The Control Series, Part 6 of 6 · Chokepoint: Capital. The finale. Part 5 ended on a question — you might own the door, but who’s funding the building? Here is the answer, and the close of the series.

Strip this series back to its foundation and you reach a single sentence: every chokepoint costs money. A gigawatt of power, a 555,000-GPU cluster, a war’s worth of exclusive data, a frontier training run, a category-defining interface — none of them exist without someone willing to write a very large check. Capital is the chokepoint beneath the chokepoints. Whoever can fund the buildout decides who gets to build at all.

In 2026 the bill came due, and it came due in public. Within a single span of weeks, the three most valuable private companies in AI lined up to convert their private bets into public risk — the largest concentrated fundraising Wall Street has ever been asked to absorb. And the money paying for all of it has been moving in a circle that makes everyone’s numbers look spectacular, right up until the moment it doesn’t.

This is the last lever. It’s also the one holding all the others.

Capital: The Lever Beneath the Levers

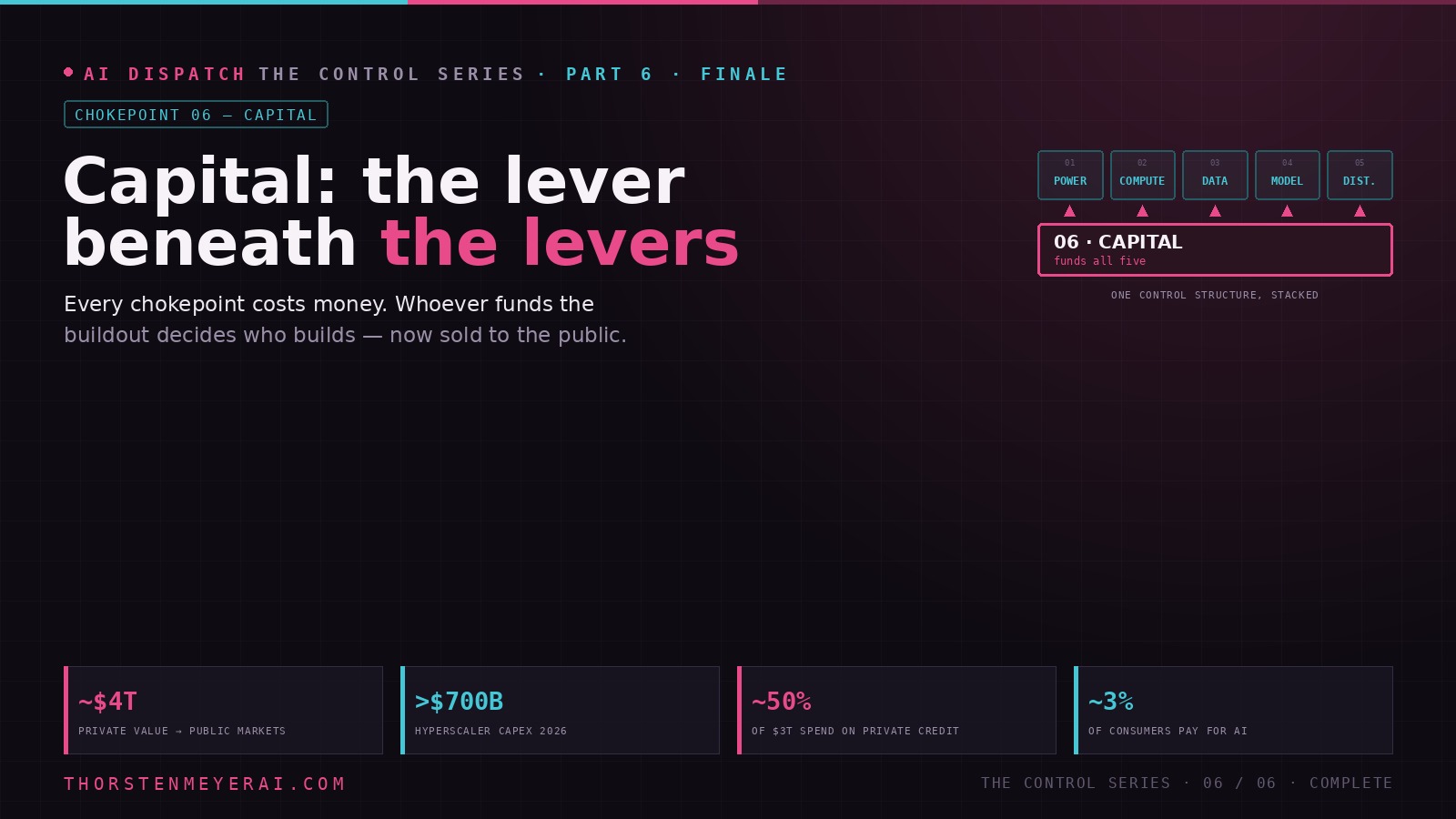

Every chokepoint costs money — so whoever can fund the buildout decides who builds at all. In 2026 the bill came due in public: a trillion-dollar IPO wave, financed by a circle of firms paying each other, now sold to everyone else.

The meta-chokepoint: it gates the other five, because you can’t build any of them without clearing the capital bar. A synchronized machine has no natural brake — no one can slow first — and the IPO wave moves the risk to the public as insiders take gains. The hedge is solvency that doesn’t depend on the music playing: sane burn, own what’s cheap, self-host where you can.

The bill comes due in public

On June 12, SpaceX — which now contains xAI — listed on the Nasdaq, priced at $135 a share for a valuation near $1.77 trillion, then surged past $2 trillion in early trading, briefly minting the world’s first trillionaire. The offering was reportedly oversubscribed several times over, against a $75 billion target, and held back something like 30% of shares for retail buyers, far above the usual 5–10%.

It was the opening act. Anthropic confidentially filed on June 1 at a roughly $965 billion valuation (against about $47 billion in annualized revenue, not yet profitable), having just closed a $65 billion round. OpenAI is reportedly filing for a fall listing at $730–850 billion, against a 2026 cash burn near $27 billion. Stacked together, these three represent something on the order of $4 trillion in private value queued to hit public markets inside an eighteen-month window.

Bank of America described the cycle plainly: it is a large-scale transfer of accumulated risk from early investors to the public market. The supporting detail is hard to unsee — more than 600 current and former OpenAI staff had already sold roughly $6.6 billion in stock on the secondary market ahead of the listing. The people closest to the numbers are taking some chips off the table at the exact moment the public is invited in. That is not proof of a bust. But it tells you which direction the risk is flowing.

INFINIBAND FOR HIGH-PERFORMANCE COMPUTING AND AI CLUSTERS: Configure RDMA networking, optimize GPU interconnects, and build low-latency infrastructure for distributed training and HPC workload

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The ouroboros

Now look at where the money goes once it’s raised, because the capital chokepoint has a peculiar shape: it bends back on itself.

The established giants — Microsoft, Amazon, Google — pour money into Nvidia. Nvidia pours money into OpenAI and others, which spend it on Nvidia chips. Microsoft “invests” in OpenAI partly through Azure credits; Amazon backs Anthropic partly through AWS credits — a currency, as one analyst noted, that can be spent nowhere else. Musk used SpaceX to acquire xAI from himself. The whole arrangement is a financial ouroboros, a snake eating its own tail.

The asset manager Man Group described the machine cleanly: OpenAI drives Microsoft’s spend, Microsoft drives Nvidia’s orders, Nvidia funds the data-center vehicles, the vehicles drive utility expansion — and if any node slows, all nodes slow. That circularity produces two specific dangers. The first is reflexive demand: revenue looks endless because each company in the loop is buying from the next, so a single pullback cascades into falling revenue across the entire cluster. The second is mispriced capacity: capital-expenditure decisions get justified by demand signals coming from inside the loop rather than from independent customers in the real economy.

You can already see the first hairline crack. Microsoft has stepped back from its commitment to supply all of OpenAI’s compute, letting Oracle and neoclouds fill the gap — a quiet signal of caution from the most important node in the machine, even as everyone else kept spending. No single player can afford to be the first to slow down, even when collective restraint would be the rational move. That is exactly how synchronized machines break.

NVIDIA Tesla A100 Ampere 40 GB Graphics Processor Accelerator – PCIe 4.0 x16 – Dual Slot

- Memory Capacity: 40 GB GDDR6

- Host Interface: PCIe 4.0 x16

- Cooling Type: Passive Cooler

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The fragility: private credit and the public

Here is what makes capital the most fragile chokepoint rather than the sturdiest. Morgan Stanley estimates roughly $3 trillion in global data-center spending between 2025 and 2028, about half of it funded by private credit. Hyperscalers alone are projected to spend more than $700 billion on AI infrastructure in 2026. And the end demand underwriting all of it remains thin — by one estimate only about 3% of consumers pay for AI at all.

That combination — enormous debt-financed capex, circular internal demand, and a slender base of real paying customers — is why economists warn that the broader economy is growing more fragile, not less. AI-exposed companies now make up a record share of the stock market, so a stumble in the cluster is no longer contained to tech. Goldman’s chief executive captured the mood with unusual candor: there is more greed than fear right now, and plenty of liquidity — so long as the world stays optimistic. That conditional is the whole ballgame. A jittery early-June selloff, when chip and hardware stocks dropped sharply on doubts about capex, was a reminder of how quickly optimism can wobble.

And the IPO wave does something specific with all this risk: it moves it. Private investors and insiders, who took the early risk and the early gains, hand the position to pensions, index funds, and retail buyers at trillion-dollar valuations set with no prior public scrutiny. The capital that underwrites every other chokepoint is being repriced and redistributed onto the public — at the top.

AI Data Center Infrastructure Engineering: Power Distribution, Liquid Cooling, High-Density Networking, and Energy Efficiency for GPU Training … Hardware & Compiler Engineering Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Who holds the capital chokepoint

A very short list. The mega-balance-sheet firms (Microsoft, Amazon, Google, Nvidia) that can fund a buildout from cash flow. The sovereign and mega-funds (SoftBank, Gulf vehicles like MGX) large enough to anchor a $500 billion data-center project. The private-credit market quietly financing half the construction. And now public-market and index investors, inheriting the position at the end.

Whoever can fund a frontier run decides who gets to attempt one — which means the capital chokepoint silently gates all five of the others. You cannot build the power, buy the compute, license the data, train the model, or win the interface without first clearing the capital bar, and that bar now excludes all but a handful.

ciciglow High Speed SAS Card 6Gbps with 8 Ports for Large Scale Data Storage Solutions

- High-Speed Data Transfer: 6Gbps on 8 channels for fast performance

- Extensive Device Support: Connects up to 256 devices

- Versatile Connectivity: 4 internal SATA and 4 external SAS ports

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The whole machine

Step back, and the six installments resolve into one picture.

Capital funds the power, which energizes the compute, which trains on the data, which produces the model, which reaches a human through the interface. Six chokepoints, but not six separate stories — a single control structure, stacked, with capital underneath holding it up. Squeeze any layer and the ones above it feel it. Starve the capital at the bottom and the entire stack contracts at once.

That is the thesis this series opened with, now fully drawn. For a decade AI was sold as a utility — abundant, neutral, always on. 2026 revealed it as a lever: scarce, controlled, revocable, and squeezable at six points, each owned by a shrinking number of hands. A government pulled the switch at the model layer. A landlord wrote a reclaim clause at the compute layer. A war became a licensed dataset. A company paid sixty billion dollars for a door. And the whole edifice turned out to be financed by a circle of firms paying each other, now asking the public to hold the bag at the top of the market.

My take

Capital is the meta-chokepoint, and I’d hold two truths about it at once.

The first: the bull case is not stupid. Demand for AI is real and growing; the liquidity is genuinely there while confidence holds; vendor financing has precedent in earlier infrastructure booms; and if the productivity gains arrive at the scale the optimists expect, the buildout pays for itself and the circularity looks, in hindsight, like ordinary ecosystem investment. Not every loop is a fraud, and not every bubble warning is right.

The second, which I weight more heavily: the structure is fragile in a way the individual deals obscure. Reflexive demand means the system has no natural brake — no one can afford to slow first. Mispriced capacity means the capex is being justified by internal signals, not external customers. And the IPO wave transfers that risk to the public precisely as insiders take gains. You don’t need fraud for a synchronized machine to seize; you just need one node to slow, which Microsoft may already be signaling.

For anyone building on top of all this — the position most companies and countries occupy — the capital chokepoint is the one you can’t out-build, so the response is not to compete with it but to avoid depending on it. Keep your burn sane enough that you don’t need the circular money. Own the layers you can own cheaply — your proprietary data, your interface, your user relationship — and self-host open-weight inference where the economics allow, so a credit contraction in the cluster doesn’t take your product down with it. Don’t tie your fate to a node in the loop. For nations, the lever is capital sovereignty: public and sovereign investment that doesn’t route through someone else’s circle. The throughline of all six installments is the same word — optionality — and at the capital layer it means solvency that doesn’t depend on the music continuing to play.

The watch items for the rest of 2026 are unusually consequential, because this is the layer that moves the others: whether OpenAI’s and Anthropic’s public filings reveal margins that justify the valuations, or compress them and cascade through every VC portfolio holding AI; whether more nodes follow Microsoft toward caution; whether private-credit lenders pull back on AI-collateralized debt; and whether the real-economy demand finally shows up to validate the capex, or doesn’t.

The series, closed

Six chokepoints — power, compute, data, model access, distribution, capital. One pattern: every layer of AI is concentrating into a few hands, and 2026 is the year those hands began to squeeze, and the year the bill went public.

The question was never whether AI is powerful. It plainly is. The question this series set out to answer is who holds the levers — and the honest reading is that a remarkably small number of firms, funds, and governments now hold all six, financed in a circle and underwritten, at the end, by everyone else. That concentration buys real things: efficiency, scale, coordinated safety, the sheer capacity to build frontier systems at all. It also buys control, and control gets used.

A utility, you’re allowed to forget about. A lever, you have to watch who’s holding. The work now — for builders, for institutions, for nations — is to keep enough optionality that when one of these six gets squeezed, you are not the one who gets crushed.

That’s the series. The levers are visible now. Watch the hands.

Sources: SpaceX, OpenAI, and Anthropic SEC filings and reporting; Bank of America; Goldman Sachs; Morgan Stanley; Man Group; CNBC; TIME; Forbes; Bloomberg; and prediction-market data (Q1–June 2026). Valuations and commitments are as reported and, in several cases, multi-year; revenue and burn figures are as disclosed or estimated. Analysis and opinions are the author’s.