By Thorsten Meyer — May 2026

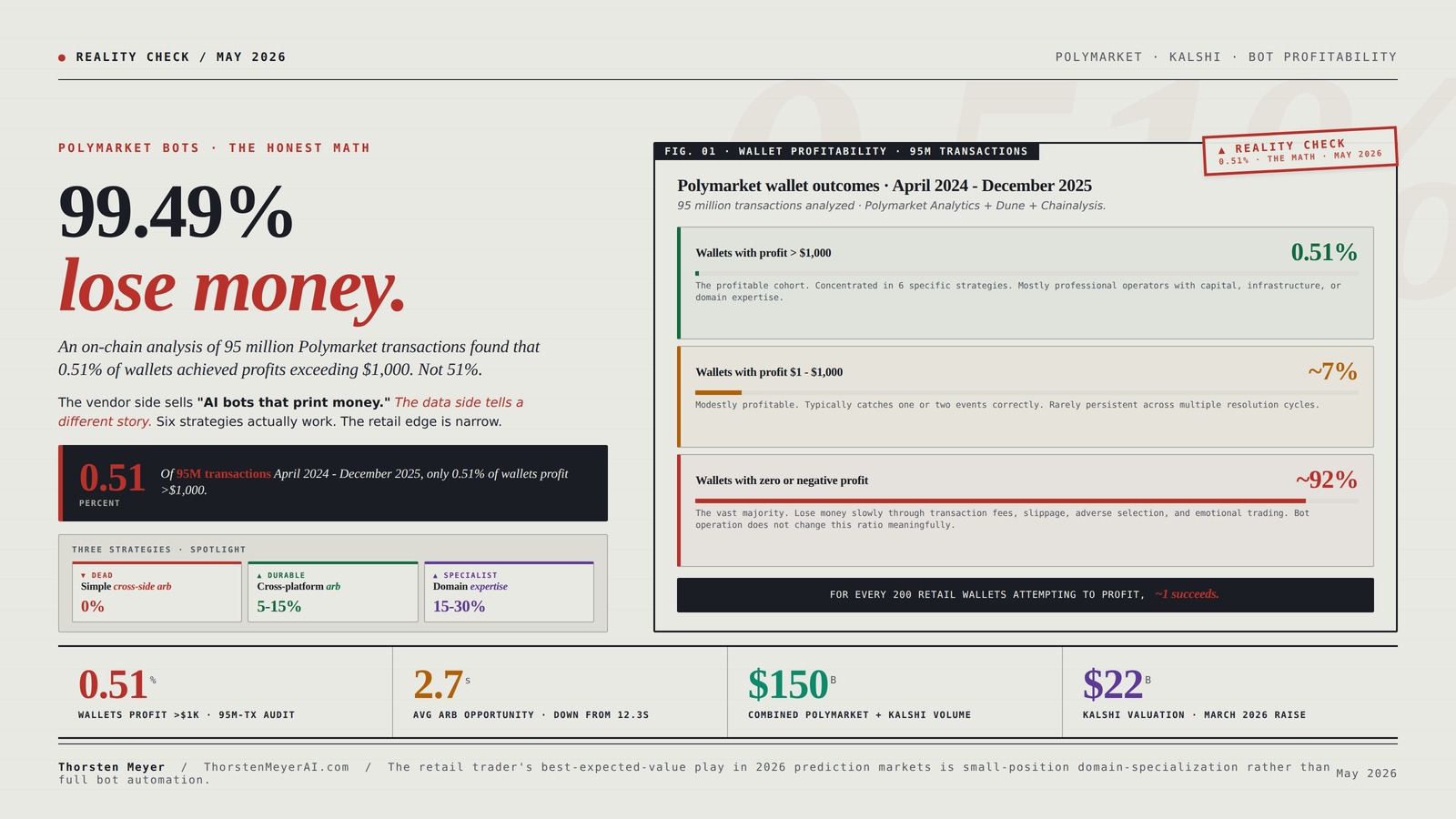

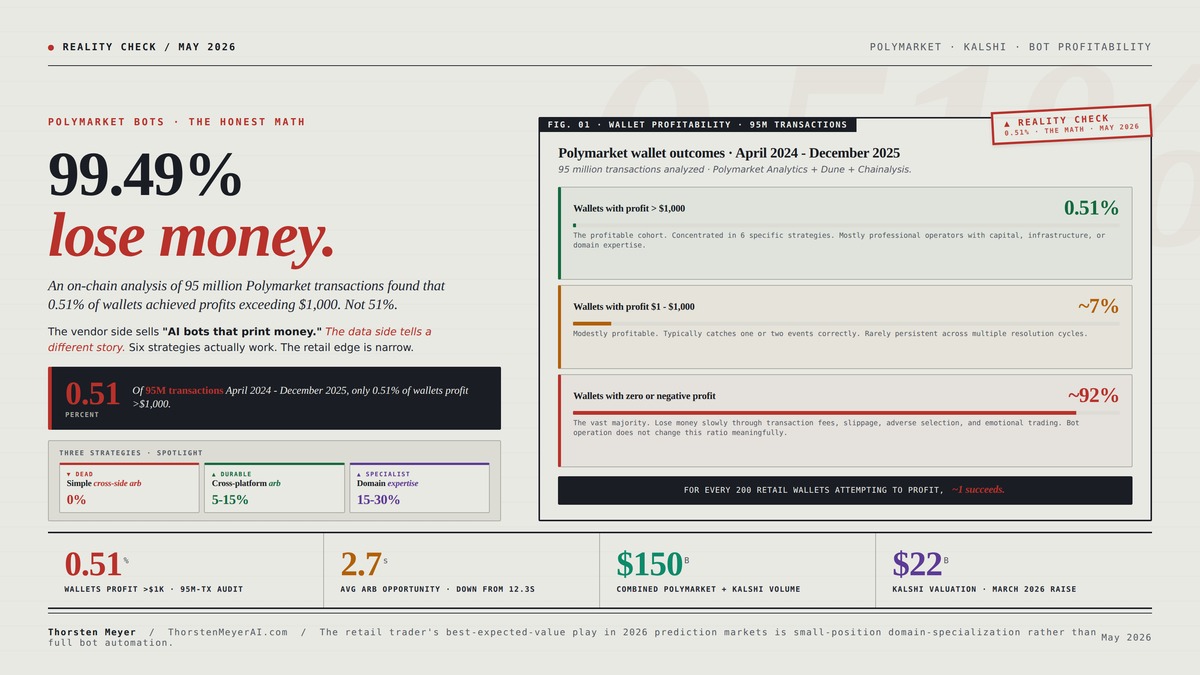

The honest answer to the question is uncomfortable. An on-chain analysis of 95 million Polymarket transactions covering April 2024 through December 2025 found that 0.51% of wallets achieved profits exceeding $1,000. Not 51%. Not 5.1%. Half of one percent. The remaining 99.49% either lost money outright, made trivial profits below the threshold, or broke even. The same study identifies six strategies that produce most of the upside in that 0.51%. None of them resemble the YouTube tutorial framing of “find arbitrage, click two buttons, collect free money.” All of them require either capital, infrastructure, domain expertise, or some combination that retail traders running off-the-shelf bots usually can’t assemble.

The “polymarket trading bot profitable” search query is one of the most-searched questions in the prediction-market category right now. It’s also one of the most asymmetrically answered. The vendor side — bot marketplaces, VPS hosting providers, automation guides — uses the framing of viral profit screenshots to sell tools and infrastructure. The data side — on-chain analyses, academic studies, and the published telemetry of competitive bot operators — tells a different story. In 2026, the median outcome for a retail Polymarket bot is to lose money slowly through transaction fees, slippage, and adverse selection. The exception cases that produce real profits are concentrated in narrow strategies that compete against well-capitalized counterparties.

This piece is the actual math. Six strategies that work. Three that look like they should work but don’t anymore. The Kalshi-vs-Polymarket cross-platform arbitrage opportunity (still alive, still hard). The information-arbitrage edge that AI agents create and immediately compete away. The regulatory overhangs from the CFTC’s March 2026 derivatives ruling and the state-level fights in Massachusetts, Nevada, and elsewhere. And an honest verdict on whether retail traders running Polymarket bots in 2026 should expect to make money — and if so, under what realistic conditions.

The deeper structural read connects to questions about AI agents in real markets generally. Polymarket and Kalshi are the cleanest available laboratory for AI-augmented trading because the markets are public, the data is transparent, the resolution is deterministic, and the regulatory environment is permissive enough to allow genuine experimentation. What works on Polymarket is a preview of what works in adjacent markets where AI agents are starting to compete — sports betting, crypto perpetuals, equity options, prediction markets on private events. The 0.51% number is informative not just for prediction-market traders but for anyone modeling how AI agents perform in efficient adversarial environments.

99.49%

lose money.

An on-chain analysis of 95 million Polymarket transactions found that 0.51% of wallets achieved profits exceeding $1,000. Not 51%. Half of one percent.

The vendor side sells the dream of “AI bots that print money” on prediction markets. The data side tells a different story. Six strategies actually work. Three look profitable but aren’t anymore. The retail edge is narrow, the legal exposure is rising, and the OpenClaw $115K-week story is real but not replicable.

Three buckets. One winner.

The on-chain analysis of 95 million transactions resolves into three populations. The mathematical baseline for any retail trader entering Polymarket.

As an affiliate, we earn on qualifying purchases.

Six categories. Different bets.

The 0.51% profitable cohort uses six identifiable strategies. Each requires a different combination of capital, infrastructure, expertise, or luck. Most retail traders cannot assemble what their chosen strategy requires.

Polymarket Profits 2 – Build 7 Trading Bots This Weekend: Arbitrage, Resolution Scanning, Copy Trading, and Claude AI Agents. The $178K Wallet Playbook. (Polymarket Profits Trading Bot Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Kalshi up. Polymarket flat.

The competitive structure has inverted from late 2024 when Polymarket held ~95% of category volume. Kalshi’s bet on CFTC regulation paid off when the agency formally classified prediction markets as derivatives in March 2026.

- Valuation$22B · Coatue raise March 2026

- Annualized volume$178B · revenue $1.5B

- Sports concentration87% of TTM volume

- FundingFiat-native · USD in/out

- State challengesNV, MA, AZ, TN, IL, CT

arbitrage

opportunity

- Valuation$15B · fundraising May 2026

- US re-entryVia QCEX (CFTC-regulated)

- Funding (intl)USDC-native on Polygon

- Active traders Apr~643K (down from 733K Mar)

- Maker feesZero · only takers pay

Use Claude to Build an AI Trading Bot: 90 Days with Stocks and Prediction Markets (AI Trading Bot Series Book 1)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five conditions. Each side.

The “polymarket trading bot profitable” search query has a specific answer. The honest one is conditional, not categorical.

- Genuine domain expertise — bot automates execution of a thesis with independent merit (NFL, Fed policy, crypto reg)

- Cross-platform arbitrage with adequate working capital ($5-50K) and tolerance for settlement delay

- Treating the bot as research — downside bounded by money you can afford to lose; learning is the value

- Built-in compliance awareness — Rule 180.1 exposure, state-by-state availability tracking

- Detailed logging from day 1 — evaluate honestly after 6 months before scaling up

- Off-the-shelf “arbitrage finder” tools — opportunity captured by sub-100ms bots before your tool finishes scan

- Following social-media bot tutorials promising $1-10K weekly profits — CFTC issued explicit fraud advisory in 2026

- Public LLMs (ChatGPT, Claude) driving trades on volatile markets without independent risk management

- Under-capitalized for chosen strategy — fees and slippage absorb most edge below $5K working capital

- Expecting “passive income” — vendor marketing pattern that does not match the empirical 0.51% baseline

The retail trader’s best-expected-value play in 2026 prediction markets is small-position domain-specialization rather than full bot automation. The capital required is lower, the edge is more durable, and the failure modes are more contained. For everyone else, the math is unforgiving.

The No-BS Guide to Prediction Market Arbitrage: AI-Powered Strategies for Polymarket & Kalshi — Find Arbitrage, Manage Risk & Profit from Real-World Events Without Code (The No-BS AI Playbooks)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The market backdrop · what 2026 actually looks like

Before the bot question, the market context. Polymarket and Kalshi together crossed $150 billion in combined lifetime trading volume in April 2026. The growth has cooled — seven-month streak of record monthly volume just ended — but absolute scale is now substantial. Year-to-date through April 20, 2026, Kalshi did $37.49 billion in notional volume vs Polymarket’s $29.23 billion. Kalshi raised $1 billion at a $22 billion valuation in March 2026 (Coatue led). Polymarket is fundraising at $15 billion. The competitive structure has inverted from late 2024, when Polymarket held roughly 95 percent of category volume against a tiny Kalshi. The flip happened because Kalshi spent two years building the federally compliant pathway through CFTC regulation, which paid off when the CFTC formally classified prediction markets as derivatives in March 2026.

Polymarket returned to U.S. users on December 2, 2025, after a three-year hiatus, via its acquisition of QCEX (a CFTC-regulated exchange). U.S. users now access Polymarket through a fiat-funded path that abstracts away the underlying USDC settlement on Polygon. International users continue through the wallet-native crypto path. Both platforms face state-level legal pressure — Massachusetts, Nevada, Arizona, Tennessee, Illinois, Connecticut have all challenged either Kalshi or Polymarket on gambling grounds, with both platforms invoking federal CFTC preemption.

Sports event contracts are now the dominant volume category. Approximately 87 percent of Kalshi’s trailing-twelve-month volume is in sports. That has implications for bot strategy. Sports markets are deep, liquid, and structurally tractable for systematic trading. Political markets are thinner, more event-driven, and more vulnerable to insider information. Cultural and economic markets sit in between. Bot strategy varies materially by category.

The other piece of context that shapes 2026 bot economics: the CFTC’s February 2026 advisory on insider trading, which followed two enforcement cases (a political candidate trading his own candidacy contracts, an employee of a YouTube-affiliated firm trading event contracts on the channel’s videos). The advisory established that Rule 180.1 covers material nonpublic information arbitrage in event contracts. The most lucrative information edges — knowing about events before public disclosure — are now legally exposed in a way they weren’t 12 months ago. The legal environment for information-arbitrage bots tightened materially in early 2026.

The strategy that died · simple cross-side arbitrage

The simplest arbitrage strategy is the one every YouTube guide leads with. A Polymarket binary contract has a YES side and a NO side. The combined price of YES + NO must equal $1.00 at resolution because exactly one side wins. If YES is trading at $0.48 and NO is trading at $0.49, you can buy both sides for $0.97 total and lock in $0.03 profit per contract pair regardless of outcome. The strategy worked routinely in 2024. It mostly doesn’t work in 2026.

The on-chain orderbook analysis from Q3 2025 to Q1 2026 quantifies why. Average arbitrage opportunity duration: 2.7 seconds, down from 12.3 seconds in 2024. Roughly 73 percent of arbitrage profits in 2026 are captured by sub-100-millisecond execution bots running on dedicated Polygon RPC nodes. A retail trader using a standard internet connection, a public RPC endpoint, and an off-the-shelf bot framework cannot compete against this infrastructure. The opportunity is gone before the retail bot even sees it on the orderbook.

The math underneath: Polymarket’s gas fees on Polygon are minimal (sub-cent per transaction), but execution speed depends on (a) RPC node latency, (b) gas-pricing strategy for inclusion in the next block, (c) MEV-aware ordering against competing transactions, (d) orderbook update frequency. Professional bot operators run dedicated Polygon validators or pay for premium RPC access (Alchemy, QuickNode, Infura with priority tiers) and use private mempools to avoid frontrunning. The infrastructure cost runs $1,000-5,000 per month for serious operations. Retail traders running Replit-hosted bots on free RPC endpoints are not in the same race.

This is the most important fact about Polymarket bots in 2026. The strategy that the popular guides describe — find mispricings, click both sides, collect spread — is structurally dead for retail. The opportunity exists, but it’s been arbitraged into a microsecond-level competition between specialized firms.

The strategies that still work · six categories, six different bets

The on-chain analysis identifies six strategy categories that produce most of the upside in the profitable 0.51%. Each one requires a different combination of capital, infrastructure, expertise, and luck.

1. Information arbitrage. This is the strategy where AI agents currently produce the most retail success — and also where the legal exposure is highest. The mechanism: news breaks, a Polymarket contract’s “true” probability shifts, but the orderbook hasn’t fully updated yet. A bot reading a news source faster than humans can update its position before the market reprices. The example circulating in 2026: on January 14, when news broke that a witness in a Trump legal case had recanted testimony, a contract trading at 54 percent had its true probability shift to roughly 68-71 percent within 90 seconds. Bots running ensemble LLM analysis (one model assigns 68 percent probability, another assigns 71 percent, a fine-tuned model on historical Polymarket data assigns 65 percent) executed against the 54 percent orderbook before human traders finished reading the article.

The math works when (a) the news is genuinely market-moving, (b) the bot processes it faster than the average human trader, (c) the orderbook depth allows meaningful position sizing before reprice. The hard parts: filtering signal from noise (most news doesn’t move markets), avoiding adversarial fake news, managing position size against orderbook depth, and avoiding the legal exposure if the information edge is material nonpublic information rather than faster public-information processing. Retail bots using public LLMs and public news feeds operate in a crowded competitive layer. The professional firms running this strategy use proprietary news feeds (Bloomberg Terminal, Refinitiv Eikon at $24,000/year per seat), private LLM deployments, and dedicated execution infrastructure. The retail edge is narrow.

2. Cross-platform arbitrage between Kalshi and Polymarket. This is the structurally durable opportunity. Same underlying event — say, “Federal Reserve cuts rates by 25bp at June meeting” — listed on both Kalshi and Polymarket with prices set independently by each platform’s order flow. When Kalshi YES trades at 45¢ and Polymarket NO trades at 52¢, the combined cost is 97¢ for a guaranteed $1.00 payout. Three cents of profit per contract pair, regardless of outcome.

The mechanism works because the two platforms have non-overlapping user bases, different funding mechanisms (Kalshi is fiat-native, Polymarket is USDC-native for non-US users), and different market-maker compositions. Persistent pricing gaps emerge from these structural differences. The cross-platform arbitrage opportunity is still tractable for retail bots in 2026 — it’s slower-moving than within-platform arbitrage, the mispricings persist for minutes rather than seconds, and the capital requirement is moderate (a few thousand dollars working capital).

The hard parts: regulatory exposure (sports contracts in some states are restricted on one platform but not the other, creating legal uncertainty), funding flow (moving USDC between Polymarket international and dollars to Kalshi creates settlement delay), platform reliability (an exchange outage during an arbitrage position is a forced loss), and capital efficiency (the spread is small, so position sizing matters). Realistic returns: 5-15 percent annualized on deployed capital for a well-run cross-platform arbitrage operation. Not lottery-ticket profit, but durable.

3. Liquidity provision / market making. Provide both bid and ask quotes on a market, capture the spread, manage inventory risk. This is the strategy that traditional financial market makers use, adapted to event contracts. In 2026, market making on Polymarket can be sustainable if you have the capital and the risk-management infrastructure. The basic economics: place bid orders below market, ask orders above market, capture the spread when both fill. The risk: directional events that move the market sharply against your inventory, leaving you holding positions at adverse prices.

Polymarket charges no fees to liquidity makers (only to takers via market orders), which structurally favors the strategy. Realistic returns: 8-20 percent annualized on deployed capital for sophisticated operations. The dominant operators in this category are professional firms with dedicated risk-management systems and capital pools in the $1-10 million range. Retail bots can participate at the margin but capture proportionally less of the available spread because they lack the inventory-risk capacity to quote on volatile markets.

4. High-probability bond strategies. Buy YES on contracts trading at 95-99 cents on near-certain outcomes, hold to resolution, collect 1-5 cents per dollar deployed. The strategy is mathematically equivalent to selling deep out-of-the-money insurance — you’re betting that the high-probability outcome resolves as expected. The annualized returns are modest (5-12 percent typically) but the volatility is low. The risk: the rare cases where the “near-certain” outcome doesn’t resolve as expected, which produces large losses on positions that were sized for low volatility.

This strategy works particularly well on Kalshi for political and economic markets where institutional traders create a baseline floor of liquidity. The capital requirement is meaningful — to generate $50K annual profit at 8% return, you need approximately $625K deployed. Retail-scale operations producing $1-5K annual profit are common but limited by capital.

5. Domain specialization. A trader with deep expertise in a specific domain (NFL injury reports, Federal Reserve monetary policy, crypto regulatory developments) can systematically beat the market in that domain. The advantage isn’t speed — it’s knowing what factors matter that the broader market underweights. A dedicated NFL bettor knows that Patriots starting quarterback ankle injury reports get systematically underpriced relative to historical injury severity patterns. A Fed-policy specialist knows that FOMC participant speeches in the two weeks before a meeting have predictive content the broader market ignores. The strategy requires hours per week of focused domain attention but produces returns that don’t decay as the broader market becomes more efficient.

Realistic returns: 15-30 percent annualized for genuinely expert traders, lower for traders who think they’re experts. Bots augment but don’t substitute for the underlying expertise. The retail trader who runs a domain-specialization strategy is the most likely retail trader to be in the profitable 0.51 percent.

6. Speed trading / latency arbitrage. Sub-100ms execution against orderbook updates as new information arrives. This is the strategy that captured 73 percent of arbitrage profits in 2026. It is unambiguously not a retail strategy. Successful speed-trading operations have dedicated co-location infrastructure, custom RPC nodes, FPGA-based order matching, and engineering teams specifically optimizing the speed advantage. The capital requirement is meaningful (low six-figures for infrastructure alone), the engineering requirement is substantial, and the competitive pressure is fierce. Retail traders should not attempt this category.

The retail bot question · should you run one?

The honest answer for retail traders considering running an off-the-shelf Polymarket bot in 2026: probably not, unless you fit specific conditions.

The conditions where retail Polymarket bots are reasonable bets:

- You have genuine domain expertise in a specific market category (sports, politics, finance, crypto) and the bot is automating execution of decisions you would otherwise make manually. The bot adds speed and discipline to a thesis that has independent merit.

- You’re running cross-platform arbitrage between Kalshi and Polymarket with adequate working capital and tolerance for settlement delay. The strategy is durable and the technical complexity is moderate.

- You’re treating the bot as research / hobby rather than expecting profits. Polymarket bot operation is genuinely educational — you learn about prediction markets, about adversarial AI dynamics, about market microstructure. As long as your downside is bounded by money you can afford to lose, the learning has value.

The conditions where retail Polymarket bots are bad bets:

- You expect to profit from off-the-shelf “arbitrage finder” tools. The arbitrage was captured by sub-100ms bots before your tool finished its scan.

- You’re following social-media bot tutorials promising $1K-10K weekly profits. The CFTC issued an explicit advisory in 2026 warning about AI trading algorithm fraud — fraudsters “exploiting public interest in artificial intelligence to tout automated trading algorithms” promising “unreasonably high or guaranteed” returns. The marketing claims do not match the empirical data.

- You’re using public LLMs (ChatGPT, Claude) to drive trading decisions on volatile markets without independent risk management. LLMs produce outputs that look confident but routinely fail on the kinds of edge cases markets punish. The bot may execute consistently; the underlying decisions may be poor.

- You’re under-capitalized for the strategy you’re running. Most profitable strategies require working capital in the $5K-50K range or higher to generate meaningful absolute profit. Below that threshold, transaction fees and slippage absorb most of the edge.

The empirical answer from the 95-million-transaction analysis: for every 200 retail wallets attempting to profit on Polymarket, approximately one achieves profit exceeding $1,000. That 1-in-200 rate is the realistic baseline. Bot operation does not materially change that ratio for most retail traders. It changes the rate of trading, the consistency of execution, and the precision of position sizing — but the underlying edge has to come from somewhere, and for most retail bots, it doesn’t.

The OpenClaw moment · what one $115K week actually meant

The headline-generating event of early 2026 was a Polymarket trader using OpenClaw — the open-source AI agent framework originally built by Peter Steinberger, later acqui-hired by OpenAI — to generate $115,000 in a single week of trading. The story circulated through prediction-market Twitter, AI-trading subreddits, and bot-marketplace blog posts as evidence that AI-augmented retail trading is now structurally profitable.

The honest read on the OpenClaw $115K week:

It happened. The numbers are documented. The trader wasn’t fabricated. The strategy involved ensemble-LLM analysis of news events, automated probability assignment, and execution against Polymarket’s orderbook in volatile political markets during a particularly news-rich week.

It is not replicable for most users. The trader had domain expertise in political markets, custom tooling on top of OpenClaw, dedicated execution infrastructure, and benefited from a specific market environment (high news flow, multiple cascading events, orderbook conditions that allowed meaningful position sizing). Subsequent weeks for the same trader produced materially smaller profits and some loss-weeks. The headline number is a peak, not a baseline.

It triggered the CFTC advisory. The same advisory that warned about AI trading algorithm fraud cited the marketing patterns that emerged after the OpenClaw week — bot vendors using the $115K screenshot to sell automation tools at $99-499/month subscription prices, with marketing claims that systematically overstated typical returns.

It’s evidence for, not against, the structural argument. Profitable AI-augmented retail trading on Polymarket exists. It is concentrated in skilled operators who combine domain expertise, custom infrastructure, and disciplined risk management. It’s not democratized. The off-the-shelf bot purchased from a Twitter advertisement is not the same product as OpenClaw running custom strategies under a domain-expert operator’s supervision.

The structural read: AI agents in adversarial markets follow the same pattern as AI agents in adjacent domains. Capability exists. Capability is heterogeneously distributed. Top-decile operators capture disproportionate share of the upside. Median operators lose money slowly. The 0.51% profit rate is not going to materially change because retail bots got better — it might shift to 0.7% or 1.2% over 2026-2028, but the long-tail distribution will hold.

The regulatory overhang · what changes through 2026-2027

Three regulatory dynamics shape the 2026-2027 trajectory for prediction-market bot operations.

The CFTC’s March 2026 derivatives classification. Prediction markets are now formally classified as derivatives under CFTC jurisdiction. This is positive for the category overall (it removes the gambling-vs-derivative legal ambiguity, clears a path for institutional participation, validates the platforms’ federally-compliant business model) but creates new compliance overhead for bot operators. Specifically: the CFTC’s surveillance and audit-trail requirements now apply to platforms, which means bot operators are creating logged, attributable trade histories that regulators can subpoena if questions arise about manipulation, insider trading, or market integrity.

State-level pushback. Massachusetts, Nevada, Arizona, Tennessee, Illinois, Connecticut, and others continue challenging both Kalshi and Polymarket on gambling grounds. The federal preemption argument is plausible but unresolved. Sports markets in particular are vulnerable to state-level prohibitions. A bot operator running cross-platform arbitrage on sports events has state-by-state availability risk that wasn’t present 12 months ago. Practical impact: position-by-position checking of state availability before execution, additional latency, occasional forced position closures when access is suspended.

The insider-trading enforcement framework. The February 2026 CFTC advisory established that Rule 180.1 applies to material nonpublic information arbitrage in event contracts. Two enforcement cases have already happened (a political candidate trading his own candidacy, a YouTube-affiliated employee trading channel-related contracts). The legal exposure for information-arbitrage bots is real and increasing. Bot operators sourcing information from non-public channels (insider sources, leaked drafts, scraped private databases) face material legal risk.

The regulatory trajectory through 2026-2027: more compliance overhead, more state-level fragmentation, more enforcement actions on edge-case strategies. Net impact on retail bot profitability: modestly negative. Net impact on professional firm profitability: marginal — they had compliance infrastructure already.

The deeper read · what AI in adversarial markets actually looks like

The question “are Polymarket trading bots profitable” is interesting beyond the immediate practical answer because prediction markets are the cleanest available test case for AI agents in adversarial markets. Public data, transparent orderbooks, deterministic resolution, permissive regulatory environment. If AI agents are going to systematically beat human traders in financial markets, prediction markets are where the evidence should appear first.

The 95-million-transaction analysis gives a reasonably clean answer to that question. AI agents do beat human traders. The beat is concentrated in specific strategies, captured by specific operators, and does not democratize to retail. The structure looks like the structure of every other AI-augmented productivity dimension: capability exists, capability is heterogeneously distributed, professional operators with capital and infrastructure capture most of the upside, retail operators capture little.

That has implications beyond prediction markets:

- Sports betting. Fantasy sports, daily fantasy, prop bets, live in-game wagering. The same dynamics apply. Sharp bettors using AI-augmented analysis already beat books. The retail edge is narrow.

- Crypto perpetual futures. Hyperliquid, GMX, Drift, dYdX. Volatile markets with public data and 24/7 trading. AI-augmented strategies are now standard for top operators. The retail strategy of “buy and hold” continues to work approximately as well as it always did, which is to say not very well in general but occasionally spectacular.

- Equity options. Robinhood retail, Webull, e*Trade. Less transparent than prediction markets but increasingly accessible to AI-augmented retail strategies. The structural pattern matches: top operators capture most of the edge, retail bots running off-the-shelf strategies lose money.

- Prediction markets on private events. Sports outcomes are public. Election outcomes are public. Insurance claims, corporate decisions, regulatory rulings, M&A announcements — all involve material nonpublic information. The legal exposure for bots trading on private-event contracts is material. This is the next frontier where regulatory clarity will matter most.

The honest answer to “is AI going to make retail traders rich in 2026-2030” remains: probably not, because the profit pool gets captured by professional operators with the infrastructure and capital to compete at the margin. The pattern is the same as every prior wave of trading-technology democratization (online trading in the 1990s, algorithmic trading in the 2000s, retail options in the 2010s). Each wave produced winners. The winners were not, in general, the median retail participant.

The honest verdict

For the retail trader who searched “polymarket trading bot profitable” looking for a yes-or-no answer:

The answer is “probably not for you, specifically, unless you fit narrow conditions.”

The realistic conditions: (1) genuine domain expertise in a specific market category, (2) adequate capital ($5K-50K minimum for meaningful absolute profit), (3) tolerance for slow returns (5-20% annualized for the most durable strategies), (4) discipline to operate the bot as augmented decision-making rather than fully autonomous black-box trading, (5) compliance awareness about regulatory and legal exposure.

The unrealistic conditions that bot vendors market: (1) “passive income” while you sleep, (2) consistent four-figure weekly profits, (3) “AI does the analysis for you” with public LLMs and public news feeds, (4) 100x returns on small starting capital, (5) zero-effort arbitrage from off-the-shelf tools.

The mathematical baseline is the 0.51 percent statistic from the on-chain analysis. Most retail Polymarket traders, whether running bots or not, lose money over time. Bot operation does not change that ratio meaningfully for most operators. The exception cases are real but specific.

The deeper structural insight: prediction markets are the cleanest available example of AI agents in adversarial financial markets. The pattern that emerges in this market — heterogeneous capability, professional concentration of profits, retail underperformance — is the pattern that will emerge in adjacent markets as AI agents proliferate. The question for the next several years is not whether AI-augmented trading works (it does) but who captures the profit pool (concentrated operators, not democratized retail). The retail trader’s best-expected-value play in 2026 prediction markets is probably small-position domain-specialization rather than full bot automation. The capital required is lower, the edge is more durable, and the failure modes are more contained.

For the trader who insists on running a bot anyway: start with cross-platform arbitrage (Kalshi vs Polymarket), keep capital under 5 percent of net worth, instrument the bot with detailed logging from day one, treat the first six months as paid education, and re-evaluate honestly after a measurable trading period whether the strategy is producing returns that justify the time investment. Most won’t be. A small fraction will be. The fraction is small because the markets are competitive and getting more competitive every quarter.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Reading

- Post-Labor Economics — the broader framework on how AI changes economic infrastructure

- The State of AI Replacing Jobs in 2026 — labor displacement reality check

- The Twelve Real Complaints About AI Tools — the user-side reality check companion piece

Sources

- On-chain analysis · 95 million Polymarket transactions · April 2024 – December 2025 · 0.51% of wallets profit > $1,000

- Polymarket orderbook analysis Q3 2025 – Q1 2026 · Average arbitrage opportunity duration: 2.7 seconds (down from 12.3 seconds in 2024) · 73% of arbitrage profits captured by sub-100ms execution bots

- Kalshi · April 2026 raise · $1 billion led by Coatue at $22 billion valuation · Annualized trading volume $178 billion · Annualized revenue $1.5 billion

- Polymarket · April 2026 fundraise at $15 billion valuation · YTD volume $29.23B vs Kalshi $37.49B

- Combined Polymarket + Kalshi lifetime volume crossed $150 billion in April 2026

- Kalshi market share ~89% in U.S., ~65% globally (April 2026, up from <5% in late 2024)

- Sports event contracts ~87% of Kalshi’s TTM volume (~$39.7B per Congressional Research Service Feb 2026)

- CFTC · March 2026 · Formal classification of prediction markets as derivatives

- CFTC · February 2026 advisory on insider trading in prediction markets · Rule 180.1

- CFTC · 2026 advisory warning about AI trading algorithm fraud

- Polymarket return to U.S. users · December 2, 2025 · via QCEX (CFTC-regulated) acquisition

- Polymarket · January 2026 · $400,000 profit on Maduro-ouster contract (insider trading concerns)

- OpenClaw · open-source AI agent framework · Peter Steinberger / OpenAI acqui-hire context

- Quicknode · Top 10 Polymarket Trading Bots overview (PolyCop, OpenClaw, CLOB API)

- State-level legal challenges: Massachusetts injunction (Jan 2026), Nevada complaint (Jan 2026), Arizona, Tennessee, Illinois, Connecticut additional pressure

- Andreessen Horowitz · 18-page letter defending prediction markets against state-level bans

- Khamenei death contract refund · Kalshi · February 2026 · federal regulations bar wagers on death