The policy menu.

Three dispatches have brought us to a question, and the question deserves an honest answer instead of a sales pitch. The stake argued that the AI transition is an ownership problem and that broad-based capital ownership is the market-friendly response. The labor share tested the premise underneath that argument and found it real at the margin, unproven in the aggregate, and resolvable only in retrospect. The bottom rung found the sharpest signal — an apprenticeship layer being dismantled with a deferred, asymmetric cost. Each piece pointed at the same problem: if value is shifting from labor to capital, even partly, even slowly, what is the response?

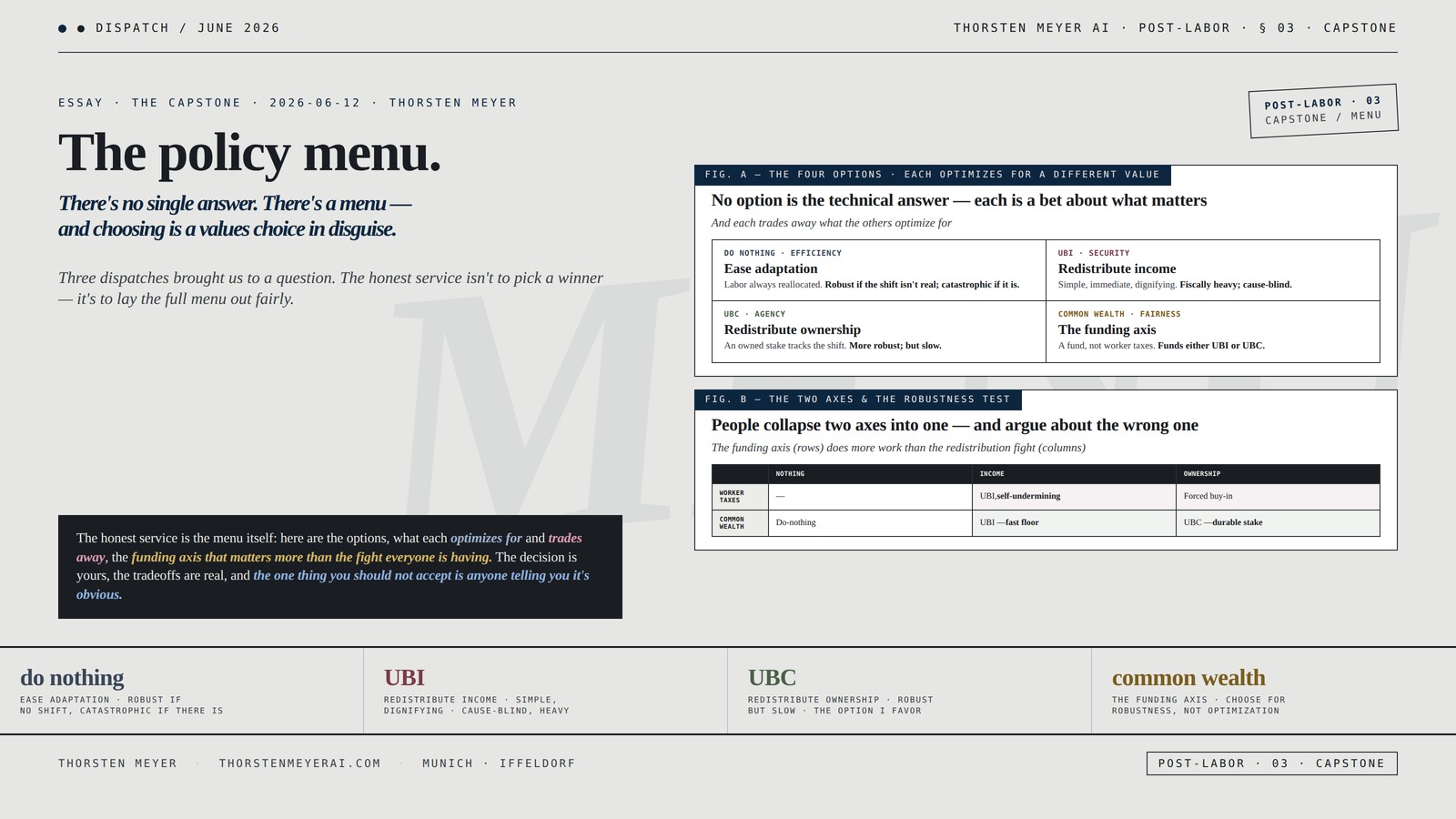

This dispatch answers that there is no single response — there is a menu. And the menu is not a technical document where one option is correct and the others are mistakes. It is a values document, where each option optimizes for a different thing, and choosing among them is a choice about what kind of society you want, disguised as a debate about economics.

The disguise is the problem. Each camp presents its option as the obviously correct technical answer and the others as errors — the UBI advocate calls do-nothing reckless, the do-nothing economist calls UBI a fiscal fantasy, the ownership advocate calls both incomplete. But strip away the certainty and what remains is a set of genuinely different bets about what is happening, what matters, and who should bear the cost — and those are not questions economics can settle, because they are questions about values.

So the honest service is not to pick a winner. It is to lay the full menu out fairly, name what each option actually optimizes for and what it trades away, and refuse the pretense that any one of them is the obvious answer. The reader can decide what they value. What they should not accept is anyone — including me — telling them the choice is technical when it is moral.

The structural argument I want to make: the distribution question the AI transition raises has no single correct answer but a menu of responses — do nothing and ease adaptation, redistribute income (UBI), redistribute ownership (UBC), or fund either from common wealth (data dividends and sovereign wealth funds) — and each option optimizes for a different value (efficiency, security, agency, fairness) and trades away the others, which means choosing among them is a values choice disguised as a technical one, and the honest service is to present the full menu evenhandedly rather than to sell the option I happen to favor. This is the capstone of the Post-Labor track: the prior three dispatches built toward a response, and this one refuses to pretend the response is obvious.

The headline integrative finding: The honest both-sides read — really an all-sides read — is that every option on the menu is right about something and wrong about something, and the disagreements are mostly about values masquerading as facts. Do-nothing is right that labor has always reallocated and wrong to assume it always will on a bearable timeline. UBI is right that cash is simple and dignifying and wrong that it addresses the cause rather than the symptom. UBC is right that ownership is more robust than income and wrong that it is fast enough to matter in a crisis. Data dividends are right about the funding source — common wealth, not worker taxes — and wrong that the funding mechanism resolves the harder questions of amount and governance. The deepest point is that the menu has two axes people keep collapsing into one: what you redistribute (income versus ownership versus nothing) and how you fund it (taxing workers versus taxing common wealth), and most of the heat in the debate comes from arguing about the first axis while the second does more of the real work — because a policy financed by taxing the workers it is meant to help is self-defeating in a way the choice between income and ownership is not. The funding source is the question under the question. And no option resolves the thing that actually determines whether any of this is needed: whether the labor-share shift is real, which The labor share showed we cannot yet know. So the menu is a set of bets under irreducible uncertainty, and the right way to read it is not “which is correct” but “which is robust to being wrong.”

This essay walks the do-nothing option, UBI, UBC, the data-dividend funding model, the two axes people collapse, the robustness test that should guide the choice, and the structural reading of a menu that is a values document pretending to be a technical one.

The policy menu.

There’s no single answer.

There’s a menu — and

choosing is a values

choice in disguise.

shift isn’t real, catastrophic if it is

dignifying · fiscally heavy, cause-blind

robust · but slow, concentration-prone

under the question · funds either

The honest service is the menu itself: here are the options, here is what each optimizes for and trades away, here is the funding axis that matters more than the fight everyone is having. The decision is yours, the tradeoffs are real, and the one thing you should not accept is anyone telling you it’s obvious.Thorsten Meyer · The Policy Menu · Post-Labor 03 · Capstone

By Thorsten Meyer — June 2026

This is the third and final dispatch in the Post-Labor track — the capstone. The first made the ownership case, the second tested its premise, the third found its sharpest signal. This one lays the full response menu on the table, holds my own preferred option (ownership) to the same scrutiny as the rest, and closes the track by refusing to sell a single answer to a question that does not have one.

The structural argument I want to make: a policy menu is honest only when each option is presented as its strongest advocates would present it and critiqued as its strongest critics would critique it — and the test of an analyst’s integrity is whether they apply the same rigor to the option they favor as to the ones they don’t. I favor ownership. This dispatch puts ownership through the same wringer as UBI and do-nothing, and if it survives, it survives on the merits, not on my thumb on the scale.

The headline integrative finding: The menu resolves not to a winner but to a way of choosing. Under genuine uncertainty about whether the labor-share shift is real, the rational selection criterion is not “which option is best if I’m right about the diagnosis” but “which option does least harm if I’m wrong” — the robustness test. By that test, the options sort differently than the rhetoric suggests: do-nothing is robust if the shift isn’t happening and catastrophic if it is; UBI is a flexible hedge but fiscally heavy and cause-blind; ownership is slow but robust across both states of the world; and the funding source matters more than the redistribution mechanism, because common-wealth funding is robust where worker-tax funding is self-undermining. The menu’s lesson is not which dish to order. It is that the choice is yours, the tradeoffs are real, and anyone who tells you it’s obvious is selling the thing they already wanted to sell.

This essay walks do-nothing (Section I), UBI (Section II), UBC (Section III), the funding model (Section IV), the two axes (Section V), the robustness test (Section VI), and the structural reading (Section VII).

Monthly Bill Payment Checklist, 4-Year Financial Planner & Bill Organizer

- Financial Goal Setting: Set and track monthly financial goals

- Income and Expense Tracking: Monitor income, savings, debts, and expenses

- Bill Management System: Track paid, unpaid, and auto-paid bills

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

I · Do nothing · ease the adaptation, trust the churn

The first-option crystallization. The first option on the menu is the one its advocates would not call “do nothing” — they would call it “let markets adapt and ease the transition.” It is the default, the burden-of-proof holder, and the most historically vindicated of the options. It deserves a fair hearing.

The case for it

Labor has always reallocated: the strongest version is the historical record. In 1900, 41% of Americans worked in agriculture; today under 2% do, and there was no mass permanent unemployment — the economy invented new categories of work. Every prior automation panic (the 1964 committee warning Johnson of computer-driven joblessness, the 1990s ATM-and-bank-teller fear) was wrong in the same way: it assumed a fixed lump of labor. The do-nothing case is that automation displaces and reallocates, it does not permanently eliminate, and the right response is to ease the reallocation — wage subsidies, skills, mobility — not to pay people for “economic resignation.”

The strongest critique it makes of the others

It confuses a transition problem with a permanent-income problem: the do-nothing camp’s sharpest point, made by Cato’s Ryan Bourne and the Aspen Institute’s analysts, is that UBI mistakes a transition problem (people need help moving to new work) for a permanent-income problem (people will never work again). If the diagnosis is transition, the cure is adaptation support — targeted wage subsidies that encourage work — not a universal check that discourages it. A UBI “does nothing to address the root causes of declining employment and wages,” while a targeted wage subsidy “would encourage work and increase take-home pay.”

Where it is weakest

The base rate is not a guarantee: the do-nothing case rests entirely on the past predicting the future, and The labor share showed why that is contestable — the marginal signals (entry-level displacement, the apprenticeship severance) are pointed where the theory predicts, and “it always reallocated before” is a base rate, not a law. If AI is the first technology to automate the training layer itself — which The bottom rung argued — then the reallocation mechanism that saved every prior transition may be exactly what breaks, and do-nothing becomes a bet that the past holds against evidence that it might not. Do-nothing is robust if the shift isn’t real and catastrophic if it is.

The do-nothing observation

The do-nothing option — ease adaptation, trust the churn — is the default and the most historically vindicated: labor has always reallocated (41% to under 2% in agriculture, no mass unemployment), and its sharpest critique is that UBI confuses a transition problem with a permanent-income problem. But it rests entirely on the base rate, and the base rate is not a law. If the labor-share shift is real — which we cannot yet know — do-nothing is a bet that the past holds against evidence it might not, robust if the diagnosis is wrong and catastrophic if it is right. It is the option for those who weight the historical record over the marginal signal.

ABA Certified Wealth Strategist Exam Study Guide Flashcards

- Exam Preparation: Updated flashcards aligned with exam blueprint

- Comprehensive Content: Covers all core topics in wealth strategy

- Convenient Format: 300+ flashcards on perforated card stock

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · UBI · redistribute the income

The income-option crystallization. The second option is the most famous and the most debated: a universal cash payment, no conditions. It is simple, it is dignifying, and it is fiscally heavy. The pilots tell a consistent and modest story.

What the evidence shows

Cash works, modestly, and doesn’t wreck work: the Alaska Permanent Fund’s ~$1,600 annual dividend has run for four decades with no measured drop in full-time work (consumer-facing sectors even expanded). Finland’s 2017-18 trial improved well-being but barely moved employment. Germany’s recent study found higher life satisfaction and no drop in hours. Across 122 experiments, the consistent finding is that UBI improves security and well-being and does not collapse work incentives — but also does little to boost employment. The pilots validate cash’s psychological and poverty-reducing benefits and do not validate the strong claims in either direction — it neither destroys work nor transforms it.

The case for it

Simple, immediate, dignifying: UBI’s virtue is its simplicity — everyone gets a check, no bureaucracy, no means-testing, no stigma. In a fast crisis, it is the option that can be deployed immediately and reaches everyone. Advocates (Santens, Yang) argue the net cost is roughly a third of the gross cost once it replaces existing programs and offsets through the tax system, and that the cost of not doing it — poverty’s downstream costs in healthcare, crime, lost potential — may exceed the net cost. UBI is the fast, simple, universal hedge: if you need to put a floor under everyone quickly, nothing else is as deployable.

Where it is weakest

Cost, cause, and the funding trap: the critiques are serious. A $10,000/year UBI would cost more than half the federal budget (Kearney and Mogstad); it is inefficiently targeted (the same check to the billionaire and the pauper); it may be inflationary if funded by deficit; and — most importantly — it treats the symptom (low income) not the cause (who owns the productive assets). And the deepest problem is the funding trap: a UBI financed by taxing workers’ wages to compensate for those wages being displaced is, as Varoufakis put it, “taxing Jill to pay Jack” — self-defeating in exactly the way Section IV’s common-wealth funding is designed to avoid. UBI’s weakness is not the cash; it is the cause-blindness and the funding source.

The UBI observation

UBI — a universal unconditional cash payment — is the simple, immediate, dignifying option, validated by 122 pilots as security-enhancing and work-neutral (Alaska’s 40-year dividend, Finland, Germany), but critiqued as fiscally heavy, inefficiently targeted, potentially inflationary, and cause-blind: it treats low income, not the ownership of the assets producing the income. Its deepest weakness is the funding trap — taxing the workers it means to help. UBI is the option for those who weight speed and simplicity and a universal floor over targeting and root-cause repair — and its merits stand or fall largely on how it is funded, which is the axis Section IV addresses.

![[1760558206] [9781760558208]Extreme Ownership: How U.S. Navy SEALs Lead and Win-Paperback](https://m.media-amazon.com/images/I/41yDxOMYQwL._SL500_.jpg)

[1760558206] [9781760558208]Extreme Ownership: How U.S. Navy SEALs Lead and Win-Paperback

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · UBC · redistribute the ownership

The ownership-option crystallization. The third option is the one The stake argued for, and integrity requires putting it through the same wringer as the others. Universal basic capital gives people an owned, compounding stake rather than an income flow. It is more robust and much slower.

The case for it

Ownership, not income: UBC (also called universal basic ownership or universal basic capital — Mark Garman, Peter Diamandis) gives every citizen an owned stake in the productive capital of the economy — shares in a diversified fund, dividends from assets they hold. The logic from The stake: if value is moving from labor to capital, the durable response is to make people capital-owners, not just income-recipients. UBC turns the citizen from a claimant on a transfer into a part-owner of the productive base — a structural fix to a structural problem, robust precisely because it does not depend on the labor market recovering.

Why it is more robust than UBI

An owned stake survives what an income transfer doesn’t: an income transfer is a political commitment that can be cut; an owned stake is property. A UBI depends on the continued political will to tax and transfer; a UBC, once granted, is the citizen’s asset, compounding, and aligned with the capital that is capturing the value. If the labor-to-capital shift is real, UBC is the option that puts citizens on the right side of it — they own a piece of the thing that is winning, rather than receiving a transfer funded by taxing the thing that is losing. This is the robustness The stake argued for.

Where it is weakest

Slow, and concentration-prone if mis-designed: UBC’s fatal flaw in a crisis is speed — building broad ownership takes years or decades (you cannot hand everyone a meaningful capital stake overnight without either confiscation or enormous expense), and a fast displacement would outrun it. Worse, if mis-designed, it can entrench concentration rather than fix it — a poorly structured “ownership” scheme that hands out tiny stakes while the founders keep control (echoes of The conversion) is ownership in name only. UBC is robust over the long run and useless in a fast crisis, and its design is the difference between broad ownership and a fig leaf — which means it needs UBI’s speed as a complement, not a competitor.

The UBC observation

UBC — an owned, compounding capital stake rather than an income flow — is the structural fix The stake argued for: more robust than UBI because an owned stake is property that survives what a political transfer doesn’t, and it puts citizens on the winning side of the labor-to-capital shift if that shift is real. But it is slow (broad ownership takes decades to build) and concentration-prone if mis-designed. UBC is the option for those who weight durability and agency and root-cause repair over speed — and held to the same scrutiny as the others, it is not the obvious answer either, because its slowness is a real flaw in exactly the fast-crisis scenario that would make it most necessary. Its honest role is as the long-run complement to a fast floor, not a standalone winner.

The Best Dividend Stocks for 2025: How to Create a Cashflow Machine Paying You Every Month

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The funding model · where the money comes from

The funding-source crystallization. Underneath the choice of what to redistribute sits the harder choice of how to fund it — and this axis, which the debate keeps treating as a detail, does more of the real work than the redistribution mechanism. The data-dividend and sovereign-wealth model is the answer to the funding question, and it can power either UBI or UBC.

The common-wealth principle

Don’t tax Jill to pay Jack: the foundational insight, from Varoufakis and the universal-dividend advocates, is that a distribution policy must not be financed by taxing the workers it is meant to help — that is self-defeating. Instead, it should be financed from common wealth: resources society has a shared claim to. Data dividends treat public data as a natural resource AI extracts and charges a royalty for; sovereign wealth funds (Alaska’s oil, Norway’s model) hold common assets and distribute the returns; an AI dividend taxes compute or takes public equity stakes in frontier AI firms. The funding comes from the capital capturing the value, not the labor losing it.

Why this is the question under the question

Funding determines whether the policy is self-defeating: a UBI funded by taxing wages undermines itself; a UBI funded by a sovereign wealth fund holding AI-capital equity does not. A UBC is, in a sense, already a common-wealth model — it gives people the assets directly rather than taxing and transferring. The funding source determines whether a redistribution policy is robust or self-undermining — which is why Section V argues it is the more important axis, and why “UBI versus UBC” is partly a false binary: both can be funded from common wealth, and a sovereign wealth fund that pays dividends (income) from publicly-held capital (ownership) is both at once.

Where it is weakest

The mechanism doesn’t resolve amount or governance: getting the funding source right (common wealth, not worker taxes) is necessary but not sufficient. It does not answer how much to pay, how to value the data or compute being taxed, who governs the fund, and what happens if the AI valuations the fund depends on collapse (the “AI bubble” risk — if the bubble bursts, the funding evaporates). The funding model solves the self-defeating-tax problem and leaves the amount-and-governance problems open — it is the right foundation, not the finished building.

The funding observation

The funding model — finance distribution from common wealth (data royalties, compute taxes, public equity stakes, sovereign wealth funds) rather than from taxing the workers being displaced — is the question under the question: it determines whether a policy is robust or self-defeating, and it can power either UBI (dividends) or UBC (direct ownership), which makes “UBI versus UBC” partly a false binary. A sovereign wealth fund paying dividends from publicly-held capital is both at once. The funding source does more real work than the redistribution mechanism — but it solves only the self-defeating-tax problem, leaving amount, governance, and the bubble-risk open. It is the foundation the whole menu rests on, and the axis the debate most underweights.

V · The two axes · what people keep collapsing

The clarifying crystallization. Most of the heat in the distribution debate comes from collapsing two separate questions into one. Separating them is the single most clarifying move available, because it reveals that the famous fights (UBI versus UBC) are partly arguments about the wrong axis.

Axis one: what you redistribute

Nothing, income, or ownership: the first axis runs from do-nothing (redistribute nothing, ease adaptation) through UBI (redistribute income) to UBC (redistribute ownership). This is the axis the debate spends its energy on, and it is a real choice — income and ownership are genuinely different (a flow you consume versus an asset you hold), and they optimize for different things (security versus agency). But it is not the only axis, and treating it as the whole question is the error.

Axis two: how you fund it

Worker taxes or common wealth: the second axis runs from funding-by-taxing-workers (self-defeating) to funding-from-common-wealth (robust). This axis cuts across the first — you can fund UBI either way, and UBC is largely a common-wealth model by construction. This is the axis that determines whether a policy works, and it is the one the debate underweights — because it is less ideologically charged and more technical, it gets treated as an implementation detail when it is actually decisive.

Why collapsing them causes confusion

The famous fights are partly about the wrong axis: “UBI versus UBC” sounds like a fight about axis one (income versus ownership), but much of the real disagreement is about axis two (a worker-tax-funded UBI is genuinely bad; a common-wealth-funded UBI is genuinely fine). When you separate the axes, the menu reorganizes: the bad options are the ones funded by taxing workers, regardless of whether they redistribute income or ownership; the good options are the ones funded from common wealth, and among those, the income-versus-ownership choice is a real but secondary values question. Separating the axes dissolves the false binaries and reveals the real choice: first get the funding right (common wealth), then choose the redistribution mix (income for speed, ownership for durability) on the values you hold.

The two-axes observation

The debate collapses two separate questions — what you redistribute (nothing, income, ownership) and how you fund it (worker taxes versus common wealth) — into one, and separating them is the most clarifying move available: the funding axis determines whether a policy works, the redistribution axis is a secondary values choice, and the famous “UBI versus UBC” fight is partly an argument about the wrong axis. Once separated, the menu reorganizes around the funding source first. The bad options are the worker-tax-funded ones; the good options are the common-wealth-funded ones; and among the good options, income-versus-ownership is a real choice about speed versus durability that reasonable people can make differently — which is exactly why no single answer is correct.

VI · The robustness test · how to choose under uncertainty

The decision crystallization. Having laid out the menu and clarified the axes, the question is how to choose — and the answer is not “which option is best if my diagnosis is right” but “which option does least harm if my diagnosis is wrong.” Under the irreducible uncertainty The labor share established, robustness is the only honest selection criterion.

Why robustness, not optimization

You cannot optimize against an unknown diagnosis: The labor share showed we cannot yet know whether the labor-to-capital shift is real — it is confirmable only in retrospect. Optimizing for one diagnosis (picking the option that’s best if the shift is happening, or best if it isn’t) is a bet on knowing what we cannot know. The rational move under genuine uncertainty is to choose the option robust across both states of the world — the one that helps if the shift is real and does little harm if it isn’t. This is the no-regrets logic that ran through the whole track, applied to the menu.

How the options sort by robustness

The sort differs from the rhetoric: do-nothing is robust if the shift isn’t happening and catastrophic if it is — fragile to the diagnosis that matters most. UBI is a flexible hedge (helps in either state, deployable fast) but fiscally heavy and cause-blind — moderately robust. UBC is slow but robust across both states (an owned stake helps if the shift is real and is simply a productive asset if it isn’t) — robust but slow. Common-wealth funding is robust where worker-tax funding is self-undermining — robustly better on the funding axis regardless of the redistribution choice. The robustness test favors common-wealth funding unambiguously, and on the redistribution axis favors a combination — fast income floor (UBI) for the crisis, slow ownership build (UBC) for the structure — over any single pure option.

What this implies

Not a winner, a portfolio: the robustness test does not crown a single dish; it argues for a portfolio funded the right way — common-wealth funding (the robust foundation), a UBI-style floor for speed (the fast hedge), and a UBC-style ownership build for durability (the structural fix), with do-nothing’s adaptation support (wage subsidies, skills) layered in because eased reallocation helps in every state. The honest answer to “which option” is “fund it from common wealth, and combine a fast floor with a slow ownership build” — which is not the answer any single camp is selling, because each camp is selling its one dish.

What this is not

It is not a claim that the diagnosis is settled. The labor share showed it isn’t. The menu is a response to uncertainty, not to a proven shift.

It is not a disguised pitch for my preferred option. Ownership survives the robustness test, but so does common-wealth-funded UBI as the fast complement — and do-nothing’s adaptation support survives as a layer. The portfolio, not ownership alone, is what robustness favors.

It is not a claim that politics will choose well. The menu is about what’s defensible, not what’s likely. The funding axis is decisive and underweighted precisely because the politics reward arguing about the redistribution axis instead.

The synthesis observation

The distribution question has no single correct answer but a menu — do nothing, UBI, UBC, common-wealth funding — where each option optimizes for a different value and trades away the others, the funding axis (common wealth versus worker taxes) does more real work than the redistribution axis (income versus ownership), and under the irreducible uncertainty about whether the labor-share shift is real, the rational criterion is robustness, not optimization — which favors a common-wealth-funded portfolio (a fast income floor plus a slow ownership build plus adaptation support) over any single pure option. Choosing among the options is a values choice disguised as a technical one.

There is no single answer. Anyone offering one is selling something. That sentence has closed every dispatch in this catalog, and it has never been more literally true than here: the UBI advocate, the do-nothing economist, the ownership evangelist, the data-dividend reformer — each is selling the one dish they came to sell, presented as the obvious technical answer to a question that is actually about values. The honest service is the menu itself: here are the options, here is what each optimizes for and trades away, here is the funding axis that matters more than the fight everyone is having, and here is why robustness — not certainty — should guide the choice. The decision is yours, the tradeoffs are real, and the one thing you should not accept is anyone telling you it’s obvious. I favor ownership, and I have told you so, and I have also shown you that ownership alone fails the robustness test that a portfolio passes — which is what holding my own preferred option to the same scrutiny as the others requires.

That is the structural editorial question the policy menu sits on top of. It is a values document pretending to be a technical one. It has two axes the debate collapses into one. And it resolves not to a winner but to a way of choosing — robustness over optimization, common wealth over worker taxes, a portfolio over a pure option. And it is the close of the Post-Labor track: The stake asked what the response should be, The labor share asked whether the problem is real, The bottom rung found the sharpest evidence, and The policy menu lays the full set of responses on the table and refuses, on principle, to pretend the choice is anything other than yours.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the Post-Labor track

This dispatch

- This piece · The policy menu · the capstone — the full response set (do nothing, UBI, UBC, common-wealth funding) laid out evenhandedly, the two axes the debate collapses, and the robustness test for choosing under uncertainty · synthesis-deep dominant, all six registers in balance

The track it closes

- The stake · Post-Labor 01 · the ownership case this menu holds to the same scrutiny as every other option — UBC survives, but ownership alone fails the robustness test a portfolio passes

- The labor share · Post-Labor 02 · the unresolved premise that makes robustness, not optimization, the right selection criterion — you cannot optimize against a diagnosis you cannot yet confirm

- The bottom rung · Post-Labor news-flex · the sharpest signal, and the apprenticeship-severance argument for why the reallocation mechanism do-nothing relies on might be exactly what breaks

Adjacent tracks

- The conversion · AI Governance 05 · the cautionary case for UBC design — “ownership” that hands out tiny stakes while founders keep control is ownership in name only

- The runway · Enterprise Reorg 04 · the concentration of AI capital returns that the common-wealth funding model would tap

Sources

The do-nothing option

- Heritage Foundation · Why UBI is still a bad idea — the lump-of-labor fallacy; the historical record (41% of Americans in agriculture in 1900, under 2% today; the 1964 Johnson committee, the 1990s ATM fear); new and unimaginable jobs emerging each time; Friedman and Murray’s market-friendly UBI variants · heritage.org

- The Daily Economy · What 122 UBI experiments show — displacement is not permanent mass unemployment; “economies are not fixed piles of jobs”; Ryan Bourne (Cato) — UBI “confuses a transition problem with a permanent income problem”; the answer is to make adaptation easier, not pay for “economic resignation” · thedailyeconomy.org

- Aspen Institute Economic Strategy Group (Kearney & Mogstad) — a UBI does nothing to address root causes; a targeted wage subsidy would encourage work and increase take-home pay; a $10,000/year UBI would cost more than half the federal budget; the pro-work, pro-skills alternative · economicstrategygroup.org

UBI · the income option

- Newsweek · AI boom risks a UBI trap — Alaska’s ~$1,600 annual dividend, 40 years, no cratered employment (consumer sectors expanded), but financed by an oil sovereign-wealth fund, not new taxes; Finland 2017-18 (well-being up, employment flat); Germany’s crowdfunded study (life satisfaction up, hours unchanged); Q4 2025 hyperscaler capex $142B · newsweek.com

- Scott Santens · The urgent case for UBI — the gross-versus-net cost distinction (net cost ~a third of gross); “what does it cost to not do a basic income”; inflation as “the strongest critique,” manageable through funding design and supply-side policy; replacing existing programs · scottsantens.com

- Britannica · UBI pros and cons — the Roosevelt Institute models (UBI grows the economy across scenarios); Alaska’s 10,000 additional jobs from increased purchasing power; the Swiss government’s opposition (work-incentive concerns); the financial-security-to-leave-a-bad-job argument · britannica.com

- Reed · Pros and cons of UBI — the cost (one analysis: £472B gross in the UK); work-incentive concerns; the inflation channel (higher disposable income → higher demand → higher prices eroding the payment); the “shifts the goalposts” inequality critique · reed.com

UBC · the ownership option

- MEXC / industry roundup — Mark Garman’s Universal Basic Capital (income-producing assets and dividends via a superfund); Peter Diamandis’s Universal Basic Ownership (everyone owns a stake in the AI companies); Altman’s Universal Extreme Wealth; the case that cash (UBI) is the most immediately practical even alongside these · mexc.com

- UBIWorks · Basic income critics debate fake models — UBI dividends give citizens a stake in shared wealth (nature, public infrastructure, technological progress); Altman’s proposed US national fund (land value + corporate shares, ~$13,500/year per adult); Common Wealth Canada’s ~$7,500/year from economic rent; Varoufakis — UBI “cannot be financed by taxing Jill to pay Jack” · ubiworks.ca

The funding model · common wealth

- GovFacts · How UBI might make sense in the age of AI — public data as a natural resource AI extracts (royalties on training data); the sovereign-wealth-fund model (Alaska Permanent Fund); government equity stakes in AI corporations; the American Equity Fund; the AI-bubble risk (if valuations collapse, the funding evaporates) · govfacts.org

- Semafor · Debatable: UBI — the AI Dividend (direct payments funded by a token tax on AI usage and government equity stakes in frontier firms, triggered by economic thresholds); reforming the tax code that “rewards companies for replacing workers”; Cato’s Bourne — premature and too costly · semafor.com

- Tax Project Institute · Universal High Income — a UHI dividend implies “an enormous asset base… or some mechanism by which society accumulates ownership claims on the AI-and-robotics capital stock over time”; the “Labor Equivalent” robot/AI-replacement tax; the distribution system as “a choice… implemented through law, enforcement, and governance design” · taxproject.org

The track backbone

- The stake / The labor share / The bottom rung · Thorsten Meyer · Post-Labor 01, 02, news-flex · the ownership case, the unresolved premise, and the sharpest signal — the three dispatches this capstone synthesizes into a menu and a way of choosing

Key reference figures crystallized

- Do nothing: agriculture 41% (1900) → under 2% (today), no mass unemployment; the 1964 and 1990s automation panics wrong; Cato/Aspen — UBI confuses a transition problem with a permanent-income problem; robust if the shift isn’t real, catastrophic if it is

- UBI: Alaska ~$1,600/yr, 40 years, work-neutral; Finland 2017-18 and Germany — well-being up, employment flat; 122 pilots — security up, work not boosted; $10,000/yr ≈ half the federal budget; net cost ~⅓ gross; the funding trap (“taxing Jill to pay Jack”)

- UBC: Garman (universal basic capital), Diamandis (universal basic ownership), Altman’s national fund (~$13,500/yr from land + shares); an owned stake survives what a transfer doesn’t; slow (decades to build), concentration-prone if mis-designed

- The funding model: common wealth not worker taxes (Varoufakis); data royalties, compute taxes, public equity stakes, sovereign wealth funds (Alaska oil, Norway); can fund either UBI or UBC; the AI-bubble risk if valuations collapse

- The two axes: what you redistribute (nothing / income / ownership) versus how you fund it (worker taxes / common wealth); the funding axis does more real work; “UBI vs UBC” is partly an argument about the wrong axis

- The robustness test: choose for least-harm-if-wrong, not best-if-right (because the diagnosis is unconfirmable); favors common-wealth funding unambiguously and a portfolio (fast income floor + slow ownership build + adaptation support) over any pure option