By Thorsten Meyer — May 2026

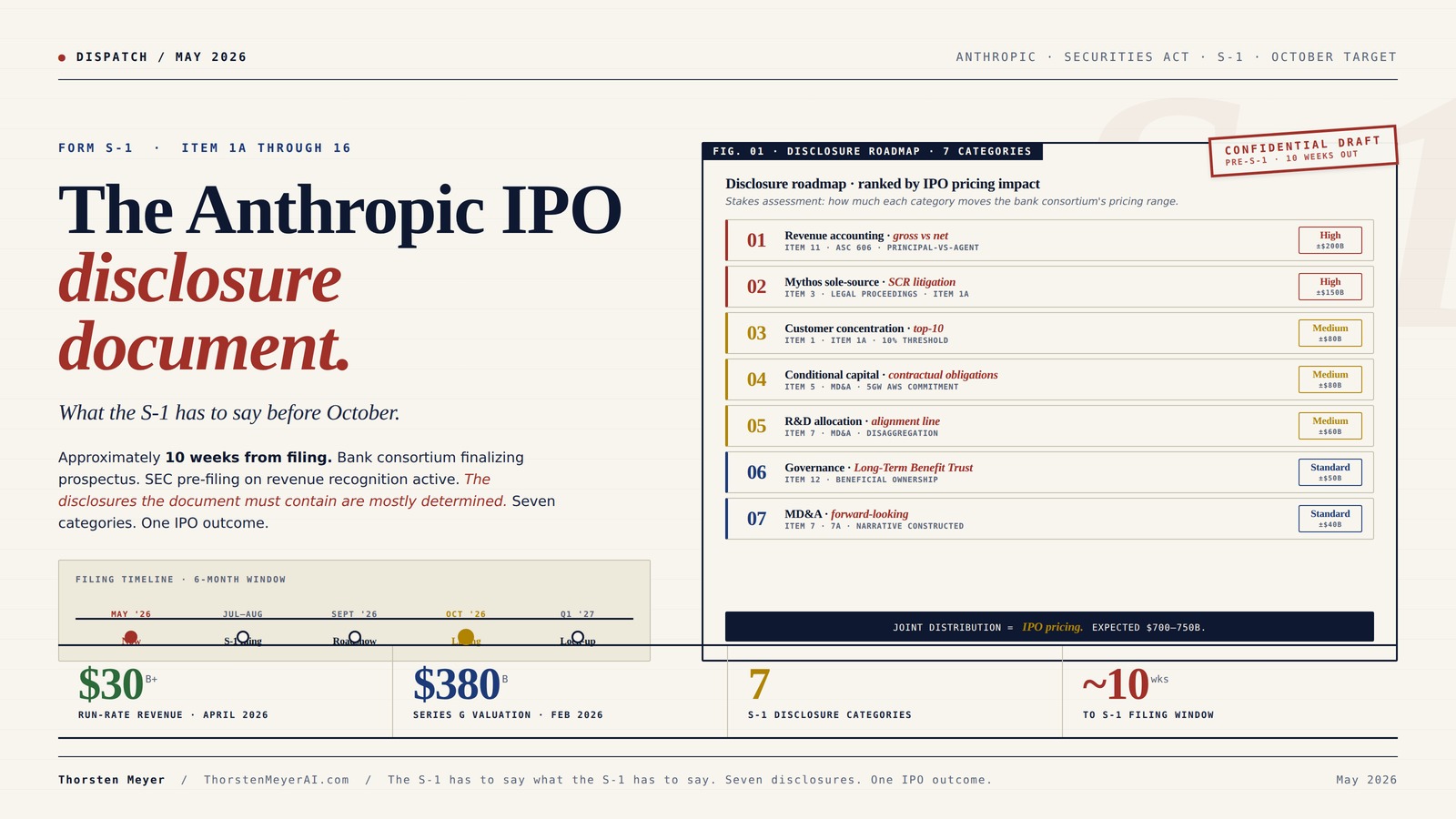

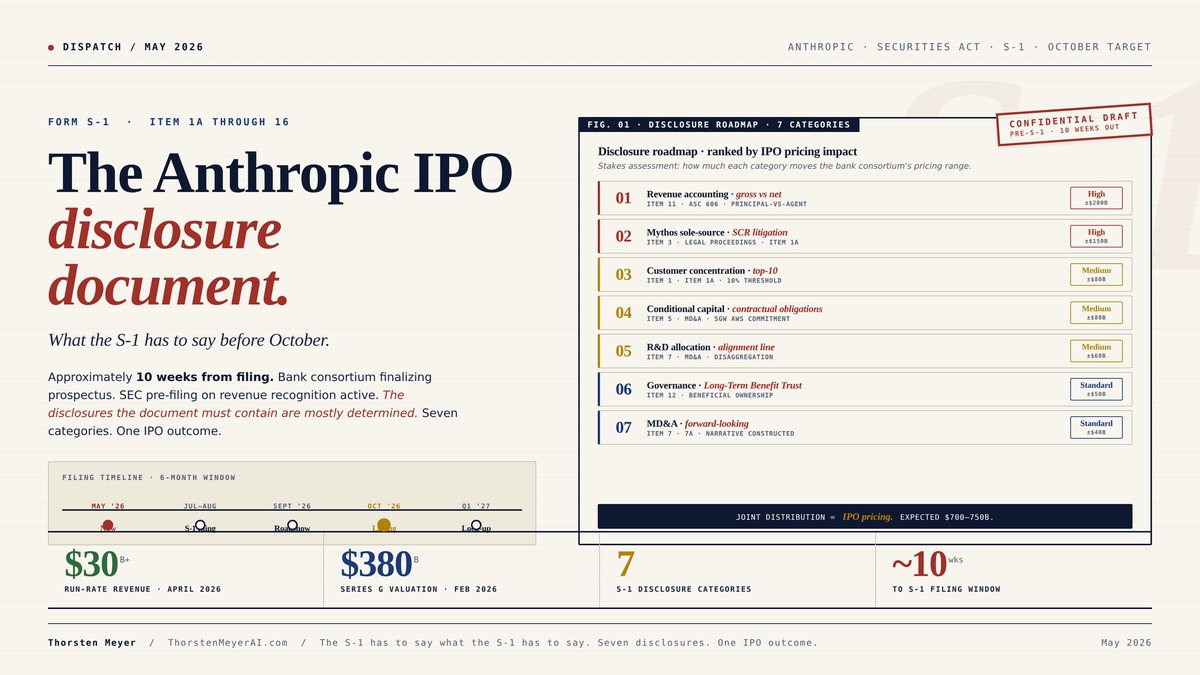

The Anthropic S-1 is approximately ten weeks from filing. The bank consortium (Goldman Sachs, JPMorgan, Morgan Stanley) is finalizing the prospectus with Wilson Sonsini. The SEC pre-filing discussions on revenue recognition and cloud-credit accounting are active. The roadshow is scheduled for September. The Nasdaq listing is targeted for October 2026.

Most IPO commentary at this stage is performative. The bull case, the bear case, the prediction markets odds, the secondary-market implied valuations of $1 trillion plus. None of it is wrong. None of it is what the document will actually contain. A registration statement under Section 5 of the Securities Act has specific disclosure requirements that the company cannot redact, paraphrase, or summarize. Items 1A through 16, plus the financial statements, plus the consolidated risk factors. The company has more discretion in how it characterizes its risks than in whether it discloses them. The S-1 has to say what the S-1 has to say.

This piece reads the disclosure document before it ships. Seven categories of disclosure that Anthropic’s S-1 must address, what each will likely reveal, and what each signals for the IPO pricing and the broader AI economy. The point is not to predict the IPO outcome. The point is to identify the specific places where the document will surface information that is currently private, and to position for what those disclosures change.

The dispatch on the compute concentration audit covered the regulatory environment that Anthropic enters this disclosure cycle inside of. The dispatch on the 2028 model lab endgame treated Anthropic’s IPO pricing as a primary signpost between Scenarios A, B, and C. This piece sits underneath both. The S-1 is the document that converts Anthropic’s private narrative into public disclosure, on a fixed timeline, under regulatory and litigation pressure that no prior frontier AI company has faced.

What the document is going to say is mostly determined. The company that has to say it cannot easily say less.

The Anthropic IPO disclosure document.

What the S-1 has to say before October.

Anthropic’s S-1 is approximately ten weeks from filing. Bank consortium finalizing prospectus with Wilson Sonsini. SEC pre-filing discussions on revenue recognition active. Roadshow September. Listing target October. The disclosures the document must contain are mostly determined. Seven categories of disclosure. Seven probability distributions. One IPO outcome.

From private narrative to public disclosure.

Section 5 of the Securities Act has specific disclosure requirements that the company cannot redact, paraphrase, or summarize. The S-1 has to say what the S-1 has to say.

CAFFORIK 27PCS Metal File Set, Flat/Half-round/Round/Triangle Steel Files,12PCS Needle Files,10PCS Sandpapers, Wire Brush. Work for Metal, Wood and More

【27PCS File Set】Includes 4pcs 8" metal files (Flat,Half-Round,Round,Triangle), 12pcs needle files, 10pcs Sandpapers, 1pcs Wire Brush; It is…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What the S-1 produces. What changes when it does.

Seven categories where the disclosure produces information that is currently private. Each affects IPO pricing. Each becomes a precedent for the rest of the AI economy. The order below is by stakes — what moves the pricing range most.

Financial Analysis With Microsoft Excel 2019

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

$700–750B expected. Wide variance.

The expected pricing midpoint, weighting all four scenarios: approximately $700–750B IPO valuation. Below the secondary-market $1T+ implied range. Above the prediction-market $560B lower bound. The S-1 itself moves the distribution; this estimate is pre-disclosure.

Premium captured

Disclosures favorable. Revenue accounting affirmed. SCR language reassuring. Trust accepted. Bank prices upper end.

Pricing conservative

One or two disclosure items produce friction. Bank prices conservatively. Modest first-day premium. A and B endgames remain in play.

Capital stress

Multiple negative disclosures. Restatement required. SCR more constraining than expected. Capital stress through 2027 possible.

Window missed

Disclosure issues severe. SEC pre-filing unresolved. SCR outcome unviable for October. Anthropic raises private + retargets 2027.

The S-1 is the document that converts Anthropic’s private narrative into public disclosure on a fixed timeline under regulatory and litigation pressure no prior frontier AI company has faced. The disclosures are mostly determined.

Ultimate Guide to Franchise Disclosure Documents (FDD) (Bigger Bottom Line Ultimate Small Business Guide Books)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Read the document on filing day.

Most consequential single technology disclosure of 2026. Read it on filing day, not in summary. Seven differentiated information categories. Specifically: revenue accounting treatment, customer-concentration top-10, contractual-obligations table with AWS dollar amount, R&D disaggregation, SCR litigation language, Trust governance triggers, MD&A path-to-profitability assumptions.

Re-mark every AI position against IPO multiples.

Anthropic’s pricing sets multiples for every other frontier AI company. OpenAI, xAI, Mistral, Reflection, spinout cohort all re-marked against Anthropic’s IPO within 30 days of pricing. Positions held above implied multiples face writedown pressure. Run comparable-company analysis now, not after disclosure.

Begin comparable-company narrative work now.

OpenAI’s own S-1 will be benchmarked against Anthropic’s. Begin comparable-company work now while there’s flexibility. Specifically: revenue accounting comparison, safety-versus-product positioning, federal channel comparison. Anthropic’s S-1 effectively becomes the template for AI public-market disclosure.

Treat the S-1 as vendor-assurance input.

Customer concentration and Mythos sole-source channel disclosure has direct procurement implications. Anthropic’s status as public company changes accountability and disclosure obligations. Vendor-assurance frameworks should treat S-1 as primary input source for procurement decisions starting October.

IPO readiness kits

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive Summary · The Filing in One Table

| Variable | Where It Stands | What the S-1 Discloses |

|---|---|---|

| Filing window | S-1 confidential filing July–August 2026 | First public look at audited financials |

| Roadshow | September 2026 | Dario and Daniela Amodei present to institutional investors |

| Listing target | October 2026 (per The Information) | Nasdaq |

| Revenue (run rate) | $30B+ April 2026 | Quarterly breakdown 2024–2026, audited |

| Last private valuation | $380B (Series G, Feb 2026) | Cap table, prior round terms, secondary-market activity |

| Implied secondary valuation | $1T+, single offer reported at $1.15T | “Recent secondary transactions” disclosure |

| Customers | 8 of Fortune 10; 500+ at >$1M/year | Customer concentration, top-customer percentages |

| Enterprise mix | ~80% of revenue | Channel split, geographic split, contract terms |

| Claude Code | $2.5B ARR February 2026 | Segment disclosure if material |

| AWS commitment | 5 GW Trainium capacity | Multi-year compute obligations as off-balance-sheet |

| Cap table | ~50% hyperscaler-aligned, ~50% sovereign/institutional | Beneficial ownership, related-party transactions |

| Bank consortium | Goldman Sachs / JPMorgan / Morgan Stanley | Underwriter allocation, fee structure, lock-ups |

| Pentagon SCR designation | Active since Feb 27, 2026; appeals court denied stay April 8 | “First time applied to American company” — legal proceedings disclosure |

| Mythos Preview / Project Glasswing | Disclosed April 7, 2026 | Single-channel concentration risk + capability disclosure |

| Long-Term Benefit Trust governance | Existing structure | Non-standard governance disclosure |

| Gross margin | Reportedly ~40% post-inference cost surge | First audited margin disclosure |

| 2026 burn rate | ~$19B ($12B training + $7B inference) | Cash flow statement, capital sufficiency analysis |

| Free cash flow target | 2027 | Forward-looking statement, MD&A |

The document the SEC requires Anthropic to file is more revealing than any private fundraising deck. The seven categories below are where the disclosure will produce information that is currently held within the company.

1. The revenue accounting question · gross versus net

This is the single most consequential disclosure item, and it has been an active dispute since OpenAI Chief Revenue Officer Denise Dresser circulated an internal memo accusing Anthropic of overstating ARR by counting hyperscaler-channel revenue gross.

The factual basis of the dispute. Anthropic sells Claude through three channels in addition to direct: AWS Bedrock, Google Vertex AI, and Microsoft Azure (the Microsoft channel via the Anthropic-Microsoft commercial agreement). When an end customer purchases Claude through AWS Bedrock, the customer pays AWS, AWS pays Anthropic some portion (the partner payout), and Anthropic recognizes the difference as revenue. The accounting question is how much of the gross customer payment Anthropic books as its own revenue.

Two recognition methods exist. Gross reporting counts the full end-customer spend as Anthropic revenue and books AWS’s share as a cost. Net reporting counts only Anthropic’s share of the end-customer spend as revenue. Under GAAP and IFRS, the distinction depends on whether Anthropic is the principal or the agent in the transaction. The principal-agent test under ASC 606 examines who controls the goods or services before transfer to the customer, who has primary responsibility, who has discretion in pricing, and who bears the inventory risk. For an AI model accessed via a third-party cloud’s API, the test is genuinely ambiguous — the cloud provider controls the deployment infrastructure, the AI lab controls the model, the end customer’s contractual relationship varies by deal.

Sacra reports that Anthropic uses gross reporting for cloud-reseller revenue, which inflates headline numbers relative to net-reporting peers. The Dresser memo at OpenAI characterized this as overstatement. The S-1 will resolve the ambiguity in one of three ways.

Path A · Gross reporting affirmed. Anthropic’s auditors (Deloitte, PwC, EY, or KPMG — the identity of the audit firm itself will be a disclosure item) sign off on the existing methodology. The revenue numbers in the S-1 match the Sacra estimates. The risk-factors section discloses the methodology with disclosure of the agent-versus-principal analysis. This is the most likely outcome — auditors generally do not require restatement of a methodology a company has applied consistently.

Path B · Restatement. SEC pre-filing discussions force restatement of prior periods to net reporting. The headline revenue numbers shrink. The growth rates remain similar (because the methodology is consistent across periods). The narrative damage is meaningful — a restatement before IPO is a reputational item that affects pricing.

Path C · Disaggregated disclosure. The S-1 reports gross revenue at the consolidated level and provides a separate disclosure of the partner-payout deduction, allowing investors to compute net. This is the most informative outcome and is consistent with SEC guidance for revenue recognition transparency. The market then prices off whichever number it considers more meaningful.

The probability distribution: Path A 50%, Path C 40%, Path B 10%. The reason Path C is plausible at 40% is that the SEC has been increasingly demanding on AI-revenue disclosure standards, and the agent-versus-principal ambiguity is genuinely material at Anthropic’s scale.

The strategic implication: Anthropic’s $30B “ARR” figure is what the company emphasizes externally. The S-1 will produce, for the first time, a number that is auditor-validated. Whatever that number is (within a range), it sets the basis on which all forward analysis of the company is built. Investors who have been pricing the company off Sacra-grade estimates will need to recalibrate to the audited figure on the day the document files.

2. The customer concentration disclosure

Eight of the Fortune 10 are Claude customers. Five hundred customers spend more than $1 million per year. Three hundred thousand business customers in total. Eighty percent of revenue is enterprise.

These are the public talking points. The S-1 has to disclose more.

Item 1A risk factors in any technology IPO requires customer-concentration disclosure if any single customer accounts for more than 10% of revenue. For most enterprise SaaS companies, this is a non-issue — the long tail of mid-market customers prevents any single account from reaching the threshold. Anthropic at $30B run-rate revenue with 500+ customers paying $1M+ annually is structurally different. The top customer at Anthropic might be Amazon (via the AWS Bedrock channel relationship that includes Anthropic’s own compute consumption), Microsoft, Google (via the Anthropic-Google partnership), or a single large enterprise.

Three concentration questions the S-1 must answer.

Question 1 · Single-customer concentration. Does any individual end-customer or channel partner account for more than 10% of revenue? If Amazon-via-Bedrock counts as a single customer (it doesn’t, contractually, but the SEC may take a view), the answer is materially yes. If Bedrock end-customers are counted individually, the answer is likely no.

Question 2 · Government concentration. What percentage of Anthropic revenue flows from federal government contracts, including via the Mythos / Project Glasswing channel? The Pentagon SCR designation makes this materially complicated to disclose — Anthropic is excluded from the multi-vendor procurement channel but is the sole-source vendor on the cybersecurity channel. The disclosure has to characterize both. Estimated federal revenue: $1.5-3B annualized as of Q2 2026, growing rapidly.

Question 3 · Hyperscaler-channel concentration. What percentage of revenue flows through AWS, Azure, and Google Cloud channels respectively? The cap-table bifurcation noted by TMB suggests roughly half the company’s funding comes from hyperscalers. The revenue side is similarly weighted. If any single hyperscaler channel accounts for more than 25% of total revenue, the concentration risk language becomes meaningful.

The S-1’s customer concentration section will be one of the most-read parts of the document for institutional allocators. The disclosures will affect how the bank consortium prices the offering.

3. The Mythos sole-source channel as concentration risk

This is the disclosure that has no precedent in prior tech IPOs.

The Mythos Preview disclosure of April 7, 2026 — covered in the Mythos CISO Playbook dispatch — established Anthropic as the sole-source provider of frontier defensive cybersecurity capability via the Project Glasswing consortium. The federal procurement architecture announced May 1 split AI procurement into a multi-vendor channel (excluding Anthropic) and a single-source cybersecurity channel (Anthropic exclusively).

Single-source channels are structurally favorable on margins. They are structurally fragile on customer concentration. The S-1 has to disclose both.

The favorable disclosure: Anthropic has secured a unique federal channel that competitors cannot enter. Project Glasswing usage credits ($100M scale) plus operational deployment in 40+ consortium organizations plus mandatory federal cybersecurity workflows produce a high-margin revenue stream that compounds without competitive pricing pressure. The S-1 will frame this as a competitive advantage and a capability moat.

The fragile disclosure: the same single-source structure creates concentration risk if (a) the Pentagon SCR designation litigation produces a worse outcome than expected, (b) a Mythos-class capability proliferates to a competitor, (c) the Glasswing consortium reorganizes around a different vendor, or (d) regulatory pressure forces multi-vendor procurement on the cybersecurity side as well. Each of these has to be disclosed as a risk factor.

The most consequential element: the SCR designation itself. Pentagon designated Anthropic as a supply-chain risk on February 27, 2026. The appeals court denied Anthropic’s stay request on April 8. Anthropic has stated this designation has not previously been applied to an American company. This is a litigation disclosure item in Section 4 (“Legal Proceedings”) that the S-1 must address with specificity. The disclosure has to characterize the SCR designation, the company’s response, the litigation status, the financial impact estimate, and the range of possible outcomes including resolution timelines.

This is where the S-1 becomes genuinely difficult to write. The litigation is active. The financial impact depends on the outcome. The company cannot be definitive about either. The disclosure language will be carefully negotiated between Anthropic, the underwriters, Wilson Sonsini, and the SEC. The language that gets approved becomes the public record on which secondary litigation, investor lawsuits, and analyst valuation models all build.

If the disclosure language leans toward “we expect resolution favorable to Anthropic,” the IPO prices toward the upper bound. If the language characterizes the SCR designation as a meaningful ongoing constraint, pricing compresses. The stakes on this single section of the document are substantial.

4. The conditional capital structure

Anthropic’s funding history through May 2026 includes the Series G at $380B post-money, the prior $183B round in September 2025, the $61.5B mark from March 2025, the Amazon $8B investment, the Google $2B+ partnership, plus earlier Series A through F. Total external capital raised across all rounds: approximately $30-35B as of S-1 filing.

The cap table is the routine disclosure. The interesting disclosure is what conditions attach to which capital, and how the conditional capital is treated in financial reporting.

OpenAI’s $122B raise in March-April 2026 was structured with substantial conditional tranches: $50B from Amazon (only $15B upfront, $35B conditional on milestones), $30B from Nvidia, $30B from SoftBank in three $10B tranches through October. The conditional structure was designed to give OpenAI capital firepower without requiring the full amount to be drawn immediately. The S-1 (when OpenAI eventually files) will have to disclose the conditional structure, the milestones, and the financial-reporting treatment of the unfunded tranches.

Anthropic’s structure appears less conditional in publicly available reporting, but the S-1 will disclose the actual terms. Three specific items the document must address.

Item 1 · Forward funding commitments. Are there outstanding commitments from existing investors to provide additional capital under specific conditions? If so, what are the conditions and what is the financial-reporting treatment?

Item 2 · Strategic-investor governance rights. Amazon and Google as strategic investors typically retain consultation rights, observer rights, or first-refusal rights on certain transactions. The S-1 has to disclose these. The disclosures themselves will signal how operationally constrained Anthropic is by its strategic relationships.

Item 3 · Compute commitments as off-balance-sheet obligations. Anthropic’s 5 GW Trainium commitment to AWS is a multi-year contractual obligation. Under standard accounting treatment, multi-year compute commitments are not capitalized on the balance sheet (they are operating commitments rather than capital leases or finance leases unless specific tests are met). They appear in the contractual-obligations table in MD&A. The dollar amount of the contractual obligation as of S-1 filing will be the first public disclosure of Anthropic’s actual compute commitment scale. Order of magnitude: $30-60B over the 2026-2030 period, depending on how the AWS Trainium pricing works and how the 5 GW translates to dollars.

The conditional capital structure disclosure will surface information that is genuinely private today. Until the S-1 files, Anthropic’s effective capital position is uncertain — what’s drawn, what’s conditional, what’s locked into compute commitments versus available for operating use. The S-1 makes it visible.

5. The R&D allocation and the alignment expense line

Most tech S-1s disclose research and development expense as a single line item, with optional breakdown between “research” and “development” if the company chooses. The breakdown is rarely informative because most R&D in software companies is product engineering rather than fundamental research.

Anthropic is structurally different. Three categories of R&D expense exist within the company: model training (the largest, dominated by compute costs), product engineering (Claude product, Claude Code, the API platform, integrations), and alignment / safety research (interpretability, Constitutional AI, red-teaming, the Frontier Red Team that produced Mythos).

The S-1 has discretion on how to disaggregate these categories. The way the company chooses to disaggregate is itself a signal.

Option 1 · Single R&D line. Anthropic reports R&D as a single number, in the range of $14-18B for 2026 if compute costs are included as R&D rather than COGS. This is the simplest treatment and the least informative.

Option 2 · Two-line disaggregation. Model training expense reported separately from “other R&D.” This makes the magnitude of the training expense visible while keeping product engineering and safety bundled.

Option 3 · Three-line disaggregation. Model training, product engineering, and alignment/safety reported separately. This is the most informative treatment and would surface a number that is currently completely unknown publicly: how much Anthropic actually spends on alignment research as a percentage of total R&D.

The third option matters strategically. Anthropic’s market positioning depends on the company being credibly the “safety-focused frontier AI lab.” The disclosure of alignment R&D as a percentage of total R&D either supports or undermines that positioning. If the number is below 5%, the safety positioning is largely marketing. If the number is above 15%, the safety positioning is a real organizational commitment. My estimate: the actual number is in the 8-12% range, which is meaningful but not dominant.

The S-1 will use the disaggregation that best supports the company’s positioning. Almost certainly Option 2 or a hybrid that reports “model training expense” separately while bundling product and safety. The full three-line disaggregation would be informative but is not required and would expose Anthropic to comparisons it would prefer not to make.

The most consequential single number in this section: model training expense for 2026. This is the number that converts the abstract “Anthropic spends a lot on compute” narrative into an audited line item. Estimated range: $11-14B.

6. The governance structure disclosure

Anthropic’s Long-Term Benefit Trust is the unusual governance feature that most tech IPOs do not have. The Trust holds a class of stock with the right to elect a portion of the board. The Trust’s mandate prioritizes the long-term benefit of humanity over shareholder returns under specified conditions. The Trust members include figures whose primary commitment is to AI safety rather than to investor returns.

This is a non-standard governance structure for a public company. The S-1 has to disclose it in detail in the Beneficial Ownership and Related Party Transactions sections, plus in the Risk Factors section under “Risks Related to Our Common Stock.”

Three disclosure questions.

Question 1 · Voting power. What percentage of board seats does the Trust elect? What percentage of voting power does the Trust hold on shareholder matters? How does the Trust’s voting interact with the dual-class share structure that is likely already in place for the founders?

Question 2 · Mandate triggers. Under what specific conditions does the Trust’s mandate to prioritize long-term humanity benefit override standard fiduciary duty to shareholders? The Trust’s governing documents must contain specific triggers; the S-1 has to disclose them. Investor reaction to specific triggers will matter — vague language is reassuring, specific language about (e.g.) capability deployment decisions affecting safety will be received with concern by some investors.

Question 3 · Modification provisions. Can the Trust be modified, dissolved, or constrained after IPO? If yes, by whom? The flexibility (or absence) of the structure determines how durable the governance commitment is.

The S-1 disclosure will not satisfy investors who view the Trust as a structural risk to shareholder returns. It will reassure investors who view AI safety as an operational priority. The IPO pricing will reflect the balance — institutional investors who would pay $1T for a standard AI lab will pay less for a Trust-governed one, which is offset by the marketing benefit of being explicitly aligned with safety.

The most strategic question: does the Trust survive contact with public-company quarterly pressure? Public company investors push for predictable quarterly results. The Trust’s mandate is explicitly to override that pressure when long-term safety considerations require. If the Trust ever exercises its override authority on a quarter-impacting decision, the stock reaction will be severe. The S-1 has to characterize this risk in language that does not panic the market.

7. The MD&A forward-looking statements

Management’s Discussion and Analysis is where the S-1’s narrative gets constructed. It is also where the most strategically-revealing disclosures usually appear, because the MD&A has to tie the historical financial performance to the company’s forward-looking strategy.

Six topics the Anthropic MD&A will need to address.

Topic 1 · Path to profitability. Public reporting cites 2027 as Anthropic’s free-cash-flow positive target. The MD&A will detail the assumptions underlying that target: revenue growth trajectory, gross margin expansion, opex leverage, capex normalization. The most consequential single assumption is whether the company assumes continued revenue acceleration or normalization to “merely strong” growth. If the MD&A assumes acceleration through 2027, the FCF target is achievable. If it assumes normalization, the target slips.

Topic 2 · Competitive dynamics. The MD&A has to characterize the competitive landscape — OpenAI, Google DeepMind, Meta, xAI, Reflection, the Chinese sphere. The way the company characterizes its competitors is a signal about its strategic positioning. Anthropic’s likely framing: enterprise focus, regulated-industry depth, safety differentiation, Mythos sole-source channel. The framing will explicitly distinguish Anthropic from OpenAI’s consumer-heavy mix.

Topic 3 · Compute strategy and supply. The 5 GW AWS Trainium commitment, the multi-cloud diversification (or lack thereof), the dependency on Amazon as compute supplier and as investor, the mitigation strategies. This section will be heavily lawyered because it touches on the compute concentration audit regulatory environment that the prior dispatch covered.

Topic 4 · Regulatory environment. EU AI Act enforcement starting August 2, 2026. SEC AI disclosure rules (in development). FTC Section 6(b) inquiry findings. Pentagon SCR designation. State-level AI legislation. The S-1 has to acknowledge each as a forward risk.

Topic 5 · Safety and capability deployment philosophy. This is where Anthropic’s Constitutional AI, Responsible Scaling Policy, and Frontier Red Team get formalized into public-company disclosure language. The Responsible Scaling Policy commits the company to specific deployment constraints based on capability evaluation. The S-1 has to characterize how those commitments interact with shareholder value.

Topic 6 · Capital sufficiency. Given the burn rate of $19B per year (training plus inference) and revenue growth trajectory, does the company have sufficient capital to reach FCF positive without further dilution? The MD&A has to address this directly. The answer determines whether the IPO is positioned as the final capital raise or as one of several.

8. What the S-1 changes

The document files. The market reads it. Three things change immediately.

Change 1 · The valuation conversation gets specific. The current secondary-market range of $700B to $1.15T is based on private estimates. The S-1 surfaces audited revenue, gross margin, customer concentration, and burn rate. The bank consortium prices the offering against those numbers. The IPO range narrows to a specific window — most likely $600-900B based on the available data. Pricing above that range requires the S-1 disclosures to be unambiguously favorable. Pricing below that range requires disclosure issues that are not currently visible.

Change 2 · The competitive comparisons become explicit. Once Anthropic’s actual revenue, margin, and growth numbers are public, every other AI company gets compared to them. OpenAI’s eventual S-1 will be benchmarked against Anthropic’s. The Chinese frontier labs will be priced against Anthropic’s audited numbers. The spinout cohort’s funding rounds will be marked against Anthropic’s IPO multiples. The S-1 becomes the benchmark document for the entire frontier AI economy.

Change 3 · The regulatory environment intensifies. The SCR designation litigation, the compute concentration audit, the EU AI Act enforcement, and the SEC’s evolving AI-disclosure standards all get specific disclosure language in the S-1. The language sets the precedent for how every future AI IPO has to disclose similar risks. Anthropic’s S-1 effectively becomes the template document for AI public-market disclosure.

9. The three pricing scenarios

I want to be direct about the IPO outcome. The S-1 produces the disclosures; the bank consortium prices the offering; the market reacts. Three scenarios, with my probability estimates.

Scenario A · Strong reception ($800B-$1.15T pricing, probability 40%). S-1 disclosures are favorable: revenue accounting affirmed at gross with disclosure (Path A or C), customer concentration manageable, SCR litigation language reassuring, Mythos channel clearly differentiated, Long-Term Benefit Trust accepted by institutional investors. Bank consortium prices at the upper end of the secondary-market range. First-day trading produces a premium. Anthropic captures the upside. The 2028 endgame piece’s Scenario A duopoly outcome looks more likely.

Scenario B · Measured reception ($550-800B pricing, probability 40%). S-1 has one or two disclosure items that produce friction: revenue restatement, SCR litigation language ambiguous, Trust governance receives institutional investor pushback, customer-concentration disclosure surfaces unexpected facts. Bank consortium prices conservatively. First-day trading is flat to modestly positive. Anthropic captures most of the upside but loses the premium. The 2028 endgame’s Scenarios A and B remain in play.

Scenario C · Difficult reception ($350-550B pricing, probability 15%). Multiple disclosure items go negatively: revenue accounting restatement is required, SCR litigation appears more constraining than expected, customer concentration is high, governance structure receives meaningful institutional pushback, MD&A path-to-profitability assumptions look stretched. Bank consortium prices at the lower end. First-day trading is flat. Anthropic raises substantially less than expected. Capital stress through 2027 becomes a real possibility. Scenario C of the lab endgame piece becomes more likely.

Scenario D · Postponement (probability 5%). Disclosure issues are severe enough that the S-1 filing is delayed or the listing is postponed. SEC pre-filing discussions on revenue recognition do not resolve in time. SCR litigation outcome is sufficiently negative that the offering becomes unviable in the October window. Anthropic raises additional private capital and retargets 2027. This is the lowest-probability scenario but not zero.

The expected pricing midpoint, weighting all four scenarios: approximately $700-750B IPO valuation, with substantial standard deviation. This is below the secondary-market implied valuation of $1T+ and above the lower-bound estimates of $560B from prediction-market models. The S-1 itself moves the probability distribution; this estimate is pre-disclosure.

What to Do This Quarter

1. Public-equity allocators. The Anthropic S-1 will be the most consequential single technology disclosure document of 2026. Read it on filing day, not in summary. The seven categories above are where the differentiated information will be. Specifically: revenue accounting treatment, customer-concentration top-10 disclosure, contractual-obligations table with the AWS commitment dollar amount, R&D disaggregation choice, SCR litigation language, Trust governance triggers, and MD&A path-to-profitability assumptions.

2. Private-equity and venture allocators. Anthropic’s pricing sets the multiples for every other frontier AI company. Existing positions in OpenAI, xAI, Mistral, Reflection, and the spinout cohort will be re-marked against Anthropic’s IPO multiples within 30 days of pricing. Positions held above those implied multiples face writedown pressure. Run the comparable-company analysis against the realistic IPO range now, not after the disclosure.

3. Anthropic competitors. OpenAI’s own S-1 (whenever it files) will be benchmarked against Anthropic’s. Begin the comparable-company narrative work now, while there’s still flexibility. Specifically: the revenue accounting comparison, the safety-versus-product positioning, the federal channel comparison.

4. Enterprise CIOs. The S-1 disclosure of customer concentration and Mythos sole-source channel structure has direct procurement implications. Anthropic’s status as a public company changes its accountability and disclosure obligations. Vendor-assurance frameworks should treat the S-1 as a primary input source for procurement decisions starting in October.

The Strategic Read

The Anthropic IPO is not just a capital event. It is the document that converts the most strategically complex private AI company into public-market disclosure on a fixed timeline under unprecedented regulatory and litigation pressure.

Seven disclosure categories will produce information that is not currently public. Revenue accounting methodology. Customer concentration breakdown. Mythos channel and SCR designation litigation. Conditional capital structure. R&D disaggregation. Governance structure mechanics. MD&A forward-looking statements.

Each of these has a probability distribution of outcomes. Each affects the IPO pricing range. Each becomes a precedent document for the rest of the frontier AI economy. The IPO outcome probabilities cluster around $700-750B expected pricing, with meaningful upside and downside variance.

The strategic question is not whether Anthropic prices at $1T or at $600B. The strategic question is which of the seven disclosure categories produces the inflection. Whichever one moves the most determines the reception. Investors who have read the disclosure landscape carefully before October are positioned for the actual outcome. Investors who price the IPO off the secondary-market headlines and the prediction-market odds are pricing the wrong information.

The document is approximately ten weeks from filing. The disclosures are mostly determined. The reception is mostly determinable from the disclosures. The S-1 has to say what the S-1 has to say.

Anthropic’s S-1 will be the most consequential AI public-market disclosure of 2026. Seven disclosure categories produce information that is not currently public. Each has a probability distribution. The IPO pricing reflects the joint distribution. The document files in approximately ten weeks.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- The Compute Concentration Audit — when sovereign wealth funds notice three companies own the frontier

- The 2028 Model Lab Endgame — scenario forecast

- The Memento Constraint — continual learning trillion-dollar bottleneck

- The Channel Move — Anthropic × Wall Street PE channel acquisition

- The 27% Problem — Anthropic’s enterprise lead and Google’s $750M check

- The Bubble Is Not in Valuations — the productivity gap

- The Two Channels — Pentagon AI procurement architecture

Sources

- TechMarketBriefs, Anthropic IPO 2026: $380B Valuation, Complete Analysis (May 2026)

- Sacra, Anthropic revenue, valuation & funding — $30B run-rate, customer breakdown, gross-vs-net reporting analysis (May 2026)

- TECHi, Anthropic IPO: $60B Raise, $380B Valuation, Timeline & How to Invest (April 2026)

- The Information, October 2026 IPO target reporting

- Forge Global, Insights: Anthropic Upcoming IPO & Private Stock Price — $259.14 Forge Price, $380B implied

- Morningstar, OpenAI, Anthropic Highlight Revenue Gains as IPO Hype Builds — Dresser memo, gross-versus-net dispute

- EBC Financial Group, Anthropic IPO 2026: Latest Timeline, Valuation, and Risks (January 2026)

- FutureSearch, Anthropic and OpenAI IPO timelines and valuations — first-day market cap forecasts (March-April 2026)

- The Verge, internal OpenAI memo from Denise Dresser on Anthropic ARR methodology

- Pentagon SCR designation Feb 27, 2026; appeals court denial of stay April 8, 2026

- Anthropic Frontier Red Team, Claude Mythos Preview (April 7, 2026)

- Securities Act of 1933, Sections 5 and 7; Regulation S-K Items 1A through 16

- ASC 606 principal-vs-agent revenue recognition guidance