In 18 months between November 2024 and May 2026, the AI lab business model for enterprise finance reorganized from “sell models to CFOs” to “vertically integrate the implementation, capture the consulting margin, and ship pre-built agent templates for the most-billed parts of investment banking, equity research, private equity, wealth management, accounting, and Office of the CFO operations.”

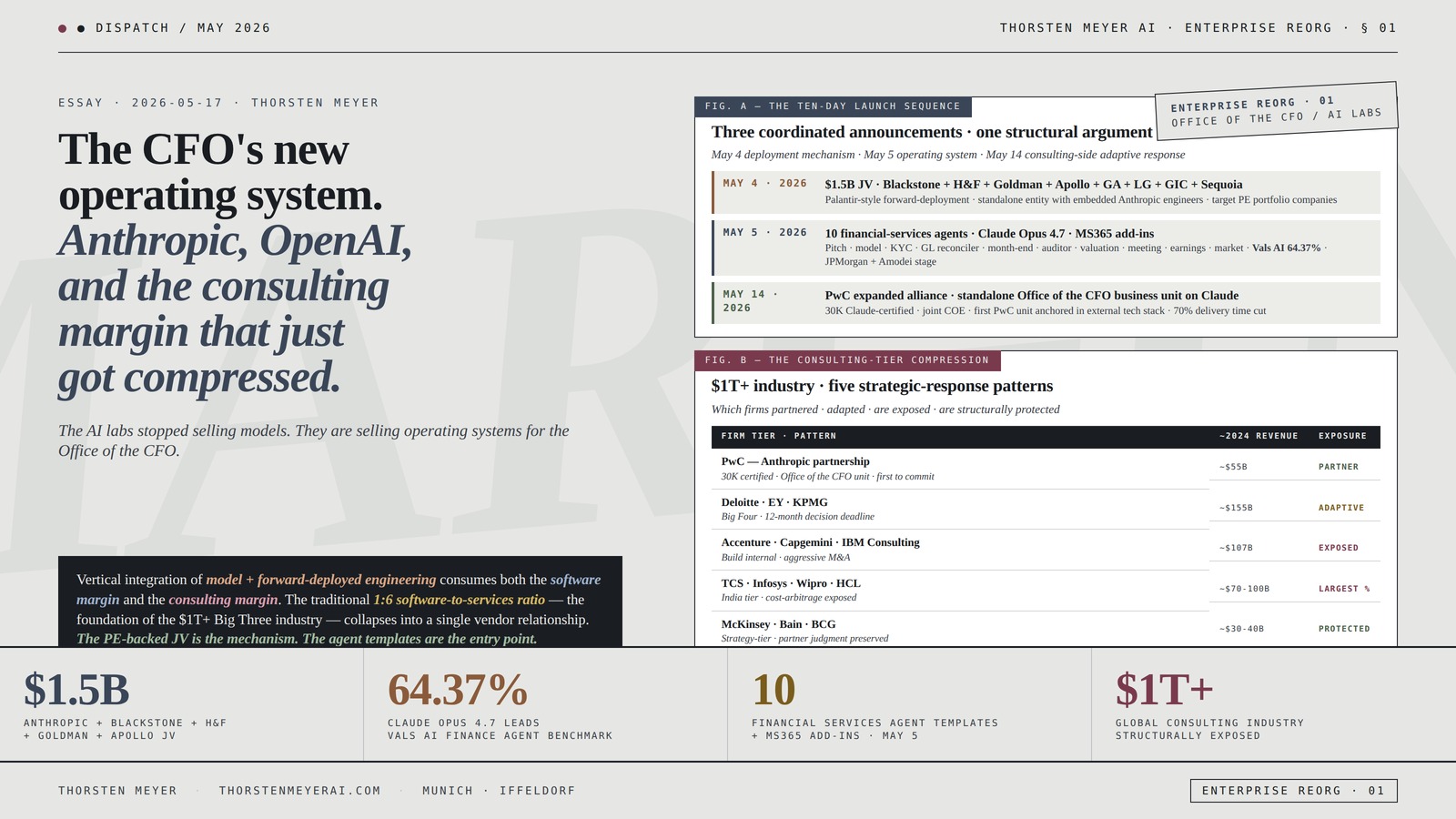

On May 4, 2026, Anthropic announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs (plus Apollo, General Atlantic, Leonard Green, GIC, and Sequoia) to embed Claude inside PE portfolio companies at Palantir-style forward-deployment economics.

On May 5, the company launched ten ready-to-run financial-services agents on Claude Opus 4.7 — pitch builder, model builder, KYC screener, GL reconciler, month-end closer, financial statement auditor, valuation reviewer, meeting prep, earnings reviewer, market researcher — paired with Microsoft 365 add-ins for Excel, PowerPoint, Word, and Outlook so context carries across the daily-billed analyst stack without re-explanation.

Claude Opus 4.7 leads the Vals AI Finance Agent benchmark at 64.37%. On May 14, PwC announced an expanded strategic alliance — 30,000 Claude-certified professionals, a joint Center of Excellence, and the first standalone PwC business unit anchored in Anthropic technology: an Office of the CFO group built on Claude. OpenAI is pursuing a parallel structure: a Bloomberg-reported separate joint venture with private-equity firms expanding adoption of its tools, and a $4B raise on a $10B valuation for the venture.

The share data has shifted accordingly: Anthropic’s share of US enterprise AI spending climbed to approximately 40% by early 2026 while OpenAI’s fell from 50% to 27%; Ramp’s April 2026 corporate-card data has Anthropic at 34.4% paid business adoption vs OpenAI at 32.3% — the first time Anthropic has led on the business-adoption metric. The structural significance of this is not the agent templates. It is the deployment architecture wrapped around them.

The traditional pattern — software vendor sells license, customer hires consultant to implement, takes 18-36 months and 5-10x the software cost — is being replaced by a vertically integrated model where the AI lab brings the implementation, the PE capital backs the forward-deployed engineering, the consulting margin compresses, and the CFO function reorganizes around managed agents that get deployed in weeks rather than years.

This essay walks what shipped, how it’s architected, what gets compressed, how PwC’s partnership-not-competition response reads against the alternative, what OpenAI’s parallel structure tells us about the second-mover dynamic, what the share data signals about the enterprise inversion already in progress, and what consumer-grade fintech and PE-grade finance ops look like once the AI labs are vertically integrated into both.

The CFO’s new

operating system.

Anthropic, OpenAI,

and the consulting

margin that just

got compressed.

+ Goldman + Apollo + others JV

Finance Agent benchmark

+ MS365 add-ins shipped May 5

structurally exposed to compression

The AI labs stopped selling models. They are selling operating systems for the Office of the CFO — and the layer that historically sat between the software vendor and the enterprise, the consulting tier, is what gets vertically captured.Thorsten Meyer · The CFO’s New Operating System · Enterprise Reorg 01

By Thorsten Meyer — May 2026

This is a dispatch on the consolidation move that just happened — and on its consulting-side sibling. The personal-finance piece earlier this week walked the consumer-side intermediation transfer; this one is the enterprise-side equivalent. Same structural argument applied to a different stack: the chat layer is taking delivery of the work, the AI lab is taking delivery of the implementation, and the intermediation tier that historically sat between the software vendor and the enterprise — the Big Three consulting firms, the technology-implementation consultancies, the boutique AI integrators — is the layer that re-prices.

The structural argument I want to make: Anthropic and OpenAI have stopped selling models. They are selling operating systems for the Office of the CFO, packaged as vertical-specific agent templates, deployed by forward-deployed engineers backed by PE capital, integrated into Microsoft 365 so the work happens inside the workflow rather than alongside it. The $1.5B Anthropic-PE joint venture is the deployment mechanism; the 10 finance agents are the operating system; the PwC Office of the CFO standalone unit is the consulting-side adaptive response that demonstrates the alternative. OpenAI’s parallel $4B raise for an equivalent JV is the second-mover validation. The share data — Anthropic 40% / OpenAI 27% in enterprise; Ramp’s first-time Anthropic-leads-paid-adoption data — is the empirical signal that the inversion is already happening. The consulting tier ($1T+ industry) is the structurally compressed party. The CFO function itself reorganizes around managed agents in 18-36 months. What this means for the IPO storyline at both Anthropic and OpenAI is that the enterprise revenue base — not the consumer chat product — is the load-bearing argument for the valuations.

The headline integrative finding: Vertical integration of model + implementation + workflow integration consumes both the software margin and the consulting margin. The traditional ratio (1 software dollar : 6 services dollars) is being collapsed into a single vendor relationship at a fraction of the cost. The PE-backed forward-deployment model is the mechanism. The named workflow agents are the entry points. The MS365 add-ins are the surface. The consulting tier responds either by partnership (PwC pattern) or by direct disruption (the JV-versus-Big-Three pattern). The empirical scoring at the model layer (Vals AI Finance Agent 64.37% on Claude Opus 4.7) demonstrates the capability is now sufficient for analyst-grade work — staged for human sign-off, but performant. Anthropic and OpenAI are not adjacent to enterprise finance any more. They are inside it.

This essay walks what shipped in the Anthropic May 4 / May 5 double-launch (Section I), the deployment-architecture innovation that the PE-backed JV represents (Section II), the 10 financial-services agent templates and what they replace (Section III), the PwC alliance as the canonical adaptive response from the consulting tier (Section IV), OpenAI’s parallel structure and the share-data inversion (Section V), the consulting-margin compression math at the industry tier (Section VI), and the structural reading of what enterprise finance looks like 24 months out (Section VII).

I · What shipped · the May 4-14 timeline

The launch-density crystallization. In ten days at the start of May 2026, three structurally significant announcements landed. They are not independent. They are the three legs of a single coordinated move.

May 4 · the $1.5B joint venture · Blackstone + Hellman & Friedman + Goldman Sachs + the full PE syndicate

The empirical announcement: Anthropic, Blackstone, Hellman & Friedman, and Goldman Sachs unveiled a $1.5B-capitalized joint venture to deploy Claude inside mid-market enterprises, especially PE portfolio companies. Anthropic, Blackstone, and Hellman & Friedman each contributed approximately $300M; Goldman Sachs approximately $150M; Apollo Global Management, General Atlantic, Leonard Green, Singapore’s GIC sovereign wealth fund, and Sequoia Capital participated alongside. Total committed: $1.5B against a target market estimated at the $1T+ consulting tier and the broader enterprise services category.

The structural mechanism: the venture is a standalone entity with Anthropic engineering resources embedded directly within its team. Per Anthropic CFO Krishna Rao: “Enterprise demand for Claude is significantly outpacing any single delivery model. This new firm brings additional operating capability to the ecosystem.” Per Goldman Sachs’ Marc Nachmann: the venture would help “democratize access to forward-deployed engineers” for companies that currently can’t afford the talent or the consulting fees to build AI systems on their own. Per Blackstone’s Jon Gray: it would break down “one of the most significant bottlenecks to enterprise AI adoption” — the scarcity of engineers who can implement frontier AI systems at speed.

The structural innovation: this is a Palantir-style forward-deployment model, capitalized by PE rather than by traditional consulting partnerships, with the AI lab owning both the model layer and the implementation layer. No previous software vendor has had this distribution channel at this scale, with this level of capital backing, and this degree of vertical integration with the underlying model technology.

May 5 · 10 financial-services agents on Claude Opus 4.7 + Microsoft 365 integration

The product announcement: Anthropic released ten purpose-built financial-services agent templates, available as plugins in Claude Cowork and Claude Code, and as cookbooks for Claude Managed Agents (the platform-deployed agent product). The templates: Pitch builder · Meeting prep · Earnings reviewer · Financial model builder · Market researcher (research-side) · General ledger reconciler · Month-end closer · Financial statement auditor · KYC screener · Valuation reviewer (operations and controls-side).

The model: Claude Opus 4.7 — Anthropic’s most capable model — leads the Vals AI Finance Agent benchmark at 64.37%, positioning it as the highest-scoring model on financial reasoning tasks at launch.

The integration: full Microsoft 365 add-ins generally available for Excel, PowerPoint, and Word, with Outlook in beta. Context carries automatically between applications — a financial model started in Excel does not need to be re-explained when it moves into a PowerPoint deck or an Outlook email draft. This is structurally important: the daily-billed analyst stack at investment banks, accounting firms, PE shops, and corporate finance functions runs entirely inside Microsoft 365.

The data partners announced alongside: Dun & Bradstreet (business identity) · Fiscal AI (real-time public-equity fundamentals) · Financial Modeling Prep (real-time quotes, fundamentals, filings, transcripts across equities, ETFs, crypto, forex, commodities) · Guidepoint (100,000+ compliance-reviewed expert interview transcripts) · IBISWorld (industry-level revenue, financial ratios, risk scores, cost structures across thousands of sectors) · SS&C Intralinks (DealCenter AI data-room access) · Third Bridge (expert calls) · Verisk (insurance data). Moody’s launched a separate MCP app surfacing proprietary credit ratings and data on 600M+ public and private companies.

May 5 · the JPMorgan dimension

The product announcement was made at Anthropic’s invite-only “Briefing: Financial Services” event in New York, the first-ever shared stage appearance of Anthropic CEO Dario Amodei and JPMorgan CEO Jamie Dimon. Dimon described having logged into Claude Code over the previous weekend and asking it to assemble a dashboard on Treasury bid-ask spreads, asset swaps, and investment-grade markets — “and in 20 minutes it created a huge dashboard, with all the backup, and all the research, and it was very accurate about what I wanted.” Amodei used the moment to disclose that Anthropic’s projected 10× revenue growth over a recent period had instead come in at approximately 80× annualized growth in one quarter — “the cone is even wider than I thought.”

May 14 · the PwC expanded alliance

The strategic-partnership announcement: PwC and Anthropic announced an expansion of their strategic alliance covering three areas of “highest leverage”: agentic technology build · AI-native deal-making · reinvention of the enterprise function. PwC will deploy Claude Code and Cowork starting with US teams and expanding toward a global workforce of hundreds of thousands of professionals. The companies are establishing a joint Center of Excellence and a program to train and certify 30,000 PwC professionals on Claude.

The standalone business unit: PwC is launching a new finance business group (Office of the CFO) built on Claude as the first standalone business unit anchored in Anthropic’s technology. This is the first time PwC has structured a business unit around an external technology partner’s stack rather than around its own services framework.

The deployment scale signal: “Most enterprises are still running on systems and processes built for a pre-AI world — a drag that is estimated to be more than $2 trillion.” Production-use cases Anthropic disclosed alongside the PwC announcement: insurance underwriting reduced from 10 weeks to 10 days · security work that took hours now takes minutes · “production across professional sports operations, insurance underwriting, mainframe modernization, HR transformation, and cybersecurity — cutting delivery times by up to 70%.”

The ten-day-window observation

Three coordinated announcements. One structural argument. The May 4 JV is the deployment mechanism; the May 5 agents are the operating system; the May 14 PwC alliance is the consulting-side adaptive response. Anthropic has demonstrated in ten days that the model + implementation + workflow integration can be delivered together at scale. OpenAI’s parallel structure (BNY · BBVA · ServiceNow workflow partnerships · the $4B-raise-at-$10B-valuation JV) confirms this is the category-level move, not an Anthropic-specific play.

Financial Modeling and Reporting with Microsoft Power BI: Build models, KPIs, and modern finance reports in Power BI from scratch

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The deployment-architecture innovation · why the $1.5B JV is the structurally significant launch

The forward-deployment crystallization. The $1.5B JV is the launch that does the structural work. The agent templates are the entry point; the deployment vehicle is what allows them to land at scale in 18 months rather than the 36-60 months traditional enterprise-software adoption typically requires.

The traditional enterprise-software pattern

The historical ratio: for every $1 enterprises spend on software, they spend approximately $6 on services. This 1:6 software-to-services ratio is the foundation of the $1T+ Big Three consulting industry (Accenture · Deloitte · EY · KPMG · IBM Consulting; plus McKinsey, Bain, and BCG on the strategy side; plus Capgemini, Wipro, TCS, Infosys on the implementation side).

The deployment timeline: enterprise software typically takes 18-36 months from license signature to production rollout. For finance-function transformations, the timeline runs longer — typical SAP S/4HANA migration or Workday Financials implementation in a Fortune 500 takes 3-5 years. The Anthropic / PE-backed JV explicitly targets compression of this timeline to weeks-to-months for individual workflows, and 6-18 months for full Office of the CFO transformations.

The talent constraint: the binding constraint on enterprise AI adoption has been the scarcity of engineers who can implement frontier AI systems at production scale. Per Blackstone’s Jon Gray, this is “one of the most significant bottlenecks to enterprise AI adoption.” Per Goldman Sachs’ Marc Nachmann, the JV’s purpose is to “democratize access to forward-deployed engineers” for companies that can’t afford the talent.

The Palantir analog

Palantir Technologies pioneered the forward-deployment model in the 2000s-2010s, embedding engineers directly inside customer organizations (intelligence agencies first, then commercial enterprises) rather than selling licenses and leaving implementation to the customer or to consultants. The model produced higher-margin, longer-term contracts because the deployed engineers became indispensable to customer operations.

Palantir’s market validation: $100B+ market cap by 2024, ~$3B 2024 revenue, ~80% gross margin, ~25% operating margin at maturity. The model is profitable, defensible, and produces strong customer retention.

The Anthropic / PE-backed JV is a Palantir-style structure with two important differences: (1) the JV is capitalized by PE rather than by retained earnings, allowing much faster scaling — $1.5B in committed capital available immediately for hiring forward-deployed engineers, versus Palantir’s gradual scale-up; (2) the customer pipeline is pre-built into the structure — Blackstone, Hellman & Friedman, Goldman Sachs, Apollo, General Atlantic, Leonard Green, and GIC collectively own portfolio companies numbering in the hundreds, with combined portfolio company revenue in the hundreds of billions of dollars. The deployment-target pipeline is the structural innovation.

The economics of the JV’s competitive position

The pricing arbitrage: traditional Big Three consulting engagements for enterprise AI transformation typically run $500-2,000 per hour for senior partners, $300-800 per hour for engagement managers, $150-400 per hour for senior consultants. A 6-month enterprise AI implementation might cost $5-25M in consulting fees alone, with the resulting solution still requiring customer-side maintenance and frequently failing to achieve the original business objectives.

The JV’s structural position: forward-deployed Anthropic engineers (with full access to Claude’s model layer and managed-agents infrastructure) embedded inside the customer organization, capitalized to deliver implementations at what Fortune characterized as “likely a fraction of the cost” of Big Three consulting. The cost arbitrage is plausibly 60-80%, with implementation timelines compressed by 50-70%.

The exit-value dimension: per Fortune’s earlier reporting, 85% of PE buyers now factor AI-enabled finance capabilities into company valuations at exit. PE-backed CFOs face mounting sponsor pressure to embed AI into planning, forecasting, and reporting. Firms that fail to integrate AI risk being penalized at exit. The JV offers PE sponsors a turnkey alternative to hiring Big Three consultants at a fraction of the cost, with the additional benefit of being capitalized by the same PE syndicate that will be evaluating the exit.

The deployment-architecture observation

The $1.5B JV is not a feature launch. It is a re-platforming of the enterprise-software-to-services bundle. The traditional 1:6 software-to-services ratio is being collapsed into a single vendor relationship. The implementation talent that was previously hired through Big Three consulting is being delivered directly by the AI lab through PE-backed embedded engineering. The consulting margin that previously sat between the software vendor and the enterprise is being captured by the AI lab’s own operation. This is the structurally significant move.

AI Tools for Real Estate Agents: The 1-Hour Setup Guide to AI Workflows That Save 5+ Hours a Week (AI Workflows for Real Estate Agents)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The ten financial-services agent templates · what gets replaced inside the firm

The workflow-agent crystallization. The 10 agents Anthropic shipped on May 5 are not generic AI assistants. They are reference architectures for specific finance workflows that map directly to existing analyst and operator roles, with packaged skills, connectors, and subagents that can be deployed in days rather than months. The structural significance is what each one replaces in the daily-billed work of finance professionals.

Research-side · what investment banks and equity research replace

Pitch builder: takes a target list and underlying data, produces a comps model in Excel + a draft pitchbook in PowerPoint + a cover note in Outlook. What it replaces: 20-40 hours of associate-and-VP-tier work per pitch. Investment banking groups historically run 200-500 pitches per analyst per year at major bulge-bracket firms; the cost per pitch in associate hours is approximately $5-15K. The Pitch builder agent compresses this to roughly 2-8 hours of human review-and-approval per pitch.

Meeting prep: assembles client meeting materials (financials, recent news, recent broker research, comparable transactions, sector positioning) from the connected data sources. What it replaces: 4-12 hours of analyst-tier preparation per client meeting. At ~$200-400 per loaded analyst hour, this is approximately $800-4,800 per meeting compressed to roughly 1 hour of review.

Earnings reviewer: reads earnings transcripts and SEC filings, flags model updates relevant to the analyst’s coverage. What it replaces: 6-12 hours of analyst work per earnings cycle per covered name. For a sell-side equity research analyst covering 12-20 names through quarterly earnings, this is 72-240 hours per quarter (roughly 18-60% of an analyst’s quarter) compressed.

Financial model builder: constructs financial models in Excel and audits formula correctness. What it replaces: 20-60 hours of model construction per deal or per coverage initiation. The Vals AI Finance Agent benchmark at 64.37% on Claude Opus 4.7 is the empirical demonstration that the model-building work is now within reach of analyst-grade quality — staged for human review, but performant.

Market researcher: tracks sector and issuer developments, synthesizes news + filings + broker research, and flags items for credit or risk review. What it replaces: 10-20 hours per week of analyst-level monitoring work per coverage area.

Operations-and-controls-side · what controllers, auditors, and compliance replace

GL reconciler: reconciles general ledger entries with subledger and supporting documentation. What it replaces: 40-120 hours of accountant-tier reconciliation work per month-end close. A typical Fortune 500 finance department runs 10-30 separate reconciliations during month-end close; the GL reconciler agent compresses this from days to hours.

Month-end closer: orchestrates the month-end close workflow — accruals · adjustments · intercompany eliminations · variance analysis · management reporting. What it replaces: 5-10 business days of controller-tier work compressed to 1-2 business days, with the human role shifting to exception handling and review rather than data assembly.

Financial statement auditor: reviews financial statements, identifies anomalies, traces transactions to supporting documentation, flags items for human auditor review. What it replaces: 30-50% of the audit-team time historically spent on routine substantive testing. The Big Four audit firms (Deloitte, EY, KPMG, PwC) collectively bill ~$160B annually for audit-and-assurance services; this is the layer of the audit fee that compresses.

KYC screener: assembles entity files for know-your-customer review, packages escalations for compliance teams, traces beneficial ownership across complex ownership structures. What it replaces: 6-20 hours of analyst-tier compliance work per onboarded entity. KYC is currently one of the most cost-inflationary parts of banking operations — global spend on KYC and AML compliance exceeded $200B annually by 2024. The KYC screener agent is the canonical example of regulatory-process compression.

Valuation reviewer: stress-tests inputs and assumptions in an existing financial model, identifies model errors, flags assumption sensitivities. What it replaces: 8-16 hours of senior-analyst-tier review per model. Equity research, M&A, and corporate development teams produce thousands of valuation models annually; the Valuation reviewer agent compresses the review layer.

Deployment surfaces and the MS365 integration

Each template ships three ways: (1) as a Cowork plugin that runs alongside the analyst’s existing desktop software; (2) as a Claude Code plugin for engineering-tier deployments; (3) as a Claude Managed Agent cookbook that deploys autonomously on the Claude Platform with long-running sessions, per-tool permissions, managed credential vaults, and full audit logs in the Claude Console.

The Microsoft 365 integration: Claude add-ins for Excel · PowerPoint · Word are generally available; Outlook is in beta. Once installed, context carries between applications automatically — a financial model started in Excel does not need to be re-explained when it moves to PowerPoint or Outlook. This is the surface where the daily-billed analyst stack actually lives, and Anthropic shipped into it.

The vertical-skill bundle

The GitHub repository (anthropics/financial-services) organizes the templates into four vertical bundles: investment banking · equity research · private equity · wealth management. Each bundle includes the underlying skills (instructions and domain knowledge), connectors (governed real-time access to the data), and subagents (additional Claude models called for specific sub-tasks like comparables selection or methodology checks).

The disclaimer language

The repository explicitly disclaims: “Nothing in this repository constitutes investment, legal, tax, or accounting advice. These agents draft analyst work product — models, memos, research notes, reconciliations — for review by a qualified professional. They do not make investment recommendations, execute transactions, bind risk, post to a ledger, or approve onboarding; every output is staged for human sign-off.”

The agent-template observation

The 10 agents are not just productivity tools. They are workflow re-architectures that compress the routine analytical and operational work of investment banking, equity research, accounting operations, and compliance — each into a Claude-mediated workflow with human sign-off at the end. The structural impact is not that AI does the analyst’s job. The structural impact is that the analyst’s productivity-output ratio shifts by 3-10x, which means that fewer analysts produce the same output, or the same analysts produce dramatically more output. Either way, the headcount math at the firm shifts, the consulting fees that historically supported AI-transformation engagements compress, and the surface of where the work happens moves into Claude.

AI-driven CFO operational tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The PwC alliance · the canonical adaptive response from the consulting tier

The partnership-not-competition crystallization. PwC is one of the Big Four accounting and consulting firms (Deloitte, EY, KPMG, PwC) collectively employing approximately 1.5 million people globally and billing approximately $200B annually. The PwC-Anthropic alliance is the canonical example of consulting choosing partnership rather than getting disrupted.

The May 14 announcement details

The three areas of “highest leverage”: agentic technology build · AI-native deal-making · reinvention of the enterprise function.

The scale commitments: 30,000 PwC professionals to be trained and certified on Claude · global rollout across “hundreds of thousands of professionals” · joint Center of Excellence · Claude Code + Cowork deployed across US teams first, then global expansion.

The standalone business unit: PwC’s new Office of the CFO business group, built on Claude as the first standalone business unit anchored in Anthropic’s technology. Per PwC’s announcement, this targets “transforming client finance organizations with Claude.” Per Anthropic CEO Dario Amodei: “PwC has been leading AI’s expansion into the parts of the economy where accuracy and reliability are non-negotiable — financial services, healthcare, life sciences, cybersecurity — and the results are clear. Insurance underwriting that took 10 weeks now takes 10 days. Security work that took hours now takes minutes.”

The deployment-time signal: “cutting delivery times by up to 70%” across the listed verticals.

What this means for PwC’s positioning

PwC chose partnership over disruption. Rather than build its own AI implementation capability and compete with Anthropic’s PE-backed JV, PwC accepted the model and positioned itself as the human-touch wrapper around Claude. The 30,000 certified professionals are the implementation talent that Anthropic’s JV is also building — but PwC delivers them through its existing client relationships, partner network, and consulting brand.

The risk PwC has accepted: its services are now structurally dependent on Anthropic’s technology stack. If Claude pricing changes, if model capabilities shift, if Anthropic enters direct competition through the JV, PwC is exposed. PwC has bet that the value it adds — domain expertise, client relationships, audit-tier credibility, partner-level judgment — is durable even when the underlying technology is a partner’s model.

What this means for the other Big Three

Deloitte · EY · KPMG · Accenture face the equivalent strategic choice. Each can:

- Replicate the PwC model by partnering with Anthropic (likely) or OpenAI (also likely). Multiple firms can partner with multiple AI labs.

- Build internal AI implementation capability using OpenAI / Anthropic / Google / Mistral models through API access rather than through structured alliance.

- Build proprietary AI capability (the route Accenture appears to be pursuing through aggressive M&A in AI-services-specialist firms).

- Accept compression of the AI-implementation services line and double down on adjacent service lines (tax, audit-and-assurance, regulatory compliance, M&A advisory).

The strategic pressure is asymmetric: doing nothing is the most-exposed position. The Big Three firms that move first on structured alliances capture the early implementation contracts; the ones that move slowly face client expectations they cannot meet.

The McKinsey / Bain / BCG dimension

The strategy-consulting tier (McKinsey, Bain, BCG) is structurally distinct from the implementation-consulting tier (Big Three accounting, Accenture, etc.). McKinsey, Bain, and BCG bill at much higher rates ($1,000-5,000+ per hour senior-partner-tier) for strategic advisory work that historically required less technology implementation expertise.

The exposure pattern: the strategy-consulting tier is less directly disrupted by the JV-style forward-deployment model because the strategic-advisory work is more dependent on partner-level judgment, board-room presence, and longitudinal client relationships. However, the boundary between strategy and implementation is collapsing — McKinsey’s QuantumBlack acquisition (2015), Bain’s Vector capability, BCG’s BCG X — these are the strategy firms’ attempts to capture the implementation-services adjacency. The JV-style model puts pressure on this strategy-to-implementation extension.

The consulting-tier observation

PwC’s partnership choice is the canonical adaptive response. It demonstrates that the consulting tier can partner with the AI labs rather than competing with them — at the cost of being structurally dependent on the AI lab’s technology stack. Whether this trade is sustainable depends on whether the AI labs honor the partnership boundary or eventually compete directly with their consulting partners through the JV’s direct deployment channels. The Palantir precedent is instructive here: Palantir’s forward-deployment model has historically been complementary-to-consulting rather than competitive, but the JV’s PE-backed scale and Anthropic’s model-layer ownership make direct competition more feasible than Palantir alone ever managed.

Deloitte Dstart Journal: 6×9 inches composition notebook featuring 110 lined pages, white paper and glossy cover

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · OpenAI’s parallel structure · the second-mover dynamic and the share-data inversion

The category-level-move crystallization. Anthropic moved first and most visibly in the May 4-14 window. OpenAI is pursuing a structurally similar architecture on a parallel timeline. The share data tells the story of where this is converging.

OpenAI’s parallel JV

Bloomberg-reported structure: OpenAI is finalizing a separate joint venture with private-equity firms to expand adoption of its tools. Reuters and Bloomberg report a $4B raise on a $10B valuation for the venture, with named participants overlapping the Anthropic JV partners in some cases.

The target segment: same as Anthropic’s — PE portfolio companies and mid-market enterprises, “given that segment’s emphasis on efficiency and cost reduction.”

The structural read: this is second-mover validation of the deployment-architecture innovation. The fact that OpenAI is pursuing the same structure — PE-backed forward-deployed engineering JV for enterprise AI implementation — confirms that the category-level shift is not Anthropic-specific. It is the new enterprise AI go-to-market model.

OpenAI’s existing enterprise commitments

Workflow partnerships in flight: BNY Mellon, BBVA, ServiceNow (three-year workflow partnership). The ServiceNow deal in particular is structurally significant — ServiceNow is the dominant enterprise-workflow platform for IT operations, HR operations, and increasingly finance operations. OpenAI’s three-year ServiceNow partnership embeds OpenAI’s models inside the workflow surface that competes most directly with Microsoft 365 in the enterprise.

The personal-finance leg: as covered in the prior dispatch, OpenAI launched personal-finance features in ChatGPT Pro on May 15, 2026, with Plaid + forthcoming Intuit integration. The consumer-side play and the enterprise-side play run in parallel.

The share-data inversion

Industry research cited in Anthropic Claude Financial Agents 2026 CRE Investor Guide (May 5): “Anthropic’s share of US enterprise AI spending climbed to 40 percent by early 2026, while OpenAI’s share fell from 50 percent to 27 percent.” This is a 23-percentage-point swing in approximately 18 months.

Ramp Corporate Card AI Index (April 2026): Ramp tracks corporate card and invoice payments from 50K+ US businesses, making this a spend signal rather than a full market-share measure. April 2026 Ramp data: Anthropic 34.4% paid business adoption (up 3.8% MoM); OpenAI 32.3% (down 2.9%); overall AI use 50.6%. Anthropic took the paid business-adoption lead from OpenAI for the first time. Claude Code anchored much of the swing, expanding from technical teams into finance, legal, and adjacent functions.

Microsoft Copilot context: per the WinBuzzer analysis citing February 2026 data, Microsoft Copilot held 38.6% enterprise usage share with OpenAI at 25.7%. Anthropic’s tool-use and workflows API rose from 0% in January to 5.7% in February. The combined Microsoft+OpenAI footprint in enterprise is still larger than Anthropic’s standalone footprint by a significant margin — but the trajectory is moving toward Anthropic, particularly on the finance-services-specific vertical.

The capability-benchmark layer

Claude Opus 4.7 vs GPT-5.4 on Vals AI Finance Agent: Anthropic’s stated leadership at 64.37% positions it as the highest-scoring model on financial reasoning tasks at the May 2026 launch. This is consistent with the broader pattern: Claude has been the preferred model for analyst-and-operator-tier work because of its reliability profile. OpenAI’s GPT-5.5 (newer than 5.4, released in early 2026) scores comparably on general reasoning but trails on the vertical-specific finance benchmark.

The second-mover observation

OpenAI’s parallel structure validates the category-level shift; the share data shows Anthropic ahead at this particular moment in the finance vertical. The race is far from decided. The structural read: enterprise finance is now a head-to-head competition between two AI labs operating on the same deployment architecture (PE-backed forward-deployed engineering JVs), with the same target segment (PE portfolio companies and mid-market enterprises), with overlapping data-partner ecosystems (Anthropic has D&B / Moody’s / Verisk / Guidepoint; OpenAI has BNY / BBVA / ServiceNow / Plaid). Whoever executes faster on the implementation-talent side wins more market share; whoever maintains the capability lead on vertical-specific benchmarks wins more renewals.

VI · The consulting-margin compression math · the $1T+ industry that just got vertically attacked

The industry-tier crystallization. The structural argument is not abstract. The compression math at the consulting-tier industry level is large and the time horizon is short.

The consulting-tier baseline

Global consulting industry, 2024: approximately $1T+ in revenue. Approximately $300B at the Big Four (Deloitte ~$67B · PwC ~$55B · EY ~$50B · KPMG ~$38B), approximately $65B at Accenture, approximately $30-40B at McKinsey/Bain/BCG combined, approximately $200B+ at India-based implementation firms (TCS · Infosys · Wipro · HCL), plus the long tail of boutique firms and specialist integrators.

AI-transformation services subsegment (2024-2025 estimates): approximately $50-100B annually across all consulting firms. Growing 30-50% YoY pre-2026. This is the segment most directly exposed to the Anthropic / OpenAI JV-style models.

The 1:6 ratio that the JV model collapses

The historical ratio: $1 of software revenue is typically accompanied by $6 of services revenue. The Anthropic-PE JV explicitly targets this ratio, per Fortune’s analysis: “For every dollar companies spend on software, they spend six on services — a ratio that has made consulting a multitrillion-dollar industry and that AI-native firms are now positioning to disrupt.”

The compression math: if the JV-style model captures even half of the AI-transformation services subsegment by 2028, that is approximately $25-50B of consulting revenue absorbed into the AI lab + JV structure. At the higher end, this is the order of magnitude that creates visible compression at the Big Four revenue line.

The PwC adaptive response · what it costs PwC

PwC’s bet: partnership with Anthropic preserves PwC’s client relationships and adds Claude as an implementation accelerator. The trade: PwC gives up some of the consulting margin to Anthropic (through licensing fees and through the JV’s direct competition for PE-backed clients), but retains the client-relationship layer and the partner-judgment-and-trust layer that consulting historically owned.

The Office of the CFO group: PwC’s first standalone business unit anchored in an external technology partner’s stack. The strategic read: PwC has accepted that finance-transformation work will be Claude-mediated regardless of who delivers it — better to be the delivery partner than to be displaced.

The non-PwC Big Three pressure

Deloitte · EY · KPMG: each faces the choice PwC made first. Each has internal AI capability (Deloitte has been the most-public, with multi-billion-dollar internal AI investment commitments). Each will likely partner with at least one AI lab — Anthropic or OpenAI — within 12 months. Whoever does not partner faces accelerating share loss in the AI-transformation subsegment.

Accenture · Capgemini · IBM Consulting: more directly exposed because the AI-implementation-services line is a larger share of their revenue. Accenture’s response has been aggressive AI-firm M&A (acquiring smaller AI services specialists at significant multiples). Capgemini and IBM have similar strategies but smaller capital pools.

The India-based implementation firm dimension

TCS · Infosys · Wipro · HCL · Tech Mahindra: collectively the largest source of global software implementation talent, with hundreds of thousands of engineers and consultants. Their cost-arbitrage business model — Indian-based engineering talent delivering global enterprise software implementations at significantly lower hourly rates than Western consulting firms — is structurally exposed to the JV-style model. The JV’s forward-deployed engineering team is geographically located (likely US-based for the highest-margin engagements), but the agent-mediated implementation model means that fewer total engineer-hours are required per implementation. Compression at the India-based implementation tier could be larger in percentage terms than at the Big Four.

The compression-math observation

The compression is not hypothetical. The PwC adaptive response, the Accenture M&A strategy, the Big Four partnership pursuit, the India-based implementation firms’ margin pressure — these are visible market signals that the structural compression is already in motion. By 2028, plausible scenarios put consulting industry revenue 10-25% lower than the 2024 baseline, with the AI-transformation services subsegment specifically 30-60% compressed and reallocated to AI labs and their JVs. This is the order-of-magnitude reorganization that yesterday’s launch sequence sets in motion. Whether the consulting tier adapts (PwC pattern) or compresses (Accenture/Capgemini risk) or fragments (boutique-firm risk) is the open structural question.

VII · The structural reading · what enterprise finance looks like 24 months out

The synthesis crystallization. The May 2026 launches mark the moment the AI labs stopped selling models to finance functions and started selling operating systems for the Office of the CFO. The 24-month forward view sorts into four observations.

Observation 1 · The Office of the CFO reorganizes around managed agents

The empirical signal: 10 agent templates ship on Cowork + Code + Managed Agents; Vals AI Finance Agent benchmark at 64.37%; PwC standalone Office of the CFO unit launched; MS365 add-ins generally available for Excel, PowerPoint, Word, with Outlook in beta.

The forward shape: by mid-2027, the typical Fortune 500 Office of the CFO operates with managed agents handling roughly 60-80% of routine analytical and operational work — month-end close · GL reconciliation · variance analysis · financial statement preparation · KYC/AML screening · regulatory reporting · pitch and meeting preparation · valuation model building and review. The human-tier shifts to exception handling, judgment work, partner-level approval, and strategic finance. Headcount in the Office of the CFO either holds flat with significantly more output, or compresses by 20-40% with the same output. Both patterns are visible in early 2026 production deployments.

Observation 2 · The consulting tier bifurcates

The empirical signal: PwC partnered with Anthropic; Accenture pursued aggressive M&A; the Big Three face the strategic choice; the India-based implementation firms face the largest percentage compression.

The forward shape: by mid-2028, the consulting industry has bifurcated structurally:

- Adaptive partners (PwC pattern): have multi-AI-lab alliances, certified workforces, AI-anchored business units. Revenue holds approximately flat with shifted margin mix (lower per-engagement margin, higher per-engagement scale).

- Direct competitors (Accenture pattern): built or acquired internal AI capability, compete directly with AI labs on implementation. Revenue grows but margin compresses.

- Compressed firms: did not adapt fast enough; AI-transformation subsegment revenue absorbed by AI labs and JVs. Revenue declines 10-25%, particularly at the India-based implementation tier and at boutique AI-services specialists who lack the capital to compete at JV scale.

- Strategy-tier protected: McKinsey, Bain, BCG retain strategic-advisory pricing power but face implementation-services adjacency pressure.

Observation 3 · The IPO storyline rests on enterprise revenue

The empirical signal: Anthropic projected 80× annualized revenue growth in one quarter; targeted $20-26B revenue by end of 2026 (up from $7B run rate in October 2025); 80% of revenue from enterprise customers; 300,000+ business customers. OpenAI similarly enterprise-weighted with the $4B PE-backed JV raise and the BNY/BBVA/ServiceNow partnerships.

The forward shape: by Q4 2026 or 2027, both Anthropic and OpenAI are likely to IPO at valuations supported principally by enterprise revenue contracts and the forward-deployed-engineering deployment model — not by the consumer chat product. The “AI consumer success story” narrative gives way to the “AI enterprise revenue lock” narrative as the load-bearing argument for $500B-$1T public-market valuations. The valuations depend on the enterprise revenue base being durable, which depends on the JV-style deployment architecture continuing to deliver implementations faster and cheaper than the consulting alternative.

Observation 4 · The capital-allocation pattern reshapes the consulting alternative

The empirical signal: $1.5B Anthropic + Blackstone + H&F + Goldman JV; $4B OpenAI parallel raise; participation from Apollo, General Atlantic, Leonard Green, GIC, Sequoia. These are the same LPs that fund the Big Four’s institutional service contracts.

The forward shape: PE-backed JV vehicles become the dominant deployment mechanism for enterprise AI through 2028, with $20-50B+ of PE capital directly committed to AI-implementation joint ventures across the major AI labs. The consulting industry’s traditional employer-of-implementation-talent role gets disintermediated. The implementation talent (forward-deployed engineers) is hired directly into JV vehicles capitalized by the same PE syndicates that previously paid the consultants. This is the structural disintermediation move.

What this is not

It is not the end of consulting. Big Four audit, tax, regulatory advisory, M&A advisory, strategy consulting, and partner-judgment-tier work are protected by regulatory framework, longitudinal client relationships, and the human-judgment-trust layer. Consulting remains a $700-900B industry through 2028 even at the compressed scenario. What ends is the easy AI-implementation services growth that consulting expected to capture through 2025-2027.

It is not the end of the human in finance. The agent-templates are explicitly staged for human sign-off; the regulatory framework around fiduciary work and audit-tier credibility remains intact; the senior-judgment work at the partner / CFO / treasurer / chief auditor tier is structurally preserved. What compresses is the entry-level-and-mid-tier analytical work, which is precisely the work that built the headcount pyramid at investment banks, audit firms, and corporate finance functions for the past 40 years.

It is not a clean Anthropic win. OpenAI’s parallel structure, Microsoft’s Copilot footprint (38.6% enterprise usage), Google’s Gemini Enterprise, Mistral in Europe, domestic Chinese AI firms in their respective markets — all compete for the same enterprise-finance deployment market. What’s structurally won is the category-level shift; who wins inside the category is open. Ramp’s first-time-Anthropic-leads-paid-adoption data point is significant but not yet decisive.

The synthesis observation

The Office of the CFO is the canonical enterprise function for AI agent deployment because the work is structured, the data is structured, the deliverables are structured, the regulatory framework is structured, and the cost-savings ROI is calculable. Anthropic moved first and most visibly with the May 4-5-14 launch sequence. OpenAI is moving second with parallel architecture. PwC chose adaptive partnership; the other Big Three face the same choice with a 12-month deadline.

The structural compression is in the consulting margin. The structural capture is at the AI lab + PE-backed JV layer. The structural reorganization is inside the Office of the CFO itself, which operates with managed agents handling routine work and humans handling judgment work within 24 months. The IPO storyline at both major AI labs depends on this reorganization being durable and the enterprise revenue lock being defensible.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the AI labs are not selling models any more. They are selling operating systems for enterprise finance — packaged as agent templates, deployed by forward-deployed engineers, integrated into Microsoft 365, capitalized by PE, and shipped at velocity that the traditional enterprise-software-and-consulting bundle cannot match.

That is the structural editorial question the CFO’s new operating system is sitting on top of. It is intermediation, not feature. It is implementation-and-talent capture, not just model sales. It is the consulting tier’s first existential structural challenge in 40 years. And it is the layer of enterprise AI where the next generation of category leadership gets decided — most likely by Q4 2027, by which time the enterprise revenue lock at one or both major AI labs is either structurally durable or structurally exposed.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Enterprise Reorganization track

This dispatch

- This piece · The CFO’s new operating system · structural reading of the Anthropic May 4-5-14 launch sequence, the OpenAI parallel structure, and the consulting-margin compression that just got priced in · structural-slate register

Forthcoming · the enterprise reorganization track

- Forthcoming · The consulting-tier compression · Big Four and Big Three forensic — Deloitte / EY / KPMG / Accenture / Capgemini / IBM Consulting exposure and adaptive response · labor-rose register

- Forthcoming · The Palantir model at scale · what PE-backed forward-deployed engineering economics look like when capitalized at $5B+ per AI lab · empirical-clay register

- Forthcoming · The Office of the CFO unbundling · what changes inside the actual finance function when 10 named agents handle the work that 50 analysts used to · structural-slate register

- Forthcoming · The IPO storyline · how enterprise revenue locks become the load-bearing valuation argument for both major AI labs · synthesis-deep register

- Forthcoming · The vertical-agent economics · the Cowork / Managed Agents / MS365 stack as the new enterprise software margin · transition-bronze register

Adjacent tracks

- The bank account in the chat · Agentic Commerce 01 · consumer-side intermediation transfer (Plaid + ChatGPT) · same structural argument applied to the consumer surface

- The gigawatt gap · AI Energy & Infrastructure 01 · industrial-policy analysis at the physical-infrastructure layer · what enables the model layer that this piece’s deployments run on

- Post-Wire Piece 01 · The death of the identical paragraph · Post-Wire 01 · publisher-side intermediation transfer · structurally parallel to this piece’s consulting-tier compression analysis

- Post-Wire Piece 02 · Raw-feed licensing · Post-Wire 02 · contract-forensic analysis · cross-references this piece’s discussion of how partnership architecture intermediates regulated work

Sources

The May 4-14 launch sequence

- Anthropic blog · Agents for financial services · May 5 2026 · 10 agent templates · Claude Opus 4.7 · Vals AI Finance Agent 64.37% · Microsoft 365 integration · expanded connector ecosystem · anthropic.com/news/finance-agents

- Fortune · Anthropic deepens push into Wall Street · Jamie Dimon + Dario Amodei shared stage · 80× annualized growth in one quarter disclosure · “absolute radical uncertainty” framing · May 5 2026 event coverage · fortune.com

- Fortune · Anthropic takes shot at consulting industry · $1.5B JV with Blackstone + H&F + Goldman Sachs · 1:6 software-to-services ratio framing · 85% of PE buyers factoring AI into valuations · Palantir analog · fortune.com

- CNBC · Anthropic Goldman Blackstone AI venture · $1.5B JV mechanics · embedded engineers · “having the model alone doesn’t change workflows” (Nachmann) · cnbc.com

- CIO Dive · Anthropic deepens push into financial services · agent templates · partnership formation · Deloitte report on enterprise AI infrastructure tripling by 2028 · ciodive.com

- InvestmentNews · Anthropic financial services agents arms race · OpenAI parallel JV reporting · D&B + Fiscal AI + Financial Modeling Prep + Guidepoint + IBISWorld + SS&C IntraLinks + Third Bridge + Verisk + Moody’s connector ecosystem · investmentnews.com

- WinBuzzer · Anthropic 10 Finance Workflow Agents · agent template breakdown · ServiceNow OpenAI partnership · Microsoft Copilot 38.6% enterprise usage · OpenAI 25.7% · Anthropic 5.7% workflows API · winbuzzer.com

- AI Consulting Network · Anthropic Claude Financial Agents 2026 CRE Investor Guide · Anthropic 40% US enterprise AI spending share / OpenAI fell from 50% to 27% · 92% AI program initiation / 5% goal achievement · theaiconsultingnetwork.com

- GitHub · anthropics/financial-services · agent template reference architecture · plugin install instructions · vertical bundle structure · MS365 admin tooling · github.com/anthropics/financial-services

The PwC expanded alliance

- Anthropic blog · PwC expanded partnership · May 14 2026 · 30,000 PwC professionals trained on Claude · Office of the CFO standalone business unit anchored in Anthropic technology · Insurance underwriting 10 weeks → 10 days · Security work hours → minutes · delivery times cut up to 70% · anthropic.com/news/pwc-expanded-partnership

Enterprise adoption share data

- The Rundown AI · Enterprise shift OpenAI saw coming · Ramp AI Index April 2026 · Anthropic 34.4% paid business adoption (up 3.8%) · OpenAI 32.3% (down 2.9%) · overall AI use 50.6% · Claude Code anchoring swing · expansion from technical teams to finance and legal · therundown.ai

Revenue trajectory and IPO context

- Tipranks · Anthropic $26B revenue target 2026 · projected $9B end-2025 · base case $20B 2026 · best case $26B 2026 · current ARR ~$7B October 2025 (up from $1B early 2025) · 80% revenue enterprise · 300,000+ business clients · Claude Code at $1B ARR · tipranks.com

- Cryptopolitan · Anthropic $26B target on AI demand · $13B Series F · $183B valuation · ICONIQ led · Haiku 4.5 launch · Series F context · referenced cross-source

- Neuron Expert · Anthropic $20-26B revenue target · Google + Amazon investment scale · Bengaluru office plan · enterprise positioning · neuron.expert

Consulting industry context

- Industry baseline · Big Four 2024 revenue · Deloitte ~$67B · PwC ~$55B · EY ~$50B · KPMG ~$38B · Accenture ~$65B · McKinsey/Bain/BCG ~$30-40B combined · TCS/Infosys/Wipro/HCL collectively ~$70-100B at the India-based implementation tier · global consulting industry ~$1T+

- Strategy-tier framing · McKinsey QuantumBlack 2015 · Bain Vector · BCG X · the strategy-firms’ implementation adjacency

- Palantir reference · ~$100B+ market cap 2024 · ~$3B 2024 revenue · ~80% gross margin · ~25% operating margin · forward-deployed engineering model precedent

Companion-piece source backbone

- The Bank Account in the Chat · Thorsten Meyer · Agentic Commerce 01 · consumer-side intermediation analysis · same structural argument applied to a different stack

- The Gigawatt Gap · Thorsten Meyer · AI Energy & Infrastructure 01 · industrial-policy at the physical-infrastructure layer

- Post-Wire Pieces 01-02 · Thorsten Meyer · publisher-side intermediation forensics · structurally adjacent to this piece’s consulting-tier compression analysis

Key Piece reference figures crystallized

- Anthropic May 4 JV: $1.5B · Blackstone + H&F + Goldman Sachs + Apollo + General Atlantic + Leonard Green + GIC + Sequoia

- Anthropic May 5 product launch: 10 financial-services agents · Claude Opus 4.7 · Vals AI Finance Agent 64.37% · MS365 add-ins for Excel/PPT/Word + Outlook beta

- The 10 agents: Pitch builder · Meeting prep · Earnings reviewer · Financial model builder · Market researcher · GL reconciler · Month-end closer · Financial statement auditor · KYC screener · Valuation reviewer

- Data partners: D&B · Fiscal AI · Financial Modeling Prep · Guidepoint · IBISWorld · SS&C IntraLinks · Third Bridge · Verisk · Moody’s MCP app (600M+ entities)

- PwC alliance May 14: 30,000 Claude-certified professionals · joint COE · Office of the CFO standalone business unit

- Anthropic revenue: ~$7B ARR October 2025 · $9B end-2025 internal target · $20-26B 2026 target · 80× annualized growth disclosure

- OpenAI parallel structure: $4B raise at $10B valuation for similar JV · BNY/BBVA/ServiceNow partnerships

- Enterprise share inversion: Anthropic 40% / OpenAI 27% US enterprise AI spending (industry research early 2026) · Ramp April: Anthropic 34.4% / OpenAI 32.3%

- Consulting industry: $1T+ global · 1:6 software-to-services ratio · AI-transformation services subsegment ~$50-100B · 30-60% plausible compression by 2028 in the JV scenario