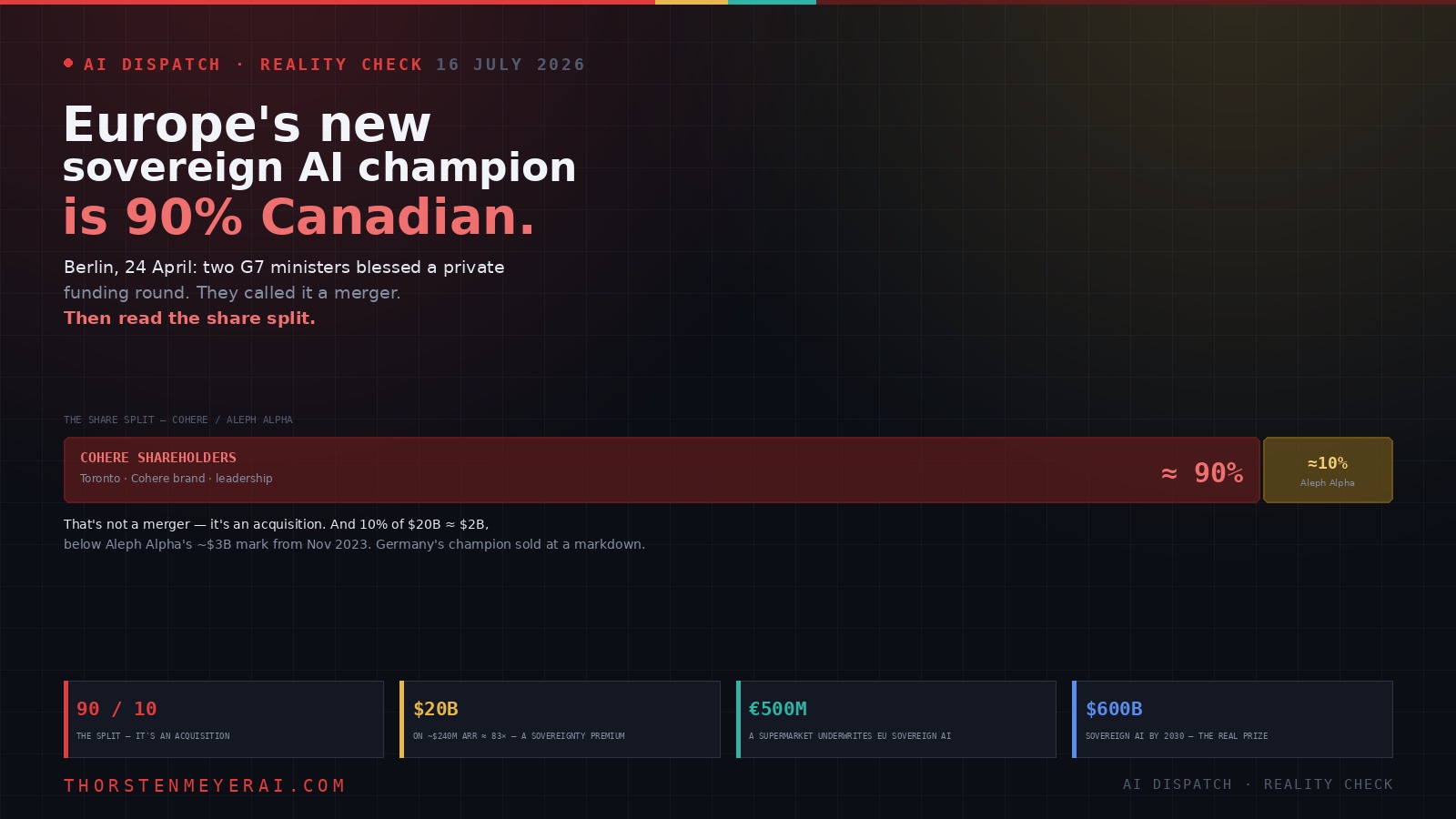

On 24 April 2026, in Berlin, Germany’s Digital Minister and Canada’s AI Minister stood together on a stage to bless a private company’s funding announcement. That staging tells you what kind of deal this was: two G7 governments treating a corporate transaction as an instrument of statecraft.

They called it a merger. Then read the share split. Cohere’s shareholders take roughly 90% of the combined company. Aleph Alpha’s take about 10%.

That’s not a merger. That’s an acquisition, dressed in merger language because both governments needed the political weight the word carries. And the entity it creates — pitched as Europe’s answer to American AI dependence, valued around $20 billion, underwritten by the company that owns Lidl — raises a question European procurement lawyers are going to have to answer in public: is a 90%-Canadian company with Toronto leadership actually European sovereign AI?

Here’s the honest read: what happened, why Aleph Alpha had to sell, what it means for North America, for Brussels, for Mistral, and for every other European lab now doing the arithmetic on its own survival.

Europe’s new sovereign AI champion is 90% Canadian

Berlin, 24 April: two G7 ministers stood on stage to bless a private funding round. They called it a merger. Then read the share split. The entity it creates — ~$20B, underwritten by the company that owns Lidl — forces a question European procurement will have to answer in public.

- ~90% Cohere shareholders · Toronto leadership · Cohere brand

- Canada is not in the EU; GDPR adequacy is partial

- Cohere carries a Microsoft strategic partnership

- Canada is a Five Eyes member — if your threat model is US intelligence access, that’s not obviously the fix

- “Canadian-German company” gets harder after an IPO

- Parent is Canadian, not American → no CLOUD Act reach

- STACKIT hosting in German data centres; EU-only DC plans

- Heidelberg security-cleared facility + BSI C5

- Sovereignty delivered contractually & technically, not by passport

Cohere’s deal of the decade — bought European government access for 10% of equity. It could never have built it.

Canada gets a champion + an export: sovereignty-as-a-service (Ottawa pre-seeded CAD $240M of compute).

US market unchanged — but the fight moves to regulated/gov, where jurisdiction beats benchmarks.

“Only credible European option” died on 24 April. The market bifurcates: purity vs coalition.

Mistral = French parent, SecNumCloud (covers jurisdiction), open weights. Cohere+AA = BSI C5 (doesn’t), but 2 governments + a supermarket.

Damage is Germany — Mistral demoted from continental to regional, while chasing $1B ARR by December.

If Germany’s champion couldn’t survive alone, the message is: consolidate, specialize, or die.

New exit category: acquired by a friendly non-US power.

Survivors are the specialists — Helsing, Black Forest Labs, Wayve, Nscale, AMI. And watch the Schwarz template: industrial capital as sovereign capital.

Strip the staging and it’s a smart deal built on an honest admission: Europe stopped trying to win the model race and started trying to win the deployment layer. Aleph Alpha’s alternative was irrelevance; Cohere’s was never entering Europe; Schwarz’s was an empty cloud. Everyone got what they needed. But the risks are real — 83× on known ARR is a sovereignty premium, not a revenue multiple. Europe’s new champion is 90% Canadian, led from Toronto, partnered with Microsoft, hosted by a supermarket. Sovereignty stopped being a status and became a spectrum. Don’t walk away — read the documents instead of the press release.

The deal, plainly

Toronto-based Cohere — founded 2019 by Aidan Gomez, Ivan Zhang, and Nick Frosst out of the University of Toronto — acquires Heidelberg-based Aleph Alpha, Germany’s designated national AI hope. Combined valuation approximately $20 billion, per the term sheet reported by Handelsblatt. Structured as a simultaneous acquisition and Series E.

The anchor is Schwarz Group — the Neckarsulm retail conglomerate behind Lidl and Kaufland, already an Aleph Alpha shareholder with a stake reported above 20% — committing €500 million (~$600 million) in structured financing and leading the Series E. In exchange, the combined entity runs on STACKIT, the sovereign cloud operated by Schwarz’s IT arm, Schwarz Digits.

The combined company keeps the Cohere brand, dual headquarters in Toronto and Heidelberg (the latter as “European center of excellence”), folds Aleph Alpha’s Pharia model family into Cohere’s Command series, and targets exactly the verticals you’d expect: defence, energy, finance, healthcare, manufacturing, telecoms, and the public sector. Regulatory clearance is still pending, expected later in 2026 — and not guaranteed, given the Commission’s hardened stance on AI-sector consolidation.

The backdrop: Canada and Germany signed a Sovereign Technology Alliance earlier this year. McKinsey projects sovereign AI at roughly $600 billion of $1 trillion in total AI spend by 2030. That number is the prize, and it explains everything about why ministers showed up.

AI Engineering: Building Applications with Foundation Models

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Why Aleph Alpha had to sell

The polite version is “complementary strengths.” The honest version is that Aleph Alpha was a distressed asset with excellent relationships.

The sequence is unambiguous. Aleph Alpha pivoted away from building its own frontier models, repositioning as something closer to a systems integrator — helping clients deploy AI regardless of who built the underlying model. Co-founder and CEO Jonas Andrulis was forced out in 2025. Roughly 50 layoffs followed in early 2026. Ilhan Scheer, ex-Accenture, was elevated to Co-CEO on 1 February 2026; the COO exited. Founder out, operators in, research-led ambition swapped for enterprise deployment, cost base right-sized.

Read in sequence, those weren’t crises — they were preparation. Each move primed the company for exactly this transaction. As one German analysis put it bluntly: without the merger, the most likely outcome was Aleph Alpha’s quiet irrelevance.

And the price reflects it. Aleph Alpha was marked at roughly €2.7 billion (~$3 billion) after its November 2023 round. Ten percent of a $20 billion entity is about $2 billion. Do the arithmetic: Germany’s national AI champion was sold at a markdown to its 2023 valuation, and the headline number is doing a lot of work to disguise it.

What Aleph Alpha genuinely brings is not technology. It’s access: relationships with Germany’s Digital Ministry, the Baden-Württemberg state government, Deutsche Bank, SAP, Bosch, plus a German security-cleared facility, small-language-model expertise, and European-language tokenizers. Berlin’s state government is already lined up as a customer. For Cohere, that’s an entry point into European public procurement that would have taken years and possibly never arrived. They didn’t buy a model lab. They bought a Rolodex and a passport.

Accelerate Everything with Tensor Cores: A Developer’s Guide to High-Performance AI, Efficient Training, and Scalable Models

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The kingmaker is a supermarket

Pause on this, because it’s the most genuinely novel thing in the deal.

Europe’s sovereign AI strategy is now substantially underwritten by the company that runs Lidl. Dieter Schwarz — who controls the group personally, with a net worth around $44 billion — is now, functionally, the third strategic actor in European AI alongside the EU institutions and the hyperscalers.

And the decisive move isn’t the €500 million cheque. It’s making STACKIT the substrate. That contract makes Schwarz a beneficiary of every enterprise and government deployment the new entity ever wins. The retailer gets an anchor tenant for its cloud business; the AI company gets sovereign European infrastructure it doesn’t have to build. It’s elegant, and it’s the clearest expression yet of a pattern worth naming: industrial capital as sovereign capital.

That’s arguably more durable than government money, which shifts with election outcomes. It also concentrates enormous leverage in one privately-controlled German conglomerate — and a strategic backer with that much leverage can become a constraint on commercial decisions later. Nobody should pretend that’s a risk-free structure.

AI for Small Business: From Marketing and Sales to HR and Operations, How to Employ the Power of Artificial Intelligence for Small Business Success (AI Advantage)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The question nobody wants to answer

Is this European sovereign AI?

The case that it isn’t: Cohere’s shareholders own ~90%. Leadership is in Toronto. The brand is Cohere. Canada is not in the EU, and its GDPR adequacy is partial rather than absolute. Cohere carries a strategic partnership with Microsoft — the exact dependency the sovereignty pitch exists to escape. And the point a procurement officer will eventually make out loud: Canada is a Five Eyes member. If your threat model is intelligence-sharing with the United States, a Canadian parent is not self-evidently the fix. Gomez’s promise that “Cohere will become a Canadian-German company” is sincere — and, as TechCrunch noted, considerably harder to keep after an IPO puts ownership in the hands of global shareholders with no allegiance to either country.

The case that it is: jurisdiction of the controlling parent is what actually decides CLOUD Act exposure, and Cohere’s parent is Canadian, not American — so US authorities cannot compel it the way they can compel Microsoft or AWS. Add STACKIT hosting in German data centres, EU-only data-centre plans, the Heidelberg security-cleared facility, dedicated compliance staff, and BSI C5 certification, and the operational answer is defensible. Sovereignty is delivered contractually and technically, not by passport alone.

My read: it’s defensible on the letter and vulnerable on the politics. And in this market, politics is half the product. European sovereignty has just been redefined from “incorporated in the EU” to “not incorporated in the United States” — a meaningfully weaker standard, adopted because Europe couldn’t produce a champion that met the stronger one. That’s the real news, and nobody on that Berlin stage said it.

Trust.: Responsible AI, Innovation, Privacy and Data Leadership

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

What it means for North America

For Cohere, it’s the deal of the decade — if it closes. At roughly $240 million ARR (September 2025) and a $6.8–7 billion pre-deal mark, Cohere was the largest enterprise AI lab outside the US and still a niche player against OpenAI, Anthropic, and Google. It could not have bought European government access at any price; it just did, for 10% of its equity. Its existing base — Oracle, Salesforce, RBC, Fujitsu, LG CNS — plus an MOU with Saab on the GlobalEye defence programme, now gets a European public-sector channel bolted on.

For Canada, it’s national-champion consolidation and an export industry. Ottawa had already put a reported CAD $240 million into Cohere’s compute infrastructure through its Sovereign AI Compute Strategy before the merger — which is precisely what demonstrated to Berlin that Canadian backing was real and durable. Canada is now positioned to sell “sovereignty-as-a-service” to Europe.

And there’s the irony worth sitting with: a Five Eyes country is selling Europe independence from America. That works only as long as nobody in a European procurement committee reads the intelligence-sharing agreements — or as long as “not American” is genuinely the standard, which it now apparently is.

For the US market, little changes. The merger doesn’t make Cohere competitive with the frontier labs on general enterprise AI; US labs are valued somewhere between roughly 15× and 40× larger depending on which reported mark you use (and those figures conflict wildly right now). What it changes is where Cohere chooses to fight: regulated and government work where jurisdiction, not benchmark score, decides the deal. That’s a smaller market than “all enterprise AI” — and a defensible one.

What it means for Mistral

This is the part Paris should be reading twice.

The “only credible European option” claim died on 24 April. That claim was load-bearing in Mistral’s entire pitch, and it’s gone.

The European market now bifurcates along a purity-versus-coalition axis:

Mistral is France-primary and jurisdictionally purer: a French parent (Mistral AI SAS), SecNumCloud — a certification covering both operational security and legal sovereignty that US hyperscalers structurally cannot hold in native form — Bpifrance backing, OVHcloud and Scaleway delivery, open weights, and 100% EU incorporation.

Cohere–Aleph Alpha is Germany-primary and politically bigger: two G7 governments on stage, Schwarz’s balance sheet and cloud, BSI C5, deep German federal and Länder relationships, Bosch/SAP/Deutsche Bank ties — but 90% Canadian ownership and a Microsoft partnership.

Note the asymmetry in the certifications, because it matters: BSI C5 certifies security practices; it does not address jurisdictional exposure. SecNumCloud addresses both. On the letter of sovereignty, Mistral wins. On the politics and the balance sheet, Cohere–Aleph Alpha wins.

The concrete damage to Mistral is Germany — its largest market outside France, and the one where a German buyer can now choose a German-hosted, German-relationship-rich, government-endorsed alternative. Mistral’s French-primary positioning just got demoted from continental to regional.

And the timing is brutal. Mistral has publicly committed to $1B ARR by December 2026, from ~$400M in early 2026 — roughly 2.5× in ten months. It now has to hit that number while a $20 billion rival with two G7 governments and a supermarket conglomerate behind it hunts the same regulated verticals.

What Mistral should do about it: stop competing on “European” and start competing on European incorporation — the one thing Cohere structurally cannot copy without redomiciling. If sovereignty is binary, say so loudly, and make SecNumCloud versus BSI C5 the procurement conversation. That’s a fight Mistral wins on the documents.

What it means for every other EU player

The consolidation signal is the headline. If Germany’s national champion — backed by Bosch, SAP, Schwarz, and the federal economics ministry — couldn’t survive as an independent frontier lab, the message to every sub-scale European lab is unambiguous: consolidate, specialize, or die.

A new exit category just opened: acquired by a friendly non-US power. That’s now a legitimate, government-blessed outcome, and it will shape how European AI founders and their boards think about endgames. Expect more of it.

Specialization is the survivable path. The generalist European LLM lab is now a two-horse race — and one horse is Canadian. The labs with durable positions are the ones that aren’t trying to be Europe’s OpenAI: Helsing (defence), Black Forest Labs (image), Wayve (autonomy), Nscale (infrastructure), AMI Labs (LeCun’s Paris lab). Narrow, deep, and structurally defensible beats broad and underfunded.

And watch the Schwarz template. If a supermarket can become a sovereign-AI kingmaker, so can Siemens, Bosch, Volkswagen, or SAP. European industrial capital deciding that domestic AI capability is strategic infrastructure rather than discretionary procurement may end up mattering more than any Brussels programme. That’s the pattern to track over the next 18 months.

The honest risks

Five, and they’re all real. Integration — two culturally distinct organizations under a 90/10 power split rarely merge as equals, whatever the press release says. Compute — European grid constraints are a hard physical limit on scaling. Revenue execution — $20 billion against roughly $240 million of known ARR is about an 83× multiple; that’s a sovereignty premium, not a revenue multiple, and Aleph Alpha’s contribution to combined revenue hasn’t been disclosed. Regulatory clearance — pending, with the Commission newly hostile to AI consolidation. Schwarz dependency — the leverage cuts both ways.

And the structural one: Europe has traded model leadership for deployment control. That’s a coherent bet — arguably the right one — but it means the combined entity must either keep importing leading-edge capability or build a research function inside Cohere that stays credible as US labs compound. Procurement-led growth is defensible and slow; product-led growth compounds. They’ve chosen the former.

The take

Strip away the ministers and the staging and this is a smart deal built on an honest admission: Europe stopped trying to win the model race and started trying to win the deployment layer. In a regulated economy with $600 billion of sovereign-AI spend coming by 2030, controlling how AI gets deployed may well be more durable than controlling which model wins this generation. Aleph Alpha’s alternative was irrelevance. Cohere’s alternative was never getting into Europe. Schwarz’s alternative was an empty cloud. Everyone in the room got what they needed.

But the uncomfortable truth is the one nobody said out loud in Berlin. Europe’s new sovereign AI champion is 90% Canadian, led from Toronto, partnered with Microsoft, hosted by a supermarket, and endorsed by two governments who needed the word “merger” more than the facts supported it. Sovereignty just stopped being a status and became a spectrum — and the standard quietly slid from “European” to “not American.”

For anyone buying: that’s not a reason to walk away. It’s a reason to read the documents instead of the press release. Ask who owns the parent, which certification actually covers jurisdiction (SecNumCloud does; BSI C5 doesn’t), where the weights live, whether you can leave, and who’s still standing in five years. On those questions, this deal is defensible — and Mistral, for all its own contradictions, still has the cleaner answer on paper.

The race for Europe’s AI future now has exactly two runners. One is French and jurisdictionally pure but outgunned. The other is Canadian, politically armored, and calling itself European. Neither is what Europe said it wanted in 2023.

Sources: TechCrunch (Anna Heim) and The Next Web on the merger structure, the 90/10 split, Schwarz/STACKIT and the Gomez quotes; Handelsblatt via TNW/tech-insider for the ~$20B term-sheet valuation; CorpDev, DelMorgan, BigGo, AI CERTs and theaiworld.org for deal terms, ministers’ attendance (Karsten Wildberger, Evan Solomon) and target verticals; Startuprad.io for the leadership-change sequence and the deployment-control framing; SoftwareSeni for the Canada–Germany Sovereign Technology Alliance and Ottawa’s CAD $240M pre-merger compute investment; McKinsey (March 2026) for the ~$600B-of-$1T sovereign-AI projection; Dr. Raphael Nagel and DATASOLUTION on SecNumCloud vs BSI C5 and CLOUD Act reach. Cohere ARR (~$240M, Sept 2025) and valuations are as reported and unaudited; competitor valuation figures conflict widely across sources. The deal remains subject to regulatory and shareholder approval. Not investment advice; not legal advice — jurisdictional questions require counsel. Analysis and framing are the author’s.