You have clicked it thousands of times. The banner slides up, asks you to manage your preferences, hides “reject all” behind one more tap, and disappears — until the next site, where you do it again. The cookie banner is the most-used European software interface of the decade. It is also the perfect emblem of what went wrong.

Because while Europe was perfecting the consent pop-up, the most consequential technology of the century was being built somewhere else. And now, in the second half of 2026, Brussels wants to buy its way back in — without changing any of the laws, capital, or energy reality that put it on the outside in the first place.

This is not a story about whether privacy or safety matter. They do. It is a story about a continent that mistook regulating the interface for having a seat at the table, and is now discovering you cannot set the rules for a technology you do not build, cannot power, and will not fund.

Europe regulated the interface and forgot the engine

The cookie banner is the most-used European software of the decade. While Brussels perfected the consent pop-up, the frontier was built elsewhere — and now, in H2 2026, Europe wants to buy back in without changing what put it on the outside.

This isn’t about whether privacy or safety matter — they do. It’s that Europe mistook regulating the interface for having a seat at the table. You can’t grant your way out of a structural problem while keeping the structure — the laws, the capital gaps, the energy costs, the talent drain all left untouched. The fix isn’t another framework: it’s open weights as a product, sovereign compute on affordable power, real capital plumbing — and to stop mistaking a check for a strategy.

The banner is the symbol, not the disease

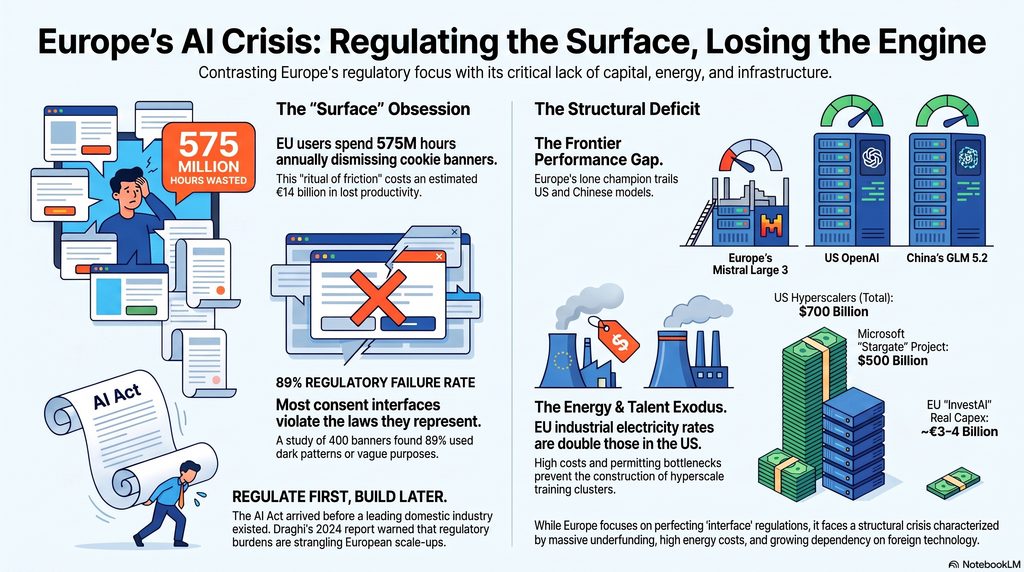

Start with the emblem, honestly. A consent-management vendor, Legiscope, estimates that EU internet users collectively spend around 575 million hours a year dismissing cookie banners — valued, at €25/hour, near €14 billion, or roughly 280,000 full-time jobs. Treat that as a back-of-envelope scale estimate from an interested party, not a hard fact. The number isn’t the point.

The point is that the banner is a failed consent interface. Most people click whatever makes it vanish; studies of real-world banners have found legal violations in the majority of them — one analysis of around 400 banners found roughly 89% broke the rules in some way, through dark patterns or vague purposes. And the irony runs deeper: the banner isn’t even mainly a GDPR artifact. The trigger is the older ePrivacy Directive’s Article 5(3), on storing information on your device. Europe built a continent-wide ritual of friction that annoys its citizens, fails to protect them well, and signals — to anyone watching — exactly where the regulatory reflex points: at the surface of technology, not its substance.

The clincher is that Brussels now agrees. Its own Digital Omnibus proposal tries to undo the mess with one-click choices and browser-level preferences, claiming it could save businesses €800 million a year. When your flagship digital achievement is a pop-up you are now urgently legislating to remove, that tells you which muscle Europe has been exercising.

Delete All Cookies Software Engineer T-Shirt

Are You Sure You Want To Delete All Cookies? Funny software developer engineer design. Makes a great gift…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The scoreboard nobody in Brussels wants to read

Now the substance. Where does Europe actually stand in the technology that became geopolitics?

The honest count of European labs in the frontier LLM conversation is one: Mistral. And Mistral, for all its genuine achievement, is a mid-tier player starved of the capital its rivals take for granted. Its strongest open model, Mistral Large 3, lands well behind the leaders on hard reasoning (around 44% on GPQA Diamond); its consumer app sits around seventh in usage, behind Gemini, Claude, Perplexity and OpenAI. Its edge is price, efficiency, and a French passport — not capability.

Here is the part that should sting. Europe’s single contender now trails not only the American closed frontier — OpenAI’s GPT-5.5, Anthropic’s Claude Opus 4.8, Google’s Gemini 3.1 — but also the Chinese open-weight models that anyone on earth can download for free. In June 2026, Zhipu shipped GLM 5.2, a 744-billion-parameter, MIT-licensed model that cracked the global top five and beats GPT-5.5 on several long-horizon coding benchmarks at roughly a sixth of the price. DeepSeek V4, Moonshot’s Kimi, Alibaba’s Qwen — China is shipping near-frontier capability as a free download. Europe cannot match, for money, what China is giving away.

And there is a tier above even that, the one that turned AI into statecraft: the export-controlled frontier. When Washington’s June 12 directive forced Anthropic to shut down Fable 5 and Mythos 5 worldwide, it was because those models are capable enough — in cyber, in bio, in AI research itself — to be treated as national-security infrastructure, gated like munitions. Europe has no model anywhere near that tier. Not behind the frontier — absent from the category that has become an instrument of state power. Tellingly, Mistral’s response is to start building a cybersecurity model as an alternative to Mythos, and its CEO is musing about designing custom chips. Europe’s champion is reacting to a board it does not set.

HIPAA Privacy and Security Compliance – Simplified: Practical Guide for Small and Medium Organizations

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why the talent and the money leave

None of this is an accident of national character. It is the predictable output of three structural choices, and they belong to Berlin, Paris, and Brussels in roughly equal measure.

Brussels regulates first and builds later. The AI Act arrived as the world’s first comprehensive AI law — a rulebook for an industry the bloc does not lead, written before the thing it governs existed at scale. This is not a fringe complaint: Mario Draghi’s own 2024 competitiveness report, commissioned by the Commission, warned that fragmented markets and regulatory burden were strangling European scale-ups, and the CEPS think tank and the Jacques Delors Centre have since argued the sovereignty push risks building new dependencies rather than ending them. When the establishment’s own economists are sounding the alarm, “anti-regulation rant” is not a available dismissal.

The capital simply isn’t here. There is no deep, unified European capital market; pension money largely won’t touch venture; the concentrated late-stage rounds that exist in San Francisco do not exist in Frankfurt or Paris. The proof is in Mistral’s own numbers: Europe’s flagship has raised roughly $3–4 billion across its life and is now reportedly in talks for about €3 billion more at a ~€20 billion valuation. Set that against the single rounds its rivals close — Anthropic’s $65 billion at a valuation near $1 trillion, OpenAI’s $122 billion at $852 billion. Europe’s entire AI champion is funded by less than one American lab raises in one go. Talent does the math and boards a flight to SF or London, where the compute, the comp, and the capital are.

And the lights cost twice as much. This is Berlin’s chapter. Germany completed its nuclear phase-out in 2023 and now carries some of the industrialized world’s highest electricity prices, with grid and permitting bottlenecks layered on top — exactly as AI turned cheap, abundant power into the binding input. Across the bloc, European industry pays roughly double US electricity rates (ACER, 2026). You cannot run a hyperscale training cluster on power that costs twice what your competitor pays, in a grid you can’t get connected to, permitted on a timeline measured in years. France, with its nuclear fleet, is the partial exception that proves the rule — and even Paris pairs cheap power with a statist instinct to pick champions rather than build deep markets.

browser cookie blocker extension

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The contradiction at the heart of 2026

Which brings us to the present, and the move that doesn’t add up.

In February 2025 the Commission launched InvestAI, promising to mobilise €200 billion for AI. Read the word carefully: “mobilise” means €50 billion of actual public money plus €150 billion the EU hopes private investors will add at a 10:1 leverage ratio that does not yet exist. Of the €50 billion, €20 billion is ring-fenced for four or five “gigafactories,” and even there Brussels funds only up to 17% of a facility’s capex — member states must match the rest. The formal call opens in July 2026; the facilities aren’t expected to run until 2027–2028; one site, in Norway, has broken ground.

The June 3 “Technological Sovereignty Package” that accompanied it is, stripped of the rhetoric, mostly legislation, not money: a Chips Act 2.0 that revises the 2023 act (first advanced fab “envisaged” for 2030–2033), a Cloud and AI Development Act whose flagship feature is a framework to assess how dependent you are, an open-source strategy, and an energy roadmap. Its cornerstone instrument is a sovereignty rating system. Faced with a dependency crisis, Europe’s instinct was, once again, to build an assessment framework.

Now put the numbers side by side, all of them sourced, none of them inflated:

- Europe spends, by the Commission’s own admission, around €264 billion every year importing non-EU digital products and services. It depends on foreign providers for more than 80% of its digital stack; American hyperscalers hold roughly 70% of its cloud market.

- Its answer is €20 billion “mobilised” — perhaps €3–4 billion in real, committed Commission capex — for compute that is not built yet.

- Meanwhile the four US hyperscalers are spending a combined ~$700 billion in capex in 2026 alone — Amazon and Microsoft around $200 billion and $190 billion each. The Stargate project alone is $500 billion. Microsoft is sitting on an $80 billion backlog of cloud orders it physically cannot fill for lack of power.

A single American company’s one-year capex is roughly ten times Europe’s entire multi-year gigafactory envelope. Stargate alone is twenty-five times it. And much of the compute actually rising on European soil is being built by non-European firms — Nebius, Nvidia, Microsoft’s $10 billion Portuguese data center — so that even the “sovereignty” buildout imports the providers it was meant to replace.

The contradiction, then, isn’t merely that the check is small. It is that Europe is writing a small, mostly-hypothetical, years-late check while leaving every upstream cause untouched — the AI Act unchanged, the consent regime intact, the capital markets still fragmented, the German grid still expensive and slow, the talent still leaving. You cannot grant your way out of a structural problem while preserving the structure.

Build Financial Software with Generative AI (From Scratch)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The honest other side

A fair critique has to meet the best defense, so here it is.

The Brussels Effect is the long game — set the global rules and everyone follows. Real, but it only works if you also have something to sell; you cannot regulate a market you have exited, and a rulebook is not a product.

Europe’s edge is applied and industrial AI, not frontier models. Partly true — and a reasonable bet. But applied AI still runs on someone else’s models and someone else’s compute, which is precisely the dependency the June 12 shutdown exposed: build your hospital triage on a model Washington can dark in ninety minutes and your “applied” sovereignty is a fiction.

It’s the fragmented single market and capital, not just the AI Act. Correct — and conceded. Regulation is one cause among several. That is the point. The failure is systemic, which is exactly why a single compute fund cannot fix it.

What would actually move the needle

Diagnosis without prescription is just complaint, so, briefly, the shape of a real answer — and it is not another framework.

Lean into the one position Europe can actually win: open weights and sovereignty as a product, not a paragraph. The Chinese labs just demonstrated that open, self-hostable models can reach near-frontier capability; a model you run on your own hardware is one no foreign directive can switch off. Back Mistral and the open-weight ecosystem like the strategic assets they are. Build sovereign compute that’s actually sovereign — European-owned, on power Europe can afford, which means treating energy and grid permitting as AI policy, because they are. Fix the capital plumbing so a European lab can raise a European round at frontier scale. And stop mistaking a grant for a strategy. The €20 billion is not the problem; the unchanged everything-else is.

Europe still has the researchers, the universities, the industrial base, and — in Mistral — a real foothold. What it has lacked is the willingness to change the structure that keeps sending its talent, its capital, and its compute somewhere else. Until that changes, the most-used piece of European software will remain the cookie banner: a small, friction-filled box, asking for your consent to something that has already been decided elsewhere.

Sources: European Commission (InvestAI; Tech Sovereignty Package, June 3, 2026; €264bn dependency figure); EuroHPC JU; ACER (2026) on industrial electricity prices; Draghi competitiveness report (2024); CEPS, “Sanctuaries or Cathedrals” (Nov 2025); Jacques Delors Centre; FT-compiled 2026 hyperscaler capex; Bloomberg/TechCrunch on Mistral; Artificial Analysis, BenchLM and vendor benchmarks for model standings; Legiscope (cookie-time estimate, flagged as a vendor estimate); academic studies on cookie-banner non-compliance. Model-capability and export-control specifics reflect reporting as of late June 2026. Analysis and opinions are the author’s.