When Intuit shut down Mint in early 2024, it left roughly 3.6 million active users without a personal-finance anchor — and it created the opening that built the category that exists today. Monarch Money, founded by a former Mint product manager, grew its user base roughly twentyfold in the wake of the shutdown and raised $75 million at an $850 million valuation in May 2025, one of the largest consumer-fintech rounds of the year.

The category looked healthy. YNAB owned the behavior-change segment, Copilot owned the Apple aesthetic, Empower owned the free net-worth dashboard, Quicken Simplifi owned the low-price tier, and Rocket Money — owned by a public mortgage company — owned the mass market with 10 million-plus members.

Then, on May 15, 2026, OpenAI launched a personal-finance surface inside ChatGPT. Connect your accounts through Plaid, across more than 12,000 institutions, and the chatbot builds a dashboard of spending, subscriptions, portfolio, and upcoming payments — then answers questions grounded in your actual money rather than generic advice. OpenAI noted that more than 200 million people already ask ChatGPT financial questions every month.

One month earlier, OpenAI had acqui-hired the team behind Hiro Finance, a standalone AI personal-finance startup that shut down its own app on April 20, 2026. That sequence is the entire thesis of this piece in miniature: a standalone personal-finance app’s team was absorbed into a conversational surface, the standalone app died, and the capability re-emerged as a feature of something larger.

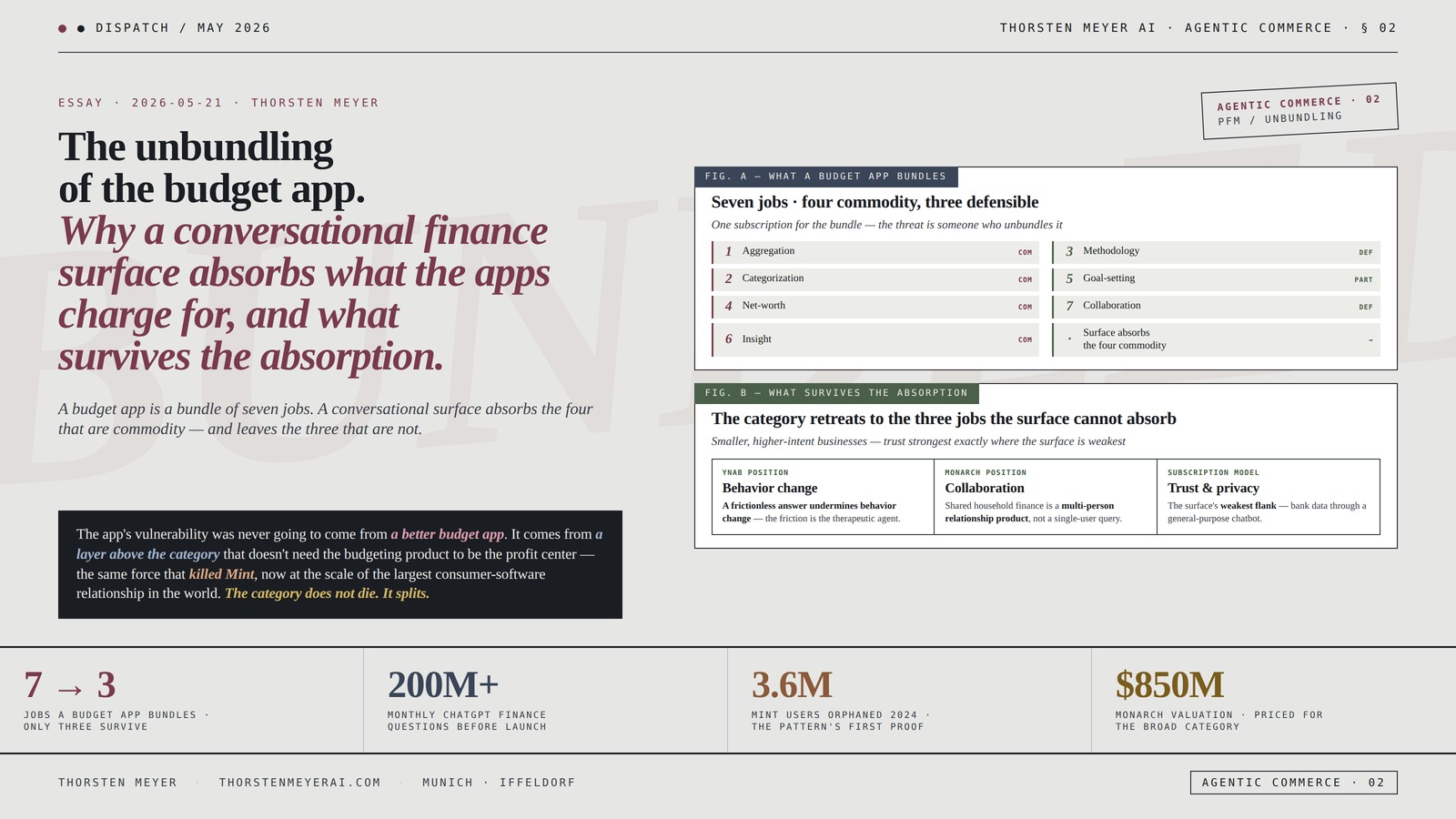

The structural argument I want to make: a personal-finance app is a bundle of seven distinct jobs, and a conversational AI surface with aggregator rails absorbs the commodity ones — aggregation, categorization, and insight — essentially for free, as a feature of a relationship it monetizes elsewhere. What it does not absorb easily are the three jobs that require friction, relationship, or trust: behavior change, household collaboration, and the privacy promise. The unbundling does not kill the category. It splits it.

The headline integrative finding: The middle of the personal-finance-app market — the “good-enough dashboard you check less than you expected” — is the part that gets hollowed out, because that is precisely the part a conversational surface does better at zero marginal cost. What survives is the high-friction behavioral tier (YNAB), the relationship tier (Monarch for couples), and the trust tier (subscription apps that sell privacy) — and the cruel irony is that the trust tier’s strongest argument is the dimension where the conversational surface is structurally weakest.

This essay walks the category that rose from Mint’s grave, what a budget app actually bundles, the surface that absorbs the commodity layers, the ecosystem-bundling threat that predated the chatbot, the engagement inversion that breaks the dashboard model, what survives the absorption, and the structural reading of a category that splits rather than dies.

The unbundling

of the budget app.

Why a conversational finance

surface absorbs what the apps

charge for, and what

survives the absorption.

three survive the absorption

before the surface even launched

the pattern’s first demonstration

broad category, not the defensible one

- Aggregation · same Plaid integration, 12,000+ institutions

- Categorization · performed at the shared aggregator layer

- Net-worth & dashboard · generated as a side effect of connection

- Insight & explanation · the surface’s native strength, tuned to a finance benchmark

- Behavior change · requires friction the surface is built to remove

- Collaboration · multi-person workflow, not a single-user query

- Trust / privacy · the surface’s structurally weakest flank

- Action jobs · surface is read-only — for now

The category does not collapse into the chatbot. It splits into the part the surface absorbs and the part it cannot. The passive-dashboard middle hollows out. What survives is the behavior, the relationship, and the privacy promise a general-purpose surface can least credibly make.Thorsten Meyer · The Unbundling of the Budget App · Agentic Commerce 02

By Thorsten Meyer — May 2026

This is the second dispatch in the AI Agentic Commerce track. The first — The bank account in the chat — walked the launch of OpenAI’s personal-finance surface and the seven-tier intermediation map it implies. This piece narrows to one tier: the personal-finance-management app, the standalone subscription product that sits between the bank and the user, and whether it survives the surface that now sits above it.

The structural argument I want to make: the personal-finance app’s vulnerability was never going to come from a better personal-finance app. It comes from a layer above the category that does not need the budgeting product to be the profit center. Mint died not because a competitor out-budgeted it but because Intuit had a more valuable use for those users inside Credit Karma and TurboTax. The same logic now applies at a larger scale: the conversational AI surface monetizes the entire relationship, of which money management is one feature, and can therefore offer good-enough aggregation and insight at a price the standalone subscription app cannot match — eventually, zero.

The headline integrative finding: The category does not collapse into the chatbot. It separates into the part the chatbot absorbs and the part it cannot. The part it absorbs is the data-and-insight layer that most users engage with passively. The part it cannot absorb is the behavior-change ritual, the household relationship, and the privacy promise — the parts that require friction, trust, or a relationship that a general-purpose chatbot monetizing the broader relationship is poorly positioned to provide. The standalone apps that understand which part they are now survive. The ones still selling commodity aggregation do not.

This essay walks the category that rose from Mint’s grave (Section I), what a budget app actually bundles (Section II), the surface that absorbs the commodity layers (Section III), the ecosystem-bundling threat that predated the chatbot (Section IV), the engagement inversion that breaks the dashboard model (Section V), what survives the absorption (Section VI), and the structural reading of a category that splits rather than dies (Section VII).

I · The category that rose from Mint’s grave · the post-shutdown boom

The category-history crystallization. The current personal-finance-app market is, almost entirely, a product of one event: Intuit’s decision to shut down Mint in early 2024. Understanding what the category is requires understanding what rushed in to fill the vacuum.

The Mint vacuum

The shutdown: Intuit, which had acquired Mint in 2009, shut it down in early 2024 and steered users toward Credit Karma. At its peak, Mint served more than 3.6 million active users — a large, suddenly-unanchored population of people accustomed to free, ad-supported account aggregation and budgeting.

The structural lesson of Mint’s death: Mint was free because Intuit monetized it through advertising and lead-generation for credit products. When that model became less valuable than steering the same users into Credit Karma’s lending-and-tax monetization, Mint was expendable. Mint did not die because it was a bad budgeting product. It died because its owner had a more valuable use for its users. That is the pattern this entire essay is about.

Who filled the vacuum

Monarch Money: founded in 2018 by Val Agostino (a former Mint product manager) with Ozzie Osman and Jon Sutherland. Subscription-only from day one — no ads, no data sale — at $14.99/month or roughly $99/year. Grew its user base approximately twentyfold after Mint’s shutdown and raised a $75 million Series B at an $850 million valuation in May 2025, led by Forerunner Ventures and FPV Ventures, on roughly $95 million total raised. The positioning: the privacy-first, subscription-aligned successor to Mint.

YNAB (You Need A Budget): the zero-based-budgeting incumbent, priced around $109/year, with the steepest learning curve in the category and the strongest behavior-change claim. YNAB does not try to be a passive dashboard; it is a method that requires active participation.

Copilot Money: Apple-ecosystem only (iOS and Mac), with the category’s best AI auto-categorization and a design-forward aesthetic. A premium product for a specific platform population.

Empower Personal Dashboard (formerly Personal Capital): free aggregation, net-worth tracking, and investment analytics — offered as top-of-funnel for Empower’s wealth-management business. The budgeting is not the product; the assets-under-management relationship is.

Quicken Simplifi: the low-price tier at roughly $48/year, owned by Quicken (a private-equity-backed company), broad-enough coverage at half the headline price of Monarch.

Rocket Money (formerly Truebill): more than 10 million members, having saved users a reported $2.5 billion-plus through bill negotiation and subscription cancellation. Owned by Rocket Companies, the public mortgage lender — which means its distribution and bundling options are those of a large financial ecosystem, not a standalone app.

The two business models already in the category

The subscription-aligned model (Monarch, YNAB, Copilot, Simplifi): the user is the customer, the app sells no ads and no data, and the revenue is the subscription. This model’s integrity is its marketing — “you, not an advertiser, are the customer.”

The ecosystem-funnel model (Empower, Rocket Money, Credit Karma): the budgeting product is free or cheap because it is top-of-funnel for a more valuable monetization — wealth management, mortgage, lending, tax. The budgeting is the hook, not the business.

The category observation

The category that rose from Mint’s grave already contained the seeds of its own next disruption. The subscription-aligned apps were structurally exposed to anyone who could offer good-enough money management as a free feature of a broader relationship — exactly what the ecosystem-funnel players were already doing, and exactly what a conversational AI surface is now positioned to do at far greater scale. Mint’s death was the first demonstration of the pattern. The conversational surface is the second.

AI in Finance: Automate Stock, Crypto, and Budget Tracking: Build Smart AI Dashboards for Personal Investing and Forecasting

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · What a budget app actually bundles · the seven jobs

The decomposition crystallization. To understand what a conversational surface absorbs and what it does not, the personal-finance app has to be decomposed into the distinct jobs it performs. It is not one product; it is a bundle of seven.

The seven jobs

Job 1 · Account aggregation: connecting to the user’s banks, cards, and investment accounts and pulling balances and transactions into one place. Technically performed by aggregators — Plaid, Yodlee, Finicity (Mastercard) — that the app licenses. The app does not do this itself; it rents it.

Job 2 · Transaction categorization: turning cryptic bank-transaction strings into labeled, categorized spending. Increasingly an AI task, and increasingly performed by the aggregator itself rather than the app — Plaid’s transaction model identifies merchant identity and payment context from raw data.

Job 3 · Budgeting methodology: the actual system — zero-based (YNAB), flexible/needs-wants-savings (Monarch), envelope (Goodbudget). This is the part that requires the user to do something, and the part that produces behavior change if any does.

Job 4 · Net-worth and investment tracking: aggregating assets and liabilities into a net-worth figure and tracking portfolio performance. Empower’s core. Largely a display-and-calculation job once the aggregation exists.

Job 5 · Goal setting and planning: defining targets (house, emergency fund, debt payoff) and tracking progress toward them. A combination of data and forward projection.

Job 6 · Insight and explanation: the “why am I always broke two days before payday” layer — surfacing patterns, flagging anomalies, answering questions about the data. The fastest-growing part of every app’s pitch and the most directly AI-shaped.

Job 7 · Collaboration: shared access for couples, households, and financial advisors. Monarch’s distinguishing strength. A relationship product, not a data product.

Which jobs are commodity and which are defensible

Commodity jobs (the app rents or the AI does trivially): aggregation (Job 1, rented from Plaid), categorization (Job 2, increasingly done by the aggregator), net-worth display (Job 4, calculation on aggregated data), and insight/explanation (Job 6, the single most AI-native task in the bundle).

Defensible jobs (require friction, relationship, or trust): budgeting methodology (Job 3, because behavior change requires participation), goal-setting-as-commitment (Job 5, partially), and collaboration (Job 7, because it is a relationship product).

The decomposition observation

The personal-finance app charges a single subscription for a bundle of seven jobs, four of which are commodity and three of which are defensible. The subscription price is justified by the bundle. The threat is not that a competitor offers a better bundle. The threat is that someone unbundles it — absorbs the four commodity jobs into a surface that does not charge for them, and leaves the standalone app to justify its subscription on the three defensible jobs alone. That is precisely what a conversational AI surface does.

Clever Fox Budget Planner – Expense Tracker Notebook. Monthly Budgeting Organizer, Finance Logbook & Accounts Book, Bill Tracker, A5 (Black)

TAKE CONTROL OF YOUR MONEY & ACHIEVE YOUR FINANCIAL GOALS – Are you looking for the best monthly…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The surface that absorbs the commodity layers · what ChatGPT finance does

The absorption crystallization. OpenAI’s personal-finance surface, launched May 15, 2026, is a near-perfect machine for absorbing the four commodity jobs in the budget-app bundle. It performs them not as a product but as a feature of a conversation.

What the surface does

Aggregation (Job 1): through the same Plaid integration the apps use, across more than 12,000 institutions including Schwab, Fidelity, Chase, Robinhood, American Express, and Capital One. The surface rents the exact same rails the apps rent.

Categorization (Job 2): Plaid syncs and categorizes the data; the surface displays it. The categorization is performed at the aggregator layer that both the apps and the surface share.

Net-worth and dashboard (Job 4): once connected, the surface generates a dashboard of portfolio performance, spending, subscriptions, and upcoming payments — the Empower core, as a side effect of connection.

Insight and explanation (Job 6): the native strength. The surface answers “I feel like I’ve been spending more recently — has anything changed?” in conversation, grounded in the actual data, using a model OpenAI tuned against a finance-specific benchmark. The most AI-native job in the bundle is the surface’s home turf.

The Hiro tell

The acqui-hire: roughly one month before launch, OpenAI absorbed the team behind Hiro Finance — an AI personal-finance startup co-founded by Ethan Bloch (who had earlier founded the savings app Digit, acquired by Oportun in 2021 for more than $200 million), backed by Ribbit, General Catalyst, and Restive, which had helped clients manage more than $1 billion in assets. Hiro shut down its standalone app on April 20, 2026; about ten employees joined OpenAI to build consumer-finance capability inside ChatGPT.

Why this matters structurally: Hiro is the unbundling made literal. A standalone AI personal-finance app could not sustain itself as a standalone product, and its team’s value was realized by being absorbed into the conversational surface. The capability did not disappear — it relocated from a product you pay for into a feature of a relationship you already have. That is the entire thesis enacted in a single transaction.

What the surface deliberately does not do

Read-only: per OpenAI’s product lead, the surface’s access is read-only — it cannot move money, execute trades, or pay bills, and cannot see full account numbers. It absorbs the information jobs, not the action jobs. This is the current boundary, and the boundary will be the subject of every future dispatch in this track, because the seven-tier intermediation map from the first piece is precisely about how that boundary moves.

Not free yet: the surface is currently available only to ChatGPT Pro subscribers in the U.S. ($100-$200/month), with Plus ($20/month) access flagged as the next phase. This is the most important qualification in this piece: the absorption is not yet a free-versus-paid contest. It is a premium feature of a premium subscription. The structural threat is directional — the absorption gets cheaper and broader from here, not more expensive and narrower.

The absorption observation

The conversational surface absorbs the four commodity jobs in the budget-app bundle — aggregation, categorization, net-worth display, and insight — using the same aggregator rails the apps rent, as a feature of a relationship monetized elsewhere. The Hiro acqui-hire demonstrates the direction: standalone personal-finance capability migrating into the surface. The surface does not yet do the action jobs, and it is not yet free. Both of those are matters of time and product roadmap, not of structural possibility.

Finance (Quick Study Business)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The threat that predated the chatbot · ecosystem bundling

The pre-existing-threat crystallization. The most important thing to understand about the conversational surface is that it is not a new kind of threat. It is the largest instance of a threat the category already faced — and lost ground to — before ChatGPT had a finance feature at all.

The ecosystem-bundling players

Intuit / Credit Karma: when Intuit killed Mint, it steered users into Credit Karma, which it integrates with TurboTax and increasingly with year-round AI-driven financial guidance. Credit Karma does not need its budgeting proposition to match Monarch’s, because the monetization happens in lending, tax filing, and product recommendations. The budgeting is a hook for a more valuable relationship.

Rocket Money: owned by Rocket Companies, the public mortgage lender. Its 10 million-plus members and concrete, marketable value proposition (bill negotiation, subscription cancellation, savings automation) capture mass-market users before they ever look for a holistic planner. Rocket’s ownership gives it distribution and bundling options a standalone subscription app cannot match.

Empower: offers free aggregation and investment tracking as top-of-funnel for its wealth-management business. The free dashboard is subsidized by the assets-under-management relationship it is designed to produce.

The structural disadvantage this creates

The subscription-aligned app’s problem: a standalone app whose only revenue is the subscription cannot outspend, on customer acquisition, a player for whom the budgeting product is a loss-leader for lending, tax, mortgage, or wealth management. The ecosystem player can offer good-enough money management for free, or near-free, and make its money elsewhere. The subscription app has to charge for the thing the ecosystem player gives away.

The trust-concentration risk: the subscription app’s defense is its privacy promise — no ads, no data sale, the user is the customer. But that promise creates concentration risk: a single serious security incident, AI misstep, or perceived data misuse would damage a trust-positioned subscription app more severely than an ad-supported competitor, precisely because trust is the entire reason a user pays.

Where the conversational surface fits

The surface is the ecosystem-bundling threat at maximum scale. OpenAI does not need the finance feature to be a profit center any more than Intuit needed Mint to be one. The finance surface is a feature of the ChatGPT relationship — the same relationship 200 million people already bring financial questions to every month. The conversational surface is to the entire personal-finance-app category what Credit Karma was to Mint: a larger relationship that can absorb the budgeting job as a feature, monetized elsewhere.

The pre-existing-threat observation

The category was already losing the structural argument to ecosystem bundling before the chatbot arrived. Mint died of it. Empower and Rocket Money were already exploiting it. The conversational surface does not introduce a new threat — it scales the existing one to the size of the largest consumer-software relationship in the world. The subscription-aligned apps were always going to have to defend the question “why pay for this when an ecosystem gives it away?” The conversational surface just makes the question unavoidable.

privacy-focused subscription finance app

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The dashboard you stopped opening · the engagement inversion

The engagement crystallization. There is a behavioral fact about personal-finance apps that the industry knows and rarely advertises, and it is the single most important reason the conversational surface is dangerous to the category: most people stop opening the dashboard.

The passive-dashboard problem

The observed pattern: heavy users of aggregator-based apps frequently report that they check the app less than they expected to — because a passive dashboard reduces engagement rather than increasing it. The numbers are there whenever you look, which means you stop looking. The dashboard is a thing you have to decide to open, and the decision-to-open is exactly the friction that erodes the habit.

The contrast with active models: manual-entry users (the YNAB and envelope-method populations) report higher daily awareness, because the act of logging is itself a form of attention. The friction is the product. This is why YNAB’s behavior-change claim survives where passive dashboards’ do not.

Why the conversational surface inverts this

The dashboard model: the user must remember to open the app, navigate to the relevant view, and interpret the numbers. The burden of initiation is on the user. Engagement decays because initiation is friction.

The conversational model: the user asks a question — “can I afford this?” / “where did my money go this month?” / “am I on track for the house?” — at the moment the question arises, inside a surface they are already using for a dozen other things. The burden of initiation collapses, because the user is already there, and the question is answered in context rather than displayed for interpretation.

The structural inversion: the dashboard requires the user to go to the data and interpret it. The conversational surface brings the answer to the user at the moment of the question. For the large population that engages with money management passively — the population that “checks Monarch less than expected” — the conversational model is simply a better fit for how they actually behave.

What this does to the subscription justification

The subscription app’s implicit promise: pay us, and you will engage with your money. For the passive majority, that promise quietly fails — they pay, and then they don’t open the app. The conversational surface does not require them to engage on a schedule; it answers when asked. For the passive user, the conversational surface is not just cheaper. It is a better behavioral fit, which is worse news for the apps than the price difference.

The engagement observation

The passive dashboard was always the category’s weakest point, and the conversational surface attacks it precisely. The users who engage actively — the YNAB behavior-change population — are defensible, because their engagement is the product. The users who engage passively — the larger population that bought a dashboard and stopped opening it — are the ones the conversational surface absorbs most easily, because for them the conversational model is what they actually wanted: an answer when they have a question, not a dashboard they have to remember to open.

VI · What survives the absorption · behavior, collaboration, trust

The survival crystallization. The unbundling does not leave the category with nothing. It leaves it with the three jobs the conversational surface cannot easily absorb — and the apps that retreat to those jobs survive, while the apps still selling commodity aggregation do not.

Survivor 1 · Behavior change (the YNAB position)

The defensible claim: behavior change requires friction, ritual, and active participation. YNAB’s zero-based method works precisely because it makes the user assign every dollar — an act of attention the user performs, not a number the system displays. A frictionless conversational answer actively undermines the mechanism of behavior change, because the friction is the therapeutic agent.

Why the surface cannot absorb it: the conversational surface optimizes for removing friction — answering the question so the user does not have to work for the answer. That is the opposite of what behavior change requires. A method that changes habits cannot be delivered as a frictionless answer, because the friction is the method. YNAB’s moat is that it sells the thing the surface is structurally designed to eliminate.

Survivor 2 · Collaboration (the Monarch position)

The defensible claim: shared household finance — couples, families, advisor-client relationships — is a relationship product, not a data product. Monarch’s distinguishing strength is genuine collaborative access: both partners with equal access, shared goals, annotated transactions. This is a multi-person workflow, not a single-user query.

Why the surface cannot absorb it easily: a personal conversational surface is, by construction, personal — it answers the individual user’s questions about the individual user’s connected accounts. Multi-person shared financial workflow is not a natural fit for a single-user assistant, and the trust-and-permission structure of shared household money is a product in itself. Monarch’s collaboration, advisor channel (Monarch for Professionals at $14.99 per active client), and employer channel (Monarch at Work) are relationship distribution, not data display — the part of the bundle least exposed to absorption.

Survivor 3 · Trust and privacy (the subscription-model position)

The defensible claim: the subscription-aligned apps sell the promise that the user, not an advertiser, is the customer — no ads, no data sale. And here is the irony at the center of this piece: the trust dimension is precisely where the conversational surface is structurally weakest.

Why this is the surface’s weakest flank: bank data flowing through a general-purpose chatbot — even with read-only access, no visible full account numbers, and a 30-day deletion window — is a novel and, for many users, uncomfortable arrangement. A general-purpose AI company monetizing the broader relationship is, almost by definition, less able to make the clean “you are the customer, not the product” promise than a subscription app whose only revenue is the subscription. The subscription apps’ strongest argument — we sell you nothing but the product — is the argument the conversational surface can least credibly make.

The qualification: this is a strong argument for the population that values it and a weak argument for the population that does not. The 200 million people already asking ChatGPT financial questions every month have already demonstrated a willingness to discuss their finances with the surface. Trust is a real moat for the subset of users who prioritize it, and a moat that protects a smaller, higher-intent population than the one the apps currently serve.

The survival observation

The category survives by retreating to its defensible jobs: behavior change, collaboration, and trust. The apps that understand this — that stop selling commodity aggregation and start selling the friction, the relationship, and the privacy promise — survive as smaller, higher-intent, higher-margin businesses. The apps that keep selling “a nicer dashboard than your bank’s” do not, because the conversational surface gives that away as a feature of a relationship it monetizes elsewhere. The defensible jobs are real, but they support a smaller category than the one Mint’s death created.

VII · The structural reading · a category that splits, not dies

The synthesis crystallization. The conversational finance surface is routinely described as either a Mint-style extinction event for budgeting apps or as overhyped and easily survived. The structural reality is neither. The category splits into the part the surface absorbs and the part it cannot, and the split is the story.

Observation 1 · The middle hollows out

The empirical signal: the most-exposed segment is the “good-enough dashboard you check less than expected” — the passive-aggregation product that does the four commodity jobs adequately and the three defensible jobs weakly. This is the largest part of the current category by user count and the part the conversational surface absorbs most directly.

The forward shape: the middle hollows out. The passive-dashboard user migrates to the conversational surface, because for them the surface is cheaper (eventually free) and a better behavioral fit. The apps positioned in the middle — broad, passive, aggregation-first — face the Mint problem: a larger relationship can do their core job as a feature. The middle is where the absorption lands hardest.

Observation 2 · The behavioral tier and the relationship tier survive as smaller, higher-intent businesses

The empirical signal: YNAB’s behavior-change population and Monarch’s collaborative-household population are engaged for reasons the surface does not satisfy — friction and relationship, respectively. These populations are smaller and higher-intent than the passive middle.

The forward shape: the survivors are smaller, higher-margin, higher-intent businesses than the post-Mint boom suggested the category could support. A subscription app that retreats to behavior change or household collaboration is a good business — but a smaller one than a subscription app that tried to be the everything-dashboard for the mass market. The $850 million valuation that the post-Mint vacuum supported was priced for the broad category. The defensible category is narrower.

Observation 3 · The aggregator wins regardless

The empirical signal: Plaid is the rails for the apps and for the conversational surface. Whichever layer wins the user relationship, the aggregation underneath is rented from the same place. Plaid’s own framing — that more than half of Americans expect money management without AI to feel outdated, that a majority of AI-finance users report improved product evaluation — is a bet on the surface, but Plaid is paid either way.

The forward shape: the value migrates from the application layer (the app) toward the surface layer (the conversational assistant) and the infrastructure layer (the aggregator). The app — the thing in the middle — is the layer being squeezed from both directions: the surface absorbs its commodity jobs from above, and the aggregator owns the rails from below. The standalone PFM app is the classic disintermediation casualty: squeezed between the relationship that owns the user and the infrastructure that owns the data.

Observation 4 · The action boundary is the next battle

The empirical signal: the conversational surface is currently read-only — it absorbs the information jobs, not the action jobs (moving money, trading, paying bills). And Intuit integration is flagged as next, which would extend the surface from analysis into action: tax estimates, credit-approval odds, application submission.

The forward shape: the absorption so far is of the information layer; the action layer is the next frontier. When the surface can act — move money, optimize, execute — the intermediation question moves from “where do you look at your money” to “what acts on your money,” which is the higher-stakes tier the first dispatch in this track mapped. This piece is about the absorption of the information jobs. The absorption of the action jobs is a separate, larger dispatch — and the one the Intuit integration foreshadows.

What this is not

It is not an extinction event for the category. Behavior change, household collaboration, and trust-positioned privacy are real, defensible jobs that the conversational surface does not absorb. The category survives — smaller, more specialized, more defensible.

It is not a vindication of the conversational surface as superior. The surface is currently a premium feature of a premium subscription, read-only, US-only, and carries the novel discomfort of bank data flowing through a general-purpose chatbot. Its trust flank is its weakest, and the subscription apps’ privacy promise is a genuine moat for the population that values it.

It is not a prediction that any specific app dies. Monarch, YNAB, Copilot, and the others have specific defensible positions. The prediction is structural: the passive-aggregation middle hollows out, and the survivors are the apps that retreat to friction, relationship, or trust.

The synthesis observation

The unbundling of the budget app is the unbundling of a seven-job bundle by a surface that absorbs the four commodity jobs and leaves the three defensible ones. The category does not die; it splits. The passive-dashboard middle migrates to the conversational surface, which does that job better and eventually cheaper as a feature of a relationship it monetizes elsewhere. The behavioral tier, the relationship tier, and the trust tier survive as smaller, higher-intent businesses. And the aggregator underneath — Plaid — is paid regardless of which layer wins, because it owns the rails that both the app and the surface rent.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the personal-finance app that rose from Mint’s grave is now facing the exact force that killed Mint — a larger relationship that can do the core job as a feature — at the largest scale that force has ever operated. The apps that survive will be the ones that stop selling the dashboard and start selling the thing the dashboard was never able to deliver: the behavior change, the shared household relationship, and the privacy promise that a general-purpose surface monetizing the broader relationship can least credibly make.

That is the structural editorial question the unbundling sits on top of. It is the absorption of the commodity layers, not the death of the category. It is the hollowing of the middle, not the extinction of the whole. It is the migration of value from the app to the surface and the rails — from the thing in the middle to the relationship above it and the infrastructure below it. And it is the layer where the next phase of consumer fintech gets decided: not in whether the apps have good dashboards, but in whether they understand which of their seven jobs the surface above them cannot take.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Agentic Commerce track

This dispatch

- This piece · The unbundling of the budget app · why a conversational finance surface absorbs the commodity layers of personal-finance management and what survives the absorption · labor-rose dominant, alternative-sage and structural-slate balance

The track

- The bank account in the chat · Agentic Commerce 01 · the launch of OpenAI’s personal-finance surface and the seven-tier intermediation map · the direct predecessor to this piece

- Forthcoming · The European architecture · why PSD2/PSD3/FIDA and the EU AI Act mean the US conversational-finance rollout does not translate to Europe · structural-slate register

- Forthcoming · The action boundary · what happens when the conversational surface moves from read-only analysis to moving money, and the higher-stakes intermediation tier that opens · synthesis-deep register

- Forthcoming · The aggregator’s position · why Plaid wins regardless of which surface owns the user, and what owning the rails is worth · transition-bronze register

Adjacent tracks

- The CFO’s new operating system · Enterprise Reorg 01 · the enterprise-side mirror of this consumer-side unbundling — finance work absorbed into agentic surfaces

- The cleaner cap table · AI Governance 02 · the corporate structure of the company building the surface that does the absorbing

- The calendar technicality · AI Governance 01 · the IPO calendar that the consumer surface’s monetization is being built to support

Sources

The personal-finance-app category

- Monarch Money funding and scale — Series B May 2025: $75M at $850M valuation (Forerunner Ventures + FPV Ventures lead) · ~$95M total raised · founded 2018 by Val Agostino (ex-Mint PM), Ozzie Osman, Jon Sutherland · subscription-only $14.99/mo / ~$99/yr · ~20x user growth post-Mint · ~124-161 employees · Monarch for Professionals ($14.99/active client/mo) and Monarch at Work channels · Sacra · TechFundingNews · Connecting the Dots in Fintech

- Sacra · Monarch Money analysis — the structural-threat framing: the biggest threat is not another standalone budgeting app but large financial ecosystems (Intuit/Credit Karma, Rocket Companies, Empower) embedding personal finance as a feature within a broader monetization stack · trust-concentration risk for subscription-aligned apps · Rocket Money 10M+ members, $2.5B+ saved · sacra.com/c/monarch-money

- NerdWallet · Best Budget Apps 2026 — category overview: Monarch (flexible), YNAB (zero-based), Copilot (auto-categorization, Apple-only), Empower (free wealth + spending), Rocket Money, Quicken Simplifi · aggregators Plaid, Yodlee, Finicity (Mastercard) · nerdwallet.com

- Finny · Apps Like Monarch Money — the engagement-inversion observation: heavy aggregator-app users report checking the app less than expected because the passive dashboard reduces engagement, while manual-entry users report higher daily awareness because logging is a form of attention · getfinny.app

- Techno-Pulse · Best AI Personal Finance Tools 2026 — positioning by use case: YNAB for behavior change, Copilot for Apple-first AI categorization, Monarch for couples/households, Simplifi for low cost, Empower for free investment analytics · techno-pulse.com

The Mint precedent

- Mint shutdown — Intuit acquired Mint 2009, shut it down early 2024, steered users to Credit Karma · 3.6M+ peak active users · ad-and-lead-gen model made expendable once Credit Karma’s lending-and-tax monetization was more valuable · Credit Karma now integrated with TurboTax and AI-driven year-round guidance

The conversational finance surface

- TechCrunch · OpenAI launches ChatGPT for personal finance — launched May 15 2026 preview for Pro subscribers (US) · Plaid integration, 12,000+ institutions (Schwab, Fidelity, Chase, Robinhood, Amex, Capital One) · dashboard of portfolio/spending/subscriptions/upcoming payments · 200M+ monthly finance questions · GPT-5.5 reasoning · Intuit integration planned (tax-impact, credit-approval odds, application) · Hiro acqui-hire April 2026 · techcrunch.com

- TheStreet · ChatGPT cheapest financial advisor — Hiro Finance detail: co-founded by Ethan Bloch (2024), backed by Ribbit/General Catalyst/Restive, managed $1B+ assets, shut down standalone app April 20 2026, ~10 employees acqui-hired · Bloch previously founded Digit (acquired by Oportun 2021 for $200M+) · read-only access (Ty Geri, OpenAI), no money movement/trades/bills, no full account numbers · Pro $100-$200/mo ($1,200-$2,400/yr) · thestreet.com

- how2shout · ChatGPT personal finance preview — Financial memories layer separate from regular memory · 30-day deletion on disconnect · temporary chats exclude financial accounts · Plus tier next phase · US-only · how2shout.com

- Plaid · What ChatGPT’s new experience signals — Plaid as rails for the surface · transaction foundation model categorizes at the aggregator layer · 64% of AI-finance users report improved product evaluation, 53% report better day-to-day spending management · “more than half of Americans say managing money without AI will soon feel outdated” · Plaid paid regardless of which surface wins · plaid.com/blog

- Engadget · ChatGPT personalized financial advice — read-only scope (balances, transactions, investments, liabilities), no full account numbers, no account changes · disconnect anytime · data-controls settings apply · engadget.com

Adjacent dispatch backbone

- The bank account in the chat · Thorsten Meyer · Agentic Commerce 01 · the launch analysis and seven-tier intermediation map · the dashboard-vs-conversation inversion · the direct predecessor and structural frame for this piece

Key reference figures crystallized

- Mint: shut down early 2024 · 3.6M+ peak active users · steered to Credit Karma · the original demonstration of the ecosystem-bundling pattern

- Monarch: Series B May 2025 $75M at $850M · ~$95M raised · $14.99/mo / ~$99/yr · ~20x post-Mint growth · subscription-only, no ads, no data sale

- The category: YNAB (behavior change, ~$109/yr) · Copilot (Apple-only, AI categorization) · Empower (free dashboard, wealth funnel) · Simplifi (~$48/yr, PE-backed) · Rocket Money (10M+ members, $2.5B+ saved, Rocket Companies-owned)

- The seven jobs: aggregation · categorization · methodology · net-worth/investment · goals · insight · collaboration — four commodity (1,2,4,6), three defensible (3,5,7)

- The conversational surface: launched May 15 2026 · Pro-only ($100-$200/mo) · Plaid 12,000+ institutions · 200M+ monthly finance questions · read-only · Intuit integration next · Plus tier next

- The Hiro tell: acqui-hire April 2026 · Ethan Bloch (ex-Digit, $200M+ Oportun exit) · Ribbit/General Catalyst/Restive backed · $1B+ assets managed · standalone app shut down April 20 2026 · ~10 employees to OpenAI — the unbundling made literal

- The aggregator position: Plaid rails for both the apps and the surface · transaction foundation model categorizes at the aggregator layer · value migrates from app to surface and rails

- What survives: behavior change (YNAB) · collaboration (Monarch) · trust/privacy (subscription model) — the trust tier strongest where the surface is structurally weakest