Part 10 of a five-day series on the 2026 memory crunch — the finale. The first nine chapters explained the squeeze and how to live inside it. This one asks when, if ever, it ends.

Every reader who’s followed this series to here is really asking one quiet question: do I just have to wait this out? You’ve right-sized, you’ve quantized, you’ve decided whether to build or rent. Now you want to know if there’s a date on the calendar when memory gets cheap again and the discipline can relax.

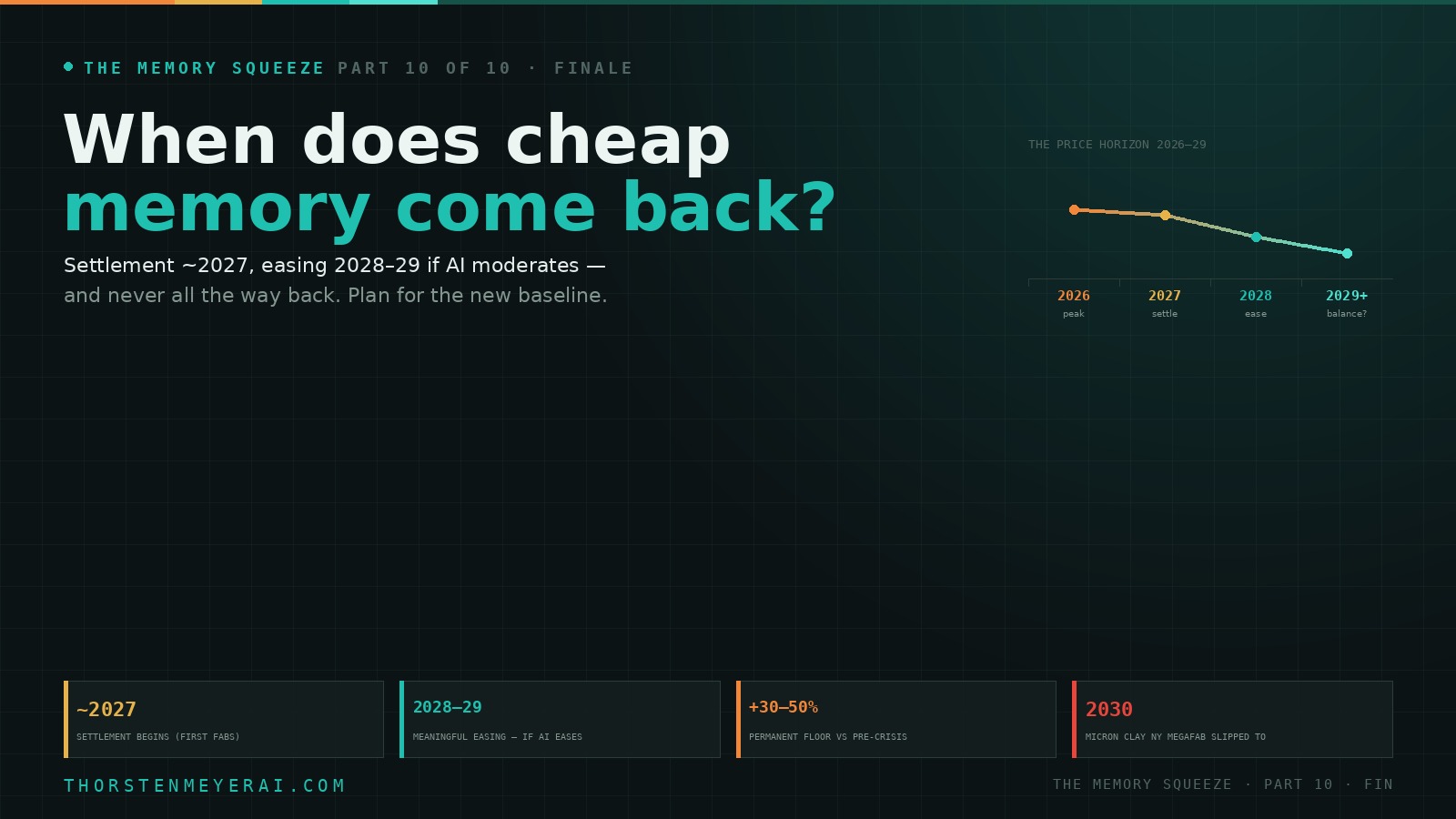

The honest answer is a timeline, three scenarios, and a piece of news you may not want to hear: the cheap memory you remember isn’t coming back. A less expensive memory market probably is — but later than you’d like, and resting at a permanently higher floor. Here’s the map.

When does cheap memory come back?

The question everyone’s really asking: do I just wait this out? The honest answer is a timeline, three scenarios, and news you may not want — the cheap memory you remember isn’t coming back. A less-expensive market probably is — later, and at a higher floor.

Capacity ramps ’27–’28; price climbs stop, then ease. Settles ~30–50% above pre-crisis — the new baseline, not a return to 2024.

AI keeps accelerating; OpenAI locked ~40% of DRAM through 2029; makers pause expansion to protect record margins; each HBM gen worsens the math.

AI demand moderates just as delayed ’27–’28 fabs all arrive → classic overshoot → prices crash. Not the bet — but never impossible in this industry.

The one relief valve that needs no fab is efficiency: if compression (Part 9) cuts how much memory each model needs, demand softens on the timescale of a software update, not a construction project. So the posture isn’t waiting — it’s the discipline this series has been about. Memory is now a scarce, valuable resource; treat it that way. Buy what you need, right-size, own what’s steady, rent what’s spiky, quantize either way. The people who do best won’t be the ones who guessed the bottom — they’ll be the ones who stopped needing so much. That’s the squeeze, end to end.

The consensus timeline

Strip away the noise and the analysts converge on a fairly tight range. Settlement begins around 2027. IDC expects prices to stabilize by mid-2027; Counterpoint calls Q4 2027 the “earliest inflection point”; Intel’s CEO has flatly said there’s “no relief until 2028.” The memory makers themselves — Samsung and SK Hynix — warn the shortage could run through 2027 “and beyond,” with the industry consensus landing on late 2028 for a genuine easing and 2028–2029 for anything resembling normal pricing and availability.

The reason for the lag is physical, and it’s worth seeing concretely, because it’s why no amount of money makes relief arrive sooner. New fabs take years to build and ramp. The 2027 wave — Micron’s Idaho fab starting DRAM production mid-year, Micron Singapore and Taiwan, SK Hynix’s Yongin cluster and its $13 billion Cheongju packaging plant — is the first real capacity addition, and much of it is HBM-focused. The 2028 wave adds SK Hynix’s Indiana plant and a new Samsung Pyeongtaek line. And the single largest planned addition, Micron’s Clay, New York megafab, slipped to 2030. CHIPS Act-funded US fabs mostly target 2028–2030 starts, so they don’t touch the near term at all. Cleanroom space is the bottleneck, and you cannot pour concrete faster than concrete pours.

CORSAIR Vengeance LPX DDR4 RAM 32GB (2x16GB) Up to 3200MHz CL16-20-20-38 1.35V Intel XMP AMD EXPO Computer Memory – Black (CMK32GX4M2E3200C16)

Disclaimer: Maximum Speed requires overclocking/PC BIOS adjustments. Maximum speed and performance depend on system components, including motherboard and…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three scenarios, honestly weighed

No one knows the future of a market this turbulent, so the responsible thing is to lay out the plausible paths rather than pretend at a single forecast.

The base case — gradual relief, higher floor (most likely). New capacity ramps through the second half of 2027 and into 2028. The brutal quarter-over-quarter price climbs stop, then reverse modestly. By 2028–2029, supply and demand move back toward balance — if AI infrastructure spending grows at a merely rapid pace rather than an explosive one. But “relief” here means prices stop rising and ease somewhat, not a return to 2024. The settling point is widely expected to be 30–50% above pre-crisis levels, permanently. IDC’s framing is the one to internalize: the mid-2026 market is the new baseline, not a temporary deviation.

The bear case — the shortage extends past 2029. Several forces could keep it tight well beyond the consensus. AI demand is still accelerating, not cooling. A huge share of supply is already spoken for — OpenAI reportedly locked up long-term agreements for roughly 40% of global DRAM wafer output through 2029 for its Stargate buildout. The makers are posting the most profitable quarters in their history and have signaled they may pause expansion rather than overbuild, because flooding the market would crush the margins the scarcity created. And each new HBM generation makes the underlying math worse: HBM4E in late 2027 and HBM5 toward 2028–2029 each concentrate more wafer capacity in lower-yield, more wafer-hungry processes, so future transitions could deliver fresh commodity-DRAM shocks rather than relief.

The wildcard — a glut and a crash. The memory industry’s entire history is boom and bust, and the classic ending is still possible: AI demand moderates — a spending pullback, an “AI winter,” or simply efficiency catching up — at the exact moment all those delayed 2027–2028 fabs come online at once. Supply overshoots a softening demand, and prices crash the way they always eventually have. It’s not the bet to make, but anyone who tells you it’s impossible hasn’t watched this industry for forty years.

G.SKILL RipjawsV Series DDR4 RAM (XMP) 16GB (2x8GB) 3200MT/s CL16-18-18-38 1.35V Intel AMD Desktop Computer Memory U-DIMM – Black (F4-3200C16D-16GVKB)

G.SKILL RipjawsV Series DDR4 U-DIMM Memory Kit, Model: F4-3200C16D-16GVKB

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why even relief will disappoint

Notice that even the base case is modest, and that’s not an accident. Three structural features cap how good “better” can get.

First, the packaging bottleneck. Even when DRAM wafers exist, HBM has to be assembled with advanced packaging — TSMC’s CoWoS, SK Hynix’s MR-MUF — and that capacity is its own hard ceiling. Wafers alone don’t make finished memory. Second, the makers’ discipline. With AI demand sitting at predictable, contracted levels, adding capacity beyond current plans genuinely may not make financial sense for them — and the record profits give them every reason to keep supply tight. As flagged back in Part 1, that’s not a conspiracy; it’s rational behavior by three firms that control over 90% of the market, and it points away from a price-collapsing glut. Third, the generational treadmill of HBM keeps redirecting the newest, best capacity toward the most wafer-intensive product, so consumer and commodity memory stays at the back of the line by design.

A-Tech DDR3L RAM 16GB Kit (2x8GB) 1600MHz PC3L-12800 SODIMM Laptop Memory

A-Tech 16GB RAM Kit (2 x 8GB Modules), DDR3/DDR3L SO-DIMM 204-Pin, 1600MHz PC3L-12800 (PC3L-12800S)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The one relief valve that doesn’t need a fab

There is a more hopeful thread, and it’s the one this series has been pulling toward: the supply side isn’t the only lever. Demand can fall without anyone buying less AI — if the AI needs less memory.

That’s the quiet promise of the compression work from Part 9. If techniques like Google’s TurboQuant and the broader move to 4-bit weights and compressed caches meaningfully cut how much memory each model and each query consumes, the demand curve softens without waiting for a single new cleanroom. Efficiency, not fabrication, may be the faster path to relief — better stacking yields, tighter coordination between memory makers and chip designers, and software that simply needs fewer gigabytes to do the same work. It won’t reverse the shortage on its own. But it’s the one force that can ease the squeeze on the timescale of a software update rather than a construction project, and it’s entirely in builders’ hands.

CORSAIR Vengeance LPX DDR4 RAM 32GB (2x16GB) Up to 3200MHz CL16-20-20-38 1.35V Intel XMP AMD EXPO Computer Memory – Black (CMK32GX4M2E3200C16)

Disclaimer: Maximum Speed requires overclocking/PC BIOS adjustments. Maximum speed and performance depend on system components, including motherboard and…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The take — and the close

So: when does cheap memory come back? Settlement around 2027, meaningful easing 2028–2029, and never all the way back — the floor has reset higher, probably for good. Plan for the new baseline, not the old one.

Which means the right posture isn’t waiting; it’s the discipline this whole series has been about. Memory is no longer the cheap, abundant afterthought it was for twenty years — it’s a structurally scarce, structurally more valuable resource, and treating it that way is simply how computing works now. Buy what you genuinely need, when you need it. Right-size everything. Own what you’ll run steadily, rent what you’ll run unpredictably, and quantize either way. Don’t panic-buy capacity against a future that may not arrive, and don’t wait on a price drop that the fab calendar says isn’t coming.

The AI era was built on an unspoken assumption that memory would always be cheap and plentiful. That assumption broke in 2025, and it isn’t being repaired so much as replaced — with a market where memory is precious, allocated, and contested, all the way from a wafer in Korea to the RAM you almost didn’t notice you were buying. The people who do best in it won’t be the ones who guessed the bottom. They’ll be the ones who stopped needing so much.

That’s the squeeze, end to end. Thanks for reading all ten.

Sources: IDC and Counterpoint (price-stabilization timing); Intel CEO comments via tech-insider; TechPowerUp and ASML (fab/EUV ramp timelines, late-2028 expectations, expansion-pause signals); SoftwareSeni and The Diligence Stack (2027/2028 fab waves, Micron $200B plan, Clay NY delay to 2030, packaging bottleneck); Tom’s Hardware (Samsung/SK Hynix multi-year warnings, record profits); financialcontent/TokenRing (OpenAI ~40% DRAM-through-2029 reporting); TurboQuant/compression per Part 9. Figures reflect reporting as of late June 2026 and are fast-moving; forecasts are inherently uncertain. Analysis and opinions are the author’s and not financial advice.