By Thorsten Meyer — May 2026

April 19, 2026. Honor’s “Lightning” humanoid robot, built by the Honor / Monkey King team, won the Beijing E-Town Half-Marathon in 50 minutes 26 seconds — beating the standing human world record (57:31) by nearly 7 minutes. Fully autonomous, no teleoperation, navigating the course’s elevation changes and crowd pacing dynamics in real time. The result was less a marathon than a capability demonstration. Three days earlier, Tesla had confirmed Optimus Gen 3 production would begin at Fremont in late July or August. Five days before that, Figure AI demonstrated Figure 03 running 24/7 fully autonomous operations including overnight runs. Apptronik’s Apollo continues at Mercedes; Figure 02 supports 30,000+ vehicles at BMW Spartanburg. Unitree shipped 5,500+ humanoids in 2025 and is targeting 10,000-20,000 in 2026.

The cumulative narrative through Q1-Q2 2026: humanoid robotics is shipping. The honest picture is more nuanced. Production-cost targets are converging but not yet achieved at consumer scale. Deployments are real but largely pilot-stage at industrial customers. The bifurcation between Chinese mass-manufacturing (Unitree’s 5,500+ unit volume) and Western prestige pilots (Figure at BMW, Apollo at Mercedes) is structural rather than transitional. The “year of shipping” framing is partly true and partly hype, and disentangling the two is the most important read of the May 2026 robotics status.

This dispatch is the Q2 reality check. Where companies actually stand. What’s deployed at production scale versus pilot scale. Which regional positions are leading in which categories. What production-cost economics make sense at scale. How robotics connects to the broader AI infrastructure story covered in the hyperscaler capex dispatch — robotics deployment is one of the “new application categories” the $725B 2026 capex assumes will materialize. If robotics scales as projected, the capex is justified. If robotics deployment delays, the demand-pull risk on that capex compounds.

The dispatch on the China Sphere capability gap covered the AI cost dynamics in the model layer. The dispatch on the continual learning research map covered the architectural bottleneck for production AI deployment. Both connect directly to robotics: Chinese mass-manufacturing of robots is the parallel to Chinese cost advantage in AI APIs, and continual learning is the architectural prerequisite for genuinely autonomous robot deployment. Q2 2026 robotics status sits at the intersection of these threads.

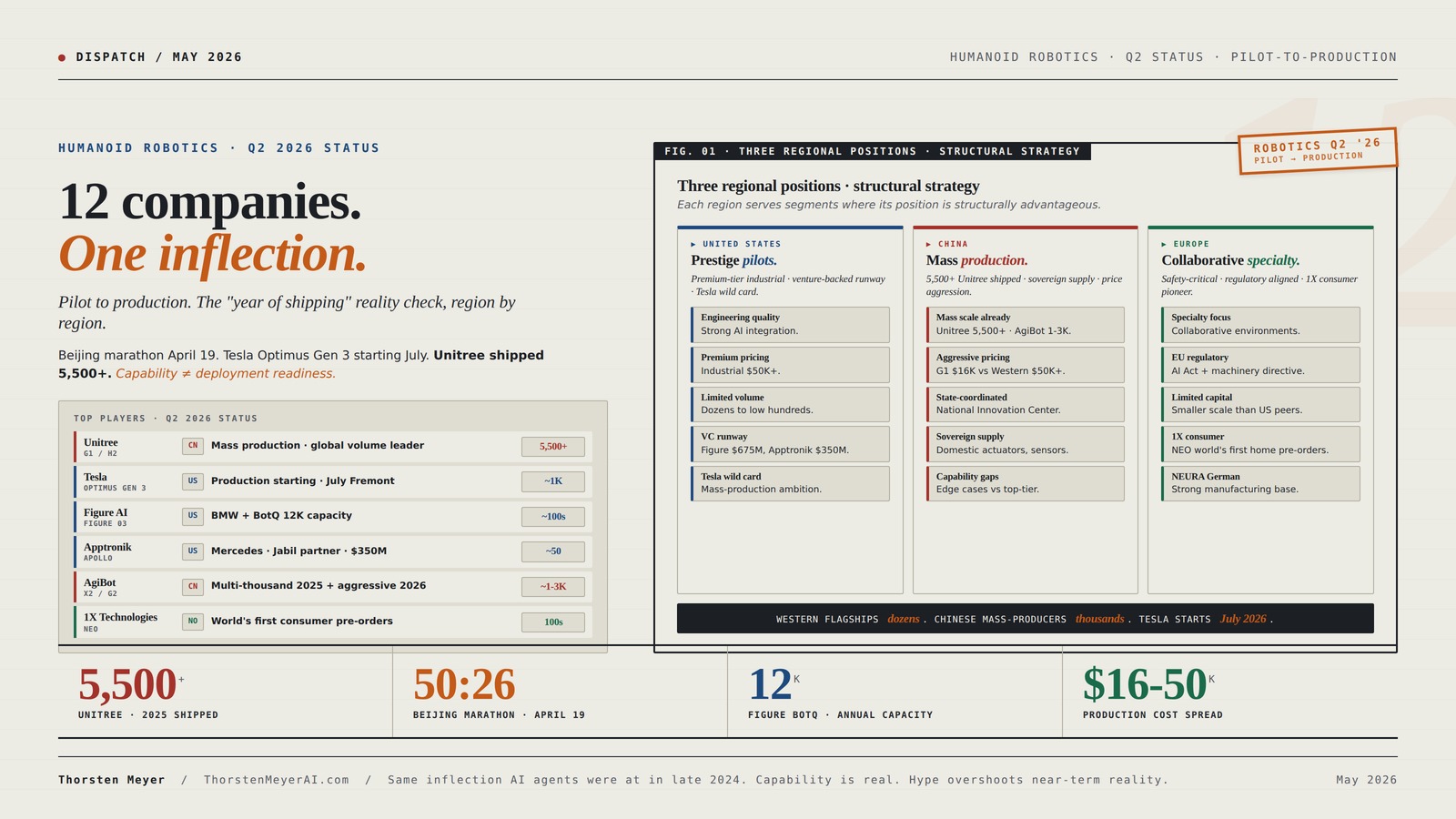

12 companies. One inflection.

Pilot to production. The “year of shipping” reality check, region by region.

Beijing marathon win April 19. Tesla Optimus Gen 3 starting July. Figure 03 BotQ scaling to 12K. Unitree shipped 5,500+ humanoids in 2025. Capability demonstration ≠ deployment readiness. The bifurcation between Chinese mass production and Western prestige pilots is structural.

Twelve companies. Three regions. Where each one stands.

Production scale, regional position, real deployment, current status. Chinese mass-producers (Unitree, AgiBot) are at production volumes Western companies haven’t matched. Western flagships are prestige pilots — measured in dozens, not thousands.

HIWONDER Humanoid Robot with ChatGPT Multimodal AI Models AI Embodied Intelligent Vision Scene Voice Understanding 18DOF Educational Robot Kit Python Programming, TonyPi Standard & RaspberryPi 5 8GB

Al-Driven & Raspberry Pi Powered. TonyPi is a high-performance AI vision robot designed for AI education applications. It…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three strategies. Three segments.

Each region has a structural strategy. Not directly competitive on every dimension; each region serves segments where its position is structurally advantageous.

- Engineering qualityStrong AI integration.

- Premium pricingIndustrial customers at $50K+.

- Limited volumeDozens to low hundreds 2025-2026.

- VC runwayFigure $675M, Apptronik $350M.

- Tesla wild cardMass-production ambition could shift positioning.

- Mass scale alreadyUnitree 5,500+ · AgiBot 1-3K.

- Aggressive pricingG1 starts $16K vs Western $50K+.

- State-coordinatedNational Humanoid Robot Innovation Center.

- Sovereign supplyDomestic actuators, sensors, batteries.

- Capability gapsEdge cases vs Western top-tier.

- Specialty focusCollaborative human-robot environments.

- EU regulatoryAI Act + machinery directive aligned.

- Limited capitalSmaller scale than US peers.

- 1X consumerNEO world’s first home humanoid pre-orders.

- NEURA German industryStrong manufacturing customer base.

Humanoid Robotics in China 2026 Edition: A Complete Industry Catalog and Technical Atlas (Humanoid Robotic Systems Engineering: Design, Deployment, and Operation of Humanoid Robots)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three trajectories. One question.

25/55/20 probability allocation reflects production-ramp execution uncertainty. Industrial / logistics economics are real and incentivize deployment. Consumer market difficulty is structurally intractable on the 2027-2028 timeline.

- 500K-1M annual globalMultiple companies at 100K+ each.

- Industrial 50K+ deployedLogistics scaling fast.

- Consumer market begins$10-15K credible products.

- Capital costs decline$15-20K consumer · $30-50K industrial.

- Outcome: Productivity impact measurable.

- 50-150K industrial 2028Logistics steady growth.

- Consumer pilot onlyGenuine market 2029-2030.

- Tesla rampsExternal lags internal.

- Chinese dominate volumeWestern frontier capability.

- Outcome: Bifurcation hardens through 2028.

- Cost targets missed$50K+ floor for non-Chinese.

- Tesla slipsBeyond 2027.

- Pilot-stuck WesternSingle-digit unit deployments.

- Hype → disappointment2027-2028 cycle.

- Outcome: Mass market deferred 2030+.

Humanoid robotics in May 2026 is at the same inflection that AI agents were at in late 2024. Capability is real, production is starting, the hype cycle is overshooting near-term reality. Companies and investors who pace to the structural reality will benefit; those who pace to the peak face the disappointment-cycle correction in 2027-2028.

Autonomous Robots: From Biological Inspiration To Implementation And Control (Intellegent Robotics And Autonomous Agents)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Distinguish demonstration from deployment.

Marathon wins are engineering capability statements; production deployments at industrial customers are revenue indicators. Position long deployment-credible names (Apptronik, Figure, Agility); cautiously on demonstration-only names. Chinese mass-producers genuine production but face geopolitical risk for Western customers.

Begin pilot deployments now.

2026-2027 is the right window for structured-task workloads. Logistics / sortation / repetitive assembly are credible categories. Integration cost is binding constraint; partner with systems integrators rather than running integration internally. Multi-vendor sourcing strategy reduces lock-in risk.

Begin retraining for 2027-2028 displacement.

Industrial / logistics labor displacement begins meaningfully in 2027-2028. Concentrated in warehousing, automotive manufacturing, sortation. Policy lag of 24-36 months is historical pattern; current preparation appropriate timing. Consumer / home displacement deferred to 2029-2030+.

Treat robotics timing as capex risk factor.

$725B 2026 hyperscaler capex thesis depends partially on robotics inference demand materializing through 2027-2028. Update infrastructure-revenue models accordingly. Bifurcation between industrial-deployable (real) and consumer-deployable (delayed) is the central distinction to model.

BASICS OF FANUC INDUSTRIAL ROBOTICS: A Practical Beginner's Guide to FANUC Robot Operation, Programming & Simulation

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive Summary · Where Each Player Actually Is

| Company | Country | Flagship | Production scale 2025 | 2026 target | Real deployment | Status |

|---|---|---|---|---|---|---|

| Unitree | China | G1 / H2 | 5,500+ shipped | 10-20K | Mass consumer + research | Mass production |

| Tesla | US | Optimus Gen 3 | Internal pilot | 1K external + scaling | Internal Tesla factories | Production starting |

| Figure AI | US | Figure 03 | Limited pilot | BotQ 12K capacity | BMW Spartanburg + Leipzig | Pilot expanding |

| Apptronik | US | Apollo | Limited pilot | “Early scale” 2027 | Mercedes-Benz | Pilot deepening |

| Boston Dynamics | US | Atlas (electric) | Limited pilot | Production ramp | Hyundai 2028 target | Production ramping |

| Agility Robotics | US | Digit | Commercial pilot | Production scaling | Amazon warehouses | Commercial pilot |

| 1X Technologies | Norway | NEO | Pre-order open | First consumer deliveries | Home consumer | Consumer launch |

| XPENG | China | IRON | Q1 2026 launch | Physical AI rollout | Manufacturing + showroom | Launch stage |

| Honor | China | Lightning | Demo / showcase | Beijing marathon win | Showcase + pilots | Demo + commercial |

| AgiBot | China | X2 / G2 | Multi-thousand 2025 | Aggressive 2026 | Manufacturing + pilots | Mass production |

| NEURA Robotics | Germany | 4NE-1 | Limited pilot | Production launch | Industrial + collaborative | Launch stage |

| Sanctuary AI | Canada | Phoenix | Limited pilot | Pilot expansion | Retail / logistics | Pilot stage |

Three structural facts emerge. First, Unitree and AgiBot in China are at production volumes (5,000+ units/year) that no Western company has matched. Second, the Western flagship deployments (Figure at BMW, Apollo at Mercedes, Atlas at Hyundai) are prestige pilots rather than mass deployment — measured in dozens of units, not thousands. Third, 2026 is genuinely the year multiple Western companies move from pilot to production scale (Tesla Optimus Gen 3 starting, Figure BotQ 12K capacity, Apptronik-Jabil ramp), but the production scale they’re targeting in 2026 is roughly where Chinese mass-producers were in 2025.

1. The Beijing marathon · what it actually demonstrated

The Honor “Lightning” Beijing marathon win April 19, 2026 is the single most-cited datapoint in May 2026 humanoid robotics. The detail matters.

What happened. Honor (Huawei spin-off) and the Monkey King team entered a fully autonomous bipedal humanoid robot in the Beijing E-Town Half-Marathon. The robot completed the 21.1 km course in 50:26 — beating the men’s half-marathon world record (57:31, set by Yomif Kejelcha in 2024) by approximately 7 minutes. No teleoperation. The robot navigated elevation changes, pacing decisions, crowd dynamics, and the course’s specific obstacle features autonomously.

What the result demonstrates. Three capabilities beyond simple bipedal mobility. First, sustained energy efficiency at marathon distance — the robot’s battery and thermal systems were designed for endurance rather than burst performance. Second, real-time navigation in a partially predictable environment (the marathon route is known but conditions vary). Third, autonomous decision-making about pacing, obstacle avoidance, and recovery from minor disruptions over a 50-minute continuous operation period.

What the result does not demonstrate. Production-grade deployment readiness. Marathon courses are smooth-surface roads with clear visual markers and largely predictable conditions. Industrial floors with workpieces, fluctuating lighting, debris, and human collaboration are structurally different problems. Home environments with stairs, pets, irregular obstacles, and unpredictable human behavior are even more demanding. A robot that runs a marathon is not necessarily a robot that can fold laundry without breaking dishes. The marathon win is a capability demonstration, not a deployment readiness signal.

The broader Honor positioning. Honor unveiled humanoids at MWC 2026 in Barcelona March 2026 with dance routines, moonwalking, and backflips. Targeting shopping assistance, workplace inspection, companionship roles. The marathon followed this trajectory — Honor is positioning humanoids as showcase-grade capabilities rather than as enterprise-deployment products. The strategic question for Honor is whether the showcase positioning translates into commercial deployment, or whether they remain a capability-demonstration company while production-deployment goes to others (Unitree, AgiBot, Western firms).

The marathon result is genuinely impressive engineering. It is also the most-quoted datapoint in May 2026 robotics coverage, which means it will be over-cited as evidence of capability that production deployments do not yet support. The careful read: the engineering bar is moving up rapidly; the deployment bar is moving up more slowly.

2. The three deployment categories · where humanoids actually work

Production deployment of humanoids in May 2026 sits in three structurally distinct categories.

Category 1 · Industrial / manufacturing. The category where deployment is most production-credible. Apptronik Apollo at Mercedes-Benz European plants for intralogistics. Figure 02 at BMW Spartanburg supporting 30,000+ vehicles annually, expanding to Leipzig. Boston Dynamics Atlas at Hyundai targeting 2028. Agility Digit at Amazon warehouses for logistics. The economics work because: (a) industrial environments are structured and predictable; (b) tasks are repetitive enough that humanoids can be trained for specific workflows; (c) the customer is sophisticated enough to manage integration; (d) the ROI math (replacing labor at $30-60/hour with $20-50K capital cost amortized over 5-7 years) produces favorable unit economics within 18-30 months payback. Deployment scale per customer: dozens to low hundreds of robots in 2026, scaling to 1,000+ per customer by 2028.

Category 2 · Logistics / warehousing. Adjacent to industrial but with different deployment dynamics. Agility Digit at Amazon. Apollo at distribution centers. Unitree variants in Chinese e-commerce fulfillment. The economics work because: (a) the task profile (pick-and-place, sortation, packaging) is well-defined; (b) warehouse environments are structured for robot operation; (c) labor cost is the dominant operating expense in warehousing; (d) e-commerce volume growth justifies sustained capacity expansion. Deployment scale: hundreds per customer in 2026; thousands by 2028.

Category 3 · Consumer / home. The category with the most hype and the weakest production readiness. 1X NEO opened pre-orders for first consumer deliveries 2026. Tesla Optimus eventually targeting consumer market at $20-30K. Honor positioning for “companionship” in some markets. The economics are more difficult because: (a) home environments are unstructured; (b) tasks vary unpredictably; (c) safety requirements are higher (children, pets); (d) consumer willingness to pay $20K+ for a robot that does household chores is unproven. Deployment scale in 2026: hundreds to low thousands of units globally, almost entirely early-adopter / hobbyist customers. The genuine consumer-mass market is 2028-2030 at minimum.

The bifurcation is structural. Industrial and logistics deployments are real, growing, and economically justified. Consumer deployments remain speculative. Companies that target both (Tesla, Figure, 1X) are pursuing the larger market opportunity but face the structural difficulty of meeting two very different deployment-readiness bars. Companies that focus on industrial / logistics (Apptronik, Boston Dynamics, Agility, Unitree industrial variants) have a clearer near-term path to revenue.

3. The three regional positions · US prestige, China mass, EU specialty

Geographic positioning in humanoid robotics is structurally similar to the AI-model layer covered in the China Sphere dispatch but with different dynamics.

US position · prestige pilots and capital-rich startups. Figure AI ($675M raised, BMW deployments). Apptronik ($350M, Mercedes partnership, Jabil manufacturing partner). Boston Dynamics (Hyundai-owned). Agility Robotics (Amazon partnership). Tesla (vertically integrated, Optimus Gen 3 starting). Sanctuary AI (Canada-based, US market focus). The US position is characterized by: (a) high-quality engineering with strong AI integration; (b) prestige industrial customer relationships at premium pricing; (c) limited production volume in 2025-2026; (d) substantial venture capital available to extend runway; (e) Tesla’s mass-production ambitions as the wild card that could shift the position significantly if Gen 3 ramp goes as planned.

Chinese position · mass production and price aggression. Unitree (5,500+ units shipped 2025; G1 starting at ~$16K). AgiBot (multi-thousand unit production 2025). XPENG (IRON, Q1 2026 launch, leveraging EV manufacturing). Honor (showcase capabilities, expanding production). Leju Kuavo (industrial focus). Multiple smaller players. The Chinese position is characterized by: (a) substantial mass-production capacity already deployed; (b) aggressive price points (Unitree G1 starts at ~$16K versus Western premium tier $50K+); (c) state-supported industrial coordination (the National Humanoid Robot Innovation Center provides shared infrastructure); (d) sovereign-supply-chain advantages (Chinese-manufactured actuators, sensors, batteries reduce dependence on Western suppliers); (e) capability gaps relative to top-tier Western models on edge cases but parity or near-parity on core production tasks.

European position · specialty and collaborative. NEURA Robotics (Germany, 4NE-1 collaborative humanoid). 1X Technologies (Norway, NEO consumer focus). Humanoid (UK, HMND 01). Smaller scale than US or Chinese cohorts. The European position is characterized by: (a) specialization on collaborative human-robot environments and safety-critical applications; (b) strong industrial integration with European manufacturing customers; (c) limited venture capital scale relative to US peers; (d) regulatory advantages within EU markets through compliance with EU AI Act and machinery directive frameworks.

The cumulative picture: each region has a structural strategy. US optimizes for premium-tier industrial deployment with venture-backed runway. China optimizes for mass production at aggressive price points. Europe optimizes for collaborative-environment specialty. The strategies are not directly competitive on every dimension; each region serves segments where its position is structurally advantageous.

4. The production economics · what’s the actual ROI math

Production economics for humanoid robotics deployment depends on three components: capital cost (robot purchase), operating cost (energy, maintenance, integration labor), and labor-replacement value (the wages the robot avoids paying).

Capital cost benchmarks May 2026. Unitree G1: $16K starting (entry tier). Tesla Optimus Gen 3 target: $20-30K (Tesla guidance). Apptronik Apollo target: sub-$50K (Apptronik guidance). Figure 03: not publicly priced but estimated $50-80K based on industry benchmarks. Boston Dynamics Atlas: not publicly priced; premium tier estimated $100K+. NEURA 4NE-1: similarly premium tier. The price spread is wide — entry-tier Chinese at $16K, premium-tier Western at $100K+.

Operating cost benchmarks. Energy: 2-4 kWh per 8-hour shift, approximately $0.50-1.50 per shift in industrial electricity. Maintenance: 5-10 percent of capital cost annually for high-utilization deployment. Integration labor: 100-300 hours per deployment for setup, training, integration with existing systems — approximately $20-50K depending on engineer rates. Spare parts and replacement: budget 8-12 percent of capital cost annually for first 3 years. Total operating cost run rate for an actively deployed humanoid: approximately 20-30 percent of capital cost per year.

Labor-replacement math. US industrial labor: $30-60 per hour fully loaded. European industrial labor: €25-50 per hour. Chinese industrial labor: $10-25 per hour. Annual labor cost (8-hour shift, 250 working days): US $60-120K; Europe €50-100K; China $20-50K. The labor-replacement value sets the ceiling on what humanoid deployment can pay back over time.

Payback period calculations. US industrial deployment: $30K robot + $20K integration + $7-9K annual operating = approximately $50K all-in cost, replacing $60-120K annual labor. Payback in 6-12 months on the headline math. Chinese industrial: $20K robot + $10K integration + $5-7K annual operating = approximately $30K, replacing $20-50K labor. Payback 12-24 months.

Why the headline math overstates the reality. Three caveats. First, robots do not work the equivalent of 100 percent of human labor — they work on the subset of tasks they can handle reliably, and reliability remains imperfect. Second, integration costs scale faster than capital costs at production scale — deploying 100 robots in a facility requires 10-50× the integration effort of deploying 1. Third, the depreciation-vs-obsolescence tradeoff: early-generation humanoids will be obsolete within 3-5 years as next-generation models ship; the capital cost should depreciate over the obsolescence horizon, not the physical-life horizon.

The honest payback math for first-wave deployments (2025-2026): 24-48 months for industrial / logistics, considerably longer for any consumer / home application. The math improves substantially through 2027-2028 as production volumes scale and capital costs decline.

5. The capability gap · what’s real vs what’s hyped

Hype has been a structural feature of humanoid robotics coverage for several years. May 2026 is the moment to disentangle real capabilities from marketing.

Real capability 1 · Bipedal mobility on structured surfaces. Mature. Multiple platforms (Unitree G1, H2; Boston Dynamics Atlas; Tesla Optimus; Honor Lightning) demonstrate stable walking, running, stair navigation, recovery from minor pushes. The marathon win confirms endurance. Bipedal locomotion is no longer the binding capability constraint.

Real capability 2 · Object manipulation in structured environments. Maturing. Figure 02 at BMW handles sheet metal parts within millimeter tolerances. Apptronik Apollo at Mercedes handles intralogistics tasks. Unitree platforms handle industrial pick-and-place. The gap remains in unstructured environments and novel objects, but structured-environment manipulation is approaching production readiness.

Real capability 3 · Long-horizon autonomous operation. Emerging. Figure 03 24/7 demos. Marathon-length continuous operation. Multi-hour shift operation in industrial settings. Battery-life and thermal-management constraints are being addressed. The gap is in genuine adaptive operation across changing task profiles within a single deployment.

Hyped capability 1 · Generalist home assistant. Far from production. The “robot that does household chores” framing ignores the structural difficulty: home environments are unstructured, tasks vary unpredictably, safety requirements are high, and humans expect natural interaction. The 1X NEO consumer launch is the first attempt; results through 2026-2027 will determine whether this is a 2027-2028 commercial market or a 2030+ market.

Hyped capability 2 · Cognitive understanding and natural language interaction. Improving but limited. Vision-language-action models provide semantic understanding of tasks, but the gap from “I can identify a cup” to “I can navigate the social and physical context of clearing a table after dinner” is substantial. The continual learning constraint covered in the research map dispatch applies acutely to robotics: a robot that learns from each deployment’s experience without forgetting prior tasks is the genuine target, and this remains 2028-2030 capability.

Hyped capability 3 · Mass production at consumer-market prices. Not yet achieved. Tesla’s $20K target is forward-looking guidance. Unitree’s $16K G1 is real but at entry-tier capability. The gap between current production economics and consumer-market prices ($5-10K for genuine mass adoption) is closeable through scale but not yet closed. Optimistic forecasts require 1M+ unit annual production globally; current production is 10-20K annually across all manufacturers combined.

The cumulative read: industrial and logistics deployment capabilities are approaching production readiness with real economics. Consumer / home deployment is years from production readiness with unproven economics. The hype cycle pushes both into the same “humanoids are here” framing, which conflates two structurally different deployment categories.

6. The connections to other dispatches

Robotics Q2 2026 status connects to multiple structural threads from this dispatch series.

Connection 1 · The hyperscaler capex story. The $725B capex dispatch flagged that “the next leg of growth requires new categories” and listed robotics as one of the key categories. If robotics deployment scales as the bullish case projects (1M+ units globally by 2028), the AI infrastructure capex is justified through robotics-driven inference demand. If robotics deployment delays to 2030+, the demand-pull risk on the existing capex compounds.

Connection 2 · The China Sphere capability gap. The Q2 update dispatch covered the Chinese position in AI models. Chinese position in robotics is structurally similar: mass-production scale advantage, aggressive pricing, capability parity on production tasks, gap remains on top-tier engineering. The sovereign-supply-chain advantages compound — Chinese-manufactured actuators, sensors, batteries reduce dependence on Western suppliers in ways that AI-model dependencies don’t apply.

Connection 3 · The continual learning research map. The CL research map dispatch covered the architectural bottleneck for production AI. Robotics surfaces continual learning gaps faster than text-based AI because each deployment encounters genuinely novel physical-world situations. ALMA-style meta-learned memory designs and Evo-Memory benchmarks have specific relevance to robotics deployment. The “production CL by 2028” timeline maps to the “robotics genuinely-deployable mass market by 2028-2030” timeline.

Connection 4 · FDE economics. The FDE Economics 2.0 dispatch covered embedded-engineer economics for AI deployment. Robotics deployment requires similar embedded-engineering pools — 100-300 hours per deployment for setup, training, integration. The Apptronik-Jabil partnership is a structural answer to this: Jabil provides manufacturing-engineering capacity at scale, freeing Apptronik to focus on robotics-specific capability. Similar structures (manufacturing-partner + robotics-IP holder) are likely to proliferate through 2026-2027.

Connection 5 · The PE consortium structure. The Anthropic-Blackstone-Goldman JV dispatch covered the JV-with-PE-consortium template for AI deployment scaling. Robotics deployment faces the same scaling challenge — too much customer demand, too few engineers to deliver. PE-backed JVs that fund the deployment-engineering pool are likely candidates through 2026-2027. Carlyle + Apptronik, KKR + Figure, Bain + Boston Dynamics — speculative but structurally plausible.

Connection 6 · The agentic loop failure modes. The failure modes dispatch covered taxonomy of agentic-AI failure modes (drift, state, coordination, termination, adversarial, tool interface). Each maps to robotics with physical-world manifestations. Drift becomes spatial drift. State becomes physical state. Coordination becomes multi-robot fleet coordination. Termination becomes “when does the robot stop the task.” Adversarial becomes physical safety. Tool interface becomes manipulation. The taxonomy applies; the failure mode magnitudes are different (physical failures have safety-critical consequences).

The cumulative picture: robotics is not a separate AI story; it is the embodied-deployment manifestation of the same structural threads. The labs and infrastructure providers building the model and infrastructure layers are also implicitly enabling the robotics layer, and the timing constraints on robotics scale (2028-2030 for genuinely mass-deployed) constrain the timing of the broader AI deployment economics.

7. Three scenarios for 2027-2028

Three scenarios for how humanoid robotics deployment evolves through 2027-2028.

Bullish scenario · 25% probability · “Mass production arrives by 2028.” Multiple Western companies (Tesla, Figure, Apptronik) and multiple Chinese companies (Unitree, AgiBot, XPENG) reach 100K+ unit annual production by 2028. Aggregate global humanoid production hits 500K-1M annually. Industrial and logistics deployments scale to 50,000+ deployed units globally. Consumer / home deployments begin in earnest with first credible mass-market products at $10-15K. Capital costs decline to $15-20K consumer-tier and $30-50K industrial-tier. The economics work; the deployments accumulate; the productivity impact on industrial labor markets becomes measurable.

Base scenario · 55% probability · “Industrial scales, consumer delays.” Industrial / logistics deployment grows steadily through 2028 to 50-150K deployed units globally. Consumer / home deployment remains pilot-stage and early-adopter through 2028, with the genuine consumer market deferred to 2029-2030. Capital costs decline gradually but remain above mass-consumer thresholds for non-Chinese platforms. Tesla Optimus production ramps but external deployments lag internal deployments. Chinese mass-producers (Unitree, AgiBot) continue to dominate volume but capability-frontier remains Western. The bifurcation between industrial-credible and consumer-not-yet hardens through 2028.

Bearish scenario · 20% probability · “The deployment-versus-promise gap widens.” Production-cost targets are missed materially. Tesla Optimus ramp slips beyond 2027. Figure / Apptronik / Boston Dynamics struggle to scale beyond pilot deployments. Capital costs remain above $50K for non-Chinese platforms, and labor-replacement math fails to justify deployment at scale. Industrial customers limit deployments to single-digit-unit pilots. The hype cycle through 2025-2026 produces a deployment-disappointment cycle in 2027-2028. Chinese mass-producers continue at scale but are confined to consumer-grade Chinese-domestic deployments. The genuine humanoid mass market deferred to 2030+.

The 25/55/20 probability allocation reflects the genuine uncertainty in production-ramp execution. The base scenario is most likely because the industrial / logistics economics are real and incentivize deployment, while the consumer market difficulty is structurally intractable on the 2027-2028 timeline. The bullish scenario requires multiple production ramps to execute simultaneously without significant slippage. The bearish scenario requires deployment economics to break down even on the industrial side.

8. Strategic implications by stakeholder

The Q2 2026 status has direct consequences for five distinct stakeholder groups.

For robotics company investors. The deployment-stage matters more than the capability-demonstration stage. Companies with real industrial customer deployments (Apptronik-Mercedes, Figure-BMW, Agility-Amazon, Boston Dynamics-Hyundai) are positioned for revenue ramp through 2026-2027. Capability-demo-only companies (Honor, Tesla Optimus pre-production) face execution risk in moving from demo to deployment. Position accordingly. Chinese mass-producers (Unitree) are interesting at production scale but face geopolitical-disruption risk in Western-customer deployments.

For industrial customers evaluating deployment. 2026-2027 is the right window to begin pilot deployments at structured-task workloads (logistics, sortation, repetitive assembly). Vendor lock-in risk is real; multi-vendor sourcing strategy is appropriate. Integration cost is the binding constraint for first-deployment customers; sourcing implementation partners (Jabil, the systems integrators in the Claude Partner Network) reduces the integration-cost overhead.

For policymakers and labor economists. Industrial / logistics labor displacement begins meaningfully in 2027-2028 as production volumes scale. The displaced labor is concentrated in specific industries (warehousing, automotive manufacturing, sortation) and specific demographic categories. Policy response (retraining programs, social safety net adjustments, tax structure for capital-intensive vs. labor-intensive operations) needs to begin now to be effective for the 2027-2028 transition. Consumer / home robotics labor implications are deferred to 2029-2030+.

For AI labs and infrastructure providers. Robotics inference demand is one of the demand sources that justifies the $725B 2026 hyperscaler capex. If robotics deployment scales, the inference workload growth supports the capex thesis. If robotics deployment delays, inference demand falls short of capex assumption, and impairment risk increases. The lab-and-infrastructure positioning should include robotics-deployment timing as a forward-looking risk factor explicitly.

For PE firms and structured-financing players. Robotics deployment-engineering pools are the natural target for PE-consortium-funded JV structures, following the Anthropic-Blackstone-Goldman template. Robotics-IP holder + manufacturing-partner + PE-consortium-customer-pipeline = structurally similar to AI deployment JVs. Apptronik’s existing Jabil partnership is a precursor; full PE-backed structures emerge through 2026-2027. Engage now while the structural template is replicating.

What to Do This Quarter

1. Robotics company evaluation. Distinguish demonstration capabilities from deployment readiness. Marathon wins are engineering capability statements; production deployments at industrial customers are revenue indicators. Position long deployment-credible names (Apptronik, Figure, Agility); position cautiously on demonstration-only names. Chinese mass-producers are genuine production but face geopolitical risk for Western customers.

2. Industrial customer deployment. Begin pilot deployments now at structured-task workloads. Logistics / sortation / repetitive assembly are the credible categories. Integration-cost management is the binding constraint; partner with systems integrators rather than running integration internally. Multi-vendor sourcing strategy reduces lock-in risk.

3. Policy and labor. Begin retraining and social-safety-net design now for the 2027-2028 industrial / logistics displacement wave. Policy lag of 24-36 months is the historical pattern; current preparation is appropriate timing. Consumer / home displacement is deferred but worth strategic consideration.

4. Connection-mapping to AI infrastructure. Treat robotics deployment timing as a forward-looking risk factor for AI infrastructure capex. The $725B capex thesis depends partially on robotics inference demand materializing through 2027-2028. Update infrastructure-revenue models accordingly. The bifurcation between industrial-deployable (real) and consumer-deployable (delayed) is the central distinction to model.

The Strategic Read

Q2 2026 humanoid robotics is in an inflection. Multiple Chinese companies are at mass-production scale (Unitree 5,500+ shipped 2025, AgiBot multi-thousand). Multiple Western companies are moving from pilot to production (Tesla Optimus Gen 3 starting July, Figure 03 BotQ scaling to 12K, Apptronik-Jabil ramp). The Beijing marathon win April 19, 2026 demonstrated capability that production deployments do not yet support. The disentanglement between capability demonstration and deployment readiness is the central read of the May 2026 status.

The three deployment categories have structurally different economics. Industrial / manufacturing is real, growing, and economically justified through 24-48 month payback periods. Logistics / warehousing is similar with somewhat longer payback periods. Consumer / home remains speculative with unproven economics through 2026-2027. The bifurcation is structural rather than transitional.

The three regional positions optimize for different segments. US optimizes for premium-tier industrial deployment with venture-backed runway. China optimizes for mass production at aggressive price points. Europe optimizes for collaborative-environment specialty. Each position has structural advantages in its segment; cross-segment competition will sort out through 2027-2028.

The capability gap between demonstration and deployment remains. Bipedal mobility, structured-environment manipulation, long-horizon autonomous operation are real capabilities approaching production. Generalist home assistance, cognitive social interaction, mass production at consumer prices are hyped capabilities still 2028-2030+ from production. The hype cycle conflates these into a single “humanoids are here” framing; the careful read separates them.

Three scenarios are plausible for 2027-2028. Bullish (25%): mass production arrives, 500K-1M annual global production, industrial and consumer deployment both scaling. Base (55%): industrial scales steadily, consumer delays to 2029-2030, bifurcation hardens. Bearish (20%): deployment-versus-promise gap widens, capital costs miss targets, mass market deferred to 2030+.

The strategic implications run by stakeholder. Robotics investors should distinguish demonstration capabilities from deployment readiness. Industrial customers should begin pilot deployments now at structured-task workloads. Policymakers should begin retraining preparation for 2027-2028 industrial displacement. AI labs should treat robotics deployment timing as a forward-looking risk factor for the $725B capex demand-pull thesis. PE firms should engage on robotics-deployment-engineering JV structures.

The deeper signal: humanoid robotics in May 2026 is at the same inflection that AI agents were at in late 2024 — capability is real, production deployment is starting, the hype cycle is overshooting near-term reality, and the structural transition through 2027-2030 will produce both winners and losers based on execution. The companies and investors who pace their commitments to the structural reality rather than the hype-cycle peak will benefit; those who pace to the peak will face the disappointment-cycle correction in 2027-2028.

The connection to the broader AI infrastructure story is the structural fact. Robotics is one of the demand-pull application categories that justifies the $725B 2026 hyperscaler capex. If robotics scales as projected, the capex is justified. If robotics delays, the capex demand-pull risk compounds. The May 2026 status puts robotics deployment timing on the same critical-path as AI infrastructure ROI. Both threads resolve through 2027-2028 quarterly prints.

Q2 2026 humanoid robotics is at the pilot-to-production inflection. Chinese mass-production is real (Unitree 5,500+ shipped 2025). Western prestige pilots are real (Figure-BMW, Apollo-Mercedes). Tesla Optimus Gen 3 starts production July. Beijing marathon demonstrated capability that production doesn’t yet support. The bifurcation between industrial-deployable (real) and consumer-deployable (delayed) is the central distinction.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The $725B Hyperscaler Capex Question

- The China Sphere Capability Gap Q2 Update

- The Continual Learning Research Map

- The Anthropic-Blackstone-Goldman JV Structure

- Forward-Deployed Engineer Economics 2.0

- Agentic Loop Failure Modes

Sources

- humanoid.press · multi-source aggregation through May 2026

- Honor / Monkey King · Beijing E-Town Half-Marathon · April 19, 2026 · Lightning autonomous win 50:26

- Figure AI · Figure 03 24/7 autonomous demos · BotQ facility 12,000+ units annually

- Tesla · Optimus Gen 3 production starting July/August 2026 Fremont; Giga Texas 2027

- Apptronik · Apollo · $350M raised; Mercedes-Benz partnership; Jabil manufacturing partner; sub-$50K target

- BMW Press Release 2024 · Figure 02 at Spartanburg; expansion to Leipzig

- Unitree · 5,500+ humanoids shipped 2025; targeting 10-20K 2026

- Boston Dynamics · Atlas production ramp 2026; Hyundai 2028 target deployments

- Agility Robotics · Digit at Amazon warehouses (commercial pilot stage)

- 1X Technologies · NEO consumer pre-orders open · 2026 delivery

- XPENG · IRON · Q1 2026 launch · Physical AI strategy

- Honor · MWC 2026 Barcelona unveiling · March 2026

- AW 2026 Seoul · March 2026 · multi-platform showcase

- Standard Bots · Top 12 humanoid robotics companies analysis

- Articsledge · AI Humanoid Robots 2026 technology guide · January 2026

- Wins Solutions · Humanoid robots reality vs hype December 2025 analysis