The queue.

For two years the story of the AI buildout was a chip story — who had the GPUs, who could buy them, who could fabricate them. That story is over. The binding constraint is no longer silicon. It is the grid — and specifically, the line you wait in to connect to it.

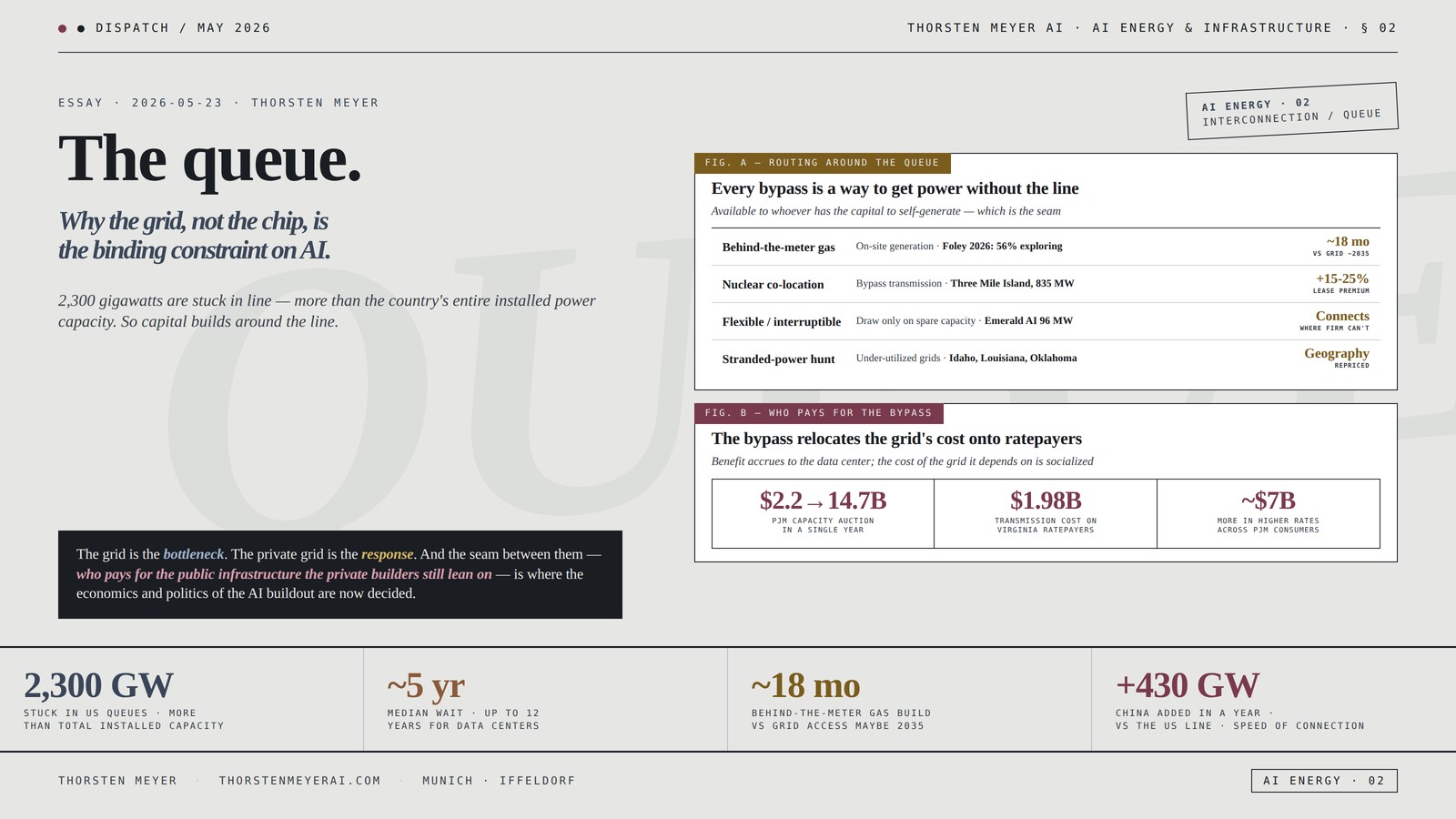

The number that defines the new constraint is the interconnection queue. Roughly 2,300 to 2,600 gigawatts of generation and storage capacity is currently stuck in US interconnection queues — more than the entire installed power capacity of the country. The median wait to reach commercial operation is approaching five years, up from under two in 2008; some data-center projects face quoted timelines of up to twelve. Nearly 80% of projects in the queue eventually withdraw.

The demand hitting that queue is unprecedented. US data-center power demand is projected to reach roughly 76 gigawatts in 2026, up from about 50 in 2024, and global data-center consumption could pass 1,000 terawatt-hours annually by the early 2030s, up from 460 in 2022. In Texas, CenterPoint reported a 700% increase in large-load interconnection requests in a single year — from 1 gigawatt to 8. Utilities including ComEd, PPL, and Oncor now report more gigawatts of data-center applications than their historical maximum peak demand.

So capital is routing around the queue. A behind-the-meter gas plant can be built in roughly 18 months; grid access for the same site might not arrive until 2035. Hyperscalers are co-locating at nuclear plants to claim baseload power while bypassing transmission entirely — Microsoft’s deal to restart Three Mile Island Unit 1 delivers 835 megawatts of carbon-free baseload. A Foley survey in 2026 found 56% of developers exploring co-located or on-site generation.

But the bypass has a cost, and it does not fall on the bypasser. When hyperscalers build private power and lean on the shared grid for backup, the transmission and capacity costs land on ratepayers. PJM’s capacity auction ballooned from $2.2 billion to $14.7 billion in a single year; in 2024, $4.3 billion of transmission costs to connect data centers in PJM were passed to ratepayers, with Virginia alone bearing $1.98 billion — a political flashpoint that produced a nonbinding White House “Ratepayer Protection Pledge” in March 2026.

The structural argument I want to make: the grid is the binding constraint on AI, and the industry’s response is to build a parallel private grid that solves time-to-power for whoever has the capital — and externalizes the cost of the shared grid onto everyone else. The interconnection queue does not stop the buildout. It bifurcates it: into the self-powered, who build now behind the meter or beside a reactor, and the grid-dependent, who wait in a five-to-twelve-year line.

The headline integrative finding: The queue reprices everything. It reprices geography — the “search for megawatts” now beats latency and fiber as the primary driver of where data centers go. It reprices the P&L — queue position is the most expensive line item, and power-certain sites command a 15-25% lease premium. And it reprices cost allocation — the bypass that solves the developer’s problem shifts the grid’s cost onto ratepayers, which is now the central political fight of the AI buildout. The constraint is real, the bypass is real, and the bill for the bypass is real — and it lands on people who are not building data centers.

This essay walks how the binding constraint moved from chip to grid, the anatomy of the queue, the demand wall hitting it, how capital routes around it, the parallel private grid being built, who pays for the bypass, and the structural reading of a buildout that bifurcates into the self-powered and the grid-dependent.

The queue.Why the grid, not the chip,

is the binding constraint on AI.

more than total installed capacity

up to 12 years for data centers

vs grid access maybe 2035

ratepayers · the cost-shift, concrete

in a single year

Virginia ratepayers (2024)

across PJM consumers

The grid is the bottleneck. The private grid is the response. And the seam between them — who pays for the public infrastructure the private builders still lean on — is where the economics and politics of the AI buildout are now decided.Thorsten Meyer · The Queue · AI Energy & Infrastructure 02

By Thorsten Meyer — May 2026

This is the second dispatch in the AI Energy & Infrastructure track. The first — The gigawatt gap — walked the US-China power-buildout asymmetry: Stargate’s $400-500 billion of planned capacity against a 2,300-gigawatt queue, PJM capacity prices running from $29 to $329 per megawatt-day, China adding roughly 430 gigawatts of capacity in a single year. This piece narrows to the specific mechanism inside that gap: the interconnection queue, the bureaucratic-and-physical chokepoint that turns abundant capital and available generation into a five-year wait.

The structural argument I want to make: the United States does not have a generation problem in the abstract — it has an interconnection problem. There is capital to build power, there is demand to consume it, and there are 2,300 gigawatts of projects that want to connect. What there is not is a fast path from “project” to “energized,” because the queue, the transmission system, the permitting process, and the transformer supply chain all move on timescales measured in years while AI capital moves on timescales measured in months. China adds 430 gigawatts a year; the US has 2,300 gigawatts stuck in line. The difference is not money or even generation — it is the speed of connection.

The headline integrative finding: Because the queue moves so much slower than the capital, the capital builds around it. The result is a privatization of power generation — behind-the-meter gas, co-located nuclear, on-site everything — that lets the best-capitalized players bypass the constraint entirely while the shared grid they still depend on for backup absorbs the cost. The grid is the bottleneck; the response is a private grid; and the seam between them — who pays for the transmission and capacity the private builders still lean on — is where the politics of the AI buildout now lives.

This essay walks the moved constraint (Section I), the anatomy of the queue (Section II), the demand wall (Section III), the routing-around (Section IV), the parallel private grid (Section V), who pays for the bypass (Section VI), and the structural reading of a bifurcated buildout (Section VII).

Tripp Lite SMART500RT1U UPS Smart 500VA 300W Rackmount AVR 120V USB DB9 SNMP 1URM (Rack-mountable) – AC 120 V – 300 Watt – 500 VA – Output connectors: 7-1U – Black

Power Device Type: UPS| UPS Technology: line-interactive| Voltage Output: AC 120 V| Voltage Input: AC 120 V| Power…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

I · The binding constraint moved · from chip to grid

The constraint-shift crystallization. Every buildout has one binding constraint — the thing that, if relaxed, lets everything else proceed. For AI, that constraint moved, and most of the discourse has not caught up.

The chip era

2021-2024: the constraint was compute. The questions were about GPU allocation, fab capacity, export controls, and who could secure the silicon. Partnerships in this era revolved around cloud integration, hardware supply, and software ecosystems. The implicit assumption was that if you had the chips and the capital, you could build the data center.

The grid era

2025-2026: the constraint is power, and more precisely, the ability to connect power to the load. Acute power constraints and interconnection bottlenecks are effectively closing the primary data-center markets to new large-scale development. The questions are now about megawatts, queue position, transmission upgrades, and time-to-power. Partnerships revolve around energy — securing a “spot in line,” co-developing grid upgrades, contracting generation directly.

The tell: the search for megawatts is now the primary driver of data-center geography, superseding latency, fiber, and tax incentives. When site selection is driven by where you can get power rather than where the network is fastest, the binding constraint has moved from compute to energy.

Why the grid is harder than the chip

The timescale mismatch: a fab takes years but is a known, financeable, replicable project. The grid is a shared, regulated, slow-moving public system whose expansion requires permitting across many jurisdictions, transmission upgrades that take years, and equipment with multi-year lead times. Chips can be manufactured faster than grids can be expanded, which is why the constraint moved to the grid the moment chip supply loosened.

The maturity gap: a critical gap has opened between the rapid innovation cycles of data-center technology and the slow, linear deployment pace of electrical-grid infrastructure. The data center can be designed, financed, and built in 18-24 months. The grid connection it needs can take five to twelve years. That gap is the single greatest constraint on the buildout.

The constraint-shift observation

The AI buildout is no longer gated by how many chips you can buy; it is gated by how fast you can connect power to them. The discourse still talks about GPUs, but the developers talk about megawatts and queue position, because that is where the actual constraint now lives. The binding constraint moved from a thing you manufacture to a thing you wait in line for — and the line is the subject of this piece.

Gettysburg and Stories of Valor – The Civil War

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · Anatomy of the queue · why it takes five years

The mechanism crystallization. The interconnection queue is not one bottleneck. It is four compounding bottlenecks stacked on a process that was designed for a slower era, and understanding why it is slow is necessary to understand why the bypass exists.

What the queue is

The function: before any new generation or large load can connect to the grid, it must pass through an interconnection study process that assesses the impact on grid stability and assigns the cost of any necessary upgrades. The queue is the line of projects waiting for that study and the upgrades it identifies.

The scale: roughly 2,300-2,600 gigawatts of capacity is in the queue — more than the entire installed generating fleet of the United States. About 95% of it is solar, wind, or storage. The queue contains more than a doubling of the nation’s power capacity, waiting to connect.

The four compounding factors

Factor 1 · Utility study backlogs: the volume of requests has far outpaced what utilities have ever processed. The studies are sequential, complex, and under-resourced for the current volume. A request can wait years just to be studied.

Factor 2 · Transmission upgrade requirements: many projects, once studied, require transmission upgrades to connect — new substations, new lines, reconductoring. These upgrades take years and their cost is contested.

Factor 3 · Permitting complexity: transmission and generation both require permits across multiple jurisdictions, each with its own timeline and veto points. Permitting is increasingly the binding step even when the study is fast.

Factor 4 · Equipment lead times: high-voltage transformers and other grid equipment now have multi-year lead times. Even an approved project can wait years for the physical hardware to connect it. The bottleneck has begun shifting from the study process to the supply chain for physical infrastructure.

The withdrawal problem

The 80% number: nearly 80% of projects that enter the queue eventually withdraw. The queue is clogged with speculative and non-viable projects that occupy study slots without intending to build, slowing the viable projects behind them. The queue is both too long and full of phantom demand, which makes the real wait worse than the raw numbers suggest.

The reform attempt

FERC Order 2023: issued in mid-2023 and affirmed in 2024, it replaced the old serial “first-come, first-served” queue with a “first-ready, first-served” cluster model — studying viable, ready projects in batches rather than one at a time. The reform is real and helps, but it addresses the study process, not the transmission, permitting, or equipment bottlenecks that increasingly dominate. Analysts note that even with faster studies, projects remain stalled — validating the view that the long-term fix is building a larger grid, not just managing the queue more cleverly.

The anatomy observation

The queue is slow because four bottlenecks compound on a process built for a slower era, and the easiest one to fix — the study backlog — is the one the reform addresses, while the harder ones — transmission, permitting, transformers — increasingly dominate. Lawrence Berkeley National Laboratory’s data shows interconnection wait times have more than doubled in fifteen years. The queue is not a temporary congestion that clears; it is a structural mismatch between the speed of demand and the speed of the system that connects it.

IronBox Electric – NEMA L15-30 Extension Power Cord – Rated for 30A/250V – Heavy Duty 8/4 SOOW Cable – Power Cable for Generators, RVs, PDUs & Data Centers – Ideal for Indoor and Outdoor Use (6 Feet)

HEAVY DUTY 8/4 SOOW CONSTRUCTION FOR DURABILITY: Built with rugged 8/4 SOOW cable and a L15-30P to L15-30R…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The demand wall · what is hitting the queue

The load crystallization. The queue would be manageable if demand were growing at its historical pace. It is not. The demand hitting the queue is unlike anything the grid has planned for.

The numbers

US data-center power demand: roughly 76 gigawatts projected for 2026, up from about 50 in 2024 — a step-change, not a trend.

Global data-center consumption: could exceed 1,000 terawatt-hours annually by the early 2030s, up from 460 in 2022. Global AI data-center consumption alone is expected to reach about 90 terawatt-hours annually by 2026.

The capacity gap: Grid Strategies estimates the US needs more than 150 gigawatts of additional capacity within five years, by 2030, driven by AI, manufacturing reshoring, electrification, and the retirement of aging generation.

The scale of individual loads

Hyperscale density: hyperscale data centers (100+ megawatts) now account for roughly 41% of worldwide data-center capacity. Campuses drawing 300-600 megawatts — the consumption of a mid-size city — are routine in the development conversation. Sites of 1 gigawatt or more — the output of a large nuclear unit — are now being explored by single developers for single campuses.

The utility shock

The CenterPoint number: in Texas, CenterPoint reported a 700% increase in large-load interconnection requests in a single year, from 1 gigawatt to 8. A single utility saw its large-load pipeline grow eightfold in twelve months.

The peak-demand inversion: utilities including ComEd, PPL, and Oncor now report more gigawatts of data-center applications than their historical maximum peak demand. The new load requests exceed the total peak the utility has ever served — meaning a single category of new customer is asking for more power than the entire system was ever built to deliver at once.

Why the grid cannot absorb it

The structural problem: the power system does not have enough spare transmission capacity and generation to serve dozens of gigawatts of new, high-utilization, always-on demand. Data centers run near 100% utilization — they are not peaky loads that can be served from reserve margin; they are constant baseload that requires firm, dedicated capacity. The grid was built for diversified, variable demand, not for single sites asking for a nuclear plant’s worth of constant power.

The demand-wall observation

The demand hitting the queue is a step-change in scale, density, and utilization that the grid was not designed for, arriving faster than the queue can process it. A single data-center campus can now request more power than a utility’s historical peak. This is why the queue is not clearing and will not clear on the current trajectory — the demand is growing faster than the system that connects it can possibly expand. That is the wall the bypass is built to climb over.

The Saltwater Battery Guide: Sustainable Solution for Renewable Energy Storage (DIY Sustainable Projects)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · Routing around the queue · the bypass

The adaptation crystallization. Faced with a five-to-twelve-year queue and AI projects generating billions in annual revenue that cannot wait, capital does what capital does: it routes around the constraint.

Behind-the-meter generation

The model: behind-the-meter (BTM) generation places power production on or adjacent to the data-center site, consumed directly, bypassing the grid interconnection entirely or supplementing it. The generation sits, literally, behind the utility meter.

The speed advantage: a BTM gas plant can be built in roughly 18 months, against grid access that might not arrive until 2035. For an AI project generating billions a year, time-to-power is the whole game — an 18-month private plant beats a decade-long queue regardless of cost. The Foley 2026 survey found 56% of developers exploring co-located or on-site generation, the third most common strategy after PPAs and securing early grid interconnection.

The technologies: natural gas turbines and reciprocating engines (the most accessible near-term option), fuel cells, solar-plus-storage, and increasingly co-located or campus-adjacent power plants. Midstream gas companies are pivoting from being wholesale transporters to being direct, on-site power providers — building a parallel, private energy infrastructure dedicated to AI.

Nuclear co-location

The model: tie a data center directly to an operating or restarting nuclear plant — claiming massive blocks of carbon-free baseload power while bypassing the transmission queue entirely.

The flagship deal: Microsoft’s 20-year PPA to restart Three Mile Island Unit 1 (the Crane Clean Energy Center), back online in late 2024, delivering 835 megawatts of carbon-free baseload. Nuclear is the only dispatchable clean option with the scale characteristics hyperscalers require, and existing-plant restarts plus future SMRs are becoming a core pillar of hyperscale energy strategy.

The pricing signal: power-certain sites — those with a credible nuclear-backed interconnection on a compressed timeline — command a 15-25% lease premium over grid-constrained alternatives. Land within a 20-mile radius of operating or restarting nuclear plants is attracting meaningfully higher valuations. Power certainty is now the primary differentiator in site selection, and the market is pricing it explicitly.

Flexible and interruptible load

The model: design the data center to draw from the grid only when spare capacity is available, using on-site generation or storage otherwise — turning the load from a firm demand into a flexible one the grid can accommodate without new capacity.

The example: the Nvidia-backed Emerald AI 96-megawatt data center in Manassas, Virginia, designed to draw from the grid only when spare capacity exists, demonstrating the interruptible-load model. Flexibility is itself a way around the queue — an interruptible load can connect where a firm one cannot.

Geographic diversification

The stranded-power hunt: developers are hunting “stranded power” — existing generating capacity not fully allocated — and diversifying into emerging markets (Idaho, Louisiana, Oklahoma) where grids are not yet overwhelmed, even where fiber and other infrastructure are less mature. The established hubs (Northern Virginia) are closing to new large-scale development; the megawatts are now in places the data-center industry never used to consider.

The routing-around observation

Every form of the bypass — behind-the-meter gas, nuclear co-location, flexible load, stranded-power hunting — is a way to get power without waiting in the queue. The common thread is time-to-power: an 18-month private plant or a nuclear co-location beats a decade-long queue, and the best-capitalized players are choosing to build their own power rather than wait for the shared grid. The bypass is rational, it is fast, and it is available only to those with the capital to self-generate — which is the seam the rest of this piece is about.

V · The parallel private grid · the privatization of power

The infrastructure crystallization. The sum of all the bypasses is something larger than a collection of workarounds. It is the construction of a parallel, private energy infrastructure alongside the public grid — and that is a structural change in how power is built and owned.

The scale of private procurement

Hyperscaler buying: Microsoft has surpassed Amazon as the world’s largest corporate clean-power buyer, with roughly 40 gigawatts contracted as of late 2025 — a portfolio spanning the Constellation nuclear restart, a Brookfield framework for 10.5 gigawatts of new renewables, investments in fusion (Helion) and SMRs, and natural-gas contracts for firm backup. Amazon, Meta, Google, and Microsoft together accounted for roughly half of all global clean-energy purchase agreements signed in 2025, and the four spent over $200 billion in capital expenditure in 2024.

The shift in counterparty: power partnerships used to be between utilities and their regulated customers. Increasingly they are between hyperscalers and independent power producers, midstream gas companies, and nuclear operators — direct, private, bilateral deals that bypass the regulated utility model. The largest buyers of power are no longer utilities serving the public; they are technology companies serving themselves.

What “private grid” means

The integrated model: a hyperscale campus increasingly draws from three sources converging at its own switchgear — the utility grid, on-site behind-the-meter generation, and dedicated PPAs. The most aggressive developers build the generation, the storage, and the data center as a single integrated private system, using the public grid only as backup or not at all. Physical-Infrastructure-as-a-Service offerings now bundle on-site gas plants with pre-permitted, construction-ready data-center sites — selling time-to-power as a product.

The midstream pivot: gas companies that used to transport fuel to power plants now build and operate the power plants on-site, providing fuel and electricity as a single service. The energy industry is reorganizing around serving private AI load directly, outside the regulated-utility framework.

The bridge-versus-permanent debate

The 2026 reframing: through 2025, behind-the-meter gas was pitched as a primary solution. In 2026, the framing shifted to gas as a bridge to the grid, not a permanent replacement — a stopgap until grid access arrives or cleaner on-site options scale. But “bridge” and “permanent” look identical for the years the bridge is load-bearing, and the bridge framing does not eliminate the growth in gas demand tied to AI. The private generation is being built now, whatever it is called later.

The private-grid observation

The bypass is not a set of one-off workarounds; it is the construction of a parallel private energy system owned by the largest technology companies, alongside and increasingly independent of the public grid. The hyperscalers are now the largest power buyers in the world, contracting directly with generators outside the utility model. The privatization of power generation for AI is the structural event the queue produced — and it raises the question the public grid cannot avoid: if the biggest players build their own power, who pays for the shared grid they still depend on?

VI · Who pays for the bypass · the cost-shift

The cost-allocation crystallization. The bypass solves the developer’s problem. It does not eliminate the cost of the grid — it relocates who bears it. And that relocation is now the central political fight of the AI buildout.

The PJM cost explosion

The capacity-auction number: PJM’s capacity auction ballooned from $2.2 billion to $14.7 billion in a single year, driven largely by the demand surge and slow interconnections. The earlier dispatch noted PJM capacity prices running from $29 to $329 per megawatt-day. Consumers in the PJM region will pay up to $7 billion more in higher rates — costs driven by data-center demand but spread across all ratepayers.

The transmission cost-shift

The Virginia flashpoint: in 2024, $4.3 billion of transmission costs to connect data centers in PJM were passed directly to ratepayers, with Virginia alone bearing $1.98 billion. The residents of Virginia are paying nearly two billion dollars to connect data centers they do not own and whose power they do not consume. This is the cost-shift made concrete, and it is a political flashpoint now embedded in future regulation.

The mechanism of the shift

How the cost lands on ratepayers: when a data center connects to the grid (or leans on it for backup), the transmission and capacity upgrades it triggers are often socialized across all ratepayers under existing cost-allocation rules. The data center captures the benefit of the connection; the ratepayer base absorbs the cost of the upgrade. When the data center self-generates behind the meter but still relies on the grid for backup and reliability, it can avoid much of the cost while retaining the benefit — the bypass at its most extractive.

The political response

The Ratepayer Protection Pledge: in early March 2026, leading hyperscalers met at the White House and agreed to a nonbinding pledge to shoulder the electricity-generation costs associated with their data centers. The pledge is a recognition that the cost-shift is politically untenable — but it is nonbinding, and it covers generation, not necessarily the transmission and capacity costs that are the larger ratepayer burden.

The regulatory direction: Clean Transition Tariffs and similar mechanisms are emerging to provide data centers dedicated clean resources without cost-shifts to other customers. The regulatory fight is about forcing the data centers to bear their own grid costs rather than socializing them — and the outcome determines whether the AI buildout is subsidized by ratepayers or paid for by its beneficiaries.

The tax-credit dimension

The clean-energy credits: projects missing 2026-2028 start dates for the 45Y and 48E clean-energy credits face cost increases of 30-50%. The federal subsidy structure is itself a timing pressure that interacts with the queue — a project stuck in the queue past the credit deadline becomes dramatically more expensive, compounding the incentive to bypass the queue entirely.

The cost-shift observation

The bypass solves time-to-power for the developer and relocates the grid’s cost onto ratepayers, which is the central equity problem of the AI buildout. Virginia’s $1.98 billion, PJM’s $7 billion in higher rates, the White House pledge — these are the visible edges of a structural transfer: the benefit of the connection accrues to the data center, and the cost of the grid it depends on is socialized. The politics of AI energy is not really about whether to build — it is about who pays for the grid the buildout requires, and the answer is currently “everyone, whether or not they benefit.”

VII · The structural reading · a buildout that bifurcates

The synthesis crystallization. The interconnection queue is told two ways: as a temporary bottleneck that reform will clear, or as a hard ceiling that will stall AI. The structural reality is neither. The queue bifurcates the buildout, and the bifurcation is the story.

Observation 1 · The grid is the binding constraint, and it is structural, not cyclical

The empirical signal: 2,300-2,600 gigawatts stuck, five-year median waits, 80% withdrawal, wait times more than doubled in fifteen years, the bottleneck shifting from studies to transmission and transformers. This is not congestion that clears; it is a speed mismatch between demand and the system that connects it.

The forward shape: the queue does not clear on the current trajectory, because demand is growing faster than the grid can expand, and the hardest bottlenecks — transmission, permitting, transformers — are the ones reform addresses least. The constraint is structural and will persist through the decade. The fix is building a larger grid, which takes the kind of time AI capital does not have.

Observation 2 · The bypass bifurcates the buildout into the self-powered and the grid-dependent

The empirical signal: behind-the-meter gas (18 months), nuclear co-location (835 MW bypassing transmission), flexible load, stranded-power hunting — all available to the best-capitalized, none available to those without the capital to self-generate.

The forward shape: the buildout splits into two classes. The self-powered — hyperscalers and well-funded developers who build behind the meter or co-locate at reactors — proceed now. The grid-dependent — everyone who must wait in the queue — proceed in five to twelve years, or not at all. The queue does not stop AI; it concentrates AI in the hands of those who can afford to bypass it. The constraint is a moat: the ability to self-generate is now a competitive advantage as decisive as access to chips or capital.

Observation 3 · The privatization of power shifts cost to the public

The empirical signal: hyperscalers are the largest power buyers in the world, building private generation while the shared grid absorbs the transmission and capacity cost — Virginia’s $1.98 billion, PJM’s $7 billion, the nonbinding White House pledge.

The forward shape: the parallel private grid lets its builders avoid the cost of the shared grid they still depend on for backup, and that cost lands on ratepayers unless regulation forces otherwise. The Clean Transition Tariff fight, the Ratepayer Protection Pledge, and the Virginia flashpoint are the opening moves in a long regulatory battle over cost allocation. The outcome determines whether AI’s power demand is paid for by AI’s beneficiaries or subsidized by the public — and the default, absent regulation, is subsidy.

Observation 4 · The constraint reprices geography, the P&L, and cost allocation simultaneously

The empirical signal: the search for megawatts beats latency in site selection; queue position is the most expensive line item; power-certain sites command 15-25% premiums; the cost-shift is a political flashpoint.

The forward shape: the queue reprices the entire data-center value chain. Geography moves to where the power is (Idaho, Louisiana, nuclear-adjacent land). The P&L is dominated by time-to-power and queue position. And cost allocation becomes the central regulatory and political question. Every layer of the buildout — where, how fast, how expensive, who pays — is now downstream of the queue. The constraint that moved from chip to grid did not just slow the buildout; it reorganized its economics, its geography, and its politics around a single bottleneck.

What this is not

It is not a hard ceiling on AI. The bypass is real and effective; the best-capitalized players are building now. AI is not stalling — it is concentrating in the hands of those who can self-generate.

It is not a temporary congestion that reform clears. FERC Order 2023 helps with studies, but the binding bottlenecks — transmission, permitting, transformers — are structural and persist. The queue is a decade-long condition, not a passing jam.

It is not a free bypass. The private grid externalizes the cost of the shared grid onto ratepayers, and the politics of that transfer — Virginia, the White House pledge, the tariff fights — is the central unresolved question of the buildout.

The synthesis observation

The binding constraint on AI moved from the chip you manufacture to the grid you wait in line for, and the industry’s response is to build a parallel private grid that bypasses the line for whoever has the capital. The queue does not stop the buildout; it bifurcates it into the self-powered and the grid-dependent, reprices geography and the P&L around time-to-power, and shifts the cost of the shared grid onto ratepayers who do not benefit. The grid is the bottleneck. The private grid is the response. And the seam between them — who pays for the public infrastructure the private builders still lean on — is where the economics and the politics of the AI buildout are now being decided.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that China adds 430 gigawatts of capacity a year while the United States has 2,300 gigawatts stuck in a five-year line — and the difference is not capital, not generation, not even chips, but the speed of connection. The country that solves interconnection wins the buildout. The country that does not watches its best-capitalized companies build private grids around the public one, and watches its ratepayers pay for the public grid those companies left behind.

That is the structural editorial question the queue sits on top of. It is a binding constraint, not a passing jam. It is a bifurcation into the self-powered and the grid-dependent, not a uniform slowdown. It is a cost shifted onto ratepayers, not a free bypass. And it is the layer where the next phase of the AI buildout gets decided — not in how many chips ship, but in how fast power can be connected, who can afford to build their own, and who pays for the grid that everyone still depends on.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Energy & Infrastructure track

This dispatch

- This piece · The queue · why the grid, not the chip, is the binding constraint on AI — and why the bypass bifurcates the buildout into the self-powered and the grid-dependent · structural-slate dominant, transition-bronze and labor-rose balance

The track

- The gigawatt gap · AI Energy & Infrastructure 01 · the US-China power-buildout asymmetry, Stargate’s $400-500B, the 2,300 GW queue, PJM capacity pricing, China’s 430 GW/year · the direct predecessor to this piece

- Forthcoming · The transformer bottleneck · why high-voltage equipment lead times are becoming the binding constraint inside the constraint · empirical-clay register

- Forthcoming · The nuclear premium · what power-certainty pricing and the SMR buildout mean for the geography of AI · alternative-sage register

- Forthcoming · The ratepayer fight · the regulatory battle over cost allocation and whether AI’s power demand is subsidized or self-funded · labor-rose register

Adjacent tracks

- The cleaner cap table · AI Governance 02 · the corporate structure of the labs whose compute demand drives this power constraint — including Anthropic’s SpaceX 300 MW / 220,000 GPU agreement

- The CFO’s new operating system · Enterprise Reorg 01 · the capital-deployment engine funding the buildout this power constraint gates

- The pyramid cracks · Enterprise Reorg 02 · the labor-side reorganization running parallel to this infrastructure-side one

Sources

The interconnection queue

- Hanwha Data Centers · Data Center Grid Limitations — nearly 2,300 GW stuck in US interconnection queues, more than the country’s entire installed power capacity · four compounding factors (utility study backlogs, transmission upgrades, permitting, equipment lead times) · LBNL: wait times more than doubled over 15 years, ~5-year average · CenterPoint 700% increase (1→8 GW in a year) · stranded-power hunting (Idaho, Louisiana, Oklahoma) · hanwhadatacenters.com

- EnkiAI · Grid Interconnection Delays 2026 — queue swelled to 2,600 GW · median ~5-year wait, data centers up to 12 years · nearly 80% of projects withdraw · bottleneck shifting from study process to permitting and transformer supply chains · FERC reform 2025 implementation · enkiai.com

- Global Data Center Hub · The Interconnection Bottleneck — PJM capacity auction $2.2B → $14.7B in a single year · consumers up to $7B more · 2024 $4.3B transmission costs to connect data centers passed to ratepayers, Virginia $1.98B · ~95% of backlog solar/wind/storage · 45Y/48E credits, 30-50% cost increase for missing 2026-2028 start dates · FERC Order 2023 “first-ready, first-served” cluster model · queue time <2 years (2008) → ~5 years · globaldatacenterhub.com

- Camus Energy · Why It Takes So Long — CenterPoint 700% increase · ComEd, PPL, Oncor reporting more GWs of data-center applications than historical maximum peak demand · the system lacks spare transmission and generation for dozens of GWs of high-utilization demand · camus.energy

The demand wall

- PowerMag · Data Centers and the Grid — global data-center consumption could exceed 1,000 TWh annually by early 2030s (up from 460 TWh in 2022) · hyperscale (100+ MW) ~41% of worldwide capacity · 300-600 MW campuses routine, 1 GW+ sites being explored · the power paradox: availability determines where, how fast, how large · powermag.com

- Energy IB · The Data Center Power Boom — US data-center demand ~76 GW by 2026 (from ~50 GW 2024) · global AI consumption ~90 TWh by 2026 · Microsoft 40 GW contracted (world’s largest clean-power buyer), Brookfield 10.5 GW framework, Helion fusion, SMRs, gas backup · big four ~half of 2025 global clean PPAs, $200B+ capex 2024 · ibinterviewquestions.com

- Novogradac — Grid Strategies (Nov 2025): >150 GW additional capacity needed within 5 years by 2030, driven by AI, reshoring, electrification, retiring generation · GridLab/Aurora analysis on queue-build shortfall · novoco.com

The bypass

- Natural Gas Intel · On-Site Gas Gains Favor — BTM gas plant buildable in ~18 months vs grid access maybe 2035 · 2026 reframing of gas as bridge-to-grid not permanent · Nvidia-backed Emerald AI 96 MW Manassas VA, interruptible/flexible load drawing from grid only when spare capacity available · naturalgasintel.com

- DataCenterHawk · Behind-the-Meter Power — BTM definition (generation on/adjacent to site, bypassing grid) · technologies (gas turbines, fuel cells, solar+BESS, co-located plants) · Foley 2026 survey: 56% of developers exploring co-located/on-site (3rd most common strategy) · gas-as-bridge framing · datacenterhawk.com

- DataCenterKnowledge · Why Data Centers Produce Their Own Power — Bloom Energy March 2026 survey: time-to-power ~1.5-2 years longer than expected · White House early-March 2026 Ratepayer Protection Pledge (nonbinding) · interconnection queues stretched, boosting on-site appeal · datacenterknowledge.com

- LandGate · Behind the Meter vs The Grid — PJM and ERCOT queues 4-7 years · BTM moved from niche to strategic necessity · nuclear co-location bypassing transmission queue (Three Mile Island restart) · Constellation/Microsoft 835 MW · landgate.com

- Build.inc · Nuclear Power for Data Centers — Constellation/Microsoft 20-year PPA (Sept 2023) restarting Three Mile Island Unit 1, online late 2024, 835 MW carbon-free baseload · power-certain sites 15-25% lease premium · land within 20-mile radius of nuclear plants attracting higher valuations · nuclear the only dispatchable clean baseload at hyperscale scale · build.inc

- Gas-to-Power Boom (EnkiAI) — midstream gas pivot from transporters to on-site power providers · parallel private energy infrastructure · BTM bypasses congested public grid, ~18-month build · enkiai.com

The energy-infrastructure backbone

- The gigawatt gap · Thorsten Meyer · AI Energy & Infrastructure 01 · Stargate $400-500B, the 2,300 GW queue, PJM $29→$329/MW-day, China’s 3.89 TW installed / 430 GW added in 2025 · the US-China power-buildout asymmetry · the dispatch this piece narrows into

Key reference figures crystallized

- The queue: 2,300-2,600 GW stuck (more than total US installed capacity) · ~5-year median wait (up to 12 for data centers) · ~80% withdrawal · ~95% solar/wind/storage · wait times >2x in 15 years (LBNL) · FERC Order 2023 cluster reform

- The four factors: utility study backlogs · transmission upgrades · permitting · equipment (transformer) lead times

- The demand: US data-center ~76 GW by 2026 (from ~50 GW 2024) · global AI ~90 TWh by 2026 · global data-center >1,000 TWh by early 2030s (from 460 TWh 2022) · >150 GW needed by 2030 · hyperscale (100+MW) ~41% of capacity · 1 GW+ single-campus sites

- The utility shock: CenterPoint 700% (1→8 GW in a year) · ComEd/PPL/Oncor applications exceed historical peak demand

- The bypass: BTM gas ~18 months vs grid ~2035 · Foley 2026 survey 56% exploring on-site · Bloom March 2026 time-to-power +1.5-2 years · Emerald AI 96 MW interruptible · TerraVolt SE Idaho 200-240 MW

- Nuclear: Constellation/Microsoft Three Mile Island Unit 1 restart, 835 MW, 20-year PPA, online late 2024 · power-certain sites 15-25% lease premium

- Hyperscaler procurement: Microsoft 40 GW (world’s largest), Brookfield 10.5 GW, Helion, SMRs · big four ~half of 2025 global clean PPAs · $200B+ capex 2024

- The cost-shift: PJM capacity auction $2.2B → $14.7B · consumers up to $7B more · 2024 $4.3B transmission to ratepayers, Virginia $1.98B · White House Ratepayer Protection Pledge (nonbinding, March 2026) · 45Y/48E credits, 30-50% cost increase for missing 2026-2028 dates

- The China contrast: China ~430 GW/year added vs US 2,300 GW stuck in queue — the difference is the speed of connection