The Associated Press was founded in May 1846 when five New York newspapers pooled the cost of telegraphing copy from the Mexican–American War. Reuters followed in 1851, starting with homing pigeons between Aachen and Brussels. For 178 years, the wire was the answer to a single economic problem: original reporting cost more than any one outlet could carry, so everyone paid in and everyone ran the same paragraph. That arrangement is unwinding.

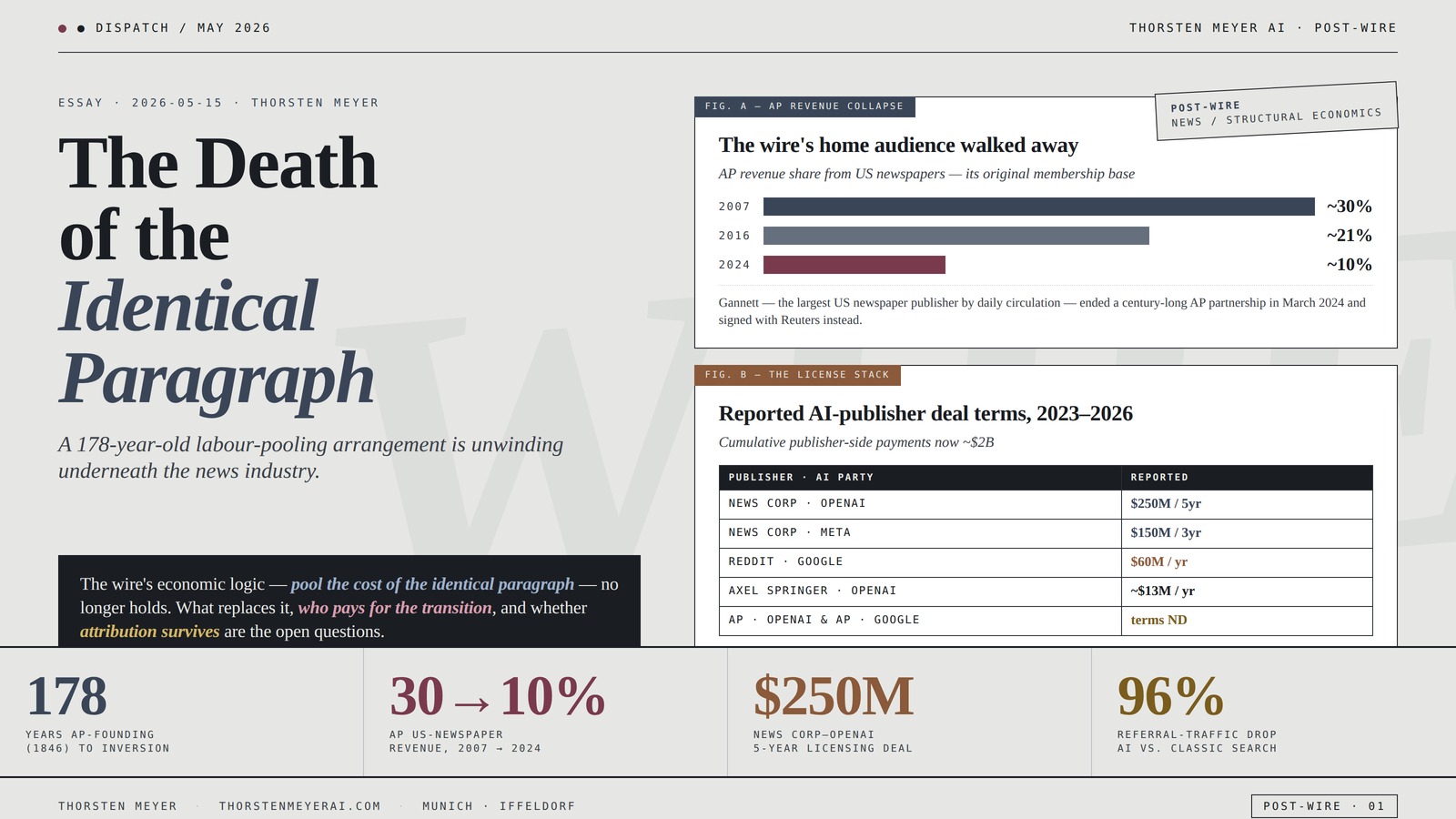

AP’s revenue from US newspapers fell from roughly 30% in 2007 to 10% in 2024. In March 2024, Gannett — the largest US newspaper publisher by daily circulation — ended a century-long AP partnership and signed a competing local-news offering with Reuters instead. News Corp signed a five-year, $250M licensing deal with OpenAI in May 2024 and a $150M three-year deal with Meta in March 2026. AP signed its first deal with Google in 2025 to put real-time news into Gemini. The New York Times is in active discovery against OpenAI and Microsoft and filed a separate complaint against Perplexity in December 2025 alleging “skip the click” substitution and 175,000 unauthorized scraping attempts in August 2025 alone.

A TollBit study cited in that complaint found AI search engines send roughly 96% less referral traffic to news sites than traditional search. The wire’s economic logic — pool the cost of the identical paragraph — no longer holds. What replaces it, who pays for the transition, and whether attribution survives the shift are the open questions of the post-wire era.

The Death of the

Identical Paragraph

(1846) to economic inversion

newspapers, 2007 → 2024

five-year licensing deal

traffic collapse (TollBit)

results AI-generated, Sept 2025

reaching Google results

March 2024 Helpful Content Update

AI search vs. classic search (TollBit)

Five New York papers founded the AP cooperative in 1846 because no single one of them could afford a correspondent in the field — but five sharing the telegraph bill could. That arithmetic is what has changed.Thorsten Meyer · The Death of the Identical Paragraph

I · The Wire That Was

The thing to understand about the wire is that it was always a labor-cost trick.

Five New York papers founded the AP cooperative in 1846 because no single one of them could afford a correspondent in the field for the Mexican–American War, but five sharing the telegraph bill could. Paul Julius Reuter, working out of Aachen, was running stock prices to Brussels by homing pigeon by 1850 and to London by undersea cable by 1851. By 1865, Reuters, the French Havas (later AFP), and the German Wolff signed a cartel agreement designating exclusive reporting zones across Europe — Havas got the French Empire and South America, Reuters got the British Empire and the Far East, Wolff got central Europe — and pooled the output. A French provincial newspaper in the 1880s paid Havas 10,000 francs a year for 1,800 lines of telegraphed text per day. That is the arithmetic of the wire: divide the cost of a foreign bureau by the number of subscribers, multiply by a markup, and run the same paragraph in every paper.

The cooperative form mattered. AP is still a not-for-profit member cooperative — its members are the publishers, its job is to keep their joint reporting costs down. By 2016, copy filed by AP correspondents was being republished by more than 1,300 newspapers and broadcasters. AP today operates 235 bureaus in 94 countries and pulls roughly 128 million monthly website visits in its own right. Reuters runs about 2,500 journalists across 200 locations and attracts 105 million monthly readers. Both agencies still produce most of the international news that appears in the world’s papers — that figure has been estimated at 90%-plus by Big-Three watchers for half a century and there is no evidence the number has materially fallen.

The number that has fallen is who pays them for it. AP’s share of revenue from US newspapers — its historical home audience — was around 30% in 2007. By 2024 it was 10%. Print advertising collapsed; print circulation collapsed faster; the cooperative survived by diversifying into broadcast (37% of revenue), digital ventures (15%), and international (18%). The newspaper-cooperative model survived the newspaper. The question is how long.

As an affiliate, we earn on qualifying purchases.

II · The Floor Falls Out

The wire existed because everyone wanted the same paragraph and no one could afford to write their own. That second clause is the one that broke.

The marginal cost of rewriting a wire story in the voice of a specific magazine — not summarising it, not translating it, but recasting it for a different audience with different priors — used to require a human editor. By 2024 it required an LLM call costing fractions of a cent. In production, in the system I run, the cost per per-site rewrite of a 600-word source story lands around $0.003 in inference, on a Mac fleet running open-weight models locally; even at the high end of cloud-API pricing it would be under $0.02. A 50-site fan-out is a dollar. A 500-site fan-out is ten. That is below the marginal cost of not rewriting — below the cost of running the same paragraph through a CMS twice.

When the cost of differentiated copy drops under the cost of identical copy, the wire’s economic logic inverts. It is now cheaper to publish a per-audience rewrite than to syndicate the identical paragraph. The pool-the-cost-of-the-paragraph trade that built AP and Reuters does not stop working — the wire still has the bureau in Kyiv that nobody else does — but the distribution side of the trade dissolves. There is no reason for a niche audio-engineering magazine and a niche home-improvement magazine to run the same paragraph just because they both subscribed to the same wire. There is no reason for either of them to run wire copy at all if they can rewrite the source story in their own register for less than the licensing fee.

This is not theoretical. The system I built behind StrongMocha News Group is one example among many. A live news globe of 227 RSS sources feeds an engine that ranks each story against a catalog of 450-plus magazines, picks up to five best fits (rejecting the story entirely if no site clears a confidence floor), extracts the source body once, and fans out per-site rewrites that preserve attribution back to the original publisher. Eight per cent of stories get rejected. Average fan-out is 4.2 sites. The economics work because the rewrite cost is lower than the not-rewriting cost.

publisher ops

source → fit

Read the World,Then Publish

A 3D news globe of 227 sources, a top-N matcher, and 450+ magazines form a system where one source story is recast only where it structurally belongs.

Intelevia 7" Smart E-Paper Desktop Calendar, Wi-Fi Digital Desk Clock with Weather & News, Eye-Friendly E-Ink Display, Auto-Refresh Perpetual Calendar for Office, ABS Shell – Black

- Wi-Fi Sync & Weather Updates: Automatically updates weather and time

- 7-Inch Eye-Care E-Ink Display: Zero blue light, flicker-free screen

- Wide Viewing Angle: 180° ultra-wide clarity from any angle

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

From globe to fan-out

Stenvrik watches the world. DojoClaw decides which few magazines have standing. WordPress becomes the durable truth surface.

227 sources

matcher

extract

per voice

published

Industrial Network Security: Securing Critical Infrastructure Networks for Smart Grid, SCADA, and Other Industrial Control Systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The machine has a reason not to publish

Low-confidence matches are dropped. Zero matches return 422 no_matching_site. Scarcity is imposed inside an abundant system.

~92% clear the match floor.

~8% are cleanly rejected.

The Wall Street Journal. | World Business & Market News

- Trusted journalism from WSJ: Trusted insights from a renowned newspaper

- Unlimited news access: Access Business, Markets, Politics, World, U.S. News & Economy

- Comprehensive business coverage: World-renowned coverage on economy and stock data

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Large enough to matter, constrained enough to trust

The unglamorous center

Readability pulls the article body once. If extraction fails, the system degrades to a headline-only source marker instead of inventing unsupported body text.

The status chip is a truth surface

A queue can fail and recover. A published WordPress URL is durable evidence. The status route must distinguish job noise from publication fact.

failed > generating > queued > exists > published

What the wire still uniquely does — the part the LLM cannot do — is the bureau in Kyiv. The reporting itself. The wire is shifting from a paragraph-distribution business to a fact-supply business: the question is no longer “what paragraph do I run” but “what did the wire correspondent actually report, and how do I render that for my readers.” This is a different industry. It pays differently, structures differently, and — critically — values original reporting differently from how the cooperative did.

III · The License Era

Three economic models for AI-and-news compensation are visible in the deals signed since 2023, and they are doing different things.

The first is training-data licensing — paying for archival access so a model can learn from the corpus, with no ongoing display obligation. AP’s original July 2023 deal with OpenAI was largely this: a two-year license to AP’s text archive going back to 1985. Financial terms undisclosed; useful as a precedent, modest as cash flow.

The second is display licensing — paying for the right to surface summaries, quotes, and logos inside a chat interface or assistant, with links back to the publisher. This is what most of the 2024–2025 deals are doing structurally. News Corp’s deal with OpenAI is reported at $250M over five years across the Wall Street Journal, New York Post, Barron’s, MarketWatch, and other titles. Axel Springer reportedly receives around $13M a year for Business Insider, Politico, Bild, and Welt. The Financial Times deal is reported at $5–10M a year. The Guardian, Le Monde, Prisa, Schibsted, Hearst, Dotdash Meredith, Vox Media, Condé Nast — most large Western publishers now have an OpenAI deal of this shape. Google signed AP for Gemini in 2025; Mistral signed AFP for Le Chat (2,300 stories a day in six languages); News Corp signed Apple in October 2025; Meta is paying News Corp up to $50M a year over three years from March 2026.

The third — and the one that matters for the post-wire era specifically — is raw-feed licensing for downstream rewrite and re-publication. Almost no current deal is structured this way. The training/display split assumes the AI is a destination (a chatbot, an assistant, a search interface) and the publisher’s content is displayed inside it. The post-wire model assumes the AI is an intermediate layer that consumes the source and produces N differentiated outputs for N publication endpoints downstream — which is what a newsroom historically did with wire copy. There is no industry-standard contract for this yet. Publishers selling “summaries inside ChatGPT” rights have not generally sold “raw feed for downstream per-audience rewrite” rights, and the cooperative wire agencies — AP, Reuters, AFP — sold the latter to human newsrooms for 150 years without contemplating that an LLM might be on the receiving end of the same feed.

This gap is where the next round of negotiation will happen. It will not happen cleanly. The publishers least interested in selling raw-feed rights are the ones with the strongest brands; the publishers most interested are the wire agencies themselves, whose entire business model is selling raw feeds and whose unit economics have not adjusted to the fact that the buyer is now sometimes a model rather than a copy editor.

IV · The Trust Problem

The search engines, which underwrite most of news economics through referral traffic, have made the post-wire era harder, not easier.

Google’s helpful-content systems — Helpful Content Update through 2024, the “scaled content abuse” manual actions in June 2025, the December 2025 core update — have all been pointed at the same target: pages that are technically competent but indistinguishable from fifty other pages covering the same topic in the same way. The March 2024 update reportedly cleared roughly 45% of low-value sites overnight. The December 2025 update, by SEO-industry reports, hit “competent but generic” content — pages that answer the query but do not demonstrate that the writer has done the thing. Roughly 17% of top-20 Google results are AI-generated as of mid-2025; one industry study finds over 50% of new web content is AI-produced while only 12% of it reaches search results.

The paradox sits exactly here. Per-site rewrite at scale, done well, should be exactly what Google’s helpful-content systems want: a home-improvement magazine treating a tariff story as a home-improvement story, a defence-procurement site treating it as a procurement story, both with attribution back to the source. That is differentiation in the sense Google claims to reward. The problem is that the same fan-out architecture, done badly, produces fifty interchangeable AI-paraphrases of the same wire copy — exactly what Google’s systems are pointed at killing.

The trust signal that distinguishes the two is attribution. A per-site rewrite that links back to the source story, names the source publisher, and inherits that publisher’s authority is structurally different from a paraphrase with no provenance. The wire’s economic model produced authority through identical reproduction — every reader of every newspaper that ran the AP paragraph saw the same paragraph, traceable back to AP. The post-wire model produces authority through attributed differentiation — every reader sees a rewrite, but every rewrite carries a link back to whatever reporting it stands on. Different mechanism, same function. The search engines are still calibrating to the new mechanism, which is why this period is so noisy.

Whether attribution holds is the question that decides whether the post-wire model produces a healthier news ecosystem or a worse one. The wire era’s tradeoff — labour pooling at the cost of paragraph monotony — was at least legible to a reader who knew to look at the byline. The post-wire era’s tradeoff — per-audience differentiation at the cost of provenance complexity — only works if the attribution link is unambiguous, persistent, and machine-readable. None of those three is currently guaranteed.

V · The Aggregator Question

The Perplexity lawsuit cluster is the test case for what happens when attribution fails.

The New York Times filed against Perplexity on December 5, 2025, two years almost to the day after suing OpenAI and Microsoft. The complaint differs from the OpenAI suit in a specific way: it is not principally a training-data complaint. It is a substitution complaint. The Times alleges that Perplexity’s retrieval-augmented generation product scrapes the Times’ content (including past paywalls), uses it to construct what amount to near-verbatim summaries, and serves those summaries to users in lieu of sending them to the source — Perplexity’s “skip the click” tagline, dropped after the Dow Jones complaint, was cited as evidence. The TollBit study quoted in the filing reports that AI search engines send roughly 96% less referral traffic to news sites than conventional search engines. Perplexity reportedly made over 175,000 attempts to access nytimes.com in August 2025 alone, ignoring its robots.txt and a hard block. Other complaints in the same posture: Dow Jones / News Corp (October 2024), Chicago Tribune (December 2025), Encyclopaedia Britannica and Merriam-Webster (September 2025), Reddit (October 2025), Penske Media against Google over AI summaries (September 2025).

What these complaints are testing, structurally, is whether attribution at the AI layer is enforceable. Perplexity’s defence — recycling a sentence variant attorneys have been deploying since the radio era — is that publishers have been suing new technologies for a century and have generally lost, or “we’d all be talking about this by telegraph.” This is rhetorically nice and structurally incomplete: the broadcast-rights settlements of the 1930s, the cable-retransmission consent regime of the 1990s, the music-streaming licensing regime of the 2010s all were the publisher-side wins, just packaged as licensing rather than prohibition. The Anthropic settlement with the authors in Bartz v. Anthropic — $1.5B in September 2025, the largest publicly reported copyright recovery in history — is the same shape. So is the German Munich court ruling against OpenAI on lyrics memorisation in November 2025. So is the UK High Court split on Getty v. Stability AI, where the model weights themselves were ruled not to be infringing copies but the trademark claims on reproduced watermarks succeeded.

The pattern across these is that AI companies will pay, eventually, for content used in ways that substitute for the original. The unsettled question is the rate and the mechanism. The current display-licensing rate — roughly $13–50M per year per major publisher group, scaling with brand authority — is the AI industry’s opening bid. The publisher lawsuits are the counter-bid. Where this settles will determine whether per-site rewrite at fan-out scale is licensed as an extension of wire syndication (cheap, voluminous, with attribution preserved) or as a substitute for the original reporting (expensive, contested, with attribution disputed).

VI · Who Pays For The Transition

The cooperative wire model was, among other things, a labour-pooling subsidy. Five New York papers in 1846 could not afford their own correspondent in northern Mexico; together they could afford one, and the correspondent’s wages came out of the joint subscription. AP’s $100M nonprofit launch in June 2024, aimed at state and local news, is a recognition that the cooperative form is failing to fund that labour at the scale it used to. Gannett’s departure from AP in March 2024 — ending a partnership of over a century — and its switch to a Reuters-Gannett joint local-news offering is the same recognition from the publisher side: the cost of pooled reporting is no longer reliably amortisable across a shrinking newspaper base.

The post-wire economics threaten to make this worse before they make it better.

The reason is that the per-site rewrite cost has dropped to fractions of a cent, but the per-bureau reporting cost has not. A Reuters correspondent in Kyiv still costs what a correspondent costs. The economics of fan-out reward whoever sits closest to the source feed: the publisher who licenses raw AP material and runs it through 50 per-audience rewrites captures most of the value the wire used to capture from 50 separate subscribers. If the licensing payment to AP for that raw feed is set at one-fiftieth of what 50 newsroom subscriptions used to cost — which is broadly what the current display-license rate cards suggest — the wire’s revenue per unit of reporting collapses. The bureau in Kyiv gets harder to fund.

The hopeful version of this story is that the licensing dollars flowing from AI companies to publishers ($250M from OpenAI to News Corp, $150M from Meta, $60M/year from Google to Reddit, the AP-Google Gemini deal, the cluster of mid-eight-figure deals to the Axel Springers and Schibsteds of the world) are large enough in aggregate to fund the bureaus that publisher subscriptions no longer do. The sceptical version is that those dollars accrue mostly to brand-strong publishers (NYT, WSJ, the Murdoch titles) rather than to the wire cooperatives whose original-reporting function is most structurally exposed. AP is a member cooperative; it sells news; it does not have a Murdoch.

It is not yet clear which version is true. The structure of the next round of deals — particularly whether the cooperative wire agencies negotiate display-licensing deals at the same per-publisher rate as the major individual brands, or at a different, higher rate that reflects their aggregate output — will determine whether the bureau in Kyiv stays funded through the transition or gets cut as a line item in the next reorganisation. Reporters who used to file wire copy for 1,300 outlets and now compete with AI fan-out from a single licensed source are not, structurally, in a stronger position. Whether the dollars flow back far enough down the stack to keep them employed is a labour-economics question and an open one.

VII · The Shape After

The wire is not dead. The identical paragraph is.

AP and Reuters will both exist in 2030. Their bureaus will exist. Their reporters will still file. What will not exist in 2030 is the world in which a wire story moves from a single source through a paragraph-distribution layer to a thousand mastheads all carrying the same paragraph below their nameplates. That layer is being replaced by a per-audience rewrite layer that produces N versions of the story instead of one, with attribution running back from each version to the originating reporter. The cost structure is different. The trust signals are different. The licensing economics are different. The labour economics are different.

What stays the same is the underlying problem the wire was invented to solve in 1846: original reporting costs more than any one outlet can carry alone. The cooperative answer to that problem worked for 178 years because the marginal cost of the paragraph layer — the distribution part, not the reporting part — was very low and the marginal cost of differentiation was very high. The post-wire era inverts those two costs. The reporting layer is still expensive; the paragraph layer is now essentially free; and the differentiation layer is also essentially free.

Three things follow. First, distribution economics will keep compressing toward zero, and any business model built on selling the paragraph itself will keep getting harder. Second, the reporting economics will keep getting worse unless the licensing dollars from the AI side flow back further down the stack than they currently do. Third, the attribution layer — the link from a rewrite back to the originating reporter — becomes the actual load-bearing piece of the post-wire information ecosystem, and the legal fights now playing out in the Southern District of New York are about who controls and enforces it.

The wire was, for most of its history, an elegant solution to a brutal problem. The post-wire era has not yet found an elegant solution to the same problem, and there is no guarantee it will. The systems being built right now — the licensing regimes, the search-engine quality signals, the per-site rewrite engines, the lawsuit settlements — will collectively decide whether the bureau in Kyiv stays funded or whether the identical paragraph is replaced by a thousand differentiated paragraphs all pointing at nothing.

That is the structural editorial question the post-wire era is sitting on top of. It does not have a single verdict, and anyone offering one is selling something.

Sources & references

· Read the World, Then Publish: Inside the DojoClaw + Stenvrik Loop — Thorsten Meyer · operator-side account of the per-site rewrite engine referenced here · thorstenmeyerai.com · 78,000+ articles, 361M+ words, 450+ WordPress magazines, 3,500+ Stenvrik syndications, average fan-out 4.2 sites

· Associated Press — Wikipedia · founding 1846, revenue mix shifts, Gannett departure March 2024, $100M nonprofit launch June 2024 · en.wikipedia.org/wiki/Associated_Press · US newspaper revenue share: 30% (2007) → 10% (2024); 235 bureaus / 94 countries; 128M monthly visits

· Reuters — Wikipedia · founding 1851, cartel agreement 1865, current operations · en.wikipedia.org/wiki/Reuters · 2,500 journalists / 200 locations; 105M monthly readers

· News agency — Wikipedia · Havas/Reuters/Wolff 1865 cartel, 1880s subscription economics, Big Three share of global foreign news · en.wikipedia.org/wiki/News_agency · 90%+ of foreign news in world’s papers from AP/Reuters/AFP

· Wall Street declares war on the Associated Press — Matt Pearce (Substack) · Reuters–Gannett deal January 2025, structural analysis of cooperative vs. financialised wire competition · mattdpearce.substack.com

· A timeline of the major deals between publishers and AI tech companies in 2025 — Digiday · OpenAI/Google/Meta/Mistral/Apple deals across Axios, AP, Guardian, AFP, Schibsted, Hearst, News Corp · digiday.com

· The Billion-Dollar Bailout: Publisher AI Licensing Deal Tracker — PR News (Everything-PR) · running tracker with deal values, cumulative ~$2B publisher-side · everything-pr.com/ai-licensing-tracker · News Corp–OpenAI $250M/5yr; News Corp–Meta $150M/3yr; Reddit–Google $60M/yr; Axel Springer–OpenAI ~$13M/yr; FT–OpenAI $5–10M/yr

· OpenAI Must Turn Over 20 Million ChatGPT Logs, Judge Affirms — Bloomberg Law, January 5, 2026 · Judge Stein affirms Magistrate Wang’s order in In re OpenAI Copyright Infringement Litigation, 16 consolidated cases · news.bloomberglaw.com · summary judgement schedule April 2, 2026

· The New York Times sues Perplexity, alleging copyright infringement — CNBC, December 5, 2025 · “skip the click” tagline, RAG-output substitution claim, 175,000 scraping attempts August 2025 · cnbc.com

· News Outlets’ Perplexity AI Suits Strike at Existential Threat — Bloomberg Law, February 9, 2026 · structural analysis of substitution vs. training-data claims; TollBit 96% referral-traffic finding · news.bloomberglaw.com

· AI Lawsuit Tracker · 166 active AI copyright cases as of April 2026 · ailawsuittracker.com · Bartz v. Anthropic settlement $1.5B (largest in US copyright history); GEMA v. OpenAI Munich ruling Nov 2025; Getty v. Stability AI UK High Court Nov 2025

· Google’s December 2025 Helpful Content Update — Dev.to / Synergist Digital Media · “competent but generic content” target, 40–60% traffic-loss reports · dev.to

· Google AI Content Penalties: February 2026 Truth — Maintouch · 17% of top-20 results AI-generated as of September 2025, scaled-content-abuse manual actions June 2025 · maintouch.com

· World Press Trends Outlook 2024–2025: Revenue Trends — WAN-IFRA via Damian Radcliffe (Medium) · print revenue below 50% of total for the first time, down 12% in two years · medium.com/damian-radcliffe

· Exclusive: AP strikes news-sharing and tech deal with OpenAI — Axios, July 13, 2023 · AP archive licensing back to 1985, first major news-AI deal · axios.com

· News Corp, OpenAI Sign $250 Million Journalism Content Licensing Deal — VCPost / WSJ reporting, May 22, 2024 · five-year deal, WSJ/NY Post/MarketWatch/Barron’s included, Factiva and HarperCollins excluded · vcpost.com

About the author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine described in the operator-side companion piece below. More at ThorstenMeyerAI.com.

Related reading

· Read the World, Then Publish: Inside the DojoClaw + Stenvrik Loop — the operator-side technical account of the per-site rewrite engine referenced throughout this essay. Top-N matcher with a confidence floor, Readability fail-soft, attribution preservation, status truth-source rule. Read →

· DojoClaw — the editorial engine itself. dojoclaw.com

· Stenvrik — the upstream news globe. 227 RSS sources, 24 topics, 49 cities, refreshed every ten minutes. stenvrik.com

· StrongMocha News Group — the publisher portfolio that the post-wire economics described here are actually running through. strongmocha.com

— Thorsten Meyer · ThorstenMeyerAI.com · 2026-05-15