By Thorsten Meyer — May 2026

The original Forward-Deployed Engineer dispatch landed in late 2025. Six months later, the numbers it relied on are out of date in three directions. The compensation ladder has steepened. The job-posting volume has compounded. The customer industries have stratified. The role itself has institutionalized in ways the prior piece did not anticipate — Salesforce committed to a thousand-FDE rollout, BCG renamed BCGX engineers to FDEs, EY launched a UK and Ireland practice, Naver Cloud and Krafton stood up Korean programs. The phrase “Forward-Deployed Engineer” went from a Palantir tradecraft term in 2023 to the central mode of enterprise AI deployment in 2026.

The piece nobody has written is the unit economics math. Six-figure compensation packages, fully-loaded costs in the $220-400K range per FDE, multi-million-dollar enterprise contracts attached to each engagement. Is this profitable for the labs, or is it a loss-leader subsidizing distribution? The answer determines whether the FDE motion scales the way the labs are betting it will, or whether it collapses to a smaller specialty role once the distribution moat is built.

This dispatch updates the prior FDE piece against the May 2026 data, runs the unit economics math against actual contract sizes and attach rates, and makes the case that FDE economics are the most under-analyzed structural variable in frontier AI revenue scaling. The labs that get this math right capture the enterprise margin. The labs that get it wrong spend their way into operating losses that compound through the IPO window and beyond.

The dispatch on the Anthropic IPO disclosure document covered why customer concentration and channel disclosure become public in October. The dispatch on the compute concentration audit covered the substrate that makes FDE deployment expensive at scale. This piece sits between them. The FDE is the human layer that converts compute and capability into enterprise revenue. The economics of that conversion determine which labs reach FCF positive and which do not.

The unit economics math.

Six months later, the FDE compensation ladder has steepened. The customer-mix discipline is now the difference between margin and operating loss.

FDE postings +800% Jan–Sept 2025. Comp ladder spread now 4.6× from Palantir baseline to Anthropic top-end. Salesforce committed 1,000 FDEs. EY launched UK + Ireland practice. BCG renamed BCGX engineers. Korea, Japan, India scaling. The role institutionalized. The math is now computable.

From $200K to $920K. Same job title.

Levels.fyi data, May 5 2026. Palantir set the original FDE benchmark. Anthropic + OpenAI re-priced the role for frontier-lab competition. Total compensation packages including equity. The 4.6× spread reflects the gap between defense-and-finance customers vs. Fortune 10 enterprise agentic deployment.

Your AI Survival Guide: Scraped Knees, Bruised Elbows, and Lessons Learned from Real-World AI Deployments

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

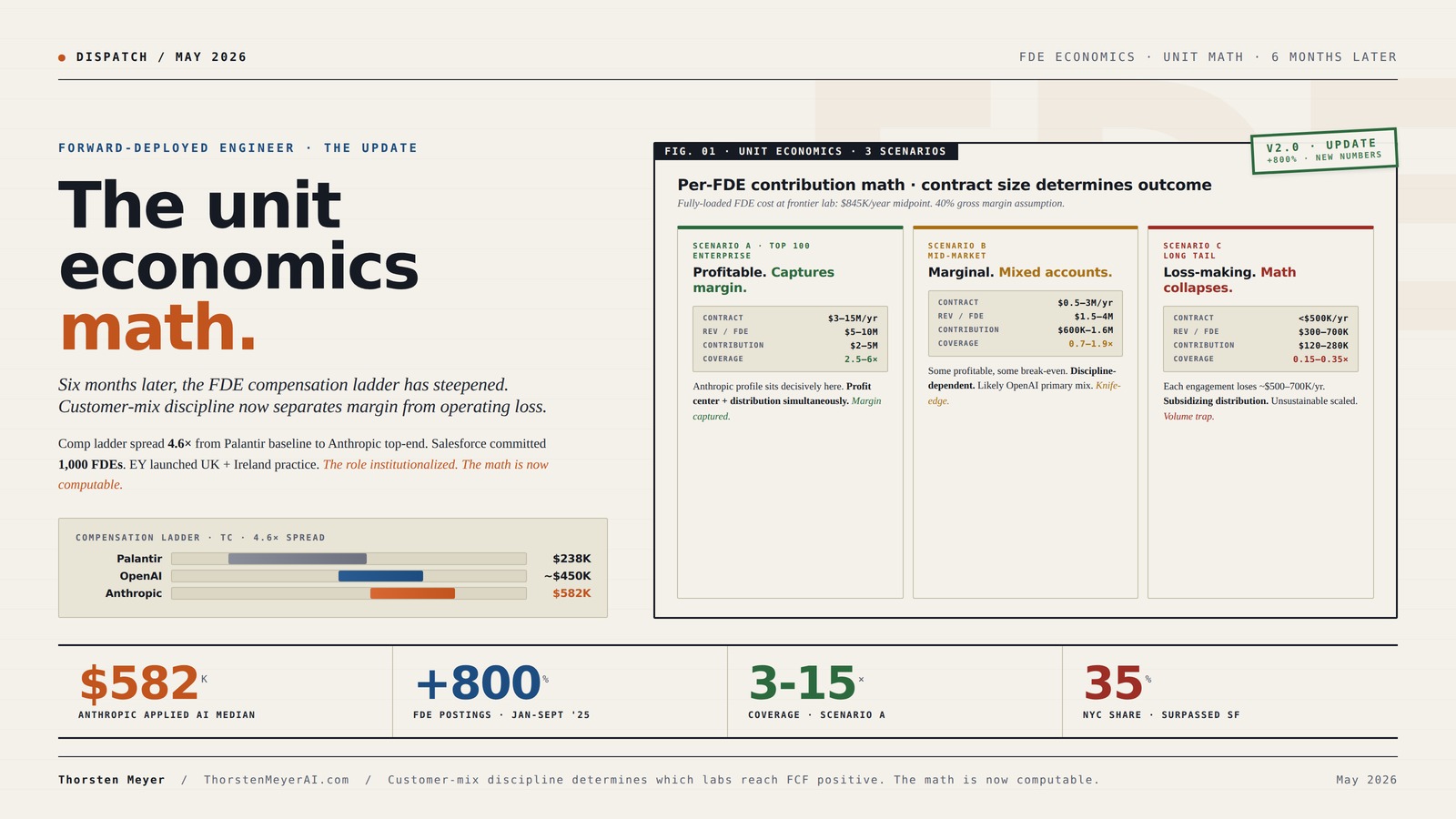

Three customer scenarios. Three different answers.

Fully-loaded FDE cost at a frontier lab: $845K/year midpoint ($350-756K TC + 30% benefits + tooling + travel + management overhead). Revenue per FDE depends entirely on customer-mix discipline. The labs that maintain Scenario A targeting capture margin. The labs that chase volume across Scenarios B and C produce operating losses.

Anthropic profile (8 of Fortune 10, 500+ at $1M+/yr) sits decisively here. Profit center + distribution simultaneously. Margin captured.

Some accounts profitable, some break-even. Discipline-dependent. Likely OpenAI primary mix · contributes to operating loss profile. Knife-edge.

Each engagement loses ~$500–700K/yr fully-loaded. Subsidizing distribution. Unsustainable as scaled motion. Volume trap.

Sticker Pack 20 pcs AI Technology Stickers, Artificial Intelligence Circuit Vinyl Decals for Laptop Tablet

20 artificial intelligence themed stickers featuring circuit patterns, algorithms, and futuristic tech designs for decorating laptops, tablets, notebooks,…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Agentic dominates. Top 3 industries = 59%.

Bloomberry analysis of 1,000+ FDE postings. The skill mix has shifted decisively from RAG to agentic. The customer-industry distribution explains where the unit economics work. Financial Services + Government + Healthcare are the absorbing categories.

Learning Spark: Lightning-Fast Big Data Analysis

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five categories. 40-60 institutional employers.

From a dozen frontier-AI labs and Palantir two years ago to ~50 institutional employers globally now. Total category: 15,000–25,000 FDE roles. Actively employed: ~8,000–12,000. Demand exceeds supply by 2×. Compresses to 1.2–1.5× by 2028 as consulting + international supply scales.

The labs that maintain customer-mix discipline capture margin. The labs that chase volume across Scenarios B and C produce operating losses. The math is now computable.

Project Management with AI For Dummies

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Negotiate aggressive equity at frontier labs now.

Comp ladder at peak premium. Frontier-lab roles will moderate by 18–24 months as talent pool expands (consulting + international supply). Pre-IPO equity at Anthropic has highest expected value now. Skills to develop: agentic-loop production debugging, MCP server engineering, customer-facing technical communication.

Maintain Scenario A discipline.

Resist competitive pressure to deploy against Scenarios B and C accounts even when volume looks attractive. Build customer-mix dashboards that explicitly track contract size distribution. The FDE motion is profitable on the right side and unprofitable on the left. Anthropic’s mix is structurally healthy; OpenAI’s mix is at risk.

Two implications: quality and pricing.

FDE-led deployment at $3M+ annual contract sizes produces high-quality outcomes. Expect to pay for it in contract pricing. Don’t accept FDE-light deployment from labs whose comp data suggests they’re using junior engineers as branded FDEs. The economics don’t work; the deployment quality won’t either.

The window is 24–36 months.

FDE practice is the most strategically important new line of business in professional services in 15 years. After 24-36 months, the category consolidates around firms that scaled fastest. BCG, EY, and early movers have structural advantage. Firms that delay materially in 2026 will compete from a lower position through 2030.

Executive Summary · The FDE Economics in One Table

| Metric | Number | Source |

|---|---|---|

| FDE job posting growth | +800% Jan–Sept 2025 | Indeed × Financial Times |

| Palantir FDE average TC | $238K, range $205-486K | Levels.fyi |

| Palantir staff-level FDE TC | $630K+ | Levels.fyi |

| Anthropic Applied AI Engineer median TC | $582,500 | Levels.fyi, May 5 2026 |

| Anthropic Applied AI Engineer range | $563-756K, top reported $920K | Levels.fyi |

| OpenAI / Anthropic FDE mid-to-senior | $350-550K stabilized | Industry composite |

| Fully-loaded FDE cost / year | $220-400K | Industry analysis |

| Salesforce FDE commitment | 1,000 | Public announcement |

| EY FDE practice launch | UK + Ireland, April 2026 | Public announcement |

| NYC share of FDE postings | 35% | Bloomberry analysis, 1,000+ postings |

| SF share of FDE postings | 11% | Same |

| Skills mix · AI Agents | 35% of postings | Same |

| Skills mix · LLM | 31% | Same |

| Skills mix · RAG | 12% | Same |

| Customer industry · Financial Services | 24% | Same |

| Customer industry · Government | 18% | Same |

| Customer industry · Healthcare | 17% | Same |

| Postings with equity | 70% | Same |

| Anthropic customers >$1M/year | 500+ | Sacra |

| Estimated revenue per FDE (frontier lab) | $3-15M / year | Author calculation |

| FDE engagement margin contribution | 3-15x fully-loaded cost | Author calculation |

The math is unambiguous: at frontier-lab scale, with high-value enterprise contracts, the FDE motion is structurally profitable as a service line in addition to its distribution role. At lower scale or against lower-value accounts, the math collapses. The labs that build FDE practices on customer cohorts capable of absorbing $1M+ annual contracts capture the margin. The labs that deploy FDEs against the long tail subsidize distribution out of operating cash flow.

1. The compensation ladder, May 2026

The compensation data is the cleanest signal. Levels.fyi updated its Anthropic Applied AI Engineer entry on May 5, 2026 — three days ago at this writing. The numbers are precise. The median total compensation for an Applied AI Engineer (Anthropic’s internal title for FDE) is $582,500. The range across reported levels is $563,000 at the senior level to $756,000 at the lead level. The top reported package is $920,000.

Compare this to the Palantir baseline. Palantir invented the FDE role and set the original benchmark. Levels.fyi reports Palantir Forward Deployed Engineer compensation at an average of $238,000, range $205-486,000, with staff-level FDEs clearing $630,000+. The range from Palantir to Anthropic is wide.

OpenAI’s compensation data is less granularly reported, but industry composites place OpenAI’s mid-to-senior FDEs in the $350-550,000 range — slightly below Anthropic’s median, slightly above Palantir’s. The Anthropic premium is real and is driven by two factors. First, Anthropic competes for talent against OpenAI and Google DeepMind, which sets a higher benchmark than Palantir’s defense-and-finance customer base. Second, Anthropic’s gross margin pressure (reportedly 40% post-inference cost surge) means the FDE has to drive higher contract sizes to justify cost; the comp ladder follows the revenue-per-FDE expectations.

Three observations on the comp data.

Observation 1 · The frontier-lab premium is structural, not transitional. When the FDE role first surged in 2024-2025, comp packages bid up rapidly because demand outpaced supply. The 2026 compensation has stabilized at the elevated level rather than reverting toward the Palantir baseline. This is the signal that the role has become differentiated — frontier-lab FDEs are not the same job as Palantir FDEs anymore, and the labor market prices them differently.

Observation 2 · Equity is now the central comp component. Seventy percent of FDE postings mention equity. At Anthropic, the gap between $582K median and $756K lead-level is largely equity-driven. At a $380B private valuation pre-IPO, equity has substantial expected value but high uncertainty. The IPO in October will resolve part of the uncertainty and likely produce a wave of FDE comp renegotiations as the realized equity value becomes known.

Observation 3 · The dispersion is high. From $200K (low-end Palantir) to $920K (top-end Anthropic) is a 4.6x range for nominally the same job title. The dispersion reflects different skill mixes, different customer types, different deployment complexity, and different lab compensation philosophies. An FDE working with a Palantir government customer doing data integration is a different job than an FDE building Claude agent skills at a Fortune 10 bank. The compensation reflects the gap.

2. The 800% growth, six months later

The Indeed-Financial Times analysis published in late 2025 documented an 800 percent surge in FDE job postings between January and September of that year. Six months later, the growth has continued but the composition has changed.

The volume now is harder to size precisely because the role has fragmented across multiple naming conventions: Forward Deployed Engineer, Applied AI Engineer (Anthropic), Solutions Engineer (revised), Deployment Strategist (Palantir-derived), AI Implementation Engineer, Agentic Solutions Architect. Aggregating across all titles, the May 2026 posting volume is approximately 4-5x the September 2025 baseline, which itself was 9x the January 2025 baseline. The cumulative growth from Jan 2025 to May 2026 is on the order of 35-45x.

The volume is no longer concentrated in AI labs. The expansion to enterprise consulting (BCG, EY), to integrated cloud-AI partnerships (Salesforce committed 1,000 FDEs, Databricks scaled, Cohere expanded), to international markets (Naver Cloud, Krafton, KDDI in Japan), and to specialized verticals (financial services AI, healthcare AI, defense AI) means FDE demand is now structurally distributed across 30+ employer categories.

Three structural shifts produced this expansion.

Shift 1 · The “integration wall” became visible. The original FDE dispatch identified the distinction between a model API and a deployed application as the structural reason FDEs exist. Six months later, the integration wall is no longer a niche analysis — it’s the default framing inside enterprise AI procurement. CIO surveys through 2025-2026 consistently identify integration complexity as the primary barrier to AI deployment, not model capability. The FDE is the role that breaks the wall.

Shift 2 · The agentic loop made FDE work harder. Six months ago, FDE work was largely RAG, prompting, fine-tuning, and integration. The agentic loop architecture — covered in the agent trap dispatch — produced a step-change in deployment complexity. Multi-step agents that span tool calls, sub-agents, MCP servers, and persistent memory layers cannot be deployed by sales engineers or implementation consultants. They require engineers who can write production code, understand model failure modes at 20-100 step horizons, and debug agentic loops in real customer environments. The FDE became more specialized as the work got harder.

Shift 3 · Salesforce, BCG, and EY institutionalized the role. When the original FDE piece ran, the role was an AI-lab specialty plus a Palantir niche. The Salesforce 1,000-FDE commitment, BCG’s BCGX → FDE rebrand, and EY’s UK and Ireland practice converted FDE from specialty to mainstream professional services category. The institutionalization compounds the demand: now consulting firms compete for the same talent pool that AI labs and Palantir compete for, and the comp ladder is structurally pressured upward.

3. The geographic shift · NYC overtakes SF

This is the structural surprise of the May 2026 data. Bloomberry’s analysis of 1,000+ FDE job postings places New York at 35 percent of postings versus San Francisco at 11 percent. Six months ago the ratio would have been roughly inverted.

Three drivers explain the shift.

Driver 1 · Financial services concentration. Twenty-four percent of FDE postings target financial services customers. Wall Street, the major investment banks, the asset managers, the regulated derivatives platforms — most are NYC-headquartered. An FDE deploying at a top investment bank works substantially in New York, regardless of where the AI lab is headquartered. The lab follows the customer.

Driver 2 · Federal government clients in the DC corridor. Eighteen percent of FDE postings target government and defense customers. The cybersecurity, intelligence, and federal-procurement work concentrates in the DC-Virginia-Maryland region, which is staffed from NYC more often than from SF. The Pentagon SCR designation litigation involving Anthropic plus the Mythos sole-source channel means a meaningful portion of frontier-AI federal work runs through East Coast hubs.

Driver 3 · The decoupling of AI labs from physical headquarters. Anthropic remains SF-headquartered. OpenAI is SF. Google DeepMind has a Mountain View base. But the FDE work is by definition not at headquarters — it’s at the customer. As the customers concentrate in NYC for finance and DC for federal, the FDE roles follow. This is structurally similar to how Goldman Sachs, JPMorgan, and Morgan Stanley have technology teams in Salt Lake City, Bangalore, and Warsaw — the work goes where the work is, not where the company is.

The NYC concentration affects compensation. New York living costs plus the financial-services compensation benchmarks produce upward pressure on FDE comp packages that exceeds what the AI labs would set if they were anchoring to Bay Area benchmarks alone. The Anthropic median TC of $582K is partly explained by NYC-weighted customer demand pulling the comp ladder up.

4. The skill mix has evolved

The skill mix in 2024-early 2025 was dominated by traditional AI engineering: machine learning, RAG, prompt engineering, model fine-tuning. The May 2026 skill mix, per Bloomberry’s analysis of 1,000+ FDE postings, has shifted decisively toward agentic capabilities.

| Skill | Share of FDE postings |

|---|---|

| AI Agents (autonomous systems) | 35% |

| LLM experience | 31% |

| RAG (Retrieval-Augmented Generation) | 12% |

| OpenAI specific | 8% |

| Anthropic / Claude specific | 7% |

| LangChain | 4% |

| LlamaIndex | 2% |

The agentic plus LLM categories together account for 66 percent of all skill mentions. RAG, which six months ago was the dominant deployment architecture, has receded to 12 percent. This is the structural signal: enterprise AI deployment has moved from “add a model to a knowledge base and retrieve” to “build an autonomous agent that operates across tool calls and sub-agents.”

This matches the role description that Anthropic’s Applied AI Engineer Greenhouse posting publishes. The job lists specific deliverables: “MCP servers, sub-agents, and agent skills that will be used in production workflows” plus “white glove deployment support for Anthropic products in enterprise environments.” The deliverables are agentic infrastructure, not RAG configurations.

The implication for compensation: the engineers who can build agentic systems in production environments are a smaller talent pool than the engineers who could configure RAG. Supply has not expanded as fast as demand. The comp ladder reflects the scarcity. An engineer with two years of production agentic-loop debugging experience commands materially more than an engineer with two years of RAG configuration experience, even though both are nominally “FDE” roles.

5. The customer industry mix · who buys FDE engagements

The 1,000-posting analysis reveals the customer industry distribution. Twenty-one percent of FDE postings explicitly specify target customers; the other 79 percent are vertical-agnostic. Of the explicit specifiers:

| Customer industry | Share |

|---|---|

| Financial Services / Banking | 24% |

| Government / Defense | 18% |

| Healthcare / Life Sciences | 17% |

| Insurance / Compliance | 12% |

| Manufacturing / Industrial | 9% |

| Retail / E-commerce | 7% |

| Public sector (non-defense) | 6% |

| Other | 7% |

The top three industries — financial services, government, healthcare — account for 59 percent of explicit-target postings. These are also the three industries with the highest enterprise contract sizes, the most complex regulatory requirements, and the highest tolerance for fully-loaded FDE costs.

This concentration matches the unit economics. An FDE deployed at a Fortune 50 bank can plausibly support a $5-15M annual contract. An FDE deployed at a federal defense customer can support multi-year contracts in the $10-50M range. An FDE deployed at a top hospital system or pharma can support $3-10M annual contracts. These contract sizes absorb the $220-400K fully-loaded FDE cost with significant margin headroom.

The industries that do not appear in the top tier — retail, e-commerce, mid-market software, consumer applications — are the industries where the FDE math collapses. Contract sizes too small to absorb the cost, deployment complexity too low to justify the role, customer integration depth too shallow to compound. The labs that try to deploy FDEs against these segments lose money on each engagement. The labs that focus FDE deployment on the top three industries capture the margin.

This is the strategic discipline that distinguishes FDE-positive from FDE-negative deployment. The volume of postings does not tell you whether the deployments are profitable. The customer-industry mix does.

6. Who’s expanding · the institutional landscape

The May 2026 institutional landscape for FDE practices includes substantially more employers than the original dispatch covered. Five categories.

Category 1 · AI labs (incumbent). Anthropic, OpenAI, Cohere, Mistral, Google DeepMind (via Vertex AI), AWS Bedrock services, Azure AI services. Each runs an in-house FDE practice, usually under varied internal titles (Applied AI Engineer at Anthropic, Solutions Engineer or FDE at OpenAI, Customer Engineer at Cohere). Comp packages range $350-920K total compensation depending on level and lab.

Category 2 · Palantir (incumbent benchmark). Continues to set the original FDE benchmark. Average TC $238K, range $205-486K, staff-level $630K+. Different customer mix from frontier labs (defense and finance vs. broad enterprise) means different skill profile. Palantir’s continued growth despite the AI-lab competition validates that the FDE motion has structural depth — the original employer is not being displaced.

Category 3 · Big Tech enterprise (rapid expansion). Salesforce committed to 1,000 FDEs publicly. Databricks expanded its FDE practice through 2025-2026. Microsoft, Google, AWS each run FDE-equivalent practices internally. The Big Tech enterprise expansion is partly competitive (countering the lab-direct motion) and partly customer-driven (existing enterprise relationships demand FDE deployment for AI workloads).

Category 4 · Consulting and professional services (institutionalization). BCG renamed BCGX engineering staff to FDEs in April 2026. EY launched a UK and Ireland FDE practice in the same month. Accenture, Deloitte, McKinsey Digital, and KPMG each have FDE-equivalent practices in expansion. The consulting expansion is meaningful because it validates FDE as a billable professional services category, not just an internal AI-lab function. Consulting firms charge $500-2,500/hour for FDE-equivalent work, which sets an external benchmark for the value the role produces.

Category 5 · International expansion. Korean expansion (Naver Cloud TF + Krafton) is the most visible international move. Japan (KDDI, NTT Data, SoftBank) has FDE practices in expansion. India (Tata Consultancy Services, Infosys, Wipro) has begun rebranding solution architects as FDEs. European consulting firms (Capgemini, Atos, T-Systems) are expanding FDE practices to capture EU AI Act compliance work that requires on-site enterprise deployment.

The total professional category as of May 2026 spans approximately 40-60 institutional employers, a 10x expansion from the dozen-or-so frontier-AI-lab and Palantir-only employer set of two years ago. The total addressable population of FDE roles globally is now in the 15,000-25,000 range; the actively employed population is approximately 8,000-12,000. Demand exceeds supply by approximately 2x.

7. The unit economics math

This is the central question the original dispatch did not fully answer. With the 2026 data, the answer is computable.

Cost per FDE. Fully-loaded FDE cost includes total compensation ($350-756K at frontier labs, midpoint $550K), benefits and overhead (~30% of TC, $165K), tooling and infrastructure ($30K), customer travel and engagement costs ($25K), management and oversight overhead ($75K). Total fully-loaded cost per FDE per year at a frontier lab: $845K at the midpoint, range $700K-1.2M. At Palantir or a consulting firm with lower TC and higher utilization, the fully-loaded cost is $400-700K.

Revenue per FDE. This is the variable that determines whether the math works. Three scenarios.

Scenario A · High-value enterprise (top 100 accounts). An FDE deployed at a top financial services, defense, or healthcare customer typically supports a contract in the $3-15M annual range. With one FDE primary plus partial allocation of other FDEs, the revenue per FDE FTE is approximately $5-10M. At a 40-50% gross margin, contribution per FDE: $2-5M. Coverage of fully-loaded $850K cost: 2.5-6x. Profitable as a service line.

Scenario B · Mid-market enterprise (next 1000 accounts). An FDE deployed at a mid-market bank, regional healthcare system, or specialized industrial company typically supports a contract in the $500K-3M annual range. Revenue per FDE FTE approximately $1.5-4M. At 40% margin, contribution per FDE: $600K-1.6M. Coverage of fully-loaded cost: 0.7-1.9x. Marginal — some accounts profitable, some break-even, some losing money.

Scenario C · Long-tail enterprise. An FDE deployed at a sub-$500K annual contract is structurally unprofitable. Revenue per FDE FTE approximately $300-700K. Contribution: $120-280K. Coverage of fully-loaded cost: 0.15-0.35x. Each engagement loses approximately $500-700K per year on a fully-loaded basis. The math collapses.

The strategic discipline question: which scenario is the lab targeting?

Anthropic’s customer profile — 8 of Fortune 10, 500+ customers at $1M+ annually, 80% enterprise revenue mix — places the company decisively in Scenario A. The company’s published Applied AI Engineer role description emphasizes “most strategic customers” and “transformational AI adoption,” which is the Scenario A targeting language. At this scale and mix, the FDE motion is profitable as a service line in addition to its distribution role.

OpenAI’s customer profile is more mixed. Stronger consumer revenue base, less concentrated enterprise. OpenAI’s FDE deployment likely spans Scenarios A and B, with the B portion producing margin pressure that contributes to the company’s $14B projected 2026 losses. The scale of OpenAI’s FDE operation is reportedly larger in absolute headcount than Anthropic’s; the per-FDE economics are likely worse on average.

The labs that do not yet have FDE programs — Mistral, Reflection AI, the spinout cohort, xAI — face the strategic decision now. Build FDE practices on Scenario A targeting from the start, or attempt Scenarios A and B simultaneously and accept the margin compression. The disciplined answer is Scenario A only. The competitive pressure pushes toward A and B simultaneously, which is how distribution growth races become operating-loss races.

8. The Anthropic Applied AI Engineer role · what the job actually is

Anthropic’s Greenhouse posting for Forward Deployed Engineer, Applied AI is the cleanest published description of what the frontier-lab FDE actually does in 2026. Five elements, each strategically meaningful.

Element 1 · “Embed directly with our most strategic customers.” This is Scenario A targeting in role description form. The FDE is not a generalist deploying to mid-market customers. The FDE works with the top accounts — the ones that absorb the cost.

Element 2 · “Deliver technical artifacts for customers like MCP servers, sub-agents, and agent skills that will be used in production workflows.” The deliverables are agentic infrastructure. MCP (Model Context Protocol) servers are connection points between Claude and external systems. Sub-agents are specialized Claude instances orchestrated by a primary agent. Agent skills are reusable behavioral packages. The FDE is building the agentic stack in customer environments, not just configuring RAG.

Element 3 · “Provide white glove deployment support for Anthropic products in enterprise environments.” The white glove framing acknowledges that Anthropic’s enterprise customers expect bespoke service. This is the structural cost driver — the work is high-touch and customer-specific by design. It is also the structural moat — once Anthropic is embedded in a Fortune 10 enterprise’s agentic infrastructure, the integration depth makes vendor switching expensive.

Element 4 · “Identify and codify repeatable deployment patterns and contribute insights back to our Product and Engineering teams.” This is the productization path. The FDE work is initially custom; the patterns get codified back into Anthropic’s product roadmap (skills marketplace, sub-agent orchestration, MCP server templates). The customization slowly converges toward productized capability, which reduces future FDE workload per customer.

Element 5 · “Maintain strong knowledge of the latest developments in LLM capabilities, implementation patterns, and AI product development stacks.” The FDE has to keep up with Anthropic’s own capability evolution — Mythos, Claude 4.7, agent skills, extended context. This is non-trivial because the capabilities ship faster than enterprise deployment cycles. An FDE who falls behind on Anthropic’s roadmap cannot effectively deploy current capabilities, which produces customer-specific technical debt.

The job is harder, more specialized, and higher-value than the 2024 FDE role description would have suggested. The compensation reflects the scope.

9. The strategic question · loss-leader or profit center

The original framing of the FDE motion treated it as a distribution mechanism — a way for AI labs to embed in enterprise customers at high cost in exchange for long-term contract expansion and integration depth. The unit economics math suggests this framing is wrong, or at least incomplete.

At Scenario A targeting, the FDE motion is simultaneously a profit center and a distribution mechanism. The contribution margin per FDE is positive (2.5-6x coverage of fully-loaded cost), the customer integration depth compounds into multi-year contract expansion, and the productized patterns reduce future per-customer FDE load. The economics work in three dimensions at once.

At Scenario B or C targeting, the FDE motion is genuinely a loss-leader, and the lab is funding distribution out of operating cash flow. This works only if the long-term value of the customer relationship exceeds the near-term loss, which requires assumptions about expansion economics that are difficult to validate at the time of deployment.

The question that matters for the IPO and forward valuation analysis: how much of Anthropic’s $30B run-rate revenue comes from Scenario A engagements versus Scenarios B and C? The customer concentration data — 8 of Fortune 10, 500+ at $1M+ — suggests the substantial majority is Scenario A. The S-1 disclosure will reveal the actual mix. If Anthropic’s enterprise revenue is 75-85 percent Scenario A, the FDE economics are structurally healthy and the path to FCF positive in 2027 is plausible. If the mix is closer to 50-60 percent Scenario A with a meaningful Scenarios B and C tail, the FCF target slips and the comp pressure compounds.

OpenAI faces the same disclosure question whenever its eventual S-1 files. The current information set suggests OpenAI’s mix is more Scenario B-weighted than Anthropic’s, which is consistent with OpenAI’s higher absolute losses ($14B projected 2026) and longer FCF horizon (2030 target).

For the spinout cohort and the smaller labs, the strategic implication is direct. Build FDE practices on Scenario A targeting from inception. Resist the competitive pressure to deploy against Scenario B and C accounts even if the volume looks attractive. The labs that maintain discipline on customer mix capture the margin. The labs that deploy widely to chase distribution growth produce operating losses that compound.

10. The talent supply constraint and what relieves it

The 2x demand-supply gap in the FDE labor market has held remarkably stable through 2025-2026 despite substantial expansion in employer base. Three reasons the gap persists.

Reason 1 · The role requires production engineering plus customer-facing skills. Most engineers can do one or the other; few can do both at production quality. The intersection is structurally narrow, and the training pipeline (universities, bootcamps, traditional employer paths) does not produce many candidates with both capabilities at scale.

Reason 2 · The agentic-loop specialization is new. Engineers with three or more years of production agentic-loop experience are rare because production agentic systems are themselves only 18-24 months old. The talent pool grows linearly with time as engineers accumulate experience. The 2027 cohort will be substantially larger than the 2026 cohort.

Reason 3 · The role is not yet a default career destination. Computer science graduates default toward software engineering at FAANG, machine learning research, or startup founding. FDE is an emerging path that is not yet visible on the standard career-mapping documents at top universities. As the role’s compensation, status, and intellectual content become more widely understood, the default-path effect will shift more candidates toward FDE roles. The shift is happening but slowly.

Two structural relievers will compound through 2026-2028.

Reliever 1 · BCG, EY, Accenture, Deloitte, McKinsey, KPMG, and Capgemini will collectively train 5,000-10,000 FDEs over 18-24 months. Consulting firms have the institutional capability to recruit, train, and deploy professional staff at scale. The consulting expansion adds meaningful supply to the talent pool. The FDEs trained at consulting firms will move into AI lab roles over 24-36 months as they accumulate experience, which expands the supply available to the labs.

Reliever 2 · International expansion adds non-US talent pools. The Korean (Naver, Krafton), Japanese (KDDI, NTT, SoftBank), Indian (TCS, Infosys, Wipro), and European (Capgemini, T-Systems) expansions add 10,000-20,000 FDEs to global supply over 24-36 months. Many of these will work primarily on regional customers, but cross-border talent flow into US AI lab roles will expand meaningfully.

By 2028, the supply-demand gap is likely to close to roughly 1.2-1.5x rather than the current 2x. The compensation premium will compress correspondingly, though probably not to the Palantir baseline. A 2028 frontier-lab FDE will likely earn $400-700K rather than $500-900K.

What to Do This Quarter

1. Engineering candidates. The FDE comp ladder is at peak premium. Frontier-lab roles will moderate by 18-24 months as the talent pool expands. Negotiate aggressive equity participation now while equity has the highest expected value (pre-IPO Anthropic, pre-restructured OpenAI). Focus skill development on agentic-loop production debugging, MCP server engineering, and customer-facing technical communication. The skills mature at scarcity premium.

2. AI lab strategy. Maintain Scenario A targeting discipline on FDE deployment. Resist competitive pressure to deploy against Scenarios B and C accounts even when volume looks attractive. Build customer-mix dashboards that explicitly track contract size distribution; the FDE motion is profitable on the right side of the distribution and unprofitable on the left.

3. Enterprise CIOs / CTOs. Two implications. First, FDE-led deployment at $3M+ annual contract sizes produces high-quality outcomes; expect to pay for it in contract pricing. Second, don’t accept FDE-light deployment from labs whose comp data suggests they’re using junior engineers as branded FDEs. The economics don’t work; the deployment quality won’t either.

4. Consulting firms. The FDE practice is the most strategically important new line of business in professional services in 15 years. The window to build leadership position is 24-36 months. After that, the category consolidates around the firms that scaled fastest. BCG, EY, and the early movers have the structural advantage; the firms that delay materially in 2026 will compete from a lower position through 2030.

The Strategic Read

Six months after the original FDE dispatch, the role has institutionalized, the compensation has stratified, the geographic concentration has shifted, and the unit economics have become computable.

The labs that deploy FDEs against high-value enterprise customers (Scenario A · top 100 accounts at $3M+ annual contracts) capture both distribution and margin simultaneously. The labs that deploy against mid-market or long-tail customers subsidize distribution out of operating cash flow at a cost that compounds through the IPO window.

Anthropic’s customer concentration profile suggests the company is targeting Scenario A primarily, which makes the FDE motion structurally healthy and consistent with the 2027 FCF positive target. OpenAI’s profile suggests a more Scenarios A and B mix, which is consistent with the company’s higher losses and longer FCF horizon. The S-1 disclosures will resolve which lab is which.

The 2x talent supply-demand gap will compress through 2026-2028 as consulting firms and international markets train and deploy substantially more FDEs. The compensation premium will moderate but not collapse to the Palantir baseline; the frontier-lab differentiation persists.

The single under-priced strategic variable: customer-mix discipline. Labs that maintain Scenario A targeting capture the margin. Labs that chase volume across Scenarios B and C produce operating losses. The discipline is hard because competitive pressure pushes toward volume; the labs that hold the line capture the structural advantage.

The FDE motion is the human layer of frontier AI revenue scaling. The economics determine which labs reach FCF positive and which do not. The math is now computable. The discipline determines who wins.

Forward-Deployed Engineers are the human layer that converts compute and capability into enterprise revenue. The unit economics work decisively at high-value enterprise scale and collapse at mid-market and long-tail. Customer-mix discipline determines which labs reach FCF positive and which do not. The math is now computable.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The Anthropic IPO Disclosure Document — what the S-1 has to say

- The Compute Concentration Audit — sovereign wealth funds notice

- The 2028 Model Lab Endgame — scenario forecast

- The Memento Constraint — continual learning trillion-dollar bottleneck

- The Two Channels — Pentagon AI procurement architecture

- The Agent Trap — feature vs. infrastructure

- The 27% Problem — Anthropic’s enterprise lead

Sources

- Levels.fyi, Anthropic Software Engineer Salaries — May 5, 2026 update; median $582,500, range $563-756K, top $920K

- Levels.fyi, Palantir Forward Deployed Engineer Salaries — average $238K, range $205-486K, staff-level $630K+

- Anthropic Greenhouse, Forward Deployed Engineer, Applied AI job posting (May 2026)

- Hashnode, Tech’s secret weapon: The complete 2026 guide to the forward deployed engineer — comp benchmarks and geographic shift data

- Bloomberry, What I learned analyzing 1K forward deployed engineer jobs — skills mix and customer industry distribution

- Indeed × Financial Times analysis, FDE postings +800% Jan-Sept 2025

- Seoul Economic Daily, Hiring for ‘Forward Deployed Engineers’ Surges 8-Fold in AI Era (May 1, 2026) — Korean expansion (Naver Cloud, Krafton, BCG rebrand)

- Entrepreneur Loop, What Is a Forward Deployed Engineer? — Salesforce 1,000-FDE commitment, EY UK+Ireland practice launch April 2026

- Sundeep Teki, Forward Deployed AI Engineer career guide — RS compensation $350K-$1.4M

- Sacra, Anthropic revenue, valuation & funding — 8 of Fortune 10, 500+ customers at $1M+/year

- Author calculations on revenue per FDE, fully-loaded FDE cost, and contribution margin scenarios