For forty years, computer memory ran on one of the most reliable cycles in technology. Shortage pushed prices up, high prices pulled in new fabs, the new capacity created a glut, prices crashed, and the survivors waited for the next shortage. Brutal, predictable, and — for buyers — eventually generous: cheap RAM always came back.

Micron just announced, in effect, that the generous part is over.

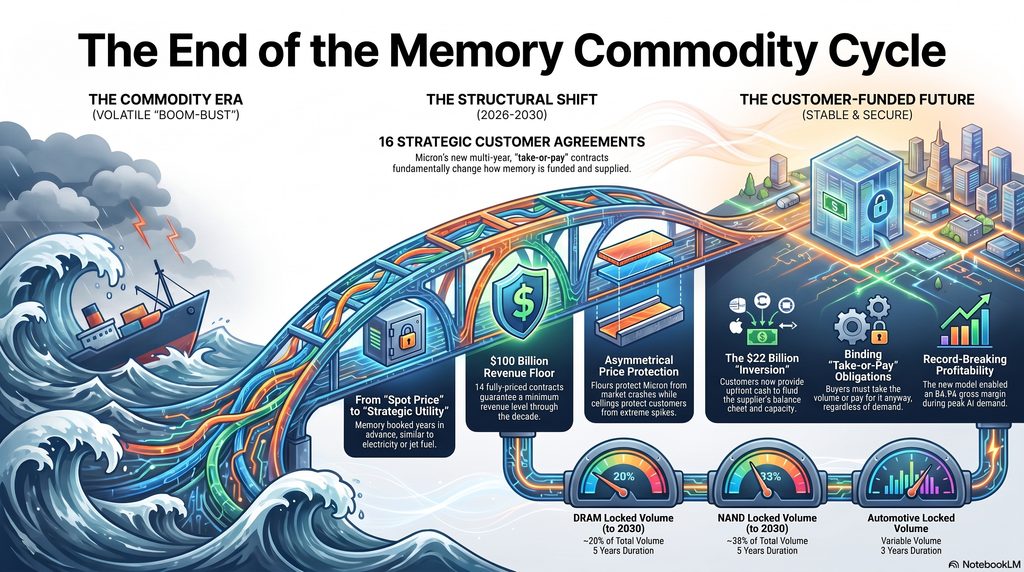

In its record June quarter, the memory maker disclosed 16 long-term “take-or-pay” contracts that lock up a large slice of its output through 2030, carry roughly $100 billion in minimum guaranteed revenue, and — the detail that should make every hardware buyer sit up — come with $22 billion in cash and financial commitments paid by the customers, to Micron, up front. Memory has stopped being something you buy at the spot price when you need it. For the largest buyers, it has become a contracted, prepaid, strategic input — booked years in advance, like electricity or jet fuel.

Memory stopped being a commodity

Micron just locked up a fifth of its DRAM and a third of its NAND through 2030 with binding take-or-pay contracts — and collected $22 billion in deposits from the customers, up front. The boom-bust cycle that always brought cheap RAM back is being contracted away.

A dream deal for Micron — near-peak prices, margin floors above any past peak, customer-funded fabs. Insurance for the buyers who signed — real protection against a real shortage, bought dear. And for everyone else, a forecast: don’t expect cheap memory back soon. The structure is also a large, leveraged bet on AI demand holding to 2030 — and floors get tested in a genuine downturn. The contracts run to 2030; the test arrives sooner.

What Micron actually signed

The contracts are called Strategic Customer Agreements. They run mostly five years, from calendar 2026 to the end of 2030 (automotive deals run three), and they are take-or-pay: the customer commits to buy a set volume each year, or pay for it regardless. Together the 16 cover about 20% of Micron’s DRAM volume and roughly a third of its NAND over the period. The 14 that are fully priced add up to that ~$100 billion floor in contracted revenue.

The pricing is the clever part. Most of the big deals sit inside a band. The ceiling is set near today’s already-elevated market prices — around the level of spring 2026. The floor is set to guarantee Micron a gross margin above any level it has hit in any previous cycle — and the previous peak was about 62%. In other words, even if the memory market collapses in 2028, these contracts keep Micron earning better than it ever did at the top of past booms. The ceiling protects the customer only if prices climb even higher from here; the floor protects Micron against the crash that historically always came. The asymmetry is the whole point.

And they are not casually cancellable. Micron describes them as binding take-or-pay commitments — the obligation to take the volume, or pay for it anyway, is itself the penalty for walking away.

CORSAIR Vengeance LPX DDR4 RAM 32GB (2x16GB) Up to 3200MHz CL16-20-20-38 1.35V Intel XMP AMD EXPO Computer Memory – Black (CMK32GX4M2E3200C16)

Disclaimer: Maximum Speed requires overclocking/PC BIOS adjustments. Maximum speed and performance depend on system components, including motherboard and…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The inversion: customers now fund the supplier

Here is the part that genuinely breaks with how this industry has always worked. Under the signed deals, Micron expects to collect $22 billion in customer deposits and financial commitments — roughly $18 billion in cash deposits plus about $4 billion in letters of credit. That money sits on Micron’s balance sheet for the life of the contracts and is returned to customers later, on a back-end-weighted schedule.

Read that again. The customers are putting billions of dollars into the supplier’s balance sheet to secure the right to buy its product. Building a memory fab costs tens of billions and takes years; historically the manufacturer carried that risk and the buyers waited for the glut. Now the buyers are pre-funding the capacity and accepting the price floor that pays for it. The party that used to wait for prices to fall is now financing the factory that ensures they won’t.

The quarter that framed all this was the strongest in Micron’s history: revenue of $41.5 billion, up 346% year on year; a record gross margin of 84.9%; record free cash flow of $18.3 billion; debt cut to under $6 billion. Management guided the next quarter to $50 billion in revenue and an ~86% margin. HBM4 — the high-bandwidth memory that sits next to AI accelerators — is ramping twice as fast as the prior generation. Wall Street responded with price targets that would have looked deranged eighteen months ago. This is what pricing power looks like when the cycle that used to discipline it has been contracted away.

gaming computer memory modules

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

“Cycle break” is the claim every peak makes

Micron’s pitch is that it has tamed the boom-bust cycle — turned a commodity producer into a strategic infrastructure supplier with predictable, contracted demand. There is real substance to it. But sobriety is warranted, because every cycle peak produces confident declarations that this time the cycle is broken, and they are usually made right before it isn’t.

Two caveats keep this honest. First, by Micron’s own account this covers only about 20% of DRAM and a third of NAND so far; the company wants to get past half of revenue under these terms, but it isn’t there yet. The cycle is being smoothed and extended, not abolished. Second, the framing comes loaded. Micron’s chief business officer pointedly blamed certain large customers — implicitly Apple among them — for slashing prices in the last downturn and starving the company of the cash to invest in capacity, which (the argument goes) seeded today’s shortage. Whatever the merits, that is the language of a supplier seizing pricing power after years of being commoditized, and dressing the power shift as industry stability. It may be stability. It is also, unmistakably, leverage.

KlNGST0N 1 x 96GB DDR5 5600MT/s ECC RDIMM Server RAM (KSM56R46BD4PMI-96MBI) – Dual Rank, CL46, 288-Pin, 1.1V Registered DIMM Memory with Locked BOM & Micron B-Die DRAM for Servers & Threadripper PCs

[ Maximize Data Center Throughput ] Upgrade your infrastructure with a powerhouse 96GB DDR5 5600MT/s Registered DIMM. This…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Insurance against the bubble — pointing both ways

The sharpest way to read the $22 billion in deposits and the take-or-pay floors is as insurance against the AI bubble bursting — and it is worth being clear about who is insuring whom.

For Micron, the structure is a hedge against demand evaporating. If the AI capital-expenditure boom cools in 2028 or 2029, Micron still collects on floor prices and still holds customer deposits. The downside is capped. For the customers — hyperscalers, AI-infrastructure operators, large device makers — it is the opposite bet: they are wagering that their need for memory stays high enough that locking in volume at near-peak prices was the prudent move. If they are right, they secured scarce supply in a brutal market. If AI demand disappoints, they are holding multi-year obligations to buy memory at floor prices they no longer need, and the interesting questions become enforceability and renegotiation — because a $100 billion floor is only as solid as the counterparties’ willingness and ability to honor it. Micron calls $100 billion the floor. In a genuine demand collapse, floors get tested.

Samsung 990 PRO SSD 2TB NVMe M.2 PCIe Gen4, M.2 2280 Internal Solid State Hard Drive, Seq. Read Speeds Up to 7,450 MB/s for High End Computing, Gaming, and Heavy Duty Workstations, MZ-V9P2T0B/AM

MEET THE NEXT GEN: Consider this a cheat code; Our Samsung 990 PRO Gen4 SSD helps you reach…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What it means for everyone outside the 16 contracts

If you are not one of the seven-or-so very large and medium customers who signed, this news is simpler and less pleasant: memory stays expensive, for longer. Micron was blunt that demand is running well ahead of supply, that the shortage will take considerable time to ease, and that it has no clear line of sight to when supply catches up — with tightness expected to persist beyond 2027.

The pressure lands hardest where the contracts concentrate: server DRAM, HBM for AI accelerators, the DDR5 and coming DDR6 generations, enterprise SSDs, and high-end PCs and workstations. Consumer gear doesn’t move one-for-one with data-center pricing, but when the largest buyers lock up a fifth of DRAM and a third of NAND on multi-year terms, the flexibility that used to let spot prices fall is simply removed from the market. Less slack upstream tends to hold retail prices up too. For anyone building memory-heavy systems — local inference rigs, workstations, well-specced servers — the era of waiting six months for RAM to get cheap may be on hold.

There is a strategic footnote worth flagging, too. Memory is yet another layer of the AI stack that is highly concentrated and sits outside Europe almost entirely — Micron in the US, Samsung and SK Hynix in Korea. The compute-supply story everyone tells about Nvidia has a quieter twin one layer down, in the chips that hold the data. Whoever controls the memory, and the contracts for it, holds a chokepoint just as real.

The take

For Micron, this is close to a dream: near-peak prices, margin floors above any prior peak, multi-year demand visibility, and customers pre-funding the fabs. For the buyers who signed, it is insurance — real protection against a scarcity that is genuinely painful right now, bought at a genuinely high price. For everyone else, it is a forecast: don’t expect cheap memory back soon.

The honest verdict is that Micron has done something smart and structurally significant, and that the same structure is a large, leveraged bet on AI demand holding up through 2030. If it holds, the cycle really will have been bent. If it breaks, the world will get to watch what happens when $100 billion in take-or-pay floors meets a market that no longer wants the volume. The contracts run to 2030. The test arrives well before then.

Sources: Micron Technology fiscal Q3 2026 earnings call and prepared remarks (16 Strategic Customer Agreements; ~$100bn minimum contracted revenue across 14 of 16; ~20% DRAM / ~⅓ NAND coverage; $22bn deposits / ~$18bn cash + ~$4bn letters of credit; price floors/ceilings; $41.5bn revenue, 84.9% gross margin, Q4 guidance); Reuters, Tom’s Hardware, Investing.com, TheStreet, Yahoo Finance reporting (June 2026). Figures reflect reporting as of late June 2026; quotes are paraphrased. Analysis and opinions are the author’s.