Read the 2026 agentic-AI numbers side by side and they appear to describe different planets.

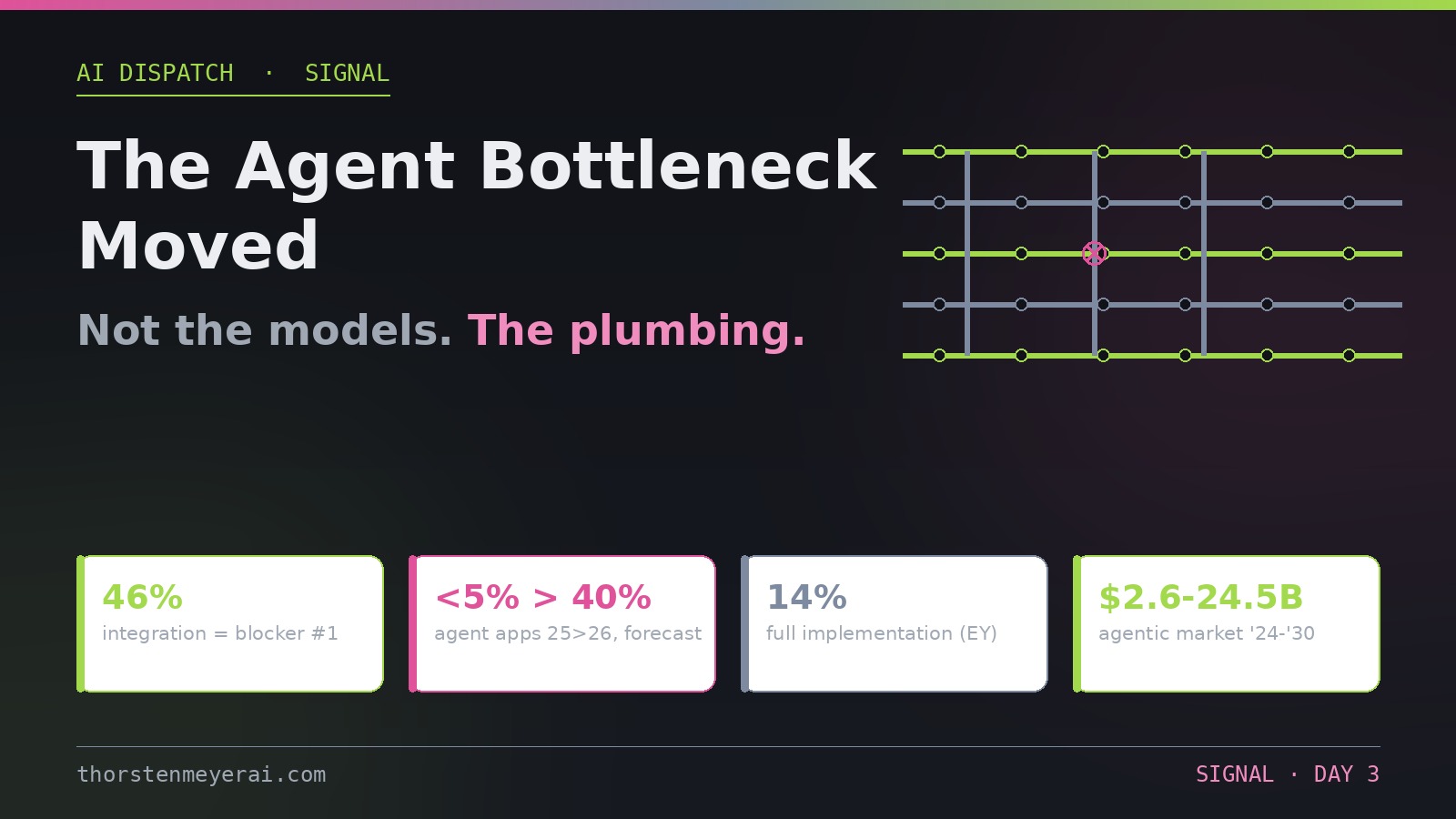

Gartner projects 40% of enterprise applications will carry task-specific AI agents by the end of 2026 — up from under 5% in 2025, an eight-fold jump in a single year. EY’s survey finds 34% of organizations have started implementing agentic AI and only 14% report full implementation. One industry tracker claims 72% production adoption; a meta-analysis of thirty-plus surveys finds most companies still stuck in experimentation, with a ~56-point gap between experimenting and even partial deployment.

These can’t all be true, and the honest reading is that most of them are measuring hype-adjacent categories with elastic definitions. But underneath the survey chaos, one finding shows up consistently across sources that otherwise agree on nothing — and it’s the actual signal.

The Agent Bottleneck Moved —

It’s Not the Models, It’s the Plumbing

Same-day-verified meta-trend · the one finding the conflicting surveys agree on

The survey chaos, plotted honestly

The inversion

2024–25: WHICH MODEL?

Capability was scarce, so the model was the moat. That race now resets weekly — frontier-class open weights every few weeks, from multiple labs.

2026: WHOSE PLUMBING?

Orchestration, tool access, evaluation harnesses, queues, audit trails, inference economics. Capability commoditized; infrastructure didn’t.

STEELMAN: WHY ENTERPRISES ARE SLOW

Not stupidity — their agents touch payroll, patients, and production, where cascading failures have consequences a solo builder’s stack never faces. Bounded autonomy and governance gaps are rational responses to real risk. Small operators defer that reckoning; they don’t escape it.

The signal: stop watching model benchmarks to predict who wins the agent era. Watch who owns the plumbing. The bottleneck moved there, the money is following — and the structural advantage runs, for once, toward operators small enough to own their whole stack.

ENTERPRISE COHERENCE in the Age of AI

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The bottleneck relocated

Anthropic’s State of AI Agents report puts it plainest: 46% of teams building agents cite integration with existing systems as their primary challenge. Not model capability. Not cost. Integration — secure, reliable, governed access to the CRMs, ticketing systems, internal APIs, and databases where real work lives.

That matches what the trend literature converges on for 2026: orchestration frameworks maturing, tool integration standardizing, evaluation pipelines becoming embedded infrastructure, “bounded autonomy” replacing free-running agents, and governance frameworks lagging deployment badly. The models got good enough quarters ago — this week’s earlier Signal showed frontier-class capability now refreshes on a weeks-long cycle, from multiple labs, at open-weight prices. Capability is being commoditized. Infrastructure is not.

That inversion is the meta-trend: the competitive question has shifted from which model to whose plumbing — who owns the orchestration layer, the tool connections, the evaluation harness, the queue, the audit trail, and the inference economics underneath it all. And on that last point, one widely-cited projection puts global inference spending above $150 billion in 2026 — the ongoing cost of running agents, which dwarfs the training costs everyone fixates on. (Treat the precise figure with care; the direction is what matters.)

Agentic AI Orchestration: Building Multi-Agent Systems from Scratch

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why this favors small operators more than anyone admits

Here’s the reading you won’t find in the consulting decks, though it follows directly from their own data. If integration and governance are the bottleneck, then the advantage goes to whoever has the shortest integration surface — and nobody’s is shorter than a solo operator who owns every layer of their own stack.

An enterprise deploying agents must thread them through decade-old systems, three compliance regimes, and a security review board. A builder running an agent fleet against their own infrastructure — own queue, own database, own local inference, own tooling — skips the entire 46%-problem. This morning’s Corvus dispatch is the live demonstration: the reason a one-person WAMI exploitation product is even thinkable is not that models got smart. It’s that for a vertically-owned stack, the integration tax rounds to zero, and that’s where all the friction was.

The enterprise agentic market is forecast to grow roughly tenfold — $2.6 billion in 2024 to $24.5 billion by 2030 — and most of that spend will land not on models but on exactly this connective tissue: orchestration, metering, governance, evaluation. Which means the incumbent software vendors and the agent-native builders are now racing toward the same layer from opposite directions.

AI and Microservices: Integrating AI into API Design and Distributed Microservice Architecture

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The steelman and the caveat

The case against the small-operator thesis is real: enterprises aren’t slow because they’re stupid — they’re slow because their agents touch payroll, patients, and production systems, where a cascading agent failure has consequences a solo builder’s stack never faces. Bounded autonomy and governance gaps are rational responses to genuine risk, and the survey chaos partly reflects honest difficulty in defining what “deployed” even means when the failure modes are still being discovered. Small operators don’t escape this — they defer it until the day their product has to pass someone else’s security review.

And the numbers caveat, per house policy: nearly every figure above is vendor- or consultancy-reported, definitions vary wildly between surveys, and the 40%-by-2026 projection is a forecast, not a measurement. The convergent finding — integration is the bottleneck — is the only claim here that multiple independent sources support.

Workflow Automation with Microsoft Power Automate: Design and scale AI-powered cloud and desktop workflows using low-code automation

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The signal, compressed

Stop watching model benchmarks to predict who wins the agent era; that race resets weekly. Watch who owns the plumbing — orchestration, tool access, evaluation, inference economics. The bottleneck moved there, the money is following it, and for once the structural advantage runs toward operators small enough to own their whole stack.

Sources: Anthropic State of AI Agents 2026 via Arcade.dev (integration finding); Gartner projections via Nevermined and Accelirate summaries (flagged as forecasts); EY AI Pulse Survey via Nevermined; First Page Sage agentic adoption meta-analysis (July 2026); AI Handbook agentic trends review; market sizing and inference-spend projections via Nevermined and AetherLink (vendor-reported, treated as directional).