For two decades, the open web ran on a single unwritten contract. Publishers let search engines crawl and index their content; in exchange, the search engines sent readers — the referral — back to the publishers’ sites, where advertising and subscriptions turned that traffic into revenue. Content for traffic. That was the deal, and the entire economic structure of digital publishing was built on top of it.

The deal is being severed. Not renegotiated — severed. Google’s AI Overviews now answer the query directly on the results page, and the reader never clicks through. As of early 2026, roughly 58-60% of Google searches end in zero clicks; for queries where an AI Overview appears, the zero-click rate runs 80-83%. The user asked, Google answered, and the publisher’s site never saw them.

The data is no longer ambiguous. An Ahrefs study in February 2026 found AI Overviews correlate with a 58% reduction in click-through rates on top-ranking pages — nearly double the 34.5% measured in April 2025. Pew found that only 8% of users click a traditional result when an AI Overview is present, versus 15% when it is not. Chartbeat, tracking thousands of publisher sites, recorded Google search referrals falling 33% globally in the year to November 2025, and 38% for US publishers.

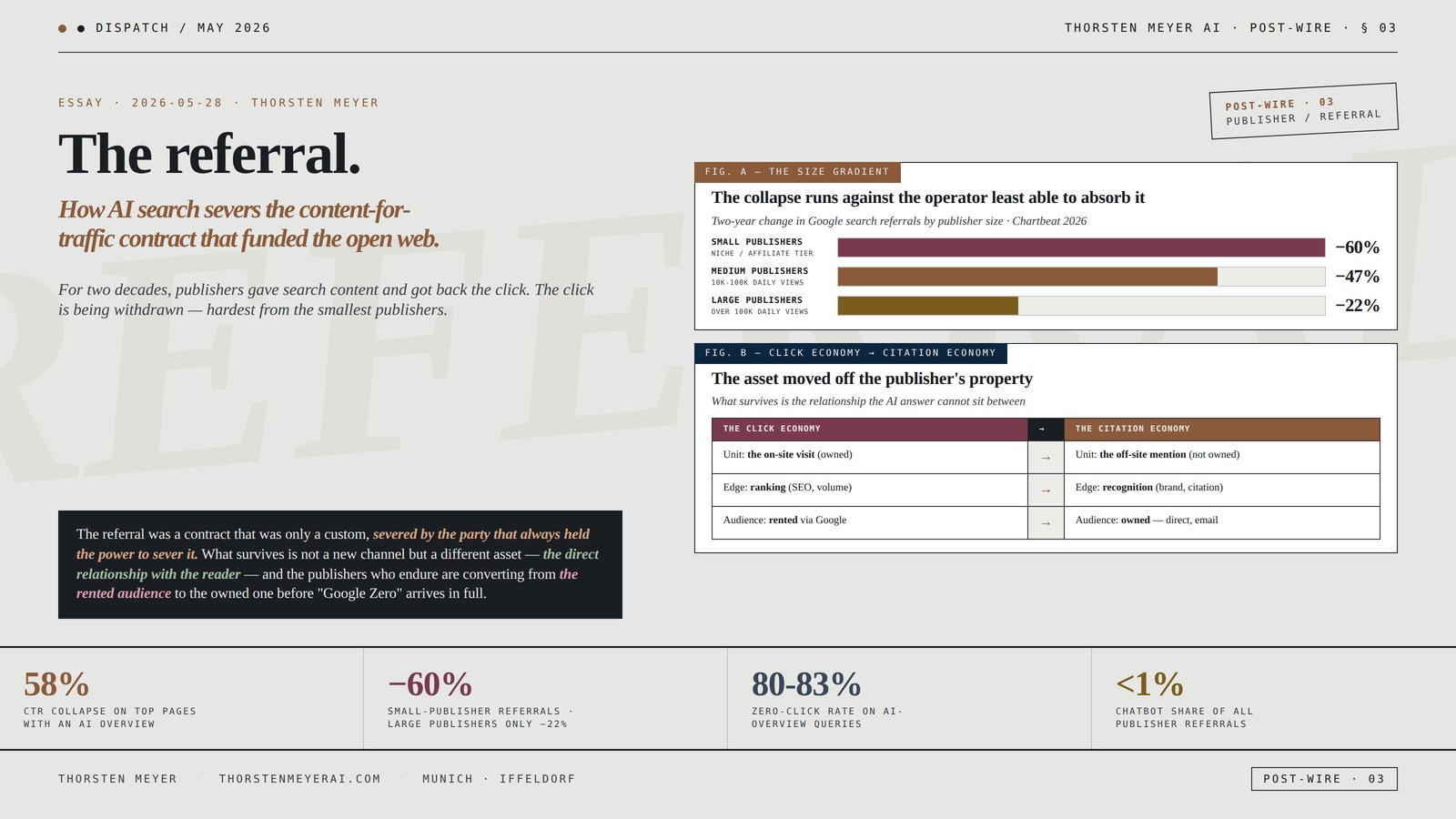

And the loss is not landing evenly. Chartbeat’s March 2026 data, reported by Axios, found small publishers lost 60% of their Google search referrals over two years; medium publishers lost 47%; large publishers lost 22%. The smaller the site, the harder the bleed. This is the publisher-side forensic that matters most to anyone running a portfolio of niche sites: the referral economy is collapsing fastest exactly where the margin was already thinnest.

The structural argument I want to make: the referral was the load-bearing contract of the open web, and AI search is dissolving it — replacing a click economy (be found, get the visit, monetize the visit) with a citation economy (be named in the answer, get nothing but the mention) — and the value of the mention does not pay the bills the click used to pay. This is the second death in the Post-Wire sequence. The first was the death of the identical paragraph — the commoditization of the content itself. This is the death of the referral — the severing of the channel that monetized it.

The headline integrative finding: What is collapsing is not traffic in general but the specific reciprocity that funded independent publishing — and nothing is replacing it at scale. Chatbot referrals (ChatGPT, Perplexity, Claude) grew over 200% in the year, but still account for less than 1% of all publisher referrals. The honest both-sides read matters here: AI-referred traffic converts far better when it does arrive (one measure puts it at 14.2% versus Google’s 2.8%), zero-click rates may be leveling off, and citation appears to redistribute clicks toward named brands rather than uniformly suppress them. But for the small publisher, the redistribution runs the wrong way: toward recognized brands and away from the long tail, which is precisely where independent and niche publishing lives. The click economy is becoming a citation economy, and the citation economy is a brand economy — which is a harder economy for the small operator than the one it replaces.

This essay walks the reciprocity contract that the referral was, the data forensic of its collapse, the small-publisher asymmetry, the thing that is not replacing it, the production-disincentive paradox that traps Google itself, the genuine counter-reading, and the structural shift from a click economy to a citation economy — and what survives it.

The referral.

How AI search severs the

content-for-traffic contract

that funded the open web.

AI Overview · up from 34.5% in 2025

two years · large publishers only −22%

AI Overview appears

despite 200%+ growth

for

traffic

The referral was a contract that was only a custom, severed by the party that always held the power to sever it. What survives is not a new channel but a different asset — the direct relationship with the reader — and the publishers who endure are converting from the rented audience to the owned one before “Google Zero” arrives in full.Thorsten Meyer · The Referral · Post-Wire 03

By Thorsten Meyer — May 2026

This is the third dispatch in the Post-Wire track — the publisher-side forensics of AI intermediation. The first walked the death of the identical paragraph: the commoditization of syndicated, wire-style content when the same paragraph appears on five hundred sites and AI can generate the five-hundred-and-first for free. This one walks the layer beneath that: even content that is not commoditized still depended on the referral to be monetized, and the referral is the thing AI search is now severing.

The structural argument I want to make: publishing’s business model was never really “content.” It was “content plus the referral that monetized it” — and the two have always been separable, which means one can die while the other persists. A site can produce genuinely valuable, non-commoditized content and still go bankrupt if the channel that delivered paying readers to it closes. That is the precise situation AI search is creating: the content is still good, the ranking may still be high, and the click no longer comes — because the answer was delivered before the reader ever reached the link.

The headline integrative finding: The collapse is real, it is size-graded against the small publisher, and it is structural rather than cyclical — but it is also not uniform, and the shape of what survives is becoming legible. The publishers who endure are converting from a traffic business to a relationship business: direct subscriptions, email lists, brand recognition, owned audiences on platforms the AI answer cannot fully intermediate, and — for those large enough to negotiate — content-licensing deals with the AI companies themselves. The referral is dying as the primary channel. What replaces it is not a new channel but a different asset: the direct relationship with the reader, which the AI answer cannot sit between.

This essay walks the reciprocity contract (Section I), the data forensic (Section II), the small-publisher asymmetry (Section III), the non-replacement (Section IV), the production-disincentive paradox (Section V), the counter-reading (Section VI), and the structural shift to a citation economy (Section VII).

I · The reciprocity contract · what the referral was

The contract crystallization. To see what is dying, you have to name the deal precisely — because it was never written down, and its informality is exactly why it could be dissolved unilaterally.

The two-decade deal

The exchange: publishers allowed search engines to crawl, index, and excerpt their content. In return, the search engine ranked that content and sent users who clicked through — the referral — to the publisher’s site.

Where the money was: the referral landed the reader on the publisher’s page, where the publisher monetized the visit through display advertising, affiliate links, subscription prompts, and audience data. The search engine captured the query; the publisher captured the visit. Both were paid.

Why it held for twenty years: the arrangement was genuinely reciprocal. Google’s search product was only valuable because the web had content worth finding; the web’s content was only economically viable because search delivered the readers who monetized it. Each side needed the other, and the referral was the settlement layer between them.

What the contract was not

It was never a legal agreement: there is no signed contract entitling a publisher to referral traffic. The reciprocity was a practice, not a promise — which is the crux of the current dispute. In litigation, Google has argued precisely that it never “promised to deliver” any referral traffic. The publishers’ counter is that two decades of documented practice constituted a de facto contract.

It was never guaranteed to persist: because the deal was informal, it could be altered the moment one side found it advantageous to alter it. The publishers had no enforceable claim on the referral; they had a custom. Customs can be ended.

The asymmetry that was always there

Google held the distribution; publishers held the content: in a healthy reciprocity, that balance is stable because each needs the other. But the balance was always asymmetric — Google could send traffic to a different site; a publisher dependent on Google for 40-60% of its referrals could not easily replace Google. The dependency ran one direction harder than the other, and AI search is the moment that latent asymmetry became an exercised one.

The contract observation

The referral was a twenty-year reciprocity — content for traffic — that funded the entire open web, and it was never anything more durable than a custom. Its informality was its fatal flaw: a deal that powerful should have been a contract, and because it was only a practice, it could be dissolved the instant the distributor found a way to answer the query without sending the reader onward. AI search is that way. The referral did not break; it was discontinued, by the party that always held the power to discontinue it.

As an affiliate, we earn on qualifying purchases.

II · The collapse · the data forensic

The empirical crystallization. The dissolution is measurable, and the measurements converge from independent sources on the same conclusion: the click is going away.

Zero-click as the baseline

The headline rate: as of early 2026, roughly 58-60% of all Google searches end without a click to any website. For the subset of queries where an AI Overview is displayed, the zero-click rate climbs to 80-83%. The default outcome of a search is now no visit.

The CTR collapse on the pages that do rank: an Ahrefs study (February 2026) found a 58% reduction in click-through rate on the top-ranking page when an AI Overview is present — up from a 34.5% reduction measured in April 2025. The decline is accelerating, not stabilizing, on this measure. Pew’s parallel finding: an 8% click rate with an AI Overview present versus 15% without — roughly half.

The aggregate referral decline

Chartbeat (the broadest measurement): tracking thousands of publisher sites, Google search referrals fell 33% globally in the year to November 2025, and 38% for US publishers. Google Discover referrals fell 15-21% over the same window.

AI Overview prevalence is climbing: AI Overviews now appear in over 25% of Google searches, roughly double the 13% of a year earlier. As the surface expands, the zero-click default expands with it.

The named casualties

The disclosed declines read like a casualty list: Business Insider lost 55% of monthly search traffic between April 2022 and April 2025 (and cut staff by 21%); HubSpot estimated a 70-80% organic-traffic decline; CNN reported 27-38%; Chegg’s non-subscriber traffic fell 49% and revenue 24% year-over-year (the company filed an antitrust suit); the Daily Mail’s desktop CTR on a surfaced query dropped from 25.23% to 2.79% — an 89% collapse.

The forward forecast: the Reuters Institute reported that media executives worldwide expect search referrals to fall 43% over the next three years; roughly 20% expect declines greater than 75%. Publishers from People Inc. to Wired to the Wall Street Journal are openly planning for “Google Zero” — the point at which referral traffic from the search giant dwindles toward nothing.

The forensic observation

The measurements converge from independent methodologies — Ahrefs, Pew, Chartbeat, Reuters Institute, named publisher disclosures — on a single finding: the click is being withdrawn, the withdrawal is accelerating on the per-page CTR measure, and publishers themselves are planning for its near-total disappearance. This is not a soft patch in a traffic cycle. It is a structural change in what a search engine does — from delivering readers to answering questions — and the referral is the casualty of that change.

Hands-On Predictive Analytics with Python: Master the complete predictive analytics process, from problem definition to model deployment

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The small-publisher asymmetry · why the smallest bleed most

The distributional crystallization. The collapse is not landing evenly, and the gradient runs against exactly the operator least able to absorb it.

The size gradient

Chartbeat’s March 2026 finding (reported by Axios): over a two-year window, Google search referrals fell 60% for small publishers, 47% for medium publishers (10,000-100,000 daily pageviews), and 22% for large publishers (over 100,000 daily pageviews). The smaller the site, the steeper the loss.

Why the gradient runs this way: large publishers have brand recognition that survives the AI summary — users search for them by name, arrive directly, and are more likely to be cited inside the AI Overview (cited brands reportedly get 35% more organic clicks and 91% more paid clicks). Small publishers depend disproportionately on the long-tail, unbranded query — “how to get rid of [insect],” “best [product] under $50” — which is precisely the query type the AI Overview answers most completely and most often.

The long-tail evaporation

The query types most fully absorbed: informational and how-to queries — the staple of niche, affiliate, and service-content publishing — are the ones AI Overviews answer most comprehensively. A lifestyle publisher cited in the PPA evidence saw CTR on a “how to get rid of [insect]” query fall from 5.1% to 0.6% while still ranking on page one with steady impressions. The ranking held; the click did not. That is the small publisher’s nightmare scenario: do everything right, rank well, produce useful content, and watch the traffic evaporate anyway because the answer was delivered upstream.

Why this is the publisher-operator’s central problem

The niche portfolio is the most-exposed structure: a portfolio of small, niche, search-dependent sites — the dominant model for independent and affiliate publishing — is the single most-exposed configuration in the entire collapse. It combines the highest dependency on the long-tail query (most absorbed by AIOs), the lowest brand recognition (least likely to be cited or searched-by-name), and the thinnest margin (least able to absorb a revenue shock). Everything that makes a niche-site portfolio efficient in the click economy makes it fragile in the citation economy.

The Bing hedge and the diversification logic: this is precisely why publisher-operators who diversified away from Google dependency — leaning on Bing-led traffic, building direct and email channels, owning audiences on platforms the AI answer cannot fully intermediate — were buying insurance against exactly this asymmetry, before it became this visible. The collapse rewards the operators who treated Google referral as a channel to be hedged rather than a foundation to be trusted.

The asymmetry observation

The referral collapse is size-graded against the small publisher — 60% versus 22% — because the small publisher lives on the long-tail, unbranded query that AI Overviews answer most completely, and lacks the brand recognition that survives the summary. The structure that made niche-site portfolios efficient — high search dependency, low brand investment, thin margins — is the structure most exposed to the severing of the referral. For the publisher-operator, this is not a headwind. It is a redefinition of what the business is.

Mobile App Marketing And Monetization: How To Promote Mobile Apps Like A Pro: Learn to promote and monetize your Android or iPhone app. Get hundreds … of downloads and grow your app business

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The non-replacement · the thing that does not fill the gap

The substitution-failure crystallization. A natural hope is that AI referrals replace search referrals — that ChatGPT and Perplexity and Claude send the readers Google stopped sending. The data says they do not, at least not at anything near replacement scale.

The AI-referral reality

The growth rate is real; the base is tiny: chatbot referrals to publishers grew over 200% in the year — but still account for less than 1% of all publisher page-view referrals. A 200% increase on a sub-1% base is still a sub-1% base. AI referrals are not offsetting the search-referral decline; they are a rounding error against it.

Why the AI answer refers so rarely: the entire design of an AI answer is to resolve the query without sending the user onward. A chatbot that fully answers the question has, by construction, removed the reason to click. The referral is not a feature of the AI-answer model the way it was a feature (however grudging) of the search-results model. The link, in an AI answer, is a citation, not a destination.

The measurement fog

Even the sub-1% is hard to see: free ChatGPT users send no referrer data, so their visits land in analytics as “Direct”; mobile apps strip referrer headers. The visible AI traffic in a standard analytics dashboard is the tip of an iceberg — but the iceberg, fully measured, is still small relative to the search referrals being lost. The fog makes the collapse harder to attribute, which makes it harder to fight.

The citation-not-click reality

Being named is not being visited: the AI economy substitutes citation for click. Your content may be the source the AI Overview synthesizes; you get the mention (sometimes), and you get no visit. The publisher provides the raw material for the answer and receives neither the traffic nor — for most publishers — the compensation. The licensing deals that do pay (the AI companies’ content agreements) are available almost exclusively to the largest publishers with the leverage to negotiate them; the small publisher provides the training and grounding data for free and receives a citation, at best.

The non-replacement observation

Nothing is replacing the search referral at scale: AI referrals are sub-1% of the total despite rapid growth, the AI-answer model is designed to resolve queries without referring onward, and the compensation that substitutes for traffic flows only to publishers large enough to negotiate it. The hope that one channel simply succeeds another is not supported by the data. The referral is not migrating from Google to AI. It is disappearing — and the citation that replaces it does not pay.

Web Analytics 2.0: The Art of Online Accountability and Science of Customer Centricity

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The production-disincentive paradox · the trap Google is in

The reflexive crystallization. The collapse contains a paradox that constrains the very company causing it — and that paradox is the strongest reason to expect the dissolution to be partial rather than total.

The dependency loop

Google’s ads need the web’s content: Google’s search-advertising business generated over $50 billion in the first quarter of 2026 alone, and it depends on the continued existence of web content — the pages AI Overviews summarize, and the advertising inventory attached to the broader web. If publishers stop producing content because the referral no longer pays, the raw material for the AI Overviews disappears, and so does the advertising ecosystem.

The disincentive Google is creating: by answering queries directly, Google reduces the traffic that funds the content production that feeds the answers. It is, in the long run, eroding its own input supply. A search engine that disincentivizes the production of the content it indexes is consuming its own substrate.

The squaring-the-circle attempt

The May 2026 updates: in May 2026, Google announced five updates to AI Overviews and AI Mode explicitly designed to send more traffic back to publishers — inline source links next to the relevant sentences, hover previews of linked sites, “Further Exploration” / “Explore new angles” sections with curated article links, and “Subscribed” labels for content from publications the user already pays for. These are Google’s most direct acknowledgment yet that AI search and the open web have a relationship problem.

Why they are UX optimizations, not structural fixes: the updates can raise the probability of a click at the link layer, but they do not change the fundamental mechanic — a complete AI answer makes the click optional. Inline links and hover previews lower the barrier to clicking; they do not restore the reason to click. Google is trying to keep AI Overviews as the primary interface while letting just enough clicks through that the ecosystem does not collapse. That is the circle it is trying to square, and the May updates are the attempt.

The litigation pressure

The antitrust front: Penske Media (Rolling Stone, Variety, Deadline, The Hollywood Reporter, Billboard) filed an antitrust suit in September 2025 and a February 2026 memorandum opposing dismissal, arguing Google is “cannibalizing” publisher traffic and that the reciprocity relationship — index in exchange for referral — has been broken. Chegg filed its own suit; the European Publishers Council and the UK’s PPA filed complaints; the UK CMA intervened. The legal theory is that the informal reciprocity contract was real enough to be enforceable. Whether courts agree is unresolved — but the pressure is itself a force pushing Google toward partial restoration.

The paradox observation

Google is trapped in a reflexive bind: its AI answers erode the content production and referral economy that its advertising business ultimately depends on, which is why it is simultaneously expanding AI Overviews and shipping UX updates to send some traffic back. The paradox is the publisher’s one structural source of leverage — Google cannot let the ecosystem fully collapse without undermining itself. The dissolution of the referral will therefore likely be partial, not total, not out of goodwill but out of Google’s own dependency on the substrate it is eroding. How partial is the open question, and litigation and regulation are the forces pushing it toward “more partial.”

VI · The counter-reading · the case that the collapse is overstated

The both-sides crystallization. The bear case is strong, but the honest forensic has to state the genuine counter-evidence — and it is more substantial than the crisis framing usually admits.

The conversion-quality argument

AI-referred traffic converts far better: one measure puts AI-search traffic conversion at 14.2% versus Google’s 2.8% — roughly five times higher. The logic is plausible: a reader who arrives via an AI answer has already been pre-qualified by the AI’s synthesis, arriving with higher intent. Fewer, better visitors may be worth more than more, worse ones — which would mean the raw traffic decline overstates the revenue decline.

The stabilization signal

Zero-click may be leveling off: Datos’s Q1 2026 State of Search report found the US zero-click rate actually fell from 24.5% in December 2025 to 22.4% in March 2026 (on a strict clickstream methodology). Seer data showed CTR on AIO queries collapsing to 0.61% by September 2025 and then rebounding 85% to 2.4% by February 2026. One reading is that the worst of the 2025 disruption has passed and AIO prevalence is stabilizing.

The redistribution argument

Citation redistributes rather than uniformly suppresses: brands cited inside an AI Overview get 35% more organic clicks and 91% more paid clicks; branded queries with AIOs present have shown CTR increases in some data. The picture is not uniform suppression but redistribution — toward cited, recognized brands, and toward the AIO-absent queries (where CTR actually rose). The collapse is concentrated, not universal, and there are pockets where AI search is additive.

Why the counter-reading does not rescue the small publisher

The redistribution runs the wrong way for the long tail: every element of the counter-reading favors the large, recognized, branded publisher. Higher-converting AI traffic, citation-driven redistribution, and brand-query CTR increases all accrue to the brands users already know — not to the niche site competing on the unbranded long-tail query. The counter-reading is real, and it is mostly good news for exactly the publishers least in danger. For the small operator, “the collapse is redistributive, not universal” means “the redistribution is away from you.”

The counter-reading observation

The honest forensic concedes real counter-evidence: AI traffic converts roughly five times better, zero-click may be stabilizing, and citation redistributes clicks toward named brands rather than uniformly suppressing them. These are not nothing — they meaningfully soften the crisis framing for large, branded publishers. But every strand of the counter-reading favors the recognized brand over the long-tail niche site, which means it confirms rather than contradicts the central asymmetry: the citation economy rewards the brands the click economy already rewarded, and strands the long tail the click economy at least fed.

VII · The structural reading · from a click economy to a citation economy

The synthesis crystallization. Step back from the data, and the shift has a clean shape: the open web is moving from a click economy to a citation economy, and the two reward fundamentally different assets.

Observation 1 · The monetizable unit changed from the visit to the mention

The empirical signal: the click — the visit that could be monetized with ads, affiliate links, and subscription prompts — is being replaced by the citation, the mention inside an AI answer that delivers no visit.

The structural reading: the publisher’s monetizable unit has changed from something it controlled (the on-site visit) to something it does not (the off-site mention). In the click economy, the publisher owned the page the reader landed on and everything that happened there. In the citation economy, the value accrues at the AI answer — which the publisher does not own, cannot monetize, and is often not compensated for. The asset moved off the publisher’s property, and the publisher’s business model was built entirely on its own property.

Observation 2 · The advantage moved from ranking to recognition

The empirical signal: ranking well no longer guarantees traffic (the “rank held, click didn’t” pattern); being cited and being searched-by-name increasingly does. Citation overlap with the organic top-10 has weakened from roughly 76% to 17-54% — meaning the page that ranks is increasingly not the page that gets cited.

The structural reading: the discipline that won the click economy — SEO, ranking optimization, long-tail content volume — is decoupling from the outcome. What wins the citation economy is brand recognition, being the source the AI trusts to cite, and direct relationships that bypass the answer entirely. This is a brutal transition for the operator optimized for ranking, because the skill that built the portfolio is no longer the skill that sustains it.

Observation 3 · What survives is the relationship the AI cannot intermediate

The empirical signal: the publishers planning for “Google Zero” are converting to direct subscriptions, email lists, owned audiences on platforms (YouTube, LinkedIn, Reddit, newsletters), paywalls, and — for the few large enough — licensing deals with the AI companies.

The structural reading: the durable asset in the citation economy is the direct relationship with the reader — the one the AI answer cannot sit between. An email subscriber, a paying member, a returning direct visitor, a community: these are relationships the AI Overview cannot intermediate, because they do not route through the query. The referral was a rented audience, always intermediated by Google. The relationship is an owned audience. The transition that survives the collapse is the conversion from rented to owned — which is harder, slower, and lower-volume than the referral, but is not severable by a distributor’s product decision.

Observation 4 · The small publisher must change what the business is

The empirical signal: the collapse is size-graded against the small publisher; the counter-reading’s redistribution runs toward brands; the long-tail query is the most absorbed.

The structural reading: the niche-site portfolio cannot survive the citation economy as a traffic business; it can survive only as a relationship-and-brand business, or by occupying queries the AI answer does not fully resolve. The adaptations are concrete: build direct and email channels that do not route through search; develop brand recognition that earns the name-search and the citation; pursue generative-engine optimization (being the cited source) rather than only search optimization; diversify distribution beyond Google (Bing, social, direct); occupy transactional and community queries that AI answers resolve poorly. None of this is the business the portfolio was. All of it is the business the portfolio must become.

What this is not

It is not a claim that publishing dies. Publishing persists — but as a relationship business, not a referral business. The transition is brutal, especially for the small operator, but it is a transition, not an extinction.

It is not a claim that the collapse is uniform. Large, branded publishers are meaningfully insulated; AI traffic converts better; redistribution is real. The collapse is concentrated on the long tail, not spread evenly.

It is not a claim that the referral fully disappears. Google’s own dependency on the content substrate, plus litigation and regulation, will likely keep the referral partial rather than zero. “Google Zero” is the planning scenario, not the certain outcome.

The synthesis observation

The referral was the load-bearing contract of the open web — content for traffic — and AI search is dissolving it, replacing a click economy in which the publisher monetized the visit with a citation economy in which the publisher receives the mention and not the visit. The collapse is real, accelerating on the per-page measure, and size-graded against the small publisher who lives on the long-tail query the AI answer absorbs most completely. Nothing is replacing the referral at scale — AI referrals are sub-1% — and the value of the citation does not pay what the click paid.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the asset has moved: from the on-site visit the publisher owned to the off-site mention the publisher does not, from ranking to recognition, from a rented audience to the owned relationship the AI answer cannot intermediate. The referral is dying as the primary channel of digital publishing. What survives is not a new channel but a different asset — the direct relationship with the reader — and the publishers who endure are the ones converting from the first to the second before “Google Zero” arrives in full.

That is the structural editorial question the referral collapse sits on top of. It is a contract that was only a custom, severed by the party that always held the power to sever it. It is a click economy becoming a citation economy. It is a redistribution that runs toward the brands the old economy already rewarded and away from the long tail it at least fed. And it is the layer where the future of independent publishing gets decided — not in whether the content is good, but in whether the publisher owns the relationship that delivers the reader, now that the referral that used to deliver them is being discontinued.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the Post-Wire track

This dispatch

- This piece · The referral · the publisher-side forensic of the referral collapse — how AI search severs the content-for-traffic contract and replaces a click economy with a citation economy that does not pay the small publisher · empirical-clay dominant, structural-slate and labor-rose balance

The track

- The death of the identical paragraph · Post-Wire 01 · the supply-side forensic — the commoditization of syndicated, wire-style content when AI can generate the five-hundred-and-first identical paragraph for free · the companion to this piece

- Post-Wire 02 · Post-Wire 02 · the continuing publisher-side intermediation analysis

- Forthcoming · The licensing asymmetry · why AI content-licensing deals flow to the largest publishers and strand the long tail, and what a small-publisher collective could plausibly negotiate · transition-bronze register

- Forthcoming · The generative-engine-optimization shift · what it takes to be the cited source rather than the ranked page, and whether GEO is a durable discipline or a temporary arbitrage · empirical-clay register

Adjacent tracks

- The CFO’s new operating system · Enterprise Reorg 01 · the enterprise mirror of the same intermediation dynamic at the software layer

- The runway · Enterprise Reorg 04 · the AI labs whose answer engines are severing the referral, and how their valuations are built

- The bank account in the chat · Agentic Commerce 01 · the consumer-finance mirror of the answer-engine intermediation pattern

Sources

The referral collapse · the data

- 9to5Google / Axios / Chartbeat · Google Search referrals plummeted — the size-graded finding: small publishers −60%, medium (10k-100k daily pageviews) −47%, large (>100k) −22% over two years · Google Search referrals −34%, Google Discover −15% · chatbots still under 1% of all publisher referrals · 9to5google.com

- TheNextWeb · Google AI Overviews updates / 58% click decline — Ahrefs Feb 2026: AIOs correlate with 58% CTR reduction on top-ranking pages, nearly double the 34.5% of April 2025 · Pew: 8% click with AIO vs 15% without · Chartbeat: Google search referrals −33% in 2025 · Google search ads >$50B in Q1 2026 · the May 2026 “Further Exploration” updates · thenextweb.com

- QuickSEO · Google AI Overviews Statistics 2026 — Reuters Institute / Chartbeat: Google search traffic to publishers −33% globally / −38% US to Nov 2025 · Discover −21% · ChatGPT referrals grew 200%+ but under 1% of all referrals · forecast −43% by 2029 (median), ~20% expect >75% · HubSpot 70-80%, Business Insider −55% (cut staff 21%), CNN −27-38%, Chegg revenue −24% · Datos counterpoint (zero-click 24.5%→22.4%); Seer rebound 85% to 2.4%; cited brands +35% organic / +91% paid · quickseo.ai

- Search Engine Journal · AI Overviews impact on publishers — Daily Mail desktop CTR 25.23%→2.79% (−89%), mobile −87% · search 20-40% of major-publisher referral · Digital Content Next −10% member traffic May-June · Bauer Media’s Stuart Forrest on “the era of lower clicks” · IPA/Foxglove/MOW CMA complaint · searchenginejournal.com

- Velacore · AI Overview Traffic Loss — AIOs now in >25% of searches (double the prior year’s 13%) · 60% of searches end with zero clicks; 80-83% for AIO-present queries · AI search converts at 14.2% vs Google’s 2.8% · the referrer-data fog (ChatGPT visits land as Direct) · velacore.au

The reciprocity contract and the litigation

- ALM Corp · Penske antitrust filing / 58% click decline — Penske Media (Rolling Stone, Variety, Deadline, Hollywood Reporter, Billboard) Sept 2025 suit + Feb 2026 memo opposing dismissal · Google “cannibalizing” traffic · Google’s “no promise to deliver referral traffic” argument vs the two-decade reciprocity practice · the “answer engine” transformation · almcorp.com

- ALM Corp · One-Third of Publishers Will Block AI Overviews — ~58% zero-click as of early 2026 · search 40-60% of total referral for many publishers · Google >90% of search in most markets (blocking Googlebot = invisibility) · 79% of top news sites block at least one AI training bot · Reuters Institute: executives fear 43% referral decline over three years · almcorp.com

- Digiday · AI Overviews linked to 25% drop — PPA evidence: Google ~93% UK search · AI Mode UK launch July 28 · a lifestyle member’s “how to get rid of [insect]” CTR 5.1%→0.6% while still ranking page one · automotive publisher −25% to first-ranked articles · members include Condé Nast, Future, Immediate, Hearst · digiday.com

The “Google Zero” planning scenario

- Alta Journal · How AI Overviews Are Killing Search Traffic — Similarweb: news-site traffic −26% in the year after AIOs · Business Insider −55% (April 2022-April 2025) · People Inc., Wired, WSJ planning for “Google Zero” · the two-decade social contract framing · paywalls and GEO as the adaptations · altaonline.com

- SEO-Kreativ · AI Overviews updates 2026 — the May 6 2026 Google updates (Explore new angles / inline source links / hover previews / Subscribed labels) as UX optimizations that “change nothing about the fundamental mechanic that a complete AI answer makes the click optional” · Penske suit, European Publishers Council EU complaint · seo-kreativ.de

The Post-Wire track backbone

- The death of the identical paragraph · Thorsten Meyer · Post-Wire 01 · the supply-side forensic — the commoditization of syndicated, wire-style content · the companion piece this dispatch builds on: 01 is the death of the content’s value, 03 is the death of the channel that monetized it

Key reference figures crystallized

- The reciprocity contract: content for traffic · two decades · never a contract, only a custom · Google’s “no promise to deliver referral traffic” defense · the latent distribution asymmetry now exercised

- The collapse: ~58-60% of searches zero-click (80-83% with AIO) · Ahrefs 58% CTR reduction on top pages (up from 34.5% in 2025) · Pew 8% vs 15% · Chartbeat −33% global / −38% US referrals to Nov 2025 · AIOs now in >25% of searches

- The size gradient: small publishers −60%, medium −47%, large −22% (Chartbeat, two years) · the long-tail unbranded query most absorbed · cited brands +35% organic / +91% paid

- The non-replacement: chatbot referrals +200% but under 1% of total · AI answer designed to resolve without referring · licensing pays only the largest

- The paradox: Google search ads >$50B Q1 2026 depend on the content AIOs disincentivize · May 2026 UX updates as squaring-the-circle · Penske/Chegg suits, CMA/EPC complaints

- The counter-reading: AI traffic converts 14.2% vs 2.8% · Datos zero-click 24.5%→22.4% · Seer rebound to 2.4% · redistribution toward cited brands — all favoring the large, branded publisher

- The structural shift: click economy → citation economy · monetizable unit moved from on-site visit to off-site mention · ranking decoupled from outcome (citation/top-10 overlap 76%→17-54%) · what survives = the owned relationship the AI cannot intermediate