On May 15, 2026, OpenAI launched a preview of personal-finance tools inside ChatGPT for Pro subscribers in the United States. Users can connect bank accounts, credit cards, investment accounts, and crypto wallets through Plaid — across more than 12,000 financial institutions including Chase, Fidelity, Schwab, Robinhood, American Express, and Capital One — and ChatGPT renders a dashboard of spending, portfolio performance, subscriptions, upcoming payments, and answers questions grounded in the user’s actual balances, transactions, and liabilities.

The feature defaults to GPT-5.5 Thinking, OpenAI’s latest reasoning model, evaluated by more than 50 finance professionals on an internal benchmark (GPT-5.5 Thinking 79/100, GPT-5.5 Pro 82.5/100); FinanceAgent (the third-party agentic benchmark for earnings-report analysis and similar tasks) sits at 60%. Intuit integration is announced as forthcoming — explicitly flagged with two example flows: credit card approval-odds-plus-application submission, and tax-implications-plus-scheduling-with-local-tax-expert.

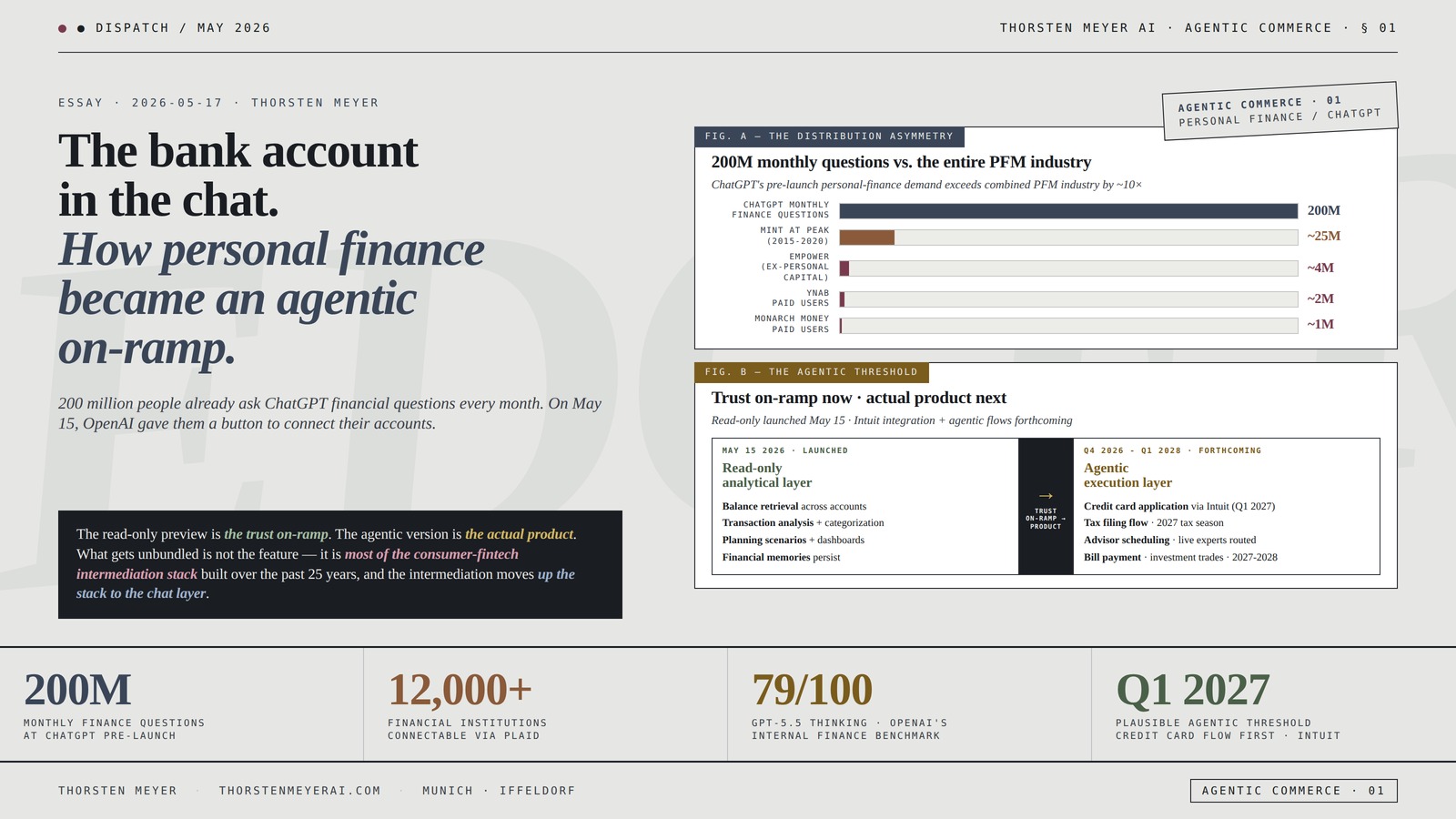

The headline observation from Plaid’s CTO post: more than 200 million people already ask ChatGPT personal-finance questions every month. The headline observation from OpenAI’s announcement: ChatGPT is “not a replacement for professional financial advice.” The headline observation neither side made: the read-only preview is the trust on-ramp, the agentic version is the actual product, and what gets unbundled when 200 million conversations already happen at the chat layer is most of the consumer-side fintech intermediation stack built over the past 25 years.

This essay walks the empirical-feature mechanics, the dashboard-vs-conversation inversion, the agentic threshold that hasn’t been crossed yet but is named explicitly in the launch, the intermediation map of who gets affected, the trust-and-regulatory frontier the read-only framing sits on top of, the European-architecture mismatch that PSD2/PSD3/FIDA produces, and the structural reading of what this means for consumer fintech over the next 24 months.

The bank account

in the chat.

How personal finance

became an agentic

on-ramp.

arriving at ChatGPT (pre-launch)

connectable via Plaid

internal finance benchmark

credit card flow first · Intuit

analytical layer

- Balance retrieval across accounts

- Transaction analysis + categorization

- Pattern identification over time

- Planning scenarios with grounded data

- Dashboard rendering + financial memories

on-ramp →

product

execution layer

- Credit card application + approval odds (Q1 2027)

- Tax filing flow via Intuit · 2027 tax season

- Advisor scheduling · routed to live experts

- Investment trades · partnership-mediated

- Bill payment + savings switching · 2027-2028

The read-only preview is the trust on-ramp. The agentic version is the actual product. What gets unbundled is not the feature; it is most of the consumer-fintech intermediation stack built over the past 25 years — and the intermediation moves up the stack to the chat layer.Thorsten Meyer · The Bank Account in the Chat · Agentic Commerce 01

By Thorsten Meyer — May 2026

This is a dispatch on a launch that landed yesterday, and it is the first piece of a new editorial track on AI agentic commerce and consumer-side intermediation. The launch is interesting on its own terms — a read-only personal-finance assistant grounded in live account data, available to Pro subscribers in one country, on web and iOS — but it is much more interesting as the marker of a structural transition that the consumer fintech industry has been pointing at for a decade and has not yet had to confront. What changed yesterday is not the feature; it is the surface where the feature lives. 200 million people already ask ChatGPT financial questions every month without any account context. Connecting those accounts is the move that turns the chat layer into the primary consumer interface for money — not the only one, not yet — and starts the clock on how the intermediation downstream of that interface re-prices.

The structural argument I want to make: ChatGPT’s personal-finance preview is not the product. It is the on-ramp to the product. The product is the agentic layer that OpenAI explicitly named in the launch announcement — credit card application submission, tax filing, advisor scheduling, with Intuit and ecosystem partners — which arrives in 12-24 months and changes which industry-tier players have a relationship with the consumer and which have a relationship with the agent the consumer delegates to. The read-only preview is the trust on-ramp because trust at the agentic layer requires evidence-grounded answers at the read-only layer first. The conversational interface is the unit shift; the dashboard is a side effect. The 200-million-questions-monthly figure is the empirical baseline that makes this a different launch from every prior personal finance management tool that ever existed. And the regulatory framing — “not a replacement for professional advice” — is the bridge that has to hold while the agentic capabilities catch up to where the marketing wants them.

The headline integrative finding: The personal finance feature is structurally a Trojan horse for agentic consumer-finance. The read-only preview de-risks the trust transfer; the announced Intuit integration crosses the agentic threshold; the 200-million-monthly-questions distribution asymmetry compresses the user-acquisition cost that traditional PFM apps spent a decade buying. The downstream intermediation — banks, credit-card issuers, brokerages, robo-advisors, fintechs, traditional PFM, Plaid itself, Intuit, human advisors — re-prices based on where it sits relative to the chat layer. Some get commoditized into rails; some get unbundled; some become surface partners. The next 24 months determine which goes which way. What is not yet visible: the European regulatory architecture (PSD2/PSD3/FIDA) produces a structurally different open-banking framework that does not depend on Plaid and is governed by mandated APIs rather than data-aggregator infrastructure. The US rollout’s path to Europe is not a translation; it is a re-architecture.

This essay walks the feature mechanics as the launch announced them (Section I), the dashboard-vs-conversation inversion that changes who can use the product (Section II), the agentic threshold that the read-only launch deliberately stops short of and the Intuit integration that signals where it goes (Section III), the intermediation map of who gets affected and how (Section IV), the trust-and-regulatory frontier that the “not a replacement for professional advice” framing sits on top of (Section V), the European architecture that PSD2/PSD3/FIDA produces and why the US rollout doesn’t translate (Section VI), and the structural reading of what consumer fintech looks like 24 months from now (Section VII).

I · What launched · the empirical-feature mechanics

The empirical-launch crystallization. OpenAI announced the preview on Friday, May 15, 2026. The mechanics are precise and constrained, and they matter for what they include as much as for what they explicitly do not.

The user-side experience

The connection flow: users open Finances from the ChatGPT sidebar and select “Get started,” or type @Finances, connect my accounts from anywhere in ChatGPT. ChatGPT guides them through Plaid’s secure account-linking flow.

The supported institutions: more than 12,000 financial institutions including Chase · Fidelity · Schwab · Robinhood · American Express · Capital One · Bank of America · Wells Fargo · Citi · plus credit unions, regional banks, and crypto wallet support (Coinbase, others). Plaid supports nearly every major account type — checking, savings, credit cards, brokerage, retirement, mortgage, crypto wallets.

The dashboard rendered: portfolio performance · spending categorization · subscription tracking · upcoming payments · cash flow snapshot · transaction history.

The data scope: ChatGPT can access balances · transactions · investments · liabilities when accounts are connected. It cannot see full account numbers and cannot make changes to accounts. Read-only by design at launch.

The conversational interface

The example queries provided in the launch:

- “I feel like I’ve been spending more recently. Has anything changed?”

- “Help me build a plan to buy a house in my area in the next 5 years”

- “Help me understand where I can save for my children’s tuition”

- “How do I pay off my debt faster?”

The financial memories layer: users can add context manually beyond the connected-account data — savings goals · mortgage details · planned purchases · loans from family · personal obligations · long-term financial priorities. These are stored as “financial memories” that persist across conversations and shape future answers.

The model: defaults to GPT-5.5 Thinking, OpenAI’s latest reasoning model. Benchmark scores on OpenAI’s internal personal-finance benchmark, developed with more than 50 financial professionals: GPT-5.5 Thinking 79 / 100 · GPT-5.5 Pro 82.5 / 100. On the third-party FinanceAgent benchmark (earnings-report analysis and similar tasks), GPT-5.5 scored 60%. GPT-5.5 set a separate record on FrontierMath Tier 4 (doctorate-level math).

The release constraints

Geography: United States only at launch.

Tier: ChatGPT Pro subscribers only at launch. Plus and free tiers will follow “based on feedback from Pro users” with no committed timeline. OpenAI’s announcement says it plans to “make available to everyone” eventually.

Platforms: ChatGPT on web and iOS at launch. Android, desktop apps, and API access not yet enabled.

Data control: users can disconnect any account through Settings or the Finances page; synced data is removed within 30 days of disconnection. Financial memories are individually deletable. Temporary chats do not access connected accounts or save financial history.

What’s explicitly forthcoming

OpenAI named two flows the read-only launch does not yet support but the announcement promises:

- Credit card flow: “going from a credit card recommendation to understanding approval odds and submitting an application”

- Tax flow: “from asking about tax implications of a stock sale to getting a trusted tax estimate and scheduling a session with a live, local tax expert, powered by Intuit”

These are the agentic flows. They cross the boundary from read-only-analysis to take-action-on-the-user’s-behalf. They are not in the May 15 preview. They are named in the launch. This is the most important thing about the announcement.

The empirical-mechanics observation

What launched is a read-only analytical assistant with live account access, gated to Pro / US / web+iOS. What was promised but not launched is the agentic version that submits credit card applications and routes users to Intuit-powered tax services. The gap between what shipped and what was promised is structurally significant — it is the gap between trust on-ramp and product.

bank account aggregator device

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The dashboard-vs-conversation inversion · why this is not just Mint with a chatbot

The interaction-model crystallization. Every prior personal-finance management tool has been dashboard-first. Account-aggregation tools (Mint launched 2006, acquired by Intuit 2009, sunset 2024; Monarch · Copilot Money · YNAB · Tiller; bank-native budgeting tools) all share the same shape: connect accounts, render a dashboard, the user interprets charts and adjusts categorization. ChatGPT inverts this.

The two interaction models

Dashboard-first PFM: connect accounts → render dashboard → user interprets visualization → user manually drills into transactions → user manually categorizes / tags / budgets → user manually plans against goals. Interaction unit: graph or table.

Conversation-first PFM (ChatGPT): connect accounts → ChatGPT renders dashboard (still, the dashboard is still there) → user asks questions in plain language → ChatGPT answers grounded in connected data → ChatGPT proactively surfaces patterns. Interaction unit: natural-language question + grounded answer.

What changes when the interaction unit is conversation

Who can use the product expands. Dashboard-first PFM requires the user to be able to interpret financial visualizations — a skill that has historically gated adoption to the numerate-and-disciplined slice of consumers. Conversation-first PFM does not require this skill at the front door; the AI does the interpretation and renders the answer in prose. This is the same shift that ChatGPT itself produced for general computing: it moves the unit of interaction from “knowing how to specify what you want” to “describing what you want.” Applied to personal finance, it broadens the addressable user base by an order of magnitude — at the cost of removing one of the natural filters that kept overconfident decisions out of the product.

What gets asked changes. The dashboard-first product surfaces questions that are answerable visually: “Did I spend more this month than last?” Conversation-first surfaces questions that are answerable through reasoning across the data: “If I make this purchase, what does my emergency fund look like in 6 months?” / “Help me build a plan to buy a house in my area in the next 5 years” — the actual example queries from the launch. The conversational interface invites planning questions; the dashboard interface invites tracking questions. Different products, different problems solved.

Where the trust boundary sits moves. With a dashboard, the trust boundary is at the data layer — the user trusts the aggregator (Mint, Monarch) to pull correct transactions, and the user does the interpretation. With a conversation, the trust boundary sits at the interpretation layer — the user trusts the AI to reason correctly over the data. This is a larger and harder trust ask, especially in a domain where confidently wrong answers have direct financial consequences. The benchmark scores (79/100, 82.5/100, 60% on FinanceAgent) tell you exactly how much that trust is currently warranted — useful but not fiduciary-grade.

The 200-million-questions baseline

The Plaid CTO post says: more than 200 million people ask ChatGPT financial questions every month. The OpenAI announcement repeats the figure. This is the empirical baseline that makes this launch different from every prior personal-finance management tool.

For comparison: Mint at its peak (~2015-2020) had approximately 25 million users. Monarch Money (the Mint successor most cited) has approximately 1 million paid users. Personal Capital (now Empower) has approximately 4 million users. YNAB approximately 2 million users. The personal-finance question demand that already lives inside ChatGPT exceeds the entire installed base of every PFM tool that has ever existed, combined, by approximately an order of magnitude.

The unit-acquisition-cost implication: traditional PFM tools spent ten years and billions of dollars in marketing, partnerships, and brand-building to acquire that user base. ChatGPT has it as an existing organic-intent flow. Adding personal finance to ChatGPT does not require user acquisition; it requires conversion. The conversion funnel runs from “asked ChatGPT a finance question” to “connected an account through @Finances.” That conversion rate determines how much of the 200M monthly addressable base becomes a connected-account base — and even at single-digit percentage conversion, the absolute scale dwarfs the incumbent base.

The inversion observation

ChatGPT is not adding personal finance to ChatGPT. It is wrapping personal finance around the conversational query flow that already exists. The dashboard is the rendered surface; the conversation is the actual interaction. The 200-million-monthly-questions baseline is the structural advantage. The PFM industry as it exists in 2026 was built around dashboard-first interaction with painstakingly-acquired users; the ChatGPT layer is conversation-first with users who arrived for other reasons. These are not the same product category competing on features. They are different categories operating on different unit economics.

Personal Finance – Moneyble

Spreadsheet based

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The agentic threshold · what the read-only preview deliberately does not do, and what it announces will follow

The forward-shape crystallization. The read-only preview is bounded by an explicit constraint: ChatGPT can analyze accounts but cannot transact through them. The Intuit integration named in the launch is the explicit pre-announcement of crossing that boundary.

What read-only does and doesn’t permit

Read-only permits: balance retrieval · transaction analysis · spending categorization · pattern identification · planning scenarios · question-answering grounded in the data · dashboard rendering · financial memory persistence.

Read-only does not permit: moving money between accounts · paying bills · applying for credit cards · placing investment trades · filing taxes · scheduling advisor sessions · purchasing financial products · opening new accounts · making payments to merchants.

The boundary: agentic action requires either OAuth + write-scope permissions on the financial institution’s API (Plaid supports some payment initiation through Plaid Transfer and Plaid Auth) or partnership with a transactional-service provider (Intuit for tax · a fintech for credit applications · a brokerage API for trades).

What the Intuit partnership signals

OpenAI named Intuit explicitly in the launch announcement, with two example agentic flows:

Credit-card flow: “a user could go from getting a credit card recommendation to understanding their approval odds and submitting an application”

Tax flow: “from asking about tax implications of a stock sale to getting a trusted tax estimate and scheduling a session with a live, local tax expert, powered by Intuit”

The structural significance: Intuit owns TurboTax (consumer tax filing, ~40M users) · Credit Karma (consumer credit + financial products marketplace, ~135M members) · QuickBooks (SMB accounting) · Mint until 2024. Through Credit Karma, Intuit has direct integrations with most major credit card issuers, mortgage lenders, auto loan providers, personal-loan fintechs, and brokerages for transactional flows. Through TurboTax, Intuit has direct integrations with the IRS and state tax authorities. The Intuit partnership essentially borrows Intuit’s transactional rails for the agentic actions ChatGPT cannot directly perform.

The Hiro acquisition · April 2026

One month before this launch, OpenAI acquired the team behind personal-finance startup Hiro, backed by Ribbit · General Catalyst · Restive. The Hiro team had been building consumer personal-finance products. OpenAI is not specific about whether the new Finances feature was built by the Hiro team, but says their finance expertise was “useful” in launching it. The acquisition predates the launch by a month — short enough that Hiro’s product DNA likely influenced the design, but not so short that the launch is purely Hiro.

The agentic-threshold observation

The read-only preview is the trust on-ramp. It teaches the user to expect that ChatGPT understands their financial picture and produces useful answers grounded in their actual data. It collects the user’s consent to connect accounts. It establishes the @Finances surface as the route to the user’s money.

The agentic version is the actual product. Credit card applications submitted from chat. Tax filings prepared from chat. Advisor sessions booked from chat. Bill payments executed from chat. The trust required to give ChatGPT the right to spend, borrow, and file on your behalf is structurally larger than the trust required to let it read your transactions. The read-only preview is the trust-building exercise that precedes the agentic threshold crossing.

Timeline: OpenAI has not committed to a date for Intuit integration. The Intuit announcement (Intuit’s side) has not been published. Industry expectation based on adjacent launches (Anthropic’s Claude in Excel, the OpenAI–Mattel and OpenAI–Walmart agentic-commerce partnerships announced earlier in 2026): the agentic version arrives in 12-24 months, with credit-card application flows likely first (the OAuth and risk-disclosure infrastructure is simpler than tax filing) and tax flows second. Whether the agentic crossing produces the value the launch announcement implies — or whether regulatory friction, model accuracy ceilings, and consumer skepticism extend the timeline materially — is one of the open structural questions.

Financial Statements: A Step-By-Step Guide to Understanding and Creating Financial Reports

Used Book in Good Condition

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The intermediation map · who gets unbundled, commoditized, or partnered with

The industry-impact crystallization. Personal finance is intermediated by a stack of companies operating between the consumer and their money. The chat-layer surface re-prices that stack based on where each player sits relative to the conversational interface.

Tier 1 · Banks · core deposits, mostly insulated

The deposit relationship is sticky: Chase, Bank of America, Wells Fargo, Citi, US Bank, the regional bank network. These hold checking, savings, and core consumer deposits. The chat layer abstracts the user’s day-to-day interaction with the bank — the bank app becomes less important as ChatGPT becomes the surface where balances are reviewed and questions are asked.

The impact: banks become utility rails. The Plaid integration treats them as data sources rather than relationship-owners. Their brand loyalty and switching costs are protected by regulatory friction (FDIC insurance, ACH routing numbers, payroll direct deposit) more than by consumer love. They are not unbundled, but they are commoditized.

Tier 2 · Credit card issuers · marketplace partnership tension

The intermediated market: Amex, Chase Sapphire, Capital One, Citi rewards, Discover. Credit cards are where consumer financial intermediation produces the most revenue (interchange fees, interest charges, annual fees, rewards spend).

The chat-layer implication: the credit card recommendation question is one of the highest-value queries ChatGPT can answer. “Which credit card should I get?” is a question with millions of dollars of intermediation revenue downstream of the answer. Through Credit Karma (Intuit partnership), ChatGPT can become the front door for credit card applications. This either (a) makes issuers’ marketing/affiliate channels (NerdWallet, The Points Guy, Credit Karma direct) less valuable as ChatGPT becomes the new affiliate channel, or (b) consolidates affiliate revenue toward whoever wins the chat-layer placement deal.

Tier 3 · Brokerages and robo-advisors · advice commoditization

The intermediated market: Schwab, Fidelity, Vanguard, Robinhood, Webull (brokerages); Betterment, Wealthfront, Personal Capital/Empower, Schwab Intelligent Portfolios (robo-advisors); the human-advisor network (RIAs, wirehouses, regional firms).

The chat-layer implication: personalized investment advice has been the explicit value proposition of robo-advisors for a decade. A ChatGPT with full read access to your accounts can produce more contextual advice than most robo-advisors deliver today — at no marginal cost beyond the Pro subscription. The robo-advisor revenue model (10-30 basis points on AUM) competes with a $20/month flat fee from OpenAI that includes everything ChatGPT does. The robo-advisor category is structurally exposed. Brokerages are partially protected by execution and custody (you still need a Schwab account to actually buy the stock), but the advice layer compresses.

Tier 4 · Traditional PFM · direct competition

The intermediated market: Monarch Money, Copilot Money, YNAB, Tiller, Empower (formerly Personal Capital), Quicken Simplifi, EveryDollar. These are the dashboard-first PFM tools that survived Mint’s 2024 sunset.

The impact: this tier is in direct competition. The 200-million-monthly-questions baseline at ChatGPT exceeds their combined user bases by an order of magnitude. Their structural defenses are quality of categorization, depth of budget tooling, and budget-specific brand loyalty — none of which protects against an AI-native chat layer that produces dashboards from the same Plaid data. Monarch Money’s roughly 1 million paid users, Copilot Money’s much smaller base, and YNAB’s roughly 2 million users are exposed to direct competition from a feature that ships free-eventually inside a $20/month general-purpose product. The traditional-PFM category is the most-displaced tier.

Tier 5 · Plaid · rails commoditized but volume up

The intermediated market: Plaid (the dominant US data-aggregator), Yodlee (smaller share), MX (smaller still), Finicity (acquired by Mastercard).

The chat-layer implication: Plaid wins the OpenAI partnership and gains massive incremental transaction volume. The Plaid CTO post is enthusiastic, calling the moment “a change starting to take shape in the delivery of consumer financial experiences.” Plaid becomes the rails for the chat-layer surface. This is high-volume, lower-margin, infrastructure positioning. Plaid is not displaced; Plaid is consolidated as critical infrastructure. The 48%-more-accurate income classification from Plaid’s transaction foundation model (described in the Plaid blog post) is exactly the kind of capability that gets more valuable as the user-facing layer commoditizes.

Tier 6 · Intuit · transactional partner

The intermediated market: Intuit owns TurboTax (40M), Credit Karma (135M members), QuickBooks (SMB), Mint until 2024. Intuit is the largest consumer-finance software company in the US.

The impact: Intuit is the named partner for ChatGPT’s agentic flows. This consolidates Intuit’s position as the transactional layer underneath chat-layer commerce — credit applications, tax filing, expert routing all flow through Intuit’s rails. Intuit gets the strategic distribution it has been trying to build for two decades; OpenAI gets the regulatory and execution infrastructure it does not have. The Intuit position is the strongest of any incumbent in this list. This deal is the structurally significant one in the entire launch.

Tier 7 · Human financial advisors · top-of-funnel disruption with bottom-of-funnel protection

The intermediated market: RIAs (registered investment advisors, ~$10T AUM in the US), wirehouses (Morgan Stanley, Merrill, UBS), insurance-aligned advisors (Northwestern Mutual, NY Life), the CFP network.

The chat-layer implication: the top of the advisor funnel — initial financial planning, basic budget questions, retirement projections, simple tax-strategy questions — compresses. The bottom of the funnel — fiduciary advice, complex estate planning, high-net-worth tax strategy, behavioral coaching — does not, because regulation and consumer skepticism preserve it. Advisors get displaced on the “should I switch credit cards?” tier and protected on the “should I exercise these options?” tier.

The intermediation-map observation

The chat layer commoditizes some intermediaries (banks, PFM apps, brokerage advice, advisor top-of-funnel) and elevates others (Plaid as rails, Intuit as transactional partner). Credit card issuers face channel-rebalancing tension. Robo-advisors face direct competitive displacement. Traditional PFM faces direct extinction risk. Whoever wins the chat-layer surface partnerships — which institutions get recommended, which products get suggested, which advisors get routed to — captures the affiliate-economics layer that the consumer-finance category has been built on for two decades. This is not a feature launch. It is a re-mapping of who has the consumer relationship.

TANGEM Crypto Wallet Pack of 2 – Trusted Cold Storage Hardware Wallet for Bitcoin, Ethereum, NFTs & Altcoins – 100% Offline Crypto Cold Wallet

Proven security at scale: Over 9 years and millions of cards issued with no known remote hacks, while…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The trust and regulatory frontier · “not a replacement for professional advice”

The fiduciary-risk crystallization. Personal finance is one of the most-regulated consumer categories. The launch makes a careful framing choice — read-only, US-only, Pro-only, “not a replacement for professional advice.” That framing is doing structural work.

The regulatory layers

FINRA: investment-advice regulation. The Investment Advisers Act of 1940 distinguishes “investment advice” (fiduciary, requiring registration) from “general financial information” (not regulated as advice). ChatGPT’s read-only analytical assistant sits inside the latter, but its outputs frequently look like the former. The line is not legally clean.

SEC: securities regulation. Recommending specific investments, particularly to retail customers, triggers Reg BI (Regulation Best Interest) for broker-dealers and the fiduciary rule for RIAs. ChatGPT does not register under either. Its recommendations are not legally fiduciary.

CFPB: consumer-finance regulation. Credit advice, debt collection, lending, deposit accounts all sit under CFPB jurisdiction. ChatGPT’s debt-payoff advice has not been certified under any CFPB framework.

GLBA: Gramm-Leach-Bliley Act, financial privacy. Connected-account data is non-public personal information (NPI) under GLBA. OpenAI’s data handling for connected-account data has to meet GLBA standards. The Plaid integration likely satisfies this; OpenAI’s downstream use does not yet have a public audit framework.

State regulators: state-level securities and lending regulators apply additionally. California’s CCPA/CPRA and other state privacy laws apply to financial data.

The accuracy ceiling

OpenAI’s internal benchmark: GPT-5.5 Thinking 79/100, GPT-5.5 Pro 82.5/100, developed with 50+ finance professionals.

FinanceAgent third-party benchmark: 60%.

The structural read: these are mid-range scores. Useful, certainly. Not fiduciary-grade. A human CFP scoring 79/100 on a personal-finance examination is competent but not exceptional. An AI scoring 79/100 on a benchmark designed with finance professionals is roughly equivalent — but with the variance pattern that LLMs produce, which is confidently-wrong-some-of-the-time rather than uniformly-better-or-worse. This variance pattern is the issue.

The “not a replacement for professional advice” framing

OpenAI’s announcement language: ChatGPT is “not a replacement for professional financial advice.” This is the standard disclaimer that any consumer-finance product carries.

The framing’s function: it preserves the regulatory category of “general financial information” rather than “investment advice.” It positions ChatGPT outside the fiduciary perimeter. It limits OpenAI’s liability for confidently-wrong outputs.

The framing’s weakness: 200 million people asking ChatGPT financial questions every month are not, in practice, treating its answers as “general information.” They are treating them as advice. The connected-account flow makes this even more pronounced — answers grounded in the user’s actual data feel more like personalized advice than answers grounded in general principles. The legal distinction is preserved; the consumer interpretation is not.

The trust frontier

The two trust questions:

- Accuracy trust: does ChatGPT give correct answers about my finances? Empirically, mostly yes, with variance. The benchmark scores suggest 75-85% reliability on the kinds of questions the launch advertises.

- Action trust: should ChatGPT be allowed to act on my finances? The read-only preview defers this question. The agentic version will force it.

The agentic threshold magnifies the trust question. A read-only answer that’s confidently wrong about a budget projection costs the user a planning misjudgment. An agentic action that’s confidently wrong about a credit card application or a tax filing costs the user actual money, a credit-score hit, an IRS notice, or worse. The trust required to permit agentic action is structurally larger than the trust required to permit analytical answers — and the regulatory framework that governs agentic action is materially stricter.

The frontier observation

The read-only preview navigates the regulatory frontier carefully. “Not a replacement for professional advice” + read-only data scope + US-only + Pro-only + 30-day data deletion + no full account numbers + no ability to make changes. This is the design of a product that has been built to be regulatorily defensible while remaining useful.

The agentic version cannot navigate it as easily. Agentic credit applications, agentic tax filings, agentic investment trades, agentic bill payments all cross into more-heavily-regulated territory. The “not a replacement for professional advice” framing does not survive the agentic transition without statutory clarification, regulatory engagement, or partnership-mediated risk-shifting (the Intuit partnership is doing exactly the third). How OpenAI navigates that transition is one of the open structural questions of the next 24 months.

VI · The European architecture · why this doesn’t translate, and what would replace it

The cross-jurisdictional crystallization. The US launch is gated to the US for reasons that go beyond licensing. The European open-banking architecture is structurally different and does not depend on Plaid.

The US model · data-aggregator-mediated

The historical pattern: US financial institutions did not have a unified standard for sharing account data with third parties. Plaid, Yodlee, MX, and Finicity emerged to solve this by aggregating data through screen-scraping (initially) and now through institution-by-institution API partnerships. The US model is private-sector infrastructure built around the absence of a regulatory mandate.

The legal foundation: CFPB Section 1033 of the Dodd-Frank Act (finalized October 2024) requires financial institutions to provide consumer access to account data through standardized APIs, with full compliance staggered through 2026-2030. This is the regulatory framework catching up to what Plaid has been doing commercially for 12 years. The relationship between Plaid and the new 1033 framework is currently a regulatory open question — Plaid may become the favored implementation partner or may be displaced by direct bank APIs.

The European model · regulatorily-mandated

PSD2 (Payment Services Directive 2) went into effect in 2018. It requires European banks to expose standardized APIs for third-party access to account information (AISP) and payment initiation (PISP), under license. This is the regulatory framework the US is now belatedly catching up to.

PSD3 + PSR (Payment Services Directive 3 + Payment Services Regulation), proposed by the European Commission in June 2023, currently in trilogue, expected to enter into force in 2026 with phased compliance. Tightens PSD2’s API requirements, increases fraud-liability protections, strengthens enforcement.

FIDA (Financial Data Access Regulation), proposed in parallel with PSD3, expands the open-banking framework beyond payment accounts to cover savings, mortgages, loans, pensions, insurance, and investment accounts. FIDA, when it enters force, makes European open-banking infrastructure structurally broader than what Plaid currently aggregates in the US.

The licensing layer: third-party providers (TPPs) operating under PSD2/PSD3 must hold AISP or PISP licenses issued by national competent authorities. ChatGPT, to offer personal finance services in Europe, would need to either become a licensed TPP itself, partner with one, or operate through a structure that delegates the regulated activity. None of these is impossible, but none is trivial.

What the European rollout requires

Translation, not transplantation: the US Plaid integration does not work in Europe. The product would need to integrate with PSD2/PSD3-licensed TPPs (Tink, acquired by Visa; TrueLayer; Belvo; Yapily; the German bank-direct APIs; the French and Italian aggregators). Multiple TPPs across multiple jurisdictions.

Language and currency localization: not just translation but country-specific tax, regulatory, and product context. The credit card market in Germany is structurally different from the US; the tax regime in Italy is different from France; the mortgage products in the UK are different from the Netherlands. A “European launch” is plausibly 15-20 country-specific launches.

Regulatory engagement at the EU level: the EU AI Act came into force August 2024 with phased compliance through 2026-2027. Personal-finance-oriented AI is plausibly classified as high-risk under Annex III, requiring conformity assessment, post-market monitoring, and transparency obligations. OpenAI’s path to Europe goes through the AI Act compliance framework as much as through PSD2/PSD3.

The cross-jurisdictional observation

The US launch is a US product. The European version is a different product. It would integrate with different rails, operate under different regulation, address different financial-product categories. OpenAI’s path to making personal finance globally available depends on architectural choices it has not yet announced. The most plausible structure is partnership-mediated entry into each major European market — likely Tink in the Nordics and France/Spain, TrueLayer in the UK and parts of Europe, possibly direct integration with German bank APIs. Timeline expectation: European launch lags US by 12-18 months minimum, with full feature parity (Intuit-equivalent transactional flows) likely 24-36 months out at minimum. This timeline gap matters competitively — European-native AI personal finance startups have a window to build defensible position before ChatGPT arrives, and incumbent European fintechs (Revolut, Wise, N26, Monzo, Klarna) have time to build conversational layers of their own.

VII · The structural reading · what consumer fintech looks like 24 months out

The synthesis-of-the-launch crystallization. Yesterday’s launch is the marker of a transition that has been pointed at for several years and is now starting in earnest. The 24-month forward view sorts into four observations.

Observation 1 · The conversational interface becomes the consumer-finance front door

The empirical signal: 200 million monthly personal-finance questions already arriving at ChatGPT before account integration. Conversion of that flow into connected-account use produces a connected-account base that exceeds the entire incumbent PFM industry by an order of magnitude.

The forward shape: the chat-layer surface is the new default for “where I check my money.” Bank apps, brokerage apps, PFM apps don’t disappear, but the gravity of consumer attention shifts. By mid-2027, “I asked ChatGPT” replaces “I checked my Mint / Monarch / Empower / bank app” as the default consumer narrative for personal-finance interactions. This is a roughly 24-month shift driven by Pro-then-Plus-then-free tier expansion, geography expansion, and Android/desktop platform expansion of what launched yesterday.

Observation 2 · Agentic flows arrive, with regulatory friction

The empirical signal: Intuit partnership named explicitly in the launch. Credit-card application flow and tax-filing flow named explicitly as forthcoming.

The forward shape: credit-card application from chat arrives first, likely Q4 2026 or Q1 2027. Tax filing from chat arrives second, likely 2027 tax season (Q1 2028). Investment trading, bill payment, and savings-account-switching follow in 2027-2028. Each agentic flow lands with a layer of regulatory engagement, partnership-mediated risk-shifting, and “powered by [Intuit / Plaid / specific licensed partner]” framing that preserves the read-only-AI-plus-licensed-rails structure the May 15 launch establishes.

Observation 3 · The incumbent reshuffling

The empirical signal: Plaid is the named rails partner. Intuit is the named transactional partner. The traditional-PFM category is in direct competition.

The forward shape: by end-2027, traditional PFM is largely extinct as a standalone category (Monarch, Copilot, YNAB persist as niche or pro tools; the mass-market PFM lives in chat). Robo-advisors face existential pressure — Betterment, Wealthfront, and similar are forced to either become chat-integrated (partnership) or accept commoditization. Banks become utility rails more visibly than they already are. Credit card issuers and lenders compete for chat-layer affiliate placement through Intuit and OpenAI’s partnership programs. Plaid wins as critical infrastructure. Intuit wins as transactional partner. Human financial advisors split — top-of-funnel commoditizes, fiduciary-tier advisors retain pricing power.

Observation 4 · The trust and regulatory framework adapts, slowly

The empirical signal: “Not a replacement for professional financial advice” + read-only + Pro/US-only + 30-day deletion + no account numbers + no changes.

The forward shape: as agentic flows arrive, the regulatory framework adapts incrementally. FINRA and SEC issue guidance on AI-mediated investment advice — likely 2027. CFPB issues guidance on AI-mediated lending recommendations — likely 2026-2027. State-level regulators engage variably, with California leading. The EU AI Act compliance framework applies in Europe from 2026 onward, classifying personal-finance AI as high-risk under Annex III. OpenAI’s path through this is partnership-mediated risk-shifting (the Intuit pattern) plus careful product design that keeps the chat layer outside the fiduciary perimeter while letting partners take the regulated actions.

What this is not

It is not the end of the bank. Banks have FDIC insurance, ACH routing, payroll direct deposit, regulatory protection. They get commoditized but not displaced.

It is not the end of the human financial advisor. Top-of-funnel compresses; bottom-of-funnel (fiduciary work, complex estate planning, behavioral coaching) preserves pricing power and may actually grow as the chat-layer surface generates more aware-but-confused consumers asking for guidance on harder questions.

It is not a clean win for OpenAI. Anthropic, Google, Meta, Apple Intelligence (forthcoming), Mistral (in Europe), and domestic Chinese AI firms in their respective markets all compete for the same chat-layer-as-finance-interface position. The 200-million-questions baseline at ChatGPT today is not durable if competitors execute. What’s structurally won is the category; who wins inside the category is open.

The synthesis observation

ChatGPT’s personal finance preview is the marker of the moment consumer financial intermediation starts moving from app-and-dashboard surfaces to conversational-AI surfaces. Yesterday’s launch is read-only, US-only, Pro-only, narrow in scope, careful in framing — and it is the most-significant consumer-fintech product launch in roughly a decade because of what it implies about where the category goes next.

The agentic transition crosses the regulatory frontier; the partnership architecture (Intuit, Plaid, ecosystem partners) is the structural mechanism for managing that crossing. The 24-month window is open. The incumbents that get reshuffled will be visible by Q4 2027. The European version will lag and look different. The free-tier rollout will determine whether the category-level shift happens at the scale the 200-million-questions baseline implies, or whether it remains a premium-subscription affordance for a smaller addressable user base.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the chat layer has taken delivery of a connected account, the dashboard renders out of the connected account, and the 200 million people who already arrive at ChatGPT with financial questions every month now have somewhere to put the actual answer.

That is the structural editorial question the bank account in the chat is sitting on top of. It is intermediation, not feature. It is distribution, not capability. It is the on-ramp to agentic consumer finance, not the destination. And it is the layer where the next generation of consumer-finance category leadership gets decided.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI agentic commerce & consumer-side intermediation track

This dispatch

- This piece · The bank account in the chat · structural reading of OpenAI’s personal-finance launch and what gets unbundled when 200 million conversations already live at the chat layer · structural-slate register

Forthcoming · the agentic commerce track

- Forthcoming · The agentic threshold · the architecture of how AI assistants cross from read-only to take-action-on-the-user’s-behalf · what statutory and contractual structure has to exist for this to scale · transition-bronze register

- Forthcoming · Plaid as rails · the structural position of data-aggregator infrastructure when the surface above it consolidates around AI chat · empirical-clay register

- Forthcoming · The PFM unbundling · what happens to Monarch / Copilot / YNAB / Empower when the 200-million-monthly-questions surface ships an integrated alternative · labor-rose register

- Forthcoming · The European architecture · PSD2 / PSD3 / FIDA / AI Act compliance frameworks and why the US rollout doesn’t translate · structural-slate register

- Forthcoming · The regulatory frontier · FINRA / SEC / CFPB / GLBA engagement with AI-mediated financial advice and agentic execution · synthesis-deep register

Adjacent tracks

- Post-Wire Piece 01 · The death of the identical paragraph · structural-economics on the wire’s collapse · adjacent intermediation-transfer analysis on the publisher side

- Post-Wire Piece 02 · Raw-feed licensing · the contract-forensic analysis of the missing licensing category in the publisher-to-AI flow · cross-references this piece’s discussion of how Intuit-style partnerships intermediate AI-mediated transactions

- The gigawatt gap · Why China is structurally positioned for AI power · the AI-energy infrastructure dispatch · adjacent industrial-policy analysis at a different layer of the AI stack

Sources

OpenAI launch announcement and direct coverage

- OpenAI blog · Personal finance ChatGPT preview · May 15 2026 · “preview of a new personal finance experience in ChatGPT” · Pro / US / web + iOS · openai.com/index/personal-finance-chatgpt/

- TechCrunch · OpenAI launches ChatGPT for personal finance · May 15 2026 · 12,000+ institutions · Plaid partnership · Hiro acquisition April 2026 · @Finances command · techcrunch.com

- MacRumors · ChatGPT connects to financial accounts · May 15 2026 · example queries · 200M monthly finance questions · GPT-5.5 Thinking · privacy controls · macrumors.com

- 9to5Mac · OpenAI releases new personal finance features · OpenAI quote: “securely connect your financial accounts, see a dashboard of where your money is going, and ask ChatGPT questions grounded in your financial context — all while staying in control of your data” · phased rollout language · 9to5mac.com

- CryptoBriefing · OpenAI launches ChatGPT personal finance preview · GPT-5.5 Thinking 79/100 · GPT-5.5 Pro 82.5/100 internal benchmark · 50+ finance professionals · financial memories · Intuit integration roadmap · cryptobriefing.com

- SiliconANGLE · OpenAI previews personal finance features · GPT-5.5 Thinking FinanceAgent 60% score · FrontierMath Tier 4 record · “available to everyone” eventual rollout · siliconangle.com

- The Tech Portal · OpenAI rolls out ChatGPT Personal Finance · 200M monthly finance questions · Plaid as financial-data connectivity provider · institution coverage · thetechportal.com

- SQ Magazine · ChatGPT personal finance dashboard · financial memories · 30-day data deletion · temporary chat exclusion · privacy protections · sqmagazine.co.uk

- Yahoo Tech · ChatGPT lets you connect bank accounts · OpenAI agentic-flow examples · credit card application + tax expert routing · tech.yahoo.com

- The News PK · OpenAI rolls out ChatGPT finance tools · use-case framing · contextual queries · thenews.com.pk

- CryptoBriefing · ChatGPT personal finance preview · Estefano Gomez analysis · GPT 5.5 Thinking + Pro scoring breakdown · ecosystem partner framing · cryptobriefing.com

Plaid partnership and account-aggregation infrastructure

- Plaid blog · What ChatGPT’s new experience signals · Will Robinson, Plaid CTO · 200M monthly finance questions baseline · 12,000+ institutions · 64% of AI-finance consumers say it improved product evaluation · 53% say day-to-day spending help · transaction foundation model 48% more accurate income classification · plaid.com/blog/chatgpt-personal-finance-plaid/

- Plaid platform documentation · AISP/PISP equivalent in US data-aggregator model · supported account types (checking, savings, credit cards, brokerage, retirement, mortgage, crypto wallets) · screen-scraping-to-API evolution · plaid.com

Benchmark and model framing

- OpenAI internal personal finance benchmark · developed with 50+ finance professionals · GPT-5.5 Thinking 79/100 · GPT-5.5 Pro 82.5/100 · evaluation of complex personal finance tasks · OpenAI blog disclosure

- FinanceAgent third-party benchmark · earnings-report analysis · agentic financial tasks · GPT-5.5 60% score · industry-standard reference for LLM financial reasoning

- FrontierMath Tier 4 · doctorate-level math evaluation · GPT-5.5 set record · referenced in launch as model-capability signal

Incumbent fintech and PFM industry context

- Monarch Money · Mint successor · approximately 1M paid users · subscription model · Plaid-integrated · target market: ex-Mint power users

- Copilot Money · Apple-ecosystem-focused PFM · smaller user base · subscription model · iOS-native

- YNAB (You Need A Budget) · approximately 2M users · zero-based budgeting · subscription model · methodology-driven

- Empower (formerly Personal Capital) · approximately 4M users · investment + budgeting hybrid · acquired by Empower Retirement

- Intuit Mint sunset · March 23 2024 · acquired by Intuit 2009 · ~25M users at peak · users migrated to Credit Karma

- Intuit Credit Karma · approximately 135M members US · credit + financial products marketplace · acquired by Intuit 2020 for $7.1B

- Intuit TurboTax · approximately 40M US consumer-tax users · IRS integration · state-tax authority integrations · category-leading position

- Hiro acquisition · OpenAI · April 2026 · backed by Ribbit · General Catalyst · Restive · consumer personal-finance startup · team described as “useful” in launching new feature

Regulatory framework references

- FINRA · Investment Advisers Act of 1940 · fiduciary perimeter · “investment advice” vs “general financial information” distinction · registration requirements

- SEC Regulation Best Interest (Reg BI) · 2019 · broker-dealer duty to retail customers · disclosure obligations · conflict-of-interest management

- CFPB · Section 1033 of Dodd-Frank · finalized October 2024 · consumer access to financial data · standardized APIs · phased compliance 2026-2030

- GLBA (Gramm-Leach-Bliley Act) · 1999 · financial privacy · NPI standards · safeguards rule · applies to connected-account data handling

- EU PSD2 · 2018 · open-banking mandate · AISP/PISP licensing · strong customer authentication · regulatory architecture US is belatedly catching up to

- EU PSD3 + PSR · proposed June 2023 · in trilogue · enters force 2026 with phased compliance · tightens PSD2 · expanded fraud-liability framework

- EU FIDA (Financial Data Access Regulation) · proposed in parallel with PSD3 · expands open-banking to savings, mortgages, loans, pensions, insurance, investments · broader than current Plaid US coverage

- EU AI Act · August 2024 force · phased compliance 2026-2027 · Annex III high-risk classification likely applicable to personal-finance AI · conformity assessment + transparency obligations

Companion-piece source backbone

- Post-Wire Piece 01 · The Death of the Identical Paragraph · Thorsten Meyer · adjacent intermediation-transfer analysis on the publisher side

- Post-Wire Piece 02 · Raw-Feed Licensing · Thorsten Meyer · partnership-mediated transactional architecture · Intuit/Plaid pattern echoes the wire-cooperative licensing framework

- The Gigawatt Gap · Thorsten Meyer · the energy-infrastructure dispatch · adjacent industrial-policy analysis at a different layer of the AI stack

Key Piece reference figures crystallized

- Launch date: May 15, 2026 · ChatGPT Pro · US · web + iOS · preview

- Distribution baseline: 200M monthly finance questions arriving at ChatGPT before account integration

- Institution coverage: 12,000+ financial institutions via Plaid · account types (checking, savings, credit cards, brokerage, retirement, mortgage, crypto wallets)

- Model: GPT-5.5 Thinking (default) · 79/100 internal benchmark · GPT-5.5 Pro 82.5/100 · FinanceAgent 60% · FrontierMath Tier 4 record · evaluated by 50+ finance professionals

- Agentic threshold: read-only at launch · Intuit integration forthcoming · credit-card application flow + tax-filing flow named explicitly

- Hiro acquisition: April 2026 · Ribbit / General Catalyst / Restive backed · team “useful” in launching feature

- Intermediation map: 7 tiers (banks · credit card issuers · brokerages/robos · traditional PFM · Plaid · Intuit · advisors) with differentiated impact pattern

- European architecture: PSD2 / PSD3 / PSR / FIDA / AI Act · structurally different from US Plaid-mediated rails · 12-18 month minimum lag to European launch

- Forward shape: chat-layer surface as default consumer-finance front door by mid-2027 · agentic flows arrive 2026-2028 · traditional PFM largely extinct as standalone category by end-2027 · robo-advisors face existential pressure · banks become utility rails · Plaid wins as critical infrastructure · Intuit wins as transactional partner