By Thorsten Meyer — May 2026

The Department of Defense announced classified-network AI agreements with seven companies on May 1, 2026: SpaceX, OpenAI, Google, Microsoft, Amazon Web Services, Nvidia, and a $2 billion startup called Reflection AI run by ex-Google DeepMind researchers. Oracle joined shortly after. Anthropic was the one frontier lab cut from the list.

The press read this as exclusion. The headlines wrote themselves: “Pentagon freezes out Anthropic.” “Cutting out Anthropic.” “Shunning Anthropic.” Most of the analysis stopped there.

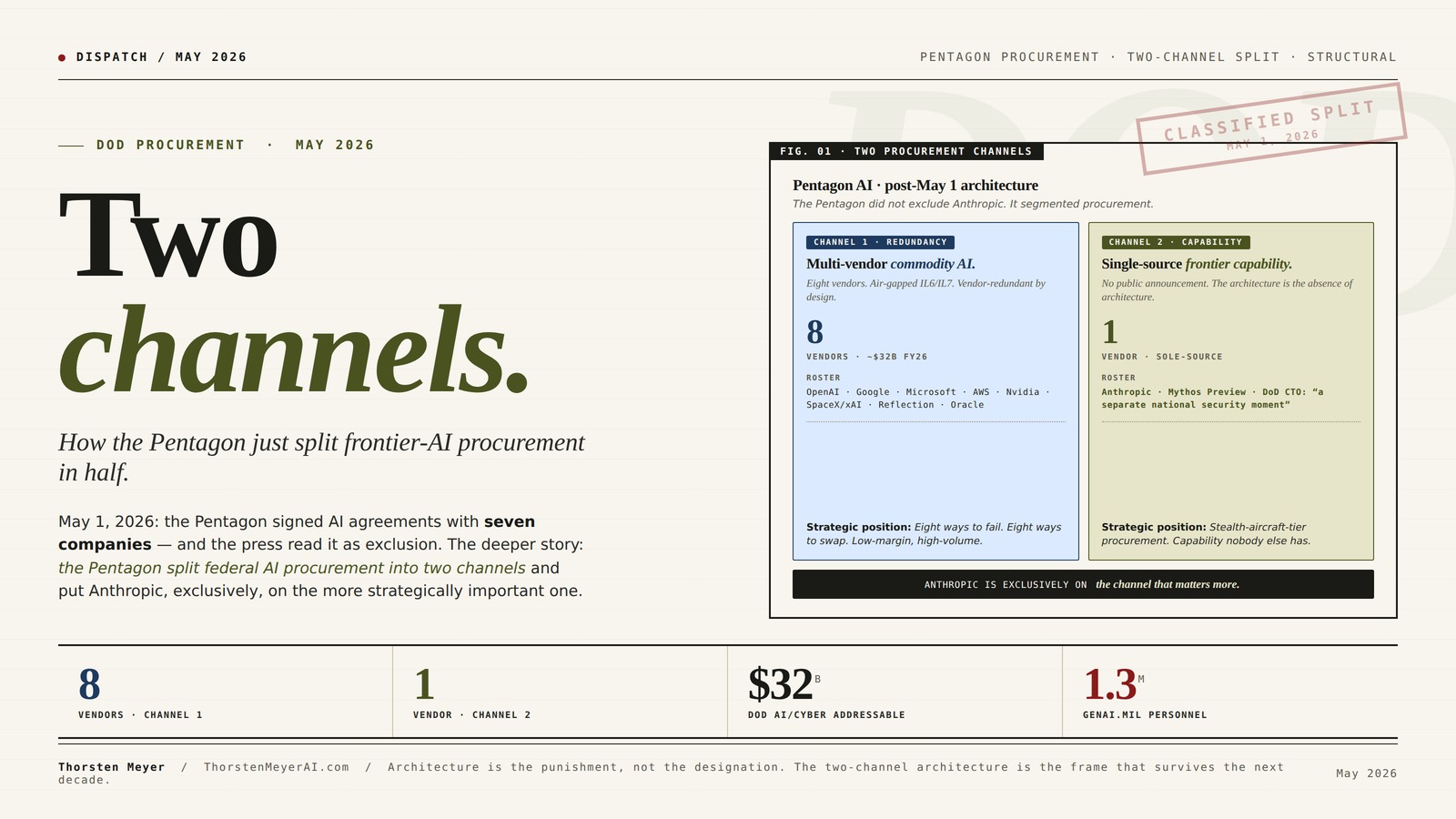

The deeper story is that the Pentagon did not actually exclude Anthropic from federal procurement. It split federal AI procurement into two channels — and put Anthropic, exclusively, on the more strategically important one.

Channel One is the multi-vendor classified-network channel announced May 1: seven companies, Impact Level 6 and 7 environments, the GenAI.mil portal that 1.3 million Pentagon personnel already use. This is the explicit redundancy play. Pentagon CTO Emil Michael, in March, told Bloomberg “I need redundancy.” Last Friday he got it. Anthropic is not in this channel. By design.

Channel Two is the cybersecurity channel, and it is structurally different. Anthropic launched Claude Mythos Preview on April 7. SiliconANGLE confirmed last week that the Defense Department is using Mythos despite the supply-chain-risk designation. Multiple federal agencies have adopted it. Mythos is Anthropic’s offensive-cybersecurity-capable frontier model, designed to find zero-day and undisclosed vulnerabilities. The DoD CTO referred to Mythos’s capabilities as “a separate national security moment” — meaning, treated as its own category, with its own access regime, distinct from the supply-chain dispute.

Two channels. Two procurement architectures. One company excluded from the redundant channel and exclusively present in the strategic one. That is not exclusion. That is segmentation.

This dispatch is about what that segmentation means for the ten companies sitting on either side of the line.

Two channels.

How the Pentagon just split frontier-AI procurement in half.

On May 1, 2026 the Pentagon signed classified-network AI agreements with seven companies — and the press read it as exclusion. The deeper story: the Pentagon split federal AI procurement into two channels and put Anthropic, exclusively, on the more strategically important one. Channel One is redundancy. Channel Two is capability.

One Pentagon. Two channels. One vendor in each role.

Pentagon CTO Emil Michael, March 2026: “I need redundancy.” The May 1 announcement is the architecture of that redundancy — eight vendors in Channel 1, the procurement model designed to prevent any one of them from becoming dominant. Channel 2 is the inverse: a single-source procurement architecture for capability the redundant pool cannot match.

Multi-vendor commodity AI.

Single-source frontier capability.

AI and Machine Learning for Cybersecurity Engineering: Detect Advanced Threats, Minimize False Alerts, and Build Scalable Intelligent Defenses

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Eight ways to fail. Eight ways to swap.

The redundancy logic does not depend on the dispute.

Pre-Anthropic-conflict trajectory was already toward multi-vendor classified procurement — JWCC’s four-cloud structure is the precedent. The May 1 announcement accelerated the timeline. It did not invent the architecture. The eight fall into three rough buckets.

Amazon (AWS)

Google (GCP + Gemini)

Oracle (multi-vendor)

Reflection AI ($2B raise · ex-DeepMind · “tens of trillions of tokens”)

SpaceX/xAI (Grok · politics · satellites)

Generative Artificial Intelligence in Healthcare: Current Practices and Future Development (Artificial Intelligence in Smart Healthcare Systems)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The part the courts cannot reverse.

The supply-chain-risk designation has a second-order effect that extends well beyond the Pentagon itself. It limits what defense contractors can use. Lockheed, RTX, Northrop Grumman, General Dynamics, BAE — the whole industrial base — has now had three months to migrate. The market structure that emerged is the new baseline.

Even if Anthropic wins in court, the procurement environment around it has shifted.

Defense contractor model migration.

Primes that had Anthropic baked into delivery pipelines have migrated. Replacements: Microsoft (Azure OpenAI), Amazon (Bedrock minus Anthropic = Mistral, Llama, Cohere), Google (Gemini). Procurement-driven distribution gain — durable.

The compliance-friction tax on smaller AI vendors.

Cohere, Mistral, AI21, the open-weight cohort all face the same procurement standard Anthropic was excluded under. Most lack the lobbying or legal resources. Either accept the standard contractual language preemptively or lose access by inaction.

The international read-across.

UK MoD, France’s defense AI, Germany’s Bundeswehr, Israel’s MOD — all running internal assessments of whether the U.S. classification cascades into their own eligibility decisions. Anthropic’s international defense market shrinking on the same timeline as its U.S. defense market.

classified AI model access control solutions

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three reasons it does not collapse back to one.

The natural prediction is temporary: Trump and Amodei reach a deal, the SCR designation lifts, Anthropic re-enters Channel 1. This prediction is probably wrong.

The redundancy logic predates the dispute.

Pentagon was already moving toward multi-vendor classified procurement. JWCC’s four-cloud structure is the precedent. May 1 accelerated the timeline. Even if Anthropic returns to Channel 1, it returns as one of nine — not the pre-2026 dominant vendor.

Mythos’s capability profile is not easily replicated.

None of the other seven has shipped a model with Mythos’s specific offensive-cyber profile. The capability gap may close in 12–18 months — or not. Either way, the Channel 2 architecture, once built, becomes the template for any frontier capability the Pentagon cannot get from a redundant pool.

The political symmetry favors keeping both.

Channel 1 satisfies the political coalition that drove the SCR designation. Channel 2 keeps superior capability flowing to Pentagon staff and intelligence-community personnel who consider Claude superior. Both constituencies get their preferred outcome.

The Pentagon did not exclude Anthropic. It segmented procurement. Channel 1 is the redundancy channel. Channel 2 is the capability channel. Anthropic is exclusively present in the one that matters more.

Hewlett Packard Enterprise ProLiant DL320 Gen11 Rack Server w/one Intel Xeon Scalable 5416S Processor, 2.0GHz 16‑core 1P 64GB‑R 8SFF 800W PS (HPE Smart Choice P69302-005)

HPE PROLIANT DL320 GEN11 5416S 2.0GHZ 16-CORE 1P 64GB-R 8SFF 2X800W SERVER (P69302-005): Powered by one Intel Xeon…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

The next 18 months are a market-share war among eight peers.

$32B addressable spend. Win by GenAI.mil integration depth, IL6/IL7 deployment speed, willingness to compress accreditation timelines. Vendor lock-in to a specific cloud or compute substrate works against you.

The SCR designation creates precedent. Smaller vendors will be reviewed against it.

Be proactive about your defense compliance posture. If you do not have a federal sales motion, the procurement-driven distribution gap to your hyperscaler-distributed competitors is widening monthly.

Your AI delivery stack needs an operational answer to “what if our model vendor gets an SCR?”

The May 1 precedent makes that question operational, not theoretical. Multi-vendor delivery architectures are now a procurement requirement, not a best practice.

Model both channels. Channel 2 revenue should be a higher multiple.

The “multiple billions” CFO Krishna Rao warned about are partially offset by Mythos and federal-agency adoption. Q4 / Q1 disclosures will reveal the split. The pre-IPO valuation should incorporate Channel 1 exclusion AND Channel 2 inclusion.

Executive Summary

| Channel | Who’s in | Spend ceiling | Procurement model | Strategic position |

|---|---|---|---|---|

| Channel 1 · Classified, multi-vendor | OpenAI, Google, Microsoft, AWS, Nvidia, SpaceX/xAI, Reflection AI, Oracle | ~$800M+ direct (FY26 H1), $32B addressable in DoD AI/cyber/cloud through 2027 | Vendor-redundant, IL6/IL7 air-gapped, 3-month accreditation | Pentagon is buying redundancy and vendor lock-out protection |

| Channel 2 · Cybersecurity, single-source | Anthropic (Mythos Preview) | Not publicly disclosed; reported in active use | Capability-driven, sole-source on capability gap | Pentagon is buying frontier capability it cannot get elsewhere |

| Status of supply-chain-risk designation | Active. Anthropic is suing in two federal courts. Injunction prevents formal ban. | — | — | Architecture is the punishment, not the designation. |

| Pentagon AI-platform users (GenAI.mil) | 1.3M+ personnel; hundreds of thousands of agents built | — | — | The userbase is built. The model layer is the variable. |

| Anthropic FY26 revenue at risk | “Multiple billions of dollars” per CFO Krishna Rao | — | — | Channel 2 revenue partially compensates. Channel 1 revenue is gone. |

| Other-channel signal | OpenAI, Google, Anthropic, xAI all received $200M agentic-AI contracts in Q1 2026. Palantir holds $10B+ in Army data ceiling. | $800M (the four-vendor agentic deal) | — | The agentic procurement preceded the May 1 split. |

The Pentagon did not pick OpenAI over Anthropic. The Pentagon picked redundancy at the application layer over single-vendor dependency, and decided that for offensive cyber it would accept single-vendor exposure because the capability gap justifies it. Two different procurement decisions. Two different channels. One company sitting on the strategically narrower but more durable side.

1. The Original Conflict

To understand the May 1 announcement, you have to understand what Anthropic refused to sign.

The Pentagon’s standard contractual language requires AI vendors to permit their models for “all lawful purposes” — meaning any use that does not violate U.S. law. This phrasing, in the context of a Defense Department contract, is broader than it sounds. It does not exclude domestic surveillance because domestic surveillance, when conducted under a warrant or other lawful authority, is legal. It does not exclude autonomous weapons because autonomous weapons, when operated within international humanitarian law, are legal. The phrasing is designed to give the Pentagon maximum operational flexibility.

Anthropic refused this language. The company’s position was that “all lawful purposes” was too broad and that it would require explicit guardrails carving out fully autonomous weapons targeting and mass domestic surveillance. The Pentagon refused to negotiate that scoping. In February 2026, the Trump administration designated Anthropic a supply chain risk — a label previously reserved for companies tied to foreign adversaries, never before applied to a U.S. AI company. In March, Defense Secretary Pete Hegseth formalized the designation. In a public X post, Hegseth wrote that “no contractor, supplier, or partner” doing business with the Pentagon could engage commercially with Anthropic. He called CEO Dario Amodei an “ideological lunatic” in congressional testimony.

Anthropic filed two lawsuits — one in San Francisco, one in DC — challenging the designation. A federal judge granted an injunction blocking the formal ban. CFO Krishna Rao’s filings warned the designation could cost the company “multiple billions of dollars” in 2026 revenue. Pentagon staff continued using Claude unofficially because they considered it superior to alternatives, and Reuters reported that DoD personnel were given six months to remove Anthropic tools — and that they were not complying willingly.

The April rapprochement attempts followed. President Trump’s chief of staff Susie Wiles met Amodei at the White House on April 17. Trump told CNBC a deal “is possible.” Anthropic announced Mythos Preview on April 7. The May 1 multi-vendor announcement is the procurement-side operational consequence: the Pentagon proceeded with the vendor-redundancy strategy regardless of the diplomatic conversations. Architecture is the punishment.

The architecture, however, has a gap. And the gap is Mythos.

2. Channel 1 · The Multi-Vendor Classified Stack

The May 1 announcement is the Pentagon’s largest-ever AI procurement decision. Eight companies (seven announced, Oracle confirmed shortly after) deploying frontier AI models inside Impact Level 6 and Impact Level 7 classified environments. Air-gapped from the commercial internet. Accessed via the GenAI.mil portal, which 1.3 million Pentagon personnel have already used to build hundreds of thousands of agents. The Pentagon compressed the standard accreditation timeline from 18 months to three.

The strategic intent is explicit. Pentagon language in the announcement targets “vendor lock” — Pentagon-speak for over-dependence on a single AI provider. Reuters interpreted this as a direct reference to Anthropic. The user base inside the Pentagon was Anthropic-heavy. The new procurement diversifies the model layer underneath the same user base.

The companies in this channel fall into three rough buckets.

Bucket 1 · Cloud + model combinations. Microsoft (Azure + OpenAI), Amazon (AWS + Anthropic-via-Bedrock-still-blocked), Google (GCP + Gemini), Oracle (cloud + multi-vendor model hosting). These are the four hyperscalers. Their inclusion is structural — the Pentagon needs cloud infrastructure regardless of model choice, and these four already hold positions on the $9 billion JWCC ceiling.

Bucket 2 · Pure model labs. OpenAI (GPT-5.5, frontier reasoning), Reflection AI (the only newcomer, $2B raised, ex-DeepMind founders, training a “tens of trillions of tokens” model). These are the model layer plays — the Pentagon wanted multiple frontier-model options not bundled with cloud.

Bucket 3 · Strategic platform partners. Nvidia (chips and inference platform), SpaceX/xAI (the Grok models post-merger). These have non-substitutable capabilities — Nvidia for compute substrate, xAI for the Musk-political-alignment-and-satellite-network combination that no other vendor offers.

The strategic consequence: the Pentagon now has eight ways to fail and eight ways to swap. If OpenAI breaches a security review, the Pentagon can shift workload to Google. If Reflection AI’s model underperforms, the Pentagon can move to Nvidia’s hosted partners. If a vendor refuses scope, the Pentagon has seven others. Channel 1 is the redundancy channel because that is exactly the architecture the Pentagon values most.

The eight vendors are also competing with each other for the same $32 billion FY26 DoD AI/cyber/cloud spend pool. The agentic AI contracts awarded in Q1 ($200M each to OpenAI, Google, Anthropic, xAI per the federal procurement coverage) preceded the May 1 split. Anthropic’s Q1 agentic-AI contract is in legal limbo. The other three are now well-positioned for Channel 1 expansion.

3. Channel 2 · The Mythos Channel

Channel 2 is harder to see from the outside because it does not have an announcement, a contract ceiling, or a public list of vendors. It is the channel that exists in the gap between the Pentagon’s supply-chain-risk designation and the operational reality that Pentagon staff continue to use Anthropic tools.

The pivot point is Mythos.

Claude Mythos Preview was unveiled on April 7, 2026. It is Anthropic’s offensive-cybersecurity-capable model — described publicly as “highly adept at finding zero-day or yet-undiscovered cybersecurity vulnerabilities.” It has not been made publicly available. Access is limited. Multiple federal agencies — not just Pentagon-adjacent intelligence agencies — have adopted it.

Pentagon CTO Emil Michael’s public framing of Mythos’s cyber capabilities as “a separate national security moment” is the most strategically important sentence in the entire procurement story. “Separate” is the word that does the work. It positions Mythos outside the supply-chain-risk dispute. It signals that the procurement architecture for Mythos is being treated as a different category — a single-source, capability-driven, exception-based architecture. The kind of procurement the Pentagon uses for capabilities it cannot get from anyone else.

The list of capabilities the Pentagon would put in this single-source category is short. Stealth aircraft. Hypersonic weapons. The intelligence community’s specialized SIGINT systems. Capabilities where the procurement officer’s question is not “which of our seven vendors should we buy this from?” but “is the one company that can do this willing to sell?”

Mythos is in that category. The Pentagon’s behavior makes that explicit. The supply-chain-risk designation prevents formal acquisition of Claude. It does not prevent operational use of Mythos under exception authorities. The injunction in Anthropic’s lawsuit does not require the Pentagon to buy anything; it prevents the Pentagon from formally banning Anthropic. The space between those two limits is exactly large enough to contain a single-source cybersecurity-capability acquisition that operates under a different procurement architecture than the May 1 announcement.

The strategic asymmetry: in Channel 1, the Pentagon has eight vendors competing for procurement budget. In Channel 2, the Pentagon has one vendor providing capability the other eight cannot match. Anthropic’s negotiating position in Channel 2 is structurally stronger than any Channel 1 vendor’s negotiating position in Channel 1.

4. The Industrial-Base Cascade

The supply-chain-risk designation has a second-order effect that extends well beyond the Pentagon itself. It limits the access that defense contractors have to Anthropic’s models. Any contractor working on a defense program now has to weigh whether using Claude in their stack creates compliance friction — even on unclassified work.

This is the part of the story most coverage missed. The defense industrial base is large. Lockheed Martin, RTX, Northrop Grumman, General Dynamics, BAE, L3Harris, and the next ten primes all build AI capabilities into their delivery stacks. Until February 2026, Anthropic was a viable vendor for that stack. Today, in most readings of the designation, it is not.

Three downstream effects, in order of magnitude.

Effect 1 · Defense contractor model migration. Primes that had Anthropic infrastructure baked into delivery pipelines are now migrating away. Replacement choices flow predominantly to Microsoft (Azure OpenAI), Amazon (Bedrock with Anthropic blocked, so Mistral / Llama / Cohere), and Google (Gemini). Each of these gains procurement-driven adoption inside the industrial base independent of model quality. The procurement-driven distribution advantage is real and durable.

Effect 2 · The “compliance friction” tax on smaller AI vendors. Cohere, Mistral, AI21, and the open-weight cohort all face the question of whether their models qualify under the same procurement standards Anthropic was excluded under. The supply-chain-risk designation creates a precedent that smaller vendors will be reviewed against. Most do not have the lobbying or legal resources to navigate this proactively. The result is that they either (a) accept the Pentagon’s standard contractual language preemptively or (b) lose access to defense industrial-base distribution by inaction.

Effect 3 · The international read-across. UK NCSC’s recent warning about AI-accelerated vulnerability discovery sits in the same conceptual frame as the Pentagon’s Mythos handling. UK Ministry of Defence procurement watchers are now examining whether the U.S. supply-chain-risk classification cascades into UK eligibility for sensitive work. France’s defense AI procurement, Germany’s Bundeswehr, Israel’s MOD — all are running internal assessments. The U.S. precedent, regardless of its court outcome, will inform how allied defense ministries approach AI vendor selection. Anthropic’s international defense market is shrinking on the same timeline as its U.S. defense market.

The industrial-base cascade is the part of the supply-chain-risk designation that the courts cannot reverse. Even if Anthropic prevails on the formal designation, the procurement environment around it has shifted. Other vendors have now built defense-distribution relationships that would not have existed in February. Those relationships are durable. The market structure that emerges from the May 1 announcement is the new baseline.

5. Why the Two-Channel Architecture Persists

The natural prediction is that this is temporary. Trump and Amodei reach a deal, the supply-chain-risk designation lifts, Anthropic re-enters Channel 1 alongside the other seven, and the two-channel architecture collapses back into one.

This prediction is probably wrong. Three structural reasons.

Reason 1 · The redundancy logic does not depend on the dispute. Pentagon CTO Emil Michael’s “I need redundancy” statement was made before the May 1 announcement and would have been true regardless of the Anthropic conflict. The Pentagon’s pre-Anthropic-dispute trajectory was already toward multi-vendor classified procurement — JWCC’s four-cloud structure is the precedent. The May 1 announcement accelerated the timeline. It did not invent the architecture. Even if Anthropic returns to Channel 1, it returns as one of nine, not as the pre-2026 dominant vendor.

Reason 2 · Mythos’s capability profile is not easily replicated. OpenAI, Google, Microsoft, and the open-weight cohort have all been working on offensive-cyber-capable models. None has shipped one with Mythos’s specific capability profile. The capability gap may close in 12-18 months — or it may not. Either way, for the period in which it exists, the Pentagon has structural reason to maintain a Channel 2 procurement architecture for capability gaps that do not fit the redundancy model. Mythos is the first one. There will be others. The two-channel architecture, once built, becomes the template for any capability the Pentagon cannot get from a redundant vendor pool.

Reason 3 · The political symmetry favors keeping both channels. Channel 1 distributes Pentagon AI spend across eight vendors with strong Republican-aligned political relationships (xAI especially), satisfying the political coalition that drove the supply-chain-risk designation. Channel 2 keeps the most operationally consequential capability flowing through Anthropic, satisfying the Pentagon staff and intelligence-community personnel who consider Claude superior. Both political constituencies get their preferred outcome. Collapsing back to one channel would force a choice that neither side wants to make.

The two-channel architecture is structurally stable. It will persist beyond the Trump administration. It will likely become the template for federal AI procurement more broadly — multi-vendor commodity AI on one channel, single-source capability AI on a separate channel, with the capability bar set high enough that few vendors qualify for Channel 2 in any given year.

What to Do This Quarter

1. Defense AI vendors: If you are in Channel 1, the next 18 months are a market-share war among eight peers for $32B in addressable spend. The differentiation that wins is integration depth with the GenAI.mil platform, IL6/IL7 deployment speed, and the willingness to compress accreditation timelines. Vendor lock-in to a specific cloud or specific compute substrate works against you.

2. AI vendors not in either channel: The supply-chain-risk designation creates a precedent that smaller vendors will be reviewed against. Be proactive about your defense compliance posture. If you do not have a federal sales motion, the procurement-driven distribution gap to your hyperscaler-distributed competitors is widening monthly.

3. Defense primes and integrators: Your AI delivery stack needs an explicit answer to “what happens if our model vendor gets a supply-chain-risk designation.” The May 1 precedent makes that question operational, not theoretical. Multi-vendor delivery architectures are now a procurement requirement, not a best practice.

4. Anthropic shareholders, secondary buyers, IPO investors: The “multiple billions” of revenue at risk per CFO Krishna Rao are partially offset by Mythos and federal-agency adoption. The full picture will not be visible until Q4 2026 or Q1 2027 disclosures. Until then, model the company’s revenue with both Channel 1 exclusion and Channel 2 inclusion built in. The pre-IPO valuation discussion should incorporate both.

The Strategic Read

The most important fact about the May 1 Pentagon announcement is not that Anthropic was excluded. It is that the Pentagon split AI procurement into two channels — a multi-vendor channel for commodity AI capability, and a single-source channel for frontier capability — and the architecture of that split is now the template for federal AI procurement going forward.

For the eight vendors in Channel 1, the strategic position is volume. They get scale, distribution, GenAI.mil integration, and access to the $32B addressable spend pool. They are also competing with each other for that pool, with the Pentagon explicitly designing the architecture to prevent any one of them from becoming dominant. Channel 1 is structurally low-margin, high-volume, and politically diversified.

For Anthropic in Channel 2, the strategic position is capability rent. Mythos is a single-vendor procurement because no other vendor can match the capability. The capability gap is the moat. The procurement architecture flows around the supply-chain-risk designation through exception authorities. The revenue is smaller in absolute terms than what Anthropic lost in Channel 1, but it is durable in a different way: it depends on continued frontier-capability leadership, not on procurement-officer relationships.

The deeper read is that this is what mature AI procurement looks like. The 2023-2025 period of “let’s just buy Claude” was always going to end. The end-state is segmented procurement where the agency buys redundancy for commodity work and exception-based access for frontier capability. The May 1 announcement is the moment that segmentation became visible at the federal level. It will replicate. State governments, allied defense ministries, regulated enterprise sectors — all of them will eventually arrive at the same architecture.

The companies that win in this architecture are the ones who recognize which channel they are in. Channel 1 vendors compete on integration, deployment speed, and cloud bundling. Channel 2 vendors compete on capability that nobody else has. The middle — vendors who are neither commodity-redundant nor frontier-unique — gets squeezed.

The Pentagon did not exclude Anthropic. The Pentagon told Anthropic which channel it had been routed to. The channel is the more strategically defensible one. The revenue is smaller but more durable. The valuation implication for the upcoming IPO is that the Channel 2 revenue should be modeled separately, with a higher multiple, because it is structurally less substitutable than Channel 1 revenue.

The exclusion narrative is the wrong frame. The two-channel architecture is the frame that survives the next decade.

The Pentagon did not exclude Anthropic. It segmented procurement. Channel 1 is the redundancy channel. Channel 2 is the capability channel. Anthropic is exclusively present in the one that matters more.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. More at ThorstenMeyerAI.com.

Related Dispatches

- Your AI Vendor’s AI Vendor — agent supply chain compromise (Vercel × Context AI)

- Single Digits — the April 2026 open-weight inflection

- AI-Washed — the 47.9% / 9% layoff narrative gap

- The 27% Problem — Anthropic’s enterprise lead and Google’s $750M check

- The Bubble Is Not in Valuations — the productivity gap

- The Agent Trap — why 90% of AI launches are infrastructure liars

- The Channel Move — Anthropic × Wall Street PE channel acquisition

Sources

- CNN Business, Pentagon strikes deals with 8 Big Tech companies after shunning Anthropic (2026-05-01)

- Defense News, Pentagon freezes out Anthropic as it signs deals with AI rivals (2026-05-01)

- SiliconANGLE, Pentagon inks AI procurement deals with seven companies, leaves out Anthropic (2026-05-01)

- Wall Street Journal / gHacks, Pentagon Signs AI Deals With OpenAI, Google, Microsoft, Nvidia (2026-05-04)

- Roborhythms, The Pentagon Just Picked Seven AI Vendors and Anthropic Wasn’t One (2026-05-02)

- Let’s Data Science, Pentagon Signs Eight AI Companies for Classified Networks, Excludes Anthropic (2026-05-01)

- Fed-Spend, Federal AI and Cybersecurity Contract Awards 2026: $32 Billion in Zero Trust, Cloud, and Autonomous Systems (2026-04-19)

- Reuters / Bloomberg coverage of the supply-chain-risk designation (Feb–May 2026)