The ownership argument I made in The stake rests on a premise: that value is moving from labor to capital. If that premise is false — if labor’s share of income is stable and AI reshapes work rather than capturing its returns — then the case for broad-based ownership loses its urgency, and the honest thing to do is say so. So this dispatch tests the premise against the data, and the data is not on anyone’s side yet.

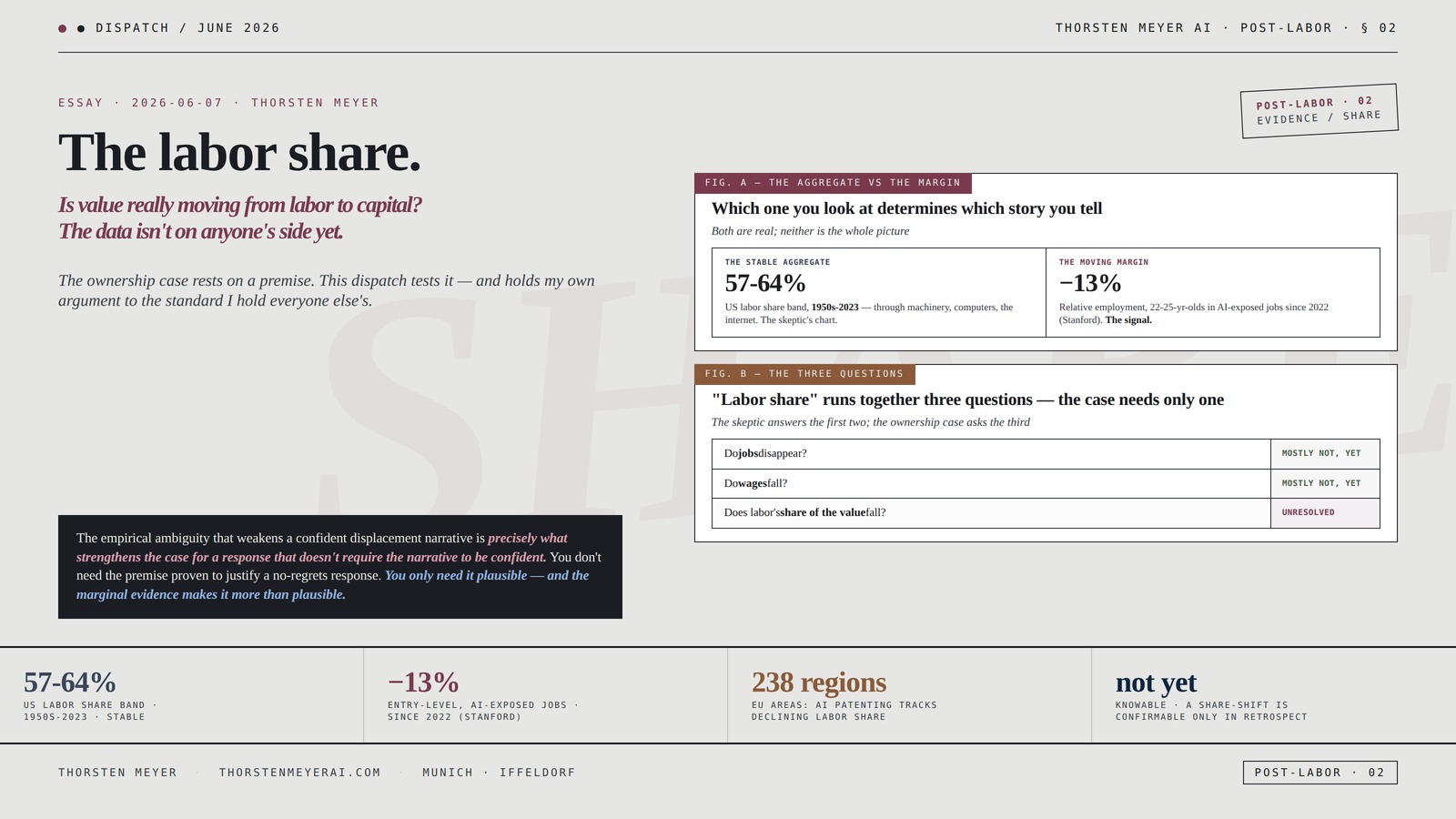

Start with the number that anchors the skeptics. The US labor share of income has fluctuated within a relatively narrow band — roughly 57 to 64 percent — from the 1950s to 2023, through industrial automation, computers, and the internet. Seventy years of enormous technological change, and labor’s slice of the pie stayed within a seven-point range. The strongest version of the case against my premise is simply this chart: if labor’s share survived every prior wave, why would AI break it?

Now the number that anchors the other side. A Stanford study of millions of payroll records found a roughly 13 percent relative decline in employment for 22-to-25-year-olds in the most AI-exposed occupations since late 2022 — even controlling for firm-level shocks — while older workers in the same jobs held steady or grew. The aggregate is stable; the margin is moving. And the margin is moving exactly where the theory predicts: the entry-level, routine-cognitive work that AI automates first.

The gap between those two numbers is the whole dispatch. The aggregate labor share is stable, and the margin is shifting — and which one you look at determines which story you tell. Look at the seventy-year band and AI is just the next wave that labor will absorb. Look at the entry-level cohort and AI is a capital-biased technology already reallocating returns. Both are real. Neither is the whole picture. And the disagreement between serious people is not about the facts but about which facts are load-bearing.

The structural argument I want to make: the premise under the ownership case — that value is moving from labor to capital — is true at the margin and not yet true in the aggregate, and the honest reading of the evidence is that it is genuinely unresolved, because the aggregate labor share has been stable for seventy years while the early, marginal signals (entry-level displacement, European regional labor-share declines tied to AI patenting, eroding bargaining power) point in the direction the theory predicts — which means the ownership case rests not on a proven aggregate shift but on a marginal one that may or may not become aggregate. This is the second Post-Labor dispatch, and it is the empirical floor under the first: The stake argued ownership is the right response if value is moving to capital; this asks whether it is, and finds the answer is “at the edges, so far, maybe.”

The headline integrative finding: The honest both-sides read is that the displacement camp and the stability camp are looking at different time horizons of the same process, and the data cannot yet tell us which horizon wins. The stability camp is right that the aggregate has not moved and that workers have always reallocated before. The displacement camp is right that the marginal signals are real, concentrated, and pointed in the predicted direction. The deepest point is that “labor share” is three different questions people conflate — whether jobs disappear (mostly not, yet), whether wages fall (mostly not, yet), and whether labor’s share of the value falls (the real question, and the one the aggregate has not yet answered but the margin has begun to) — and the ownership case depends on the third question, which is precisely the one the data is least equipped to settle in real time, because a share-shift is visible only in retrospect. The premise is not proven. It is also not refuted. And a policy that helps whether or not the premise proves true — which is what broad-based ownership is — is the rational response to exactly this kind of unresolved evidence.

This essay walks the stable aggregate, the moving margin, the three questions people conflate, the bargaining-power channel, the skeptic’s strongest case, the verdict the data can and cannot support, and the structural reading of a premise that is real at the edges and unproven at the center.

The labor share.

Is value really moving

from labor to capital?

The data isn’t on

anyone’s side yet.

the skeptic’s strongest chart

in AI-exposed jobs since 2022 (Stanford)

declining labor share (Minniti et al.)

confirmable only in retrospect

The empirical ambiguity that weakens a confident displacement narrative is precisely what strengthens the case for a response that doesn’t require the narrative to be confident. You don’t need the premise proven to justify a no-regrets response. You only need it plausible — and the marginal evidence makes it more than plausible.Thorsten Meyer · The Labor Share · Post-Labor 02

By Thorsten Meyer — June 2026

This is the second dispatch in the Post-Labor track — the economics of value migrating from labor to capital. The first made the structural and policy case for broad-based ownership; this one tests the empirical premise that case rests on. It is the dispatch that holds my own argument to the standard I hold everyone else’s: state the strongest version of the case against, and do not claim the data proves more than it does.

The structural argument I want to make: the labor-share debate is not a factual disagreement but a disagreement about which signal is load-bearing — the stable aggregate or the moving margin — and that disagreement cannot be resolved by more data in the present, only by the passage of time, because a durable share-shift is a thing you can only confirm after it has happened. The skeptic points at the stable seventy-year band; the worrier points at the entry-level cohort; and both are reading the same economy correctly, because the economy is in the early, ambiguous part of whatever process this is.

The headline integrative finding: The premise under the ownership case is unproven, and that is the most useful thing to know about it. Not false — the marginal evidence is real and predicted. Not proven — the aggregate has not moved. The correct response to a premise that is real at the margin and unconfirmed at the center is not to wait for proof (which arrives only after the shift is irreversible) and not to act as if it were certain (which the data does not support) — it is to favor responses robust to the uncertainty, which is exactly the no-regrets argument for broad-based ownership: it helps if the margin becomes the aggregate, and it does little harm if it does not. The empirical ambiguity is not an argument against the ownership case. It is the strongest argument for it.

This essay walks the stable aggregate (Section I), the moving margin (Section II), the three questions (Section III), the bargaining-power channel (Section IV), the skeptic’s case (Section V), the verdict (Section VI), and the structural reading (Section VII).

I · The stable aggregate · the skeptic’s strongest chart

The stability crystallization. Begin with the evidence against my own premise, because it is genuinely strong and deserves to be stated at full strength. The aggregate labor share has not moved, and it has not moved through technological changes as large as AI.

The seventy-year band

57 to 64 percent, 1950s to 2023: the US labor share of income has fluctuated within a relatively narrow band — roughly 57 to 64 percent — from the 1950s through 2023 (ITIF, May 2026). That span includes the spread of industrial machinery, the computer, and the internet. Each of those was, in its moment, the technology that was going to break the relationship between work and income — and the labor share absorbed all of them and stayed in its band.

The reallocation pattern

Workers move; they do not vanish: the historical record is one of reallocation. Workers displaced by automation transition to new occupations and industries, including ones the new technology creates. The labor share is stable because the economy keeps inventing new labor-side work as fast as the old work is automated. The skeptic’s case is not that AI does nothing — it is that AI, like every prior wave, reshapes the composition of work without shrinking labor’s slice.

The current data backs the skeptic, so far

No economywide displacement through 2024-25: multiple 2025-26 studies using administrative records and large surveys find no evidence of economywide job loss or wage decline despite rapid AI adoption (35.9% of US workers used generative AI by December 2025, with small positive wage effects in some studies). The Dallas Fed found wages in AI-exposed jobs not uniformly declining — consistent with augmentation, not replacement. As of early 2026, the aggregate data is on the skeptic’s side: the share is stable, employment is stable, and wages are not falling.

The stable-aggregate observation

The aggregate labor share has been stable within a 57-64% band for seventy years through automation, computers, and the internet, workers have reliably reallocated rather than disappeared, and the 2024-25 data shows no economywide displacement or wage decline despite rapid AI adoption. This is the skeptic’s strongest case and it is genuinely strong. Any honest version of the ownership argument has to begin by conceding that the aggregate evidence does not yet show value moving from labor to capital — and that the burden is on the displacement camp to explain why this wave differs from the ones the labor share absorbed.

The Graduate AI Survival Guide: Stand out and Get Hired in a Hyper-Competitive Job Market

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The moving margin · where the signal actually appears

The marginal crystallization. The aggregate is stable, but the aggregate is a sum, and sums can be flat while their components move in opposite directions. Look beneath the aggregate and a signal appears — concentrated, real, and pointed where the theory says it should be.

The entry-level decline

13 percent, 22-to-25-year-olds, AI-exposed jobs: the Stanford study (Brynjolfsson, Chandar, Chen) of millions of payroll records found a roughly 13 percent relative decline in employment for 22-to-25-year-olds in the most AI-exposed occupations since late 2022 — controlling for firm-level shocks — while older workers in the same occupations stayed steady or grew. The displacement is not economywide; it is concentrated at the entry level of exactly the jobs AI automates — customer service, junior software, routine analysis.

The automation-versus-augmentation split

The signal tracks the mechanism: the same research finds the effect depends on how AI is used. Where AI automates a task (writing code, handling customer chats), entry-level hiring declines; where it augments (supporting problem-solving, checking accuracy), employment holds or rises. The displacement appears precisely where the theory predicts — where AI substitutes rather than complements — which is evidence that the signal is causal, not coincidental.

The European share evidence

AI patenting tracks declining labor share: analysis across 238 regions in 21 European countries finds that regions with higher AI-patenting intensity have experienced more pronounced declines in labor’s share of income, particularly in industrial areas (Minniti et al.) — suggesting AI functions as a capital-biased technology, reallocating returns toward firms and capital owners. This is the share-shift itself, observed regionally: where AI is most intensively developed, labor’s share falls fastest.

The moving-margin observation

Beneath the stable aggregate, a real signal appears: a ~13% relative employment decline for young workers in AI-exposed jobs (concentrated where AI automates rather than augments), and European regional evidence linking AI-patenting intensity to declining labor share. The margin is moving in the direction the theory predicts. This is the displacement camp’s strongest case, and it is also genuinely strong: the signal is concentrated, mechanism-consistent, and — in the European data — visible as an actual share-shift. The aggregate has not moved; the margin has, exactly where it should.

J. J. Keller 2024 Emergency Response Guidebook (ERG), Spiral Bound, 4” x 5.5” Pocket Size, English, 1-Pack

- Compliance with DOT Regulations: Meets 49 CFR 172.602 requirements

- Emergency Response Preparedness: Color-coded, indexed ERGs for quick access

- 2024 Updates with QR Code: Includes QR code for incident reporting access

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The three questions · what “labor share” actually means

The disaggregation crystallization. Much of the disagreement dissolves once you separate three questions that “is AI taking the jobs” runs together. They have different answers, and the ownership case depends on only one of them.

Question one: do jobs disappear?

Mostly not, yet: the employment data is, in aggregate, stable — no economywide job loss through 2024-25. Even the entry-level decline is a relative decline (young workers in exposed jobs growing slower than older ones), not mass unemployment. On the jobs question, the skeptic is winning: AI is not, so far, producing aggregate joblessness.

Question two: do wages fall?

Mostly not, yet: wages in AI-exposed occupations are not uniformly declining; some studies find small positive wage effects. On the wages question, too, the skeptic is largely winning: AI is not, so far, cutting pay across the board.

Question three: does labor’s share of the value fall?

The real question — and the unresolved one: the ownership case does not depend on jobs vanishing or wages falling. It depends on labor capturing a smaller share of the value created, even if employment and wages hold. A worker can keep their job and their wage while the share of output going to wages (versus profits) declines — that is the capital-share rise, and it is compatible with full employment. This is the question the aggregate has not answered (the share is stable so far) but the margin has begun to (the European regional evidence) — and it is the only one of the three the ownership case actually rests on.

Why the conflation matters

The skeptic answers questions one and two; the ownership case asks question three: the stability camp’s strongest evidence (stable employment, stable wages) addresses the first two questions. The ownership case concedes those and asks the third — which is harder to measure, slower to appear, and visible mainly in retrospect. The debate often talks past itself because the skeptic is refuting “AI causes mass unemployment” (which the ownership case does not claim) while the ownership case is asserting “AI raises capital’s share” (which the skeptic’s employment data does not address).

The three-questions observation

“Labor share” runs together three distinct questions — do jobs disappear (mostly not, yet), do wages fall (mostly not, yet), and does labor’s share of the value fall (the real question, unresolved) — and the ownership case depends only on the third, which is the hardest to measure and the slowest to appear. The skeptic’s strongest evidence answers the first two; the ownership case asks the third. Much of the apparent factual disagreement is actually a disagreement about which question matters — and once you see that the ownership case rests on the share question, not the jobs question, the stable employment data stops being a refutation and becomes simply an answer to a different question.

Advanced Analytics with Power BI and Excel: Learn powerful visualization and data analysis techniques using Microsoft BI tools along with Python and R … Automation — Excel & Power Platform)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The bargaining-power channel · how the share moves without jobs vanishing

The mechanism crystallization. If the share can fall while jobs and wages hold, there has to be a mechanism. The clearest one is bargaining power: AI shifts leverage from labor to capital even when it does not eliminate the job.

The leverage shift

The credible threat changes the negotiation: AI does not have to replace a worker to weaken their position; it only has to be a credible partial substitute. When an employer can plausibly do more with fewer people — or with AI assistance that makes each worker more replaceable — the worker’s bargaining power falls. A worker whose tasks are partly automatable negotiates from a weaker position, which shows up as a smaller share of the surplus going to wages over time, not as a layoff.

The entry-level mechanism

The automated learning curve: the entry-level decline reveals a specific channel. The “deal” of junior work — trading rote labor for mentorship and skill-building — breaks when AI does the rote labor. Firms that once hired juniors to do the grunt work (and learn from it) now have AI do the grunt work, narrowing the entry pathway. The career ladder loses its bottom rung — which does not show as aggregate unemployment but as a structural shift in who captures the value of early-career work: the firm with the AI, not the worker who used to do it.

Why this is hard to see

Bargaining-power shifts are slow and invisible: a layoff is an event; a bargaining-power shift is a gradual erosion. It appears as wages growing slower than productivity, as the share drifting down over years, as the surplus from AI-driven gains accruing to the firm rather than split with labor. This is precisely the kind of shift that is invisible in real time and obvious in retrospect — which is why the aggregate has not “moved” yet even if the mechanism is already operating.

The bargaining-power observation

The share can fall without jobs vanishing through the bargaining-power channel: AI weakens labor’s leverage by being a credible partial substitute, and it breaks the entry-level deal by automating the rote work juniors used to trade for mentorship — both of which shift value to capital gradually, as eroding wage share rather than as layoffs. This is the mechanism that reconciles stable employment with a falling share. It is also why the share question is so hard to answer in real time: bargaining-power erosion is a slow drift, not an event, visible in retrospect as the gap between productivity and wages — which means the ownership case rests on a mechanism that is, by its nature, confirmable only after it has done its work.

Sources of Income Inequality and Poverty in Rural Pakistan (RESEARCH REPORT (INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE))

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The skeptic’s strongest case · the premise might genuinely be wrong

The strongest-counter crystallization. Intellectual honesty requires the best version of the case that the whole premise is wrong — not just that the aggregate is stable, but that the marginal signal is being misread. That case is real, and it is the one to take most seriously.

The entry-level decline might not be AI

The interest-rate confound: the most serious challenge to the displacement reading is that the entry-level hiring collapse might not be AI at all. A 2025 NBER paper studying 25,000 workers across 7,000 workplaces found zero effect on earnings or hours — and replicated the early-career employment decline while showing it was not driven by firms actually adopting AI. The timing that looks like AI (entry-level hiring cratering as AI adoption surged) coincides with the Fed’s rate hikes from near-zero, which raised the cost of the speculative hiring that fuels junior recruitment. The entry-level decline may be a monetary-policy story wearing an AI costume — and the correlation that looks causal may be coincidence.

Adoption is not displacement

The exposure-displacement gap: high AI adoption (35.9% of workers) has not produced aggregate displacement, and the real-time data on AI use for work looks stable, not non-linear (Citadel Securities). The leap from “this job is exposed to AI” to “this worker is displaced by AI” is large and frequently unjustified. Exposure is a measure of what AI could do; displacement is what it has done — and the two diverge sharply outside the most routine tasks.

The reallocation prior is strong

Two centuries of base rate: every prior general-purpose technology triggered the same fear and the same outcome — disruption, reallocation, no aggregate collapse in labor’s share. The prior that AI follows this pattern is not naive; it is the most heavily-evidenced regularity in the economics of technology. To claim AI is different is to claim a break from a two-century pattern, and the burden of proof for that claim is high — higher than a single entry-level study clears.

The skeptic’s-case observation

The strongest case against the premise is serious: the entry-level decline may be interest-rate-driven rather than AI-driven (the NBER finding of zero earnings effect and AI-independent early-career decline), exposure is not displacement, and the two-century reallocation prior is the most heavily-evidenced regularity in technology economics. This case deserves to be taken as seriously as the displacement signal. The honest position concedes that the marginal evidence is contestable, the leading confound (monetary policy) is real, and the base rate favors reallocation — which means the premise under the ownership case is not just unproven but genuinely contested by good-faith analysis using the same data.

VI · The verdict · what the data can and cannot support

The epistemic crystallization. Having stated both cases at full strength, the question is what an honest reading actually licenses. The answer is narrower than either camp would like, and the narrowness is the point.

What the data supports

A real, concentrated, mechanism-consistent marginal signal: the data supports that there is an early signal — entry-level displacement in AI-automated work, regional labor-share declines tied to AI patenting — that is concentrated where the theory predicts and consistent with the automation-versus-augmentation mechanism. It is reasonable to believe the marginal shift is real and AI-related, even granting the confounds.

What the data does not support

An aggregate share-shift, or a confident forecast: the data does not support that value has, in aggregate, moved from labor to capital — the seventy-year band holds, employment is stable, wages are not falling. Nor does it support a confident forecast that the margin will become the aggregate; the confounds are real and the base rate favors reallocation. Anyone claiming the aggregate shift is proven, or that it is certainly coming, is reading more into the data than it holds.

The honest verdict

Unresolved, and resolvable only in retrospect: the premise is real at the margin and unproven at the center, and the nature of a share-shift is that it is confirmable only after it has happened. We are in the early, ambiguous part of whatever process this is, and the data cannot yet tell us whether the margin is the leading edge of an aggregate shift or a concentrated disruption the economy will reallocate around. The verdict is not “yes” and not “no” but “not yet knowable” — and that is not a dodge; it is the accurate epistemic state.

What this is not

It is not a claim that the premise is proven. The aggregate has not moved; the marginal evidence is contestable. The ownership case rests on a premise that is real at the edges and unconfirmed at the center.

It is not a claim that the skeptics are wrong. Their aggregate evidence is strong, their confounds are real, and their reallocation prior is well-founded. They may turn out to be right.

It is not a claim that we should wait for proof. A share-shift is confirmable only in retrospect, so waiting for proof means waiting until the shift is irreversible — which is the worst possible time to respond.

The synthesis observation

The premise under the ownership case — that value is moving from labor to capital — is true at the margin and not yet true in the aggregate, and the honest reading is that it is genuinely unresolved, because the aggregate labor share has been stable for seventy years while the marginal signals point where the theory predicts, and a durable share-shift is confirmable only in retrospect. The displacement camp and the stability camp are reading the same economy correctly at different horizons; the disagreement is about which signal is load-bearing, not about the facts.

There is no single answer. Anyone offering one is selling something. What the evidence actually licenses is narrow: a real marginal signal, an unmoved aggregate, and genuine uncertainty about whether the first becomes the second. And that uncertainty — not certainty in either direction — is the strongest case for broad-based ownership, because ownership is the response that is robust to not knowing: it helps if the margin becomes the aggregate (labor’s lost share is replaced by owned capital income) and it does little harm if it does not (the citizen simply holds a productive asset in an economy where labor did fine). You do not need the premise proven to justify a no-regrets response to it. You only need it plausible — and the marginal evidence makes it more than plausible. The empirical ambiguity that weakens a confident displacement narrative is precisely what strengthens the case for a response that does not require the narrative to be confident.

That is the structural editorial question the labor share sits on top of. It is a stable aggregate and a moving margin, both real. It is three questions people conflate, of which the ownership case needs only the hardest-to-measure one. And it is a premise that is confirmable only in retrospect, which is exactly why a no-regrets response beats waiting for proof. And it is the empirical floor under the whole Post-Labor track — not a proven aggregate shift, but a real marginal one whose trajectory is unknown, which is a weaker foundation than the displacement camp claims and a stronger one than the skeptics allow, and which points, precisely because it is uncertain, toward the response that does not require certainty to be worth making.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the Post-Labor track

This dispatch

- This piece · The labor share · the empirical floor under the ownership case — testing whether value is actually moving from labor to capital, and finding it true at the margin, unproven in the aggregate, and resolvable only in retrospect · labor-rose dominant, structural-slate and empirical-clay balance

The track

- The stake · Post-Labor 01 · the structural and policy case this piece tests — ownership as the response if value is moving to capital; this dispatch asks whether it is

- Forthcoming · The policy menu · Post-Labor 03 · the response options laid side by side — UBI vs UBC vs data dividends vs do-nothing, evenhandedly · synthesis-deep register

Adjacent tracks · the margin observed in specific places

- The bottom rung · forthcoming · the entry-level compression this piece quantifies, as its own dispatch

- The referral · Post-Wire 03 · the publisher’s value share falling without the publisher disappearing — the share-shift in one industry

- The pyramid cracks · Enterprise Reorg 02 · the consultant’s billable share compressing — the bargaining-power channel in professional services

Sources

The stable aggregate

- ITIF (May 2026) · AI is not going to reduce labor’s share or destroy the tax base — the seventy-year band: US labor share fluctuated within ~57-64% from the 1950s to 2023 despite industrial machinery, computers, the internet; workers reallocate rather than disappear; the tax base erodes only if labor share falls dramatically and persistently, which is “highly unlikely”; policymakers should not restructure on the assumption of declining labor income · itif.org

- International Center for Law & Economics · AI, productivity, and labor markets review — no evidence of immediate economywide displacement through 2024-25; 35.9% of US workers used generative AI by December 2025 with small positive wage effects (Hartley et al. 2026); no aggregate employment decline (Chandar 2025); early adjustment through task reallocation, quality improvement, within-firm productivity gains; concentrated entry-level effects in highly exposed occupations · laweconcenter.org

- Citadel Securities · The 2026 Global Intelligence Crisis — little evidence of AI disruption in labor-market data as of today; the share of working-age adults using generative AI for work looks stable, not non-linear; high substitution elasticity could collapse labor share in theory, but redistribution and policy would be expected to offset worst cases · citadelsecurities.com

The moving margin

- Brynjolfsson, Chandar & Chen (Stanford) · Early employment effects of generative AI — ~13% relative decline in employment for 22-25-year-olds in the most AI-exposed occupations since late 2022, controlling for firm-level shocks; older workers in the same jobs steady or growing; the automation-vs-augmentation split (automation → entry-level decline, augmentation → stable/rising); BofA: recent-grad unemployment exceeding overall for the first time in recent memory · cnbc.com

- The Economy / Minniti et al. · When AI captures the surplus — analysis across 238 regions in 21 European countries: higher AI-patenting intensity correlates with more pronounced declines in labor’s income share, especially in industrial areas; AI as a capital-biased technology reallocating returns toward capital owners; AI diminishing worker bargaining power even when employment persists · economy.ac

- Rezi / Crisis of entry-level labor — the “learning curve” being automated; the entry-level deal (rote labor for mentorship) breaking; UK tech graduate roles −46% in 2024 (projected −53% further by 2026); US junior tech postings down sharply; healthcare/government/hospitality absorbing most 2024-25 job growth · rezi.ai

- Frontiers in Human Dynamics · Observed AI-driven labor displacement 2020-2025 — PRISMA systematic review: AI-driven displacement observable at the margin (lower-skill, lower-wage, routine cognitive work) before penetrating the core employment relationship · frontiersin.org

The skeptic’s strongest case

- Stanford Review · The class of 2026 is struggling — and it’s not because of AI — the NBER paper (25,000 workers, 7,000 workplaces): zero effect on earnings or hours, and the early-career employment decline replicated but shown not driven by firms actually adopting AI; the real driver as monetary — the Fed’s near-zero rates (2020-22) fueling speculative hiring that then reversed; Acemoglu/Autor on firm-level substitution not showing in macro data · stanfordreview.org

- ALM Corp · AI job displacement statistics — the Dallas Fed: wages in AI-exposed jobs not uniformly declining (augmentation, not replacement); Anthropic’s usage-based displacement measure finding high-usage AI occupations seeing modestly slower hiring (modest but accelerating); Goldman 6-7% of US workforce displaced long-term (~11M); NBER 2025 — ~3.9% at the intersection of high exposure and high automatability · almcorp.com

The ownership-case backbone

- The stake · Thorsten Meyer · Post-Labor 01 · the structural and policy case for broad-based ownership that this dispatch’s empirical test underwrites — ownership as the no-regrets response to exactly the kind of unresolved share-shift the data shows

Key reference figures crystallized

- The stable aggregate: US labor share ~57-64% band, 1950s-2023 (ITIF); no economywide displacement through 2024-25; 35.9% AI adoption with small positive wage effects; Dallas Fed — AI augmenting not replacing; Citadel — usage data stable, not non-linear

- The moving margin: Stanford — ~13% relative employment decline for 22-25-year-olds in AI-exposed jobs since late 2022 (controlling for firm shocks); automation → decline, augmentation → stable; Minniti et al. — AI-patenting intensity tracks declining labor share across 238 EU regions; UK tech grad roles −46% (2024)

- The three questions: jobs (mostly stable), wages (mostly stable), share of value (unresolved — the only one the ownership case needs)

- The bargaining-power channel: AI as credible partial substitute weakens leverage without layoffs; the automated learning curve breaks the entry-level deal; share-shift visible as productivity-wage gap, in retrospect

- The skeptic’s case: NBER (25,000 workers) — zero earnings effect, entry-level decline not AI-driven; the interest-rate confound (Fed 2020-22); exposure ≠ displacement; the two-century reallocation prior

- The verdict: real marginal signal + unmoved aggregate + genuine uncertainty; confirmable only in retrospect; “not yet knowable” — which is the strongest case for a no-regrets response (broad-based ownership) that does not require the premise proven