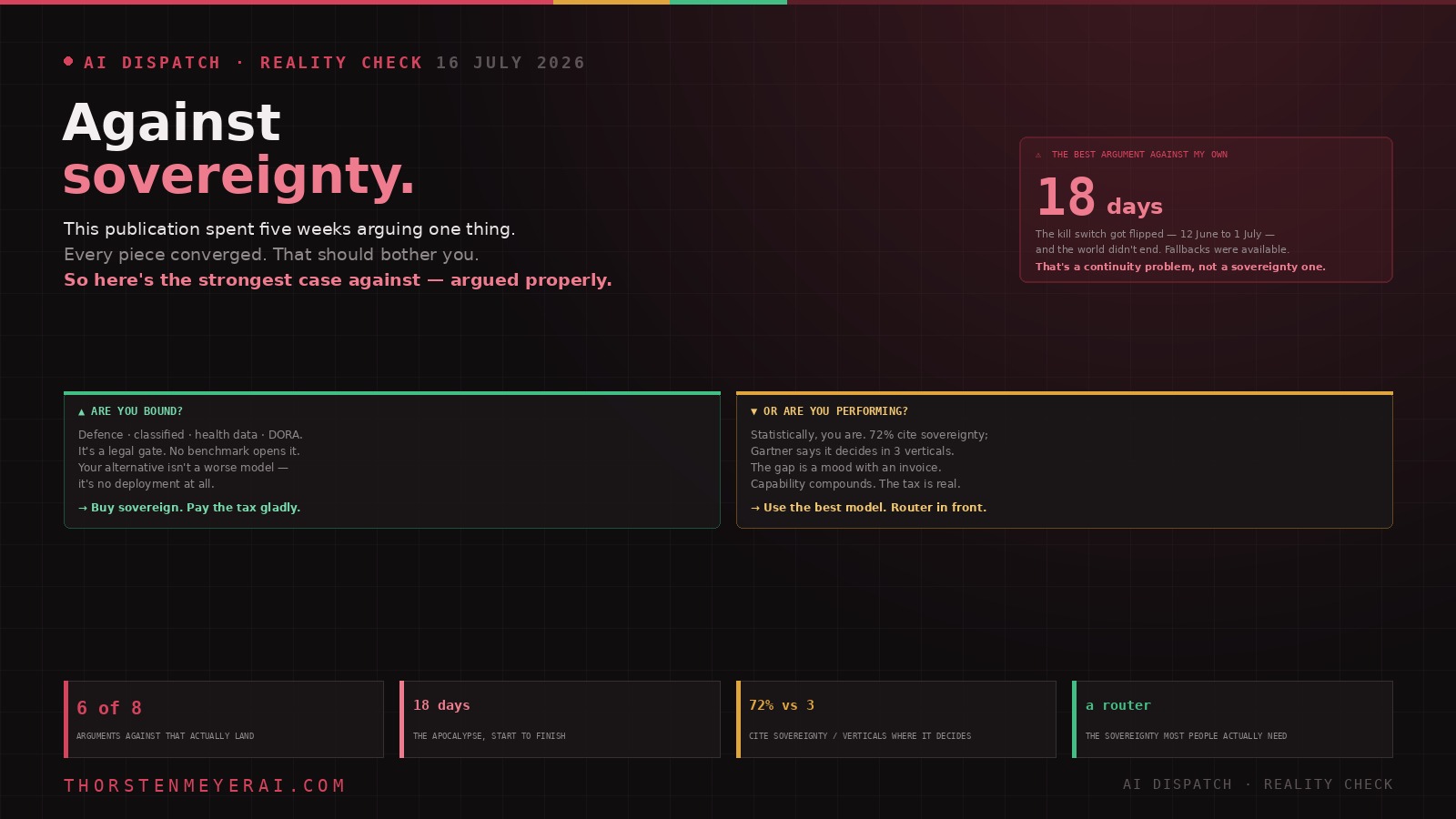

This publication has spent five weeks arguing one thing.

Own the model, not the API. Read the shareholder register. Check the VRAM. Watch who can switch you off. Every piece — the Forge trilogy, Inkling, Mistral, Cohere–Aleph Alpha, the Schwarz Group, the 24% rule, the Five Eyes question, even the read of Anthropic’s hiring year — converged on the same conclusion.

That convergence should bother you. It bothers me. When eight consecutive analyses reach the same verdict, you’re no longer running an analysis. You’re running a thesis, and the evidence has started arriving pre-sorted.

So here is the case against — argued properly, with the same evidence, turned around. Not a strawman erected to be knocked down. The version a smart CTO would put to me across a table, and which I have not yet answered in public.

The claim: for almost everyone, sovereignty is an expensive hedge against a risk they have mispriced, and the rational move is to use the best model available and get on with it.

Against sovereignty: the strongest case for just using the best model

This publication has spent five weeks arguing one thing — and every piece converged. That should bother you. It bothers me. When eight analyses reach the same verdict, you’re not running an analysis. You’re running a thesis, and the evidence has started arriving pre-sorted.

So here’s the case against — argued properly, with the same evidence, turned around. Not a strawman erected to be knocked down. The version a smart CTO would put to me across a table, and which I have not yet answered in public. The claim: for almost everyone, sovereignty is an expensive hedge against a risk they’ve mispriced — and the rational move is to use the best model and get on with it.

Defence · classified · national health data · DORA-bound finance. The foreign-legal-order risk isn’t theoretical and isn’t insurable by other means — it’s a legal gate. No benchmark opens it. Your alternative isn’t a worse model; it’s no deployment at all.

Statistically, you are. You have a reasonable, politically legible, entirely unbudgeted feeling — and an industry built to monetize it. The capability compounds, the tax is real, the opportunity cost is brutal, and 18 days is survivable.

I’ve spent five weeks arguing you should own your stack. The strongest case against says: for most of you, that’s an expensive way to be worse, sold by people whose real product is a feeling. And that case is mostly right. What survives is smaller and sharper — everything above the router line (the qualification programme, the owned cluster, the custom pre-training run, the €11B data centre) you should buy only if a law requires it, never because a narrative does. A router is the sovereignty most people actually need. 90% of the resilience for ~2% of the cost — and it would have made 12 June a non-event. So run the honest test: are you bound, or are you performing?

1. The capability gap is not a detail. It’s the product.

Five points on the Artificial Analysis index sounds like a rounding error. GLM-5.2 leads the open field at roughly five points behind Claude Opus 4.8. Close enough, surely?

No. At the agentic frontier, that margin is the difference between a run that completes and a run that dies at step seven. Look at the numbers this publication published itself: Inkling — the best American open-weight model, shipped with genuine fanfare — posts 77.6% on SWE-bench Verified against Fable 5’s 95.0%, and 63.8% on Terminal-Bench 2.1 against GPT-5.6 Sol’s 89.5%. On text-only Humanity’s Last Exam it manages 29.7% where Fable 5 reaches 53.3%.

Those aren’t rounding errors. That’s roughly a third of your agentic tasks failing that would otherwise have succeeded.

And it compounds. Better model → agent completes more tasks → more work automated → more value per engineer → faster iteration → better product. Take the sovereign option and you inherit that gap every day, forever, because the frontier keeps moving and your sovereign vendor keeps trailing it. Mistral’s own CEO says it out loud: we do not yet own the best language models. Mistral Large 3 scores below the median for comparable open-weight models and generates around 38 tokens per second — a speed that makes iterative agentic work feel like wading.

You are not buying sovereignty. You are buying a permanent capability discount, and paying extra for it.

LM Studio for Beginners: Run Private AI Models on Your Own Computer — No Cloud, No Code, No Subscription

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

2. Your threat model is probably wrong

Ask what actually happens to companies. Breaches. Outages. A vendor changing prices. A key engineer leaving. Ransomware. A misconfigured bucket.

Now ask what sovereignty insures against: a foreign government compelling your data through a legal order served on your cloud provider.

For the overwhelming majority of organizations, that has never happened and probably never will. You are buying insurance against someone else’s catastrophe — a real one, but not yours — with budget that could have bought insurance against the catastrophes that actually visit you. The DPIA line item that says residual CLOUD Act risk is, for most firms, a theoretical exposure sitting next to a dozen live ones nobody staffed.

And note what the sovereignty case rests on: structural argument, not incident. The 24% rule, the Five Eyes statutory architecture, the adequacy-scope gap — all of it reasons from what could happen given the legal architecture. That’s legitimate risk analysis. It’s also the same reasoning shape as every threat model that never fires.

Personal AI Servers: A Guide to Building Private AI Infrastructure for Secure, Offline and Self-Hosted Local LLMs for Data Privacy

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

3. The tax has a published rate

This publication has itself documented the cost, piece by piece, and never added it up. Do that now.

SecNumCloud is, per one CEO attempting it, ten times the complexity of ISO 27001 — 360+ criteria across 14 themes. In a decade, roughly nine or ten providers have qualified. That’s not a certification; it’s a moon programme.

Self-hosting needs 0.5–1 FTE at $75,000–100,000 a year — the largest line in the TCO, and it never ends. Owned GPUs carry a ~10× penalty at low utilization. The hardware floor is $2,000–20,000 a month, plus 25–40% for cooling. Break-even against budget APIs sits in the billions of tokens per month.

The sovereign premium is visible in the valuations. Cohere–Aleph Alpha priced at roughly 83× known ARR — that’s not a revenue multiple, it’s a sovereignty multiple. Schwarz is spending €11 billion against a €1.9 billion division — 5.8×. Mistral has raised $3–5.5 billion against $400M ARR and has never disclosed a loss figure.

And the products are worse. Vibe is bare-bones next to ChatGPT and Claude — TechCrunch noted Claude is more popular than Mistral’s models among founders at Station F, in Paris. Inkling’s open weights need 2 TB of VRAM at BF16, 600 GB even quantized — open weights you cannot run. Forge has no public price at all.

Add it up and the sovereign path costs more, ships slower, performs worse, and locks you in harder. The exit alone runs 12–18 months of project work.

ASRock Intel Arc Pro B70 Creator 32GB Workstation Graphics Card, Xe2-HPG, 32GB GDDR6, PCIe 5.0, 4X DP 2.1, Blower Fan, Vapor Chamber, Honeywell PTM7950

- System Compatibility: Measures 271 x 112 x 39 mm

- Power Requirements: Requires 12V-2×6-pin connector

- Customer Support: Direct Amazon contact for assistance

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

4. The opportunity cost nobody prices

Here’s the argument that should worry a European founder most, and it appears in none of this publication’s coverage.

The quarter you spend on SecNumCloud qualification is a quarter your competitor spends shipping. The FTE you assign to keeping a GPU cluster healthy is an engineer not building product. The year you spend evaluating Forge against a RAG baseline is a year of compounding for whoever just called the best API and moved on.

Compound that over three years. The sovereign company has a compliant, auditable, jurisdictionally pristine stack — and a product two years behind. The tourist company has customers.

Sovereignty is a fixed cost that buys no capability. Everything you spend on it is spent proving you could have data nobody was going to ask for.

Train It. Tame It. Teach It.: Build Your Personal AI Team and Get Every Model to Work Your Way (The AI Practitioner's Edge)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

5. Protectionism is wearing a security badge

Look honestly at the 24% rule. It is not a security control. Encryption is a security control; key custody is a security control. An ownership cap is an industrial policy that happens to have a security rationale attached.

The Cross-Border Data Forum’s critique deserves more than the one paragraph I gave it: SecNumCloud is explicitly protectionist, arguably breaches the EU’s own trade commitments on non-discrimination and national treatment, and — like China — forces foreign firms into local joint ventures to reach the market. They predicted the outcome exactly. S3NS is Thales+Google. Bleu is Capgemini+Orange on Azure. The rule didn’t produce European technology. It produced European rent extraction on American technology.

And the tell is what happened to EUCS High+: the sovereignty tier died because member states and industry called it discriminatory. If the ownership criteria were genuinely about security, the security community would have defended them. It didn’t. France did.

If the rule were about protecting data, it would test data protection. It tests shareholders.

6. The kill switch got flipped — and the world didn’t end

This is the strongest argument against my own position, and it uses my own headline story.

The entire sovereignty thesis of the last month rests on one event: the Commerce Department directive of 12 June that pulled Fable 5 and Mythos 5 worldwide.

They came back on 1 July. Eighteen days.

Sit with that. The apocalyptic scenario that anchors every “own your stack” argument actually happened — and it was an eighteen-day outage of one vendor’s flagship model, resolved, with fallback models available throughout.

If your business cannot survive eighteen days of one vendor being degraded, you do not have a sovereignty problem. You have a business continuity problem — and the fix is a $200-a-month router and a fallback tier, not an €11 billion data centre or a multi-year qualification programme.

The event that supposedly proves the thesis actually demonstrates its opposite: the market’s resilience mechanisms worked. Access was restored, competitors were available, and anyone with a gateway in front of their stack barely noticed.

7. Sovereignty is a symptom, not a strategy

Notice who talks about AI sovereignty.

The United States doesn’t. It has OpenAI and Anthropic. China doesn’t. It has DeepSeek, Qwen, GLM, and Kimi — which, as this publication has documented, are better than Europe’s and equally open.

Europe talks about sovereignty because Europe doesn’t have a frontier lab. Sovereignty discourse is what a region produces when it can’t produce models. It is the vocabulary of the trailing party, dressed as principle.

And the numbers are unkind. Mistral at ~$23B against US labs north of $850B — not a peer, a different weight class. Gartner’s read is that the sovereignty argument is genuinely decisive in three verticals, not the economy. Futurum found Forge’s addressable market narrower than pitched because 42% of organizations still spend more than half their time wrangling data — they’re not ready for the capability they’re being sold.

You cannot audit your way to a frontier model. Every euro spent on certification is a euro not spent on compute, and compute is what makes models. Europe has chosen to regulate the thing it hasn’t built.

8. And the market is full of tourists

Two numbers from this publication’s own reporting, placed side by side:

CISPE: ~72% of European enterprise IT decision-makers cite data sovereignty as a primary or secondary factor in vendor selection.

Gartner: the sovereignty argument is decisive in roughly three verticals — finance under DORA, healthcare, public sector and defence.

Those cannot both describe the same reality. The gap between them is people performing a preference and calling it a requirement.

Most of that 72% has no legal obligation. They have a feeling — a reasonable, politically legible, entirely unbudgeted feeling — and vendors have built an industry to monetize it. That’s not a market. That’s a mood with an invoice.

What survives the argument

Now the honest part, because a steelman you can’t answer is just a change of mind.

Six of those eight arguments land. The capability gap is real and I’ve been underweighting it. The tax is enormous and I’ve reported the pieces without summing them. The opportunity cost is real and I’ve never priced it. The protectionism critique is stronger than the one paragraph I gave it. The eighteen-day kill switch genuinely undercuts the apocalyptic framing. And the tourist problem is real — most of that 72% is performing.

Two don’t.

“Your threat model is probably wrong” is right about most buyers and irrelevant to some. For a defence ministry, a classified programme, a hospital under national health-data law, or a bank under DORA, the foreign-legal-order risk isn’t theoretical and isn’t insurable by other means. It’s a legal gate. No benchmark score opens it. For those buyers, “just use the best model” isn’t a trade-off — it’s not an option that exists. The argument doesn’t apply; it just isn’t addressed to them.

And “sovereignty is a symptom” proves too much. Yes, Europe talks about sovereignty because it lacks a frontier lab. But the absence of a lab is exactly why the exposure is real. “You’re only worried because you’re dependent” isn’t a rebuttal of dependence. It’s a description of it.

The synthesis

So the honest position is narrower and more useful than the one I’ve been arguing:

Sovereignty is not a virtue. It’s a requirement — for some.

If you are legally bound — defence, classified, DORA, national health data — buy sovereign, pay the tax gladly, and stop apologizing for the benchmark gap. Nothing in the case against applies to you, because your alternative isn’t a worse model. It’s no deployment at all.

If you are not bound — and statistically, you are not — then the case against is largely right. Use the best model. The capability compounds, the tax is real, the opportunity cost is brutal, and eighteen days is survivable.

And here’s the part that should sting the people selling to the 72%: the tourists make the products worse for the people who have no choice. When vendors optimize for buyers performing a preference, they build marketing — badges, frameworks, Gaia-X memberships, “sovereign” clouds with US parents. When they optimize for buyers who are legally bound, they build SecNumCloud, air-gap, and exportable weights. The mood is crowding out the requirement.

The take

I’ve spent five weeks arguing you should own your stack. The strongest case against says: for most of you, that’s an expensive way to be worse, sold by people whose real product is a feeling.

And that case is mostly right.

What survives is smaller and sharper: a router is the sovereignty most people actually need. A model-agnostic gateway, a fallback tier, an eval harness, and a documented exit. That’s 90% of the resilience for maybe 2% of the cost — and it would have made 12 June a non-event for anyone who had one. Everything above that line — the qualification programme, the owned cluster, the custom pre-training run, the €11 billion data centre — you should buy only if a law requires it, never because a narrative does.

So run the honest test on yourself. Are you bound, or are you performing?

If you’re bound, you already know, and this whole argument was never addressed to you — go read the shareholder register and check the VRAM.

If you’re performing: use the best model, put a router in front of it, and spend the difference on shipping.

That’s not a retreat from the thesis. It’s the thesis with the tourists removed — which is the only version worth defending.

Sources: all figures in this piece are drawn from this publication’s own prior reporting and the sources cited there — capability comparisons (GLM-5.2, Inkling, Fable 5, GPT-5.6, Mistral Large 3) via Artificial Analysis and vendor-published benchmark tables, all self-reported and awaiting independent replication; self-hosting economics (DevOps FTE, ~10× idle penalty, GPU floor, cooling, break-even) via Costlens, Alpacked, AceCloud and DigitalApplied; SecNumCloud complexity and qualified-provider count via ANSSI’s catalogue and Scalingo; the 83× multiple and €11B/€1.9B figures via TechCrunch, Handelsblatt-derived reporting and Data Center Dynamics; Mistral’s ARR, funding and Station F observation via Forbes, Sacra and TechCrunch; the Cross-Border Data Forum’s protectionism critique and the EUCS High+ collapse via those outlets and Legiscope; CISPE’s 72% survey and Gartner’s vertical assessment via trade coverage; Futurum’s data-maturity finding; the 12 June Commerce directive and 1 July restoration per contemporaneous reporting; Gartner’s 12–18-month cloud-exit estimate. Where this piece argues against positions taken in earlier articles here, that is deliberate. Not investment or legal advice. Analysis and framing are the author’s.