By Thorsten Meyer — May 2026

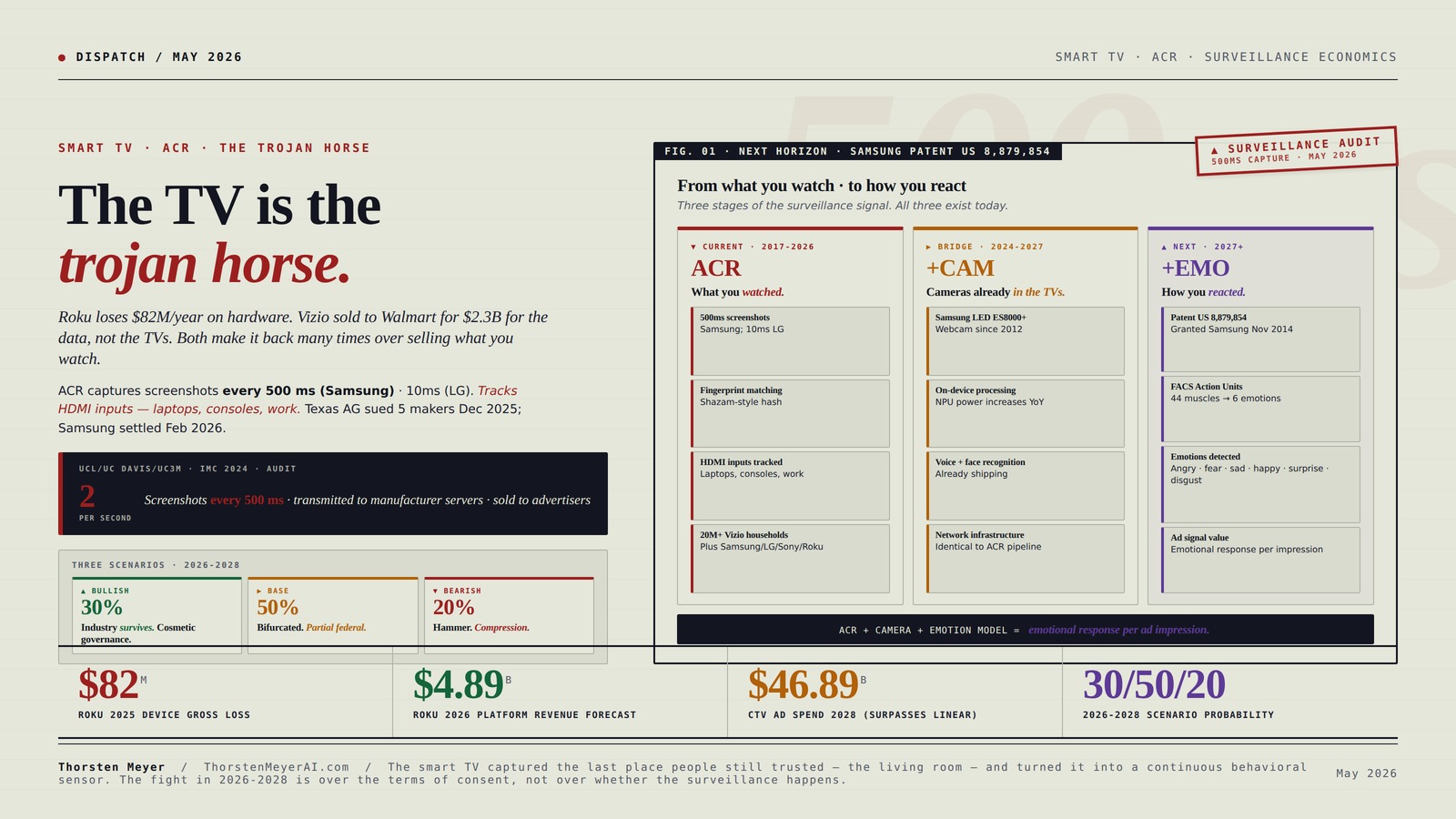

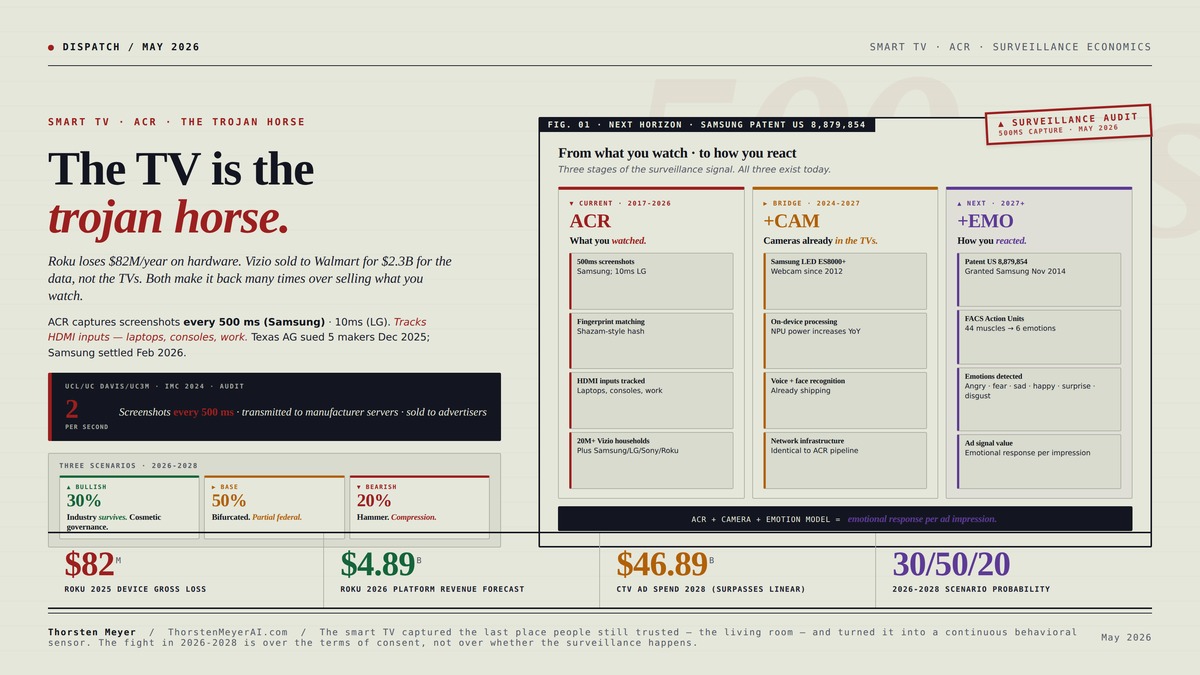

The economics tell you everything, if you know where to look. Roku’s device segment ran a gross loss of approximately $82 million in 2025 — devices gross margin negative 13.8 percent in Q1 2025, deteriorating to negative 23.3 percent by Q4. The 2026 forecast: device revenue ~$610 million with gross margin in the negative mid-teens, “roughly in line with 2025” per the company’s own guidance. Vizio reported similar economics through the Inscape ACR-powered Platform+ business — until Walmart acquired the entire company for $2.3 billion in December 2024 specifically because the platform data, not the hardware, was the asset. Both companies are paying you to take their televisions home. The TV is the trojan horse. The ad business is the actual product.

The mechanism is called Automatic Content Recognition. Your smart TV captures a miniature screenshot of your screen every 500 milliseconds — twice per second on Samsung. LG’s documented capture rate is 10 milliseconds, with a configuration file showing a 48,000 Hz audio sample rate against a 60 Hz display refresh rate, suggesting the TV records sound and image many thousands of times more often than it shows you new pixels. The screenshots are converted into perceptual fingerprints — Shazam-style hashes that don’t store the image itself but encode enough signal to match against a content library. Samsung batches and transmits the fingerprints once per minute. LG transmits every 15 seconds. The fingerprint network identifies precisely what’s on your screen — broadcast TV, streaming, video game, work presentation displayed via HDMI from your laptop, anything. Then it sells that signal to advertisers. This is verified by peer-reviewed academic research from University College London, UC Davis, and Universidad Carlos III de Madrid published at the 2024 ACM Internet Measurement Conference. It is verified by Samsung’s own technical documentation. It is verified by the Texas Attorney General’s December 2025 lawsuits against Samsung, LG, Sony, Hisense, and TCL.

The regulatory arc is now visible. In 2017, the FTC and New Jersey Attorney General settled with Vizio for $2.2 million over ACR data collection on 11 million households. The settlement was a slap on the wrist. The industry took it as a green light to proceed with disclosure-then-monetize patterns. In November 2024, the UCL/UC Davis/UC3M paper provided the first independent peer-reviewed network audit. In December 2025, Texas AG Ken Paxton filed five separate lawsuits against the major manufacturers — alleging that consumers were “automatically enrolled in this system using dark patterns” requiring “over 200 clicks spread across four or more menus” to access privacy disclosures. In January 2026, the FTC finalized its GM/OnStar order — a structurally identical pattern in a different industry, where connected vehicles collected geolocation data without informed consent and sold it to third parties. In February 2026, Samsung became the first smart TV manufacturer to settle with Texas. No monetary penalty. Required to obtain “express consent” before ACR data collection. Required to rewrite consent screens to be “clear and conspicuous.” Sony, LG, Hisense, and TCL are still fighting. Hisense remains under restraining order. The other three are free to keep capturing screenshots every 500 milliseconds — until they lose or settle too.

The connected TV ad market is approximately $33.35 billion in the U.S. in 2025, projected to reach $37.95 billion in 2026 (~14 percent year-over-year growth), and $46.89 billion by 2028 — surpassing traditional TV advertising for the first time. By 2029 the figure is approximately $51 billion. The structural anomaly: viewers are growing faster than advertiser investment. CTV captures 20.2 percent of time spent with media in 2025 but attracts only 7.7 percent of total ad spend. The gap is the engine driving the next five years of growth. Every percentage point of ad-spend share migrating from linear TV to CTV is roughly $1 billion in revenue moving toward the platforms that own the surveillance infrastructure — Roku, Vizio (now Walmart), Samsung, LG, Sony, plus the CTV publishers (YouTube, Amazon Prime Video, Disney+/Hulu, Netflix, Paramount+).

This dispatch is the structural read on what the smart TV surveillance economy actually is, where the data goes, what the regulatory enforcement looks like in 2026, and what’s already patented for the next horizon. The next horizon is biometric. Samsung was granted U.S. Patent 8,879,854 in November 2014 for a “method and apparatus for recognizing an emotion of an individual based on facial action units.” The patent describes a system that takes facial expressions, decomposes them into FACS (Facial Action Coding System) Action Units, and outputs an emotion label across six categories: angry, fear, sad, happy, surprise, disgust. Combined with ACR, the advertising signal evolves from “what you watched” to “how you reacted to each specific ad.” That’s the trillion-dollar measurement holy grail — emotional response per impression, in real time, in your living room.

The dispatch on labor displacement covered the productivity-translation thesis for AI in knowledge work. The dispatch on the bubble question covered durable-value categories versus frothy ones. Smart TV surveillance is one of the most durable AI-driven business models on the planet — it’s been monetizing for a decade, generates 51-52 percent gross margins, and the regulatory backstop has been weak enough that the practice continued for nine years between the 2017 Vizio settlement and the 2025 Texas lawsuits. The deeper read connects to the EU AI Act enforcement framework — biometric data and emotion recognition fall under high-risk categories with extensive governance requirements that the U.S. regulatory environment doesn’t yet match.

The TV is the

trojan horse.

Roku loses $82M/year on hardware. Vizio sold to Walmart for $2.3B for the data, not the TVs. Both make it back many times over by selling what you watch.

ACR captures screenshots every 500 milliseconds (Samsung) · 10ms image / 48 kHz audio (LG). Tracks HDMI inputs — laptops, consoles, work presentations. Opt-out requires 200+ clicks across 4+ menus. Texas AG sued 5 manufacturers Dec 2025; Samsung settled Feb 2026 with no monetary penalty. Patent for next horizon — emotion recognition — granted to Samsung in 2014.

Hardware bleeds. Platform prints.

The financial filings tell the story. The TV is sold below cost. The ARPU recovers the loss many times over through advertising and data sales.

- Q1-Q4 2025 margin-13.8% → -23.3%

- Q1 2026 estimate-28.6%

- 2026 guidance$610M revenue, neg mid-teens margin

- Mgmt framing“Treats devices as loss leader for platforms”

household

- Gross margin51-52% · 2026 guidance

- Growth rate+18% YoY

- Revenue mix87.7% of total revenue

- SourceAds + streaming rev share + data sales

Magicmoon 2-Pack 24 Inch Computer Privacy Screen Filter for 16:9 Monitor

- Compatible Model: For 24-inch widescreen monitors

- Privacy Enhancement: Darkens screen from side angles

- Adjustable Privacy Level: Modify brightness to change privacy

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Eight moments. One steepening curve.

Nine years of effective non-enforcement after the 2017 Vizio settlement. The November 2024 UCL paper provided the empirical foundation. Texas filed thirteen months later.

![TOLUOHU [3 Pack] Case for Vizio XRT136 Remote Control, Smart TV Remote Cover With Lanyard (Shockproof/Anti-Slip/Lightweight) - Glow Skin Sleeve](https://m.media-amazon.com/images/I/51dzWTKkkmL._SL500_.jpg)

TOLUOHU [3 Pack] Case for Vizio XRT136 Remote Control, Smart TV Remote Cover With Lanyard (Shockproof/Anti-Slip/Lightweight) – Glow Skin Sleeve

- Removable Hand Lanyard: Includes detachable hand strap for easy carrying

- Glow in the Dark: Green and blue cases glow after light exposure

- Multiple Colors: Set includes 3 different colors for easy identification

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

From what you watch. To how you react.

The patent was granted in November 2014. Combined with ACR, the advertising signal evolves from “what you watched” to “how you reacted to each specific ad” — emotional response per impression at population scale.

- 500ms screenshotsSamsung; 10ms LG

- Fingerprint matchingShazam-style perceptual hash

- HDMI inputs trackedLaptops, consoles, work

- 20+ million Vizio householdsPlus all Samsung/LG/Sony/Roku

- Samsung LED ES8000+Webcam since 2012

- On-device processingNPU power increases YoY

- Voice + face recognitionAlready shipping features

- Network infrastructureIdentical to ACR pipeline

- Patent US 8,879,854Granted Samsung Nov 2014

- FACS Action Units44 facial muscles → 6 emotions

- Emotions detectedAngry · fear · sad · happy · surprise · disgust

- Ad signal valueEmotional response per impression

Brvlsoc Vinyl Webcam Covers – Restickable Privacy Stickers for Laptop, Smartphone, Tablet, Smart TV & Game Console – Black, Multiple Sizes

- Privacy Protection: Solid black vinyl webcam covers

- Device Compatibility: Multiple sizes for all devices

- Reusable & Residue-Free: Restickable without residue

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios. One question.

Whether the regulatory enforcement curve continues steepening or plateaus at the Texas-Samsung template. 30/50/20 probability allocation reflects the structural setup.

- Samsung template propagatesSony, LG settle by end-2026.

- 60-75% opt-in ratesConsent dialog is only friction.

- 10-20% ARPU compressionAbsorbed via more aggressive inventory.

- Next horizon proceedsEmotion recognition rolls out 2027-28.

- Outcome: Surveillance economy survives; cosmetic governance only.

- 5-10 states adopt templateCA, NY, CO, WA follow Texas.

- FTC partial action 2027Subset of manufacturers.

- EU enforcement materializes$200-500M fines per major.

- Class actions $300-800MPer-manufacturer settlements.

- Outcome: CTV market $44B 2028 vs $46.89B projection.

- Major data breach or harm caseCatalyzes federal legislation.

- 40-60% opt-out rates30-50% ARPU compression.

- Next horizon stallsEmotion recognition prohibited.

- Walmart impairment$2.3B Vizio acquisition write-down.

- Outcome: CTV market $40B 2028 vs $46.89B projection.

The smart TV is the most successful Trojan horse in consumer electronics history. It captured one of the last places people still trusted — the living room — and turned it into a continuous behavioral sensor for the global advertising market. The fight in 2026-2028 is over the terms of consent, not over whether the surveillance happens.

43 Inches Privacy Screen Filter for Widescreen 16:9 TV Monitor | Privacy Shield | Anti-Glare | Anti-Blue light TV Protector | Eye Protection | Anti Spy | Computer Security Private Filter Protector

- Size and Compatibility: Fits 43-inch widescreen monitors

- Privacy and Glare Protection: Blocks side view, reduces glare

- Eye and Blue Light Protection: Protects eyes from harmful light

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Disable ACR. Treat firmware updates as resets.

Samsung “Viewing Information Services” off. LG “Live Plus” off. Sony “Samba Interactive TV” off. Vizio “Viewing Data” off. Block ACR endpoints at DNS layer (Pi-hole, NextDNS) for defense-in-depth. Isolate TV on its own VLAN if your network supports it. Consider not connecting the TV to internet at all if you watch through a separate streaming device.

Position based on 30/50/20 scenarios.

Roku, Walmart (post-Vizio), CTV-platform ecosystem face material regulatory tail risk through 2027-2028. Samsung Texas template lacks monetary penalty (manufacturer-friendly precedent). But the regulatory curve is steepening from 2017 → 2024 → 2025-2026 → present. Hisense and TCL face additional Chinese-ownership market-access risk in the U.S.

Adopt the Samsung template voluntarily.

Sony, LG, Hisense, TCL — voluntary adoption is cheaper than litigation. Hisense’s restraining order is the warning shot. The Samsung settlement requires no monetary penalty but does require explicit consent and rewriting consent screens. Most cost-effective compliance is to roll out updated consent flows nationally rather than maintain state-specific variants. The “California effect” applies.

Establish federal connected-device framework.

State-by-state enforcement is structurally inefficient. The FTC GM/OnStar template (20-year order, 5-year CRA-sharing ban, affirmative consent, deletion rights) is structurally appropriate for smart TVs. EU AI Act biometric provisions provide the template for the next-horizon emotion-recognition framework. Federal action through 2026-2027 is the logical extension of the Samsung template.

Executive Summary · The Surveillance Economics in One Table

| Element | Data point | Source |

|---|---|---|

| Roku 2025 device gross margin | Negative 13.8% (Q1) to -23.3% (Q4) | Roku 8-K, Feb 2026 |

| Roku 2025 device gross loss | ~$82 million | Roku FY 2025 results |

| Roku 2026 device guidance | -610M revenue, negative mid-teens margin | Roku 2026 outlook |

| Roku 2026 platform revenue guidance | $4.89 billion · 51-52% gross margin | Roku 2026 outlook |

| Vizio Platform+ revenue (2025E) | ~$750M projected, ARPU >$40/user | Vizio analyst data |

| Vizio Inscape ACR coverage | 20+ million TVs | Vizio NewFronts |

| Walmart-Vizio acquisition | $2.3 billion · December 2024 | Walmart deal |

| ACR capture rate (Samsung) | Every 500 milliseconds | UCL/UC Davis/UC3M IMC 2024 paper |

| ACR capture rate (LG) | 48 kHz audio · ~10ms screenshots | UCL audit + LG config |

| ACR transmission (Samsung) | Once per minute (batched) | UCL black-box network audit |

| ACR transmission (LG) | Every 15 seconds | UCL black-box network audit |

| HDMI tracking confirmed | Yes — works on laptops, consoles | UCL paper |

| 2017 Vizio FTC settlement | $2.2M · 11M households tracked | FTC press release |

| Texas AG lawsuits filed | December 15, 2025 · 5 manufacturers | Texas AG petition |

| Samsung Texas settlement | February 26, 2026 · no monetary penalty | Texas AG announcement |

| FTC GM/OnStar parallel | January 14, 2026 · 20-year order | FTC finalization |

| CTV ad spend 2025 | $33.35 billion (US) | eMarketer / MNTN Research |

| CTV ad spend 2028 | $46.89 billion · surpasses linear TV | eMarketer projection |

| CTV ad spend 2029 | $51 billion | eMarketer projection |

| Time-spent vs ad-spend gap | 20.2% time / 7.7% spend | eMarketer |

| Samsung emotion-recognition patent | US 8,879,854 · 6 emotions from FACS AUs | USPTO |

| Patent grant date | November 4, 2014 | USPTO |

The cumulative picture: the smart TV surveillance economy is not an emerging concern — it is a mature, multi-billion-dollar business that has been monetizing for nearly a decade with minimal regulatory friction. The 2025-2026 enforcement wave is the first material check on the practice. The next horizon (emotion recognition) has been patented for over a decade and waits for technical maturity and regulatory permission to deploy at scale.

1. The hardware-loss-leader economics

The economic structure is unambiguous when you read the financial filings. Roku’s most recent annual report disclosure, per the 8-K filed February 2026, shows the device segment running deep negative gross margins quarter after quarter: -13.8 percent in Q1 2025, -15.7 percent in Q2, -23.3 percent in Q4. The Q1 2026 estimate worsens to -28.6 percent. The cumulative 2025 device gross loss was approximately $82 million on $592 million in device revenue. Management’s own framing: “Roku treats its Devices business as a loss leader for the Platforms side of the house.”

The platform side is the actual business. Roku’s 2026 guidance: platform revenue $4.89 billion (up 18 percent year-over-year), with gross margin between 51 and 52 percent. That’s approximately $2.5 billion in platform-segment gross profit annually — derived from advertising, subscription revenue-sharing with streaming services, and data sales. The full-year picture: platform revenue is 87.7 percent of Roku’s total revenue. Devices are 12.3 percent of revenue and a structural cost center. The company is paying customers (in the form of below-cost hardware) to acquire households for the advertising business.

Vizio’s economics followed the same pattern with even more visibility, until Walmart acquired the company for $2.3 billion in December 2024. The strategic logic of the acquisition was explicit: combine Vizio’s Inscape ACR data on 20+ million households with Walmart’s retail purchase data on approximately 90 percent of U.S. households. The integrated dataset allows advertisers to do something previously impossible — observe a TV ad impression, observe the household’s subsequent retail purchases, and close the loop on attribution at the household level. The deal was not paying $2.3 billion for a TV manufacturer. It was paying $2.3 billion for the largest retail-plus-viewing-data integration in the world.

The structural pattern repeats across the manufacturer category. Samsung’s TV business runs at thin hardware margins offset by Samsung Ads platform revenue. LG runs Channels and webOS ad inventory. Sony’s Bravia platform monetizes through similar mechanisms. Hisense and TCL — both Chinese-owned — operate at even thinner hardware margins and rely on platform/data revenue. Each company is a hardware manufacturer in name only. The core business is the data and ad platform that lives on the hardware.

The unit economics of the hardware loss leader are stable because the customer relationship is durable. The average smart TV is owned for 7-10 years. Each year of ownership generates approximately $40-80 in platform ARPU (Vizio’s 2024 ARPU exceeded $40 and is rising). A $300 TV sold at $30 hardware loss generates $400-800 in platform revenue over its lifetime. The math is unambiguous. Hardware is the customer acquisition cost; platform revenue is the lifetime value; the LTV/CAC ratio is roughly 13-25x. No business model in consumer electronics produces returns like this. The closest analog is the smartphone advertising model that built Google’s and Meta’s dominance over the past decade.

2. How ACR actually works · the technical mechanics

The peer-reviewed paper “Watching TV with the Second-Party: A First Look at Automatic Content Recognition Tracking in Smart TVs” (Mandalari et al., ACM IMC 2024) provides the first independent network audit of ACR transmission. The methodology: connect Samsung and LG smart TVs to a dedicated internet hub in both the UK and US; capture the network traffic in real time; analyze when, what, and how often data leaves the device. The findings:

The capture rate. Samsung’s official documentation describes a capture frequency of every 500 milliseconds — two screenshots per second. LG’s configuration file reveals a 48 kHz audio sample rate, suggesting capture of 48,000 audio snapshots per second against a display refresh rate of 60 Hz. The Texas Attorney General’s complaint cites LG capturing “every sound and image on their Smart TV every 10 milliseconds.” The discrepancy between sources reflects the difference between (a) image frame capture rate, (b) audio sample rate, and (c) actual on-device fingerprint generation rate. All three are vastly higher than the network transmission rate.

The fingerprint generation. Each captured screenshot is processed locally on the TV. Samsung’s documented process: take “glass-level screenshots every 500 milliseconds, convert them into unique patterns, and compare these visual snapshots against others in the reference library.” This is Shazam for video — the local processing produces a perceptual hash that uniquely identifies the content without requiring transmission of the actual screenshot. Audio fingerprints work similarly, encoding the spectral signature of the sound rather than the audio itself. The local-processing design is a privacy feint: it’s true that the TV doesn’t transmit the actual screenshot, but it transmits a fingerprint that is precisely sufficient to identify what’s on screen.

The transmission rate. Samsung batches the fingerprints and transmits to the manufacturer’s servers approximately once per minute. LG transmits every 15 seconds. Both rates are continuous as long as the TV is on. The transmission includes the matched content identifier, timestamp, and device-level identifiers that enable household-level data linkage with other ad-tech datasets.

The HDMI capture confirmation. This is the most consequential finding from the UCL/UC Davis/UC3M paper. The ACR system runs continuously on the TV regardless of input source. When the TV is used as an external monitor for a laptop, gaming console, work presentation, Apple TV, Roku stick, cable box, or any HDMI-connected device, the ACR system captures the screen content the same way. The TV doesn’t know it’s “just a monitor” — it captures, fingerprints, and transmits whatever appears on glass. The privacy implications extend far beyond television viewing. Anything displayed on the TV — including content the user might consider entirely outside the TV manufacturer’s purview — feeds the ACR pipeline.

The opt-out mechanics. ACR is enabled by default on every major smart TV platform. The opt-out is buried under deliberately vague feature names: “Viewing Information Services” (Samsung), “Live Plus” (LG), “Samba Interactive TV” (Sony), “Viewing Data” (Vizio). The Texas AG’s December 2025 complaint against Samsung specifically noted that disabling required “over 200 clicks spread across four or more menus.” Even disabled, firmware updates can reset the toggles. The legal characterization in the Texas filing was “dark patterns.” The technical characterization is the same: enrollment is one click, exit is two hundred.

The data destination. Captured ACR data flows to: (1) the manufacturer’s first-party data platform (Samsung Ads, LG Ad Solutions, Vizio Inscape, Roku’s data platform); (2) ad-tech intermediaries (DSPs, SSPs, programmatic exchanges, attribution measurement vendors); (3) data brokers (Acxiom, Experian, LiveRamp, Oracle Data Cloud); (4) advertisers directly through identity-resolution services. The household-level data is matched against device IDs, IP addresses, household demographic data, and increasingly, retail purchase data (the explicit logic of Walmart’s Vizio acquisition).

The cumulative system: every smart TV operates as a continuous viewing-fingerprint sensor that feeds an ad-targeting and attribution graph spanning hundreds of millions of U.S. households. The technical capability is mature. The opt-out is practically unavailable. The regulatory framework is only beginning to catch up.

3. The 2025-2026 enforcement wave · why now

The regulatory pattern is finally shifting after nearly a decade of effective non-enforcement. The 2017 Vizio settlement — $2.2 million paid by the FTC and New Jersey AG over data collection on 11 million households — was the warning shot that the industry took as a green light. The settlement amount, ~20 cents per household, established the price of getting caught at a level that simply didn’t deter the practice. The economic trade was obvious: collect data, monetize it for billions, pay the occasional millions in fines, continue collecting.

What changed in 2024-2025 was the empirical foundation. The November 2024 UCL/UC Davis/UC3M peer-reviewed paper provided the first independent network audit demonstrating ACR transmission patterns. The paper made the practice undeniable in technical detail, in venues that regulators read. Within thirteen months, Texas AG Ken Paxton filed five separate lawsuits against the major manufacturers. The TROs against Hisense and Samsung followed within weeks. The Samsung settlement followed on February 26, 2026.

The Samsung settlement structure is informative about the next phase. Samsung agreed to: (1) halt ACR data collection and processing without express consent of Texas consumers; (2) implement disclosures and consent screens that are “clear and conspicuous”; (3) replace the “dark patterns” UI with affirmative opt-in flows. No monetary penalty was disclosed. Samsung’s public position was that its existing practices “complied with existing Texas state regulations” — a notable admission that the legal threshold was simply not yet there. The settlement is template-shaped: it provides the framework that other manufacturers and other states can follow without bearing the litigation cost. The “California effect” applies — Samsung is most likely to roll out the new consent flows nationally because supporting one set of consent UIs is cheaper than maintaining state-by-state variants.

The remaining four manufacturers. Sony, LG, Hisense, and TCL are still fighting. Hisense is under restraining order. The structural risk for these manufacturers is that the Samsung settlement establishes a regulatory floor — once one manufacturer accepts the consent framework, the holdouts face increasing pressure as state attorneys general from other jurisdictions follow Texas’s lead. Kentucky has already passed ACR-specific legislation requiring permission before tracking (House vote 92-0). California, Colorado, Connecticut, and Virginia have existing comprehensive privacy laws that arguably already cover ACR but haven’t been actively enforced against manufacturers. The probability of a multi-state coordinated enforcement action by end of 2026 is high.

The FTC GM/OnStar parallel. Three months before the Samsung settlement, the FTC finalized its order against GM and OnStar for collecting and selling geolocation data without informed consent. The order structure: 20-year term; 5-year ban on sharing data with consumer reporting agencies; required affirmative express consent; consumer right to request data copies and deletion; opt-out mechanism. The structural similarity to ACR is unmistakable: a connected device collecting passive sensor data, monetized through downstream data sales, without meaningful consumer consent. The FTC pattern translates directly to smart TVs. The Texas Samsung settlement is consistent with the FTC framework but state-level rather than federal. A federal FTC enforcement action against smart TV manufacturers using the GM/OnStar template is the natural next step. It hasn’t happened yet. The probability through 2026-2027 is meaningful.

The European angle. The EU AI Act treats biometric data and emotion recognition as high-risk categories with extensive governance requirements. The current ACR implementation is arguably already non-compliant with GDPR’s data minimization and purpose limitation principles. The November 2024 UCL paper specifically noted UK regulatory implications. The Information Commissioner’s Office (ICO) has been developing IoT device guidance. EU enforcement against U.S. smart TV manufacturers is plausible through 2026-2027. The GDPR fine framework (up to 4 percent of global annual revenue) is materially larger than the U.S. enforcement framework.

The regulatory trajectory: the 2017-2024 era of effective non-enforcement is ending. The 2025-2026 wave is the inflection. The 2026-2028 phase brings federal action, multi-state coordination, and EU enforcement. The economic model that has been monetizing for a decade faces its first material headwind.

4. The next horizon · emotion recognition and Samsung’s patent

The most editorially distinctive element of this story is what’s already patented for the next phase. Samsung was granted U.S. Patent 8,879,854 (“Method and apparatus for recognizing an emotion of an individual based on facial action units”) on November 4, 2014. The patent was filed in October 2011, claiming priority from an Indian provisional filed in October 2010. The technology was conceptualized fifteen years ago and patented eleven years ago.

The patent’s technical core is a system for mapping facial expressions to emotion labels using the Facial Action Coding System (FACS). FACS was developed by psychologists Paul Ekman and Wallace Friesen in the 1970s as a method for systematically describing facial expressions through 44 discrete Action Units (AUs) — small muscle contractions like “AU 12” (lip corner puller, associated with smiling) or “AU 4” (brow lowerer, associated with frowning). The Samsung patent describes a method to take a video frame, detect which AUs are present, match the input string of AUs against template strings stored in a database, and output an emotion label across six categories: angry, fear, sad, happy, surprise, disgust.

The patent’s specific contribution is mathematical: a “discriminative power” matrix that quantifies which AUs most reliably indicate which emotions, plus a “longest common subsequence” matching algorithm that handles errors in AU detection. The patent gives a worked example: for an input AU string {4, 6, 12, 17, 26}, the system maps to the template {12, 6, 26, 10, 23} which corresponds to the emotion label “happy” — even though some AUs are missing (10, 23) and some are erroneously present (4, 17). The matching tolerance allows real-world deployment despite the noise in AU detection from low-resolution camera input.

The patent’s deployment context is what matters. The patent itself doesn’t specify the use case explicitly — it describes a Personal Computer, Tablet PC, or mobile phone as example apparatus. But Samsung is the world’s largest smart TV manufacturer. Samsung’s smart TVs have included webcams in various models since approximately 2012 (the LED ES8000 series). Samsung’s smart TVs have on-device processing power that has grown dramatically over the past decade. Samsung’s smart TVs already run continuous ACR fingerprinting. The combination of (1) webcam in TV, (2) on-device emotion recognition processing, (3) ACR identifying what’s on screen at any instant, and (4) the back-end ad-tech infrastructure that monetizes viewing data is exactly what the patent enables. The TV watches you watching the TV. It identifies the content via ACR. It identifies your emotional response via facial action units. It transmits both signals to the ad platform.

The patent technically lapsed for nonpayment of maintenance fees in 2023. The patent file shows “PATENT EXPIRED DUE TO NONPAYMENT OF MAINTENANCE FEES UNDER 37 CFR 1.362” effective late 2022. This is a meaningful but qualified data point. Samsung’s broader patent portfolio in emotion recognition, facial expression analysis, and viewer measurement is enormous — hundreds of related filings remain active. The lapsed patent is one expression of a much larger IP estate. The technical capability described in 8,879,854 is now in the public domain, which actually accelerates deployment by competitors.

The advertising signal value. Current ad measurement is built on impressions, clicks, attributed conversions. Each is a coarse proxy for the actual question advertisers want answered: did the audience like the ad? Modern measurement attempts to answer this through survey panels, focus groups, and brain-imaging studies — all expensive, slow, and small-sample. Emotion recognition through TV-embedded cameras would allow advertisers to measure emotional response to every ad impression, in real time, at population scale. The first time an ad makes the household viewer happy is a different signal than the first time an ad makes the viewer angry. The signal differential is enormous. The market value of the signal is essentially unlimited — emotion-per-impression measurement is the holy grail of advertising effectiveness research.

The competitive landscape for the next horizon. Samsung is one player but not the only one. LG, Sony, TCL, Hisense all have webcam-equipped models in their lineups. Apple Vision Pro and Meta’s smart glasses generate facial expression data through different sensors. Affectiva (acquired by Smart Eye 2021), Realeyes, Emotient (acquired by Apple 2016), and other emotion-AI vendors operate in adjacent markets. The convergence point: the smart TV with embedded camera, running on-device emotion recognition, integrated with ACR, transmitting emotion-per-impression signals to advertisers. The technical capability exists today. The deployment is constrained primarily by (1) consumer awareness backlash, (2) regulatory framework that doesn’t yet permit it, (3) commercial decisions by manufacturers about the timing of opt-in framework rollouts.

The patent is the early-warning signal. The 2014 patent grant is the structural marker that the deployment was contemplated more than a decade ago. The current ACR enforcement wave is the regulatory catch-up to that 2010s technology. By the time the regulatory framework is settled for ACR, the manufacturers will be ready with the next horizon already patented and prototyped. The pattern is the same as every consumer technology privacy cycle: the technology exists for years before anyone notices, regulators take a decade to respond, the response addresses the previous generation while the next is already in development.

5. The CTV ad market and what’s at stake

The connected TV ad market is approximately $33.35 billion in the U.S. in 2025 per eMarketer, growing to $37.95 billion in 2026 (~14 percent year-over-year), $46.89 billion by 2028 (the historical crossover where CTV exceeds traditional TV ad spending for the first time), and approximately $51 billion by 2029. Globally the market is approximately $44 billion in 2025 and is projected to exceed $70 billion by 2028. The growth rate is structural — driven by the migration of viewing from linear TV to streaming, by ad-supported tier launches at Netflix and Disney+, and by the increasing precision of CTV ad targeting that pulls budget from less measurable channels.

The structural anomaly: viewers are growing faster than advertiser investment. CTV captures 20.2 percent of time spent with media in 2025 but attracts only 7.7 percent of total ad spend. The ratio of viewing-share to ad-share is approximately 2.6:1 — meaning ad spend has substantial room to grow before it matches viewing patterns. The gap is the engine driving the next five years of CTV ad spend growth. Every percentage point of advertising migrating from linear TV to CTV represents approximately $1 billion in revenue moving toward the platforms that own the surveillance infrastructure.

The market structure is fragmented but consolidating. Three companies — YouTube, Amazon, and Disney — each capture more than 10 percent of CTV ad spending in 2026. YouTube leads at approximately 12 percent ($9.21 billion in net CTV ad sales). Amazon’s combined Prime Video, Fire TV, Twitch, Freevee inventory captures over 10 percent. Disney’s combined Hulu, Disney+, ESPN footprint similarly exceeds 10 percent. Below the top three, the market is highly fragmented across hundreds of CTV publishers and ad platforms. Roku’s platform business at $4.89 billion projected 2026 revenue ranks among the largest individual CTV platforms by revenue, despite Roku not producing original content. The platform value comes from owning the household relationship and the ACR data.

The retail media network angle. Retail media networks (Walmart Connect, Amazon Ads, Target Roundel, Kroger Precision Marketing, Best Buy Ads) are increasingly running on CTV inventory — projected to sell $4.99 billion in CTV ads in 2025, more than doubling to $10.28 billion by 2028. The retail media expansion onto CTV is the structural reason for Walmart’s Vizio acquisition. Combining household-level retail purchase data with household-level viewing data produces the highest-value advertising audience graph in the U.S. market. The retail-media-on-CTV growth rate (~27 percent annually) is materially faster than overall CTV growth (~14 percent annually).

The structural read on what’s at stake. The CTV ad market is the most concentrated AI-and-data-driven business in the consumer attention economy. ACR is the central infrastructure layer. The manufacturers, platforms, retail media networks, and ad-tech intermediaries form a tightly integrated stack where each component is dependent on the household-level surveillance signal that ACR generates. A material regulatory disruption to ACR — federal FTC action, EU enforcement, multi-state coordinated action, or a major class action ruling — would compress the CTV ad targeting precision and reduce the ARPU economics across the entire stack. Conversely, the absence of such disruption compounds the surveillance infrastructure’s economic value year by year.

The next 36 months determine whether the surveillance economy continues its 2017-2024 era of effective non-enforcement, transitions to a 2025-2026 enforcement-pattern era with required consent and transparency, or escalates to a more restrictive 2027-2028 era where biometric and emotion-recognition deployments face strict regulatory ceilings before they reach scale.

6. Three scenarios for 2026-2028

The smart TV surveillance economy resolves into one of three patterns over the next 24-36 months.

Bullish scenario · 30% probability · “Industry consolidates around opt-in framework.” The Samsung Texas settlement template propagates nationally and across manufacturers through 2026-2027. Sony, LG, Hisense, TCL settle on similar terms by end of 2026. Federal FTC enforcement action establishes baseline consent requirements consistent with the GM/OnStar template. Most consumers continue to opt in (estimated 60-75 percent acceptance rates based on similar consent-flow research) because the opt-in dialog is the only friction, and most users prefer to not engage with privacy choices. ARPU economics compress modestly (10-20 percent reduction) as opt-out rates rise from current near-zero levels. Manufacturers absorb the compression through (a) more aggressive ad inventory in opt-in households, (b) deployment of next-horizon biometric features that drive higher ARPU, and (c) integration with retail media for cross-device attribution. The CTV market still reaches $46.89 billion by 2028. The surveillance economy survives with cosmetic governance changes.

Base scenario · 50% probability · “Bifurcated enforcement; varied state outcomes.” Texas’s Samsung template gets adopted in California, New York, Colorado, Washington, and several other states through 2026-2027. Federal FTC action proceeds slowly but reaches a partial settlement by end of 2027 covering a subset of manufacturers. EU enforcement materializes through GDPR Article 22 (automated decision-making) challenges with material fines (~$200-500M range per major manufacturer). Manufacturer responses bifurcate: Samsung and LG move toward more aggressive opt-in framework deployment (cost: 10-15 percent ARPU compression). Hisense and TCL fight harder, potentially face market access restrictions in the U.S. The next-horizon emotion-recognition deployment proceeds in pilot scale through 2027 but doesn’t reach mass deployment due to political backlash. CTV ad market still grows but at slightly slower rate ($44 billion 2028 vs $46.89 billion projection). Class action litigation against major manufacturers reaches material settlements through 2027-2028 ($300-800M per manufacturer aggregate).

Bearish scenario · 20% probability · “Regulatory hammer; structural compression.” A high-profile incident catalyzes broader political response — most likely a major data breach exposing the granularity of ACR-collected data, or an investigative report linking ACR data to specific harm cases (insurance discrimination, political targeting, mental health profiling). Federal legislation establishes an Auto-Renew-Style affirmative-consent framework for connected devices similar to the FTC GM/OnStar template, applied broadly. Class action litigation produces a multi-billion-dollar industry settlement. ACR opt-out rates rise to 40-60 percent. ARPU compresses 30-50 percent. CTV ad market growth slows materially ($40 billion 2028 vs $46.89 billion projection). The next-horizon emotion-recognition deployment stalls before reaching mass scale, becoming an EU-prohibited use case and a U.S. politically toxic deployment. Walmart’s $2.3 billion Vizio acquisition becomes a substantial impairment write-down. Roku, Vizio, and the broader CTV-ad-dependent ecosystem face structural revenue compression.

The 30/50/20 probability allocation reflects current setup factors. Bullish scenario probability is supported by: the Samsung Texas settlement template’s lack of monetary penalty (manufacturer-friendly precedent); the 2017 Vizio precedent demonstrating low historical enforcement intensity; consumer awareness friction in opt-out flows; the structural revenue value to the manufacturers and retail media partners. Bearish scenario probability is supported by: the steepening regulatory enforcement curve from 2017 → 2024 → 2025-2026 → present; the FTC GM/OnStar template providing a federal framework for connected-device privacy; the EU AI Act biometric provisions providing a regulatory ceiling for the next-horizon deployment; growing political consciousness around AI surveillance.

The base scenario reflects the most likely outcome: bifurcated state-level enforcement, slow federal action, EU regulatory friction, manufacturer adaptation through additional governance theater while preserving the underlying business model. The surveillance economy compresses modestly but remains structurally intact.

7. Strategic implications by stakeholder

The smart TV surveillance arc has direct consequences for five distinct stakeholder groups.

For consumers. The practical advice is unambiguous if you care about the privacy profile: disable ACR through the buried settings (Samsung “Viewing Information Services” / LG “Live Plus” / Sony “Samba Interactive TV” / Vizio “Viewing Data”); be aware that firmware updates may reset the toggles; consider blocking ACR endpoints at the DNS layer (Pi-hole, NextDNS) for defense-in-depth; isolate the TV on its own VLAN if your network supports it; consider not connecting the TV to the internet at all if you watch primarily through a separate streaming device or cable box. The buried opt-outs are deliberately friction-loaded; treating ACR as an active threat rather than a default-on annoyance is the appropriate mental model.

For investors in the platform companies. Roku, Walmart (post-Vizio acquisition), and the CTV-platform ecosystem face material regulatory tail risk through 2027-2028. Position based on the 30/50/20 scenario probability. The bullish scenario continues current trajectory; the base scenario reduces ARPU 10-15 percent at major manufacturers; the bearish scenario produces 30-50 percent ARPU compression and meaningful impairment risk. The risk-adjusted value depends heavily on whether the regulatory enforcement curve continues steepening or plateaus at the current Texas-Samsung template.

For investors in the manufacturer companies. Samsung, LG, Sony are public; they have material exposure but diversified business models that absorb the platform-revenue risk. Hisense and TCL face additional risk from their PRC ownership compounding the privacy concerns — Texas AG specifically called out Chinese manufacturers in the December 2025 lawsuits. The market-access risk for Chinese-owned manufacturers in the U.S. market is meaningfully larger than the consent-framework risk affecting Samsung, LG, Sony.

For policymakers. The smart TV surveillance pattern is a paradigmatic case for connected-device privacy framework. The current state-by-state enforcement is inefficient. A federal framework matching the FTC GM/OnStar template — affirmative consent, opt-out rights, data deletion rights, multi-year governance terms — is structurally appropriate. The political feasibility through 2026-2027 depends on whether catalyst events emerge (major breach, investigative report, high-profile harm case). The EU AI Act provides a useful template for the biometric / emotion-recognition next-horizon framework.

For ad-tech industry participants. The structural read: ACR-derived signals will continue to flow through the ad-tech stack but with increasing governance overlay through 2026-2028. Identity-resolution, attribution measurement, and household-level targeting precision face moderate compression. The retail-media-on-CTV growth thesis remains intact but with slower realization than current 27-percent-annual projections suggest. The next-horizon emotion-recognition signal will be the most valuable ad-tech signal ever produced, but its deployment timeline is uncertain — somewhere between 2027 (aggressive) and 2032 (regulated). Position investments based on which scenario you believe.

What to Do This Quarter (Through 2026)

1. Consumers. Disable ACR through the buried settings menus. Block ACR endpoints at DNS layer if you have technical capability. Treat firmware updates as potential consent resets. Consider not connecting the smart TV to the internet at all.

2. CTV-exposed investors. Position based on 30/50/20 scenario probability through 2026-2028. The Samsung Texas template lacks monetary penalty (manufacturer-friendly), but the regulatory curve is steepening. Hisense and TCL face additional Chinese-ownership market-access risk.

3. Manufacturers. Sony, LG, Hisense, TCL — the Samsung settlement is the template. Voluntary adoption is cheaper than litigation. Hisense’s restraining order is a warning. Sony, LG should settle on similar terms by end of 2026.

4. Policymakers. Federal connected-device privacy framework matching the FTC GM/OnStar template is structurally appropriate. State-by-state enforcement is inefficient. EU AI Act biometric provisions are the template for the next-horizon emotion-recognition framework.

The Strategic Read

The smart TV surveillance economy is a mature, multi-billion-dollar business hidden inside hardware that consumers think they’re buying for $300-1,500. Roku’s 2025 device gross margin was negative 13.8 to 23.3 percent — approximately $82 million in annual hardware loss, recovered many times over through $4.14 billion in 2025 platform revenue at 51-52 percent gross margin. Vizio operated similarly until Walmart acquired the company for $2.3 billion in December 2024 specifically to combine 20+ million households of Inscape ACR viewing data with Walmart’s retail purchase data. The hardware is the customer acquisition vehicle. The surveillance is the product.

The mechanism is Automatic Content Recognition. Smart TVs from Samsung, LG, Sony, Vizio, Roku, Hisense, TCL capture screenshots of the screen every 500 milliseconds (Samsung) or audio at 48 kHz with 10-millisecond image captures (LG). The captures are converted into perceptual fingerprints locally, then transmitted to manufacturer servers every 60 seconds (Samsung) or 15 seconds (LG). Peer-reviewed research from UCL/UC Davis/UC3M (ACM IMC 2024) confirmed the same tracking runs when the TV is used as an HDMI monitor for laptops, gaming consoles, or other devices. The opt-out is buried under deliberately vague feature names — “Viewing Information Services,” “Live Plus,” “Samba Interactive TV,” “Viewing Data” — requiring per the Texas AG’s December 2025 complaint “over 200 clicks spread across four or more menus.”

The regulatory enforcement curve is steepening. The 2017 Vizio FTC settlement at $2.2 million on 11 million tracked households was effectively a green light at $0.20 per household. The November 2024 UCL paper provided the empirical foundation. December 15, 2025: Texas AG Paxton sues Samsung, LG, Sony, Hisense, TCL. January 14, 2026: FTC finalizes parallel GM/OnStar order — 20-year term, 5-year ban on consumer reporting agency data sharing, affirmative express consent required. February 26, 2026: Samsung settles Texas — no monetary penalty, required to halt ACR collection without express consent, required to rewrite consent screens to be “clear and conspicuous.” Sony, LG, Hisense, TCL still fighting. Hisense under restraining order. Kentucky has passed ACR-specific legislation (House 92-0). The probability of multi-state coordinated enforcement and federal FTC action through 2026-2027 is meaningful.

The CTV ad market is approximately $33.35 billion in the U.S. in 2025, growing to $37.95 billion in 2026, $46.89 billion by 2028 (the crossover year where CTV surpasses traditional TV ad spend for the first time), and $51 billion by 2029. The structural anomaly: viewers capture 20.2 percent of media time but only 7.7 percent of ad spend — the gap drives the next five years of growth. Three platforms (YouTube, Amazon, Disney) each capture 10+ percent of CTV ad spend in 2026. Retail media networks (Walmart Connect, Amazon Ads, Target Roundel) on CTV growing from $4.99 billion (2025) to $10.28 billion (2028) — explaining Walmart’s Vizio acquisition.

The next horizon is biometric. Samsung was granted U.S. Patent 8,879,854 in November 2014 for emotion recognition based on Facial Action Coding System (FACS) Action Units — six emotions (angry, fear, sad, happy, surprise, disgust). Combined with ACR, the advertising signal evolves from “what you watched” to “how you reacted to each specific ad.” That’s the trillion-dollar measurement holy grail — emotional response per impression, in real time, in your living room. The patent technically lapsed for nonpayment in 2023, but Samsung’s broader emotion-recognition patent estate remains active. The technical capability exists today (cameras in TVs, on-device processing, ACR signal). The deployment is constrained by consumer awareness, regulatory framework (EU AI Act biometric provisions), and manufacturer commercial decisions about timing.

Three scenarios resolve through 2026-2028. Bullish (30%): Samsung Texas template propagates nationally; opt-in framework deployed; modest 10-20 percent ARPU compression; surveillance economy survives with cosmetic governance changes. Base (50%): Bifurcated state-level enforcement; partial federal action; EU enforcement materializes; 10-15 percent ARPU compression at major manufacturers; class action litigation reaches material settlements ($300-800M per manufacturer); CTV market still grows to $44B by 2028 vs $46.89B projection. Bearish (20%): Catalyzing incident triggers federal legislation; ACR opt-out rates rise to 40-60 percent; ARPU compresses 30-50 percent; emotion-recognition next-horizon stalls before mass deployment; Walmart’s $2.3 billion Vizio acquisition becomes substantial impairment.

The connections to broader threads run deep. The ACR economy is a paradigmatic case of the bubble question’s durable-value vs frothy distinction — surveillance ad-tech is genuinely durable cash-generative business, not a hype cycle. The labor displacement Q1-Q2 2026 dispatch covered AI-augmented productivity in white-collar work; smart TV surveillance is AI-augmented productivity in advertising effectiveness measurement. The EU AI Act enforcement framework provides the regulatory template for the biometric next-horizon. The hyperscaler capex thesis demand-pull validation includes CTV ad-tech infrastructure investment.

The strategic implications run by stakeholder. Consumers should disable ACR through buried settings and treat firmware updates as potential consent resets. CTV-exposed investors should position based on 30/50/20 scenario probability. Manufacturers Sony, LG, Hisense, TCL should adopt the Samsung settlement template voluntarily — Hisense’s restraining order is the warning. Policymakers should establish federal connected-device privacy framework matching the FTC GM/OnStar template; state-by-state enforcement is inefficient.

The deeper signal: the smart TV is the most successful Trojan horse in consumer electronics history. It captured one of the last places people still trusted — the living room — and turned it into a continuous behavioral sensor for the global advertising market. The 2017-2024 era of effective non-enforcement is ending. The 2025-2026 wave is the inflection. The 2026-2028 phase brings federal action, multi-state coordination, EU enforcement, and the political battle over the next horizon — emotion recognition through TV-embedded cameras combined with ACR’s content identification. The patent for that next horizon was granted in November 2014. The deployment has been waiting eleven years for the technical maturity, regulatory ambiguity, and consumer-awareness equilibrium to align. Whether it arrives at scale through 2027-2030 depends on whether the current enforcement wave establishes a regulatory ceiling that prevents it, or whether the manufacturers find a consent-framework-shaped path to deployment.

The honest assessment: the most likely scenario is the base case — bifurcated enforcement, manufacturer adaptation through governance theater, modest ARPU compression, the surveillance economy structurally preserved. The probability of the bearish tail (regulatory hammer that compresses the model meaningfully) is real but lower. The structural insight is that the trojan horse worked. By the time the regulatory framework caught up, the surveillance infrastructure was deeply embedded in 250+ million U.S. households, the economic dependency was structural across hardware manufacturers, ad platforms, retail media networks, and ad-tech intermediaries, and the next horizon was already patented and waiting. The fight in 2026-2028 is over the terms of consent, not over whether the surveillance happens.

Smart TVs are loss-leader Trojan horses for an ad business powered by ACR surveillance. Roku 2025 device gross margin -13.8% to -23.3%, ~$82M annual hardware loss. Vizio acquired by Walmart $2.3B Dec 2024 for retail-data integration. ACR captures screenshots every 500ms (Samsung) or 10ms (LG) — confirmed by UCL/UC Davis/UC3M IMC 2024 peer-reviewed paper. Tracks HDMI inputs (laptops, consoles). Opt-out requires 200+ clicks. December 2025 Texas AG sues 5 manufacturers; February 2026 Samsung settles (no monetary penalty). January 2026 FTC GM/OnStar parallel framework. CTV ad spend $33B 2025 → $46.89B 2028 (surpasses linear TV) → $51B 2029. Next horizon: Samsung Patent 8,879,854 emotion recognition from FACS Action Units (6 emotions). Combined with ACR = emotional-response-per-ad measurement. Three scenarios with 30/50/20 probability.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The Bubble Question, Disentangled

- The Labor Displacement Q1-Q2 2026 Data

- The EU AI Act Enforcement Countdown

- The $725B Hyperscaler Capex Question

- The Compute Reckoning · Anthropic-SpaceX Deal

Sources

- Roku · Q4 2025 8-K · FY2026 outlook · February 2026 — primary financial filing

- Roku 2025 annual results · device gross loss ~$82M · platform revenue $4.145B · gross margin 50%+

- Roku 2026 guidance · device revenue $610M (negative mid-teens margin) · platform revenue $4.89B (51-52% margin)

- Variety · Roku Q4 2025 Swing to Profit, Forecasts 16% Revenue Growth in 2026 · February 13, 2026

- Walmart · acquisition of Vizio · $2.3 billion · December 2024

- Vizio NewFronts · 20+ million Smart TVs catalogued via Inscape ACR

- Vizio Platform+ revenue projections · ~$750M projected 2025 · ARPU >$40

- UCL News · Smart TV tracking raises privacy concerns · November 2024

- Mandalari, Anna; Maria Mandalari; Zubair Shafiq · Watching TV with the Second-Party: A First Look at Automatic Content Recognition Tracking in Smart TVs · ACM Internet Measurement Conference 2024 · UCL / UC Davis / UC3M

- Samsung official documentation · ACR captures every 500ms · batches and transmits per minute

- LG configuration file · 48 kHz audio sample rate · 60 Hz display refresh

- Texas Attorney General · Samsung TV Petition · December 15, 2025 · “200+ clicks across 4+ menus”

- Texas AG · lawsuits filed against Samsung, LG, Sony, Hisense, TCL · December 15, 2025

- Texas AG · Samsung settlement announcement · February 26, 2026

- Texas AG · TROs against Samsung and Hisense · January 2026

- BleepingComputer / SC Media / Malwarebytes / IAPP · Samsung Texas settlement coverage · February-March 2026

- Kentucky · ACR-specific legislation · House vote 92-0

- FTC · Vizio to Pay $2.2 Million to FTC and State of New Jersey · February 2017 — 11M households tracked

- FTC · FTC Finalizes Order Settling Allegations that GM and OnStar Collected and Sold Geolocation Data · January 14, 2026 — 20-year order, 5-year ban on CRA sharing

- USPTO · Samsung Patent US 8,879,854 B2 · Method and apparatus for recognizing an emotion of an individual based on facial action units · Granted November 4, 2014

- USPTO · Samsung patent expiration for nonpayment · 2023

- Ekman & Friesen · Facial Action Coding System (FACS) · 1978 — 44 Action Units across upper / lower face

- Lobato, Ramon · Automated content recognition (ACR), smart TVs, and ad-tech infrastructure · Sage Journals 2025

- eMarketer · CTV ad spend projections · $33.35B (2025) · $37.95B (2026) · $46.89B (2028) · $51B (2029)

- MNTN Research · CTV ad spend forecast · CTV Ad Spend Will Grow to $46.89 Billion by 2028

- Teads · Connected TV Advertising 2026 · February 12, 2026

- StackAdapt · CTV viewing share 20.2% vs ad spend share 7.7% in 2025

- WARC Media · Linear TV at ~12% of global ad spending · 2025

- Parks Associates · 68% of US households have a smart TV · 46% have streaming media player · November 2024