Sixty billion dollars for a code editor sounds like the punchline of a bubble. It might be one of the shrewdest deals Elon Musk has ever made.

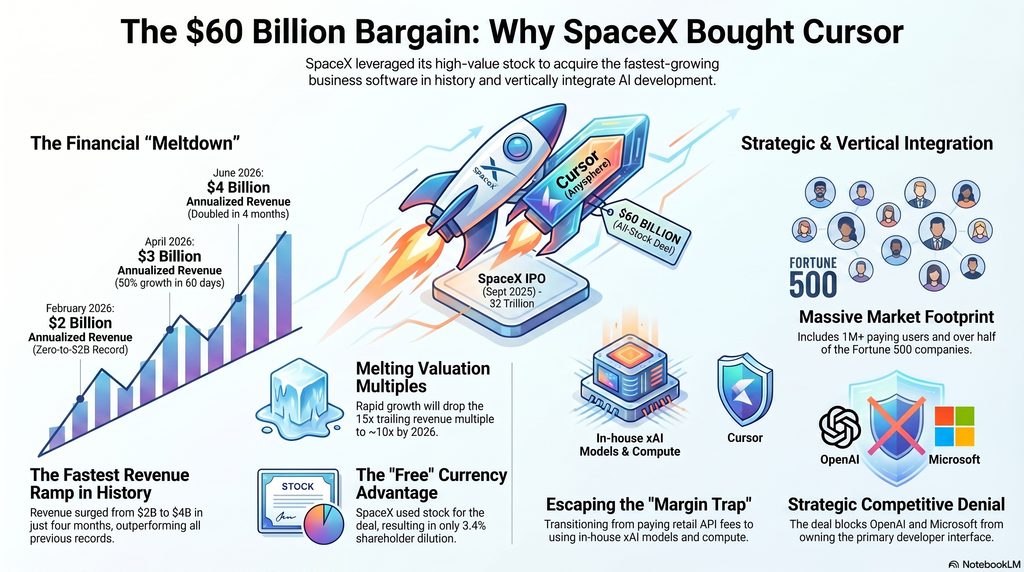

On June 16 — four days after SpaceX priced the largest IPO in history at a valuation north of $2 trillion — it exercised an option to buy Anysphere, the maker of the AI coding tool Cursor, for $60 billion in all-stock. The reflexive reaction was sticker shock: the largest acquisition of a venture-backed startup ever, at roughly 15 times revenue, for a company most people outside software had never heard of.

But look past the headline number and a different story emerges — one where the price isn’t the scandal, it’s the discount. Here is the case that SpaceX got Cursor cheap.

The $60B bargain: why Cursor could be a steal

$60 billion for a code editor sounds like a bubble. Look past the headline and the price isn’t the scandal — it’s the discount. Here’s the case that SpaceX got Cursor cheap.

A melting multiple, paid in appreciating paper that cost almost nothing, for the profitable leader of the only AI category reliably making money — plus the missing app layer and an escape from the margin trap. If the growth holds and integration doesn’t break the product, $60B will read like a down payment. The risk isn’t overpaying for what Cursor is — it’s breaking what made it worth buying.

The multiple that’s already shrinking

Start with the math everyone quotes and nobody finishes. Yes, $60 billion against Cursor’s roughly $4 billion in annualized revenue is about 15x — high by traditional software standards. But Cursor isn’t a traditional software company, and that multiple is melting in real time.

Trace the revenue curve: $2 billion in February, $3 billion in late April, $4 billion by early June. That’s a doubling in four months — the fastest ramp in the history of business software, faster even than the zero-to-$2-billion record Cursor already held. Anysphere now expects to clear $6 billion in annualized revenue by the end of 2026.

Run the multiple forward instead of backward and it collapses. At a $6 billion run-rate, $60 billion is 10x — and still falling. Acquirers routinely pay 15–25x forward revenue for AI software growing a fraction this fast. SpaceX paid a trailing-15x price for a company whose growth makes that look, within months, like a single-digit multiple. You don’t price a rocket by last year’s launches; you don’t price Cursor by last quarter’s revenue.

Cursor for Developers: Shipping Code Faster with an AI-Native Editor (Practical Programming)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The currency was practically free

Now the part that makes the price almost theoretical: no cash changed hands.

SpaceX paid entirely in its own freshly minted Class A stock — and the timing was surgical. The acquisition represented just 3.4% dilution at the IPO valuation; Cursor’s entire $60 billion price tag is under 3% of SpaceX’s market cap. Then the market did something unusual for an acquirer: SpaceX stock jumped about 16% on the news, helping push the company to roughly $2.94 trillion and briefly past Microsoft and Amazon to the fourth-most-valuable company in America.

Sit with that. SpaceX issued a sliver of richly valued paper, the paper appreciated on the announcement, and in exchange it received a business adding more than a third of SpaceX’s entire 2025 revenue of $18.7 billion. When your currency is trading at a multi-trillion-dollar valuation and the market cheers every time you spend it, acquisitions are close to free. That’s the same playbook Musk used folding xAI into SpaceX — pay with expensive stock while it’s expensive.

The AI Side Engine: Build Side Hustles and Small Businesses with AI Marketing and Lead Systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What $60 billion actually buys

A price is only a bargain relative to what you get. Strip Cursor down and SpaceX bought four things that are individually valuable and collectively strategic.

A profitable foothold in the one AI business that works. Coding is the rare corner of generative AI making real money, and Cursor leads it: over a million paying users, 50,000 enterprise customers, more than half the Fortune 500. Crucially, its enterprise subscription segment already runs positive gross margins — a profitability most AI companies can only dream of, and a sharp contrast to SpaceX’s own cash-hungry rocket and satellite lines.

The developer gateway. As AI competition shifts from benchmarking models to owning workflows, Cursor is the surface developers sit inside all day — and therefore the gateway through which enterprise AI budgets flow. Owning that surface is owning a distribution chokepoint, the layer that decides which model gets reached.

A model team and a working in-house model. Cursor didn’t just resell others’ models; in late 2025 it shipped Composer, its own coding model (built atop open weights), and by version 2.5 the model was doing the overwhelming majority of the work. SpaceX acquired a proven applied-AI team and a shipping product — plus the joint Cursor-xAI model already slated for both Cursor and Grok.

Denial to the competition. Cursor turned down OpenAI twice and rebuffed Microsoft. By taking it off the board, SpaceX denied OpenAI a key distribution channel and handed xAI — which had badly trailed in developer tools — instant leadership. Buying the asset is half the value; keeping rivals from buying it is the other half.

Competitive Programming 4 – Book 1: The Lower Bound of Programming Contests in the 2020s

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The hidden bargain: escaping the margin trap

Here’s the part the spreadsheets miss, and the single best argument that $60 billion is cheap.

Cursor was quietly being squeezed by its own suppliers. It paid retail API prices for frontier models while the labs that sold them — most pointedly Anthropic, with Claude Code — ran wholesale economics on their own competing coding tools. The result showed up in the numbers: by one spending-data measure, Cursor’s category share slid from about 41% to 26% even as its revenue grew, while Anthropic’s climbed toward 50%. Cursor was running up an escalator that its model providers controlled.

That is exactly the trap SpaceX is positioned to spring. It owns the Colossus supercomputers and, through xAI, frontier models of its own. Folding Cursor into that stack turns its single largest cost — compute and third-party API fees, the only reason it isn’t already profitable — into an in-house input. A company that’s unprofitable solely because it rents intelligence from competitors becomes a very different business when it owns the intelligence. The acquisition doesn’t just buy growth; it buys a path to fat margins on growth that’s already happening.

Vertical integration is the one move Musk has run successfully again and again — building the rockets, the engines, the satellites, and the launch pads in-house when everyone said to buy them. Cursor is the application layer of that same instinct applied to AI.

The No-Code AI Operating Manual: Design Practical Workflows, Assistants, and Systems Without Traditional Coding

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Now the other side

Because the strongest case deserves the strongest test, here’s why this could still go wrong — and why “bargain” carries an asterisk.

The cheap-currency logic cuts both ways. SpaceX paid in stock from a four-day-old IPO at a multi-trillion-dollar valuation; if that price proves frothy, it overpaid in a currency that can fall, and the “almost free” deal gets expensive in hindsight. Fifteen times revenue is still among the highest multiples ever paid for AI software — a bargain only if the torrid growth holds and doesn’t decelerate the way Cursor’s category share already has.

The margin fix has a catch, too. Escaping the trap means steering users toward in-house models — but Grok has struggled against Claude Code and OpenAI’s Codex, and Cursor’s whole appeal was best-in-class results from whatever model was best. The most-watched signal now is whether Claude, GPT, and Gemini stay first-class options inside Cursor or get throttled and repriced; the Windsurf precedent suggests restriction can happen fast, and developers are not a captive audience. Fix the margins by degrading the product and the bargain evaporates.

Then the ordinary risks: a fiercely independent startup that rejected OpenAI and Microsoft now folded into the Musk empire, with two product-engineering leads already gone; an antitrust review of a $60 billion deal by an already-sprawling conglomerate spanning launch, satellites, social media, automotive, and AI; and a coding-tools market — Copilot, Claude Code, Codex, Windsurf, Replit, Devin — that is as crowded as any in software. The deal is signed, not closed.

The bottom line

Weigh it honestly and the bull case is the stronger one. SpaceX paid a melting multiple, in appreciating paper that cost it almost nothing, for the profitable leader of the only AI category reliably making money — and, in the same stroke, handed itself the missing application layer, a model team, a distribution gateway, and an escape from the margin trap that was capping Cursor’s profits. If the growth holds and the integration doesn’t break the product, $60 billion will read, a year from now, like a down payment.

The risk isn’t that SpaceX overpaid for what Cursor is. It’s that, in absorbing Cursor, it breaks the very thing that made Cursor worth buying. Bargains, after all, are only bargains if you don’t ruin them on the way home.

Sources: SpaceX SEC filings; Reuters; Forbes; Business Insider; CNBC; Quartz; TechFundingNews; Ramp spending data as reported; and deal analyses from DigitalApplied, DigitalStrategy-AI, and TradingKey (April–June 2026). Revenue and valuation figures are as reported; forward figures are company projections. This piece argues a thesis and closes with its counter-case; it is analysis, not investment advice.