By Thorsten Meyer — May 2026

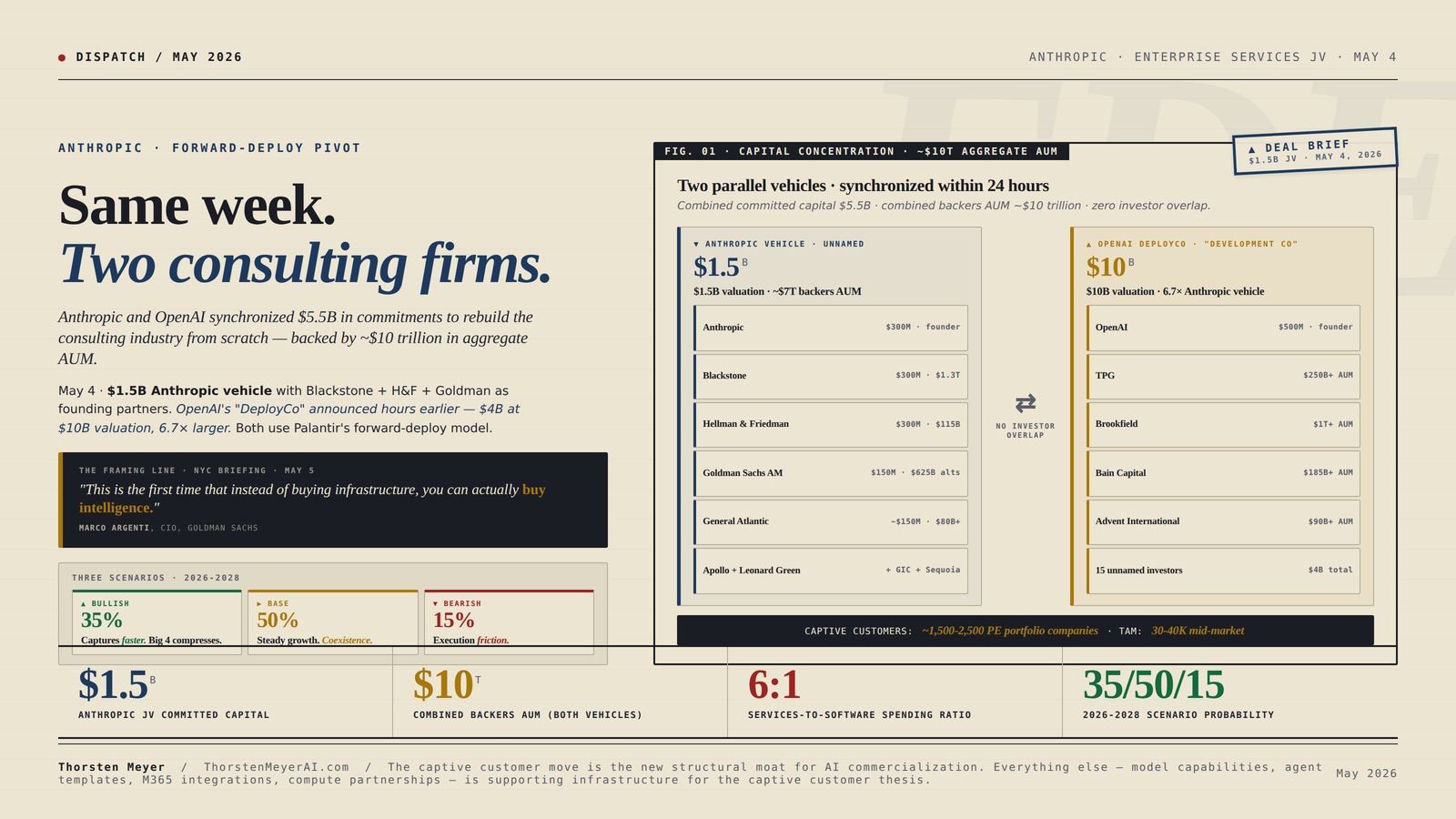

May 4, 2026 — Anthropic, Blackstone, Hellman & Friedman, and Goldman Sachs announced the formation of a new $1.5 billion AI-native enterprise services company, backed by a consortium of the world’s largest alternative asset managers — General Atlantic, Leonard Green, Apollo Global Management, GIC, Sequoia Capital. Anthropic, Blackstone, and H&F each commit approximately $300 million; Goldman Sachs and General Atlantic approximately $150 million each; the remaining backers round out the $1.5 billion capital base. The entity is currently unnamed. It will embed Anthropic’s Applied AI engineers alongside the firm’s own engineering team into mid-sized companies — community banks, regional health systems, mid-market manufacturers, professional services — to redesign workflows around Claude. The structural reference point is Palantir’s forward-deployed engineering model. The competitive context is that OpenAI announced a near-identical entity hours earlier — “The Development Company” (DeployCo) backed by TPG, Bain Capital, Advent International, Brookfield, Goanna Capital at $4 billion in PE commitments and a $10 billion valuation, 6.7 times larger than Anthropic’s vehicle on day one.

The single-week chronology resolves the strategic intent. May 4 (Monday): the enterprise services JV announcement. May 6 (Wednesday): the SpaceX Colossus 1 compute deal that closes Anthropic’s ten-month customer-experience reckoning. May 7 (Thursday): the ten finance agent templates plus Microsoft 365 add-ins plus eight new connectors plus Moody’s MCP app. Three coordinated launches across three trading days. The pattern is not coincidental — it’s IPO positioning. Anthropic is reportedly in final stages of a $40-50 billion funding round at a $900 billion valuation that would eclipse OpenAI’s most recent $852 billion mark, with a May board meeting determining the path forward and a potential public listing as early as October 2026. The three announcements form a narrative that an IPO investor reads as a coherent story: distribution capacity (May 4) plus compute capacity (May 6) plus vertical productization (May 7) equals durable enterprise revenue trajectory.

The deeper structural read is that the consulting industry is being attacked at its foundation. Sequoia partner Julien Bek argued in April: “the world’s next great company won’t sell software at all, but outcomes — legal services, financial analysis, insurance processing delivered by AI.” Fortune characterized the JV as “Anthropic takes shot at consulting industry.” Goldman’s Marc Nachmann framed it as “democratizing access to forward-deployed engineers.” The economic insight underneath is brutal in its simplicity. For every $1 companies spend on software, they spend approximately $6 on services. That ratio defines the global consulting market — McKinsey, BCG, Bain at the strategy tier; Accenture, Deloitte, PwC, KPMG, EY at the systems integration tier; thousands of regional and specialty consultancies below. Total global IT services market: approximately $1.4 trillion annually. AI-native firms are now positioning to redirect a meaningful share of that flow from human consultants to AI-augmented forward-deploy engineering. The mid-market segment — too small for the Big 4 to serve economically, too sophisticated for self-service software — is the structural opening that the JV targets first.

The competitive significance for the Big 4 SIs runs deeper than the headlines suggest. The Claude Partner Network — Accenture, Deloitte, PwC, plus dozens of regional integrators — has been Anthropic’s primary enterprise distribution channel for the largest Fortune 500 deployments. That relationship continues, per Anthropic’s announcement language. But the new JV is an equity-aligned entity, not a revenue-share partner. Anthropic has direct ownership in this venture in a way it does not in any Big 4 SI relationship. The implicit message: as enterprise demand outpaces the Big 4’s delivery capacity, Anthropic now has a vertically-integrated mid-market alternative that captures more of the value chain. The Big 4 retain the largest Fortune 500 transformations. The new JV captures the mid-market PE-portfolio deployments. Both grow, but the strategic positioning is qualitatively different.

This dispatch is the structural read on what the May 4 enterprise services announcement actually means. The PE-roll-up logic that makes the JV economically inevitable. The structural attack on the consulting industry’s $6-services-for-every-$1-software ratio. The OpenAI DeployCo competitive parallel and what 6.7× scale gap signals. The Big 4 SI repositioning that follows in the next 12-24 months. The Anthropic IPO valuation case implications. The connections to other dispatches in this series.

Same week.

Two consulting firms.

Anthropic and OpenAI synchronized $5.5B in commitments to rebuild the consulting industry from scratch — backed by ~$10 trillion in aggregate AUM.

May 4 · $1.5B Anthropic vehicle with Blackstone + Hellman & Friedman + Goldman Sachs as founding partners. OpenAI’s “DeployCo” announced hours earlier — $4B at $10B valuation, 6.7× larger. Both use Palantir’s forward-deployed engineering model. Captive customer pipeline through PE portfolio ownership = unprecedented enterprise software moat.

Two ventures. One opportunity.

The most concentrated assembly of private capital ever announced for AI services. Captive customer pipeline through PE portfolio ownership is the structural moat — when the PE firm owns both the services firm AND the customer, traditional buyer-seller dynamics break down.

- Anthropic$300M · founder

- Blackstone$300M · $1.3T AUM

- Hellman & Friedman$300M · $115B AUM

- Goldman Sachs AM$150M · $625B alts

- General Atlantic~$150M · $80B+

- Apollo + Leonard Green+ GIC + Sequoia

overlap

- OpenAI$500M · founder

- TPG$250B+ AUM

- Brookfield$1T+ AUM

- Bain Capital$185B+ AUM

- Advent International$90B+ AUM

- 15 unnamed investors$4B total commits

The Six Digital Perspectives: A Practical Guide to Digital Transformation, AI-Ready Operating Models, and High-Performance Organizations (The 6xD)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four days. Four layers.

Each layer compounds the others. Compute enables deployment scale. Models provide capability. Templates productize workflows. Services firm provides delivery. PE pipeline provides customers. The blitz is coordinated IPO positioning ahead of Q4 2026.

AI consulting tools for mid-sized companies

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five tiers. Five trajectories.

The disruption is uneven by tier. Indian IT faces structural threat (cost-arbitrage labor model obsolescence). Big Four maintain Fortune 500 dominance. Strategy consultancies durable on judgment work. Palantir’s FDE model gets validation premium.

AI Engineering Starter Kit: The Practical Guide to Build, Train, and Deploy Real AI Applications with LLMs, MLOps, and Cutting-Edge Tools – Step-by-Step Projects for Aspiring AI Engineers.

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios. One restructuring.

Whether the captive customer model scales as projected or faces execution constraints. Both vehicles likely achieve material scale rather than one collapsing — the structural setup is overwhelming.

- 1,500-2,500 deploymentsBy end-2027 across portfolio.

- 3-6 month deliveryVs 12-18 months traditional.

- Big 4 mid-market compressesIndian IT down 30-40%.

- JV revenue $1-2B by 2028Material IPO contribution.

- Outcome: October 2026 IPO at $900B+. JV is bull case.

- 800-1,500 deploymentsBy end-2027.

- Bifurcated marketFDE entities + traditional SI both grow.

- Big 4 deepen alt-AI partnershipsAccenture+OpenAI; Deloitte+Google.

- JV revenue $400-800M by 2028Supporting narrative.

- Outcome: IPO proceeds. JV is one of several threads.

- Engineering scaling hardFDE talent the binding constraint.

- PE governance frictionMultiple sponsors create overhead.

- Big 4 defends aggressivelyPricing competition compresses.

- JV revenue $100-300M by 2028Underperforms projections.

- Outcome: IPO valuation hit. Potential 2027 delay.

This is the most aggressive enterprise distribution play in tech history, executed in synchronized fashion within hours of each other, backed by approximately $10 trillion in aggregate AUM. The captive customer move is the new structural moat for AI commercialization. Everything else is supporting infrastructure.

Workflow Automation with Microsoft Power Automate: Use business process automation to achieve digital transformation with minimal code

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Track 90-180 day customer traction.

Anthropic IPO valuation case strengthens materially. The captive distribution channel adds structural multi-year revenue visibility worth plausibly $500M-$2B incremental ARR by Q4 2027. Q4 2026 IPO probability rises from ~50% pre-announcement to ~65-70% post-announcement. Verify execution before drawing valuation conclusions.

Form competing vehicles or cede captive economics.

KKR, Carlyle, Vista, Thoma Bravo, Silver Lake, Warburg Pincus face strategic choice. Form parallel vehicles with smaller AI labs (Mistral, Cohere, xAI) or with Microsoft/Google/Meta as model partners. Or accept structural disadvantage. The captive customer model is the new value-creation default.

Equity-aligned partnerships and vertical specialization.

Big 4 — deepen alt-AI partnerships (Accenture-OpenAI, Deloitte-Google likely). Indian IT — pivot to AI-native delivery aggressively or face 25-40% market cap compression. Mid-market integrators (EPAM, Genpact) face direct competition; vertical specialization in regulated industries (defense, government, large healthcare) is the defensible position.

PE-owned companies face accelerated AI deployment.

If your company is owned by Blackstone, H&F, Apollo, GA, Leonard Green, GIC, Sequoia — direct JV engagement arriving 12-24 months. If OpenAI DeployCo’s PE backers — same. Reskill toward judgment-intensive roles. The Atlassian template applies — workforce composition reshape, not just headcount cut. 15-25% restructuring across PE-portfolio companies over 2026-2030.

Executive Summary · The JV Architecture in One Table

| Element | Data point | Source |

|---|---|---|

| JV total committed capital | ~$1.5 billion | WSJ / Anthropic disclosure |

| JV valuation | $1.5 billion (initial) | WSJ |

| Anthropic commitment | ~$300 million | WSJ |

| Blackstone commitment | ~$300 million | WSJ |

| Hellman & Friedman commitment | ~$300 million | WSJ |

| Goldman Sachs commitment | ~$150 million | WSJ / FT |

| General Atlantic commitment | ~$150 million | WSJ / FT |

| Other backers | Apollo, Leonard Green, GIC, Sequoia | Anthropic |

| JV name | Not yet announced | — |

| Target market | Mid-sized PE-portfolio companies | Anthropic |

| Target sectors | Healthcare, manufacturing, financial services, retail, real estate | CNBC |

| Embedded talent model | Anthropic Applied AI engineers + JV engineers | Anthropic |

| Structural reference | Palantir forward-deploy model | Fortune |

| Big 4 SI relationship | Continues; JV joins Claude Partner Network | Anthropic |

| OpenAI parallel · DeployCo | $10 billion valuation · $4B PE commits + $500M OpenAI | TechCrunch / Bloomberg |

| OpenAI DeployCo backers | TPG, Bain Capital, Advent, Brookfield, Goanna | TechCrunch |

| Anthropic ARR run rate | $9B (end-2025) → $30B+ (late March 2026) | Anthropic |

| Anthropic funding round target | $40-50B at $900B valuation | TechCrunch / FT |

| Anthropic IPO target | As early as October 2026 | Bloomberg |

| Software-to-services spending ratio | ~$1 software : $6 services | Industry standard |

| Global IT services market | ~$1.4 trillion annually | Industry data |

| Blackstone AUM | $1.3 trillion | Blackstone disclosure |

| Hellman & Friedman AUM | $115 billion | H&F disclosure |

| Goldman Sachs Alternatives AUM | $625 billion | Goldman disclosure |

The cumulative picture: the JV is a $1.5 billion vehicle at launch but has access to a customer pipeline of approximately 1,500-2,500 mid-market companies through the PE backers’ portfolio holdings combined. The OpenAI parallel at 6.7× the valuation signals that both frontier labs view forward-deployed engineering as the primary distribution model for the next phase of enterprise AI. The consulting industry’s structural moat is being challenged from two directions simultaneously.

1. The PE roll-up logic · why this was inevitable

The economic logic of the JV is structurally compelling once you understand the participating PE firms’ portfolio composition.

Blackstone alone owns approximately 250 portfolio companies across its private equity strategies. The portfolio spans healthcare services (Pelmorex, Hyperion Materials), industrial manufacturing (Pretium Packaging, Stavola), financial services (Lexicon, Refinitiv before its sale), professional services, and dozens more. Total Blackstone portfolio company revenue: approximately $250 billion annually. The mid-market subset of Blackstone holdings — companies between $100M and $5B in revenue, which is most of them — represents perhaps 200 companies. Each is a potential JV customer.

Hellman & Friedman has invested in over 100 companies since 1984 with $115 billion in AUM as of December 2025. H&F’s portfolio is concentrated in technology, financial services, healthcare, consumer services, retail, and information services — the same sectors the JV targets. Active H&F portfolio companies: approximately 30-40 at any given time, each with the strategic mandate from H&F to deploy AI for productivity gains.

Apollo Global Management holds approximately $750 billion in AUM and an investment portfolio spanning industrial (Yahoo, Vrio), consumer (Smart & Final, Cox Media), real estate, and credit-related businesses. Active Apollo portfolio companies: approximately 100-150.

General Atlantic, Leonard Green, GIC, Sequoia each contribute additional portfolio dimensions. The combined portfolio universe of the JV’s PE backers exceeds 1,500-2,500 mid-market companies. That is the JV’s initial total addressable customer base — companies whose owners have direct economic incentive to deploy Claude through this entity rather than alternatives.

The PE economic incentive is structurally important. PE firms generate returns through (a) financial engineering (leverage, debt repayment), (b) operational improvements (margin expansion, growth acceleration), and (c) multiple expansion at exit. Operational improvements has been the most contested return driver — McKinsey-BCG-Bain consultants have historically captured significant value here, with PE firms paying $50-200M annually in advisory fees to drive operational improvements across portfolios. AI-driven operational improvements that the JV delivers are economically captured by the PE firms themselves rather than paid out to external consultants. The capture-the-value logic alone makes the JV’s existence inevitable. Add the equity stake the PE firms hold in the JV itself, and the alignment compounds.

The deeper structural insight. PE firms have been building “operational excellence” practices — Bain-trained partners on staff, dedicated portfolio operations groups — for fifteen years. The economic logic was always to capture operational value internally rather than pay it out to consultants. AI-native forward-deploy engineering is the next iteration of that capture. Instead of hiring 50 ex-Bain partners to optimize portfolio company operations, the PE firm becomes a co-owner of an AI services entity that does the optimization at scale across portfolio companies. The marginal cost per deployment drops materially. The marginal value captured rises materially.

The JV is not an experiment for these PE firms. It’s a structural extension of the operational excellence playbook they’ve been running for a decade and a half. The novelty is the AI substrate.

2. The consulting industry attack · $1.4 trillion in cross-hairs

The Fortune framing — “Anthropic takes shot at consulting industry” — captures the essential strategic move but understates its scale. The global IT services and consulting market is approximately $1.4 trillion annually. The breakdown:

Strategy consulting tier (McKinsey, BCG, Bain, plus boutiques): ~$50-80 billion globally. Premium pricing, partner-led engagements, focused on senior leadership decision support. AI-resistant in the near term — strategic judgment under uncertainty doesn’t substitute easily — but increasingly threatened by AI-augmented research and analysis capabilities. McKinsey’s revenue grew approximately 20 percent in 2024-2025 partially due to “Generative AI advisory” services that are themselves vulnerable to disruption.

Systems integration tier (Accenture, Deloitte, PwC, KPMG, EY, IBM, plus regional players): ~$600-700 billion globally. Implementation work — ERP deployments, custom application development, integration projects, infrastructure modernization, and increasingly AI implementation. Accenture’s GenAI bookings reached approximately $5 billion in fiscal 2025; Deloitte’s GenAI practice grew similarly. These firms are the primary delivery channel for enterprise AI today.

Specialized and regional consultancies: ~$400 billion globally. Industry-specific firms (life sciences, financial services, manufacturing), regional integrators, IT staffing firms. The most fragmented tier, with thousands of competitors.

Internal IT services (in-house consulting equivalents): ~$200-300 billion. Corporate IT departments, internal transformation teams, captive services.

The JV’s mid-market PE-portfolio focus targets the segment underserved by the strategy tier (too expensive) and underserved by the SI tier (mid-market economics don’t justify the engagement size for Accenture/Deloitte/PwC) — but is currently served by smaller specialized firms and internal IT teams. The competitive entry point is the easiest part of the $1.4 trillion market to attack. Once the JV proves the model, expansion into adjacent tiers follows naturally.

The structural moat the JV attacks. Consulting firms’ value is in (a) talent — partners with deep expertise, (b) methodology — repeatable frameworks for transformation work, (c) trust — long-term client relationships, (d) network — cross-industry knowledge transfer. AI-native forward-deploy firms attack each:

- Talent: instead of training Bain-grade consultants over 5-7 years, the JV combines Anthropic’s Applied AI engineers (who have direct access to Claude’s capabilities) with the JV’s own implementation engineers (hired from the SI tier). The talent equation shifts from “rare expensive partners” to “engineers + Claude-enhanced tooling.”

- Methodology: traditional consulting methodologies are codified in slide decks, training programs, and proprietary frameworks. AI-native methodologies are codified in (a) Claude prompt patterns, (b) Skills (Anthropic’s productized expertise framework), (c) reusable agent templates. The methodology iteration cycle compresses from years to months.

- Trust: the JV inherits trust from Blackstone, H&F, Goldman Sachs by association. PE-owned portfolio companies trust their owners’ recommendations. The trust transfer is faster than building independent reputation.

- Network: PE-portfolio knowledge transfer happens within Blackstone’s portfolio operations team. The JV captures cross-industry insights through deployments across its 1,500-2,500-company target universe. The network density compounds faster than traditional consulting.

The challenge is execution at scale. Consulting firms have built operational machinery over decades. The JV must build equivalent machinery in 24-36 months while delivering quality at speed. The bear case for the JV is execution friction; the bull case is that AI-native delivery economics enable faster scaling than traditional consulting.

3. The OpenAI parallel · DeployCo and 6.7× scale signal

The same week that Anthropic announced its enterprise services JV, OpenAI announced a structurally near-identical entity. The naming and timing together reveal something important.

OpenAI’s “The Development Company” / DeployCo:

- $10 billion valuation

- OpenAI commits $500 million (with option for additional $1 billion)

- TPG, Bain Capital, Advent International, Brookfield, Goanna Capital commit ~$4 billion combined

- Total committed capital: ~$4.5-5 billion

- Same forward-deploy model, same PE-portfolio focus

- Reported by Bloomberg hours before Anthropic’s announcement

The parallel structure reveals that forward-deployed engineering is the new structural model for enterprise AI distribution. Both frontier labs reached the same conclusion simultaneously: enterprise demand outpaces traditional SI delivery capacity; PE-portfolio deployment requires equity-aligned partners; the mid-market opportunity is too large to leave to the existing SI ecosystem.

The 6.7× valuation difference deserves direct examination. Why is OpenAI’s vehicle at $10B versus Anthropic’s at $1.5B?

Several plausible explanations:

(1) Larger initial capital base — OpenAI’s $4.5-5B in commits versus Anthropic’s $1.5B reflects different fundraising scales. TPG and Bain alone manage approximately $250B and $185B respectively. The OpenAI consortium chose larger total capital.

(2) Different equity structure — The valuation may reflect different equity allocations between AI lab and PE backers. OpenAI’s $500M equity might represent ~5% of the entity (implying $10B valuation); Anthropic’s $300M might represent 20% of its entity (implying $1.5B valuation). The two valuations are not comparable on equivalent metrics without more disclosure.

(3) Brand premium — OpenAI’s consumer brand recognition and ChatGPT-driven ARR are larger than Anthropic’s. The valuation premium reflects market perception of OpenAI’s broader market position.

(4) Strategic intent difference — Anthropic may have priced its JV for rapid deployment and aggressive customer acquisition; OpenAI may have priced its entity for IPO-narrative purposes given its earlier IPO trajectory.

(5) Capital efficiency framing — Anthropic’s $1.5B is more capital-efficient per dollar of customer reach if both target similar PE-portfolio universes. The JV produces more leverage per invested dollar.

The competitive read: both vehicles will deploy through 2026-2028 across overlapping mid-market segments. The PE backers are partially overlapping (TPG and Bain on the OpenAI side; Apollo and General Atlantic on the Anthropic side). Some PE-portfolio companies will end up running both Claude and OpenAI deployments through both JVs as a hedge. Most will choose one. The market structure that emerges is bifurcated forward-deploy oligopoly: two AI lab-backed forward-deploy entities, plus the established Big 4 SI ecosystem, plus thousands of smaller consultancies, all competing for share of the $1.4 trillion services market.

The simultaneous announcement is itself the most important signal. It establishes the model as the new structural standard rather than as Anthropic-specific innovation. Other AI labs (Google’s Gemini Enterprise, Meta’s Muse, Mistral, Aleph Alpha) face pressure to develop similar PE-aligned forward-deploy vehicles. The model becomes the table stakes for serious enterprise deployment. Within 12-18 months, expect Google to announce a Gemini-aligned forward-deploy JV — the strategic logic compels it.

4. The Big 4 SI repositioning · what comes next

The implications for Accenture, Deloitte, PwC, KPMG, EY through 2026-2028 are structurally significant but more nuanced than headline framings suggest.

The “preferred partner” status is preserved. Anthropic explicitly continues investing in the Claude Partner Network — Accenture, Deloitte, PwC remain primary delivery partners for largest Fortune 500 deployments. The JV is positioned as additive, not replacement. Krishna Rao’s framing: “additional operating capability to the ecosystem.”

But the equity alignment is fundamentally different. Anthropic has direct economic ownership in the JV. The JV’s success directly contributes to Anthropic’s revenue and valuation. The Big 4’s success contributes to Anthropic indirectly through revenue-share arrangements. In any conflict between JV deployment and Big 4 deployment for the same customer, Anthropic has structural reason to favor the JV. The Big 4 SIs read this immediately. Their competitive response unfolds across three vectors:

Vector 1 · Equity-aligned partnerships with other AI labs. Accenture’s existing OpenAI partnership becomes more strategically important — Accenture is likely to deepen the OpenAI alignment to balance Anthropic’s JV-aligned positioning. Deloitte explores similar moves with Google’s Gemini, Meta’s Muse, or specialized AI labs. Within 12-18 months, the Big 4 SIs are likely to have deeper equity-aligned relationships with multiple AI labs, with each lab having both a JV-aligned partner and a Big 4-aligned partner.

Vector 2 · Mid-market push. Accenture, Deloitte have been gradually moving down-market in their AI practices. The JV announcement accelerates this. The Big 4 cannot cede the mid-market entirely — even if economics are challenging at the lower end, market share matters for AI practice positioning. Expect more aggressive mid-market service offerings from the Big 4 through 2026-2027, possibly through dedicated mid-market practice units with adjusted economics.

Vector 3 · Vertical specialization. The Big 4 retain durable advantage in industries where deep regulatory and operational expertise matters — defense, government, utilities, large healthcare systems, complex financial services. The JV’s PE-portfolio focus is specifically NOT these segments. Big 4 vertical specialization deepens as their differentiation strategy.

The talent acquisition battle. The most acute Big 4 risk is talent loss. The JV’s forward-deploy engineers are exactly the profile the Big 4 SIs need for their own AI practices. If the JV pays better, has more equity upside, and offers more interesting work (because it’s at the frontier of AI deployment), the talent migrates. Accenture’s GenAI practice has reportedly hired 30,000+ practitioners; the JV’s hiring pull on this talent base is a genuine risk to Big 4 capacity.

The medium-term outcome. By 2027-2028, the enterprise AI services market structure looks like: (a) two AI-lab-backed forward-deploy JVs (Anthropic’s plus OpenAI’s plus possibly Google’s), targeting mid-market PE portfolios primarily; (b) Big 4 SIs targeting Fortune 500 transformations with multi-lab partnerships; (c) specialized vertical consultancies (life sciences, defense, government); (d) regional and boutique consultancies fragmenting the long tail. The Big 4 don’t lose market share dramatically but their growth rate moderates and their AI-practice premium pricing compresses.

5. The Anthropic IPO valuation case · why three days matter

The May 4-6-7 cluster of announcements is structurally important for the Anthropic IPO valuation framework. Each addresses a specific concern that would have appeared as a forward-risk factor in early IPO disclosures.

May 4 · Distribution capacity. The enterprise services JV addresses the question: “Can Anthropic scale enterprise revenue beyond Big 4 SI capacity?” Answer: yes, through equity-aligned forward-deploy entity targeting 1,500-2,500 mid-market PE-portfolio companies.

May 6 · Compute capacity. The SpaceX Colossus 1 deal addresses: “Can Anthropic serve growing demand without rate-limit-driven customer experience degradation?” Answer: yes, through SpaceX 220K+ GPUs plus Amazon 5GW + Google 5GW + Microsoft $30B Azure + Fluidstack $50B = the second-largest publicly-disclosed compute portfolio of any frontier lab.

May 7 · Vertical productization. The ten finance agent templates plus Microsoft 365 add-ins plus eight new connectors plus Moody’s MCP app addresses: “Does Anthropic have proven enterprise revenue traction in the highest-value vertical?” Answer: yes, with finance vertical productization that potentially adds $3-5B incremental ARR over 2026-2028.

Three concerns. Three answers. Three days. The coordination is unmistakable. Anthropic is presenting a complete IPO narrative through the three-day announcement cluster. The May board meeting that follows determines the path forward — whether to accept the $50B funding round at $900B valuation as a private capital raise, or to proceed directly to public listing.

The valuation context. Anthropic’s ARR went from $9B end-2025 to $30B+ by late March 2026 — 3.3× growth in three months. At 30× ARR multiple (consistent with frontier AI lab valuations), $30B ARR supports $900B valuation. The multiple is rich but defensible given (a) the enterprise traction visible in the May 4-6-7 announcements, (b) the durable competitive position relative to OpenAI on coding (Claude Code) and structured analysis, (c) the Constitutional AI / RSP positioning that aligns with regulatory environment, (d) the multi-vendor compute portfolio that de-risks the binding constraint.

The OpenAI competitive context. OpenAI’s $852B most recent valuation against Anthropic’s $900B target shows the labs are in the same valuation tier. OpenAI’s consumer revenue (ChatGPT subscriptions) is larger; Anthropic’s enterprise penetration and developer tools (Claude Code) generate higher per-customer value. Both labs are simultaneously preparing IPOs. The race to public market is not winner-take-all — both will list, both will trade. But the order and timing matters for narrative purposes. Anthropic listing in October 2026 (before OpenAI) would be a meaningful narrative advantage; OpenAI listing first cedes some narrative value.

6. The connections to other dispatches

The May 4 enterprise services JV connects to multiple structural threads from this dispatch series.

Connection 1 · Anthropic IPO disclosure framework. The dispatch covered the forward-risk factors that would appear in an Anthropic S-1. Distribution capacity was prominent. The JV materially de-risks that factor — Anthropic now has equity-aligned mid-market distribution alongside Big 4 SI partnership. The IPO valuation case strengthens correspondingly.

Connection 2 · Compute reckoning (May 6). The dispatch covered the SpaceX deal closing the ten-month customer experience reckoning. The JV announcement on May 4 PRECEDES the compute reckoning. The chronology reveals the strategic ordering: announce distribution capacity first, then announce compute capacity that enables the distribution. Reverse chronology would have raised the question “can Anthropic actually deliver?” The May 4 → May 6 sequence answers that question affirmatively.

Connection 3 · Finance agents impact (May 7). The dispatch covered the finance vertical productization. Goldman Sachs is a co-founder of the May 4 JV AND Goldman experts QC’d the Vals AI Finance Agent benchmark. Goldman’s positioning is structurally important: it’s a JV co-founder, it’s a benchmark validator, it’s a financial services vertical customer, and it’s an underwriter for the eventual Anthropic IPO. Goldman is positioned to capture value through every dimension of the Anthropic enterprise rollout simultaneously.

Connection 4 · Labor displacement Q1-Q2 2026 data. The dispatch covered the cohort displacement pattern in knowledge work. The JV is the structural mechanism by which AI productivity translates to mid-market labor displacement. Wall Street displacement runs through Big 4 SIs to Fortune 500 enterprises; mid-market displacement runs through this JV to PE-portfolio companies. Two distribution channels for the same underlying productivity-translation phenomenon.

Connection 5 · The bubble question disentangled. The dispatch flagged “real productivity gains in deployed contexts” as one of the durable-value categories. The JV is direct evidence — a $1.5B vehicle exists specifically because the productivity gains in deployed AI are real and economically valuable. Bubble-versus-durable-value differentiation gets clearer through this announcement.

Connection 6 · Hyperscaler capex thesis. The dispatch covered the demand-pull side of the $725B 2026 hyperscaler capex commitment. The JV’s forward-deploy model accelerates AI deployment timelines, which compresses the time horizon over which capex demand materializes. The capex demand-pull validation thesis gains support.

Connection 7 · Google I/O 2026 preview. The dispatch covered the May 19-20 I/O event. The JV announcement creates competitive pressure for Google to announce a Gemini-aligned forward-deploy entity — possibly at I/O, possibly at Google Cloud Next, possibly through 2026 standalone announcements. The forward-deploy model becomes table stakes for serious enterprise AI; Google needs an answer.

Connection 8 · OpenAI competitive context. OpenAI’s parallel DeployCo announcement is the most important competitive context. The two AI labs converging on identical distribution architecture simultaneously establishes the model as industry standard. The OpenAI 6.7× valuation gap creates IPO-narrative pressure on Anthropic to demonstrate equivalent or superior commercial validation.

The cumulative picture: the May 4 announcement is not an isolated business news event. It is the first move in a coordinated three-day strategic positioning that compounds with broader threads to support an aggressive IPO trajectory through Q3-Q4 2026.

7. Three scenarios for the JV’s 2026-2028 trajectory

The JV resolves into one of three structural patterns over the next 24-36 months.

Bullish scenario · 35% probability · “Captures the mid-market faster than expected.” The JV reaches 1,500-2,500 mid-market customer deployments by end-2027. PE backers actively direct portfolio companies into the JV’s pipeline. Forward-deploy economics demonstrate superior delivery speed (3-6 month deployments versus 12-18 months for traditional consulting). Big 4 SI mid-market practices compress accordingly. JV revenue reaches $1-2B annually by 2028. Anthropic captures meaningful share of the mid-market enterprise AI deployment market. The JV becomes a flagship case study for AI-native services. October 2026 IPO proceeds at $900B+ valuation; the JV’s traction is part of the bull case.

Base scenario · 50% probability · “Steady growth; coexistence with Big 4 SIs.” The JV reaches 800-1,500 customer deployments by end-2027. PE-portfolio deployments are significant but slower than aggressive projections. Big 4 SIs adapt successfully — Accenture deepens OpenAI partnership, Deloitte explores Google Gemini alignment. The mid-market AI services market bifurcates between AI-native forward-deploy entities and traditional SI providers, with both growing. JV revenue reaches $400-800M annually by 2028. October 2026 IPO proceeds with the JV as one of several supporting narrative threads but not the centerpiece.

Bearish scenario · 15% probability · “Execution friction; PE coordination challenges.” The JV faces difficulties scaling delivery at speed. Embedding Anthropic Applied AI engineers across 1,500+ companies is operationally complex. PE coordination across multiple sponsors creates governance friction. Big 4 SIs aggressively defend mid-market through pricing competition and accelerated AI capability development. The OpenAI DeployCo competes directly for the same PE-portfolio universe. JV revenue underperforms — reaches only $100-300M annually by 2028. Anthropic IPO valuation case takes hit; potential delay to 2027.

The 35/50/15 probability allocation reflects the specifics of the JV setup. Bullish probability is supported by: the strong PE backer alignment, Anthropic’s $30B ARR trajectory, the Goldman Sachs distribution power, the chronology that demonstrates Anthropic’s strategic execution. Bearish probability is supported by: execution risk in scaling forward-deploy models, OpenAI DeployCo competition, Big 4 SI counter-positioning, mid-market customer acquisition friction.

The base scenario reflects the most likely outcome — meaningful but not transformative growth, coexistence with Big 4 SIs, gradual mid-market penetration. The JV becomes a substantial business but not the dominant force in enterprise AI services through 2028. Beyond 2028, the model’s strategic positioning continues to compound.

8. The strategic implications by stakeholder

The May 4 enterprise services JV announcement has direct consequences for six distinct stakeholder groups.

For Anthropic IPO investors. The distribution capacity risk is materially de-risked through the JV. Combined with the May 6 compute reckoning and May 7 finance vertical productization, Anthropic’s enterprise revenue trajectory case strengthens substantially. Position based on demonstrated execution through Q3 2026 — the JV must show meaningful customer traction in its first 90-180 days for the IPO narrative to hold.

For PE firm investors and LPs. Blackstone, Apollo, KKR, Carlyle, and other major PE firms now have a precedent and structural model for capturing AI-driven operational value internally rather than paying it to external consultants. Expect within 12-18 months: KKR announces a parallel AI services JV with one of the AI labs; Carlyle explores similar moves; Bain Capital’s existing OpenAI DeployCo participation becomes a model for other PE firms. The PE-AI-lab forward-deploy entity becomes a standard component of PE portfolio operations.

For Big 4 SI competitors. Accenture, Deloitte, PwC, KPMG, EY face two parallel competitive pressures: (a) talent retention as JVs offer better compensation and equity upside for AI-native engineers; (b) market share defense in mid-market segment. The strategic response involves deeper equity-aligned partnerships with non-Anthropic AI labs (OpenAI for Accenture; Google for others) and aggressive vertical specialization. Watch for Big 4 announcements of dedicated mid-market AI practice units through 2026-2027.

For mid-market PE-portfolio companies. Companies owned by Blackstone, H&F, Apollo, General Atlantic, Leonard Green, GIC, Sequoia portfolio firms should expect direct engagement from the JV through 2026-2027. PE firm influence over portfolio decisions makes JV deployment near-mandatory in many cases. Mid-market companies NOT in the PE-portfolio universe face widening competitive disadvantage if their PE-owned competitors deploy AI faster through the JV than non-PE-owned firms can deploy through traditional channels.

For consulting industry talent. The forward-deploy engineering profile is the durable career bet. Combine technical depth (engineering, AI/ML capability, software development) with domain expertise (specific industry knowledge). Avoid the “generalist consultant” career path that has been the traditional Big 4 model — that path faces structural pressure through 2026-2028. Junior consulting hires should be very selective — the bottom-quartile consulting jobs face acute displacement risk.

For policymakers and regulators. The JV structure raises questions about (a) competition in the AI services market — is the equity-alignment between AI labs and PE firms creating anticompetitive bundling? (b) regulatory oversight of AI deployments at PE-portfolio companies — who is responsible when JV-deployed AI fails in regulated industries? (c) data governance across the JV’s deployment portfolio — does PE-shared infrastructure create data-protection risks? Regulatory framework development through 2026-2028 needs to address these questions.

What to Do This Quarter (Through Q2-Q3 2026)

1. Anthropic IPO investors. Track JV customer traction in first 90-180 days as the leading indicator for IPO narrative validation. Three-day cluster of May 4-6-7 announcements forms a coherent story; verify execution before drawing conclusions.

2. PE-portfolio company executives. Expect direct JV engagement if your company is owned by Blackstone, H&F, Apollo, General Atlantic, Leonard Green, GIC, or Sequoia. Engage proactively rather than reactively — being early in the JV pipeline carries advantages over being late.

3. Big 4 SI strategists. Develop equity-aligned partnerships with non-Anthropic AI labs (OpenAI especially). Accelerate mid-market practice development. Consider acquiring boutique AI-native consultancies to build forward-deploy capability internally.

4. Consulting industry talent. Forward-deploy engineering roles are the durable career bet through 2026-2028. Combine technical depth with domain expertise. Avoid generalist consultant paths that face structural displacement pressure.

The Strategic Read

May 4, 2026 — Anthropic announced the formation of a $1.5 billion enterprise AI services company with Blackstone, Hellman & Friedman, and Goldman Sachs as founding partners, backed by General Atlantic, Leonard Green, Apollo, GIC, and Sequoia Capital. Anthropic, Blackstone, and H&F each commit ~$300M; Goldman and General Atlantic ~$150M each. The entity will embed Anthropic Applied AI engineers alongside the firm’s own engineers into mid-sized companies — community banks, regional health systems, mid-market manufacturers. Structural reference: Palantir’s forward-deploy model. Hours earlier, OpenAI announced an identical-architecture entity called DeployCo / “The Development Company” backed by TPG, Bain, Advent, Brookfield, Goanna at $4B in PE commitments and a $10B valuation — 6.7× larger than Anthropic’s vehicle on day one.

The single-week chronology resolves the strategic intent. May 4: distribution capacity. May 6: SpaceX compute deal closing the ten-month customer experience reckoning. May 7: ten finance agent templates plus Microsoft 365 add-ins plus eight connectors plus Moody’s MCP app. Three coordinated launches across three trading days. The pattern is IPO positioning. Anthropic is in final stages of a $40-50B funding round at a $900B valuation — eclipsing OpenAI’s $852B mark. ARR went from $9B end-2025 to $30B+ late March 2026 (3.3× in three months). May board meeting determines the path forward. October 2026 potential IPO. The three-day announcement cluster presents a complete narrative an IPO investor reads as: distribution + compute + vertical productization = durable enterprise revenue trajectory.

The structural attack on the consulting industry is the deeper insight. For every $1 companies spend on software, they spend approximately $6 on services. Global IT services market: ~$1.4 trillion. Sequoia partner Julien Bek (April 2026): “the world’s next great company won’t sell software at all, but outcomes.” Fortune framing: “Anthropic takes shot at consulting industry.” Goldman’s Marc Nachmann: “democratize access to forward-deployed engineers.” The economic logic underneath: AI-native forward-deploy firms attack the consulting moat across talent (Claude-augmented engineers vs Bain partners), methodology (Skills/agent templates vs slide decks), trust (PE-backed positioning vs reputation building), and network (cross-portfolio knowledge vs single-firm experience). The mid-market segment — too small for the Big 4, too sophisticated for self-service software — is the structural opening.

The PE roll-up logic makes the JV economically inevitable. Blackstone alone owns ~250 portfolio companies. H&F has 100+ portfolio companies since founding. Apollo ~150. The combined PE-portfolio universe of the JV’s backers exceeds 1,500-2,500 mid-market companies — the JV’s initial total addressable customer base. PE firms have economic incentive to capture AI-driven operational value internally rather than pay it out to McKinsey-BCG-Bain or Big 4 SIs. The JV structure aligns PE economic incentive (capture operational value) with Anthropic distribution incentive (scale enterprise revenue) with engineering talent incentive (work at frontier of AI deployment with equity upside). Three aligned incentives, one structural model.

The OpenAI parallel at 6.7× valuation is the most important competitive signal. Both AI labs converged on identical distribution architecture simultaneously — establishing forward-deploy as the new structural standard rather than as Anthropic-specific innovation. Within 12-18 months, expect Google to announce a Gemini-aligned forward-deploy entity. The model becomes table stakes for serious enterprise AI distribution. The market structure that emerges is bifurcated forward-deploy oligopoly: two (eventually three) AI-lab-backed forward-deploy entities, plus established Big 4 SI ecosystem, plus thousands of smaller consultancies. The Big 4 don’t lose dramatically but their growth rate moderates and their AI-practice premium pricing compresses.

The Big 4 SI competitive response unfolds across three vectors. Vector 1: equity-aligned partnerships with other AI labs (Accenture deepens OpenAI; Deloitte explores Google Gemini). Vector 2: mid-market push with adjusted economics (dedicated mid-market practice units). Vector 3: vertical specialization in regulated industries where the JV’s PE-portfolio focus doesn’t reach (defense, government, large healthcare systems, complex financial services). The most acute Big 4 risk is talent loss — JV forward-deploy engineers are exactly the profile Big 4 AI practices need. Talent migration through 2026-2028 affects Big 4 capacity.

Three scenarios resolve through 2026-2028. Bullish (35%): JV reaches 1,500-2,500 customers by end-2027; revenue $1-2B by 2028; flagship case study for AI-native services; IPO at $900B+ valuation proceeds October 2026. Base (50%): JV reaches 800-1,500 customers; revenue $400-800M by 2028; coexistence with Big 4 SIs; IPO proceeds with JV as supporting narrative. Bearish (15%): execution friction; PE coordination issues; OpenAI DeployCo competes directly; JV revenue underperforms at $100-300M; IPO valuation case takes hit; potential delay.

The connections to broader threads run deep. Direct support for Anthropic IPO disclosure framework — distribution capacity de-risked. Coordinates with compute reckoning — May 4 distribution announcement precedes May 6 compute capacity, demonstrating strategic execution. Direct alignment with finance agents impact — Goldman Sachs as JV co-founder + Vals benchmark validator + financial services customer + IPO underwriter, capturing value through every dimension simultaneously. Substantiates labor displacement Q1-Q2 dispatch — JV is the mid-market-deployment mechanism for productivity-translation phenomenon. Validates bubble question’s durable-value reading — $1.5B vehicle exists because productivity gains in deployed AI are real. Sets up Google I/O 2026 preview competitive context — Google needs a Gemini-aligned forward-deploy answer.

The strategic implications run by stakeholder. Anthropic IPO investors: track JV customer traction in first 90-180 days as leading indicator. PE-portfolio executives: expect direct engagement; engage proactively. Big 4 SI strategists: develop equity-aligned non-Anthropic partnerships; accelerate mid-market practice development. Consulting industry talent: forward-deploy engineering is the durable career bet. Policymakers: address competition, regulatory oversight, and data governance questions raised by JV structure.

The deeper signal: the consulting industry — McKinsey, BCG, Bain at the strategy tier; Accenture, Deloitte, PwC, KPMG, EY at the SI tier; thousands of regional and specialty firms below — has operated for sixty years on the assumption that human consultants are the irreducible substrate of enterprise transformation. The May 4 JV announcement, paired with OpenAI’s parallel DeployCo, signals that assumption is being structurally challenged. Forward-deploy engineering with AI-native delivery economics produces 3-6 month deployment cycles versus 12-18 months for traditional consulting. The talent equation shifts from “rare expensive partners” to “engineers + Claude-enhanced tooling.” The methodology iteration cycle compresses from years to months. The PE-aligned trust transfer happens faster than independent reputation building.

The honest assessment: the most likely scenario is the base case — meaningful but not transformative growth, coexistence with Big 4 SIs, gradual mid-market penetration, JV becomes substantial business but not dominant force through 2028. The bullish tail (35%) and bearish tail (15%) are meaningful but lower probability. The structural insight is that the May 4-6-7 three-day announcement cluster reveals coordinated strategic positioning for the Anthropic IPO. Whether the IPO proceeds in October 2026 at the targeted $900B valuation depends substantially on whether the May 4 JV demonstrates initial customer traction in its first 90-180 days. The execution test starts now.

The deepest signal: AI labs are becoming consulting firms. Anthropic and OpenAI both reached the same conclusion in the same week. The distribution model that defined enterprise software for thirty years — license sale + Big 4 SI implementation — is being replaced by AI-lab-backed forward-deploy entities with PE-portfolio customer pipelines and equity-aligned engineering talent. The $1.4 trillion consulting industry is being structurally challenged from a direction it didn’t anticipate. The next decade of enterprise AI deployment runs through these new entities, not through the consulting incumbents that have dominated the previous decade.

May 4, 2026 — Anthropic announces $1.5B enterprise AI services JV with Blackstone, Hellman & Friedman, Goldman Sachs (founding) plus General Atlantic, Apollo, Leonard Green, GIC, Sequoia (consortium). Anthropic + Blackstone + H&F each commit $300M; Goldman + General Atlantic $150M each. OpenAI announces parallel DeployCo at $10B valuation, 6.7× larger, hours earlier. Three-day cluster May 4 (distribution) + May 6 (compute) + May 7 (finance vertical) reveals coordinated IPO positioning. Anthropic targeting $40-50B funding at $900B valuation; ARR $9B → $30B+ in three months; potential October 2026 IPO. Forward-deploy model attacks $1.4T global consulting industry. PE-portfolio universe ~1,500-2,500 mid-market companies as JV TAM. Three scenarios with 35/50/15 probability allocation.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The Compute Reckoning · Anthropic SpaceX Deal

- The Finance Agents Impact · Orchestration Layer Move

- The Anthropic IPO Disclosure Document

- The Labor Displacement Q1-Q2 2026 Data

- The $725B Hyperscaler Capex Question

- The Bubble Question, Disentangled

- The Google I/O 2026 Preview

Sources

- Anthropic · Building a new enterprise AI services company with Blackstone, Hellman & Friedman, and Goldman Sachs · May 4, 2026 — primary announcement

- Blackstone press release · Anthropic Partners with Blackstone, Hellman & Friedman, and Goldman Sachs to Launch Enterprise AI Services Firm · May 4, 2026

- Wall Street Journal · $1.5B JV valuation; $300M each from Anthropic, Blackstone, H&F; $150M Goldman; $150M General Atlantic

- Financial Times · Blackstone, Goldman back Anthropic’s $1.5bn AI joint venture · May 4, 2026

- Fortune · Anthropic takes shot at consulting industry in joint venture with Wall Street giants · May 4, 2026 · “$6 services for every $1 software”

- CNBC · Anthropic teams with Goldman, Blackstone and others on $1.5 billion AI venture targeting PE-owned firms · May 4, 2026

- TechCrunch · Anthropic and OpenAI are both launching joint ventures for enterprise AI services · May 4, 2026

- Bloomberg · OpenAI “The Development Company” / DeployCo · $10B valuation · TPG, Bain, Advent, Brookfield, Goanna · $4B PE commits + $500M OpenAI

- Sequoia Capital · Julien Bek thesis · April 2026 · “world’s next great company won’t sell software at all, but outcomes”

- Anthropic ARR · $9B end-2025 → $30B+ late March 2026 (3.3× in three months)

- Anthropic funding round · $40-50B target at $900B valuation; eclipses OpenAI $852B

- Bloomberg · Anthropic IPO target · as early as October 2026

- Blackstone $1.3T AUM · Q1 2026 disclosure

- Hellman & Friedman $115B AUM · December 2025 · 100+ portfolio companies since 1984

- Goldman Sachs Alternatives $625B AUM · 30+ years of alternatives investing

- Apollo Global Management ~$750B AUM

- Krishna Rao (Anthropic CFO) · “Enterprise demand for Claude is significantly outpacing any single delivery model”

- Jon Gray (Blackstone President & COO) · “break down one of the most significant bottlenecks to enterprise AI adoption”

- Patrick Healy (H&F CEO) · “rare convergence: massive market need, unmatched AI technical capability, consortium with reach to scale fast”

- Marc Nachmann (Goldman Sachs Asset & Wealth Management) · “democratising access to forward-deployed engineers”

- Global IT services market · ~$1.4 trillion annually · industry data

- Software-to-services spending ratio · ~$1 software : $6 services · industry standard

- Palantir forward-deploy engineering model · structural reference for JV architecture

- Claude Partner Network · existing relationships with Accenture, Deloitte, PwC, KPMG, EY

- Accenture GenAI bookings · ~$5B fiscal 2025