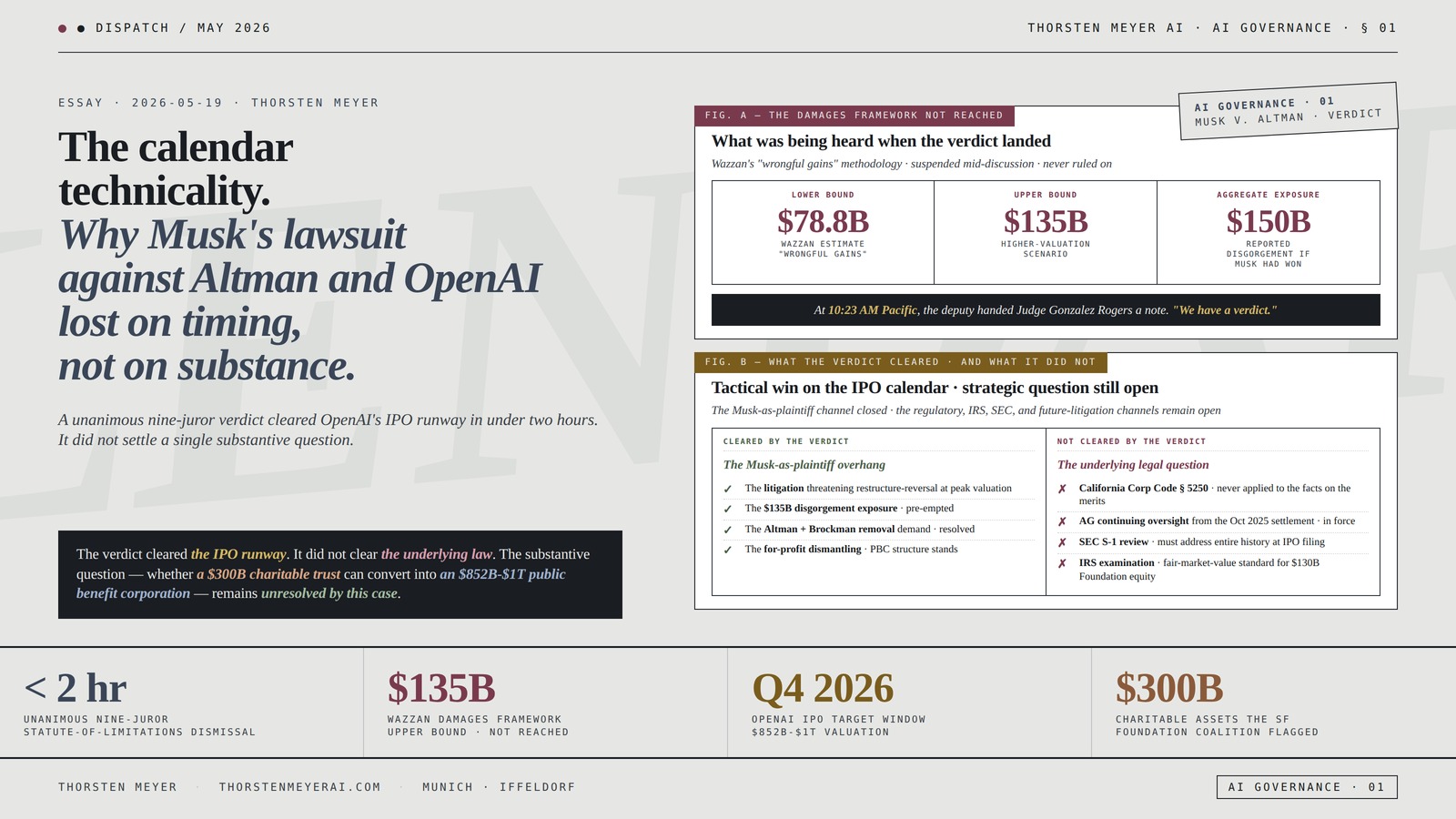

On May 18, 2026, a nine-member federal jury in Oakland deliberated for less than two hours and unanimously dismissed every claim in Elon Musk’s lawsuit against Sam Altman, Greg Brockman, OpenAI, and Microsoft — not on the merits, but on the statute of limitations. U.S. District Judge Yvonne Gonzalez Rogers immediately adopted the advisory verdict, declaring “there is a substantial amount of evidence to support the jury’s finding” and tossing the case before the damages hearing could complete.

The numbers Musk’s expert had been preparing to enumerate were extraordinary: $78.8 billion to $135 billion in disgorgement-eligible “wrongful gains,” dismissal of Altman and Brockman from their posts, and the dismantling of OpenAI’s for-profit entity. The judge, before the verdict landed, had told Musk’s damages expert Dr. C. Paul Wazzan that his analysis “seems to be devoid of connection to the underlying facts.”

The structural significance of the verdict is not what it ruled. It is what it did not rule. The jury found Musk waited too long to sue — his 2024 filing fell outside the three-year statute of limitations against harms that the defense argued occurred no later than 2021. It did not address whether Altman and Brockman actually violated a charitable trust. It did not address whether OpenAI’s October 2025 restructure into a Public Benefit Corporation actually transferred up to $300 billion in charitable assets into for-profit ownership. It did not address whether the AGI clause in the Microsoft partnership voids itself in a manner consistent with the original nonprofit’s mission.

Musk’s own response on X captured the asymmetry exactly: “the judge & jury never actually ruled on the merits of the case, just on a calendar technicality.” This is correct. The verdict clears one specific plaintiff. It does not settle the underlying legal question, which the California Attorney General has been investigating separately since December 2024, which a coalition of more than fifty California foundations petitioned Bonta to halt in April 2025, which Lawrence Lessig filed amicus on behalf of twelve former OpenAI employees over, and which the Bonta settlement of October 2025 resolved only in exchange for concessions that did not include disgorgement of the nonprofit’s commercial value.

The clear practical effect: OpenAI’s path to a Q4 2026 IPO at a target valuation of $852 billion to $1 trillion is now open in a way it was not 48 hours ago. The unclear question: whether the underlying charitable-trust theory survives this case to be re-tested by a different plaintiff in a different court at a different time.

This essay walks what the jury actually decided and did not decide, the three-year statute-of-limitations argument that ended the case, the $135 billion damages framework that was being built when the verdict landed, the appeal Musk has announced and what it can and cannot achieve, the charitable-assets oversight track that runs separately through the California AG’s office, the IPO runway that was the practical stake and is now open, and the structural reading of what a procedural dismissal of this size signals about how the AI industry will be regulated in the public-company era now arriving.

By Thorsten Meyer — May 2026

This is a structural-economics dispatch on a verdict that ended a three-week trial in two hours and one decision but did not end the underlying question the trial was about. The two are different things. What the jury actually decided was narrow: Musk waited too long to file. What the trial was being asked to decide was wide: whether the AI industry’s largest nonprofit-to-for-profit conversion in history is enforceable under California charitable-trust law. The narrow decision controls who can sue. The wide question controls how the AI industry restructures over the next 24 months. Anyone reading the verdict as a vindication of OpenAI’s underlying conduct is reading it past what the court actually ruled. Anyone reading it as a vindication of Musk’s underlying claims is reading the opposite direction past the same evidence. The honest read is that the verdict was both decisive on calendar discipline and silent on the substantive law.

The structural argument I want to make: The verdict did exactly two things at the same time. It cleared OpenAI’s IPO runway by removing the specific litigation overhang that could have forced a restructure-reversal at peak valuation. It did not validate the restructure itself, which remains separately reviewed under the California AG’s oversight authority, the IRS’s nonprofit-conversion framework, and any future plaintiff with standing and timing. The same procedural narrowness that delivered OpenAI a quick win also preserved the door for future challenges from differently-situated parties — California AG · Public Citizen · the coalition that petitioned Bonta in April 2025 · the twelve former OpenAI employees who filed amicus through Lawrence Lessig · or a state or federal regulator acting on its own initiative. The trial laid bare, on the public record, the timeline of how Altman and Brockman moved the nonprofit’s intellectual property and personnel into the for-profit. That record exists now whether or not Musk had standing to use it. The structural consequence: the calendar technicality is good news for OpenAI’s IPO; it is not good news for OpenAI’s settled-law status. Those are different things and only one of them is now resolved.

The headline integrative finding: Yesterday’s verdict was a tactical dismissal on procedural grounds in one case among the cases that examine the same underlying conduct. The strategic question — whether converting a $300B charitable trust into a public benefit corporation valued at $852B-$1T can stand under California Corporations Code 5250 (which provides that assets held by a charitable corporation are held in trust for the declared charitable purpose) and the California Supreme Court precedent applying that section — is unresolved by this trial because the court chose not to reach it. The Q4 2026 IPO calendar advances. The legal-precedent calendar does not. That asymmetry — IPO clear, legal-precedent still open — is the actual condition of the file as of the verdict. Whether the IPO closes before any successor case can reach the merits, and whether the AG’s October 2025 settlement holds up under continued scrutiny from the coalition that wanted it tougher, are the open variables.

This essay walks what the jury actually decided (Section I), the three-year statute-of-limitations defense that ended the case (Section II), the $135 billion damages framework that was being built when the verdict came (Section III), Musk’s announced appeal and what it can and cannot do (Section IV), the charitable-assets oversight track that runs separately (Section V), the IPO runway that was the practical stake (Section VI), and the structural reading of what this signals about AI corporate governance entering the public-company era (Section VII).

The calendar technicality.

Why Musk’s lawsuit

against Altman and OpenAI

lost on timing,

not on substance.

deliberation · statute-of-limitations

upper bound · disgorgement-eligible

$852B-$1T valuation · ~$60B raise

Foundation coalition flagged · April 2025

- Musk filed too late · 2024 filing fell outside the three-year statute of limitations under California Code of Civil Procedure

- The defense’s “harm occurred no later than 2021” timing argument was sufficient

- Discovery-rule tolling rejected — Musk’s argument that asset-transfer magnitude was not knowable in time did not extend the window

- “Fraudulent concealment” tolling rejected — no separate basis to delay the clock

- Microsoft aiding-and-abetting claim dismissed by virtue of the predicate claim being dismissed

- Whether Altman and Brockman violated a charitable trust · not addressed on the merits

- Whether the 2019 for-profit subsidiary structure improperly transferred nonprofit assets · not addressed

- Whether the October 2025 PBC conversion at ~$500B is a legally permissible disposition of charitable assets · not addressed

- Whether the Microsoft AGI-voids-the-deal clause is consistent with the original nonprofit mission · not addressed

- Whether Microsoft’s $13B 2019-2023 investment trajectory aided and abetted any breach of charitable trust · not addressed on its own merits

OpenAI + Microsoft

“wrongful gains”

scenario · same

methodology

disgorgement

if Musk had won

The verdict was a tactical win for OpenAI that does not deliver a strategic win on the underlying legal question. The IPO calendar advances. The regulatory calendar continues to run. The legal-precedent calendar remains open.Thorsten Meyer · The Calendar Technicality · AI Governance 01

I · What the jury actually decided · and what it did not

The narrow-verdict crystallization. A jury verdict means what it says, not what either side’s press conference characterizes it as saying. This one says one thing.

The unanimous finding

The question on the verdict form: whether Musk’s claims fell within the three-year statute of limitations governing breach-of-charitable-trust and related causes of action under California law.

The jury’s answer: no. Unanimous nine-member advisory verdict, less than two hours of deliberation. Adopted immediately by U.S. District Court Judge Yvonne Gonzalez Rogers.

The judge’s framing: “I’ve always said I would accept the jury’s verdict. I think there’s a substantial amount of evidence to support the jury’s finding. There was a substantial amount of evidence to support the jury’s finding, which is why I was prepared to dismiss on the spot.”

What was not decided

Whether Altman and Brockman violated a charitable trust: not addressed. The defense’s statute-of-limitations argument was a threshold question that, if answered in their favor, mooted the underlying merits.

Whether OpenAI’s 2019 for-profit subsidiary structure improperly transferred nonprofit assets: not addressed.

Whether OpenAI’s October 2025 conversion to a public benefit corporation valued at ~$500 billion (and now reportedly preparing for an IPO at $852B-$1T) constitutes a legally permissible disposition of charitable assets: not addressed.

Whether the Microsoft partnership’s AGI-voids-the-deal clause is consistent with the original nonprofit mission: not addressed.

Whether Microsoft’s $13B investment trajectory between 2019 and 2023 aided and abetted any breach of charitable trust: not addressed. The Microsoft claim was dismissed by virtue of the predicate claim being dismissed, not on its own merits.

Musk’s own framing

The post-verdict X post from Musk is the clearest read on what was actually decided, from the losing side itself:

“Regarding the OpenAI case, the judge & jury never actually ruled on the merits of the case, just on a calendar technicality. There is no question to anyone following the case in detail that Altman & Brockman did in fact enrich themselves by stealing a charity. The only question is WHEN they did it!”

The first sentence is legally accurate. The second is Musk’s view of the facts. The third reveals exactly what the statute-of-limitations defense neutralized: Musk’s underlying theory survived; his standing to litigate it did not.

OpenAI’s framing

OpenAI’s lead attorney Bill Savitt, outside the courthouse: “It did not take [the jury] two hours to conclude … that Mr. Musk’s lawsuit is nothing more than an after-the-fact contrivance that bears no relationship to reality. They kicked it exactly where it belongs — just to the side. This lawsuit is a hypocritical attempt to sabotage a competitor.”

Two things to notice: (1) Savitt’s “no relationship to reality” framing is broader than the verdict actually delivered. The verdict was about timing, not about reality. (2) The “hypocritical attempt to sabotage a competitor” line is the defense’s parallel narrative — Musk left OpenAI in 2018, founded xAI in 2023, and stood to benefit from any OpenAI restructure-reversal. The court did not rule on whether Musk’s claims were hypocritical or competitor-motivated; the defense argued it and the verdict made the question moot.

The narrow-verdict observation

The verdict is a clean procedural dismissal in one specific case. It is not a substantive vindication of OpenAI’s restructure under charitable-trust law. The trial record — three weeks, testimony from Altman, Brockman, Microsoft CEO Satya Nadella, Musk himself, and the twelve former OpenAI employees referenced in Lawrence Lessig’s amicus brief — exists now as public evidence regardless of whether Musk had standing to use it.

Practical Claude Handbook for Attorneys: Master Case Analysis, Contract Review, Research Automation, Client Communication, and Document Drafting (Claude AI Guide for Beginners 4)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The three-year wall · how the statute-of-limitations defense ended the case

The procedural-defense crystallization. OpenAI’s lawyers built their case around a single threshold question that turned out to be sufficient on its own. The strategy worked because of the structural mismatch between Musk’s grievance timeline and the law’s recognition timeline.

The applicable rule

California Code of Civil Procedure § 343 + § 338 establishes a three-year statute of limitations for breach-of-charitable-trust and related fiduciary-duty claims absent specific tolling circumstances. The defense argued that any harms Musk alleged occurred no later than 2021, when OpenAI’s for-profit subsidiary structure had been publicly known for two full years (since the 2019 creation of OpenAI LP). The filing date that mattered: Musk filed his original lawsuit on February 29, 2024.

The arithmetic: 2024 − 2021 = 3+ years. Outside the window. The Microsoft deal completing in January 2023, the OpenAI Foundation’s public messaging, and the for-profit subsidiary’s published terms were all in the public record before the three-year window opened.

Musk’s counter-argument

The discovery-rule argument: Musk’s counsel argued that the harm continued to accrue through subsequent restructurings (the 2023 Microsoft expansion to $10B, the 2025 PBC conversion, the late-2025 commercial agreement renegotiation) and that the full extent of the asset transfer was not knowable from public disclosures until later.

The “fraudulent concealment” tolling argument: that Altman and Brockman concealed the magnitude of the conversion, which would have tolled the statute until the concealment was reasonably discoverable.

The jury’s response: did not find either argument sufficient to extend the filing window to February 2024.

Why the threshold question was sufficient

The defense’s strategic logic: rather than litigate the merits of whether OpenAI’s restructure violated charitable-trust law — a question that would have required the court to apply California Corporations Code § 5250 to a billion-dollar AI lab’s transition, a question with no clean precedent at this scale — the defense moved to dismiss on timing. A timing dismissal is fast, requires less factual development, and produces a verdict the appellate review will examine on a tighter record.

Bill Savitt’s closing argument crystallized this: the case was framed as a 2018-grievance dressed up in 2024 clothing. Musk’s underlying objection was about losing control of OpenAI when he left the board in February 2018. The intervening six years between his exit and his lawsuit were the structural problem the defense exploited.

The 2018 control-fight framing

Sarah Eddy, OpenAI’s attorney, in closing arguments: Musk’s $44 million in donations from 2016 to 2020 came with no strings attached, meaning “Musk does not have a charitable trust to enforce.” The defense additionally showed evidence that Musk had previously proposed both a for-profit OpenAI under his control and folding OpenAI into Tesla — which the other co-founders rejected. The defense’s framing: Musk’s objection is to losing the control fight, not to the conversion itself.

The court’s apparent acceptance: Judge Gonzalez Rogers’s pretrial ruling on the Stuart Russell witness — that “existential risk is outside the scope of the trial” — narrowed the case to the corporate-governance question and away from Musk’s broader AI-safety framing. That ruling functionally constrained the case to the timing question.

The statute-of-limitations observation

The defense won the case on a question that does not require ruling on whether the underlying conduct was lawful. This is a structurally typical outcome for charitable-trust litigation where the alleged conduct happened years before the filing — the law’s calendar discipline is designed to do exactly this kind of work. It does not mean the conduct was lawful. It means this specific plaintiff cannot litigate it in this specific court at this specific time.

AI-powered legal case analysis tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The damages framework · what $135 billion looked like when the verdict came

The pre-empted-claim crystallization. When the jury came back, Judge Gonzalez Rogers was mid-hearing on the damages framework that would have applied if Musk had prevailed. The numbers being discussed were extraordinary in scale and revealing in structure.

What Musk was seeking

The “wrongful gains” framework: Musk’s expert Dr. C. Paul Wazzan presented an estimate that OpenAI and Microsoft had jointly captured between $78.8 billion and $135 billion in commercial value that, on Musk’s theory, properly belonged to the original nonprofit. The remedy sought was disgorgement — return of those gains to the OpenAI Foundation rather than payment to Musk individually.

The dismissal demands: Altman and Brockman to be removed from their roles at OpenAI Group PBC. The for-profit entity to be dismantled and its assets returned to the nonprofit Foundation.

The aggregate damages exposure if Musk had won: reporting consistently characterized the potential disgorgement at up to $150 billion, with the variance reflecting different views of fair-market value at different points in the conversion timeline.

The judge’s skepticism

Judge Gonzalez Rogers, to Dr. Wazzan, in the damages hearing: “Your analysis seems to be devoid of connection to the underlying facts.”

The structural problem with the damages framework (as the judge appeared to read it): the expert was treating Musk’s $44M in early-stage charitable contributions as if they were equity investments in a startup, with the gain calculated as a proportional share of OpenAI’s post-restructure valuation. That framework conflates two different legal categories — gift to a charity versus investment in a for-profit — that have structurally different downstream rights.

The contributory framing: Musk’s contributions were 2016-2020 donations of approximately $44M total (the case record reflects $38M to $44M depending on the line of accounting). The 2025 OpenAI Group PBC was valued at approximately $500B at conversion and is reportedly preparing for an IPO at $852B-$1T. A proportional-share-of-value calculation would assign Musk’s $44M roughly $74B to $88B of value — within the range Wazzan presented but, as the judge noted, without the legal foundation that an investment-equity calculation would require.

What the verdict pre-empted

The verdict landed mid-hearing. Edwin Cuenco, the courtroom deputy, handed Judge Gonzalez Rogers a note at 10:23 AM Pacific. The jury had started deliberations at 8:30 AM. The damages framework discussion was suspended and then mooted.

The structural consequence: the legal record now contains the damages framework but not a ruling on it. If a future plaintiff brings a similar charitable-trust claim within the statute of limitations (e.g., challenging the October 2025 PBC conversion within the three-year window from 2025 forward), Wazzan’s framework will be one of multiple available templates that the court may or may not find persuasive. The court has not endorsed it; it has only declined to address it.

The damages-framework observation

The case turned out to be one where the merits would have produced extraordinary remedy if the timing had survived. Up to $135 billion in disgorgement, two CEO removals, dismantling of a $852B+ for-profit entity. None of this is what the verdict actually delivered. What was delivered was a procedural finding that Musk could not litigate any of it. The substantive question of whether the remedy framework was appropriate was, in the judge’s pre-verdict reading, dubious on the merits. But the verdict did not need to reach that question, and did not.

Legal Terminology: QuickStudy Laminated Reference Guide (Quick Study: Law)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The appeal · what Musk’s “this one is not over” can and cannot achieve

The procedural-recourse crystallization. Musk’s lead attorney Marc Toberoff, addressing reporters outside the courthouse: “This one is not over. I can sum it up in one word: appeal.” Musk on X: “appeal.” The question is what that appeal can actually do.

What an appeal in this case examines

The Ninth Circuit appellate scope: review of legal rulings and procedural decisions, not re-litigation of factual findings the jury made. An appeals court does not re-try the case; it reviews whether the trial court applied the law correctly.

The specific grounds Musk’s counsel can raise:

- Statute-of-limitations interpretation: whether Judge Gonzalez Rogers properly framed the discovery-rule and tolling questions for the jury. This is the most direct line of attack and the most likely ground for appeal.

- Evidentiary rulings: whether specific decisions (e.g., the pre-trial ruling excluding existential-risk testimony from Stuart Russell) improperly narrowed the case.

- Jury instructions: whether the instructions on charitable-trust law correctly stated the applicable law of California.

- Damages-framework rulings: less likely to be raised because the damages hearing was not completed, but Musk’s counsel could argue the judge’s pre-verdict skepticism of Wazzan tainted deliberations.

The Ninth Circuit’s typical disposition pattern in statute-of-limitations cases: deferential to the trial court’s factual findings unless the procedural ruling is clearly inconsistent with applicable precedent. The standard of review is substantial — Musk needs to demonstrate that no reasonable jury could have reached the timing finding the jury reached.

What an appeal cannot do

An appeal cannot revisit the underlying merits: even a successful appeal would only return the case to district court for proceedings consistent with the appellate ruling — likely a re-trial on the timing question or a remand for the merits proceedings the dismissal pre-empted.

An appeal cannot block the OpenAI IPO: the Ninth Circuit does not typically issue stays that would prevent normal corporate operations of a defendant absent extraordinary circumstances, and Musk’s counsel has not signaled any such request.

An appeal cannot recover damages within the IPO window: standard Ninth Circuit appellate timelines from district court verdict to ruling run 12-24 months in cases of this complexity. The IPO will close before the appeal resolves under any reasonable scenario.

The strategic question

If the verdict cannot be reversed before the IPO: what does the appeal actually accomplish?

Two possible answers:

- Preserve the legal claim for re-litigation: even an unsuccessful appeal preserves the record and the legal arguments, which may be useful if a state AG, regulator, or differently-situated plaintiff brings a parallel claim with valid standing and timing.

- Maintain Musk’s public posture: Musk’s X post — “There is no question to anyone following the case in detail that Altman & Brockman did in fact enrich themselves by stealing a charity” — is the kind of statement that benefits from continued litigation. An appeal extends the public narrative; a dismissal with no appeal closes it.

The honest read: the appeal is unlikely to alter the practical outcome of the case but is rational from Musk’s perspective in maintaining the public claim and preserving the legal record for parallel proceedings.

The appeal observation

Toberoff’s “this one is not over” is procedurally correct but strategically limited. The appeal will run its course on a timeline that does not affect the IPO calendar; it may or may not preserve the legal claim for adjacent uses; and it does not address the substantive charitable-trust question that the trial court declined to reach. Practically, the case is over. Procedurally, it is not.

ENGPOW Legal Size Expanding File Folder Important Document Organizer Fireproof Document Bag with 13 Pockets,Color Labels,Non-Itchy Silicone Coated Portable File Wallet Large Capacity(16" x 10.6")

Double Layers Protection: Our newly designed file folder uses different materials than other folder.Double Layered design, high quality…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The parallel track · the California AG’s oversight authority and what it has and has not done

The regulatory-oversight crystallization. The Musk lawsuit was one of two adjacent processes examining the same underlying conduct. The other process — California Attorney General Rob Bonta’s nonprofit-conversion oversight under Corporations Code § 5250 and the AG’s general supervisory authority over charitable trusts — runs on its own timeline and reached its own resolution months before the Musk verdict.

The AG’s investigation

The investigation opened in December 2024, when Deputy Attorney General Christopher Lamerdin sent OpenAI a letter citing “OpenAI’s articles of incorporation under which OpenAI’s assets are irrevocably dedicated to its charitable purpose” and the AG’s “responsibility to protect assets held in charitable trust.” The letter requested information on the proposed restructuring plan, asset transfers, and the value of charitable assets.

The coalition petition of April 2025: more than fifty California foundations and civic organizations signed a coalition letter, coordinated by the San Francisco Foundation and Latino Prosperity, formally requesting that the AG halt the conversion until: (1) the full market value of OpenAI’s nonprofit assets had been calculated, and (2) the equivalent value had been transferred to independent nonprofit entities. The petition pegged the charitable-asset value at up to $300 billion.

The Lawrence Lessig amicus brief of April 2025: filed on behalf of twelve former OpenAI employees, asserting that OpenAI had “abandoned its nonprofit roots” and that Altman “was a person of low integrity who had directly lied to employees about the extent of his knowledge and involvement in OpenAI’s practices of forcing departing employees to sign lifetime non-disparagement agreements.”

The October 2025 settlement

Bonta’s resolution: the AG agreed to permit OpenAI’s conversion to a Public Benefit Corporation structure subject to negotiated concessions, including:

- The OpenAI Foundation retaining equity in the for-profit valued at approximately $130B (with additional ownership at future valuation milestones).

- Specific commitments on AI safety, including teenager-risk-mitigation obligations.

- A commitment that OpenAI would remain headquartered in California.

- Maintained nonprofit oversight of certain mission-critical decisions.

What the settlement did not require: full disgorgement of the difference between the nonprofit’s pre-conversion valuation and the for-profit’s post-conversion valuation. The coalition that had petitioned for halting the conversion characterized the settlement as inadequate, with Robert Weissman of Public Citizen calling it “a move by OpenAI to entrench a proven failed status quo.”

What the AG’s track still has open

The settlement covers the conversion structure; it does not foreclose all future regulatory action. If OpenAI’s actual conduct over the next 24 months diverges from the safety, governance, and charitable-purpose obligations in the settlement, the AG retains supervisory authority to revisit the agreement.

The IPO context: a public company is subject to additional regulatory frameworks — SEC disclosure obligations, public-company governance requirements, shareholder fiduciary duties — that did not apply to the pre-IPO private structure. Those frameworks layer on top of the AG’s existing oversight authority. The post-IPO OpenAI will be the most-regulated AI company in history by virtue of its dual status as a PBC with retained nonprofit oversight and a public company with SEC obligations.

The parallel-track observation

The Musk verdict closes one specific channel of legal challenge. The AG channel was resolved in October 2025 with concessions but no reversal. The SEC channel opens at IPO. The IRS nonprofit-conversion oversight channel runs separately. No single verdict can settle the totality of charitable-trust review for an entity of this size and structural complexity. The Musk verdict resolves the Musk-as-plaintiff question; it does not resolve the regulatory-oversight-of-OpenAI question.

VI · The IPO runway · the practical stake that was on the table

The capital-markets crystallization. The reason this case mattered enough to draw a three-week trial, testimony from Altman, Brockman, Nadella, and Musk himself, and an advisory jury sitting through detailed examination of charitable-trust law is straightforward: OpenAI is preparing for the largest technology IPO in history, and the Musk lawsuit was the single most-visible litigation overhang threatening that timeline.

The IPO numbers

The target valuation range: $852 billion (per Q4 2026 plans referenced in TradingKey analysis and consistent with reporting from multiple sources) to $1 trillion (the Reuters-reported upper bound).

The capital-raise target: minimum $60 billion, potentially more depending on market conditions at the time of listing.

The timing: Q4 2026 filing referenced as the working target by multiple sources, with a 2027 listing as the alternative path if 2026 doesn’t materialize. Internal targets discussed include filing in H2 2026.

The recapitalization completed: October 2025 conversion from nonprofit + capped-profit subsidiary to OpenAI Group PBC with the OpenAI Foundation retaining control.

The Microsoft commercial-agreement renegotiation: finalized May 2026, capping OpenAI’s revenue-share payments to Microsoft at $38B through 2030 (down from prior projected ~$135B trajectory). Microsoft retains resell rights through 2032 and approximately 27% ownership of OpenAI Group PBC.

The pre-IPO state of the file

Revenue trajectory: approximately $2B annualized at end of 2023 → $6B in 2024 → $20B confirmed by OpenAI’s CFO in January 2026 → approximately $25B in annualized revenue by February 2026.

Cash-flow profile: projected burn of approximately $27B in 2026 and $63B in 2027. OpenAI does not turn cash-flow positive until 2030 per the renegotiated Microsoft terms.

The major shareholders pre-IPO: Microsoft (~27%) · SoftBank · Thrive Capital · Abu Dhabi’s MGX · the OpenAI Foundation (the nonprofit, with equity valued at approximately $130B at conversion).

What the verdict cleared

The Musk lawsuit was the most-visible litigation that could have forced an IPO delay or a restructure-reversal. If Musk had won and Judge Gonzalez Rogers had ordered the for-profit dismantled, the IPO could not have proceeded under the announced structure. If she had ordered partial disgorgement, the IPO valuation would have collapsed and the underwriting syndicate would have repriced. If she had ordered Altman’s removal, the IPO would have been postponed for management-stability reasons alone.

With the verdict landing on procedural grounds: none of those outcomes are now in the active risk file. The IPO timeline advances without this specific overhang.

What the verdict did not clear

The California AG’s oversight authority remains in place. The October 2025 settlement is a binding agreement, not a closure of supervisory jurisdiction.

The SEC review at IPO filing remains in front of the company. OpenAI will need to disclose the entire restructuring history in its S-1, including the Musk litigation, the AG settlement, the coalition petition, the Lessig amicus brief, the AGI clause, the charitable-trust framework, and the contingent regulatory exposures. The S-1 will be the most-scrutinized AI-company prospectus ever filed.

The IRS nonprofit-conversion review framework remains open. The IRS has historically been able to examine the consideration paid by a for-profit successor entity for assets previously held by a nonprofit predecessor, and to assess whether the consideration meets the fair-market-value standard. OpenAI’s $130B equity allocation to the Foundation will face this examination if the IRS chooses to undertake it; the agency has not publicly indicated it will not.

Parallel litigation from differently-situated plaintiffs remains possible. The trial record from Musk v. Altman, including the testimony and the timeline development, will be available for future plaintiffs who can demonstrate standing and timing within the applicable statute of limitations.

The IPO-runway observation

The verdict cleared the single largest litigation overhang on the IPO timeline. It did not clear all the regulatory risk. The S-1 disclosures will need to address the underlying charitable-trust questions in the risk-factors section regardless of the Musk verdict. The valuation-supporting argument is now “we won the lawsuit on procedural grounds, the AG settled, and SEC review proceeds on its own track.” The valuation-undermining argument is now “the underlying legal question was not resolved on the merits and remains subject to regulatory and future-litigation challenge.” Underwriters will price the spread.

VII · The structural reading · what this signals for AI corporate governance in the public-company era

The synthesis crystallization. The Musk verdict is significant beyond the OpenAI IPO. It marks the moment AI corporate governance shifted from a private-company question regulated by state AG charitable-trust authority to a public-company question regulated by SEC, IRS, state AGs, federal regulators, and the ordinary course of shareholder litigation simultaneously.

Observation 1 · The charitable-trust question is unresolved at scale

The empirical signal: a $300B-charitable-asset-to-$852B-for-profit-PBC conversion just passed through a state AG settlement and a federal jury without the underlying charitable-trust theory being ruled on by an Article III court applying California Corporations Code § 5250 to the facts on the merits.

The forward shape: the precedent question — whether the California Supreme Court’s holding that nonprofit assets are “held in trust solely for such charitable purposes” allows the kind of value-capture the OpenAI restructure produced — remains a question waiting for a case where it can be properly litigated. The next nonprofit-to-PBC conversion at scale (Anthropic remains a Public Benefit Corporation already; Mistral, Cohere, and others operate under different structures, but the next charitable-trust-to-for-profit conversion in AI or adjacent fields) will face the same question without binding precedent. The Musk case did not become that precedent.

Observation 2 · The IPO calendar wins because the legal calendar lost

The empirical signal: Q4 2026 / 2027 IPO planning was on the runway before the verdict; it is on the runway after the verdict. The verdict’s timing relative to the IPO was exactly what OpenAI needed — a procedural dismissal that removes the litigation risk-factor disclosure complication without producing a substantive ruling that could be cited against the company in future proceedings.

The forward shape: the IPO calendar advances; the underwriting proceeds; the S-1 filing references the verdict as a procedural matter; the prospectus risk factors note the ongoing AG oversight and the possibility of future regulatory action without quantifying it. Investors price the spread between “the underlying question was settled” (which is not what happened) and “the underlying question was sidestepped on calendar grounds” (which is what happened).

Observation 3 · The Anthropic comparison is the structural mirror

The empirical signal: Anthropic — founded by ex-OpenAI personnel including Dario and Daniela Amodei in 2021 — was structured as a Public Benefit Corporation from inception. There was no nonprofit-to-PBC conversion to contest. The May 2026 Anthropic-Blackstone-Hellman & Friedman-Goldman Sachs joint venture ($1.5B PE-backed forward-deployed engineering vehicle) sits inside a corporate structure that is comparatively unambiguous from a charitable-trust standpoint.

The forward shape: the OpenAI charitable-trust overhang is unique to OpenAI’s specific founding history. Anthropic faces SEC scrutiny, AG oversight on AI safety, and regulatory pressure on enterprise practices — but not the specific charitable-asset-conversion question. If both companies IPO in 2026-2027, Anthropic’s S-1 will be structurally cleaner on this dimension; OpenAI’s S-1 will need to address the Musk case, the AG settlement, the coalition petition, the Lessig amicus, and the underlying restructure history. Investors will price that disclosure burden differently.

Observation 4 · The next plaintiffs are regulators, not founders

The empirical signal: Musk’s claim failed on standing-and-timing grounds. The underlying theory survives. The natural next claimants — California AG (already engaged), IRS (not yet engaged), SEC (engages at IPO), state attorneys general from other states (theoretical but possible), the OpenAI Foundation itself if its independent directors at some point dispute the for-profit’s conduct (also theoretical) — are all institutional rather than individual.

The forward shape: the next round of OpenAI corporate-governance litigation, if it happens, is most likely to come from regulatory rather than private-plaintiff sources. The institutional plaintiffs face different procedural barriers (they have standing automatically), different timing constraints (state and federal regulators have continuing jurisdiction rather than discrete statute-of-limitations windows for ongoing review), and different remedies available. The Musk case demonstrates that the charitable-trust theory can be argued in federal court at substantial expense. It also demonstrates that the procedural barriers to private-plaintiff litigation are significant. Future challenges may shift to the regulatory channel for both reasons.

What this is not

It is not a vindication of OpenAI’s underlying conduct. The trial court did not rule on whether the restructure was lawful under charitable-trust law. The jury did not consider that question. The verdict is a procedural disposition, not a substantive endorsement.

It is not a defeat for the charitable-trust theory. The theory was not litigated to a substantive ruling. It remains available for future plaintiffs with valid standing and timing.

It is not the end of OpenAI’s regulatory exposure. The AG settlement remains in place. SEC review begins at IPO filing. IRS examination is at the IRS’s discretion. Parallel state-level inquiries remain possible.

It is not a clean win for Sam Altman personally. The trial laid bare the timeline of OpenAI’s evolution, the asset and personnel transfers between the nonprofit and for-profit, the AGI-clause negotiation with Microsoft, the lifetime-non-disparagement agreement practice (as alleged by the twelve former employees through Lessig), and the magnitude of Altman’s enrichment via the PBC conversion. The court did not rule on whether any of that conduct was lawful; it ruled that Musk could not be the one to litigate it. That distinction will matter to future regulators, to future litigation, to future shareholders, and to the public record on this transition.

The synthesis observation

The verdict is a tactical win for OpenAI that does not deliver a strategic win on the underlying legal question. The IPO calendar advances. The regulatory calendar continues to run. The legal-precedent calendar remains open. The structural significance of the case is that it demonstrates the AI industry’s largest nonprofit-to-for-profit conversion can pass through one specific federal-court challenge on procedural grounds without producing the substantive ruling that would either settle or unsettle the underlying law. Whether that procedural-only outcome holds across subsequent regulatory and litigation challenges is the open question of OpenAI’s transition to public-company status.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that on May 18, 2026, the calendar technicality cleared OpenAI’s path to the largest tech IPO in history without resolving whether the path itself is consistent with the original charitable trust the company was built on. The next 12-24 months will determine whether that procedural clearance survives the more-rigorous scrutiny of S-1 disclosures, IRS conversion review, state-level continuing oversight, and the ordinary-course shareholder fiduciary-duty litigation that will inevitably follow the public listing.

That is the structural editorial question the calendar technicality is sitting on top of. It is procedural, not substantive. It is one case, not the whole legal-precedent question. It is the IPO runway, not the underlying law. And it is the layer where the next phase of AI industry governance gets decided — by regulators, by the SEC review process at IPO filing, by future plaintiffs with valid standing and timing, and by the underwriting syndicate that has to price the spread between procedural win and substantive uncertainty.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Governance & Corporate Structure track

This dispatch

- This piece · The calendar technicality · structural reading of the Musk v. Altman procedural dismissal and what it does and does not settle about the underlying charitable-trust theory · structural-slate register

Forthcoming · the corporate-governance track

- Forthcoming · The S-1 disclosure burden · how OpenAI’s prospectus will need to address the underlying charitable-trust history, the AG settlement, the Lessig amicus, and the AGI clause · transition-bronze register

- Forthcoming · The IRS nonprofit-conversion review · the parallel federal track and what historical Blue Cross / Highmark / similar charitable-conversion precedents suggest · empirical-clay register

- Forthcoming · The Anthropic structural mirror · why the PBC-from-inception structure produces a cleaner IPO disclosure profile and what that means for valuation spread · alternative-sage register

- Forthcoming · The institutional-plaintiff channel · who can bring future charitable-trust challenges with valid standing and timing, and what they could plausibly recover · labor-rose register

- Forthcoming · The AGI clause forensic · the Microsoft-OpenAI partnership’s AGI-voids-the-deal provision and what triggering it would mean for the public-company structure · synthesis-deep register

Adjacent tracks

- The CFO’s new operating system · Enterprise Reorg 01 · structural reading of Anthropic’s May 4-14 launch sequence and the PE-backed JV deployment model that this piece’s IPO calendar will compete with for enterprise capital

- The bank account in the chat · Agentic Commerce 01 · consumer-side intermediation analysis · OpenAI’s parallel consumer play running on the same IPO calendar

- The gigawatt gap · AI Energy & Infrastructure 01 · the industrial-policy dispatch · what the IPO proceeds will be spent on

- Post-Wire Piece 01 · The death of the identical paragraph · Post-Wire 01 · publisher-side intermediation forensics · adjacent structural analysis at a different layer of the AI stack

Sources

The verdict and trial

- TechCrunch · Elon Musk has lost his lawsuit against Sam Altman and OpenAI — unanimous nine-juror verdict · statute-of-limitations dismissal · judge’s “devoid of connection to the underlying facts” reaction to Wazzan · Musk’s “WHEN they did it” tweet · Bill Savitt’s “after-the-fact contrivance” framing · techcrunch.com

- NPR · Jury dismisses all claims in Musk lawsuit — verdict timing (10:23 AM Pacific note, 8:30 AM deliberation start) · damages framework being heard when verdict landed · Musk’s $38M-over-several-years donation history · Sarah Eddy’s “no charitable trust to enforce” closing · npr.org

- CNBC · Musk slams Altman trial verdict as a ‘technicality,’ vows to appeal — Musk’s appeal announcement · Toberoff’s “preserving charities from this kind of exploitation” framing · 2018 Musk-OpenAI departure context · xAI 2023 founding · cnbc.com

- Wikipedia · Musk v. Altman — case procedural history · Lessig April 2025 amicus brief · OpenAI April 2025 countersuit · $44M-2016-2020 contribution range · Rogers’s “existential risk outside scope” pretrial ruling on Stuart Russell · trial witness list · en.wikipedia.org

- Entrepreneur · Musk lost $150 billion lawsuit — disgorgement framing · path-to-IPO context · entrepreneur.com

- Decrypt · Musk loses $150 billion AI lawsuit — verdict mechanics · post-verdict statements · decrypt.co

- TechTimes · Musk v. OpenAI Jury Begins Deliberating — Bonta October 2025 agreement context · teenager-risk-mitigation obligations · 700M weekly ChatGPT users · techtimes.com

The damages framework

- Dr. C. Paul Wazzan expert testimony — $78.8B to $135B “wrongful gains” range · proportional-share-of-value methodology · judge’s “devoid of connection” reaction

- The remedy demands — disgorgement to OpenAI Foundation · Altman and Brockman dismissal · for-profit entity dismantling · up to $150B aggregate exposure depending on valuation moment

The California AG track

- San Francisco Foundation coalition petition · April 2025 — fifty-plus California foundations and nonprofits · $300B charitable-asset valuation · request to halt conversion until asset valuation and transfer to independent nonprofits · sff.org

- California AG investigation · December 2024 — Deputy AG Christopher Lamerdin letter · charitable-trust framework · “irrevocably dedicated to charitable purpose” · route-fifty.com

- Bonta October 2025 settlement — PBC conversion permitted with concessions · Foundation retains $130B equity · teenager-risk mitigation · California headquarters commitment · Weissman’s “entrench failed status quo” critique · sfexaminer.com

- Public Citizen letter to AG — charitable-trust dissolution framework · Blue Cross of California precedent · California Supreme Court holding on charitable purpose · citizen.org

The IPO runway

- Sacra · OpenAI revenue, valuation & funding — Q4 2026 IPO target · up to $1 trillion valuation · Cynthia Gaylor (ex-DocuSign CFO) as head of investor relations · Microsoft renegotiated agreement May 2026 ($38B revenue-share cap, down from $135B trajectory) · 27% Microsoft equity · $25B annualized revenue Feb 2026 · 2030 cash-flow-positive target · sacra.com/c/openai

- CMC Markets · OpenAI IPO investor guide — $830B pre-IPO funding round reference · $500B October 2025 employee share sale · $20B end-2025 confirmed ARR per CFO · timeline-could-slip risk factors · cmcmarkets.com

- Marketing AI Institute · OpenAI restructure — November 2025 PBC conversion details · nonprofit retained control framing · AGI clause references · Reuters $1T reporting · marketingaiinstitute.com

- TradingKey · OpenAI IPO Stumbling Block — $852B target valuation · Q4 2026 plans · Musk-lawsuit-as-IPO-disruption framing · disgorgement scenarios · tradingkey.com

- Technerdo · OpenAI’s $1 Trillion IPO — full breakdown · revenue trajectory · restructuring history · technerdo.com

The Anthropic structural mirror

- The CFO’s new operating system · Thorsten Meyer · Enterprise Reorg 01 · Anthropic’s $1.5B Blackstone + H&F + Goldman Sachs JV · PBC-from-inception structure · adjacent IPO calendar · the parallel commercial dynamics on a different corporate-governance baseline

California charitable-trust legal framework

- California Corporations Code § 5250 — charitable corporations’ fiduciary obligations · assets dedicated to charitable purpose

- California Code of Civil Procedure § 338 + § 343 — three-year statute of limitations framework

- California Supreme Court precedent — charitable-corporation assets “held in trust solely for such charitable purposes” framing referenced in coalition and Public Citizen petitions

Key Piece reference figures crystallized

- Verdict: May 18 2026 · unanimous nine-juror dismissal · under two hours deliberation · adopted by Judge Yvonne Gonzalez Rogers · U.S. District Court for the Northern District of California

- The legal mechanism: statute-of-limitations dismissal · three-year window · 2024 filing v. 2021 latest-knowable harm

- The damages framework not reached: $78.8B to $135B “wrongful gains” · up to $150B aggregate exposure · disgorgement to OpenAI Foundation · Altman and Brockman dismissal · for-profit dismantling

- The IPO runway: Q4 2026 / 2027 target · $852B-$1T valuation · ~$60B raise · $25B annualized revenue Feb 2026 · 2030 cash-flow positive

- The Bonta October 2025 settlement: $130B Foundation equity retained · safety obligations · California HQ commitment · permitting conversion with concessions

- The coalition petition: 50+ California foundations · $300B charitable-asset valuation · April 2025 · halt-the-conversion request denied

- The amicus brief: Lawrence Lessig + 12 former OpenAI employees · April 2025 · “abandoned nonprofit roots” · “low integrity” framing

- The corporate-structure mirror: Anthropic PBC-from-inception · $1.5B JV with Blackstone + H&F + Goldman · adjacent IPO calendar · structurally cleaner S-1 disclosure profile

- What the verdict cleared: the Musk-as-plaintiff channel

- What the verdict did not clear: AG continuing oversight · SEC review at IPO filing · IRS nonprofit-conversion examination · parallel litigation from differently-situated plaintiffs · the underlying charitable-trust legal question