platform deployments, Project Astra users, Smart Glasses preorders) would signal confidence in absolute numbers. Continued growth-rate-only disclosure suggests the absolute numbers remain small relative to broader Google revenue lines.

Variable 3 · Production case studies with named enterprise customers. Cloud Next 2026 disclosed “1,302 real-world gen AI use cases from leading organizations.” I/O 2026 is the consumer-product equivalent. Specific named-customer case studies with quantified outcomes (productivity gains, cost reduction, revenue acceleration) substantiate the deployment thesis. Anonymized or generic case studies signal that the production deployment is shallower than the marketing positioning.

Variable 4 · Pricing transparency for enterprise agents. Cloud Next launched Gemini Enterprise Agent Platform without detailed public pricing. I/O 2026 reveals whether agent pricing matures (per-agent, per-action, per-API-call structures) or remains in custom-quote phase. Transparent pricing signals product maturity; opaque pricing signals enterprise-deal-stage rather than productized stage.

Variable 5 · Developer adoption metrics. Specific developer adoption numbers for Firebase agent-native platform, AI Studio, Antigravity, Flutter GenUI. Specific app-store data for Android intent-based experiences. Concrete adoption metrics demonstrate developer pull; generic developer-engagement metrics signal Google’s push without verified pull.

The cumulative read across these five variables determines the deployment-phase thesis credibility. Strong signals across at least 3 of 5 variables would substantiate Google’s agentic positioning. Strong signals on fewer than 3 would suggest Google remains in demo-phase despite Cloud Next infrastructure readiness.

7. The connections to other dispatches

I/O 2026 connects to multiple structural threads from this dispatch series.

Connection 1 · Hyperscaler capex absorption. The capex dispatch covered Alphabet’s $185B 2026 commitment (third-largest among the Big Four). I/O announcements that demonstrate concrete consumer demand absorption support the capex thesis. Announcements that remain demo-phase signal capex deployment ahead of demand realization, which compounds the impairment risk vector covered in the capex dispatch.

Connection 2 · NVIDIA addressable share contestation. The NVIDIA Q1 FY27 dispatch flagged NVIDIA addressable share as one of three contested middle categories in the bubble question. Google’s TPU v8t/v8i positioning is the most credible challenger to NVIDIA’s hyperscaler GPU dominance. I/O 2026 announcements that demonstrate TPU v8i economic advantages for agentic workloads (80 percent better performance-per-dollar) support the in-house silicon migration thesis. The thesis gains material support if Google announces specific TPU v8i deployment numbers or customer migration patterns.

Connection 3 · The agentic deployment failure modes. The agentic loop dispatch covered the taxonomy of failures that production deployment must solve. I/O demonstrations are the empirical test. Live demos that succeed against complex multi-step scenarios validate that Google has solved or substantially mitigated the failure modes. Demos that fail or get simplified signal that the failure modes remain unsolved.

Connection 4 · The continual learning research map. The CL dispatch covered the architectural bottleneck for production AI. Memory Bank’s persistent-context capability is one practical-deployment proxy for some CL functionality. If Memory Bank ships at production scale with multi-week persistence and meaningful contextual reasoning, the practical-deployment timeline for CL-adjacent capabilities accelerates relative to the dispatch’s 2028-2030 base case.

Connection 5 · The EU AI Sovereignty dispatch. The dispatch covered the European policy framework. Google’s I/O announcements with EU-specific positioning (data residency, multi-cloud lakehouse, governance layer for agent identity) signal Google’s response to EU regulatory framework. The structural read: Google’s compliance investment is comprehensive (covered in the EU AI Act enforcement dispatch) — I/O may emphasize this as competitive differentiation against less-prepared providers.

Connection 6 · The bubble question disentanglement. The dispatch flagged frontier-lab valuations as one of three contested middle categories. Google’s I/O announcements affect the broader frontier-lab competitive dynamic. Strong agentic deployment signals from Google compress the addressable space for OpenAI, Anthropic, others; weak signals create space for non-Google players to capture the agentic deployment wave.

Connection 7 · The compute concentration audit. The dispatch covered structural concentration in AWS / Azure / GCP. I/O announcements about the cross-cloud lakehouse (zero-copy across AWS and Azure) signal Google’s recognition that pure-Google-Cloud lock-in is non-starter for AI workloads. The strategic concession is structurally important; it implies that the compute concentration audit’s “lock-in” framing may be partially obsolete for AI workloads.

The cumulative picture: I/O 2026 is not an isolated product event. It is the consumer-facing demonstration that the infrastructure announcements at Cloud Next translate to consumer-product deployment. Multiple structural theses from this dispatch series get tested against the I/O demonstration quality.

8. Three scenarios for May 19-20 announcements

The I/O event resolves into one of three structural patterns.

Bullish scenario · 30% probability · “Gemini 4.0 ships with credible agentic demos.” Gemini 4.0 confirmed with meaningful capability advances over 3.x. Live demonstrations succeed against realistic multi-step tasks. Android XR display-free smart glasses ship date confirmed for Q3-Q4 2026. Display-version timeline confirmed for early 2027. Aluminum OS for laptops gets concrete launch timeline. Specific Gemini Enterprise revenue numbers disclosed at meaningful scale. Production case studies with named customers and quantified outcomes. Stock action +3-5 percent over the I/O window. Validates the hyperscaler capex thesis demand-pull side.

Base scenario · 50% probability · “Gemini 4.0 announced with mixed demonstrations.” Gemini 4.0 announced. Live demonstrations partially succeed; some scenarios get conspicuously simplified or pre-recorded. Android XR display-free ships on schedule; display version remains unconfirmed for 2026. Aluminum OS for laptops gets directional roadmap without specific launch date. Gemini Enterprise growth rate disclosed (40 percent QoQ continued); absolute numbers remain undisclosed. Mix of generic and named-customer case studies. Stock action neutral to slightly positive. The base case in the bubble question dispatch for frontier-lab valuations applies — neither bull nor bear thesis materially advanced.

Bearish scenario · 20% probability · “Incremental update + delays.” Gemini 4.0 announcement either delayed (positioned as 3.5 or 3.x update instead) or scoped down. Live demonstrations conspicuously rely on pre-recorded segments. Android XR smart glasses launch date pushed to 2027. Aluminum OS remains conceptual. Limited revenue / case study disclosure beyond what was at Cloud Next. Stock action -3 to -7 percent over the I/O window. Apple Project Iris and OpenAI agentic-OS phone gain narrative space. The bear case in the bubble question dispatch gains material support — frontier-lab valuations face EU-and-Google-specific compression.

The 30/50/20 probability allocation reflects current setup. Setup factors favoring the bullish scenario: Cloud Next infrastructure readiness, Gemini Enterprise momentum, multi-year smart-glasses development. Setup factors favoring the bearish scenario: historical Google demo execution challenges, competitive pressure forcing premature announcements, hardware-execution track record on wearables. The base scenario is most likely because it represents normal-execution outcome where some announcements deliver and others slip.

9. The strategic implications by stakeholder

The I/O event has direct consequences for five distinct stakeholder groups.

For Google / Alphabet investors. I/O is a meaningful but not dominant catalyst for the stock. Gemini Enterprise momentum is already disclosed; I/O announcements primarily affect long-term product positioning rather than near-term financials. Position based on the demonstration-quality variables (live demos, revenue disclosure, case studies) rather than headline announcements. The deeper read: I/O provides forward signal on Q3-Q4 2026 Cloud revenue growth trajectory.

For Google AI ecosystem developers. Watch the developer-facing announcements carefully — Firebase agent-native platform, AI Studio, Antigravity, Flutter GenUI, Gemma. These announcements determine whether building on Google’s stack is durably advantaged versus building on Anthropic / OpenAI / Meta / open-source alternatives. Specific pricing transparency, production deployment patterns, and security guarantees are the criteria.

For competitive AI labs (Anthropic, OpenAI). Google’s announcements affect competitive positioning. Strong I/O demonstrations compress the addressable space for non-Google players; weak demonstrations create space. The competitive read for Anthropic IPO positioning — strong Google announcements raise the bar for Anthropic’s enterprise messaging; weak announcements give Anthropic competitive opening.

For enterprise AI customers. I/O provides decision-relevant information about Google’s agentic platform maturity. Cloud Next infrastructure announcements established platform readiness; I/O announcements about consumer/SMB agent deployment establish ecosystem viability beyond enterprise-only positioning. Multi-vendor sourcing strategies should incorporate I/O signal alongside the bubble question dispatch framework for differentiating providers.

For policymakers. Google’s I/O announcements with regulatory positioning (data residency, governance, agent identity) signal industry response to regulatory frameworks. The compliance investment depth visible at I/O reveals which providers are best-positioned for the EU AI Act enforcement Q3-Q4 2026 phase. Google’s positioning is one data point on the cooperative-vs-confrontational provider spectrum.

What to Do This Quarter (Through May 20)

1. Watch the live demonstrations carefully. The single most informative variable. Live multi-step agent demonstrations under realistic conditions either substantiate or undermine the deployment-phase thesis. Pre-recorded demos with controlled scenarios are insufficient signal.

2. Track the disclosure depth. Specific revenue numbers for Gemini Enterprise, named-customer case studies with quantified outcomes, pricing transparency for agentic products. Disclosure depth correlates with product maturity. Continuing growth-rate-only disclosure signals smaller absolute scale.

3. Evaluate the developer toolchain commitments. Firebase agent-native platform, Antigravity, Flutter GenUI, Gemma. These determine ecosystem stickiness. Production-ready announcements vs framework-with-future-shipping-path announcements signal different competitive trajectories.

4. Assess the hardware ship dates. Android XR display-free smart glasses ship date (confirmed for 2026) is the structural signal. Display-equipped version ship date, Aluminum OS for laptops launch timeline, Pixel hardware integration with Gemini agentic features. Hardware execution remains Google’s structural weakness; I/O announcements either confirm or deny improvement.

The Strategic Read

Google I/O 2026 on May 19-20 is the consumer-facing demonstration event for the agentic AI deployment thesis. Cloud Next 2026 in April already shipped the enterprise infrastructure foundation: Gemini Enterprise Agent Platform, eighth-generation TPUs (v8t training, v8i inference with 80 percent better performance-per-dollar), Agentic Data Cloud with cross-cloud lakehouse, Memory Bank persistent context. First-party Gemini API at 16B tokens/min (60 percent QoQ growth), 40 percent QoQ paid MAU growth on Gemini Enterprise. The infrastructure foundation is in place. I/O is the consumer-product layer.

The most likely outcome: Gemini 4.0 announcement paired with A2A Protocol expansion, Android XR display-free smart glasses with confirmed 2026 ship date, Android 17 (Aluminum) general release, Aluminum OS for laptops directional roadmap, Veo 4 / Project Astra / Gemma updates. The most consequential variable: live demonstrations of agentic Gemini completing real multi-step tasks under uncontrolled conditions. The credibility gap between “agent demos” and “production agent deployment” is wide; live demonstration quality is the primary signal.

Five variables collectively reveal the deployment-phase thesis: live demonstration quality, specific revenue disclosure depth, named-customer production case studies, agentic product pricing transparency, developer adoption metrics. Strong signals across at least 3 of 5 substantiate Google’s agentic positioning. Weaker signals suggest Google remains in demo-phase despite infrastructure readiness.

Three scenarios with 30/50/20 probability allocation. Bullish: Gemini 4.0 ships with credible agentic demos, smart glasses on schedule, Aluminum OS concrete timeline, specific revenue disclosure. Base: Gemini 4.0 announced with mixed demonstrations, hardware partial, growth-rate-only disclosure. Bearish: incremental update, pre-recorded demos, hardware delays, limited disclosure beyond Cloud Next. Stock action range -7 to +5 percent over the I/O window depending on scenario.

The connection to the broader threads runs deep. I/O announcements affect the hyperscaler capex thesis demand-pull validation, the NVIDIA addressable share contested middle category, the agentic loop failure modes empirical test, the continual learning research map practical-deployment timeline, the bubble question disentanglement frontier-lab competitive dynamic, the EU AI Act enforcement compliance positioning. I/O 2026 is the consumer-facing test of multiple structural theses simultaneously.

The strategic implications run by stakeholder. Google investors should position based on demonstration-quality variables rather than headline announcements. Developers should watch developer-toolchain announcements for ecosystem stickiness. Competitive AI labs should read Google’s announcements for competitive positioning effects. Enterprise customers should integrate I/O signal into multi-vendor sourcing strategies. Policymakers should observe Google’s regulatory-positioning signals.

The deeper signal: I/O 2026 either confirms or undermines the agentic deployment thesis at consumer scale. The competitive backdrop intensifies the stakes — OpenAI’s rumored agentic-OS phone, Apple Project Iris pressure, Meta’s ARI humanoid acquisition, Sierra at $15B valuation. Google enters with the strongest infrastructure position but faces the question of whether consumer-product demonstrations match back-end capability. May 19-20 settles questions that no amount of analysis can settle in advance.

The honest assessment: the most likely scenario is the base case — credible Gemini 4.0 announcement with mixed demonstration quality, partial hardware execution, continued growth-rate-only disclosure. The probability of either tail outcome (strong validation or clear shortfall) is meaningful but lower. The structural insight is that Cloud Next 2026 already established the infrastructure baseline; I/O reveals whether consumer-product deployment substantiates the infrastructure investment.

Google I/O 2026 May 19-20. T-13 days. Theme: agentic AI deployment-phase test. Cloud Next 2026 already shipped infrastructure foundation. Gemini 4.0, A2A Protocol, Android XR smart glasses, Android 17 Aluminum, Aluminum OS expected. Five variables reveal deployment-phase thesis credibility. Three scenarios with 30/50/20 probability allocation. Connects to hyperscaler capex, NVIDIA addressable share, agentic failure modes, continual learning, bubble question, EU enforcement threads simultaneously.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The NVIDIA Q1 FY27 Earnings Preview

- The $725B Hyperscaler Capex Question

- The Bubble Question, Disentangled

- The Agentic Loop Failure Modes

- The Continual Learning Research Map

- The EU AI Act Enforcement Countdown

Sources

- Adam Lobo Media · Google I/O 2026: The Rise of Agentic AI and the Gemini 4.0 Reveal · May 2026

- MSN / Mashable · Google I/O 2026 to spotlight AI, XR, and new OS · May 2026

- Google Cloud Next 2026 announcements · April 2026 — Gemini Enterprise Agent Platform, TPU v8t/v8i, Agentic Data Cloud, Memory Bank

- Google blog · Sundar Pichai shares news from Google Cloud Next 2026 · April 2026 — 16B tokens/min, 40% QoQ paid MAU growth, 50%+ ML compute investment to Cloud

- Egen.ai · Three biggest AI announcements from Google Cloud Next 2026 — Agent Platform, TPUs, Data Cloud

- OpenTools.ai · Google I/O 2026: AI, Gemini Updates, Android XR Innovations

- Gadget Hacks · What to Expect from Google I/O 2026 — official schedule, Shoreline, May 19-20

- Yahoo Tech · What to expect from Google I/O 2026 · May 2026 — Android XR two-product strategy

- TrueUp · 30% increase in AI software jobs · 67K+ openings · 2026

- Sierra · $950M round at $15B valuation · April 2026

- Sameer Samat (Google Android Ecosystem President) · Aluminum OS confirmed 2026 timeline (Android Authority)