Founded January 2019. Once “Germany’s OpenAI.” November 2023 Series B announced as “more than $500 million.” Mid-2024 pivot away from frontier-model competition. October 2025 founder departure. January 2026 17% workforce reduction. April 2026 acquisition by Canadian Cohere in a $20B combined-entity deal, with Aleph Alpha shareholders receiving 10%. The cost of getting the structural lesson right late.

By Thorsten Meyer — May 2026

This is the fifth standalone essay in the European sovereign-LLM track. The prior four essays examined four institutional answers to the European sovereign-LLM question that were still forward-looking at the time of writing: AMÁLIA (Portugal · national continuation · final version June 2026), Minerva (Italy · national from-scratch · ongoing iteration), OpenEuroLLM (pan-European consortium · first models July 31, 2026), and Mistral (France · commercial-frontier · €3B+ raised · operationally Europe’s strongest single-firm play). Together they document four distinct architectural and institutional bets about what European sovereign-AI development requires.

This piece is structurally distinct from the prior four. Aleph Alpha is not a forward-looking case study. It is a retrospective one. The company already navigated the strategic question the prior four essays document, made the pivot from frontier-capability competition to enterprise-sovereignty positioning in mid-2024, and culminated in the most institutionally important European sovereign-AI deal of 2026: the April 24, 2026 merger with Canadian Cohere in a $20 billion combined-entity transaction. Aleph Alpha shows the cost of getting the structural lesson right late.

The headline finding of this piece: Aleph Alpha is the cautionary tale that retrospectively validates the structural finding from Essay 04. Founder Jonas Andrulis stated explicitly in a December 2025 Handelsblatt interview:

“No European company can build a frontier model in isolation; the question is which combination of partners produces a credible alternative to the American hyperscalers.” — Jonas Andrulis, Aleph Alpha founder, Handelsblatt, December 2025

This is the public acknowledgment from the founder of the company that exited the frontier-capability race that the structural finding from Essay 04 is correct. The European sovereign-LLM movement’s frontier-capability gap is structural to current funding and compute scales, not to institutional choices. Mistral’s empirical results demonstrated this from the commercial-frontier side. Aleph Alpha’s strategic pivot, leadership transition, and eventual acquisition demonstrate it from the cautionary side.

The structural argument I want to make in this piece: the European sovereign-AI movement should treat the Aleph Alpha trajectory as a reference case for what happens when companies attempt frontier-capability competition at insufficient resource scale. The cost of getting the lesson right late — measured in delayed pivot, leadership transition, workforce reduction, founder departure, and 10% shareholder dilution in the Cohere merger — is substantial. The cost of getting the lesson right on time is less than the cost of getting it right late. That is what the Aleph Alpha case demonstrates for every subsequent European AI initiative.

This piece walks the Aleph Alpha trajectory forensically, surfaces the structural lessons the four-way essay track should integrate, and closes with what the Cohere merger means for the European sovereign-AI landscape broadly. The standard caveat applies: the Cohere merger is recent (April 24, 2026) and integration risks are real. The combined entity’s eventual operational trajectory may shift the strategic assessment further.

Aleph Alpha.

The retrospective

case.

Founded January 2019. Once “Germany’s OpenAI.” Mid-2024 pivot away from frontier-model competition. April 2026 acquisition by Canadian Cohere in a $20B deal — Aleph Alpha shareholders 10%. The cost of getting the structural lesson right late.

Aleph Alpha is structurally distinct from the prior four essays in this track. It is not a forward-looking case study. It is a retrospective one — the company already navigated the strategic question Essays 01-04 documented, made the pivot from frontier-capability competition to enterprise-sovereignty positioning in mid-2024, and culminated in the most institutionally important European sovereign-AI deal of 2026: the April 24, 2026 Cohere merger. Founder Jonas Andrulis’s December 2025 Handelsblatt statement is the canonical retrospective acknowledgment that Mistral’s empirical results demonstrated and the four-way essay track empirically validated. The work was real. The lesson is real. Both can be true at once.

The founder said it. Out loud. In Handelsblatt.

From Jonas Andrulis’s December 2025 Handelsblatt interview, two months after announcing his CEO departure. The single most important sentence in the public Aleph Alpha record. Public acknowledgment from the founder of the company that exited the frontier-capability race that the structural finding from Essay 04 is correct.

Handelsblatt interview · December 2025

AI Engineering: Building Applications with Foundation Models

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five phases. Seven years.

Aleph Alpha’s trajectory through five distinct phases provides the European sovereign-AI movement with a complete reference case for what happens when companies attempt frontier-capability competition at insufficient resource scale. The prior four essay-track projects are still in earlier phases of their respective trajectories.

European sovereign LLM models

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

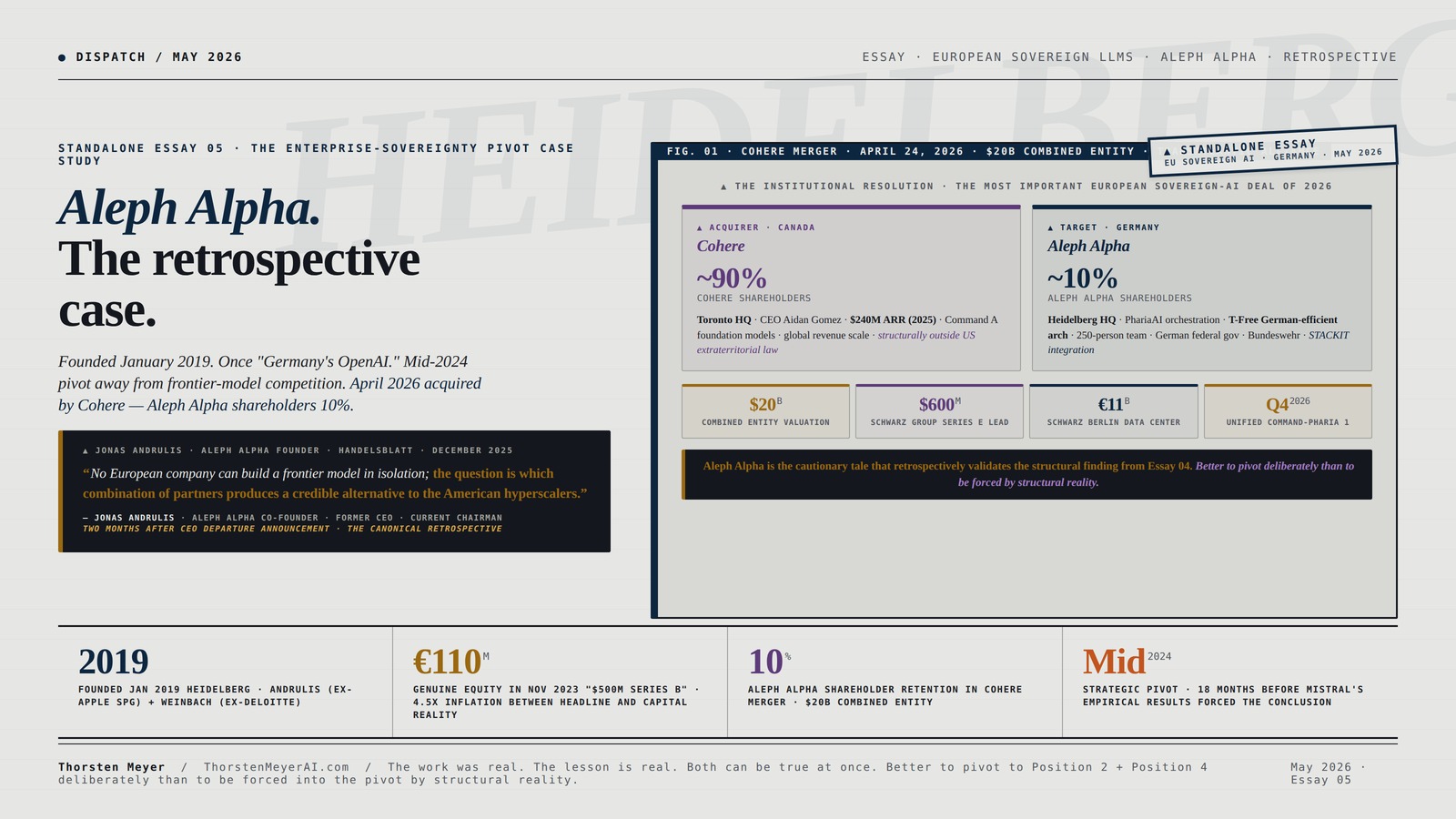

$20 billion combined entity. 10% Aleph Alpha shareholders.

The most institutionally important European sovereign-AI deal of 2026. This is not a merger of equals despite the “merger” terminology. It is a transatlantic acquisition of Aleph Alpha by Cohere, with Schwarz Group’s $600M commitment functioning as the down payment on European public-sector market access.

AI model training compute resources

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five answers. Five structural findings.

Extending the four-way comparison from Essay 04 with the Aleph Alpha retrospective case. Aleph Alpha is the only project with a completed strategic outcome. The other four are still in earlier phases of their respective trajectories.

Five projects. Five findings. Each one harder than the framing it’s wrapped in. Aleph Alpha is the only project with a completed strategic outcome — the retrospective grounding the four forward-looking cases need to integrate. What Phase 4 and Phase 5 look like for the prior four is what the Aleph Alpha case suggests.

Cross-Platform AI Agent Distribution: Portable Deployment Models and Reproducible Configuration Management with Claude and GPT Integration (Autonomous Intelligence Systems Series Book 2)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five lessons. The retrospective grounding.

Strategic lessons the European sovereign-AI movement should integrate. This is not a counsel of despair. It is the operational reference case the four forward-looking essays’ strategic recommendations should be grounded against.

The work was real. The lesson is real. Both can be true at once. Aleph Alpha’s contribution to the framework is the retrospective acknowledgment that the European AI strategic discourse needed — Andrulis’s Handelsblatt formulation is the public-record statement from the founder of the company that empirically tested the proposition and concluded it could not be sustained. The discourse should integrate this acknowledgment. Better to pivot to Position 2 + Position 4 deliberately than to be forced into the pivot by structural reality.

I · What Aleph Alpha actually was · the institutional and technical history

The factual baseline before the structural argument. From Wikipedia, the AI Wiki profile, TechCrunch’s merger coverage, Futurum Group’s deal analysis, and the broader public record including Silicon Republic’s November 2023 coverage, Grokipedia’s profile, and hightechinvesting’s analysis.

The founding architecture

Aleph Alpha GmbH was established in January 2019 in Heidelberg, Germany, by:

- Jonas Andrulis (CEO) — former senior AI R&D manager at Apple’s Special Projects Group (3 years) · third AI startup he founded · economics engineering background

- Samuel Weinbach (co-founder, later CRO) — enterprise strategy background at Deloitte

The founders’ explicit mission: develop sovereign and transparent AI solutions for European enterprises and governments to reduce dependency on US-based tech giants. The strategic positioning was clear from inception — Aleph Alpha was structurally designed as the European response to American AI labs, with explainability and regulatory compliance as core differentiators rather than secondary concerns. This positioning anticipated the EU AI Act framework by approximately 6 years. Aleph Alpha had a three-to-four-year first-mover window before EU AI Act enforcement began creating formal procurement requirements that retroactively validated the architectural choices.

The funding trajectory · the €500M complication

The funding history is operationally important because it documents both the institutional ambition and the structural complication that subsequent reporting revealed. From Wikipedia, Tracxn data, and trade press analysis:

- January 2021 · €5.3M seed round

- July 2021 · €23M Series A · co-led by Earlybird VC, Lakestar, UVC Partners · brought total to €28.3M

- November 6, 2023 · announced “more than $500 million Series B” (approximately €470M at the time of signing) · co-led by Innovation Park Artificial Intelligence (Ipai), Robert Bosch Ventures, Schwarz Group · also: Hewlett Packard Enterprise, SAP, Christ&Company Consulting, Burda Principal Investments

The structural complication that subsequent trade press reporting surfaced: the November 2023 Series B was not what the headline figure suggested. Per trade press analysis, the round broke down as:

- ~€110M in genuine equity financing (the actual capital raised)

- ~€300M in research funding directed to Aleph Alpha Research, a subsidiary focused on fundamental AI research

- ~€60M in order commitments from partners

This is structurally important because it inflated the company’s apparent capital position by approximately 4.5x relative to the actual venture capital raised. By comparison, the November 2023 €110M equity figure would have placed Aleph Alpha at less than half the scale of Mistral’s contemporaneous €385M Series A four months later. The frontier-model competition Aleph Alpha was attempting in 2023-2024 was being conducted at substantially lower effective capital scale than the headline figure implied — a gap that became operationally visible when the company missed its 2023 internal revenue target of €5.5M (actual turnover: less than €1M) and posted a €18.9M loss for the year.

Per Tracxn, total cumulative funding across 4 rounds is approximately $533M nominal. Per Clay’s analysis, prior to the 2023 round the total was €28.3M.

The Luminous era · technical foundation 2020-2024

Before the mid-2024 pivot, Aleph Alpha built a substantive technical foundation. The Luminous family of large language models, launched April 2022:

- luminous-base · 13 billion parameters

- luminous-extended · 30 billion parameters

- luminous-supreme · 70 billion parameters

- Multilingual from inception: English, German, French, Italian, Spanish

- Architecture: GPT-style decoder transformers with self-supervised learning

Supporting technical contributions:

- MAGMA · multimodal architecture · NeurIPS 2023 publication (“Multifusion”) · enables prompt with any combination of text and images · open-sourced for research

- AtMan · explainability methodology · makes patterns learned by GPT models visible and controllable · addresses the “black box” problem of generative AI · the technical differentiator the company built its enterprise positioning around

- alpha ONE data center (September 2022) · GovTech Campus Berlin · 512 NVIDIA A100 GPUs · 7.625 petaflops · marketed as the fastest commercial AI data center in Europe at launch · later became the first European site to deploy Cerebras CS-3 AI supercomputers

- LUMI chatbot (October 2022) · generative AI chatbot for public sector · deployed for City of Heidelberg

T-Free architecture (2024) is the technical contribution worth specific attention. It is a tokenizer-free LLM architecture that delivers higher efficiency for German-language tasks while maintaining competitive performance compared with larger open-source models. The structural argument: traditional tokenizers (BPE, SentencePiece, WordPiece) optimize for English vocabulary distribution and produce inefficient German encoding. T-Free’s tokenizer-free approach is architecturally aligned with German morphological complexity — long compound words, rich inflection, frequent compound nouns that traditional tokenizers fragment inefficiently. This is the kind of architectural research that justifies the “sovereign AI” framing for German-specific applications.

Pharia-1 LLM-7B was released late 2024 under Apache 2.0 license — the first model release after the strategic pivot was announced.

Customer base · the genuine institutional traction

Aleph Alpha’s customer base was substantively credible and reflected the strategic positioning. Named customers include:

- German federal government (anchor customer)

- Bavarian state administration (Freistaat Bayern)

- Baden-Württemberg state administration

- Bundeswehr (German Armed Forces · Cerebras CS-3 supercomputer deployment for defense applications)

- Siemens (DAX-listed industrial conglomerate)

- BMW (DAX-listed automotive)

- Schwarz Group (Lidl/Kaufland · also investor)

- City of Heidelberg (LUMI chatbot · 80,000 users)

- Global semiconductor manufacturer (unnamed · 90% search-time reduction case study)

- Automotive technology supplier (unnamed · 40% requirements-engineering time savings)

This is real institutional traction that the prior essay-track projects do not currently match operationally. The structural positioning Aleph Alpha built — German federal government + Bundeswehr defense + Bavaria + Baden-Württemberg + DAX-listed industrials — represents the European public-sector and regulated-industrial deployment base that the European sovereign-AI agenda is designed to serve. The customer base is the asset Cohere is paying for in the merger.

The strategic pivot · August 2024

On August 27, 2024, Aleph Alpha announced PhariaAI as an enterprise-grade operating system for generative AI. From Maginative’s coverage, Andrulis described it as:

“PhariaAI is a game-changer for enterprises and governments seeking to leverage AI without compromising control or compliance. Our technology accelerates AI innovation while ensuring transparency, auditability, and full compliance with organizational standards.”

The strategic substance of the pivot: Aleph Alpha moved from being a model provider competing with OpenAI/Anthropic/Mistral on foundation-model performance to being a deployment and orchestration platform that integrates its own specialized models alongside best-in-class open-source models (like Meta’s Llama) within a secure, explainable, and compliant framework. PhariaAI’s architectural commitment: model-agnostic governance, on-premise deployment, EU AI Act and German data-protection law compliance, explainability tooling, evaluation framework, tokenizer-free T-Free architecture for German efficiency.

By late 2024, the Luminous API was no longer actively marketed to new customers. Existing deployments continued to be supported. The Luminous frontier-model business line was operationally deprioritized in favor of PhariaAI orchestration platform business line.

The strategic logic from Tech Insider’s analysis:

“By mid-2024, Aleph Alpha conceded that it could not match the training budgets of OpenAI, Anthropic, Google, or Meta, and announced a pivot away from frontier model competition toward an ‘operating system for enterprise AI’ focused on tooling, governance, evaluation, and on-premise deployment.”

This is the same strategic recognition that Essay 04 (Mistral) demonstrated empirically and Andrulis articulated explicitly in December 2025. Aleph Alpha reached the structural conclusion approximately 18 months before Mistral’s empirical results made the conclusion unavoidable. The cost of acting on the conclusion at mid-2024 was the strategic pivot to PhariaAI. The cost of waiting longer would have been substantially higher.

Leadership transition · October 2025 to January 2026

The strategic pivot was followed by leadership transition that crystallized in late 2025 and early 2026:

- Mid-2025 · Reto Sporri (former CEO of Lidl’s commerce division) joined as co-CEO alongside Andrulis · structurally significant signal that Schwarz Group’s role was deepening

- October 2025 · Andrulis announced he would step down as CEO · reported to be founding a new AI startup

- January 1, 2026 · Andrulis transitioned to Chairman of the Advisory Board · Ilhan Scheer (former Chief Growth Officer) named co-CEO alongside Sporri · Carsten Dirks (operational business lead) departed

- ~50 employee reduction (approximately 17% of workforce) · primarily affected engineering and research teams · specifically the divisions focused on improving model performance · reflecting the strategic pivot away from in-house model development

Total employees as of February 2026: approximately 351 per Tracxn. The 17% workforce reduction was concentrated in the functions that the strategic pivot had operationally deprioritized — model-performance engineering and research. This is the operational implementation of the strategic pivot, completed approximately 18 months after the pivot was announced.

The Schwarz Group consolidation · January-February 2026

Parallel to the leadership transition, Schwarz Group (Lidl/Kaufland · Europe’s largest retailer by revenue) consolidated its position. Per European Cloud’s reporting:

- January 2026 · Schwarz Group planned acquisition of Bosch Ventures’ shareholding · further consolidating influence

- €500M+ funding round included SAP, Bosch, Schwarz Group as principals

- Additional investors: Burda Principal Investments, Deutsche Bank

- PhariaAI integration into STACKIT — Schwarz Group’s sovereign cloud platform · “PhariaAI-as-a-Service” for regulated enterprises and public-sector customers

- Anchor tenant relationship: Aleph Alpha + STACKIT positioned as the sovereign-cloud + sovereign-AI integrated offering

This was the pre-merger consolidation that structured the eventual Cohere acquisition. Schwarz Group was positioning to become the European anchor for whatever transatlantic AI alliance would eventually emerge.

II · The Cohere merger · April 24, 2026

The April 24, 2026 announcement is the institutionally most important European sovereign-AI deal of 2026. From TechCrunch’s coverage, Futurum’s analysis, and Tech Insider’s detailed breakdown.

The deal architecture

- Acquirer: Cohere (Toronto-based · Canadian AI company)

- Target: Aleph Alpha (Heidelberg-based · German AI company)

- Combined entity valuation: approximately $20 billion

- Shareholder structure: Cohere shareholders ~90% · Aleph Alpha shareholders ~10%

- Lead investor (Series E): Schwarz Group · $600M (€500M) commitment through Schwarz Digits subsidiary

- Corporate domicile: dual headquarters Canada + Germany · corporate registration likely remains Canada or relocates to Delaware holding depending on tax structuring

- Naming: combined entity retains Cohere name

- Government backing: Canada-Germany Sovereign Technology Alliance (signed earlier 2026) · German Digital Minister Karsten Wildberger + Canadian Digital Minister Evan Solomon attended Berlin announcement

The shareholder ratio is structurally significant. Cohere’s 90% / Aleph Alpha’s 10% reflects the relative revenue and scale ratio. Cohere reported $240M ARR in 2025. Aleph Alpha generated minimal revenue and significant losses (~€18.9M loss in 2023 alone). This is not a merger of equals despite the “merger” terminology. It is a transatlantic acquisition of Aleph Alpha by Cohere, with Schwarz Group’s $600M commitment functioning as the down payment on European public-sector market access for the combined entity.

The strategic rationale

From Cohere CEO Aidan Gomez’s press conference:

“Their focus on small language models, European languages and tokenizers is a really complementary one to our own, which is more of a general focus on large language models.”

The complementarity is genuine:

- Cohere brings: Command A foundation model family · retrieval models · North agentic platform · $240M ARR · global revenue scale · proprietary-API enterprise market

- Aleph Alpha brings: PhariaAI orchestration and deployment layer · T-Free German-efficient architecture · German federal government anchor customer · Bundeswehr defense contracts · Bavaria + Baden-Württemberg state administration · STACKIT integration · 250+ person team with European sovereign-AI expertise

The strategic logic the combined entity claims: full-stack sovereign AI offering combining global-scale foundation models (Cohere) with European-sovereign deployment infrastructure (Aleph Alpha + STACKIT). The combined product roadmap previewed in the April 25 technical briefing includes a unified Command-Pharia 1 model targeted for Q4 2026 release, with native Pharia-style on-premise deployment and Cohere-style retrieval-augmented generation tooling.

The sovereignty complication

This is the structural complication the merger surfaces. Several German federal agencies and three Bundesländer have contracts that contain explicit sovereignty clauses requiring the AI vendor to be “controlled in Europe.” The merger leaves the combined company majority-controlled outside the EU — 90% Cohere shareholders, with corporate domicile in Canada or Delaware holding.

This is operationally significant for the European sovereign-AI agenda. The merger’s headline strategic claim is “sovereign AI alternative to US hyperscalers.” The structural reality is that the merged entity is North-American-controlled, not European-controlled. From Tech Insider’s analysis:

“The merger leaves the combined company majority-controlled outside the EU, with corporate domicile likely to remain in Canada or relocate to a Delaware holding company depending on tax structuring.”

The defense from the merger’s proponents: Canada is structurally outside US extraterritorial law (CLOUD Act, FISA Section 702) in ways no US vendor can claim. A Cohere-Aleph Alpha entity hosted on STACKIT is unambiguously outside the US legal perimeter while offering frontier-class model performance — a combination only Mistral has been able to claim until now. The merger’s positioning is “Canadian + German sovereign alternative to American hyperscalers,” not “purely European sovereign alternative.”

Whether this satisfies the explicit “controlled in Europe” sovereignty clauses in existing German federal contracts is a procurement-law question that will be determined in specific contract negotiations. It is not currently resolved.

The Schwarz Group $600M commitment · the European anchor

Schwarz Group’s $600M Series E commitment is structurally the most important single financial detail of the deal. The investment:

- Functions as the anchor European capital commitment for the combined entity

- Secures Cohere-Aleph Alpha as the anchor tenant for Schwarz’s STACKIT sovereign cloud platform

- Gives Schwarz Group a strategic stake in the European AI sovereignty market

- Complements Schwarz Group’s €11 billion data center near Berlin infrastructure commitment

This is the European industrial capital allocation that the four-way essay track’s strategic recommendation calls for — large-scale European industrial conglomerate capital concentrating on AI infrastructure for European-sovereign deployment. Schwarz Group’s pattern of investment (data center buildout + sovereign-AI vendor anchor tenant + retail conglomerate revenue base) is the operational model for European AI investment that scales beyond what individual venture rounds can sustain.

The analyst framing

Per Holger Mueller of Constellation Research at the Berlin announcement:

“The merger creates the first European frontier-AI vendor with both global revenue scale and on-the-ground sovereignty credibility. Schwarz’s $600 million is essentially the down payment on a 10-year procurement war for European public-sector AI contracts that will run into the tens of billions.”

And per SAP CEO Christian Klein’s April 25 LinkedIn post:

“Europe needed a sovereign frontier partner with delivery scale, and now it has one.”

These statements frame the merger as the institutional resolution to the European sovereign-AI question. Whether that framing holds operationally depends on Q4 2026 unified-model release execution, on whether the sovereignty-clause procurement complications resolve, and on whether the combined entity’s frontier capability is competitive at the levels US frontier developers operate.

III · The Andrulis Handelsblatt statement · the canonical retrospective acknowledgment

The most important single sentence in the public Aleph Alpha record, from Andrulis’s December 2025 Handelsblatt interview:

“No European company can build a frontier model in isolation; the question is which combination of partners produces a credible alternative to the American hyperscalers.”

This sentence deserves careful unpacking, because it is the structural retrospective acknowledgment that crystallizes what the four-way essay track empirically demonstrated.

What Andrulis is saying

Three claims are made implicitly and explicitly:

Claim 1: No European company can build a frontier model in isolation. This is the structural finding from Essay 04 stated in negative form by the founder of the company that empirically tested the proposition and concluded it could not be sustained. Mistral’s €3B+ raised and ~44% GPQA Diamond result demonstrated this from the commercial-frontier side. Aleph Alpha’s mid-2024 pivot demonstrated it from the cautionary side approximately 18 months earlier.

Claim 2: The question is which combination of partners produces a credible alternative. This is the strategic redirection — frontier-capability competition is reframed not as “which European company will win” but as “which combination of European institutional actors can produce a competitive alternative to American hyperscalers.” This is the consortium argument made retrospectively from the commercial-frontier side. Andrulis is endorsing — implicitly — the OpenEuroLLM consortium model and the Mistral commercial-frontier model and the Cohere-Aleph Alpha transatlantic model as different attempts at the same partnership-based architectural question.

Claim 3: Credible alternative to American hyperscalers. Not “matching” American hyperscalers, but “credible alternative.” This is the strategic-positioning recalibration that the four-way essay track’s closing recommendation calls for — Position 2 + Position 4 rather than Position 1. The frontier-match positioning is implicitly abandoned even in the strategic statement. The strategic objective is reframed as European AI that is credibly alternative to American hyperscalers — i.e., sufficient for European procurement and enterprise requirements — rather than competitively superior on raw frontier capability.

What this means for European sovereign-AI strategic discourse

The Andrulis statement is structurally important because it is the most explicit retrospective acknowledgment by a European AI founder that the strategic discourse needs to recalibrate. The four-way essay track documented the empirical reality. Andrulis articulates the strategic implication. These are the same finding stated from two different perspectives.

For the European AI strategic discourse, three implications worth surfacing:

Implication 1 · The “European OpenAI” framing should be retired. The framing that produced Aleph Alpha’s original positioning, that produced public expectations of Mistral as the European frontier developer, and that produces ongoing pressure on OpenEuroLLM’s consortium to deliver frontier-class capability is now empirically unsupported. No European institutional structure — including the commercial-frontier model with substantially more capital than the others combined — is currently producing frontier-class results competitive with American hyperscalers. The framing should be retired in favor of strategic-positioning vocabulary that acknowledges the actual European competitive advantage (Position 2 + Position 4).

Implication 2 · Partnership architecture is the operational structure that scales. Andrulis’s statement implicitly endorses partnership architectures: consortium (OpenEuroLLM), commercial-strategic-investor (Mistral + ASML), and transatlantic-alliance (Cohere-Aleph Alpha) are all partnership-based responses to the structural finding that no single European company can build a frontier model in isolation. The European sovereign-AI agenda’s institutional structure should explicitly optimize for partnership architectures rather than for single-firm frontier-capability competition.

Implication 3 · The cost of getting the lesson right late is substantial. Aleph Alpha’s trajectory makes this visible: ~€110M+ in genuine equity capital spent before the pivot · €18.9M+ losses in 2023 alone · failed revenue targets · founder departure · 17% workforce reduction · 10% shareholder dilution in the Cohere acquisition. The lesson is structurally identical to what subsequent essay-track projects can learn from prospectively. The Aleph Alpha case demonstrates the cost of waiting until the structural reality forces the strategic pivot.

IV · The five-way comparison · what Aleph Alpha adds to the essay track

With Aleph Alpha now documented, the four-way structural comparison from Essay 04 extends to a five-way framework that includes the retrospective case.

The institutional comparison

| Dimension | Minerva | AMÁLIA | OpenEuroLLM | Mistral | Aleph Alpha |

|---|---|---|---|---|---|

| Strategic answer | National from-scratch | National continuation | Pan-EU consortium | Commercial-frontier | Enterprise-sovereignty pivot |

| Institutional model | Academic (Sapienza/FAIR) | Academic consortium | Academic-and-state consortium | Venture-funded private | Venture-funded private (pivoted) |

| Country | Italy | Portugal | Pan-EU | France | Germany |

| Founded | (2022 PNRR) | 2024 program | Feb 2025 | April 2023 | January 2019 |

| Cumulative funding | Large national | €5.5M state | €37.4M EU | €3B+ VC | ~€110M equity + €300M research subsidiary + €60M order commitments |

| Revenue trajectory | Academic (none) | Academic (none) | Research consortium (none) | $400M ARR (Jan 2026) | <€1M (2023) · pivoted to platform |

| Headline model | Minerva-7B (Nov 2024) | AMÁLIA base (Sep 2025) | First models (Jul 2026 target) | Mistral Large 3 (Dec 2025) | Luminous 70B (2022) · Pharia-1 LLM-7B (late 2024) |

| Strategic outcome | Operating · ongoing | Operating · 2026 final | Operating · first models 2026 | Operating · €3B+ trajectory | Acquired by Cohere · April 2026 |

| Structural finding | 3B: 4.9% INVALSI | 5.5% pt-PT mid-training | Hajič: “more compute remain” | ~44% GPQA vs 91.9% Gemini | Pivot retrospectively right · executed late |

Aleph Alpha is structurally distinct from the prior four. It is older (founded 2019 vs 2023 for Mistral and 2022/2024/2025 for the others), it pivoted earliest (mid-2024 vs Mistral’s continued frontier pursuit), and it is the only one of the five with a completed strategic outcome (the Cohere acquisition). It is the retrospective case the prior four are still living through.

The strategic-positioning comparison

| Project | Position 1 (frontier-match) | Position 2 (sovereignty/openness) | Position 3 (country-knowledge depth) | Position 4 (vertical specialization) |

|---|---|---|---|---|

| Minerva | Not targeted | ✓ Operational | ✓ Italian-specific | Not primary |

| AMÁLIA | Not targeted | Partial | Partial | Not primary |

| OpenEuroLLM | Stated · compute-constrained | ✓ Strong commitment | ✓ 35 languages | Not primary |

| Mistral | Strongest attempt · still trails | ✓ Apache 2.0 + EU-hosted | Partial (40+ languages) | ✓ Multiple verticals |

| Aleph Alpha | Attempted 2019-2024 · pivoted out | ✓ Strong commitment from inception | ✓ German-specific T-Free | ✓ Public sector + defense + industrial |

Aleph Alpha is the only project in the five-way comparison that explicitly stopped pursuing Position 1. It is also the project with the strongest Position 2 + Position 3 + Position 4 combined positioning operationally — German federal government + Bundeswehr defense + Bavaria + Baden-Württemberg + Siemens + BMW + Schwarz Group + City of Heidelberg LUMI public sector + T-Free German-efficient architecture + Apache 2.0 Pharia-1 release.

This positioning combination is exactly what the four-way essay track’s closing strategic recommendation calls for. Aleph Alpha demonstrated operationally what Position 2 + Position 4 looks like at scale — and the empirical results (genuine institutional customer base, real defense and industrial deployment, sovereign-cloud STACKIT integration) validate the positioning even as the company’s foundation-model business line was deprecated.

The strategic lesson the European sovereign-AI agenda should integrate: Aleph Alpha’s Position 2 + Position 4 positioning is correct. Aleph Alpha’s Position 1 frontier-model competition was wrong for its capital scale. The pivot in mid-2024 was strategically correct. The cost of having pursued Position 1 from 2019-2024 before pivoting is what the Cohere acquisition’s 10% shareholder dilution represents.

The temporal comparison

Aleph Alpha’s trajectory through five distinct phases provides the European sovereign-AI movement with a complete reference case:

- Phase 1 (2019-2021) · Founding and early funding · €28.3M raised · Luminous models in development · MAGMA multimodal architecture · alpha ONE data center launching

- Phase 2 (2022-2023) · “German OpenAI” framing peak · Luminous family released · LUMI public sector chatbot · €500M Series B announced (€110M genuine equity) · €18.9M loss · 2023 revenue target missed by 5.5x

- Phase 3 (2024) · Strategic pivot · PhariaAI launched (August 2024) · T-Free architecture released · Pharia-1 LLM-7B Apache 2.0 release · Luminous API deprecated for new customers

- Phase 4 (2025) · Leadership transition · Sporri joins as co-CEO mid-2025 · Andrulis announces departure October 2025 · Schwarz Group consolidation · €500M+ Series E investor preparation

- Phase 5 (2026) · Andrulis Handelsblatt acknowledgment (December 2025) · Schwarz Group / Bosch Ventures stake acquisition (January 2026) · Scheer-Sporri co-CEO team (January 2026) · 17% workforce reduction · Cohere merger announcement (April 24, 2026) · $20B combined-entity deal · Schwarz $600M Series E lead

Five distinct phases over seven years. This is the operational timeline the European sovereign-AI movement should treat as the reference case for what happens when companies attempt frontier-capability competition at insufficient resource scale. The prior four essay-track projects are still in Phases 1-3 of their respective trajectories. What Phase 4 and Phase 5 look like for the prior four is what the Aleph Alpha case suggests.

V · What Aleph Alpha demonstrates beyond the company itself

Five structural lessons emerge from the Aleph Alpha case that the four-way essay track should integrate.

Lesson 1 · The pivot to Position 2 + Position 4 is strategically correct

Aleph Alpha’s mid-2024 strategic pivot to enterprise-sovereignty positioning — moving from frontier-model competition to AI operating system / governance / on-premise deployment platform — was strategically correct. The empirical evidence across all five cases in the extended comparison framework supports this positioning combination for European institutional actors operating at sub-frontier capital scales. The strategic question is not whether to pivot to Position 2 + Position 4, but when to pivot and how to execute the pivot operationally without the workforce, leadership, and shareholder costs Aleph Alpha incurred.

Lesson 2 · Founder identity vs strategic positioning · the cost of attachment

Andrulis’s October 2025 departure announcement is structurally important. The Aleph Alpha case suggests that founder identity attachment to the original “European OpenAI” framing was operationally costly. The strategic pivot required not just architectural and product redirection, but eventual leadership replacement to operationalize the new positioning. Co-CEO Reto Sporri joining mid-2025 from Lidl commerce, and Ilhan Scheer becoming co-CEO January 2026, signal that the post-pivot company required different leadership skills than the pre-pivot company. This is a generalizable observation for European AI strategic pivots: the founder who built the frontier-model company may not be the right CEO for the post-pivot platform company.

Lesson 3 · The €500M complication · capital announcement vs capital reality

The November 2023 “more than $500M Series B” announcement that was subsequently revealed to be approximately €110M genuine equity plus €300M research subsidiary funding plus €60M order commitments is operationally instructive. European AI capital announcements should be parsed structurally rather than accepted at headline value. The 4.5x inflation between headline ($543M) and effective equity (~€110M) materially affected Aleph Alpha’s competitive position relative to US frontier developers — but the headline figure shaped public discourse and investor expectations as if the higher figure represented actual operational capital. This is a discourse-level lesson that affects how the European AI strategic conversation evaluates institutional achievement.

Lesson 4 · The Schwarz Group anchor model · what European industrial capital allocation looks like at scale

Schwarz Group’s pattern — €500M+ existing investment in Aleph Alpha + €600M Series E commitment to Cohere-Aleph Alpha + €11B data center buildout near Berlin + STACKIT sovereign cloud platform development + Aleph Alpha as anchor tenant — is the operational model for European industrial capital allocation to AI at scale. This is structurally distinct from venture capital (faster cycle times, exit-oriented), strategic-investor capital (Mistral’s ASML model · more disciplined but smaller per-deal scale), and public funding (OpenEuroLLM’s €37.4M · structurally smaller). The Schwarz Group anchor model is the European institutional structure that can scale beyond what venture and public funding currently sustain. Whether this model can be replicated at other European industrial conglomerates (Bertelsmann · Bosch · Siemens · Allianz · DAX-listed conglomerates broadly) is the strategic question.

Lesson 5 · The transatlantic alliance structure · Canada as European sovereignty partner

The Cohere-Aleph Alpha merger structures a transatlantic alliance with Canada rather than with US AI labs. This is operationally significant because Canada is structurally outside US extraterritorial law (CLOUD Act, FISA Section 702) in ways no US vendor can claim. For European sovereignty requirements that need partnership with non-EU jurisdictions, Canada is structurally distinct from the United States. The Canada-Germany Sovereign Technology Alliance signed earlier 2026 institutionalizes this distinction at the diplomatic level. The transatlantic-alliance structure is a new institutional option for European sovereign-AI development that the prior four essay-track projects did not pursue but that the European AI strategic discourse should evaluate as a legitimate fifth path.

VI · The closing argument · the five-way comparison and what comes next

Across five standalone essays, the European sovereign-LLM essay track now documents five distinct institutional answers:

- Essay 01 · AMÁLIA · national continuation answer

- Essay 02 · Minerva · national from-scratch answer

- Essay 03 · OpenEuroLLM · pan-European consortium answer

- Essay 04 · Mistral · commercial-frontier answer

- Essay 05 · Aleph Alpha (this piece) · enterprise-sovereignty pivot answer · retrospective case · culminated in Cohere transatlantic merger April 2026

Each answer is valid for its specific positioning and resource context. Aleph Alpha’s distinct contribution to the comparison framework is that it is the only one of the five with a completed strategic outcome. The other four are still in earlier phases of their respective trajectories. The Aleph Alpha case shows what Phase 4 and Phase 5 of European sovereign-AI strategic development look like operationally — leadership transition, workforce restructuring, partnership architecture, transatlantic alliance.

For the European sovereign-AI movement broadly, three integrative observations emerge from extending the comparison to five cases:

Observation 1 · The strategic recommendation from Essay 04 is structurally validated by the Aleph Alpha retrospective case. Position 2 + Position 4 (sovereignty/openness/compliance + vertical specialization) is the European competitive advantage that scales across institutional structures. Aleph Alpha’s enterprise-sovereignty positioning operationally demonstrated what Position 2 + Position 4 looks like at scale. The Cohere merger preserves and extends that positioning while adding global-scale foundation-model capability through the Canadian partner. The strategic-positioning recommendation is not theoretical — it is empirically validated by both the Mistral commercial-frontier case and the Aleph Alpha enterprise-sovereignty case.

Observation 2 · Partnership architecture is the operational structure that scales across institutional structures. OpenEuroLLM consortium partnership · Mistral commercial-strategic-investor partnership (ASML) · Aleph Alpha transatlantic acquisition partnership (Cohere) · Schwarz Group industrial-anchor partnership across multiple investments — these are all variations of the same underlying observation: European sovereign-AI development requires partnership architectures that no single European institution can replicate alone. Andrulis’s Handelsblatt formulation crystallizes this: “the question is which combination of partners produces a credible alternative.” The strategic discourse should explicitly evaluate institutional options through this partnership lens rather than through single-firm competitive frames.

Observation 3 · The cost of strategic recalibration is substantial but bounded. Aleph Alpha’s transition cost — measured in delayed pivot, leadership transition, 17% workforce reduction, founder departure, 10% shareholder dilution in the Cohere merger — is real but the resulting institutional position is operationally sustainable. The combined Cohere-Aleph Alpha entity is operationally credible as European-sovereign-with-transatlantic-partnership in ways that pre-pivot Aleph Alpha was not. This is structurally important for the broader European AI movement: the cost of strategic recalibration is bounded, and the resulting positioning is more defensible than the pre-recalibration positioning. The Aleph Alpha case demonstrates this empirically.

For Aleph Alpha specifically, the question through 2026 and 2027 is whether the merger integration with Cohere preserves the genuine European-sovereign positioning, whether the Q4 2026 unified Command-Pharia 1 model release executes operationally, whether the German federal government and Bundesländer sovereignty-clause procurements continue under transatlantic ownership, and whether Schwarz Group’s $600M commitment scales into the multi-year procurement war Constellation Research’s Holger Mueller predicted. The combined entity’s integration trajectory through 2027 is the next data point that matters.

For the European sovereign-LLM movement broadly, the five-way comparison this essay track now contains is what the strategic discourse needs — a structurally honest framework for evaluating European AI development across multiple institutional models simultaneously, surfacing the empirical complications each project’s marketing materials downplay, integrating the retrospective Aleph Alpha case alongside the four forward-looking cases, and producing strategic recommendations grounded in operational realities of what actually works at current European investment scales.

Aleph Alpha’s contribution to the framework is the retrospective acknowledgment that the European AI strategic discourse needed. Andrulis’s Handelsblatt formulation — “no European company can build a frontier model in isolation; the question is which combination of partners produces a credible alternative to the American hyperscalers” — is the public-record statement from the founder of the company that empirically tested the proposition and concluded it could not be sustained. The strategic discourse should integrate this acknowledgment.

That’s the read on Aleph Alpha as of mid-May 2026. The work was real. The institutional contribution — German federal government anchor customer, Bundeswehr defense deployment, Bavaria and Baden-Württemberg state administration deployment, Siemens and BMW industrial deployment, City of Heidelberg LUMI public sector, T-Free German-efficient architecture, MAGMA multimodal research, AtMan explainability methodology — is substantial and durable. The strategic-pivot lesson the case demonstrates is what the broader European AI movement should integrate. Better to pivot to Position 2 + Position 4 deliberately than to be forced into the pivot by structural reality.

The work is real. The lesson is real. Both can be true at once. The European sovereign-AI agenda is at the empirical-data-ground-truth moment. The Aleph Alpha case is the retrospective grounding that the four forward-looking cases need to integrate. The discourse should be ready for whatever the data actually shows across all five projects simultaneously.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Reading · the European sovereign-LLM essay track

- AMÁLIA · The Three Hard Questions — Standalone Essay 01 · Portuguese national continuation answer

- Minerva · The Opposite Path — Standalone Essay 02 · Italian national from-scratch answer

- OpenEuroLLM · The Third Path — Standalone Essay 03 · pan-European consortium answer

- Mistral · The Fourth Path — Standalone Essay 04 · commercial-frontier answer

- This piece — Standalone Essay 05 · the Aleph Alpha case · enterprise-sovereignty pivot answer · the retrospective case

Sources

- Wikipedia · Aleph Alpha · funding history, founding, model timeline, Cohere merger

- AI Wiki · Aleph Alpha profile · detailed company history, leadership transitions, Series B breakdown

- Tracxn · Aleph Alpha 2026 Company Profile · $533M total funding, investor list, leadership

- Grokipedia · Aleph Alpha · €500M Series B complication, capital structure breakdown

- TechCrunch · Why Cohere is merging with Aleph Alpha · April 25, 2026 · merger announcement, Gomez quote, sovereignty positioning

- Futurum Group · Cohere Acquires Aleph Alpha: A Deal Born of Sovereignty, Necessity · Nick Patience analysis · 2 weeks ago

- Tech Insider · Cohere’s $20B Aleph Alpha Merger: Schwarz $600M Bet · detailed deal breakdown · Andrulis Handelsblatt quote · Holger Mueller analyst framing · Christian Klein SAP quote

- European Cloud · Schwarz Group expands its influence over Aleph Alpha · February 1, 2026 · Bosch Ventures stake acquisition, STACKIT integration

- HighTechInvesting · Aleph Alpha and Cohere: The Quiet Sale of Germany’s AI Hope · skeptical analysis · stock swap structure · capital structure reality

- Silicon Republic · Aleph Alpha, Europe’s answer to OpenAI, just raised half a billion · November 7, 2023 · Series B announcement

- Maginative · Aleph Alpha Announces PhariaAI · August 27, 2024 · pivot announcement

- innFactory AI · Aleph Alpha Luminous · April 2026 update · merger talks coverage

- Kai Waehner · Enterprise Agentic AI Landscape 2026 · April 7, 2026 · landscape positioning

- Global Recognition Awards · Aleph Alpha Wins a 2026 Global Recognition Award · award analysis with deal context

- Aleph Alpha official · PhariaAI · current PhariaAI positioning

- Skywork · Aleph AI: Your Ultimate Guide to Europe’s Sovereign AI Powerhouse · funding, strategic pivot analysis

- Clay · Aleph Alpha Funding & Key Investors · early funding documentation

- Canvas Business Model · Aleph Alpha Brief History · timeline of milestones

- Jonas Andrulis · Aleph Alpha co-founder · CEO 2019-2025 · Chairman of Advisory Board from January 2026 · former Apple Special Projects Group senior AI R&D manager (3 years) · third AI startup founded

- Samuel Weinbach · Aleph Alpha co-founder · former CRO · Deloitte enterprise strategy background

- Reto Sporri · co-CEO from mid-2025 · former CEO of Lidl commerce division

- Ilhan Scheer · co-CEO from January 2026 · former Chief Growth Officer

- Aidan Gomez · Cohere CEO · April 25 press conference complementarity statement

- Karsten Wildberger · German Digital Minister · Berlin announcement attendee

- Evan Solomon · Canadian Digital Minister · Berlin announcement attendee

- Holger Mueller · Constellation Research analyst · “10-year procurement war” framing

- Christian Klein · SAP CEO · April 25 LinkedIn statement on sovereign frontier partner

- Schwarz Group · Lidl/Kaufland parent · Europe’s largest retailer by revenue · €11B data center near Berlin · $600M Series E commitment · STACKIT sovereign cloud platform

- Bosch Ventures · early/Series B Aleph Alpha investor · stake being acquired by Schwarz Group

- Innovation Park Artificial Intelligence (Ipai) · 2023 Series B co-lead · Heilbronn-based AI innovation park

- Luminous family · 13B / 30B / 70B parameters · multilingual (EN, DE, FR, IT, ES) · 2022 launch · no longer marketed to new customers from late 2024

- PhariaAI · enterprise AI operating system · August 2024 launch

- Pharia-1 LLM-7B · Apache 2.0 license · late 2024 release

- T-Free · tokenizer-free LLM architecture · 2024 · German-language efficiency

- MAGMA · multimodal architecture · NeurIPS 2023 (Multifusion) · open-sourced

- AtMan · explainability methodology · “black box” problem solution

- alpha ONE data center · GovTech Campus Berlin · September 2022 · 512 NVIDIA A100 GPUs · 7.625 petaflops · first European Cerebras CS-3 deployment site

- LUMI chatbot · City of Heidelberg public sector · October 2022 · 80,000 users

- Bundeswehr Cerebras CS-3 deployment · German Armed Forces · AI supercomputer for defense applications

- Canada-Germany Sovereign Technology Alliance · signed early 2026 · diplomatic framework for transatlantic AI partnership

- STACKIT · Schwarz Digits sovereign cloud platform · Aleph Alpha PhariaAI integration via PhariaAI-as-a-Service

- Cohere Command A family · foundation models · North agentic platform · $240M ARR 2025

- Unified Command-Pharia 1 model · combined-entity Q4 2026 target release

- AMÁLIA · Essay 01 · Portuguese national continuation answer

- Minerva · Essay 02 · Italian national from-scratch answer

- OpenEuroLLM · Essay 03 · pan-European consortium answer

- Mistral · Essay 04 · commercial-frontier answer