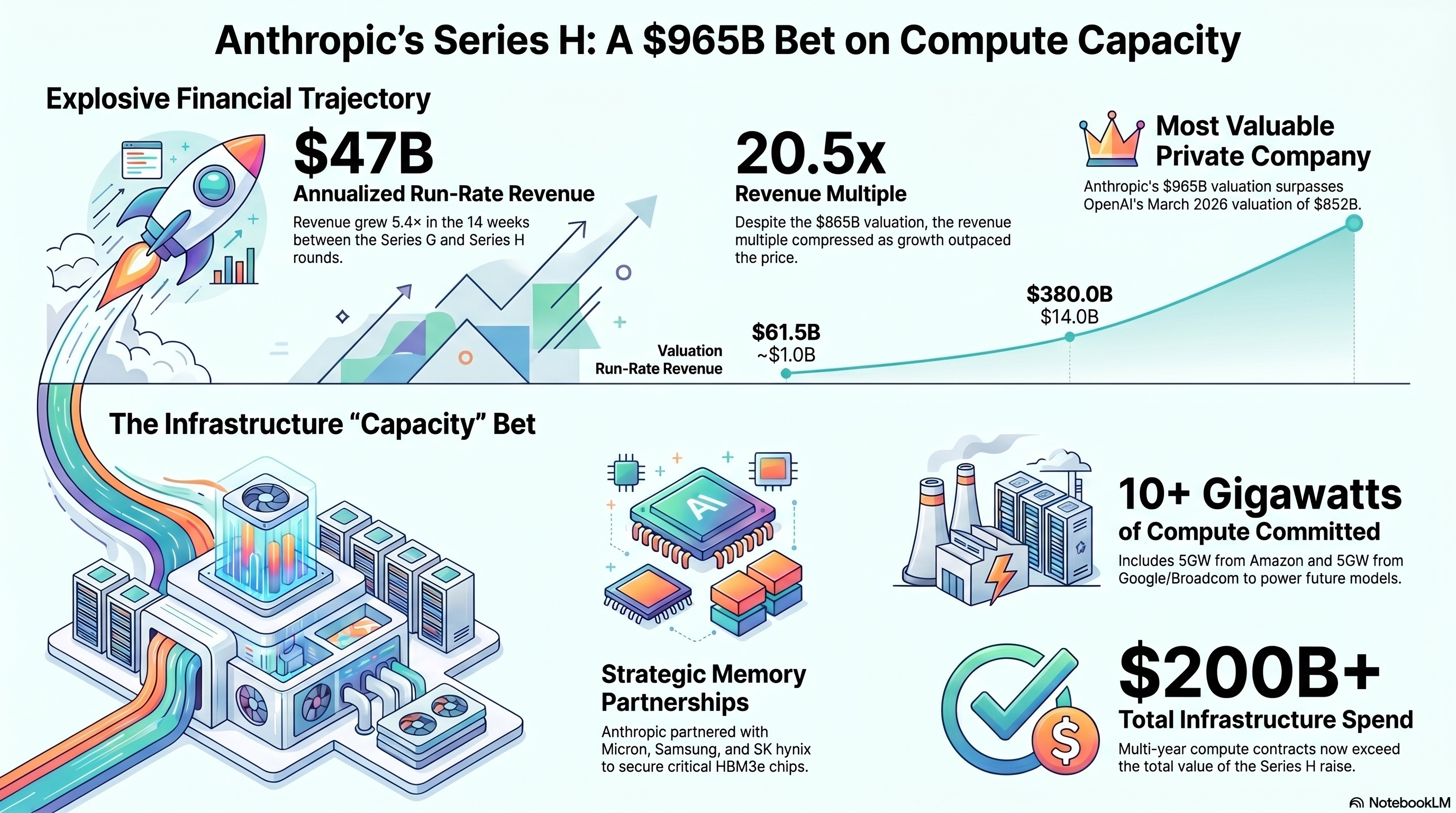

Anthropic announced today, May 28, 2026, that it has closed a $65 billion Series H round at a $965 billion post-money valuation. The headline writes itself — the largest private financing in history, edging Anthropic past OpenAI’s March valuation of $852 billion to become the most valuable private company on Earth. In just over a year, the company has gone from a $61.5 billion valuation in March 2025 to nearly a trillion dollars. That’s a 15.7× increase in fourteen months. In B2B software, no precedent exists. Salesforce took roughly two decades to reach the revenue numbers Anthropic just blew past.

But the story most coverage will land on — “AI startup raises history’s biggest round” — misses what’s actually interesting in the press release. The four paragraphs that matter most are buried in the middle, and they reframe what this round is for. Anthropic named three memory chipmakers — Micron, Samsung, and SK hynix — as “strategic infrastructure partners,” and itemized more than 10 gigawatts of compute commitments. Read carefully, this isn’t really a valuation round. It’s a capacity round — a bet, made at unprecedented scale, that compute is the bottleneck between today’s revenue and a much larger tomorrow.

Let me walk through what’s actually in the announcement, why the multiple is the most surprising number on the page, and the honest tension nobody covering this is naming clearly.

$965B and climbing — it’s really a compute bet

The viral headline is the valuation. The interesting story is in the press release’s middle paragraphs — and in three chipmakers Anthropic just named as strategic partners. This is a capacity round dressed as a funding round.

The numbers nobody can quite parse in sequence

Read together they describe a trajectory with no precedent in enterprise software. Read individually, each looks like a typo.

GEEKOM GT15 Max Strong Performance AI Mini PC, with Intel Core Ultra 9 285H&Arc 140T GPU (99 Tops), 32GB RAM&1TB SSD|Windows 11 Pro|WiFi 7|Dual 2.5GbE| USB4|8K Video Editing|for Home Office&Gaming

🚀Unmatched AI Acceleration for Ultimate Productivity – The GT15 Max Ultra 9 mini PC features Intel Core Ultra…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

From $61.5B to $965B in fourteen months

Salesforce took roughly two decades to reach revenue numbers Anthropic just blew past. The sequence below is the part most coverage skips — it’s not the size, it’s the shape.

Anthropic’s valuation ladder · Mar 2025 → May 2026

Five rounds, fourteen months. Bar height is the valuation; the climb itself is the story. Tap any milestone for context.

Hewlett Packard Enterprise ProLiant DL380 Gen11 Rack Server w/one Intel Xeon Gold 6530 Processor, 2.1GHz, 32c 1P 2x32GB-R 8SFF MR416i-o 2x960GB SSD 2x1000W PS (HPE Smart Choice P83314-005)

HPE SMART CHOICE MODEL – P83314-005 – READY FOR HPC AND AI Preconfigured and factory-tested, this Smart Choice…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The multiple actually got cheaper

Bubbles look like multiples expanding while revenue lags. Anthropic’s pattern is the inverse — the valuation tripled, but revenue grew faster, and the multiple compressed.

Revenue-to-valuation multiple · Series G → Series H

Same company, three months apart. The denominator (revenue) is outrunning the numerator (valuation) — exactly the opposite of what a bubble narrative predicts.

INLAND 16GB Class 10 SDHC Flash Memory Card Standard Full Size SD Chip USH-I U1 Trail Camera by Micro Center (2 Pack)

Full-size SD card, 16GB SDHC flash memory card 2 pack. Not compatible with mobile phones due to physical…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

10+ gigawatts and three chipmakers

When you name Micron, Samsung & SK hynix alongside your equity backers, you’re saying the binding constraint isn’t demand or model quality — it’s the physical supply of memory chips. The Series H is a capacity round.

Compute commitments backing Anthropic’s capacity bet

$200B+ in announced compute spend across multi-year contracts. The $65B Series H raise has to be read against that bill, not against operating losses.

The AI Factory Handbook: Build, Manage, and Scale NVIDIA AI Infrastructure (NCA-AIIO Exam Prep & Real-World Operations)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

A genuinely durable bet — or a structural exposure?

Both readings can be true at once. The answer arrives over the next 18–24 months as the gigawatts come online and either fill with paying demand or don’t.

Revenue growth has no precedent in B2B software ($1B → $47B in 17 months). The multiple is compressing, not expanding. Claude is the only frontier model on all 3 major clouds. Enterprise AI spend share went from ~10% to >65% in a year. Compute commitments are tied to specific contracts with capacity dates.

20× revenue is not cheap by any historical software-investing standard. Revenue is reported gross of cloud-reseller pass-throughs, which inflates the top line. Profitability is 2 years out. Amodei’s own warning: a 12-month delay in AI progress “would make him bankrupt” — the compute commitments are a structural exposure to demand persistence.

The valuation race — and the IPO context

Anthropic shipped Opus 4.8 the same morning as Series H — not a coincidence. One week after OpenAI filed confidentially for IPO. The late-2026 frame is set: two frontier AI companies racing to public markets, each pitching durability.

The numbers, ordered for sense-making

Start with the trajectory, because once you see it sequenced the speed becomes legible. March 2025: $61.5 billion valuation. September 2025: $183 billion (Series F, $13B raised). February 2026: $380 billion (Series G, $30B raised). May 2026, today: $965 billion (Series H, $65B raised). Across that span, run-rate revenue moved from roughly $1 billion in December 2024, through $9 billion at the end of 2025, $14 billion at the time of the Series G three months ago, and crossed $47 billion earlier this month per Anthropic’s own disclosure today.

Pause on that last number. Anthropic’s run-rate revenue grew 5.4× in the roughly fourteen weeks between Series G and Series H. That is not a typo. The Wall Street Journal and CNBC have separately reported the company is on track for $10.9 billion of revenue in Q2 alone — more than the entire year of 2025 — and Anthropic has told investors annualized run-rate will surpass $50 billion by the end of June. Dario Amodei told a developer audience this month that annualized revenue and usage grew 80× in the first quarter of 2026.

The round was led by Altimeter, Dragoneer, Greenoaks, and Sequoia, with the Series G’s leads (GIC, Coatue) co-leading this one alongside Capital Group, D1, ICONIQ, and XN. The investor list reads like a roster of every major institutional pool — Baillie Gifford, Blackstone, Brookfield, Fidelity, T. Rowe Price, Jane Street, Temasek, MGX, DST, the BlackRock affiliated funds. Fifteen billion dollars of the round is previously-committed hyperscaler money, including $5 billion from Amazon. Microsoft and Nvidia continue to figure as strategic partners through prior commitments. This is the kind of round where the list is the message: nobody who matters declined to participate.

The paradox: the multiple actually got cheaper

Here is the genuinely surprising arithmetic. At Series G in February — $30 billion raised at $380 billion post-money against $14 billion of run-rate revenue — Anthropic was trading at roughly 27× revenue. Substack analyst Shanaka Anslem Perera wrote at the time that this multiple “encodes a bet most allocators have not fully priced,” and called it the headline number to watch.

At Series H today — $965 billion post-money against $47 billion of run-rate revenue — the multiple is roughly 20.5×.

That’s lower. The valuation tripled in three months, but revenue grew faster than the valuation, and the multiple compressed. This is the opposite of what a bubble narrative predicts. Bubbles look like multiples expanding while revenue lags. Anthropic’s pattern is the inverse: explosive revenue growth pulling the multiple down even as the absolute valuation climbs into territory previously reserved for the largest public companies on Earth. Whether that is sustainable or simply slower-than-revenue is a real question — but it is a different question than the one the headline number invites.

The comparison to OpenAI sharpens it. OpenAI’s March 2026 valuation was $852 billion against approximately $13 billion of 2025 revenue — call it ~65× trailing-year revenue, or roughly 30× on the higher run-rate figures it reports. Anthropic at 20.5× run-rate is the cheaper of the two megacaps on the most defensible multiple. None of which makes 20.5× a bargain — public software companies trade at 10–15× even for the strongest — but it does mean the framing of “Anthropic is even more expensive than OpenAI because it’s smaller” no longer holds. As of today, Anthropic is larger by valuation, growing faster, and trading at a smaller multiple than its closest rival.

A genuine caveat worth flagging plainly: Anthropic reports revenue from cloud resellers (AWS, Google, Microsoft) on a gross basis — counting total end-customer spend through those channels as Anthropic revenue, then booking partner payouts as expenses. Sacra’s analysts have noted that this inflates the top line versus peers that report net. The $47B figure is the right number for what Anthropic discloses, but it is not the apples-to-apples comparison some readers will assume.

The bet: compute as the binding constraint

This is the part of the announcement that nobody is leading on, and it’s the most analytically interesting. Anthropic devoted three of the post’s nine paragraphs to compute. The lines that matter:

They named Micron, Samsung, and SK hynix as strategic infrastructure partners — and these aren’t cloud providers, they’re memory and storage chipmakers. That is a meaningful tell. When you start naming the companies that make HBM3e and DDR5 alongside your equity backers, you are saying that the binding constraint on your near-term growth is no longer demand and no longer model quality — it’s the physical supply of the chips that run them.

Then the gigawatts ledger, which they restated in the announcement. Five gigawatts of Amazon capacity, including nearly one gigawatt of new capacity online by end of 2026. Five gigawatts of Google plus Broadcom TPU capacity beginning in 2027 — Broadcom’s filing pegged this at 3.5GW of next-gen TPUs, ramping. SpaceX’s Colossus 1 (300 megawatts, 220,000 NVIDIA GPUs, live now) plus Colossus 2. A $30 billion Azure commitment through the Microsoft/Nvidia partnership. A $50 billion American AI infrastructure investment with Fluidstack. Claude is now the first frontier model available on all three of the world’s largest clouds — AWS, Google Cloud, Microsoft Azure — with AWS confirmed as primary cloud and training partner.

Stack that together and the compute commitments alone are well north of $200 billion in announced spend across multi-year contracts. The Series H raise of $65 billion has to be read against that bill, not against operating losses. This is why the company can be profitable in 2028 (per its own projection) while being deeply unprofitable today: the unprofitability is capital expenditure on capacity to handle revenue that hasn’t fully arrived yet. That’s a very different shape of unprofitability than burning cash to acquire customers who don’t pay.

The honest counter-read is that this is a high-stakes wager that the demand keeps arriving on the schedule the contracts assume. Amodei told Fortune in February, days after Series G, that a twelve-month delay in AI progress “would make him bankrupt.” That is not a casual remark from a CEO standing on a $965 billion valuation — it is an acknowledgement that the bet is structural. The compute commitments are roughly the size of small countries’ GDPs, made on the premise that the revenue curve doesn’t bend. If model improvement slows, if competitor catch-up accelerates, if enterprise demand normalizes, the cost structure stays. That’s the actual risk, and it’s quite different from the imagined risk of “AI bubble pops.”

Why today, and why this size

The timing is not coincidence. Anthropic shipped Claude Opus 4.8 the same morning — the launch I covered earlier today, focused on a “4× honesty” improvement and dynamic workflows in Claude Code. Ship a product and the round on the same day and the narrative pairing is deliberate: look at our momentum and our staying power, in the same news cycle. This is also one week after OpenAI filed confidentially for its IPO with Goldman Sachs and Morgan Stanley, targeting a public listing as early as September 2026. The frame for late 2026 is now set: two frontier AI companies racing toward public markets, each making the case that they are the more durable bet. Anthropic’s pitch today is “we passed them in valuation, we’re growing faster, we’re trading at a lower multiple, and we still have the option to remain private.”

The “still have the option” part may matter most. The Sacra writeup from earlier this month described this round as possibly Anthropic’s final private financing before a potential IPO. With $65 billion raised at terms that almost certainly include limited investor exit obligations, Anthropic has bought itself the ability to choose its own IPO timing rather than be forced to it. That optionality is itself worth real money in a market where public-market timing risk has burned plenty of late-stage private companies.

What I want the careful reader to take away

The bull case here is real and worth naming without hedging. Revenue is genuinely growing at a rate that has no precedent in enterprise software history. The multiple is compressing, not expanding. Claude has reached primary-tool status across enterprise AI spending — share went from ~10% at the start of 2025 to >65% in February 2026, with Claude Code holding 54% market share in programming work specifically. The investor list is exhaustive and the lead investor mix is the strongest possible. The compute commitments are aggressive but they are tied to specific contracts with capacity dates, not abstract spend.

The sober case is also real. Twenty-times revenue is not cheap by any historical software-investing standard. The gross-basis revenue reporting flatters the multiple. The $200+ billion in compute commitments is a structural exposure to demand persistence — and if demand merely normalizes rather than collapses, the math gets uncomfortable. Profitability is two years out by the company’s own projection. The “bankruptcy if AI progress delays twelve months” comment from Amodei is honest and chilling in equal measure. And there is the always-present base-rate observation that the largest private financings in history have, historically, been roughly contemporaneous with the peaks of their cycles.

Both readings can be true at once. What today’s announcement actually demonstrates is that the people writing the checks — the Sequoias, GICs, Coatues, Blackrocks, T. Rowe Prices of the world — have decided the demand is structural enough to justify capacity commitments at this scale. They could be wrong. They are not stupid. The story to watch is not whether the valuation is “justified” by next quarter’s revenue; it is whether the gigawatts Anthropic has just bought can be filled with paying demand on the schedule the contracts assume. That answer will arrive over the next eighteen to twenty-four months. Everything between now and then is positioning.

The clearest read I can offer is the one the press release itself implies but doesn’t say plainly: this round is not about validating where Anthropic is. It is about funding the physical infrastructure to find out whether it can be much larger. The product, the model lineage, the customer adoption — those are the trailing evidence that the bet is plausible. The compute is the bet itself.

Sources: Anthropic’s Series H announcement (May 28, 2026); Sacra; CNBC; Wall Street Journal reporting; Bloomberg; TechCrunch; CB Insights. Run-rate figures are Anthropic-disclosed and reflect gross-basis reporting for cloud-reseller revenue. Independent commentary in this piece is editorial, not affiliated with Anthropic or its investors. Figures current as of the May 28 announcement and will move quickly.