The bridge.

Read the headlines and you would think the AI data center runs on nuclear power. Meta signs three nuclear deals for up to 6.6 gigawatts. Microsoft restarts Three Mile Island. Amazon buys a campus next to the Susquehanna plant. Google signs the first corporate small-modular-reactor agreement. The pipeline of conditional SMR offtake agreements jumped from 25 gigawatts at the end of 2024 to 45 gigawatts a year later. The nuclear procurement rush is real, unprecedented, and accelerating.

Read the construction schedules and a different picture appears. Microsoft’s Three Mile Island restart delivers 835 megawatts — in 2027. Meta’s Oklo campus targets first reactors in 2030. Google’s Kairos SMRs come online between 2030 and 2035. The nuclear power the hyperscalers are buying mostly arrives at the end of this decade or the next. The data centers need power in the next eighteen to twenty-four months.

That gap — between when the power is needed and when the nuclear arrives — is the whole story. Grid interconnection now takes three to seven years in constrained US markets, and up to thirteen in parts of Europe; a data center takes eighteen to twenty-four months to build. The math does not work if you wait for the grid, and it does not work if you wait for the reactor. So something has to fill the gap. That something is gas.

The thing actually being built right now, behind the meter, at the data centers, is natural gas generation. Energy researchers are tracking more than 40 gigawatts of announced behind-the-meter and co-located generation — Meta, Amazon, Microsoft, Google, Oracle, xAI, Crusoe — and near-term it is dominated by gas turbines, reciprocating engines, and fuel cells. The nuclear deals buy the end of the decade. Gas builds the present. The bridge between them is the actual energy story of the AI buildout, and it is mostly fossil.

The structural argument I want to make: the AI industry’s nuclear procurement rush is real and rational, but it is a long-dated bet on certainty and a clean-energy narrative — not a near-term supply solution — because the nuclear capacity arrives at the end of the decade while the data centers need power now, which means the actual bridge being built today is behind-the-meter natural gas, and the gap between the nuclear narrative and the gas reality is where the AI buildout’s true energy and emissions story lives. This is the third dispatch in the AI Energy track, and it completes the arc the first two opened: The gigawatt gap measured the demand, The queue measured the grid delay, and this measures what fills the gap while the permanent solutions arrive.

The headline integrative finding: The honest both-sides read is that the nuclear rush is neither greenwashing nor salvation — it is a genuine signal sent on the wrong timeline. Genuine, because the hyperscalers really are willing to pay a premium for firm, carbon-free baseload (a 15-25% lease premium on power-certain sites), and that demand is accelerating the commercialization of advanced nuclear in a way nothing else has. Wrong timeline, because SMRs remain commercially unproven (no commercial SMR yet operates in the US; the Vogtle conventional build ran seven years late and $18 billion over), so the capacity cannot arrive on the schedule the AI buildout needs. The deepest point is that the gap between the two timelines is being filled by gas, and that gas is being built behind the meter — on-site, off-grid — partly to move fast and partly to route around the climate regulation and grid scrutiny that front-of-the-meter power would face. The nuclear deals are the story the industry tells; the gas turbines are the infrastructure it builds. Whether the bridge is temporary (gas until nuclear arrives) or permanent (gas because nuclear keeps slipping) is the question that decides the AI buildout’s true carbon cost — and it is genuinely unresolved.

This essay walks the nuclear rush, the timeline mismatch, the gas bridge that fills it, the behind-the-meter shift, the turbine bottleneck that constrains even the bridge, the emissions reckoning, and the structural reading of a buildout whose narrative and infrastructure diverge.

The bridge.

Why the AI buildout runs

on a nuclear story and

a gas reality.

to early 2026 · the real rush

2027-2035, grid 3-7 years

generation · near-term mostly gas

(~10M cars) · Cornell analysis

- A data center is built in under two years

- Data center electricity use +17% in 2025, doubling by 2030

- Gartner: 40% of AI data centers electricity-constrained by 2027

- Three Mile Island ~2027 · Oklo ~2030 · Kairos 2030-2035

- No commercial SMR yet operates in the US

- Grid interconnection 3-7 years (up to 13 in Europe)

early 2030s

· mostly gas

The industry leads with the nuclear it has bought for the end of the decade and builds the gas it needs for now — and sites that gas behind the meter where it moves fastest and shows least. The behind-the-meter siting is the tell that the bridge will be here longer than the word implies.Thorsten Meyer · The Bridge · AI Energy 03

By Thorsten Meyer — June 2026

This is the third dispatch in the AI Energy & Infrastructure track — the physical-constraint forensics of the AI buildout. The first walked the gigawatt gap between AI’s power demand and available supply; the second walked the interconnection queue that delays new capacity. This one walks what the industry is actually building to bridge the gap while it waits — and finds the headline (nuclear) and the infrastructure (gas) telling different stories.

The structural argument I want to make: there are two energy stories about AI, and they are both true and they are different — the procurement story (nuclear, clean, firm, long-dated) and the construction story (gas, fast, fossil, behind the meter) — and the industry leads with the first while building the second, because the first is the future it has bought and the second is the present it has to power. The divergence is not a lie; it is a timeline. The nuclear is real and coming; the gas is real and here; and the years between them are the bridge.

The headline integrative finding: The AI buildout’s energy reality is a bridge made of gas, sold under a banner of nuclear. The hyperscalers are doing both things genuinely — paying premiums for future clean baseload and building gas turbines for present firm power — and the gap between them is measured in years, emissions, and the open question of whether the bridge ever ends. If SMRs commercialize on schedule, the gas is a genuine bridge and the nuclear narrative comes true late. If SMRs keep slipping — as nuclear construction reliably does — the bridge becomes the destination, and the AI buildout is a gas buildout wearing a nuclear story. The honest position is that no one yet knows which, and the behind-the-meter siting of the gas is a tell that the industry is hedging toward speed over sequencing.

This essay walks the nuclear rush (Section I), the timeline mismatch (Section II), the gas bridge (Section III), the behind-the-meter shift (Section IV), the turbine bottleneck (Section V), the emissions reckoning (Section VI), and the structural reading (Section VII).

Natural Gas Conversion Kit Compatible with Duromax XP12000EH Generator 12KW LP 18HP Dual Fuel LP

- Natural Gas Inlet: Uses existing carburetor port

- Gasoline Compatibility: Retains ability to run on gasoline

- Easy Switch: Reconnect propane hose to revert

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

I · The nuclear rush · the story the industry tells

The procurement crystallization. The nuclear procurement is real, large, and accelerating — and understanding how real it is matters, because the argument is not that the nuclear is fake. It is that the nuclear is late.

The deals

Restarts, uprates, and SMRs: the hyperscalers have moved on every available form of nuclear. Microsoft’s Constellation deal restarts Three Mile Island Unit 1 (835 MW, online ~2027). Amazon’s deals with Talen (a 1.92 GW PPA from Susquehanna) and X-energy (SMR deployment). Meta’s three nuclear PPAs (up to 6.6 GW) plus the Oklo 1.2 GW campus in Ohio (16 Aurora reactors). Google’s Kairos SMR agreement (Hermes 2, Tennessee). Constellation’s ~1 GW of uprates and $3.9 billion capital plan. By end-2024, US nuclear PPAs totaled more than 16 GW of contracted capacity, the majority tied to data center demand — and the SMR offtake pipeline reached 45 GW by early 2026.

Why the hyperscalers want it

Firm, carbon-free baseload: data centers need 24/7 power, and nuclear provides steady, dispatchable, carbon-free baseload in a way intermittent renewables cannot. The hyperscalers have public 100%-renewable and 24/7-carbon-free commitments, and nuclear is the firm clean option that fits them. Many data center companies will pay a premium for SMR power specifically because of the reliable, clean baseload it promises — power certainty has become the primary differentiator in site selection, and nuclear-backed sites command a 15-25% lease premium.

Why it is a genuine signal

AI is accelerating nuclear’s commercialization: the data center demand is doing for advanced nuclear what no policy has — creating concentrated, creditworthy, 24/7 offtake demand that finances restarts, uprates, and SMR development. The IEA notes AI could accelerate the commercialization of these new energy technologies. The nuclear rush is not a marketing exercise; it is a real demand signal that is genuinely moving the nuclear industry. That is exactly why it deserves to be taken seriously enough to ask when the power actually arrives.

The nuclear-rush observation

The nuclear procurement rush is real, unprecedented, and accelerating — restarts (Three Mile Island), uprates (Constellation), and a 45 GW SMR offtake pipeline, the majority tied to data centers willing to pay a 15-25% premium for firm carbon-free baseload. It is a genuine demand signal that is moving the nuclear industry. The argument that follows is not that the nuclear is fake — it is that the nuclear is late: this real, accelerating procurement mostly delivers power at the end of the decade, and the data centers need it now.

Digital Turbine Flow Meter Digital LCD Display with NPT Counter Gas Oil Fuel Flowmeter for Measure Diesel Kerosene Gasoline

- Compact and Lightweight: Easy to operate and install

- Modular Design: Compatible with modules and sensors

- Digital LCD Display: Shows flow rates and totals

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The timeline mismatch · when the power arrives versus when it is needed

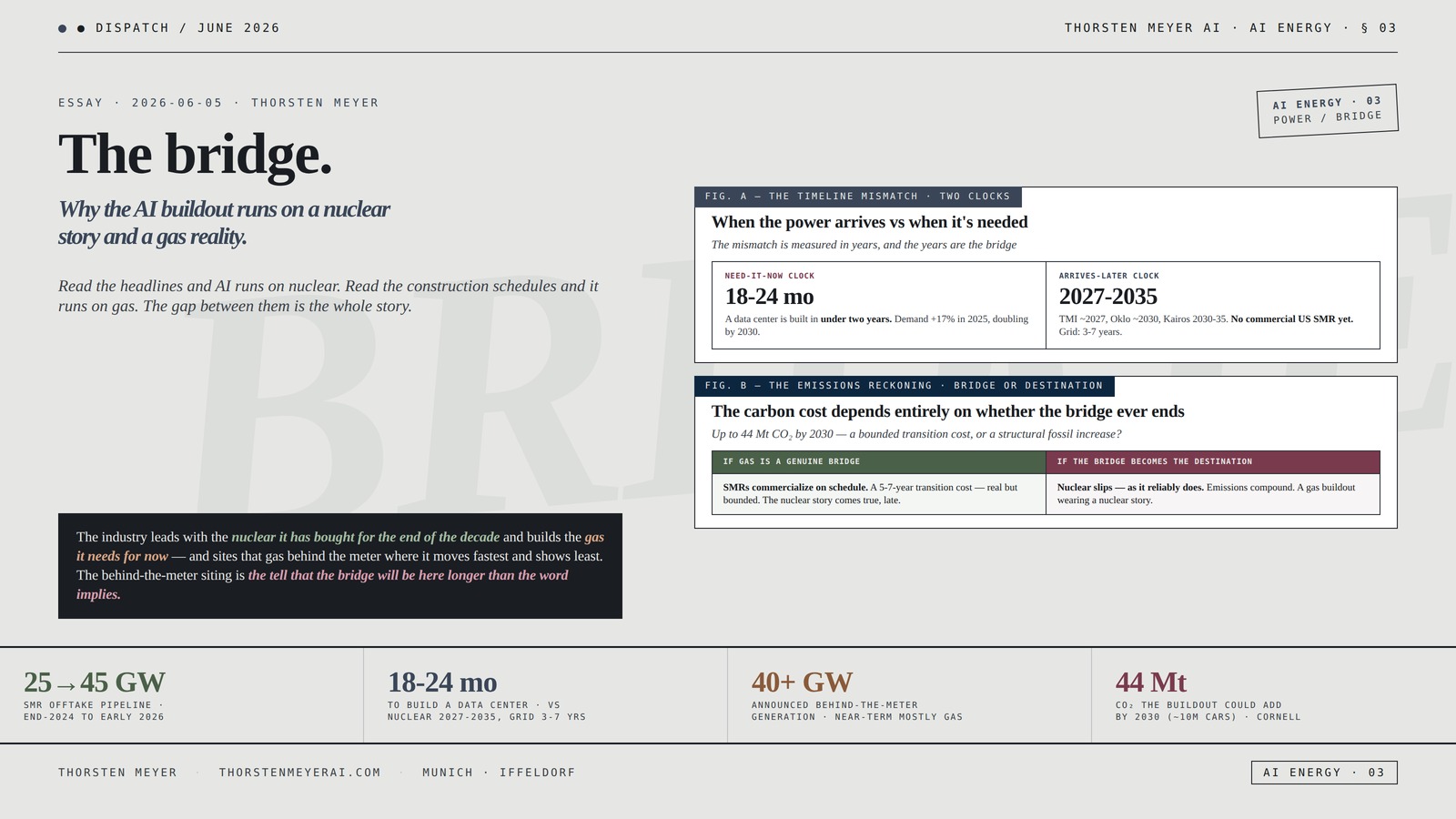

The temporal crystallization. The center of the whole piece is a mismatch between two clocks: the clock on which nuclear (and grid) power arrives, and the clock on which data centers need it. The mismatch is measured in years, and the years are the bridge.

The need-it-now clock

Data centers build in 18-24 months: a data center takes roughly eighteen to twenty-four months to construct. AI demand is accelerating — data center electricity use rose 17% in 2025, AI-focused use faster, and consumption is set to double by 2030. The demand is here now and growing fast; the facilities go up in under two years.

The arrives-later clock

Nuclear arrives 2027-2035: Three Mile Island ~2027; Meta’s Oklo first reactors ~2030; Google’s Kairos SMRs 2030-2035. No commercial SMR yet operates in the US. The nuclear power being procured now mostly arrives three to eleven years out — and SMRs, the largest part of the pipeline, are the least proven and most likely to slip.

The grid is no faster: the alternative to building your own power is connecting to the grid — but interconnection queues run three to seven years in constrained US markets and up to thirteen in parts of Europe, and a March 2026 survey found time-to-power now runs 1.5-2 years longer than expected. Both permanent options — nuclear and the grid — arrive on a clock measured in many years. The data center’s clock is measured in months.

The gap is the bridge

Years of demand with no permanent supply: the mismatch creates a multi-year window where the demand exists, the facility is built, and neither the nuclear nor the grid connection has arrived. That window — call it 2026 to the early 2030s — is the bridge, and it has to be powered by something that can be built in months, not years. Gartner forecasts that by 2027, 40% of AI data centers will be operationally constrained by electricity deficits. The gap is not hypothetical; it is the binding constraint.

The mismatch observation

The AI buildout runs on two clocks: data centers build in 18-24 months, while nuclear arrives 2027-2035 and grid interconnection takes 3-7 years (up to 13 in Europe) — so there is a multi-year window where demand exists and neither permanent supply has arrived. That window is the bridge, and it must be powered by something buildable in months. The nuclear rush addresses the end of the decade; the bridge addresses now — and the two are different problems with different solutions, which is why the headline (nuclear) and the construction (gas) diverge. The mismatch is the hinge of the entire energy story.

Generator Fuel Gauge for Generac 0H9005 GP5500 GP6500 RS5500 RS7000E GP7500E RS8000E XT8000E XT8500EFI, 5500w 6500 6500w 7500 389cc OHV Portable Generator

- Compatible with Generac models: Fits 5-8kW Generac generators

- High-quality durable construction: Made of thickened, long-lasting material

- Proper size for easy installation: Rubber side: 1.10in, Surface side: 1.25in

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The gas bridge · what actually fills the gap

The infrastructure crystallization. What fills the multi-year gap is natural gas — built fast, built on-site, built now. This is the infrastructure story, and it is the one the headlines underplay.

Gas is the fast option

Buildable on the data center’s clock: natural gas generation — combined-cycle and simple-cycle turbines, reciprocating engines, fuel cells — is the fastest practical path to large-scale firm power. It can be sited at the data center and brought online far faster than nuclear or a grid connection. Gas is the only firm-power option that fits inside the 18-24-month data center build clock — which is precisely why it, not nuclear, is what gets built for near-term need.

The scale of the gas build

40+ GW of behind-the-meter and co-located generation: energy researchers track more than 40 GW of announced behind-the-meter and co-located generation, dominated near-term by gas. Nearly half the power plants under construction in Texas will serve data centers exclusively, without connecting to the grid. OpenAI’s Stargate campus in Abilene, Meta’s El Paso data center (813 modular generators), the proposed $165 billion Project Jupiter in New Mexico (gas microgrids). The gas buildout is not a handful of edge cases; it is a structural shift adopted across every major hyperscaler.

Gas as the explicit bridge

Framed as temporary — by some: some operators explicitly frame gas as a bridge — temporary generation until grid power or cleaner options arrive. Next-generation gas (combined-cycle at ~60% efficiency, selective catalytic reduction, low-NOx burners) is cleaner than diesel or coal, and fuel cells offer fast, lower-emission interim power. The charitable read: gas is a genuine bridge, the cleanest fast-deployable firm power, holding the line until nuclear and the grid catch up. Whether that read holds depends on whether the bridge ever ends — Section VII’s question.

The gas-bridge observation

What actually fills the multi-year gap is natural gas — combined-cycle and simple-cycle turbines, reciprocating engines, fuel cells — because it is the only firm-power option buildable on the data center’s 18-24-month clock, and 40+ GW of behind-the-meter and co-located generation is being built across every major hyperscaler. Gas is the infrastructure story the nuclear headlines underplay. Some operators frame it explicitly as a temporary bridge to nuclear and the grid — and that framing is the optimistic case. The pessimistic case is that the bridge becomes permanent, which is decided not by intention but by whether nuclear arrives on time.

Comprehensive Guide to Small Modular Reactors (SMRs)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The behind-the-meter shift · why the gas goes off-grid

The siting crystallization. The gas is not just being built — it is being built behind the meter, on-site, off-grid. That siting choice is the most revealing detail in the whole story, because it is partly about speed and partly about avoiding scrutiny.

What behind-the-meter means

On-site generation, bypassing the grid: behind-the-meter (BTM) generation builds dedicated power assets on the same site as the data center, rather than relying on grid interconnection and the wholesale market. The pivot is sharp enough to have a name — Bring Your Own Generation (BYOG) — adopted by Meta, Amazon, Microsoft, Google, Oracle, xAI, Crusoe. The data center becomes its own power plant, disconnected from the grid it would otherwise wait years to join.

Why speed drives it

It compresses the interconnection wait: BTM generation compresses a multi-year interconnection wait into a timeline measured in months. When the grid queue is 3-7 years and the turbine is buildable in 1-2, building your own power on-site is the rational response to the time-to-power mismatch. The primary driver is speed — BTM is the answer to “the math doesn’t work if you wait for the utility.”

Why scrutiny-avoidance also drives it

Off-grid routes around regulation: here is the revealing part. Remaining behind the meter lets a project avoid some of the regulatory approval that grid-connected generation faces. The Project Jupiter gas microgrid in New Mexico, by staying behind the meter, avoids seeking approval from regulators who would enforce the state’s climate laws — even though its emissions could outweigh New Mexico’s recent climate gains. Behind-the-meter is partly a speed choice and partly a scrutiny choice: on-site gas faces less climate-regulatory and grid-impact review than the same gas connected to the grid. That is the tell.

The behind-the-meter observation

The gas is being built behind the meter — on-site, off-grid, as Bring Your Own Generation across every major hyperscaler — partly because it compresses the multi-year interconnection wait into months, and partly because off-grid siting routes around the climate regulation and grid scrutiny that front-of-the-meter power faces. The speed motive is legitimate; the scrutiny-avoidance motive is the tell. A buildout confident its gas was a clean temporary bridge would not need to site it where the climate regulators cannot see it. The behind-the-meter shift is the industry hedging toward speed over sequencing — and quietly toward fossil over the scrutiny that fossil would otherwise attract.

V · The turbine bottleneck · the bridge is constrained too

The supply-chain crystallization. Even the gas bridge is not friction-free. The turbines that build it are themselves scarce — booked solid for years — which means the bridge is rate-limited by the same kind of bottleneck that constrains everything else in the buildout.

The three-manufacturer chokepoint

Booked into the next decade: large-scale gas turbines come from effectively three manufacturers — GE Vernova, Siemens Energy, Mitsubishi Heavy Industries — and all three are reporting order backlogs stretching roughly five years, with delivery slots sold into the next decade. Siemens Energy reports a record €136 billion backlog; GE Vernova has ~55 GW of gas orders queued; Mitsubishi is sold out into 2028. The single most important piece of equipment for the gas bridge is the most scarce.

The capacity cannot ramp fast

Burned by the last cycle: the manufacturers, remembering the post-2018 overcapacity, did not rush to expand — and even if all three deliver their expansion plans, total output might rise only 20-25%, nowhere near demand. GE Vernova targets ~20 GW annualized output in 2026. The turbine supply chain cannot scale fast enough to power the buildout it is being asked to power — the bridge has its own gigawatt gap.

The workarounds reveal the strain

Down the stack to faster options: the backlog pushes developers toward faster, smaller, often costlier options — solid-oxide fuel cells (shippable in months, but $3,000+/kW), large reciprocating engines, aeroderivative turbines (repurposed aircraft engines, faster ramp), modular 10-15 MW engine blocks that scale incrementally. The scramble down the equipment stack — paying premiums for speed — is the same pattern as the whole buildout: when the preferred firm-power option is backlogged, pay more for the faster alternative.

The turbine-bottleneck observation

Even the gas bridge is rate-limited: large turbines come from three manufacturers (GE Vernova, Siemens, Mitsubishi) booked five years out, capacity can rise only 20-25% even with expansion, and developers are scrambling down the stack to fuel cells, reciprocating engines, and aeroderivatives — paying premiums for speed. The bridge has its own gigawatt gap. This matters because it means the gas bridge is not an unlimited fallback: it is constrained, expensive, and scrambling — which both slows the buildout and, perversely, locks in whatever gas does get built, because equipment this hard to acquire does not get decommissioned the moment nuclear arrives. The bottleneck makes the bridge stickier.

VI · The emissions reckoning · what the bridge costs

The carbon crystallization. The bridge has a price beyond dollars, and it is the part the nuclear narrative most obscures. The gas being built now emits — and the behind-the-meter siting means much of it emits with less scrutiny than grid power would face.

The carbon cost

A measurable addition: the gas buildout adds real emissions. A Cornell analysis found the data center buildout could add as much as 44 million metric tons of CO₂ by 2030 — equivalent to the annual emissions of about 10 million passenger vehicles. Meta’s own carbon footprint rose 20% to 8.2 million tonnes as AI data centers demanded more power. The bridge is fossil, and the fossil emits — the buildout’s clean-energy narrative is running alongside a measurable emissions increase.

The commitment tension

Gas versus the pledges: every major hyperscaler has 100%-renewable or 24/7-carbon-free commitments, and behind-the-meter gas creates direct tension with them. The industry reconciles this partly through the nuclear narrative (the future is clean), partly through carbon-matching and offsets (Meta matches 100% renewable while emissions rise), and partly by not connecting the gas to the grid where its impact would be most visible. The nuclear procurement is, among other things, the clean-energy story that offsets the gas-construction reality in the public ledger — the future purchase that narratively balances the present build.

Why this is the reckoning

The bridge’s permanence decides the carbon: if gas is a genuine 5-7-year bridge to nuclear, the emissions are a transition cost — real but bounded. If gas becomes permanent because nuclear slips (as nuclear reliably does), the emissions compound indefinitely, and the AI buildout is a structural increase in fossil generation. The carbon cost of the AI buildout is not yet determined; it depends entirely on whether the bridge ends — and the behind-the-meter siting, the turbine lock-in, and nuclear’s track record all tilt toward the bridge lasting longer than advertised.

The emissions observation

The gas bridge has a carbon cost the nuclear narrative obscures: the buildout could add up to 44 million tonnes of CO₂ by 2030, in direct tension with hyperscaler climate commitments, reconciled partly through the clean-nuclear future-purchase and partly through behind-the-meter siting that keeps the gas out of the most scrutinized ledgers. Whether this is a bounded transition cost or a structural fossil increase depends on whether the bridge ends. And every structural tell — the behind-the-meter siting, the turbine lock-in, nuclear’s reliable slippage — tilts toward the bridge lasting longer than “temporary” implies, which means the emissions are likelier to compound than to bound.

What this is not

It is not a claim the nuclear is fake. The procurement is genuine and is genuinely accelerating advanced nuclear. The claim is about timing — the nuclear is late relative to the need, not unreal.

It is not a claim that gas is irrational. Gas is the cleanest fast-deployable firm power, and the bridge is a defensible engineering response to the timeline mismatch. The claim is about what the bridge’s permanence and siting reveal.

It is not a prediction that SMRs fail. They may commercialize on schedule and vindicate the nuclear narrative. The claim is that they are unproven and historically slip, which makes the bridge’s end-date uncertain.

The synthesis observation

The AI industry’s nuclear procurement rush is real and rational but long-dated — a bet on future certainty and a clean-energy narrative — while the actual bridge being built today is behind-the-meter natural gas, and the gap between the nuclear story and the gas reality is where the buildout’s true energy and emissions cost lives. The procurement story (nuclear, clean, firm, 2030s) and the construction story (gas, fossil, off-grid, now) are both true and different; the years between them are the bridge; and whether the bridge is temporary or permanent is the unresolved question that decides the carbon.

There is no single answer. Anyone offering one is selling something. What is unambiguous is that the headline and the infrastructure diverge: the industry leads with the nuclear it has bought for the end of the decade and builds the gas it needs for now, and it sites that gas behind the meter where it moves fastest and shows least. The nuclear deals are the story; the gas turbines are the building. If SMRs arrive on schedule, the gas was a bridge and the story comes true late. If they slip — as nuclear construction reliably does — the bridge becomes the destination, and the AI buildout is a gas buildout wearing a nuclear narrative. The behind-the-meter siting is the tell that the industry is hedging toward speed over sequencing, which is to say toward the gas being here longer than the word “bridge” implies.

That is the structural editorial question the bridge sits on top of. It is a real nuclear procurement arriving on the wrong clock. It is a gas bridge built fast and sited quiet. And it is an emissions cost whose size depends entirely on whether the bridge ever ends. And it is the layer where the AI buildout’s environmental reality gets decided — not in the nuclear press releases that describe the future, but in the gas turbines going up behind the meter right now, powering the present while the future is still under construction, and emitting while they wait.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine. More at ThorstenMeyerAI.com.

Related Reading · the AI Energy & Infrastructure track

This dispatch

- This piece · The bridge · the timeline-mismatch forensic — how the nuclear procurement rush is a long-dated bet while behind-the-meter gas builds the present, and why the gap between the two is the buildout’s true energy and emissions story · structural-slate dominant, empirical-clay and labor-rose balance

The track

- The gigawatt gap · AI Energy 01 · the demand-supply gap this piece shows is being bridged by gas — the gap measured, now the bridge that fills it

- The queue · AI Energy 02 · the interconnection delay (3-7 years) that makes behind-the-meter gas the rational fast option — the grid bottleneck that pushes generation on-site

Adjacent tracks

- The runway · Enterprise Reorg 04 · the capex (>$400B in 2025, +75% in 2026) financing the buildout that needs the power

- The deployment · Enterprise Reorg 03 · the same hyperscaler capital intensity, in the services layer

- The stake · Post-Labor 01 · who owns the energy infrastructure and the returns it generates — the ownership question applied to power

Sources

The nuclear rush

- IEA · Data centre electricity use surged in 2025 — the SMR conditional-offtake pipeline grew from 25 GW (end-2024) to 45 GW; data center electricity demand +17% in 2025 (AI faster), set to double by 2030 (AI to triple); five tech companies’ capex >$400B in 2025, +75% in 2026; ~40% of 2025 corporate renewable PPAs; demand swings stretch onsite gas, making battery storage critical · iea.org

- Build.inc · Nuclear power for data centers — Constellation–Microsoft 20-year PPA restarting Three Mile Island Unit 1 (835 MW, online late 2024/2027); Amazon–Talen Susquehanna + X-energy SMR; Google–Kairos (Dec 2023, SMRs online 2030-2035); >16 GW US nuclear PPAs by end-2024, majority data-center-tied; power certainty as the primary site-selection differentiator; 15-25% lease premium for power-certain sites · build.inc

- iRecruit / SMR data centers — AWS–Talen 17-year 1.92 GW PPA (Susquehanna, to 2042), $20B PA investment, front-of-meter shift by spring 2026; Meta–Oklo 1.2 GW Pike County campus (16 Aurora reactors, 150 MW Phase 1, first reactors ~2030); Google–Kairos Hermes 2 (Oak Ridge, 50 MW by 2030, scaling to 500 MW) · irecruit.co

- CarbonCredits · Meta’s three nuclear deals — Meta’s PPAs up to 6.6 GW; Meta’s carbon footprint +20% to 8.2M tCO2e as AI data centers demanded more power; nuclear capacity projected to 494 GW by 2035 · carboncredits.com

The timeline mismatch

- Tech Insider · AI data center power crisis — nuclear to supply ≥5 GW dedicated data center capacity by 2030 (mostly restarts/extensions, SMR timelines will slip); gas the dominant new data center power source through 2028; US data center consumption (41 GW) rivals all US nuclear; 9-17% of US electricity by 2030; no commercial SMR yet operational in the US; NuScale (only NRC-certified design) faced cost overruns and delays · tech-insider.org

- Brookings · Global energy demands in the AI regulatory landscape — grid interconnection wait 7-10 years in established US/EU hubs, up to 13 in some projects; data centers could approach 1,050 TWh by 2026 (fifth-largest “country” consumer); 12% CAGR since 2017 · brookings.edu

- Reason · Next-generation nuclear can meet demand if regulations allow — data centers as near-perfect SMR conditions (concentrated 24/7 demand); operators willing to pay a premium for SMR power; the licensing framework was never designed for modular reactors; “the big question is whether SMRs can be permitted and built fast enough” · reason.com

The gas bridge and behind-the-meter

- Enverus · Time to power — 40+ GW of announced behind-the-meter and co-located generation (Meta, Amazon, Microsoft, Google, Oracle, xAI, Crusoe); large turbines booked through 2028; near-term gas dominates BTM; fuel cells fastest to first power (<24 months, at a premium); BTM compresses multi-year interconnection into months · enverus.com

- datacenterHawk · Behind-the-meter power — gas framed explicitly as a bridge until grid power or cleaner BTM options arrive; the renewable/24-7-CFE commitment tension; grid interconnection 3-7 years vs 18-24 months to build a data center · datacenterhawk.com

- Data Center Knowledge · Why data centers produce their own power — the March 2026 Bloom Energy survey: time-to-power runs 1.5-2 years longer than expected; the BYOG pivot; “operators may not really want to run power plants… but as a last resort, they may have to” (451 Research); hydrogen-ready systems’ 9-12-month speed advantage · datacenterknowledge.com

- Grist · Data centers scrambling to power AI with natural gas — Project Jupiter ($165B, New Mexico, simple-cycle gas microgrids) avoids climate-law regulatory approval by staying behind the meter; ~half of Texas power plants under construction serve data centers exclusively, off-grid; OpenAI Stargate (Abilene), Meta El Paso (813 modular generators); Cornell analysis: up to 44M metric tons CO₂ by 2030 (~10M cars) · grist.org

The turbine bottleneck

- Primary VC · The gas turbine bottleneck — three manufacturers (GE Vernova, Siemens Energy, Mitsubishi); ~5-year backlogs, slots sold into the next decade; GE Vernova ~55 GW gas orders, expanding 50→80 heavy-duty units/year by 2026; Mitsubishi doubling but sold out into 2028; Siemens record €136B backlog; total output might rise only 20-25% · primary.vc

- Yahoo Finance / energy strategy — hyperscalers favoring “power-now” over zero-carbon sequencing; large-frame turbines backlogged to 2027-2028, lead times 2-3 years; the shift to SOFCs ($3,000+/kW), reciprocating engines, aeroderivatives, 10-15 MW modular blocks; “BTM once a hedge, becoming strategic infrastructure” · finance.yahoo.com

- MHI / US Power Outlook — data center demand could double/triple to 325-580 TWh by 2028 (74-132 GW), largely met by gas turbines; Mitsubishi’s >100-MW turbine forecast doubled in a year; Gartner: by 2027, 40% of AI data centers operationally constrained by electricity deficits · power.mhi.com

The economics and the PJM signal

- TradingKey · PJM auction and the SMR boom — the PJM capacity auction mandating tech companies fund new capacity; 30-50% data center electricity cost increases; 5.2% capacity shortfall by 2027-2028 (~$15B new plant investment); SMR economics unproven (Vogtle: 7 years late, $18B over, ~$15,000/kW — ~5x conventional) · tradingkey.com

- S&P Global · BTM combined-cycle vs solar-plus-battery — for a 627 MW West Texas data center online 2028, combined-cycle gas is the lower-cost firm-power pathway on a 20-year basis ($2.9B); CCGT capex $2,293/kW vs solar $1,118/kW + 10-hr battery $2,103/kW · spglobal.com

The track backbone

- The gigawatt gap / The queue · Thorsten Meyer · AI Energy 01-02 · the demand-supply gap and the interconnection delay — the bridge is what fills the gap the first measured, made necessary by the queue the second measured

Key reference figures crystallized

- The nuclear rush: SMR offtake pipeline 25 GW (end-2024) → 45 GW (early 2026); >16 GW US nuclear PPAs by end-2024, majority data-center-tied; Meta up to 6.6 GW + Oklo 1.2 GW; Microsoft TMI 835 MW; AWS–Talen 1.92 GW; Google–Kairos; 15-25% power-certain lease premium

- The timeline mismatch: data center build 18-24 months; nuclear arrives 2027 (TMI) / 2030 (Oklo, Kairos) / 2030-2035; no commercial US SMR yet; grid interconnection 3-7 years (up to 13 in EU); time-to-power +1.5-2 years vs expected; Gartner — 40% of AI data centers electricity-constrained by 2027

- The gas bridge: 40+ GW announced BTM/co-located generation (Meta, Amazon, Microsoft, Google, Oracle, xAI, Crusoe); ~half of Texas plants under construction serve data centers off-grid; data center demand to 325-580 TWh (74-132 GW) by 2028, largely gas; CCGT lowest-cost firm power on 20-yr basis

- Behind-the-meter: BYOG pivot; compresses interconnection to months; Project Jupiter avoids climate-law review by staying off-grid; the speed motive + the scrutiny-avoidance tell

- The turbine bottleneck: 3 manufacturers (GE Vernova, Siemens, Mitsubishi); ~5-yr backlogs into the next decade; Siemens €136B backlog; output up only 20-25% even with expansion; scramble to fuel cells / reciprocating engines / aeroderivatives

- The emissions reckoning: Cornell — up to 44M tonnes CO₂ by 2030 (~10M cars); Meta footprint +20% to 8.2M tCO2e; gas-vs-pledge tension; permanence (bridge vs destination) decides the carbon

- The economics: PJM 5.2% shortfall by 2027-2028 (~$15B); 30-50% data center cost increases; Vogtle 7 years late / $18B over / ~$15,000/kW as the SMR-skepticism anchor