A structured deep-dive (with updated data, cross-checks, and policy implications)

Prepared for Thorsten Meyer AI

AI-Driven Automation for Business: Improve Efficiency and Reduce Costs with AI Automation Tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Executive overview

The text you provided makes one deliberate, simplifying assumption:

Machines (AI + robotics) will become better, faster, cheaper, and safer than humans at all economically valuable tasks.

If that assumption holds broadly enough, the economy eventually becomes supply-saturated: production is abundant and automated, and the real constraint flips to the demand side—especially to the hardest resource of all: human attention.

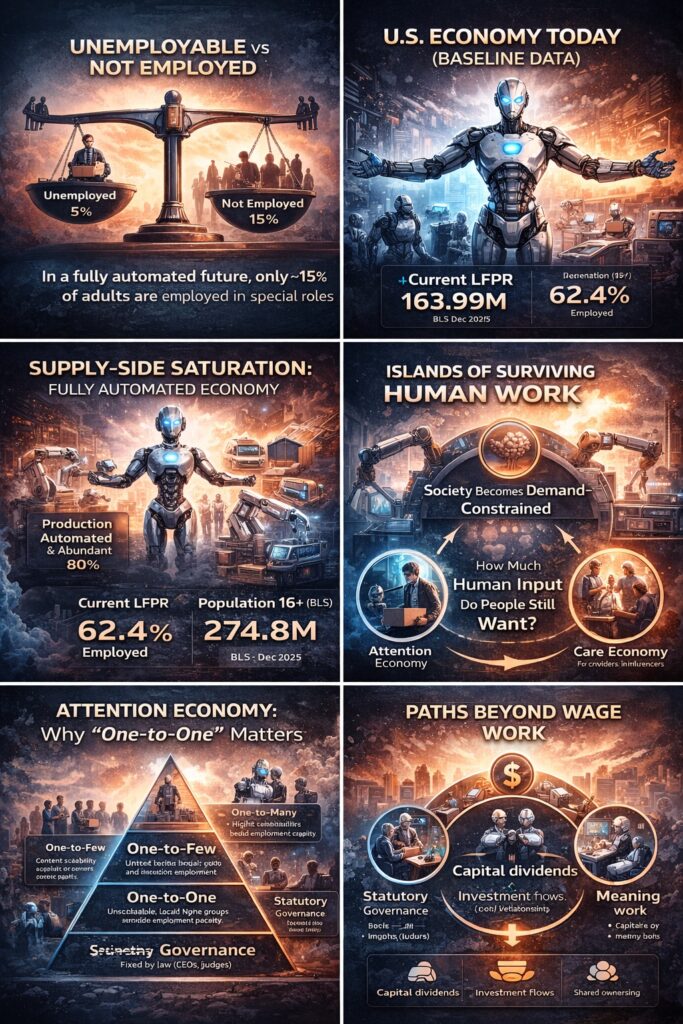

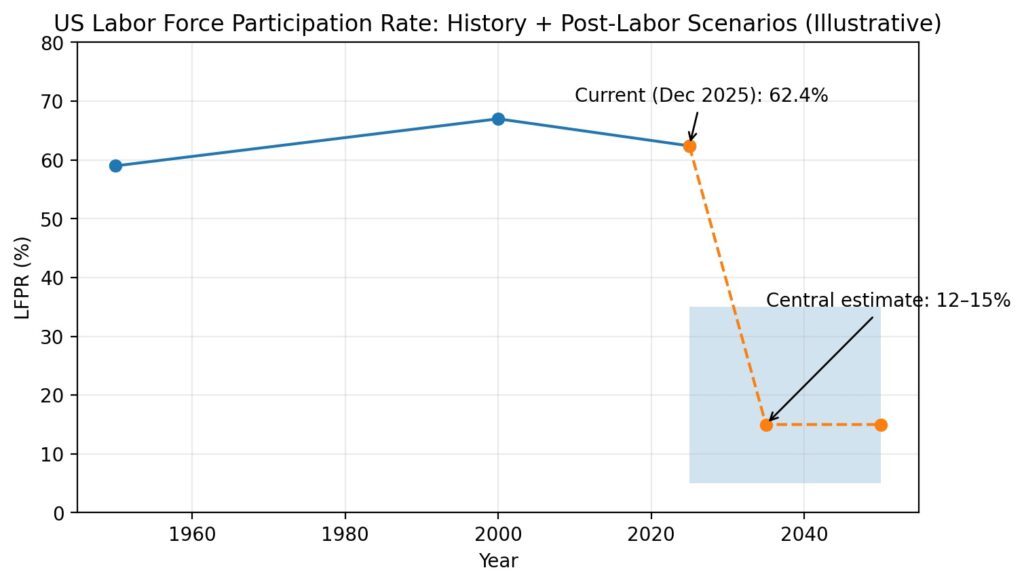

The model in your draft argues that in that “fully automated equilibrium,” only ~15% of working-age adults will be employed (meaning ~85% not employed).

This article does three things:

- Preserves and clarifies your model (the “attention constraint,” “statutory jobs,” scalability, and LFPR math).

- Cross-checks key baseline numbers (labor force, consumption share of GDP, time-use, robotics adoption, AI adoption).

- Adds evidence and nuance from credible institutions (BLS, BEA/FRED, ILO, OECD, IMF, Stanford HAI, IFR, Goldman Sachs, and recent regulatory developments).

A central correction from the cross-checking:

- Your U.S. “working-age adults = 260M” is in the right ballpark if you mean 18–64-ish, but the BLS “civilian noninstitutional population 16+” is 274.8 million (Dec 2025).

- U.S. consumption as a share of GDP is not “70–85%” in the data series most people cite. Personal consumption expenditures were ~67.9% of GDP in Q3 2025.

Those aren’t nitpicks—they matter because your whole argument is ultimately about how demand is financed when wages shrink.

Robotics and Automation in Construction Sites

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

1) First, a definition check: “unemployable” vs “not employed”

The phrase “85% unemployable” is rhetorically powerful but easy to misunderstand.

Three different states get blurred together

- Unemployed: actively looking for work but not currently working.

- Not in the labor force: not working and not actively looking.

- Not needed for production: the economy could produce what it needs without your labor—even if you could work.

In a “post-labor” world with a solid income floor (capital dividends, social wealth funds, or transfers), many people would be not employed by choice, not “unemployable” by capability.

So the core claim is better stated as:

In a fully automated equilibrium, market demand for human labor may fall so far that only ~10–20% of adults hold paid roles—mostly in governance/liability and human-premium services.

That’s the thesis we’ll evaluate.

Pocket AI Voice Recorder & Smart Assistant – Auto Transcription, Summaries & Action Items – AI Note Taker for Meetings, Calls & Productivity – Space Grey

- AI Personal Assistant: Transcribes and summarizes meetings and calls

- One-Tap Recording: Easily capture audio with a single tap

- Smart AI Insights: Generates summaries and action items automatically

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

2) Reality check: where the U.S. economy is today (baseline data)

Before projecting a post-labor future, we should anchor in current, verified numbers.

Labor force and employment (U.S.)

From the U.S. Bureau of Labor Statistics (BLS), Dec 2025 (seasonally adjusted):

- Civilian noninstitutional population (16+): 274.816 million

- Employed: 163.992 million

- Labor force participation rate (LFPR): 62.4%

- Employment-population ratio: 59.7%

This matters because your model compares a future LFPR (e.g., 12–15%) to today’s roughly ~62%.

Consumption’s role in GDP

Using a BEA series published via FRED:

- Personal consumption expenditures (PCE) share of GDP: 67.9% in Q3 2025

So your intuition is directionally right: U.S. GDP is consumption-driven. But the best-supported “anchor number” is closer to the high-60s than 70–85.

The attention budget: what Americans actually do with time

The BLS American Time Use Survey (ATUS) gives hard numbers for the “attention constraint.”

In 2023 (civilian population age 15+):

- People averaged ~5.2 hours/day in leisure and sports activities.

- Of that, watching TV accounted for ~2.7 hours/day (over half of leisure time).

Your model uses 8 discretionary hours/day in a post-work future. That’s not crazy as a scenario—but ATUS shows the current reality is lower. The key point remains: the day is finite, and attention does not scale with technology.

Robotics is scaling on the supply side

Industrial robotics adoption has real momentum:

- The International Federation of Robotics (IFR) reports ~4.28 million industrial robots operating in factories worldwide (World Robotics 2024), up ~10%.

- IFR also reports global robot density reached ~162 units per 10,000 employees in 2023, more than double seven years earlier.

This supports your “supply-side saturation” framing: automation isn’t hypothetical—it is compounding.

AI adoption is scaling on the cognitive side

Stanford’s AI Index reports major acceleration in business usage:

- 78% of organizations reported using AI in 2024, up from 55% the year before (per the AI Index summary page).

Whether that usage replaces jobs or shifts tasks is the contested part. But “adoption is happening” is well supported.

Lefant Robot Vacuum Cleaner, Strong Suction, 120 Mins Runtime, Slim, Low Noise, Automatic Self-Charging, Wi-Fi/App/Alexa Control, Ideal for Pet Hair Hard Floor and Daily Cleaning, M210

- Pet-Friendly Design: Ideal for homes with pets

- App Compatibility: Use the new Lefant app for full features

- Compact Size: 11-inch diameter, 2.99-inch height for tight spaces

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

3) The model you provided, clarified and tightened

Your “Core Model” can be expressed cleanly as:

Employment is fundamentally “hours demanded”

In a fully automated economy, remaining human employment depends on how many worker-hours society still wants from humans, divided by how many hours each worker supplies.

You wrote:

LFPR = Total Worker-Hours Demanded ÷ Hours Worked per Participant

This is the right “identity” to focus on.

Two sources of remaining worker-hours

Your model says human worker-hours come from two main buckets:

- Statutory / legitimacy labor

Humans required by law, regulation, or liability and legitimacy needs. - Human-premium services

People paying a premium for human input, even when machines are better.

That’s the correct decomposition for a post-automation equilibrium.

The single most important constraint: attention

Your argument that attention is the binding constraint is one of the strongest parts of the draft.

- Attention cannot be expanded by technology; it’s bounded by time and biology.

- Jevons paradox doesn’t “create more hours in a day.”

The ATUS data supports the idea that “leisure attention” is large, but finite—and already dominated by entertainment.

4) “Supply-side saturation”: why this thought experiment is qualitatively different

Most debates about automation implicitly assume:

- some tasks get automated,

- productivity rises,

- new sectors emerge,

- and employment “rebalances.”

Your text is making a more radical assumption:

Automation eventually wins everywhere it is economically valuable.

If that happens, employment stops being supply-constrained (“how many workers do we need?”) and becomes demand-constrained:

How much human labor do people still want to buy—at a premium?

This flips the usual policy frame from “reskilling” alone to distribution and demand maintenance.

5) The surviving islands of human work

Your categories are useful. The cross-checking adds one nuance: some “surviving jobs” won’t survive because humans are better—they’ll survive because humans are legally and morally required.

5.1 Statutory jobs and legitimacy labor

A statutory job is preserved by:

- licensing and regulation,

- accountability and liability,

- democratic legitimacy,

- safety rules and “human sign-off” requirements.

Why this category could expand, not shrink

As AI penetrates high-stakes domains, regulators often demand human oversight.

- The EU’s AI Act (Regulation (EU) 2024/1689) is an example of a risk-based framework for AI governance.

- In the U.S., health regulators are actively clarifying oversight boundaries for clinical decision support software.

Even if AI becomes technically superior, law can mandate human control points, preserving some employment (or at least preserving responsibility roles).

Why this category could also shrink

On the other hand, regulation can be redesigned to allow machine decision-making—especially if machines become demonstrably safer.

Your “doctors and lawyers may go the way of the dinosaur” claim is speculative, but not baseless. A very current example:

- On Jan 6, 2026, Utah’s Department of Commerce announced a state-approved partnership to evaluate “autonomous AI” for prescription medication renewals for chronic conditions within a regulatory sandbox.

That doesn’t mean “doctors are obsolete,” but it does show regulation beginning to test AI participation in clinical workflows.

5.2 The attention economy and human-premium work

Your framing is sharp:

In a post-labor equilibrium, the remaining jobs are largely those that sell human attention or human presence.

But it helps to separate attention from care:

- Attention work: content, entertainment, education, experiences, coaching

- Care work: child care, elder care, companionship, social support

- Trust work: counseling, fiduciary responsibility, governance

- Meaning work: communities, rituals, arts, identity-based crafts

All of these depend on a human choosing to allocate time and money to humans rather than machines.

5.3 A critical refinement: attention markets are power-law markets

Your draft says “top 1% take 30–50% of attention.” The exact percent varies by platform and metric, but the underlying point—extreme concentration—is well supported.

Example data point (creator earnings concentration):

- A CreatorIQ analysis cited by Business Insider reported the top 10% of creators received 62% of ad payments, while the top 1% received 21%.

Earnings ≠ attention, but in ad-driven markets they correlate strongly. This supports your conclusion: a “broadcast creator economy” is structurally incapable of absorbing tens of millions of displaced workers.

6) The attention architecture: why “one-to-one” matters

One of your most actionable insights is that how services scale determines how many people can be employed.

Four “attention architectures” (your model, tightened)

- One-to-many (broadcast)

- Highly scalable

- Winner-take-all

- Low employment capacity

- One-to-few (cohorts, groups, local experiences)

- Moderately scalable

- Less concentrated due to geography + relationships

- Medium employment capacity

- One-to-one (relational services)

- Not scalable

- Least winner-take-all

- Highest employment capacity

- Many-to-one (governance roles)

- Institutionally fixed

- Preserved by legitimacy constraints

Policy implication (important)

If a society wants more people employed despite automation, it should:

- favor one-to-one and local one-to-few human services,

- and avoid over-indexing on “creator economy” narratives.

This is one of the clearest “design levers” in your entire framework.

7) Quantifying the ceiling: does the math support a 12–15% labor force?

Let’s translate your estimate into updated U.S. baseline numbers.

Today’s scale vs. your post-labor scale

- Today employed (Dec 2025): ~164.0M

- Your central post-labor LFPR: ~12–15%

Apply that to the BLS population base (274.8M):

- 12% employed → ~33.0M

- 15% employed → ~41.2M

So “85% not employed” translates to a U.S. labor market shrinking from ~164M employed to ~33–41M employed in the long-run equilibrium.

That is an enormous structural discontinuity—bigger than the entire labor market transformation of the 20th century.

Does mainstream research agree?

Not directly, because most research focuses on:

- exposure, not end-state equilibrium;

- augmentation vs substitution;

- time horizons like 5–25 years, not a “full automation limit.”

But we can triangulate.

8) Cross-checking against major institutions and current evidence

8.1 “How many jobs are exposed?” is not the same as “how many vanish”

Mainstream estimates often measure task exposure.

- The IMF has argued AI will affect ~40% of jobs globally, involving both replacement and complementarity effects.

- Goldman Sachs Research wrote that generative AI could expose the equivalent of 300 million full-time jobs to automation and that roughly two-thirds of U.S. occupations are exposed to some degree, though often partially.

These are big numbers—but they are not “85% unemployment” numbers. They are exposure numbers.

8.2 The ILO’s key finding: more “augmentation” than “automation” (near-term)

Your draft says “technology doesn’t create jobs.” That claim is contested, but what’s more relevant is the ILO’s finding about this wave:

- The ILO’s Working Paper 96 (Aug 2023) explicitly frames its exposure estimates as an upper bound and concludes the “overwhelming effect” is more likely to be augmentation rather than full automation at the occupation level.

- It also identifies clerical work as unusually exposed: 24% of clerical tasks highly exposed and 58% additional exposure (as stated in the abstract section).

That supports an important nuance: even if “jobs” don’t vanish instantly, the task content and wage structure can change dramatically.

8.3 OECD: historically, AI exposure has not meant job loss so far

The OECD’s 2024 paper reports:

- No clear negative employment or wage outcomes “on aggregate so far,” and in some analyses even a positive relationship between AI exposure and employment (2012–2022).

This is one of the best “reality checks” against immediate doom narratives.

8.4 But early signals are emerging—especially for entry-level roles

Your model predicts a saturation problem: too many people competing for too few human-premium roles.

An emerging empirical signal aligns with that:

- Brynjolfsson, Chandar, and Chen (Aug 2025) report a 13% relative decline in employment for early-career workers (ages 22–25) in the most AI-exposed occupations, controlling for firm-level shocks, while more experienced workers remain stable.

This doesn’t prove the post-labor end state. But it does suggest that labor market impacts can appear first where “junior work” is easiest to automate—a pattern consistent with your framework.

9) So is “85% not employed” plausible under your assumption?

Under your assumption (machines win at all economically valuable tasks), the model’s conclusion becomes less outrageous:

- If machines can do almost everything, human labor demand collapses to:

- legally required roles, and

- roles humans insist on buying for cultural/psychological reasons.

The key question is not “can machines do it?” but:

How much will humans pay for the privilege of human involvement?

That is exactly the “human premium” parameter in your model (h_week, weekly human services consumed per person).

Why your LFPR range is sensitive but not arbitrary

Your scenario analysis shows LFPR could range from single digits to the 30s depending on:

- h_week: hours/week of paid human service people choose to consume

- s: scalability factor

- H_part: hours worked per employed person

- h_stat: statutory hours required

That’s not hand-waving. It’s a real set of levers.

The strongest argument for your conclusion

The strongest part of your case is:

- Attention is fixed

- Broadcast markets concentrate

- Oversupply saturates everything

Even if people want “meaningful work,” the economy may not need it as paid work.

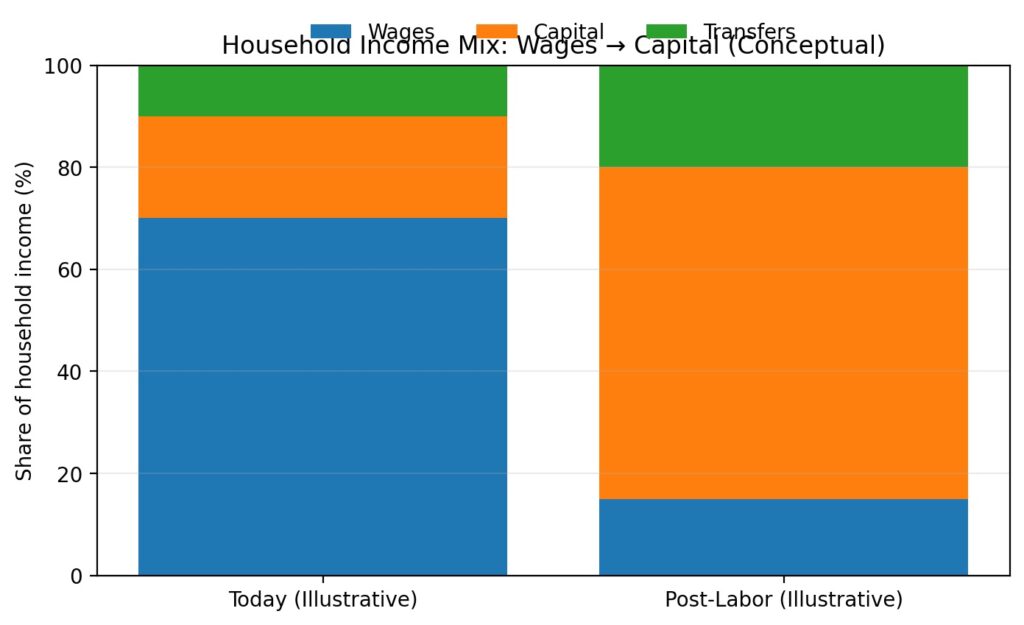

10) Demand-side economics: when wages shrink, what funds consumption?

This is the hinge of the whole piece, and the data supports your framing:

- In the U.S., consumption is about two-thirds of GDP (PCE share).

- If wages are the main distribution mechanism and wage labor collapses, aggregate demand collapses unless income is redistributed or pre-distributed.

Your three-bucket decomposition is correct:

- Wages

- Capital income (equity, dividends, rents, business ownership)

- Transfers (government payments)

If wages decline structurally, demand must be stabilized by (2) capital broadening and/or (3) transfers.

11) “Wages → Capital”: the most coherent replacement mechanism

Your draft argues for replacing wage distribution with capital distribution.

That’s not a single policy. It’s a design family. The key is to create:

- a broad ownership base, and

- dividend-like flows that scale with productivity.

11.1 The public track: social wealth funds and dividends

You gave three levels (municipal, state, national). The “proof of concept” exists:

- Alaska Permanent Fund Dividend is a well-known example of a state-level dividend funded by collectively owned resource wealth.

- New Mexico’s Land Grant Permanent Fund is another example of a large public endowment producing distributions for public beneficiaries (commonly schools and institutions).

- Norway’s Government Pension Fund Global is the world’s flagship sovereign wealth fund model.

The “value add” here is not that these are perfect UBI systems—they aren’t—but that they demonstrate:

- collective capitalization,

- professional investment,

- and public benefit flows.

11.2 The individual track: universal basic capital and “baby bonds”

If the future requires everyone to be an investor (directly or indirectly), then capital access cannot remain a privilege.

“Baby bonds” (capital endowments at birth that mature into investable wealth) are one concrete design:

- The Brookings discussion of baby bonds outlines the basic idea as an asset-building strategy aimed at closing wealth gaps.

Universal basic capital (UBC) proposals expand this concept into a broader ownership floor.

11.3 The enterprise track: employee ownership at scale

Instead of only taxing profits and transferring cash, societies can broaden ownership directly through workplace capital structures:

- ESOPs are a major U.S. mechanism for employee ownership; the National Center for Employee Ownership (NCEO) reports employee ownership at large scale (millions of participants).

- The UK’s Employee Ownership Trust (EOT) framework is another widely cited model for shifting ownership to employees over time.

This connects to your “mandatory capital disbursements” / “require companies to sell shares” category, but in a politically palatable form.

12) The statutory wildcard: regulation can “create jobs” by requiring humans

One of the most underappreciated levers in your model is h_stat: statutory labor hours required per capita.

Regulation can increase h_stat through:

- mandatory human-in-the-loop requirements,

- licensing barriers,

- audits, inspections, certifications,

- liability requirements for deployment.

Recent governance moves suggest the world may lean in this direction:

- The EU AI Act formalizes a risk-based approach and includes obligations for high-risk systems, shaping how “human oversight” functions in practice.

- In healthcare, regulators are actively refining where software is regulated as a “device” and where it is not—an ongoing boundary-setting process.

This matters because a post-labor world might still have work—compliance work—even if machines do the underlying productive tasks.

13) The saturation problem: the model’s most important sociological insight

Your draft identifies something that many automation forecasts ignore:

Even if “new work” exists, it can saturate instantly when tens of millions flood into it.

This is qualitatively different from today’s labor markets because:

- Many remaining roles become low-barrier (creator tools, coaching, services).

- Demand is capped by attention and local budgets.

- Online markets concentrate.

The likely result is:

- a small number of high-status winners,

- a long tail of precarious, part-time, low-paying participation,

- and a large share of people who want paid roles but cannot find enough paying demand.

This is one of the reasons your 12–15% “central” employment equilibrium is not obviously absurd—even if it’s not a near-term forecast.

14) Key uncertainties and wild cards (what could push LFPR up or down)

Your draft ends with “Upside risks” and “Downside risks.” Here is a completed and expanded version.

Upside risks (LFPR higher than 15%)

- Stronger human-authenticity preference

People pay for human-made goods/services the way they pay for luxury today. - Regulation mandates human oversight broadly

A larger compliance/governance labor layer emerges. - Work-sharing norms become standard

If human work is rationed across many people, LFPR can remain higher even with fewer total hours. - High-touch culture emerges

Society chooses human-to-human services as default (education, care, community, hospitality). - Geography fragments markets

Local services resist global winner-take-all dynamics.

Downside risks (LFPR lower than 15%)

- Robots become socially acceptable in care roles

If companionship, child care assistance, elder support, and therapy are widely delegated to machines, the one-to-one employment reservoir shrinks. - Human premium collapses due to oversupply

If many people compete for human-service roles, wages fall, and fewer can sustain paid work. - Regulation relaxes liability and licensing

“Human sign-off” becomes optional, shrinking statutory jobs. - AI-driven entertainment dominates attention

If hyper-personalized entertainment captures discretionary hours, less attention remains for human services. - Capital concentrates further

If ownership is not broadened, demand collapses for most humans—reinforcing low human labor demand.

15) A practical “post-labor policy stack” that fits your framework

If Thorsten Meyer AI is publishing this to drive action, the most useful output is a stack, not a single silver bullet.

Layer 1: A demand floor (so the economy doesn’t eat itself)

- Social wealth fund dividends (national + state + municipal where feasible)

- Modest unconditional income floor (UBI/negative income tax) to prevent destitution

Layer 2: Predistribution (ownership before redistribution)

- Baby bonds / universal basic capital endowments

- Employee ownership expansion (ESOP/EOT, cooperative vehicles)

Layer 3: Make capital participation “default”

- Auto-enrolled investment accounts

- Matching for low-income savers

- Simplified diversified index access

- Reduced tax friction for low-wealth capital formation (carefully designed)

Layer 4: Grow the human-premium sectors that maximize employment

- Local one-to-few experiences (education, hospitality, community events)

- One-to-one services (care, coaching, counseling, personalized craft)

- Civic work (local governance, mediation, restorative justice)

This is how you operationalize your own policy implication:

Favoring one-to-one over one-to-many architectures increases employment capacity and reduces inequality.

16) What to do now (individual + organizational playbook)

This isn’t financial advice—just a strategic translation of your model:

For individuals

- Build “human premium” skills: trust-building, coaching, facilitation, caregiving, conflict resolution, teaching.

- Build capital exposure early: even small, diversified participation matters if wages stagnate and capital grows.

- Treat AI as leverage: if your work can be augmented, learn to use AI tools aggressively rather than competing against them.

For companies

- Design “human-in-the-loop” accountability structures early; regulation is trending toward governance requirements.

- Consider ownership broadening as a stability strategy (employee ownership isn’t charity; it’s demand preservation).

For policymakers

- Stop framing the problem as only “reskilling.”

- Treat it as distribution + demand stability in a high-productivity world.

Conclusion: if the assumption holds, unemployment isn’t the tragedy—distribution is

Your model is not primarily an “AI will take your job” scare piece.

It’s a macro argument:

- Automation pushes labor demand toward zero (supply-side saturation).

- The economy becomes demand-constrained.

- Demand requires households with purchasing power.

- If wages no longer distribute income, then society must shift to:

Wages → Capital (and/or Transfers).

The strongest contribution of your framework is not the headline number “85%.”

It’s the structural insight:

Human attention and legitimacy are the last scarce inputs. Everything else becomes abundant.

If we redesign ownership and income flows accordingly, “mass non-employment” can be liberation rather than collapse.