By Thorsten Meyer — May 2026

Anthropic released ten ready-to-run agent templates for financial services this week — Pitch builder, Meeting preparer, Earnings reviewer, Model builder, Market researcher, Valuation reviewer, General ledger reconciler, Month-end closer, Statement auditor, KYC screener — paired with Claude add-ins for Microsoft Excel, PowerPoint, and Word (with Outlook coming), eight new data connectors, and Moody’s first MCP app. The technical claim: Claude Opus 4.7 leads Vals AI’s Finance Agent benchmark at 64.37 percent — state-of-the-art at the model’s April 16 release. The strategic claim is more interesting and gets less coverage in the announcement: Anthropic isn’t competing with Bloomberg Terminal. Anthropic is positioning Claude as the orchestration layer over Bloomberg-class data providers. That’s structurally different and far more disruptive to a different set of incumbents than the headline framing suggests.

The connector list reveals the real strategy. FactSet, S&P Capital IQ, MSCI, PitchBook, Morningstar, Chronograph, LSEG, Daloopa already connected. Eight new partners added: Dun & Bradstreet, Fiscal AI, Financial Modeling Prep, Guidepoint, IBISWorld, SS&C IntraLinks, Third Bridge, Verisk. Moody’s launched its first MCP app with credit ratings and data on 600+ million public and private companies. The aggregate picture: Claude becomes the single conversational interface that pulls from the entire competitive landscape of financial data providers, then orchestrates across the analyst’s existing Excel/PowerPoint/Outlook surface area. The data underneath stays where it is. The interface moves to Claude Cowork.

The Vals benchmark figure deserves precise reading. Claude Opus 4.7 at 64.37 percent leads Sonnet 4.6 at 63.33 percent, Meta’s Muse Spark at 60.59 percent, DeepSeek V4 at 60.39 percent, Claude Opus 4.6 (Thinking) at 60.05 percent. The benchmark was rebuilt in early 2026 with quality control by experts from Goldman Sachs, Silver Lake, and Citadel — 537 questions covering equity research, credit analysis, due diligence on SEC filings. The structural read: state-of-the-art is “best available” not “great.” Approximately one in three finance-analyst questions is still answered wrong. For a junior analyst trusting Claude output without senior review on professional work, that error rate is catastrophic. For a senior analyst using Claude to accelerate research synthesis with their own judgment as the validation layer, it’s transformative. The deployment pattern — and the liability framework — depends critically on which model dominates.

This dispatch is the structural read on what the May 7 announcement means for the financial services industry value chain. The ten-template-to-job-function displacement mapping. The provider impact ranking — who gains, who loses, who repositions. The customer-facing implications across corporate banking, retail wealth, compliance, and private equity. The 64.37 percent benchmark reality check and what it signals about safe deployment patterns. Three scenarios for finance-vertical AI deployment through 2026-2028. The connections to broader threads from this dispatch series.

The dispatch on labor displacement Q1-Q2 2026 data covered the ~200K Wall Street jobs cohort over 3-5 years. Anthropic just shipped the productized version. The dispatch on the Anthropic IPO disclosure covered enterprise penetration as a value driver. The financial services vertical is the highest-value enterprise vertical Anthropic could attack. The dispatch on the compute reckoning covered the SpaceX deal closing the capacity gap. Without that capacity, the finance vertical deployment would have hit the same rate-limit issues that plagued Claude Code through Q1 2026. The timing of the May 6 SpaceX announcement and the May 7 financial services announcement is not coincidental.

Above the data.

Anthropic isn’t competing with Bloomberg Terminal. It’s positioning Claude as the orchestration layer over Bloomberg-class data providers.

10 ready-to-run agent templates · Claude across Excel, PowerPoint, Word, Outlook · 8 new connectors + Moody’s MCP app. Powered by Claude Opus 4.7 · state-of-the-art on Vals AI Finance Agent benchmark at 64.37%. Connector ecosystem (FactSet, S&P CapIQ, MSCI, PitchBook, Morningstar, LSEG, Daloopa + 8 new) is the moat. UI moves to Claude Cowork; data layer stays.

Ten templates. Ten cohorts.

The ten agent templates map cleanly to specific bank job functions. Reading them as displacement signals reveals which cohorts within financial services are most exposed — and which workflow categories deploy fastest.

Excel Data Analysis For Dummies (For Dummies (Computer/Tech))

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Six providers. Three trajectories.

Bloomberg’s $32K/seat moat was the consolidated UI over data + news + analytics + chat. If Claude Cowork wins the analyst desktop, the UI moat erodes. The data layer stays where it is.

Claude AI for Financial Analysis & Investment Research : Institutional-Grade Prompts for Valuation, Forecasting, Risk Analysis & Portfolio Management

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios. One vertical.

30/50/20 probability allocation. Base case represents bifurcated deployment — back/middle office aggressive, front office cautious due to liability. The 64.37% accuracy threshold determines deployment pattern.

- 3-5× productivitySenior analysts on covered workflows.

- Gradual hiring contraction15-25% annually. Natural attrition.

- Bloomberg defense holds~30% mindshare maintained.

- 75-80% accuracy by 2027-28Vals benchmark trajectory.

- Outcome: Cooperative regulatory framework develops.

- Back/middle office aggressiveKYC, GL, audit deploy fast.

- Front office cautiousLiability concerns slow IB pitches, M&A.

- 100-150K displacementBy end of 2028.

- Coexistence with Bloomberg ASKBDifferent segments.

- Outcome: Liability framework refinement 2027-28.

- High-profile failureKYC miss · M&A error · client misrep.

- Industry deployment retreatAdvisory-only AI use.

- Stricter validationErodes productivity gains.

- 50-75K displacement onlySlower trajectory.

- Outcome: Vals accuracy stalls at 70-72%. Bear case for AI lab valuations gains support.

State-of-the-art at 64.37% means approximately one in three professional finance-analyst questions is answered wrong. Senior analysts as validation layer is the durable pattern. Junior analysts trusting AI output is the failure mode. The deployment architecture follows directly from the accuracy threshold.

Excel is not dead: It's Just got a Brain

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Back/middle aggressive. Front cautious.

Deploy back/middle office templates aggressively (KYC screener, GL reconciler, month-end closer, statement auditor) — human validation pattern is straightforward. Deploy front-office templates (pitch builder, model builder, valuation reviewer) cautiously with senior validation. Plan cohort headcount with 15-25% annual contraction in affected junior roles. Compliance and legal in deployment governance from day one.

Bloomberg accelerates. Others position.

Bloomberg should accelerate ASKB rollout and emphasize data-depth differentiation — the race is timeline-pressured. FactSet, LSEG, Moody’s should aggressively position MCP/connector integration. Specialized vertical providers should pursue first-mover advantage in their domain. Hybrid (own UI + Claude integration) is most likely durable.

Reskill toward vertical AI.

Vertical AI specialists (combining finance domain expertise with AI fluency) is the most defensible path. Senior cloud / security / data engineering paths offer durable demand. Geographic flexibility helps — financial centers (NYC, London, Singapore, Frankfurt) face most concentrated displacement; secondary centers may face less. The Atlassian template (cut + AI-hire rebalance) is the durable employer model.

Update provider competitive models.

Bloomberg position is timeline-pressured. FactSet (FDS), LSEG (LSE), S&P Global (SPGI), Moody’s (MCO) all have public equity exposure — orchestration-layer dynamic is mostly bullish for non-Bloomberg providers. Anthropic IPO valuation case strengthens with finance vertical penetration. Watch Google I/O May 19-20 for Gemini finance vertical response.

Financial Modeling Workbook with Excel: Build 3-Statement Financial Models & DCF Valuations Step by Step with Practical Exercises, Templates, and Real-World Examples (Fin Model Excel 1)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive Summary · The Industry Impact in One Table

| Stakeholder | Direction | Impact magnitude | Time horizon |

|---|---|---|---|

| Bloomberg Terminal | Most exposed (UI moat) | High | 12-36 months |

| FactSet | Beneficiary (MCP-positioned) | Medium positive | 6-18 months |

| S&P Capital IQ | Mixed (smaller footprint) | Low-medium | 12-24 months |

| LSEG / Refinitiv | Beneficiary (AI-ready datasets) | Medium positive | 6-18 months |

| Moody’s | Beneficiary (MCP app) | Medium positive | Immediate |

| Specialized providers (Verisk, IBISWorld, etc.) | Beneficiary (distribution) | Medium positive | Immediate |

| Junior IB analysts | Cohort displacement | High | 6-24 months |

| Compliance ops staff (KYC) | Cohort displacement | High | 6-18 months |

| Mid-level analysts (research / credit) | Productivity augmentation | Medium | 6-24 months |

| Senior bankers / partners | Productivity augmentation | Positive | Immediate |

| Corporate banking clients | Faster pitch cycles | Positive | 6-18 months |

| Retail / wealth clients | Trickle-down advisory improvement | Positive | 12-36 months |

| PE diligence vendors | Disrupted (model builder + valuation reviewer) | Medium-high | 12-36 months |

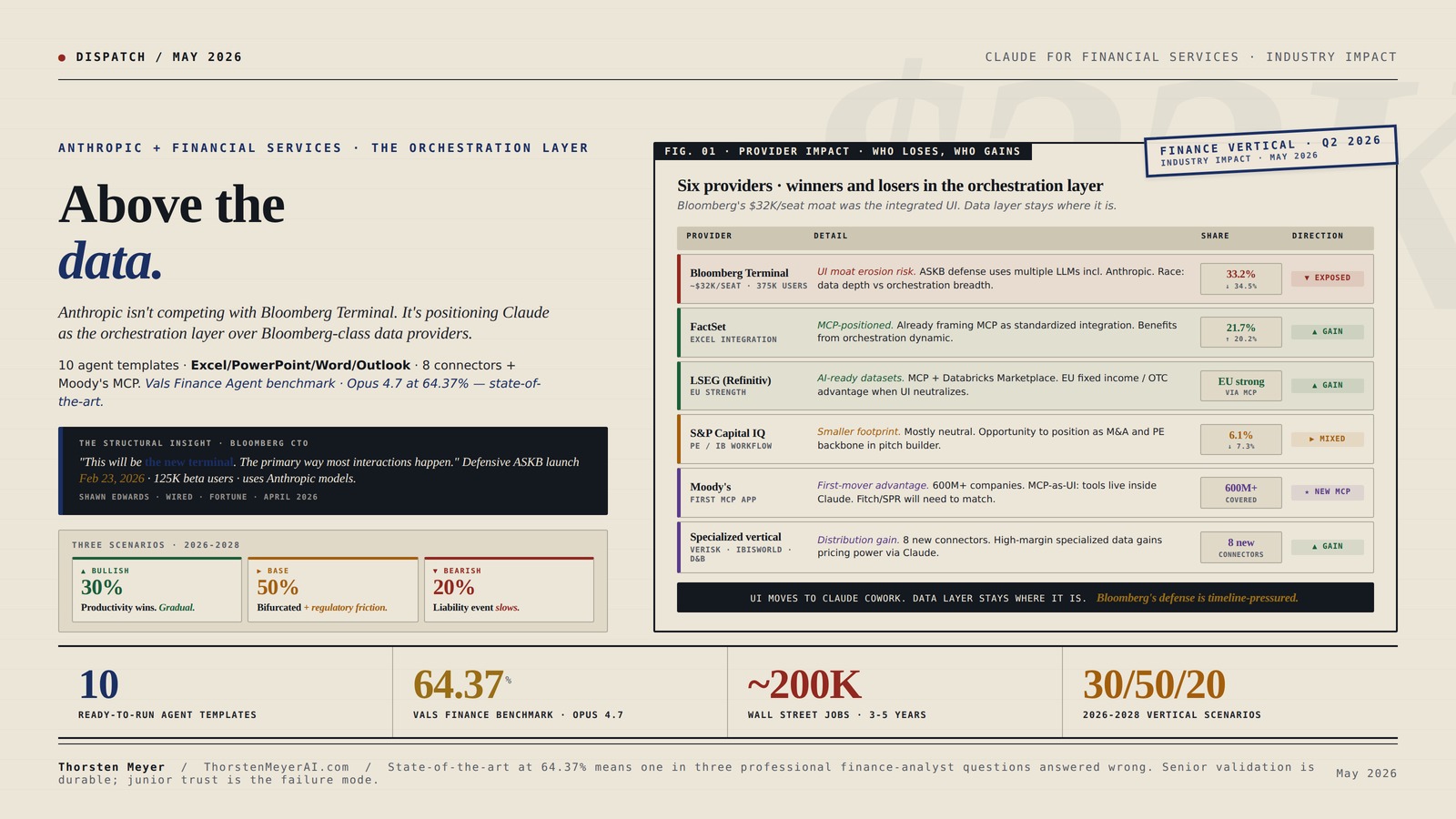

The provider impact pattern: Bloomberg’s $32K/seat moat was always the consolidated UI over data, news, messaging, analytics. If Claude Cowork becomes the primary analyst interface — pulling from FactSet, S&P, LSEG, Moody’s via connectors and orchestrating across Microsoft 365 — the UI moat collapses. Underneath data is reproducible from Bloomberg’s competitors. Bloomberg’s defensive response is ASKB, launched February 23, 2026, with roadmap update April 16, beta open to ~125,000 users (one-third of 375K Terminal users). CTO Shawn Edwards: “This will be the new terminal. The primary way most interactions happen.” ASKB uses multiple LLMs including Anthropic models — Bloomberg is hedging. The race is whether Bloomberg’s data integration depth or Anthropic’s orchestration breadth wins the analyst desktop.

1. The ten templates as direct cohort displacement

The ten agent templates map cleanly to specific bank job functions. Reading them as displacement signals reveals which cohorts within financial services are most exposed.

Pitch builder = junior IB analyst. Creates target lists, runs comparables, drafts pitchbooks for client meetings. This is the canonical first-year investment banking analyst workflow — 70-80 hour weeks of pulling comps, building football fields, formatting decks. The template ships with Excel comps modeling and PowerPoint deck drafting integrated. A senior banker can hand it a target list and get back a draft pitchbook within hours instead of having an analyst pull two all-nighters. The cohort impact is direct: the 1st-year IB analyst class at major banks (Goldman, Morgan Stanley, JPMorgan, BofA, Citi, plus elevated boutiques) was approximately 5,000-6,000 hires per year industry-wide pre-AI. The template doesn’t eliminate the role — junior analysts still review, iterate, and add judgment — but the headcount-per-deal ratio compresses substantially. JPMorgan and other major banks have already reduced 1st-year analyst hiring 15-25 percent in 2025-2026 in anticipation.

Model builder + Valuation reviewer = associate / VP-level. Creates and maintains financial models from filings, data feeds, analyst inputs. Checks valuations against comparables, methodology, firm review standards. This is the 2nd-3rd year associate workflow plus the VP review function. The template handles the modeling mechanics; the human role shifts to judgment on assumptions, scenario design, and client communication. The cohort impact: associate-level hiring contracts more slowly than analyst-level because the judgment layer is harder to automate, but the work-per-headcount expectation rises sharply.

Earnings reviewer + Market researcher = sell-side / buy-side equity research analyst. Reads transcripts and filings, updates models, flags thesis-relevant changes. Tracks sector developments, synthesizes news/filings/broker research. This is the equity research analyst’s daily workflow at hedge funds, mutual funds, sell-side research desks. The template displaces approximately 40-60 percent of routine research synthesis work. Hedge fund analysts at Citadel, Point72, Millennium have been using Claude/GPT-class tools for this since 2024. The productized version reduces the technical setup cost from “needs in-house engineering” to “install plugin.” The cohort impact: junior research analyst headcount compresses; senior analysts get force-multiplied.

KYC screener = compliance operations. Assembles entity files, reviews source documents, packages escalations for compliance review. KYC (Know Your Customer) operations is the highest-volume, lowest-judgment compliance function — major banks employ 5,000-15,000+ KYC ops staff each, often based in lower-cost geographies (India, Philippines, Poland, Mexico). The template directly attacks this cohort. The displacement potential is substantial: 30-50 percent reduction in KYC ops headcount over 18-36 months as banks deploy at scale. The catch: KYC is a regulated function, and AI-driven KYC failure produces regulatory liability. The deployment will be cautious, with senior compliance officers as the validation layer for escalations.

General ledger reconciler + Month-end closer + Statement auditor = corporate finance ops. Reconciles GL accounts, runs NAV calculations, prepares journal entries, runs close checklists, reviews statements for consistency. This is the corporate finance close cycle — work performed by accounting and finance ops teams at every public company plus dedicated close ops at fund administrators (SS&C, State Street, BNY Mellon, Northern Trust). The cohort impact: corporate finance ops headcount compresses approximately 25-40 percent in deployed AI environments. The Big Four accounting firms (Deloitte, PwC, EY, KPMG) face the same pattern — audit and advisory cohorts compress as the templates handle preparatory work that junior accountants traditionally performed.

Meeting preparer = client coverage. Assembles client and counterparty briefs ahead of calls. Meeting prep is the “invisible work” of relationship banking — the analyst pulling 20 documents, summarizing the client’s recent earnings, recent deals in their sector, recent news, recent macro context. The template handles this in 5 minutes versus 2 hours. The cohort impact: client coverage support headcount compresses; senior bankers spend more time client-facing rather than preparing for meetings.

The cumulative cohort displacement signal: approximately 150,000-300,000 financial services jobs over 3-5 years if deployment proceeds at the announcement-implied pace. This aligns with the Wall Street ~200K industry estimate covered in the labor displacement dispatch. Anthropic’s announcement is the productized acceleration of that displacement curve.

2. The provider impact ranking · who loses, who gains

The provider landscape impact runs across five distinct positions. Understanding the impact requires distinguishing between the data layer (where Anthropic doesn’t compete) and the interface layer (where Anthropic competes hard).

Most exposed · Bloomberg Terminal. ~$32,000 per year per seat for ~375,000 users globally, 33.2 percent mindshare in financial data analysis platforms (declining from 34.5 percent year-over-year per PeerSpot data). Bloomberg’s moat has always been the integrated UI over data + news + analytics + chat + messaging — the “Bloomberg ecosystem” that justifies the price premium. The structural threat: Claude Cowork as the analyst’s primary interface, pulling Bloomberg-equivalent data from FactSet/LSEG/Capital IQ/Moody’s via connectors, orchestrating across Excel/PowerPoint/Outlook. The analyst stops opening Bloomberg. The data underneath Bloomberg is reproducible from competitors. The chat function moves to Slack/Teams/Claude. The news function moves to dedicated AI summarization. The UI moat erodes.

Bloomberg’s defensive response is real and substantive. ASKB launched February 23, 2026, beta open to ~125,000 users (one-third of Terminal users), CTO Shawn Edwards explicitly framing it as “the new terminal. The primary way most interactions happen.” ASKB uses multiple LLMs under the hood including Anthropic — Bloomberg is hedging by integrating the same models that threaten its position. The roadmap update April 16, 2026 added agentic AI capabilities, ASKB Workflows for repeating multi-step tasks, integration with Third Bridge expert interviews, Bloomberg Second Measure alternative data. The Fortune coverage (April 28, 2026) framed it as “the biggest rethink of the terminal in Bloomberg’s history.”

The race specifics: Bloomberg’s data integration depth (decades of curated cross-asset coverage, alternative data, proprietary news) versus Anthropic’s orchestration breadth (Microsoft 365, all data providers via connectors, plus deployment as either plugin or autonomous Managed Agent). If Bloomberg’s response is fast enough, the Terminal survives as the primary platform with AI bolted in. If Claude Cowork wins the analyst desktop first, the Terminal becomes a data-source-among-many. The Fortune piece characterized the threat in unusually direct language: AI is “supercharging the competitive pressure on the company” as customers “can increasingly use AI to perform the kinds of modeling they once needed the terminal to do.”

Beneficiary · FactSet. 21.7 percent mindshare (rising from 20.2 percent year-over-year per PeerSpot). Already explicitly positioning around MCP integration as the standardized framework for connecting LLMs to FactSet data. FactSet has historically been Bloomberg’s distant-second competitor with strength in portfolio analytics and Excel integration. The orchestration-layer dynamic actually benefits FactSet — when Claude is the interface and data comes from connectors, FactSet’s data quality and depth become directly comparable to Bloomberg’s without the integrated-UI premium. FactSet’s Excel integration was always the second strongest behind Bloomberg’s; in the Claude-orchestrated world, that integration is increasingly handled by Claude itself, removing one of Bloomberg’s unique advantages.

Beneficiary · LSEG (Refinitiv/Eikon). Pushing AI-ready datasets through MCP and Databricks Marketplace. Similar dynamic to FactSet — when interface moves to Claude, data quality and breadth become the differentiator. LSEG’s Western European strength and Bloomberg’s relative weakness in European fixed income and OTC derivatives become more important when the UI advantage neutralizes.

Mixed · S&P Capital IQ. 6.1 percent mindshare (declining from 7.3 percent). Smaller footprint and more concentrated in private equity / investment banking workflows. The orchestration-layer dynamic is mostly neutral — Capital IQ’s data gets surfaced via connector, but the smaller absolute size means less revenue gain from increased usage. The risk: if Bloomberg’s defense fails and the broader market moves toward Claude-orchestrated workflows, Capital IQ benefits proportionally to its current share. The opportunity: if Capital IQ can position aggressively as “the M&A and PE data backbone” inside Claude’s pitch builder + valuation reviewer + KYC screener templates, share could increase.

Beneficiary · Moody’s (MCP app launch). Anthropic’s announcement specifically calls out Moody’s MCP app — proprietary credit ratings and data on 600+ million public and private companies. Moody’s gets distribution into thousands of finance firms via Claude rather than having to negotiate enterprise integration deals individually. The MCP app pattern (custom interactive UI directly inside Claude) is qualitatively different from the connector pattern — Moody’s tools live inside the Claude interface rather than being passive data sources. The competitive read: Moody’s just got first-mover advantage in the MCP-as-UI pattern that other rating agencies (S&P Global Ratings, Fitch) will need to match.

Beneficiary · Specialized vertical providers. The eight new connectors expand Claude’s data graph: Dun & Bradstreet (business identity), Fiscal AI (real-time fundamentals), Financial Modeling Prep (cross-asset data), Guidepoint (100K+ expert interview transcripts), IBISWorld (industry data), SS&C IntraLinks (deal rooms), Third Bridge (primary expert interviews), Verisk (P&C insurance data). For each, Claude becomes a distribution channel that surfaces their data into thousands of finance firms without per-firm enterprise sales. The economic effect varies — high-margin specialized data (Guidepoint expert interviews, Verisk insurance data) gains pricing power; commodity data faces commoditization pressure.

Disrupted · Private equity diligence vendors. The Model builder + Valuation reviewer + Statement auditor templates collectively address ~60-70 percent of standard PE diligence workflow. Vendors providing diligence support (specialized accounting firms, third-party diligence specialists, data room consultants) face direct displacement. The cohort impact extends beyond banks into the diligence ecosystem.

3. The 64.37 percent reality check

The Vals AI Finance Agent benchmark anchor matters because it sets the realistic expectation for what these templates actually deliver. State-of-the-art at 64.37 percent means approximately one in three professional finance-analyst questions is answered wrong by the best available model. The deployment implications follow directly.

For senior analysts as the validation layer. A senior banker with 15 years of experience can review Claude’s pitch builder output, identify the 30-35 percent of errors instantly through pattern recognition, correct them, and ship the deck. Net productivity gain is substantial — maybe 5-10× faster than starting from scratch. The error rate is acceptable because senior judgment catches it. This is the durable deployment pattern: AI as accelerator, senior human as validator.

For junior analysts trusting AI output. A 1st-year analyst without the experience to catch the errors ships a pitchbook with 30-35 percent of facts wrong. The error reaches the client. Reputational damage and regulatory exposure for the firm. This is the failure mode that compliance teams legitimately fear. The deployment must be structured to prevent it — which is why the announcement specifically emphasizes “users stay firmly in the loop—reviewing, iterating on, and approving Claude’s work before it goes to a client, gets filed, or is acted on.”

For autonomous Managed Agents. The Anthropic announcement positions Managed Agents as “running autonomously on the Claude Platform, for work that spans a whole book of deals or a nightly schedule.” For high-volume, low-stakes work (KYC screening with senior officer review of escalations only, GL reconciliation with exception flagging, market research synthesis for internal use), the 64.37 percent accuracy is acceptable because the human validation happens at exception level. For low-volume, high-stakes work (M&A modeling, credit decisions on large facilities, regulatory filings), the accuracy is not acceptable for autonomous deployment.

The benchmark trajectory matters. Vals data shows “significant improvement in the last six months” — the benchmark has been re-leveled to maintain difficulty. Models on average performed best on simple quantitative and qualitative retrieval tasks (the 80-90 percent range), worse on complex multi-step financial reasoning (the 40-50 percent range). The bull case for finance vertical deployment: accuracy continues improving 5-10 percentage points per major model release, reaching 80+ percent by 2027-2028 which is the threshold for autonomous deployment on most workflows. The bear case: the curve flattens at the 70-75 percent range as the remaining errors require human judgment that current architectures struggle with.

The liability allocation question. Major banks, asset managers, and insurers operate under regulatory frameworks (SR 11-7 model risk management at US banks, SOX, FINRA, SEC, CFTC, EU MiFID II, MAS, FCA, etc.) that impose specific accountability for analytical errors. AI-generated financial analysis exists in a gray zone — the bank is liable for the output, but the AI provider isn’t liable for the analysis quality. Anthropic’s announcement language (“users stay firmly in the loop—reviewing, iterating on, and approving”) is partly genuine deployment guidance and partly liability positioning. As deployment scales, the liability framework will be stress-tested.

4. The customer-facing implications

The downstream effects on customers of financial services firms vary substantially across customer tiers.

Corporate banking clients (large corporates, mid-market PE-backed companies). Faster pitch cycles. Investment banks can field pitchbooks to clients in days rather than weeks. The cost-per-pitch drops, which means banks pitch more aggressively for marginal opportunities. Marginal corporate clients (smaller mid-market, less-known companies in less-common sectors) get more banking attention because the cost-to-pitch is lower. The downside: pitch quality variance increases. Some Claude-generated pitches contain the 30-35 percent error rate visibly. Sophisticated corporate finance teams will calibrate trust accordingly. Less sophisticated corporate buyers may make worse decisions based on more confident-looking pitches that contain hidden errors.

Retail investors (wealth management, robo-advisors, individual brokerage). Trickle-down via better wealth management platforms. Goldman Sachs, JPMorgan, Morgan Stanley wealth divisions deploy similar AI tools to their advisor force, who deploy to retail clients. Retail customer experience improves through faster portfolio reviews, more proactive rebalancing recommendations, more personalized financial planning. The timeline for retail benefit is 12-36 months — wealth firms move slower than IB on AI deployment. The risk: retail investors trust outputs they shouldn’t trust. The 64.37 percent accuracy threshold matters for retail because retail investors lack the senior-judgment validation layer that protects institutional users.

Compliance and regulatory. KYC screener + Statement auditor templates change the regulatory liability allocation. When AI handles initial KYC screening, the question becomes: who is liable for missed flags? The bank (under existing rules), the AI provider (theoretically possible but contractually disclaimed), or some shared framework (under future rules). Regulatory response is forming. The Federal Reserve, OCC, and FDIC have been signaling expectations for AI risk management at banks. The EU is further along with explicit frameworks. Expect specific AI-in-finance regulatory guidance through 2026-2027 that establishes the liability framework.

Private equity. Model builder + Valuation reviewer templates disrupt the diligence process. Mid-market PE deals that historically required 6-8 weeks of diligence work could compress to 3-4 weeks. The diligence cost-per-deal drops, which means PE firms can pursue more marginal deals or use the saved capacity for deeper diligence on higher-stakes deals. The strategic implication: PE deal volume increases at the margins; deal quality may improve at the higher end. The disruption to diligence service vendors is direct and substantial.

Insurance industry (Verisk connector). P&C insurance underwriting workflows get AI augmentation through the Verisk data connector. Claude can pull property risk data, casualty claims history, specialty insurance data and integrate with the underwriting decision. The cohort impact within insurance: junior underwriter and claims-ops headcount compresses; senior underwriters become more productive. The customer experience: faster underwriting decisions, potentially more accurate risk pricing. The risk: AI-driven risk assessments contain biases or errors that affect pricing for specific demographics or geographies. State insurance regulators will scrutinize.

5. The competitive context · OpenAI’s parallel build

The Fortune coverage (April 28, 2026) revealed an important context point: OpenAI is reportedly building a competing agentic AI financial analysis product, with “a battalion of ex-investment analysts” helping develop it. The product hasn’t launched as of this writing. The competitive dynamic matters for reading Anthropic’s announcement timing.

Anthropic’s first-mover advantage. Shipping the productized templates today means banks and financial services firms can begin deployment immediately. The connector ecosystem (existing FactSet/S&P/MSCI/PitchBook/Morningstar/Chronograph/LSEG/Daloopa plus eight new) is the moat. OpenAI’s competing product, when it launches, will need its own connector ecosystem — and incumbent providers may find themselves choosing or supporting both Claude and OpenAI’s product, which weakens both relative to a single-orchestrator scenario.

The Microsoft 365 question. Anthropic’s Excel/PowerPoint/Word/Outlook add-ins are the most consumer-facing element of the announcement. Microsoft is OpenAI’s primary infrastructure partner ($30B Azure capacity, Anthropic disclosed in May 6 compute deal). Microsoft permitting Anthropic’s add-ins inside Office is operationally permissive but strategically interesting — Microsoft’s own Copilot for Microsoft 365 is the obvious competitor. The structural read: Microsoft is hedging its AI bets, not committing to OpenAI exclusivity for productivity scenarios. The financial services vertical is large enough that Microsoft tolerates dual integration.

Bloomberg’s hedging pattern. ASKB uses multiple LLMs including Anthropic models. Bloomberg is integrating with the same models that threaten its position. The pattern is rational — the data is Bloomberg’s moat; the model is interchangeable. If Anthropic, OpenAI, or Google produces the best model for a specific task, ASKB uses it. The structural implication: Bloomberg’s defense doesn’t depend on any specific model winning; it depends on Bloomberg’s data being indispensable. Whether the data alone is enough as the UI moat erodes is the live question.

The competitive bifurcation. Three patterns emerge for finance vertical AI deployment through 2026-2028: (1) Claude-orchestrated workflows where Claude Cowork is the analyst desktop and incumbent data providers are connected via MCP/connectors, (2) Bloomberg-orchestrated workflows where ASKB is the analyst desktop and other models are integrated under the hood, (3) custom enterprise deployments where banks build their own orchestration layer using a mix of Claude/GPT/Gemini APIs and incumbent data feeds. The market likely settles into all three patterns serving different customer segments.

6. The connections to other dispatches

The financial services announcement compounds with multiple structural threads.

Connection 1 · The labor displacement Q1-Q2 2026 dispatch. The dispatch covered the ~200K Wall Street jobs over 3-5 years industry estimate. Anthropic just shipped the productized version of that displacement curve. The mid-level analyst cohort (covered as “compressed” in the dispatch) gets specific evidence. The deployment timeline accelerates from “industry estimates” to “templates available today.”

Connection 2 · The Anthropic IPO disclosure. The dispatch covered enterprise penetration as a value driver. The financial services vertical is among the highest-value enterprise verticals globally — banks/asset managers/insurers spend $200B+ annually on technology. Capturing meaningful share of finance vertical AI spending materially strengthens Anthropic’s IPO valuation case. The Q3-Q4 2026 IPO window benefits.

Connection 3 · The compute reckoning (May 6 SpaceX deal). The dispatch covered the SpaceX Colossus 1 deal closing the capacity gap. Without that capacity, the finance vertical announcement would have hit immediate rate-limit issues at scale deployment. The May 6 / May 7 announcement timing is not coincidental — Anthropic needed compute capacity to support enterprise vertical scale before announcing enterprise vertical templates.

Connection 4 · The bubble question disentanglement. The dispatch flagged frontier-lab durable-value categories. Finance vertical penetration is concrete evidence for the durable-value reading — these are not speculative use cases, they are immediate productivity tools deployable to existing customer bases. The bull case for AI lab valuations gains specific evidence.

Connection 5 · Google I/O 2026 preview. The dispatch covers the May 19-20 event. Google’s Gemini Enterprise positioning competes directly with Anthropic’s vertical play. Watch for Google’s finance-vertical announcement at I/O — likely Gemini Enterprise + Workspace + finance-specific connectors. The competitive dynamic intensifies through Q2-Q3 2026.

Connection 6 · The agentic loop failure modes. The dispatch covered technical limitations of current agent deployment. The 64.37 percent Vals benchmark accuracy is the empirical evidence — agents fail more than one-third of the time on professional finance tasks. The deployment pattern (human-in-the-loop, senior validation, exception escalation) is the practical response to the technical limitation.

Connection 7 · The EU AI Act enforcement. The dispatch covered Q3-Q4 2026 enforcement activation. The EU AI Act classifies AI systems used for credit decisions and insurance underwriting as “high-risk,” requiring specific compliance. Anthropic’s deployment in EU financial services must navigate this framework — the announcement’s emphasis on “governed access controls” and “audit log in the Claude Console” reflects EU compliance positioning.

7. Three scenarios for finance vertical deployment 2026-2028

Bullish scenario · 30 percent probability · “Productivity wins, deployment scales, displacement is gradual.” Banks and asset managers deploy templates aggressively through 2026-2027. Senior analyst productivity 3-5× on covered workflows. Junior analyst hiring contracts gradually (15-25 percent annually) without mass layoffs as natural attrition handles cohort compression. Customer experience improvements are visible across corporate banking, wealth management, compliance. Bloomberg ASKB defense holds the Terminal share at ~30 percent mindshare; FactSet, LSEG, Moody’s gain share within a Claude-orchestrated workflow ecosystem. Vals benchmark accuracy improves to 75-80 percent by end of 2027. Regulatory framework develops cooperatively with industry input. The bull case for AI lab valuations bubble question dispatch gains evidence.

Base scenario · 50 percent probability · “Bifurcated deployment with regulatory friction.” Major banks deploy templates aggressively for back-office and middle-office work (KYC, GL reconciliation, statement audit, market research) where human-in-the-loop validation is straightforward. Front-office deployment for client-facing pitches and high-stakes M&A work proceeds more cautiously due to liability concerns. Cohort displacement reaches 100,000-150,000 jobs by end of 2028 in covered functions. Bloomberg ASKB and Anthropic’s orchestration layer coexist with different customer segments. Specific regulatory liability events produce framework refinement through 2027-2028. The base case for the bubble question frontier-lab valuations applies — substantive but bounded productivity translation.

Bearish scenario · 20 percent probability · “Liability event slows deployment substantially.” A high-profile regulatory failure or litigation event (a Claude-generated pitch contains a material misrepresentation that reaches a client and produces losses; a KYC screener miss results in an enforcement action; a model builder error produces incorrect M&A valuations) produces industry-wide deployment retreat. Major banks pull back to advisory-only AI use cases. Compliance and legal teams impose stricter human-validation requirements that erode productivity gains. Cohort displacement slows to 50,000-75,000 jobs by 2028. Vals benchmark accuracy improvement stalls at 70-72 percent. The bear case for the bubble question frontier-lab valuations gains support — productivity translation is real but slower and costlier than projected.

The 30/50/20 probability allocation reflects current setup. Setup factors favoring the bullish scenario: announcement-implied deployment readiness, multi-vendor connector ecosystem, demonstrated productivity gains at hedge funds and PE firms already using Claude. Setup factors favoring the bearish scenario: 64.37 percent accuracy still produces meaningful error rate, regulated-industry conservatism, compliance and legal team caution, demographic concentration of cohort displacement (junior analysts at major banks) creates political pressure.

8. The strategic implications by stakeholder

For banks and asset managers (deployment decisions). The deployment pattern that makes sense: senior-analyst-validated rather than autonomous. KYC and back-office GL reconciliation can scale faster than client-facing pitches. The ROI math favors aggressive deployment for back/middle office, cautious deployment for front office. Cohort headcount planning should reflect 15-25 percent annual contraction in junior analyst hiring and KYC ops over 2026-2028. Compliance and legal teams need to be in the deployment governance from the start, not bolted on afterward.

For Bloomberg, FactSet, S&P, LSEG, Moody’s. Bloomberg faces the most acute strategic challenge — UI moat erosion. The defense is real (ASKB) and the data depth is real, but the timeline pressure is severe. Other providers benefit from the orchestration-layer dynamic — their data gets surfaced into Claude’s interface without the Bloomberg ecosystem premium. The strategic question for each: how much to invest in Claude/Anthropic-specific integration versus building defensive UI of their own (LSEG’s Workspace, FactSet’s portal, Capital IQ Pro). Hybrid is most likely.

For specialized data providers (Verisk, IBISWorld, Dun & Bradstreet, etc.). First-mover advantage in MCP integration. The connector pattern provides distribution that historically required enterprise sales investment per firm. The pricing question is open — connector revenue could be lucrative if priced per-call or per-firm, neutral if priced per-Claude-subscription, dilutive if pure-promotional. Watch for revenue model disclosure as deployment scales.

For displaced cohorts (junior IB analysts, KYC ops, mid-level research). Reskilling toward AI-augmentation roles is the durable strategy. Vertical AI specialists (combining finance domain expertise with AI fluency) are the growing cohort covered in the labor displacement dispatch. Senior cloud / security / data engineering paths offer durable demand. Geographic flexibility helps — financial centers (NYC, London, Singapore, Hong Kong, Frankfurt) face the most concentrated displacement; secondary financial centers may face less.

For regulators and policymakers. The liability allocation framework needs explicit articulation. EU AI Act classification of credit decisions and insurance underwriting as high-risk applies; specific guidance for the Anthropic-pattern deployment is needed. US prudential regulators (Fed, OCC, FDIC) need to clarify SR 11-7 model risk management application to LLM-based agents. Securities regulators (SEC, FINRA, CFTC) need to address agent-generated research and pitch materials. Insurance regulators (state-level in US, EIOPA in EU) need to address AI-driven underwriting bias.

For investors. Bloomberg’s competitive position is a specific stock-level question. FactSet, LSEG (LSE Group ticker), S&P Global, Moody’s all have public equity exposure. The orchestration-layer dynamic is mostly bullish for non-Bloomberg providers, mixed for Bloomberg (private but valuation discussed). Anthropic’s IPO valuation case strengthens with finance vertical penetration.

What to Do This Quarter (Through Q3 2026)

1. Banks and asset managers. Deploy back/middle office templates (KYC screener, GL reconciler, month-end closer, statement auditor) aggressively. Deploy front-office templates (pitch builder, model builder, valuation reviewer) cautiously with senior validation. Plan cohort headcount with 15-25 percent annual contraction in affected junior roles.

2. Data providers. Bloomberg should accelerate ASKB rollout and emphasize data-depth differentiation. FactSet, LSEG, Moody’s should aggressively position MCP/connector integration. Specialized vertical providers should pursue first-mover advantage in their domain.

3. Displaced cohorts. Reskill toward AI-augmentation roles — vertical AI specialists, senior cloud/security engineering, AI safety. The Atlassian template (cut + AI-hire rebalance) is the durable employer model. Geographic flexibility expands options.

4. Investors. Update Bloomberg-competitive-position models for FactSet/LSEG/S&P Global/Moody’s. Update Anthropic IPO valuation case for finance vertical penetration. Watch Google I/O May 19-20 for Gemini finance vertical response.

The Strategic Read

Anthropic released ten ready-to-run agent templates for financial services this week — Pitch builder, Meeting preparer, Earnings reviewer, Model builder, Market researcher, Valuation reviewer, GL reconciler, Month-end closer, Statement auditor, KYC screener — paired with Microsoft 365 add-ins (Excel, PowerPoint, Word generally available; Outlook coming), eight new data connectors (Dun & Bradstreet, Fiscal AI, Financial Modeling Prep, Guidepoint, IBISWorld, SS&C IntraLinks, Third Bridge, Verisk), and Moody’s first MCP app. Powered by Claude Opus 4.7, state-of-the-art on Vals AI Finance Agent benchmark at 64.37 percent.

The strategic positioning is clearer than the headline framing suggests. Anthropic isn’t competing with Bloomberg Terminal — Anthropic is positioning Claude as the orchestration layer over Bloomberg-class data providers. The connector list (existing FactSet, S&P Capital IQ, MSCI, PitchBook, Morningstar, Chronograph, LSEG, Daloopa plus eight new) is the moat. Claude becomes the analyst’s primary interface, pulling from the entire competitive landscape of financial data providers, then orchestrating across Excel/PowerPoint/Outlook. The data layer stays where it is. The interface layer moves to Claude Cowork.

The provider impact is uneven and structurally significant. Bloomberg Terminal is most exposed — $32K/seat moat was always the consolidated UI over data + news + analytics + chat + messaging. If Claude Cowork wins the analyst desktop, the UI moat erodes. Bloomberg’s defensive response is ASKB (launched February 23, 2026, beta open to ~125K of 375K users, CTO framing as “the new terminal”). FactSet (21.7 percent mindshare, rising), LSEG (AI-ready datasets through MCP), Moody’s (first MCP app), and specialized providers (Verisk, IBISWorld, etc.) benefit from the orchestration-layer dynamic — their data gets surfaced without Bloomberg’s integrated-UI premium.

The 64.37 percent benchmark figure deserves precise reading. State-of-the-art at 64.37 percent means approximately one in three professional finance-analyst questions is answered wrong by the best available model. The deployment implications: senior analysts as validation layer is the durable pattern (substantial productivity gain because senior judgment catches errors); junior analysts trusting AI output is the failure mode (errors reach clients, regulatory exposure); autonomous Managed Agents work for high-volume low-stakes operations (KYC screening, GL reconciliation) but not for low-volume high-stakes operations (M&A modeling, large credit decisions, regulatory filings). Vals benchmark trajectory shows 5-10 percentage points improvement per major model release — 75-80 percent accuracy by 2027-2028 is plausible but not guaranteed.

The ten templates map cleanly to specific bank job functions, making the cohort displacement signal direct. Pitch builder = junior IB analyst (5-6K hires per year industry-wide pre-AI, already contracting 15-25 percent in 2025-2026). Model builder + Valuation reviewer = associate / VP-level (slower contraction, higher work-per-headcount expectations). Earnings reviewer + Market researcher = sell-side / buy-side equity research (40-60 percent routine work displacement). KYC screener = compliance ops (5-15K+ per major bank, 30-50 percent reduction potential over 18-36 months). GL reconciler + Month-end closer + Statement auditor = corporate finance ops (25-40 percent compression). Cumulative cohort displacement: 150,000-300,000 financial services jobs over 3-5 years — aligns with Wall Street ~200K industry estimate.

Customer-facing implications run across four tiers. Corporate banking clients benefit from faster pitch cycles but face quality variance risk. Retail investors benefit through trickle-down wealth management improvements (12-36 month timeline). Compliance and regulatory frameworks need explicit liability allocation articulation — EU AI Act high-risk classification applies to credit and insurance underwriting; US prudential regulators need SR 11-7 clarification. Private equity diligence cycles compress 30-50 percent; PE diligence service vendors face direct displacement.

The competitive context is intensifying. OpenAI is reportedly building competing agentic financial analysis product with “battalion of ex-investment analysts” (per Fortune April 28). Microsoft permits Anthropic’s Office add-ins despite primary OpenAI relationship — hedging across AI vendors. Bloomberg’s ASKB uses multiple LLMs including Anthropic — hedging by integrating threats. Three deployment patterns emerge for 2026-2028: Claude-orchestrated, Bloomberg-orchestrated, custom enterprise. Market settles into all three serving different customer segments.

Three scenarios resolve through 2026-2028. Bullish (30 percent): productivity wins, deployment scales, gradual displacement, regulatory framework develops cooperatively. Base (50 percent): bifurcated deployment — back/middle office aggressive, front office cautious due to liability; 100-150K cohort displacement by 2028. Bearish (20 percent): high-profile liability event slows deployment substantially; deployment retreats to advisory-only; 50-75K cohort displacement; productivity translation real but slower than projected.

The connections to broader threads run deep. The labor displacement Q1-Q2 2026 data dispatch gets specific evidence. The Anthropic IPO disclosure case strengthens through finance vertical penetration. The May 6 compute reckoning enabled the May 7 vertical scaling. The Google I/O 2026 preview gets a competitive context — Gemini finance vertical response likely at May 19-20. The agentic loop failure modes get empirical confirmation — 64.37 percent accuracy is the visible expression of the technical limitation.

The deeper signal: the financial services vertical is the highest-stakes proving ground for production AI deployment. Bank balance sheets, regulatory liability, customer trust in financial advisors — these are existential constraints that test whether AI productivity translation is real. Anthropic’s announcement is the productized version of the deployment thesis. Whether the 64.37 percent accuracy is sufficient for the deployment patterns implied determines whether the bullish or bearish scenario materializes. Whether Bloomberg’s ASKB defense holds determines whether the orchestration-layer thesis dominates or coexists with the integrated-data-platform thesis. Whether regulatory framework develops cooperatively or punitively determines the deployment pace.

The honest assessment: the most likely scenario is the base case — bifurcated deployment with regulatory friction. Back-office and middle-office templates deploy aggressively in 2026-2027 because the human-validation pattern is straightforward. Front-office deployment proceeds more cautiously through 2027-2028 as liability frameworks mature. The probability of either tail outcome (smooth absorption or acute retrenchment) is meaningful but lower. The structural insight: Anthropic just shipped the most aggressive vertical AI play any frontier lab has attempted, and the financial services industry is the most consequential vertical to test against. The next 18-24 months reveal whether the orchestration layer architecture scales as advertised.

Anthropic released 10 finance agent templates · Microsoft 365 add-ins (Excel/PowerPoint/Word GA, Outlook coming) · 8 new connectors + Moody’s MCP app. Claude Opus 4.7 leads Vals Finance Agent benchmark at 64.37%. Strategic positioning: orchestration layer over Bloomberg-class data providers, not direct competitor. Bloomberg most exposed (UI moat erosion); FactSet/LSEG/Moody’s/specialized providers benefit. 64.37% accuracy = one-in-three professional finance questions answered wrong → senior validation pattern is durable, junior trust is failure mode. Cohort displacement maps to 10 templates: 150-300K Wall Street jobs over 3-5 years. Three scenarios with 30/50/20 probability. Base case: bifurcated deployment with regulatory friction.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The Compute Reckoning · Anthropic-SpaceX Deal

- The Labor Displacement Q1-Q2 2026 Data

- The Google I/O 2026 Preview

- The Anthropic IPO Disclosure Document

- The Bubble Question, Disentangled

- The Agentic Loop Failure Modes

Sources

- Anthropic · Claude for Financial Services · 10 agent templates + Microsoft 365 add-ins + 8 new connectors · May 7, 2026 — primary announcement

- Vals AI · Finance Agent v1.1 benchmark · Claude Opus 4.7 64.37% (state-of-the-art); Sonnet 4.6 63.33%; Muse Spark 60.59%; DeepSeek V4 60.39%; Opus 4.6 (Thinking) 60.05%

- Vals AI methodology · Quality control by Goldman Sachs / Silver Lake / Citadel experts; 537 questions on equity research / credit / due diligence on SEC filings

- Anthropic · Claude Opus 4.7 release · April 16, 2026; $5/$25 per million tokens; 1M context; 128K output; xhigh effort tier

- PeerSpot Financial Data Analysis Platforms · Bloomberg Terminal 33.2% mindshare (down from 34.5%); FactSet 21.7% (up from 20.2%); S&P Capital IQ 6.1% (down from 7.3%); March 2026

- Bloomberg · Meet ASKB · Bloomberg Introduces Agentic AI to the Bloomberg Terminal · February 23, 2026

- Bloomberg · ASKB Roadmap update · April 16, 2026 · Multiple LLMs including Anthropic; ~125K beta users out of 375K Terminal users

- Wired / Bloomberg CTO Shawn Edwards · “This will be the new terminal. The primary way most interactions happen.” · April 28, 2026

- Fortune · Bloomberg, the OG of financial data firms, has a potent new AI agent · April 28, 2026 · “AI is supercharging the competitive pressure”

- Trading Dude (Medium) · Financial Data in 2026 · Bloomberg Terminal pricing ~$32,000/year per seat

- Investopedia · Bloomberg Terminal historical pricing context · 315K users (2013) to 375K (2026)

- LSEG · AI-ready datasets through MCP and Databricks Marketplace

- FactSet · MCP positioning as standardized framework for connecting LLMs to FactSet data

- Vellum / Build Fast With AI / LLM-Stats · Claude Opus 4.7 benchmark analysis · April 2026 release

- Marc0.dev · SWE-Bench Verified Leaderboard March 2026 · GPT-5.5 88.7% (#1), Claude Opus 4.7 87.6% (#2)

- Wall Street ~200,000 jobs over 3-5 years industry estimate (covered in labor displacement dispatch)

- EU AI Act · High-risk classification for credit decisions and insurance underwriting