The consulting business is a pyramid, and the pyramid is a leverage machine. A handful of partners sit at the top; a wide base of analysts and associates does the document-heavy work; and the firm bills the base out at a large multiple of what it pays them. The spread between cost and billing rate, multiplied across the base, is the profit. The model has funded the most prestigious careers in business for a century.

The base of that pyramid is exactly the work generative AI does best. Research, synthesis, first-pass modeling, slide production — high-volume, structured, document-heavy — is the analyst’s job and the language model’s home turf. McKinsey’s own Quantum Black research argues that AI can compress research-and-synthesis time on a typical engagement by 30% or more.

The cuts are already landing. McKinsey, which grew from 17,000 to 45,000 people over a decade, has pulled headcount back toward 40,000 and signaled a roughly 10% reduction across non-client-facing roles over 18-24 months. KPMG cut about 400 US advisory jobs and told staff it would shed roughly 10% of its US audit partners. Accenture’s CEO told employees that using AI is now a condition of promotion, and that the firm is exiting people it cannot retrain for the AI era.

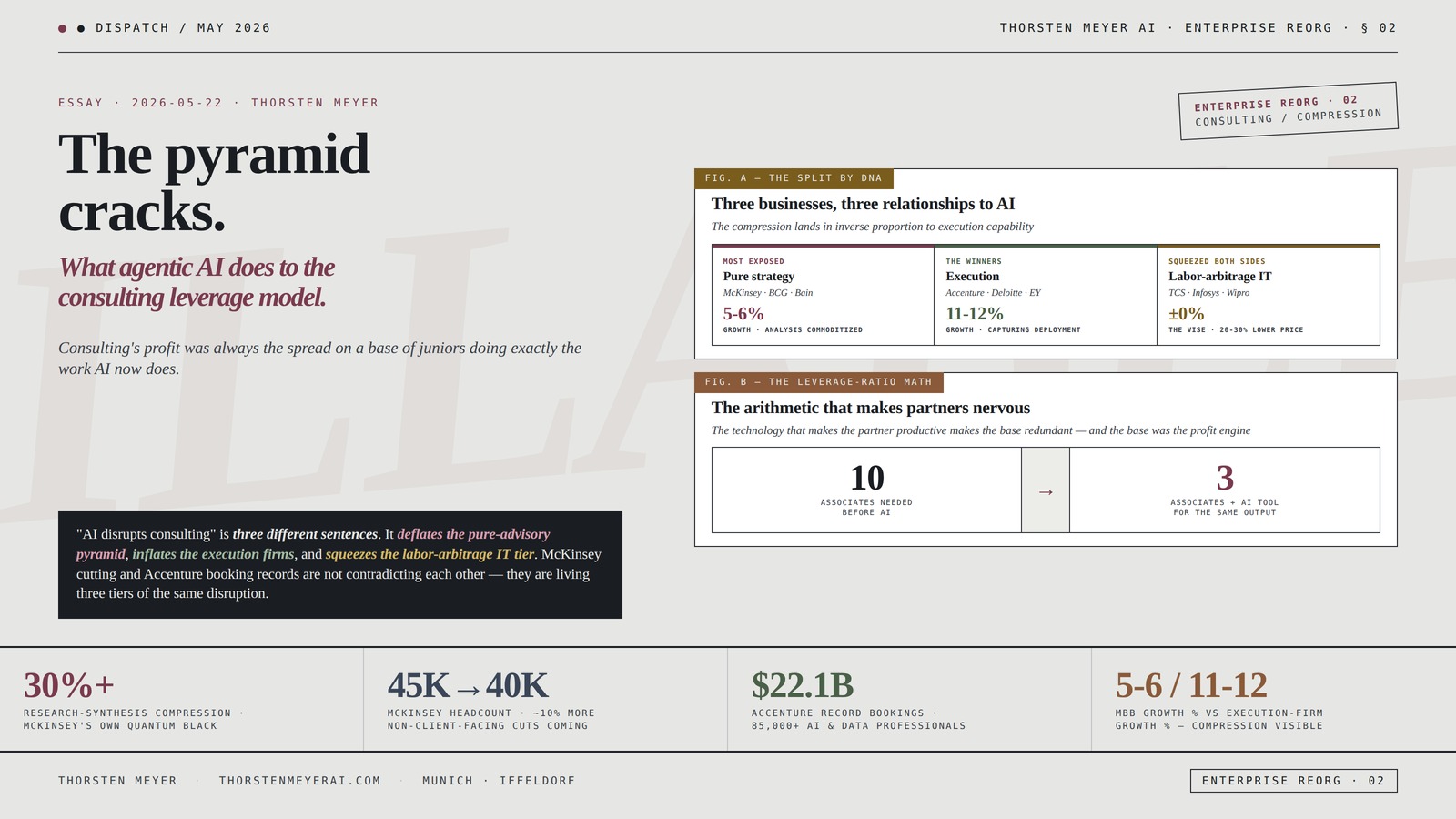

But the compression is not uniform, and that is the whole story. The pure-strategy firms — McKinsey, BCG, Bain — are growing at 5-6% while the execution-centric firms grow at 11-12%. Accenture posted a record $22.1 billion in quarterly bookings and now fields more than 85,000 AI and data professionals. The same force is hollowing out one kind of consulting firm and feeding another.

The structural argument I want to make: agentic AI does not shrink the consulting industry so much as split it by DNA. The firms whose value was analysis — the pure-advisory pyramid that monetized junior labor — face margin compression and a broken talent pipeline, because analysis is precisely what AI commoditizes. The firms whose value is deployment — large-scale implementation, change management, AI scaling — capture a new revenue line, because deploying AI at scale is work that did not exist before and that AI cannot do for itself.

The headline integrative finding: The compression is a reallocation, not a contraction. The 1:6 software-to-services ratio that funded the industry collapses on the analysis side and re-forms on the deployment side. The losers are the pure-strategy pyramids that cannot pivot to execution. The winners are the execution firms that capture the AI-deployment work. The squeezed middle is the India IT tier, caught between AI deflating its labor-arbitrage model from below and premium players taking the high-value AI work from above. And underneath all of it sits a second-order rupture the quarterly numbers do not yet show: if the base of the pyramid is the training ground for the partners, hollowing out the base breaks the machine that produces the people at the top.

This essay walks the leverage pyramid and what the model actually is, the base of it under attack, the cuts already landing firm by firm, the split by DNA into a three-tier compression map, the talent-pipeline rupture that the headcount numbers obscure, where the value reallocates, and the structural reading of an industry that splits rather than shrinks.

The pyramid cracks.

What agentic AI does

to the consulting

leverage model.

per McKinsey’s own Quantum Black

non-client-facing cuts coming

85,000+ AI & data professionals

growth % — the compression, visible

before AI

for the same output

The compression is a reallocation, not a contraction. The demand for help migrates from analysis — which AI commoditizes — to deployment — which AI creates demand for. The pyramid that monetized analysis-by-juniors compresses. The firm that monetizes deployment-at-scale grows.Thorsten Meyer · The Pyramid Cracks · Enterprise Reorg 02

The pyramid cracks.

What agentic AI does

to the consulting

leverage model.

per McKinsey’s own Quantum Black

non-client-facing cuts coming

85,000+ AI & data professionals

growth % — the compression, visible

before AI

for the same output

The compression is a reallocation, not a contraction. The demand for help migrates from analysis — which AI commoditizes — to deployment — which AI creates demand for. The pyramid that monetized analysis-by-juniors compresses. The firm that monetizes deployment-at-scale grows.Thorsten Meyer · The Pyramid Cracks · Enterprise Reorg 02

By Thorsten Meyer — May 2026

This is the second dispatch in the AI Enterprise Reorganization track. The first — The CFO’s new operating system — walked Anthropic’s May 2026 launch sequence (the $1.5 billion forward-deployment joint venture, ten finance agents on Claude, the PwC Office-of-CFO unit certifying 30,000 professionals) and named the consulting-tier compression as a consequence. This piece is that consequence in detail: the firm-by-firm forensic of how the compression actually lands, and why it lands so differently on different firms.

The structural argument I want to make: the consulting industry’s exposure to AI is not uniform because the consulting industry is not one business. It is at least three — pure strategy advisory, large-scale execution and implementation, and labor-arbitrage IT services — and AI does something different to each. To strategy advisory, AI is a direct attack on the billable base. To execution, AI is a new product to sell. To labor-arbitrage IT, AI is both a threat to the headcount model and a new managed-services line. The single phrase “AI disrupts consulting” hides three different stories, and the firms living them are reorganizing in opposite directions: McKinsey cutting non-client roles while Accenture books records.

The headline integrative finding: The leverage pyramid that defined elite consulting is the most exposed structure in professional services, because its economics depend on billing out a large base of juniors doing exactly the work AI now does. But the demand for help is not disappearing — it is migrating from “tell us what to do” to “do it with us at scale,” which favors the firms built for execution. The compression is real, it is uneven, and it carries a delayed second-order cost: the analyst base is the partner pipeline, and a firm that stops hiring analysts is, quietly, choosing to have fewer partners in fifteen years.

This essay walks the leverage pyramid (Section I), the base under attack (Section II), the cuts already landing (Section III), the split by DNA (Section IV), the talent-pipeline rupture (Section V), where the value reallocates (Section VI), and the structural reading of an industry that splits rather than shrinks (Section VII).

I · The leverage pyramid · what the model actually is

The business-model crystallization. To understand why AI is so dangerous to consulting specifically, you have to understand that consulting is not sold by the insight. It is sold by the hour, and the hours are leveraged.

The leverage math

The structure: a partner originates and oversees the engagement. Below the partner sit principals or managers; below them, a wide base of associates and analysts. The firm bills each level out at a rate that is a large multiple of that person’s cost. The leverage ratio — the number of juniors per partner — is the single most important number in the firm’s economics.

Why the base matters most: a partner’s time is finite and expensive, but a partner overseeing ten associates bills out eleven people’s hours while personally working one person’s hours. The profit is not the partner’s billing rate; it is the spread on the base, multiplied by the size of the base. A firm with high leverage (many juniors per partner) is more profitable per partner than a firm with low leverage — as long as the juniors are billable.

What the juniors actually do

The analyst’s job: gather data, build models, synthesize research, draft the deck. High-volume, structured, document-heavy work. The associate refines it; the manager packages it; the partner presents it and owns the relationship. The value the client pays for is the partner’s judgment and relationship — but the hours the client is billed for are overwhelmingly the base’s.

The dirty secret of the model: much of what the base produces is not irreplaceable insight. It is the necessary labor of turning raw information into a presentable analysis — exactly the labor that has the highest ratio of structured-process to genuine-judgment, and therefore the highest exposure to automation.

Why this is the most AI-exposed structure in professional services

The exposure profile: the leverage pyramid concentrates a firm’s labor — and its billing — in precisely the layer whose work is most automatable. A law firm has the same pyramid problem, and so does an investment bank’s analyst class, but consulting is the purest case because its product is the analysis, not a transaction or a legal filing. When the analysis can be produced by a model, the layer the firm bills the most hours for is the layer whose hours are worth the least.

The pyramid observation

Consulting’s profitability depends on billing out a large base of juniors at a multiple of their cost, and that base does the work AI does best. This is not a peripheral exposure; it is an exposure at the exact center of the business model. The firms most dependent on high leverage — many billable juniors per partner — are the firms most exposed to a technology that makes those juniors’ core output cheap. That is the structural fact everything else in this essay follows from.

AI Literature Review Toolkit: Systematic Reviews, Evidence Synthesis, Citation Mapping, and AI-Powered Scholarly Discovery (The Academic AI Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The base under attack · what AI does to the analyst’s job

The automation crystallization. The threat is not hypothetical and not future. The specific tasks that fill the analyst’s day are the specific tasks generative AI performs competently today.

The tasks that move first

Research and synthesis: reading a hundred earnings transcripts, summarizing a market, drafting a first-pass framework — work that took an analyst days now takes a model minutes. McKinsey’s own Quantum Black research puts the compression at 30% or more on a typical engagement.

First-pass modeling and analysis: structured quantitative work with defined inputs and outputs, the associate’s bread and butter, is increasingly a prompt rather than a week.

Document and deck production: the slide-from-scratch labor that consumed junior hours is among the most directly automated tasks in the entire knowledge economy.

The leverage-ratio math

The brutal arithmetic: if three associates plus an AI tool can produce what ten associates used to produce, the engagement needs three associates. Multiply that across hundreds of engagements and tens of thousands of staff, and the leverage ratio that funded the pyramid inverts from an asset into a liability.

The partner’s dilemma: the productivity gain is real and good for the partner — fewer people, same output, higher margin per engagement. But the same gain is a headcount story for everyone below the partner. The technology that makes the partner more productive makes the base redundant, and the base was the profit engine.

The hiring signal

The skill-mix shift: job postings that once asked for analytical skills and Excel modeling now ask for AI-tool deployment, prompt design, and the ability to validate AI output. A 2026 review of consulting and finance job ads found roughly one in four entry-level postings now mention AI fluency as a requirement, up from fewer than one in twenty two years earlier.

What this signals: the firms are not just hiring fewer juniors; they are hiring different juniors — ones who manage AI workflows rather than produce analysis from scratch. The job at the base of the pyramid is being redefined from “produce the analysis” to “direct and validate the machine that produces the analysis,” which requires far fewer people.

The macro frame

The scale: a World Economic Forum estimate puts roughly 300 million white-collar roles globally as reshaped by AI over five years, with around 100 million at risk of outright elimination. Junior consulting shares its exposure profile with junior banking, law, insurance underwriting, accounting, and corporate research — the structured-document professions. Consulting is not a special case; it is the leading case, because its leverage model makes the exposure most acute.

The base-under-attack observation

The analyst’s core output — research, synthesis, modeling, slides — is the most automatable knowledge work in the economy, and it is the layer the consulting pyramid bills out the most. The 30% compression McKinsey’s own researchers cite is not a ceiling; it is an early reading. The firms are already redefining the junior job from producer to validator, which is a polite way of saying the base of the pyramid needs far fewer people than it did two years ago.

AI-Powered PowerPoint: Automate Slides, Meetings & Business Storytelling with Office Scripts and Power Automate (VBA & macros)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The cuts already landing · the firm-by-firm forensic

The headcount crystallization. The compression has moved from forecast to payroll. The pattern across firms is consistent: cut the back office and the lower-performing base first, redefine the rest, and frame it as realignment rather than automation.

McKinsey

The numbers: grew from 17,000 to 45,000 over roughly a decade of hiring, then pulled back toward 40,000. Cut about 200 technology and support roles in late 2025, following 360-400 cuts in 2024. Leadership has discussed a roughly 10% reduction across non-client-facing departments over 18-24 months — potentially a few thousand roles.

The framing: global managing partner Bob Sternfels has signaled the firm will have fewer people in non-client-deployed areas, while continuing to hire client-facing consultants. The tell: revenue growth flatlined after the hiring boom, which means the pyramid got wider without getting more profitable — exactly the condition that makes leverage-ratio compression urgent. The cuts target the back office first, but the structural pressure is on the billable base.

The Big Four

KPMG: cut about 400 US advisory jobs (roughly half lower-performing consultants, no partners in that round) and informed staff it would shed about 10% of its US audit partners — roughly 100, including early retirements — framed as “strategic realignment” to match skills to future demand. KPMG noted parts of advisory are still growing (transactions, strategy, AI).

Deloitte, EY, PwC: all rolled out internal AI assistants over the prior 18 months and trimmed back-office headcount in the same window. PwC abandoned an ambitious hiring target, choosing to downsize and reorganize its existing workforce — and, per the prior dispatch, stood up an Office-of-CFO unit and committed to certifying 30,000 professionals on Claude. The Big Four are hedged: their audit franchises are regulatorily protected and their execution arms can pivot to AI deployment, so their compression is more selective than MBB’s.

Accenture

The other direction: Accenture posted a record $22.1 billion in quarterly bookings (up 6%), including 41 deals worth more than $100 million each, and now fields more than 85,000 AI and data professionals. CEO Julie Sweet told staff that using AI is a condition of promotion and that the firm is exiting people who cannot be retrained for the AI era while growing headcount where demand is strong. Accenture is not contracting; it is reallocating — out of non-adapters and into AI-deployment capacity.

The pattern

What is consistent across all of them: cut the back office and lower-performing base, redefine the surviving roles around AI, and frame it as realignment. What differs: McKinsey is cutting because its pure-advisory pyramid is most exposed; the Big Four are trimming selectively because their audit-and-execution mix is hedged; Accenture is reallocating because its execution DNA lets it sell AI deployment as a new product. Same technology, three different payroll outcomes.

The cuts observation

The layoffs are real, they are concentrated in the base and the back office, and they are uniformly framed as realignment rather than automation. But the framing obscures the structural divide: McKinsey cuts because the work it sells is the work AI commoditizes; Accenture hires because the work it sells is the work AI creates demand for. The headcount numbers are the surface; the DNA underneath them is the story.

Revolutionizing Requirements: The AI Advantage in Business Analysis: Book 1: Transform Your Approach to Requirement Writing and Discovery with … 101: Requirements Mastery with ChatGPT)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The split by DNA · the three-tier compression map

The differentiation crystallization. The single most important analytical move in reading consulting’s AI exposure is to stop treating consulting as one industry. It is three businesses with three different relationships to AI.

Tier 1 · Pure strategy advisory (MBB) — most exposed

The firms: McKinsey, BCG, Bain — the top of the traditional value chain, selling high-value strategy work through the leverage pyramid.

Why most exposed: their product is analysis and synthesis — exactly what AI commoditizes — and their economics depend most heavily on the leverage pyramid. When clients can run a hundred transcripts through a model themselves, the “tell us what the data says” engagement compresses. MBB growth has run at roughly 5-6%, against execution firms’ 11-12%, and the gap is the compression made visible.

The structural bind: MBB has invested in building technology and execution capability, but its DNA, brand, and economics are built around advisory. Pivoting to execution means competing on the execution firms’ turf, where MBB has less scale and a higher cost base. The pure-strategy pyramid is the structure with the most to lose and the hardest pivot.

Tier 2 · Execution and implementation — the winners

The firms: Accenture, Deloitte, EY — built to combine advisory with technology and large-scale execution.

Why they win: clients increasingly want integrated strategy-tech-execution packages, not pure advice. Deploying AI at scale — data cleanup, platform modernization, system integration, change management — is a large new body of work that did not exist before and that AI cannot do for itself. Accenture’s record bookings and 85,000+ AI professionals are the execution tier capturing the deployment work. Its GenAI bookings, while large, are estimated at less than 5% of a $200 billion-plus enterprise AI-services market — meaning the deployment runway is long.

The DNA advantage: these firms already sold large-scale implementation, so AI deployment is an extension of their existing product, not a pivot away from it. The technology that compresses MBB’s pyramid expands the execution firms’ addressable market.

Tier 3 · Labor-arbitrage IT services — squeezed from both sides

The firms: TCS (~$29B revenue), Infosys (~$19B), Wipro (~$11B), HCLTech, Tech Mahindra, plus Capgemini — the global-delivery model built on billing offshore labor at a discount to onshore rates.

The squeeze: AI deflates the labor-arbitrage model from below — if AI does the commodity coding and support work, the “bodies in seats at a lower rate” model loses its value. And premium players (Accenture, with industry-specific AI agents) take the high-value AI work from above. TCS’s AI-services revenue reached roughly $1.5 billion (about 5% of estimated revenue); Accenture’s was around $2.7-3 billion-plus. The India tier is pivoting hard to AI-infused managed services — Wipro’s bookings have surged, clients increasingly demand “AI-infused productivity” in large contracts — but it is doing so while defending a core model that AI directly threatens.

The map

The compression lands in inverse proportion to execution capability. Pure strategy (analysis is the product) compresses hardest. Execution (deployment is the product) grows. Labor-arbitrage (bodies are the product) is squeezed between AI taking the commodity work and premium players taking the premium work. The same technology, applied to three different business models, produces compression, growth, and a vise.

The split observation

“AI disrupts consulting” is three different sentences. It deflates the pure-advisory pyramid, inflates the execution firms, and squeezes the labor-arbitrage IT tier. The firms reorganizing in opposite directions — McKinsey cutting, Accenture booking records — are not contradicting each other; they are living three different tiers of the same disruption. Reading the industry as one business is the error that makes the headcount numbers look contradictory. Reading it as three makes them obvious.

Your AI Survival Guide: Scraped Knees, Bruised Elbows, and Lessons Learned from Real-World AI Deployments

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The talent-pipeline rupture · the cost the numbers hide

The second-order crystallization. The quarterly headcount numbers capture the first-order effect — fewer juniors needed now. They do not capture the second-order effect, which is slower, larger, and structurally harder to reverse: the base of the pyramid is the partner pipeline.

The pipeline mechanism

How partners are made: nobody is hired as a partner. A partner is an analyst who survived a decade of associate and manager roles, learning the craft, the judgment, and the relationships by doing the base work first. The pyramid is not just a billing structure; it is an apprenticeship structure. The base is where the firm trains the people who will eventually run it.

The rupture: if AI does the analyst work, the firm hires fewer analysts. But the analyst job was where future partners learned judgment by grinding through the analysis. A firm that stops hiring analysts is choosing, fifteen years early and largely without noticing, to have fewer partners. The pipeline that produces senior judgment runs through the junior work that AI is eliminating.

The judgment problem

What the apprenticeship taught: a senior consultant’s judgment about which analysis matters, which client framing will land, which recommendation is defensible, was built by personally doing thousands of hours of the analysis that AI now does. If the next generation directs and validates AI output instead of producing analysis, will they develop the same judgment — or a thinner version of it? Nobody knows, because the cohort that learns the craft by validating machines rather than building from scratch has not reached seniority yet.

The validation paradox: the surviving junior job is to validate AI output. But validating output well requires the expertise that used to come from producing the output. The firms are asking juniors to check work they were never trained to produce, which is either a manageable transition or a slow erosion of the expertise base — and the answer will not be visible for years.

Why this is hard to reverse

The lag: if a firm under-hires juniors for five years and then discovers it has a thin manager class and a thinner future-partner class, it cannot fix the gap quickly — you cannot hire a ten-year-experienced partner who never existed. The pipeline damage compounds silently and surfaces only when the senior ranks need replenishing from a base that was never built.

The pipeline observation

The headcount cuts are visible and the pipeline rupture is invisible, which is exactly why the rupture is more dangerous. The firms are optimizing the first-order cost — fewer juniors, higher margin now — and deferring the second-order cost — fewer trained seniors later. The pyramid is an apprenticeship machine disguised as a billing machine, and hollowing out the base to capture the margin gain quietly disables the machine that produces the people the firm cannot function without. That cost is real, large, and absent from every quarterly number.

VI · Where the value reallocates · the new revenue on the other side

The reallocation crystallization. The compression narrative is incomplete without its other half: the demand for help is not disappearing. It is moving, and the move creates new revenue for the firms positioned to capture it.

From analysis to deployment

The shift in what clients pay for: the value is migrating from “tell us what to do” (analysis, which AI commoditizes) to “do it with us at scale” (deployment, which AI creates demand for). A client that can run its own analysis with AI still cannot, by itself, clean its data, modernize its platforms, integrate the systems, manage the organizational change, and scale the deployment across a global workforce. That work is large, it is new, and it is human-and-firm-intensive in a way the analysis no longer is.

The new revenue lines

AI deployment services: the data cleanup, platform modernization, and security work that has to happen before AI can be deployed at scale — the groundwork the next AI-services cycle is being built on.

Change management at scale: rolling AI tools across a workforce of hundreds of thousands, retraining people, redesigning processes — the PwC-certifying-30,000-professionals model, the Office-of-CFO unit, the joint centers of excellence.

Industry-specific AI agents and platforms: proprietary AI agents built for each vertical, which justify premium pricing over commodity IT services and create switching costs — Accenture’s stated strategy.

Ongoing managed services: the optimization, upgrades, and continuous-improvement work that follows a large deployment — a long runway that favors firms with delivery scale.

Who captures it

The execution firms (Accenture, Deloitte, EY): their existing implementation DNA makes AI deployment an extension of their product. They capture the largest share.

The Big Four: their execution arms and their regulatorily-protected audit franchises let them pivot selectively — PwC’s Office-of-CFO unit is exactly this move.

The pure-strategy firms (MBB): can capture some of the high-end AI-strategy and AI-scaling advisory work, but compete for the deployment revenue on less favorable terms, because deployment is not their DNA.

The India IT tier: pivoting to AI-infused managed services, with a long runway in data and core-platform modernization — but defending a labor-arbitrage core that the same AI threatens.

The connection to the 1:6 ratio

The software-to-services ratio: historically, every dollar of enterprise software pulled roughly six dollars of services around it — integration, customization, deployment, support. AI compresses that ratio on the analysis side (the software does more, needs less analytical wrapping) and re-forms it on the deployment side (AI at scale needs new integration, change-management, and managed-services wrapping). The services revenue that funded the analysis pyramid shrinks; the services revenue that wraps AI deployment grows. The firms that can move from one to the other survive the transition; the firms anchored to the analysis side do not.

The reallocation observation

The compression and the growth are the same phenomenon viewed from two sides of the industry. The analysis revenue that funded the pyramid is migrating to deployment revenue that funds the execution firms. The demand for help is not falling — it is changing shape, from advice to implementation, in a way that rewards execution scale and punishes pure advisory. The firms that read this as “consulting is dying” mismanage the transition. The firms that read it as “the product is changing from analysis to deployment” capture the reallocation.

VII · The structural reading · an industry that splits, not shrinks

The synthesis crystallization. The consulting-AI story is told two ways in the trade press: as an extinction event for white-collar prestige work, or as overhyped disruption the firms will absorb. The structural reality is neither. The industry splits along the line between analysis and deployment, and the split is the story.

Observation 1 · The pyramid is the most-exposed structure, and it is the structure under most pressure

The empirical signal: the firms most dependent on high leverage and pure advisory — MBB — are growing slowest (5-6%) and cutting most visibly. The work they bill the most hours for is the work AI commoditizes most directly.

The forward shape: the leverage ratio compresses structurally, not cyclically. Partners hire fewer juniors per engagement, redefine the survivors as AI-workflow managers, and accept lower leverage. The pure-advisory pyramid does not disappear, but it operates at lower leverage, lower headcount, and — unless it captures deployment revenue — lower growth than the execution tier. The model that defined elite consulting for a century is being repriced.

Observation 2 · The value migrates from analysis to deployment, which favors execution DNA

The empirical signal: execution firms (Accenture 11-12% growth, record bookings) capture the deployment work; the pure-strategy firms compete for it on worse terms. The demand is migrating, not vanishing.

The forward shape: the firms built for large-scale execution win the AI transition, and the firms built for pure advisory either pivot to execution (hard, against their DNA and cost structure) or accept compression. The Big Four, hedged by audit and execution, navigate selectively. The execution firms expand. MBB faces the hardest strategic choice in its history: compete on execution turf or shrink into a smaller, higher-end advisory niche.

Observation 3 · The talent pipeline is the delayed cost nobody is pricing

The empirical signal: the cuts target the junior base and back office — the apprenticeship layer that produces future partners. The first-order margin gain is visible; the second-order pipeline cost is not.

The forward shape: a decade of under-hiring juniors produces a thin manager class and a thinner future-partner class that cannot be quickly repaired. The firms optimizing current margin by hollowing the base are deferring a structural cost into the 2030s. Whether the validate-the-machine generation develops partner-grade judgment is the open question that determines whether the industry’s senior ranks can be replenished at all. This is the cost that surfaces last and reverses slowest.

Observation 4 · The compression is a reallocation, and the 1:6 ratio is where you see it

The empirical signal: the software-to-services ratio collapses on the analysis side and re-forms on the deployment side. Services revenue does not vanish; it moves from wrapping analysis to wrapping AI deployment.

The forward shape: the total services revenue may not fall — it may grow, driven by AI-deployment demand — even as the analysis-pyramid revenue compresses. The industry’s headline numbers can stay flat or rise while its internal structure inverts: less analysis, more deployment; fewer juniors, more AI-and-data professionals; lower leverage, higher technology content. The aggregate “consulting is fine” and the specific “the pyramid is cracking” are both true, because they describe different layers of the same reallocation.

What this is not

It is not an extinction event for consulting. The demand for help with large-scale change is growing, not shrinking. The execution firms are booking records. The industry survives — reshaped, reweighted toward deployment, and operating at lower leverage.

It is not survivable without change for the pure-advisory pyramid. MBB’s 5-6% growth against execution’s 11-12% is the compression in the numbers. The pure-strategy firms face a genuine strategic crisis, and the brand and relationships that protected them do not protect the leverage economics.

It is not yet showing its largest cost. The talent-pipeline rupture is real, large, and absent from every current quarterly number, because it surfaces in the 2030s when the under-built base fails to produce the senior ranks the firms need.

The synthesis observation

The consulting pyramid cracks because its economics depend on billing out a large base of juniors doing the analytical work that AI now does — and the crack does not destroy the industry so much as split it. The pure-advisory firms whose product was analysis face margin compression and a quiet pipeline rupture. The execution firms whose product is deployment capture a new revenue line. The labor-arbitrage tier is squeezed between AI taking the commodity work and premium players taking the premium work. The demand for help migrates from analysis to deployment, the leverage ratio compresses, the talent pipeline frays, and the industry reorganizes around the firms built to do rather than the firms built to advise.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the leverage pyramid — the structure that funded the most prestigious careers in business for a century — is the single most AI-exposed structure in professional services, because its profit was always the spread on a base of juniors doing exactly the work that is now cheap. The firms that survive will be the ones that understand the product is changing from analysis to deployment, that the leverage ratio is being repriced permanently, and that the base of the pyramid was never just a billing layer — it was the machine that made the partners.

That is the structural editorial question the cracking pyramid sits on top of. It is a split by DNA, not a uniform contraction. It is a reallocation from analysis to deployment, not a disappearance of demand. It is a visible margin story today and an invisible pipeline story for the 2030s. And it is the layer where the next phase of professional-services economics gets decided — not in whether consulting survives, but in which kind of consulting firm the survival belongs to.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Enterprise Reorganization track

This dispatch

- This piece · The pyramid cracks · why agentic AI splits the consulting industry by DNA — compressing the pure-advisory leverage pyramid, feeding the execution firms, and squeezing the labor-arbitrage IT tier · labor-rose dominant, alternative-sage and structural-slate balance

The track

- The CFO’s new operating system · Enterprise Reorg 01 · Anthropic’s May 2026 launch sequence, the $1.5B forward-deployment JV, the ten finance agents, and the PwC Office-of-CFO unit — the dispatch that named this compression · the direct predecessor to this piece

- Forthcoming · The Palantir model at scale · PE-backed forward-deployed engineering economics when capitalized at $5B+ per lab, and why the JV pipeline is the structural innovation · empirical-clay register

- Forthcoming · The IPO storyline · how enterprise-revenue lock becomes the load-bearing valuation argument for the labs whose agents are doing the compressing · synthesis-deep register

Adjacent tracks

- The unbundling of the budget app · Agentic Commerce 02 · the consumer-side mirror of this enterprise unbundling — the same absorption logic, applied to personal finance

- The cleaner cap table · AI Governance 02 · the corporate structure of Anthropic, whose finance agents are a direct input to this compression

- The bank account in the chat · Agentic Commerce 01 · the consumer surface running on the same agentic substrate

Sources

The McKinsey cuts and the pyramid

- Metaintro · McKinsey Layoffs 2026 — ~200 tech/support roles cut late 2025 · Sternfels “non-client roles under active review over the next two years” · the leverage-ratio math (3 associates + AI = 10 associates’ output) · junior roles most exposed (high-volume, structured, document-heavy) · LinkedIn ~1 in 4 entry-level postings now mention AI fluency (up from <1 in 20) · WEF ~300M roles reshaped / ~100M at elimination risk · Quantum Black 30%+ research-synthesis compression · metaintro.com

- The420 · McKinsey 10% Layoff Wave — headcount 17K → 45K → ~40K · ~10% non-client-facing cut over 2 years · 200 global tech layoffs + 360-400 in 2024 · MBB 5-6% growth vs Accenture 11-12% · value shifting from analysis to large-scale change management and AI scaling · the420.in

- The HR Digest · McKinsey Job Cuts 2026 — 45K → 40K, revenue gains stalled · ~10% reduction in some areas, “a few thousand” non-client-facing roles over 18-24 months · 100th year framing · thehrdigest.com

- Medium / Alexander Simon · McKinsey at 100 — the “pyramid” framing · cutting support functions while hiring client-facing consultants · legacy growth strategies no longer coping · medium.com

The Big Four and the structural split

- TheStreet · Big Four firm KPMG cuts 100s of jobs — ~400 US advisory jobs cut (half lower-performing, no partners) · ~10% of US audit partners (~100, incl. early retirement) · “strategic realignment” · advisory still growing in transactions/strategy/AI · Accenture exiting non-retrainable staff, Julie Sweet “use AI to be promoted” · McKinsey 10% non-client-facing · thestreet.com

- Fast Company · Why the McKinsey layoffs are a warning signal — the DNA split: MBB (strategy, top of value chain) vs execution-centric firms (Deloitte, EY, Accenture) that combine advisory + technology + large-scale execution · the source of value shifting decisively · fastcompany.com

The execution tier and IT services

- Whalesbook · Accenture Record Bookings — Q2 FY26 (ending Feb 28 2026) record $22.1B bookings (+6%), 41 deals >$100M each · 85,000+ AI and data professionals · gaining managed-services share vs TCS/Infosys/Wipro/HCLTech · Gartner AI spending +44% YoY to $2.52T in 2026, global IT spending >$6T · whalesbook.com

- SWOTPal · Accenture SWOT 2026 — $3B+ GenAI bookings less than 5% of $200B+ enterprise AI-services market · Indian IT (TCS ~$29B, Infosys ~$19B, Wipro ~$11B) expanding into strategy/AI at 20-30% lower price points, targeting mid-market · Accenture differentiating via industry-specific GenAI agents and 20-30% premiums · swotpal.com

- BusinessToday · Accenture Q1 takeaways for Indian IT — AI-services revenue scale: TCS ~$1.5B (5% of FY26 est) vs Accenture ~$2.7B (4%) vs HCLTech ~$0.4B (3%) · next AI-services cycle groundwork (data cleanup, platform modernization, security) · demand improving from mid-2026 · businesstoday.in

- Forrester · The AI Effect — AI bookings accelerating across technology-services firms · clients demanding “AI-infused productivity” in large contracts · AI unlocking new revenue pools, compressing delivery timelines, enabling leaner operating models · “AI is no longer a niche” · forrester.com

The enterprise-reorganization backbone

- The CFO’s new operating system · Thorsten Meyer · Enterprise Reorg 01 · Anthropic’s May 2026 launch sequence, the $1.5B forward-deployment JV, the ten finance agents on Claude, the May 14 PwC Office-of-CFO unit certifying 30,000 professionals, the 1:6 software-to-services ratio collapse, the consulting-tier compression map · the dispatch that named this compression

Key reference figures crystallized

- The leverage pyramid: partners over a wide base of billable juniors · the leverage ratio (juniors per partner) is the key economic number · the profit is the spread on the base · the base does the most-automatable work

- McKinsey: 17K → 45K → ~40K · ~10% non-client-facing cut over 18-24 months · 200 tech cuts late 2025 + 360-400 in 2024 · revenue flatlined · Quantum Black 30%+ compression · MBB 5-6% growth

- KPMG: ~400 US advisory cut · ~10% US audit partners (~100) · “strategic realignment”

- Accenture: record $22.1B Q2 FY26 bookings (+6%) · 41 deals >$100M · 85,000+ AI/data professionals · ~$2.7-3B+ GenAI bookings (<5% of $200B+ market) · 11-12% growth · “use AI to be promoted”

- India IT: TCS ~$29B (~$1.5B AI, 5%) · Infosys ~$19B · Wipro ~$11B · HCLTech (~$0.4B AI, 3%) · 20-30% lower price points · squeezed between AI deflation and premium players

- The three-tier map: pure strategy (MBB) most exposed · execution (Accenture, Deloitte, EY) wins · labor-arbitrage IT squeezed from both sides

- The macro: Gartner AI spending +44% to $2.52T 2026 · global IT >$6T · WEF ~300M roles reshaped / ~100M at elimination risk

- The second-order cost: the base is the partner pipeline · hollowing the base breaks the apprenticeship that produces seniors · the cost surfaces in the 2030s

- The reallocation: value migrates from analysis (commoditized) to deployment (new demand) · the 1:6 software-to-services ratio collapses on analysis, re-forms on deployment