By Thorsten Meyer — May 2026

Anthropic is going public.

The $50 billion private round currently closing — at a valuation between $850 billion and $900 billion — is the last private round. The board decision happens this month. The IPO window opens in October. Goldman Sachs, JPMorgan, and Morgan Stanley are already in the room. The annualized revenue run rate that justifies the math is somewhere between $30 billion (publicly disclosed) and $40 billion (the number sources are giving the financial press). Enterprise customers are 80% of that revenue, with more than 1,000 spending over $1 million annually.

October 2026.

What an Anthropic IPO actually unlocks.

Anthropic is going public. The $50 billion private round currently closing — at $850–900B — is the last private round. Board decision this month. IPO window opens October. Goldman, JPMorgan, Morgan Stanley already in the room. The financial press has read this as a fundraising milestone. It is much more than that.

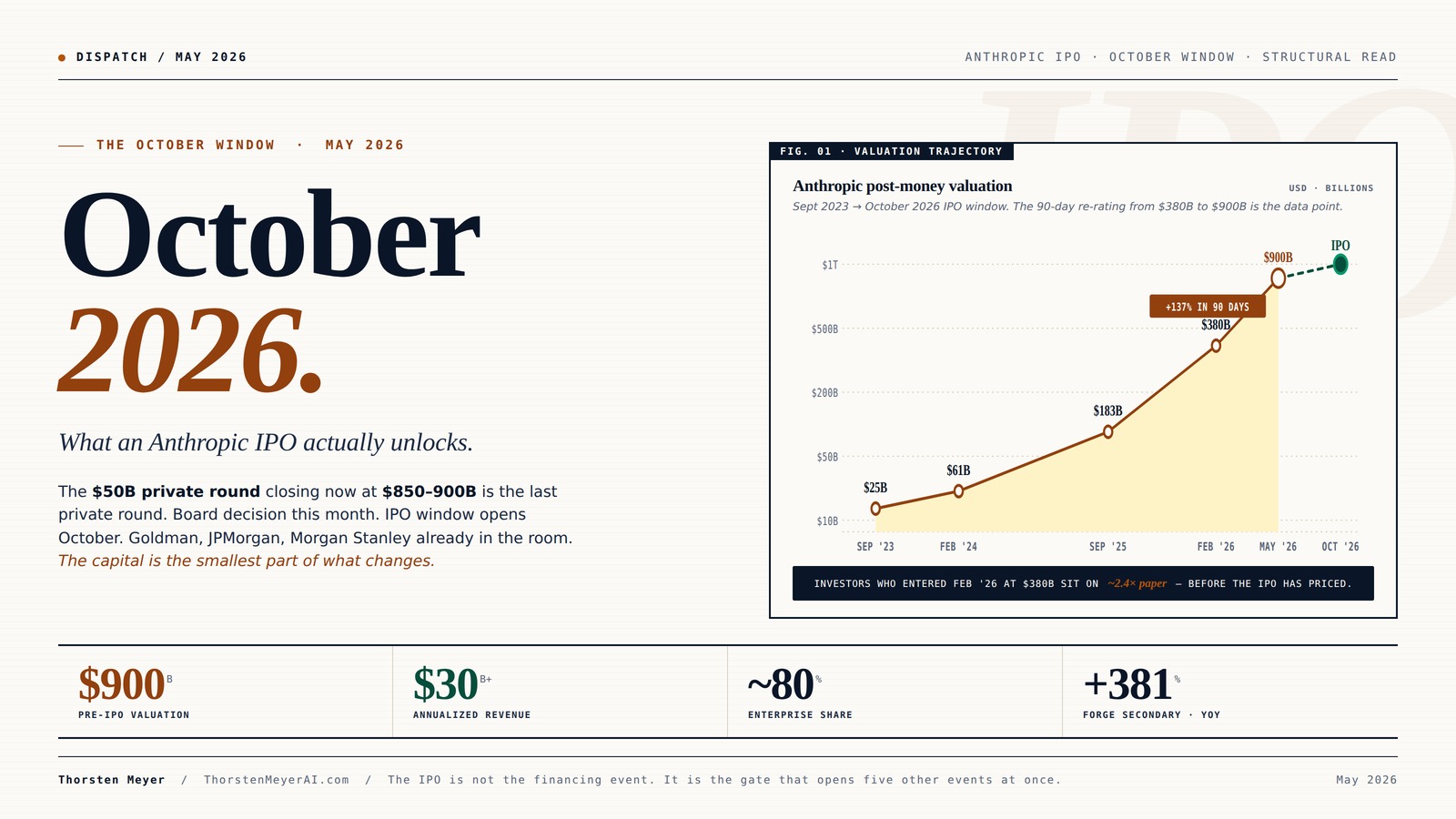

The valuation more than doubled in 90 days.

Most pre-IPO companies follow a recognizable pattern: long private growth, mezzanine round at modestly higher valuation, public listing at a slight discount. Anthropic is not following that pattern. The Feb $380B → May $900B move is closer to a public-company quarterly rerating event — except the company isn’t public yet.

Enterprise AI Solutions Architecture: The Practitioner’s Handbook for Designing, Delivering, and Scaling Production AI Systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

A public listing is a calendar problem before it is a financial problem.

Three things have to align: clean three-year audited financials, underwriter bandwidth, and macro environment. October is where they converge. November and December create year-end calendar risk. January 2027 creates Q1-earnings timing risk. The window is now or it slips a year.

Financial cleanup just finished.

Three years of audited financials, restated under public-company GAAP, only became S-1-capable earlier this year. Q3 close in late September gives a clean three-year audited base for an October filing.

Macro window is favorable.

Equity markets in productive AI-narrative phase. Fed rates stable through Q4. The first wave of enterprise customers reporting AI-productivity disappointment lands in Q1 2027 — could compress AI multiples by then. October is the last clean window before that.

Competitive pressure is acute.

OpenAI structurally further from IPO — corporate restructuring recent, capex-heavier, CFO publicly said an IPO is “not in the cards.” First-mover access to public capital, comp packages, and acquisition currency is worth 12 months of strategic edge.

The AI Stock Investor: A Beginner’s Guide to Profiting from the AI Revolution (Stock Investing 101)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The capital is the smallest part of what changes.

Most public conversation has framed the IPO as a financing event. The capital is the smallest part of the story. Five things change the moment the company is public — and most of them have not been priced into expectations yet.

Acquisition currency.

Public stock is liquid by definition. A $5B acquisition of a vertical AI company — healthcare, legal, agent platforms — becomes possible via stock issuance. Private companies can use their stock only for tiny tuck-ins. The acquisition pace will accelerate sharply.

Employee liquidity.

Existing comp packages with private RSUs become 30–40% more valuable to the employee overnight. The recruiting advantage Anthropic did not have during the private period now exists. The FDE compensation thesis becomes structurally easier to defend at public-company multiples.

Secondary-market unfreeze.

~5,000 current and former employees hold equity. After the lock-up, systematic secondary sales create a 6-month-out compounding capital flow into SF real estate, angel checks, and Series A rounds for technical founders departing to start the next AI cohort. October 2026 → April 2027 is the window.

Chip and infrastructure round.

The Fractile conversation, multi-year compute commitments, and Project Rainier-class capacity buildout all run on a different timescale post-IPO. Mythos-class frontier capabilities can be funded against public-market expectations rather than private-round timing.

Sovereign & institutional access.

Sovereign wealth funds (PIF, ADIA, GIC, NBIM, Mubadala) cannot easily participate in $900B private rounds. They can take public-market positions at scale on day one. The only buyer class with the capital depth to absorb the float without distortion. The IPO becomes a geopolitical event, not just a financial one.

Enterprise Artificial Intelligence Transformation

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The IPO doesn’t just price Anthropic. It re-prices everything around it.

The whole talent and capital ladder shifts up by one rung.

OpenAI’s IPO timeline compresses. Smaller-lab valuations re-anchor. Secondary-market liquidity unfreezes across the sector. The acqui-hire window opens for vertical AI. Comp wars intensify. Each effect compounds the next.

AI for Small Business: From Marketing and Sales to HR and Operations, How to Employ the Power of Artificial Intelligence for Small Business Success (AI Advantage)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three disclosures land in Q1 2027.

The IPO will succeed. The bigger question is what happens 90 days after. The first earnings as a public company is late Jan / early Feb 2027 — the first time Anthropic discloses revenue concentration, gross margins, R&D as % of revenue, and most importantly, capex. The IPO premium implicitly assumes flawless execution through a quarter that has not yet happened.

The compute capex line.

Compute spend is large. Public companies must disclose it. The market currently models with rough assumptions. If the disclosed capex-to-revenue ratio is high, the multiple compresses immediately.

Revenue concentration.

1,000+ customers spending $1M+ is impressive. Top-10 concentration is the more impressive — or less so — number. Public reporting requires it. If top 10 are >40% of revenue, every one becomes a single point of failure.

Productivity compression timing.

Most enterprise customers have not yet seen the AI productivity gains they projected. The first wave of measurable disappointment lands in the same quarter as Anthropic’s first public earnings. Renewals slow. Expansion stalls. The thesis tested at exactly the wrong moment.

The IPO is not the financing event. It is the gate that opens five other events at once.

Four assignments. By role.

The acquisition window opens after October. Six-month window.

If you are mid-Series A or B in vertical AI, be ready to take a strategic conversation. The number you used to refuse may be the number you are offered.

Talk to a financial advisor before the lock-up date.

The IPO is the single most consequential financial event in your career. The IPO makes most of you wealthier overnight; the post-lock-up period is where wealth either consolidates or evaporates. Diversification timing is not theoretical.

The pre-IPO discount window is closing.

Pre-IPO positions still available on Forge and the secondary markets. After May, the discount narrows. After October, the public price rules. The window for entry-via-secondary at meaningful discount is closing.

You need a 6-month retention and acquisition response plan.

The strategic consequence is not Anthropic’s valuation. It is the comp pressure, the acquisition pressure, and the talent flow it creates. If you do not have a plan, you are about to be on the wrong side of the trade for two quarters.

The financial press has read this story as a fundraising milestone. It is much more than that. The Anthropic IPO is a structural event for the entire AI cycle, and most of the second-order effects have not been priced — by buyers, by competitors, by employees, or by the secondary markets that have to absorb the liquidity event.

This is the dispatch about what changes the moment the bell rings.

Executive Summary

| Element | Detail |

|---|---|

| Pre-IPO round size | $40B–$50B |

| Pre-IPO valuation | $850B–$900B |

| Board decision | May 2026 |

| IPO target window | October 2026 |

| Underwriters in discussion | Goldman Sachs, JPMorgan, Morgan Stanley |

| Public-market raise estimate | ~$60B |

| Annualized revenue run rate | $30B+ disclosed, ~$40B per sources |

| Enterprise share of revenue | ~80% |

| $1M+ enterprise customers | 1,000+ |

| Last comparable private round | $380B, Feb 2026 |

| OpenAI post-money valuation (March 2026) | $852B |

| Forge secondary price | $259.14 (May 4) — +381% YoY |

| Time from $380B → $900B | ~3 months |

The valuation more than doubled in 90 days. Anthropic’s revenue grew from a $9B run rate at end of 2025 to $30B+ by April 2026. No company in American technology history has scaled at this rate. The IPO that follows will reset the pricing of everything around it.

1. The Numbers Are Doing Something Unusual

Most pre-IPO companies follow a recognizable pattern: a long private growth period, a final mezzanine round at modestly higher valuation than the prior, then a public listing at a multiple compressed slightly from the private mark. Investors who entered late in private rounds typically take small mark-to-market gains; the IPO mostly liquidates earlier holders.

Anthropic is not following that pattern.

The company raised $30 billion in February 2026 at a $380 billion valuation. Three months later, it is closing a $50 billion round at $850–$900 billion. The valuation has more than doubled in ninety days. The revenue run rate has tripled in the same window. Enterprise revenue is 80% of the total and growing. The Forge secondary-market price is up 381% over twelve months. Investors who got into the February round at $380B are now sitting on a paper return of roughly 2.4x in three months, before the IPO has even priced.

This is not a normal pre-IPO trajectory. It is closer to a public company having a single-quarter rerating event, except the company isn’t public yet.

The implication for the IPO itself is that the public listing is not going to be a “modest discount to private” event. The demand structure suggests it will be a “public market catches up to private” event. The institutional investor who tried to commit $5 billion to the May round and could not get a meeting with the CFO is the same institutional investor who will be on the IPO call queue. The pent-up allocation pressure will set the opening tape, not the underwriters’ fundamental model.

2. Why October Is the Window, Not Earlier and Not Later

A public listing is a calendar problem before it is a financial problem. The window has to align with three things: the company’s audited financials being public-company-clean, the underwriters’ bandwidth, and the macro environment.

Three reasons October is the answer.

Reason 1 · The financial cleanup just finished. Companies typically need three years of audited financials, restated under public-company GAAP, before filing an S-1. Anthropic’s revenue arc only became public-IPO-capable when the FY24 and FY25 restatements completed earlier this year. The Q3 close in late September gives the company a clean three-year audited base for an October filing.

Reason 2 · The macro window is favorable. Equity markets are in a productive AI-narrative phase. The Federal Reserve has signaled stable rates through Q4. The earnings calendar in October-November will include the first wave of enterprise customers reporting AI-driven productivity numbers — most of which, per the productivity-bubble analysis, will land below executive projections. That gap could compress AI-stock multiples by Q1 2027. October is the last clean window before that compression hits the IPO calendar.

Reason 3 · The competitive pressure is acute. OpenAI is structurally further from an IPO — the corporate restructuring is recent, the financial profile is more capex-heavy, and the CFO publicly said an IPO is “not in the cards right now” in late October 2025. If Anthropic lists in October 2026 and OpenAI follows in 2027 or later, Anthropic gets first-mover access to public-market capital, public-market employee comp packages, and public-market acquisition currency. The list of strategic moves that become possible after a successful IPO is the list of strategic moves OpenAI cannot match for at least twelve months.

The compression of these three factors — clean financials, favorable macro, competitive timing — into a single quarter is rare. October 2026 is the window. November and December create year-end calendar risk. January 2027 creates Q1-earnings timing risk. The window is now, or it slips a year.

3. What the IPO Unlocks That a Private Round Does Not

Most of the public conversation has framed the IPO as a financing event — Anthropic raising capital. The capital is the smallest part of the story. Five things change the moment the company is public.

Unlock 1 · Acquisition currency. Public stock is a usable acquisition currency. Anthropic could acquire a $5 billion AI-native vertical company — a healthcare AI specialist, a legal-tech firm, a vertical agent platform — by issuing stock. Private companies can use private stock as currency only for tiny tuck-in acquisitions because target shareholders have no liquidity. Public stock is liquid by definition. The acquisition pace will accelerate sharply.

Unlock 2 · Employee compensation reform. Anthropic’s internal compensation packages have heavy private-RSU components — valuable on paper at $900B but illiquid until either an IPO or a tender offer. Engineers debating whether to take a comparable offer at a public AI competitor have, until now, been making a discount-rate judgment about Anthropic’s RSU vs. the competitor’s liquid stock. After the IPO, that discount disappears. Anthropic’s existing comp packages become 30–40% more valuable to the employee overnight, and the company gains a recruiting advantage it did not have during the private period. The forward-deployed engineer compensation analysis discussed last week becomes structurally easier to defend at public-company multiples.

Unlock 3 · Secondary-market unfreeze. Roughly 5,000 current and former Anthropic employees hold equity. Most of it has been illiquid since the company’s founding. The IPO unlocks systematic secondary sales after the lock-up. Lock-up expiration creates a six-month-out compounding capital flow into San Francisco real estate, into early-stage AI startup angel checks, and into the Series A market for technical founders departing Anthropic to start their own companies. The talent flow that follows IPO lock-up expirations is one of the most important leading indicators of where the next AI cohort will form. October 2026 → April 2027 is the window when this becomes visible.

Unlock 4 · The chip and infrastructure round. Anthropic has been in talks with Fractile (UK SRAM-based inference startup) about a fourth silicon supplier. That conversation is bounded today by Anthropic’s balance-sheet capacity and its private-market funding rhythm. Post-IPO, with public capital available and a credible currency, Anthropic can fund infrastructure relationships on a different timescale — including taking strategic stakes in chip startups, signing multi-year compute commitments at scale, and accelerating the Project Rainier-class capacity buildout. The competitive implication is that the Mythos-class cybersecurity model and any successor frontier capabilities can now be funded against public-market expectations rather than private-round timing.

Unlock 5 · Sovereign and institutional access. Sovereign wealth funds (Saudi PIF, ADIA, GIC, Norway’s NBIM, Mubadala) cannot easily participate in late-stage private rounds at $900B because of allocation rules and disclosure requirements. They can, however, take public-market positions at scale on day one. This is the only buyer class with the absolute capital depth to absorb the Anthropic float at IPO pricing without driving distortion. The fact that the institutional bid is sovereign-fund-sized is, structurally, the only thing that keeps the IPO math from immediately compressing the multiple. It also makes the IPO a geopolitical event, not just a financial one.

4. What the IPO Does to the Rest of the AI Market

Five second-order effects, in order of immediacy.

Effect 1 · OpenAI gets pressed into a faster IPO timeline. OpenAI’s CFO said an IPO is “not in the cards right now” in October 2025. After Anthropic’s October 2026 listing, OpenAI’s board will face investor pressure that did not exist before — particularly from secondary-market holders and 2023-vintage investors who need a liquidity path. Expect OpenAI’s IPO timeline to compress from “2027 or later” to “early 2027” within 60 days of Anthropic’s pricing.

Effect 2 · Smaller AI lab valuations re-anchor. Mistral, Cohere, Databricks’s AI division, and the open-weight cohort are currently priced against private-market AI multiples that took shape in 2024–2025. After Anthropic’s IPO sets a public reference, every smaller lab gets re-priced against that reference. Most will see their multiples compress, because Anthropic’s premium reflects scale advantages they cannot match. The mid-tier AI companies that raised at peak private-market multiples will face down rounds in 2027 unless they ship something genuinely differentiated.

Effect 3 · Secondary-market unfreeze across the sector. Anthropic’s IPO doesn’t just unfreeze its own employees’ equity. It creates the template — and the comparable — for OpenAI, Mistral, and the next wave. Funds that have been holding pre-IPO AI positions for liquidity will see exit paths open across the portfolio. The secondary-market AI position becomes systematically more liquid, which lowers the discount on private-market AI valuations by 200–400 basis points. The boring back-end implication is that more late-stage AI capital becomes available because the holding period is now bounded.

Effect 4 · The acqui-hire window opens for vertical AI companies. The 50–100 vertical AI companies founded in 2023–2024 that have not achieved enterprise scale on their own are now acquisition targets in a way they were not three months ago. Anthropic, with its new acquisition currency, will be the most aggressive buyer of vertical AI. Expect a wave of $200M–$1B vertical AI acquisitions in Q4 2026 and Q1 2027 — not because the targets are healthy, but because the buyer needs vertical reach into legal, healthcare, financial services, and government, and building it in-house is slower than buying it.

Effect 5 · Comp packages reprice across the entire AI sector. Anthropic SWE total compensation already runs $582K median, $920K at the top per Levels.fyi. After the IPO, that compensation has a public liquid currency component, which makes it harder to match for smaller AI competitors. Expect comp wars to intensify in Q4 2026, particularly for senior engineering, FDE, and product talent. The mid-tier AI companies that cannot match will lose senior staff to Anthropic and OpenAI; the smaller AI companies will lose them to the mid-tier. The whole talent ladder shifts up by one rung.

5. The Risk That Is Not Priced

The IPO will succeed. The bigger question is what happens 90 days after.

The first earnings report as a public company is scheduled for late January or early February 2027. That earnings report will be the first time Anthropic discloses, under public-company reporting standards: revenue concentration, customer churn, gross margin by product line, R&D spend as a percentage of revenue, and most importantly, capex outlays for compute infrastructure.

Three risks become visible at that report that are currently invisible.

Risk 1 · The compute capex line. Anthropic’s compute spend is large. Public companies have to disclose it. The market currently models Anthropic with rough assumptions about compute cost. The actual numbers — particularly the gap between revenue growth and compute spend growth — may not flatter the multiple. If the disclosed capex-to-revenue ratio is high, the multiple compresses immediately.

Risk 2 · Revenue concentration. 1,000+ customers spending $1M+ annually is impressive. The disclosure of how much revenue comes from the top 10 customers is more impressive — or less so, depending on the number. Anthropic has not disclosed customer concentration. Public-company reporting will require it. If the top 10 customers are >40% of revenue, every one of them becomes a single point of failure in the multiple.

Risk 3 · The productivity-bubble compression timing. Per the productivity gap analysis, most enterprise customers have not yet seen the AI productivity gains they projected. The first wave of measurable disappointment lands in the same Q4 2026 – Q1 2027 window in which Anthropic will be reporting its first public earnings. If 1,000 of Anthropic’s largest customers go into 2027 having missed their AI productivity targets, renewals slow, expansion stalls, and the public-market thesis on Anthropic gets tested at exactly the wrong moment.

Each of these risks is manageable. None of them is fatal. But the IPO premium implicitly assumes that the disclosure events do not surface them in a way that compresses the multiple. The premium is, in effect, an option on flawless execution through a quarter that has not yet happened.

What to Do This Quarter

1. AI startup founders: If you are mid-Series A or B in vertical AI, the acquisition window opens after the Anthropic IPO and stays open for roughly six months. Be ready to take a strategic conversation. The number you used to refuse may be the number you are offered.

2. Anthropic employees: The IPO is the single most consequential financial event in your career. Talk to a financial advisor before the lock-up date about diversification timing. The IPO makes most of you wealthier overnight; the post-lock-up period is where wealth either consolidates or evaporates.

3. Institutional investors: Pre-IPO positions are still available on Forge and the secondary markets. After May, the discount narrows. After October, the public price rules. The window for entry-via-secondary at meaningful discount is closing.

4. Competing AI labs: The strategic consequence of an Anthropic IPO is not Anthropic’s valuation. It is the comp pressure, the acquisition pressure, and the talent flow it creates. If you do not have a 6-month plan for retention and acquisition response, you are about to be on the wrong side of the trade for two quarters.

The Strategic Read

Most public-market events get priced into expectations months before they occur. The Anthropic IPO has been priced into the secondary market — Forge has it at $259.14, up 381% in twelve months — but the second-order effects have not been priced into the rest of the AI ecosystem.

The IPO is not the story. The IPO is the mechanism that opens five gates simultaneously: acquisition currency, employee liquidity, secondary-market unfreeze, infrastructure funding, and sovereign-wealth access. Each of these gates changes the speed at which the entire AI sector reshuffles.

The pre-IPO Anthropic was already the most strategically positioned AI company on the enterprise platform race, the Wall Street channel acquisition, and the forward-deployed engineering function. The post-IPO Anthropic has all of those structural advantages plus the financial mechanics to execute on a different timescale than its competitors. That is the gap that opens in October. It is not a gap that closes quickly.

The risks — capex disclosure, revenue concentration, productivity-bubble timing — are real and can compress the multiple. But the structural events the IPO sets in motion are durable regardless of where the multiple settles. Anthropic public is a different company in the market than Anthropic private. The market’s reaction to Q1 2027 earnings will determine the multiple. The IPO itself determines the structural shape of the AI sector for the next two years.

The bell rings in October. Most of the second-order effects will not be visible until Q1 2027. The work to be ready for them happens now.

The IPO is not the financing event. It is the gate that opens five other events at once.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- Your AI Vendor’s AI Vendor — agent supply chain compromise (Vercel × Context AI)

- Single Digits — the April 2026 open-weight inflection

- AI-Washed — the 47.9% / 9% layoff narrative gap

- The 27% Problem — Anthropic’s enterprise lead and Google’s $750M check

- The Bubble Is Not in Valuations — the productivity gap

- The Agent Trap — why 90% of AI launches are infrastructure liars

- The Channel Move — Anthropic × Wall Street PE channel acquisition

Sources

- TechCrunch, Sources: Anthropic could raise a new $50B round at a valuation of $900B (2026-04-29)

- TechCrunch, Sources: Anthropic potential $900B+ valuation round could happen within 2 weeks (2026-04-30)

- The Next Web, Anthropic eyes a $900b valuation in a potential $50b round (2026-05-01)

- Bloomberg, Anthropic Weighs Funding Offers at Over $900 Billion Valuation (2026-04-29)

- Forge Global, Anthropic Upcoming IPO & Private Stock Price (accessed 2026-05)

- Yahoo Finance, Anthropic (ANTH.PVT) Forge Price (accessed 2026-05-04)

- Tech Startups, Anthropic eyes $900B valuation in new funding round ahead of IPO (2026-04-30)