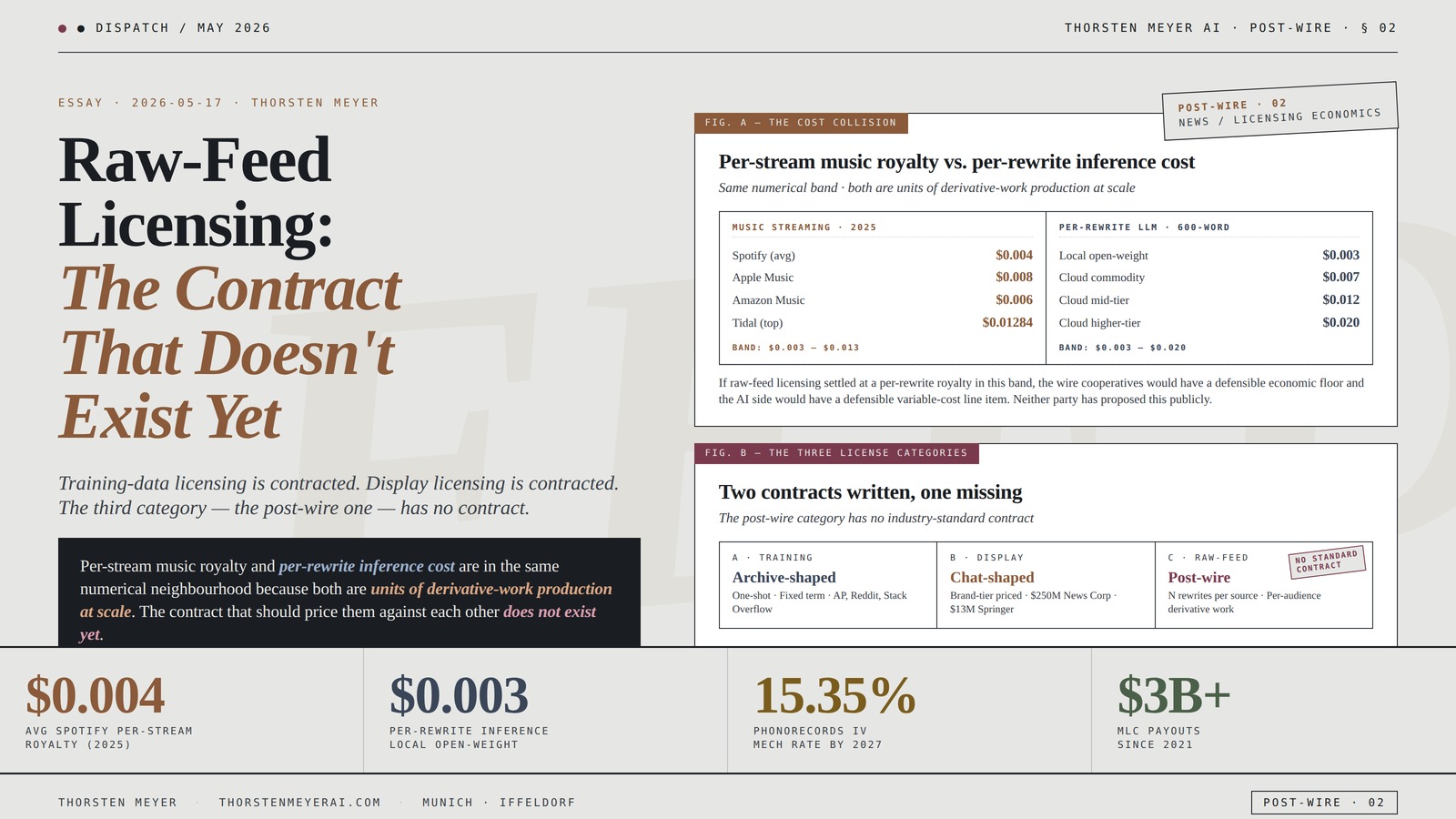

Training-data licensing exists. Display licensing exists. Raw-feed licensing for downstream per-audience rewrite — the third category, the post-wire category, the one the wire cooperatives should be selling — has no industry-standard contract. Spotify pays songwriters roughly $0.004 per stream. Apple Music pays roughly $0.008. The Copyright Royalty Board under Phonorecords IV sets the all-in mechanical streaming royalty at 15.1% of platform revenue in 2023, scheduled to rise to 15.35% by 2027 — a number that traces a continuous legal thread back to the 1909 Copyright Act and the player-piano fight. The marginal cost of one LLM rewrite of a 600-word wire story lands in the same band: $0.003 on local open-weight inference, up to about $0.02 on the higher-tier cloud APIs. The numbers collide. The contract that should price them against each other does not exist yet. Piece 01 of this track flagged the gap; Piece 02 walks through what the contract has to specify, why it isn’t there, who structurally doesn’t want it written, and what shape the answer eventually takes.

By Thorsten Meyer — May 2026

This is Post-Wire Piece 02 — the contract-forensic analysis that follows Piece 01’s structural-economics account of the wire’s collapse. Piece 01 established the cost inversion (per-rewrite inference falling below the cost of identical-paragraph distribution), the three-category licensing framework (training-data · display · raw-feed-for-rewrite), and the labour-economics gap (who pays for the bureau in Kyiv when raw-feed dollars don’t flow back). Piece 02 walks the missing contract category at the centre of that framework — what it has to specify, what it would cost, what historical precedent its scaffolding would have to mirror, who is at the table refusing to write it, and what shape it eventually takes when statutory pressure forces the answer.

The structural argument I want to make: The post-wire era requires a third licensing category — raw-feed licensing for downstream per-audience rewrite — that has no industry-standard contract yet, even though the unit economics that should price it (a per-rewrite royalty in the $0.005-0.02 band) collide cleanly with the music-streaming royalty economics that have existed under statutory compulsory licensing since the 1909 Copyright Act. The contract category is missing because each of the four parties at the table — AI labs, brand-strong publishers, wire cooperatives, search engines — prefers the equilibrium that mis-prices the gap in their favour. This is the contract-forensic crystallization Piece 02 produces, and it sets up the labour-economics, attribution-standard, and statutory-framework essays that follow.

The headline integrative finding: Training-data licensing and display licensing are contracted. Raw-feed licensing for downstream rewrite — the post-wire category — has not been written. The numerical collision with music-streaming royalty economics is structural, not coincidental — both are units of derivative-work production at scale. The legal scaffolding music has (the 1909 Act framework · the 1976 revision · the DPRA 1995 · the MMA 2018 · the CRB · the Mechanical Licensing Collective · $3B+ in payouts since 2021) is the scaffolding raw-feed licensing currently lacks. The 2026 contract gap is the same structural moment music was in around 1908 — after White-Smith v. Apollo and before Congress responded.

This essay walks the three-category framework as it actually stands today (what’s contracted and what isn’t), the six specifications the missing contract has to settle (pricing unit · attribution requirement · derivative-work scope · right-to-ingest · audit and reporting · modification scope), the music-streaming comparison with the cost-collision math (per-stream royalty vs. per-rewrite inference in the same numerical neighbourhood), the TollBit reality (the closest deployed infrastructure and where it stops short), the five contract shapes that could emerge (per-rewrite royalty · per-source-story flat fee · per-endpoint subscription · revenue-share · statutory compulsory), the four-party standoff that prevents resolution (AI labs · brand-strong publishers · wire cooperatives · search engines), and the historical-precedent observation about how these gaps eventually settle.

Raw-Feed Licensing:

The Contract That

Doesn’t Exist Yet

royalty (2025)

local Mac fleet, open-weight

streaming rate by 2027

(scaffolding scale)

Reddit–OpenAI 2024

Stack Overflow–OpenAI 2024

Shutterstock multi-deal

News Corp–Meta $150M/3yr

Axel Springer ~$13M/yr

FT $5–10M/yr · AP–Google

No standard contract.

Contract

via TollBit

via TollBit

by both licenses

as a license type

Per-stream music royalty and per-rewrite inference cost are in the same numerical neighbourhood because both are units of derivative-work production at scale. The contract that should price them against each other does not exist yet.Thorsten Meyer · Raw-Feed Licensing · Post-Wire 02

I · The three license categories today · what’s contracted and what isn’t

The empirical accounting of what’s being sold in 2026. Three structural categories of AI-publisher licensing exist as use-cases. Two are contracted at industry-recognised pricing. The third — the post-wire one — has no industry-standard contract and almost no public deal terms.

Category A · Training-data licensing · archive-shaped · contracted

The empirical signature: archive-shaped (publisher grants AI company access to a back-catalogue of text · AI company uses it to train a model · payment is a fixed sum or sum-plus-credits for a fixed term).

The contracted deals: AP–OpenAI July 2023 (two-year archive license back to 1985 · financial terms undisclosed · first major news–AI deal) · Reddit–OpenAI May 2024 (terms undisclosed) · Reddit–Google February 2024 (~$60M/year for API access) · Stack Overflow–OpenAI May 2024 (developer content licensing) · Shutterstock multi-deal 2023–2024 (image and video).

The structural mechanism: one-shot consumption with no ongoing usage scaling. Most attractive to the AI lab because the cost structure is fixed and predictable. The category is well-understood and the contract structure is mature.

Category B · Display licensing · chat-shaped · contracted at brand-tier rates

The empirical signature: chat-shaped (publisher grants right to display summaries, quotes, logos inside the AI product · with attribution back to the publisher · payment scales with brand authority).

The contracted deals: News Corp–OpenAI May 2024 ($250M over five years across WSJ + NY Post + Barron’s + MarketWatch + others · Factiva and HarperCollins excluded) · News Corp–Meta March 2026 ($150M over three years) · News Corp–Apple October 2025 (“significant” partnership · undisclosed) · Axel Springer–OpenAI December 2023 (~$13M/year over three years covering Politico + Business Insider + Bild + Welt) · Financial Times–OpenAI April 2024 ($5–10M/year reported) · Guardian–OpenAI 2025 · Le Monde–OpenAI 2024 · Prisa Media–OpenAI 2024 · Schibsted–OpenAI 2025 · Dotdash Meredith–OpenAI · Hearst–OpenAI · Vox Media–OpenAI · Condé Nast–OpenAI · AP–Google for Gemini 2025 (first Google AI content deal · real-time news to Gemini · terms undisclosed) · AFP–Mistral 2025 (multi-year · 2,300 stories/day across six languages).

The structural mechanism: the AI is treated as a destination (a chatbot the user reads inside) and the publisher’s content is displayed inside it with link-back attribution. Cumulative publisher-side licensing volume now approximately $2B across all major deals. Category is younger than training-data licensing but is now standardly contracted across most major Western publishers.

Category C · Raw-feed licensing for downstream rewrite · post-wire-shaped · uncontracted

The empirical signature: post-wire-shaped (AI is not a destination but an intermediate processing layer · consumes the source feed · produces N differentiated derivative works for N publication endpoints downstream).

The contracted deals: none with industry-standard pricing structure. The Mistral–AFP deal is structurally closest but priced as display-plus-RAG, not per-rewrite or per-republication. AP and Reuters have no public contract that licenses raw feeds to AI companies for downstream rewrite-and-publish. The contract category exists structurally and is being consumed at scale unlicensed.

The structural mechanism: this is what a newsroom historically did with wire copy — ingest the source, write a version for the local audience, publish under the local masthead with wire attribution. The post-wire architecture (top-N matcher · per-site voice rewrite · attribution preservation · documented in the operator-side companion piece) runs on exactly this category. The cost economics are tractable; the contract is missing.

The three-category observation

The current AI-publisher licensing market has two contracted categories and one structural gap. The gap is the post-wire category specifically — the one the cooperative wire agencies should be selling, the one the per-rewrite inference economics actually map to, and the one no party at the table has yet proposed an industry-standard contract for. This is the empirical setup for everything that follows.

Library Licensing: A Manual for Busy Librarians

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

II · The six specifications the missing contract has to settle · what raw-feed has to specify

The contract-forensic crystallization. Six things a raw-feed-for-rewrite contract has to answer that the two existing categories don’t. Each has large distributional consequences; none has an industry-standard answer yet.

Specification 1 · The pricing unit

The structural question: per source story consumed? Per rewrite produced? Per endpoint published to? Per audience-reached? Per fan-out endpoint?

The distributional consequences: per-source-story flat fee favours volume-publishers · per-rewrite royalty favours fan-out publishers · per-audience-reach royalty favours high-reach brand-strong publishers and disadvantages niche networks · per-endpoint subscription rewards static publication relationships and is hostile to dynamic per-story routing.

The contracting state: different wire agencies will lobby for different units, and the choice will not be neutral. No standard exists yet.

Specification 2 · The attribution requirement

The structural question: machine-readable link back to originating source story? Canonical URL chain that survives N rewrites? Schema.org NewsArticle citation with wire-agency provider field? C2PA-style content-credentials signature?

The architecture gap: display licensing currently mandates attribution at the display layer (the chat interface). Raw-feed licensing has to mandate it at the publication layer (every one of N rewrites). This is harder, more architecturally specific, and structurally tied to the still-unsettled provenance-standard fight.

The contracting state: no industry-standard answer. The provenance-standard work (C2PA · Adobe Content Credentials · IPTC NewsML · the proposed llms.txt extension to robots.txt · the EU AI Act Article 50 transparency obligations) is still in early deployment.

Specification 3 · The derivative-work scope

The structural question: where does “rewrite” end and “substantial transformation” begin?

The music-licensing precedent: Section 115 handles this with the statutory restriction that an arrangement “shall not change the basic melody or fundamental character of the work.” A 12-second pop sample is clearly licensed; a full cover with reordered verses is clearly licensed; a “sound-alike” reconstruction that uses the same chord progression and lyrics but doesn’t reproduce the recording is litigation territory.

The wire analogue: a per-site rewrite that re-frames the story for a defence audience, or adds original analysis, or selects a different lede — still a licensed rewrite or has become a separate work? This matters because it determines how far downstream the wire agency’s royalty claim runs. No industry-standard answer.

Specification 4 · The right to ingest

The structural question: real-time fetch from the source URL (RAG-style)? Licensed feed pipe with retention rights? Polling cadence? Push-based delivery?

The litigation pivot: this is the exact axis the NYT v. Perplexity complaint pivots on. Perplexity argues it is indexing publicly-accessible pages to construct citations (a search-engine activity historically protected under fair use); the NYT argues the AI is ingesting content for downstream substitution, which is not. A raw-feed contract has to specify the ingest mechanism on the front end before it can price the rewrite obligations on the back end.

The contracting state: the legal answer to “what counts as ingestion vs. indexing” is being decided in the SDNY right now. The contract will have to wait on or anticipate that decision.

Specification 5 · The audit and reporting

The structural question: how does the wire agency verify what was published?

The music-licensing precedent: the Mechanical Licensing Collective in music processes ~$3B+ in payouts since 2021 specifically because the audit layer was built into the Music Modernization Act of 2018. Streaming services report play counts to the MLC; the MLC distributes royalties to publishers and songwriters; the audit infrastructure is centralised and statutorily-required.

The wire analogue: a raw-feed deal where the AI company is producing N rewrites across N publication endpoints requires audit infrastructure that does not currently exist. The current display-licensing deals rely on the chatbot publisher reporting usage in good faith. Raw-feed licensing has no equivalent collective and no statutory audit requirement.

Specification 6 · The modification scope

The structural question: can per-site rewrites add original commentary? Change framing? Alter the order of facts? Drop the lede? Add a new lede? Update with later reporting from a different source?

The boundary problem: each of these expands the boundary between “rewrite of the licensed source” and “new work that incorporates the licensed source as one input.” The wider that boundary, the harder it becomes to enforce a per-rewrite royalty without litigating each border-line case.

The contracting state: no industry-standard answer. The closest analogue is music’s “arrangement that doesn’t change basic melody or fundamental character” language from Section 115, but that doctrine has been litigated for over a century and is still contested.

The six-specification observation

None of these six questions has a clean answer. The argument here is not that they’re easy to settle — it’s that nobody is currently in the contract category that would force the settlement. The standoff that produces this is structural, not accidental, and is the subject of Section VI.

Commercial Contracts : A Practical Guide to Deals, Contracts, Agreements and Promises

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

III · The music-streaming comparison · per-stream royalty vs. per-rewrite inference cost

The empirical-collision crystallization. Per-stream music royalty and per-rewrite LLM inference cost sit in the same numerical neighbourhood because both are units of derivative-work production at scale. This is not coincidence — it is structural.

The per-stream music royalty band · 2025

- Spotify · average $0.003–0.005 per stream · approximately 65–70% of platform revenue allocated to rights-holders, distributed pro-rata by stream share

- Apple Music · average $0.006–0.01 per stream · approximately 70% allocated to rights-holders after Apple’s ~30% platform cut

- Amazon Music · average $0.004–0.008 per stream

- Tidal · approximately $0.01284 per stream · highest of the major platforms

- YouTube Music Premium · approximately $0.005–0.007 per stream

- YouTube ad-supported / Content ID · $0.0007–0.00139 per play · dragged down by lower-engagement traffic

The band: roughly $0.003–0.013 per unit across the major platforms, with $0.004 as the Spotify median and $0.008 as the Apple Music median.

The per-rewrite LLM inference cost band · 600-word source

- Local open-weight inference (Mac fleet · Qwen3 MLX models · operator-side environment documented in the DojoClaw companion piece) · approximately $0.003 per rewrite · dominated by electricity

- Cloud commodity models (Claude Haiku · GPT-4o mini · Gemini Flash 2) · $0.005–0.01 per rewrite

- Cloud mid-tier · approximately $0.012 per rewrite

- Cloud higher-tier · up to $0.02 per rewrite at production volumes most fan-out publishers don’t pay

- 50-site fan-out total cost · under $1 at local-inference rates · under $5 at cloud-commodity rates

The band: roughly $0.003–0.020 per unit, with $0.003 as the local-inference floor and $0.02 as the cloud-higher-tier ceiling.

The cost-collision observation

Per-stream music royalty and per-rewrite inference cost are in the same numerical neighbourhood. The order-of-magnitude collision is structural, not accidental — both are units of derivative-work production at scale, distributed across pooled audiences, with marginal-cost economics that compress toward platform-cost-plus-rights-share.

The implication for raw-feed licensing: if a raw-feed royalty settled at $0.005–0.02 per rewrite produced, the wire cooperatives would have a defensible economic floor (within the same band as the music industry pays songwriters), and the AI side would have a defensible variable-cost line item (within the same band as the inference cost already absorbed). Neither party has proposed this publicly. The collision is in the empirical record; the contract is not.

The Phonorecords IV scaffolding

The legal infrastructure music has and news doesn’t. Phonorecords IV — set by the US Copyright Royalty Board in 2022 covering 2023–2027 — establishes the all-in mechanical streaming royalty rate at 15.1% of platform revenue in 2023, rising to 15.35% by 2027. This is the “headline” rate; performance-rights payouts to ASCAP / BMI / SESAC are deducted from it to determine the actual mechanical royalty paid through the Mechanical Licensing Collective.

The MLC has processed over $3B in payouts since launch in 2021 under the Music Modernization Act of 2018. The CRB structure has analogues going back to the 1909 Copyright Act, which set the original mechanical royalty at 2 cents per unit — a rate that did not change for 67 years until the 1976 Copyright Act raised it to 2.75 cents. The current statutory mechanical rate is 12.7 cents per composition (or 2.45 cents per minute, whichever is more) as of 2025.

What’s worth noticing is not the specific numbers but the existence of the structure — the federal rate-setting body, the statutory compulsory licensing regime, the centralised collection collective, the multi-billion-dollar payout history, the 117 years of doctrinal evolution. The post-wire era currently has none of these. The empirical position raw-feed licensing is in resembles the music industry in 1908 — after White-Smith Music Publishing v. Apollo and before the 1909 Act — where the technology has outrun the licensing infrastructure and the question is whether Congress and the rate-setting bodies catch up or whether the market settles on private contracts that lock in unfavourable rates.

raw feed licensing software

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

IV · The TollBit reality · necessary infrastructure, insufficient contract category

The deployed-infrastructure crystallization. The closest existing infrastructure to a raw-feed licensing layer is TollBit. What it actually does is useful precisely because it shows what the missing contract is not.

What TollBit operationally provides

The empirical scale: founded 2023 by Toast alumni Olivia Joslin and Toshit Panigrahi · ~$31M total funding (including a $24M Lightspeed-led Series A on top of seed funding) · approximately 7,000 publisher sites including TIME · Fast Company · Digital Trends · Washington Post Arc XP integration (adds approximately 2,000 publisher properties) · roughly 20% of those publishers currently earn revenue ranging from hundreds to tens of thousands of dollars per month · bot-paywall adoption on the platform reportedly grew 730% between Q4 2024 and Q1 2025.

The operational mechanism: sits behind the bot-detection layer (Cloudflare · Fastly · Akamai · DataDome · HUMAN) · meters AI-bot traffic · lets publishers set rates per 1,000 pages accessed · routes payments · charges AI buyers a transaction fee on top of publisher-set rates · publisher receives the full listed rate.

The platform extension: the MCP-server integration that goes live with one toggle (tollbit.yoursite.com/mcp) is the move toward agent-protocol licensing infrastructure. This is structurally significant — agent-mediated raw access is the architectural pattern raw-feed licensing will operate on.

TollBit’s two existing license types

Summarization License: allows the AI customer to access a page once to create “a summary, grounding, or citation.” Pricing per 1,000 pages accessed. Closest current analogue to the citation economy.

Full Display License: allows the AI customer to display the complete text of an article once. Pricing per 1,000 pages, benchmarked against syndication rates. Closest current analogue to lightweight syndication.

What both license types explicitly do not permit: model training. What neither license type addresses: ingestion-and-rewrite for downstream republication — the raw-feed-for-rewrite use case.

The TollBit gap observation

The infrastructure for metered, per-unit, publisher-set AI-bot pricing now exists; the contract category that infrastructure should be carrying is not yet built into the platform. TollBit’s two license types are both citation-economy primitives, not raw-feed-rewrite-economy primitives.

What this means in practice: a wire agency that wanted to license raw feed for downstream rewrite via TollBit today would have to use the Full Display license, which is priced for one-time complete-text display and prohibits the actual use case (further republication after transformation). The infrastructure is not blocking raw-feed licensing — it’s just not yet contracted to enable it.

The structural reading: TollBit is necessary infrastructure but insufficient contract category. Whoever drafts the first raw-feed-rewrite license type for TollBit — or for Skyfire, Cloudflare AI Audit, the proposed llms.txt extensions, or any of the other emerging publisher-AI rails — establishes precedent for what the broader industry-standard contract eventually looks like. That license type has not been drafted yet, by anyone.

Social Work Licensing Clinical Exam Guide: Comprehensive ASWB LCSW Exam Review with Full Content Review, 500+ Total Questions, and Practice Exams

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

V · The five contract shapes that could emerge · what the answer could look like

The forward-shape crystallization. Five plausible structures for the missing contract. Scored on near-term feasibility. None currently leading. The shape that wins determines who captures the value.

Shape A · Per-rewrite royalty · music-streaming model

The structure: the wire agency receives $0.005–0.02 per per-site rewrite produced from a source story, with rates negotiated against the inference-cost band. Pro-rata pool model possible if multiple wire agencies sell into the same blanket framework.

The strengths: unit economics map cleanly onto per-rewrite inference cost · distributional logic is transparent · audit is conceivable using the same provenance-attribution infrastructure that solves the trust-signal problem · the music-streaming precedent is well-understood.

The weaknesses: requires audit infrastructure that doesn’t exist · requires AI companies to commit to a variable-cost line item they currently resist.

Near-term feasibility: medium.

Shape B · Per-source-story flat fee · modified wire-subscription

The structure: the wire agency receives a fixed payment per source story consumed by the AI, regardless of fan-out volume downstream. Tiered by audience reach or AI-product class.

The strengths: simpler to administer · mirrors existing wire-subscription unit economics (AP’s “Member Choice” charges by circulation tier, not by story-output count) · avoids fan-out audit overhead.

The weaknesses: under-prices high-fan-out usage and over-prices low-fan-out · gives the AI company unbounded downstream production rights for a fixed upstream cost — which is exactly the value-capture asymmetry the wire agencies are trying to escape.

Near-term feasibility: high.

Shape C · Per-endpoint subscription · extends existing AP/Reuters model

The structure: the AI company pays a subscription per downstream publication endpoint served from the wire feed, on the model of how AP currently charges per newspaper subscriber.

The strengths: most directly extends current cooperative-subscription economics into the AI era · no new audit infrastructure.

The weaknesses: assumes static publication relationships · breaks down for dynamic per-story routing where the set of publication endpoints is determined story-by-story by a matcher — which is the actual post-wire architecture.

Near-term feasibility: medium.

Shape D · Revenue-share on AI-attributed traffic

The structure: the AI company shares advertising and subscription revenue derived from content traceable to the wire feed.

The strengths: aligns incentives · ties licensing dollars to actual realised value.

The weaknesses: requires attribution-traffic measurement that doesn’t currently exist (TollBit’s analytics are the closest) · revenue-sharing splits are litigation-heavy historically · the TollBit study cited in the NYT v. Perplexity complaint — finding AI search engines send 96% less referral traffic than classic search — suggests the realised traffic value is already collapsing toward zero before the contract is signed.

Near-term feasibility: low.

Shape E · Statutory compulsory licensing · CRB-equivalent for news

The structure: a federal rate-setting body (a Copyright Royalty Board analogue for news, or an expansion of the existing CRB’s scope under amended legislation) sets a statutory royalty rate that any AI company can obtain a compulsory license at.

The strengths: stops private-contract underpricing · distributes rate-setting authority outside the parties most interested in mispricing · mirrors the structure that has worked for music for 117 years · long-term stable.

The weaknesses: requires legislative action · will not happen quickly · requires the industry to define “wire copy” as a copyright category eligible for compulsory licensing — currently it isn’t.

Near-term feasibility: low (slow timeline; high long-term likelihood).

The five-shape integrative observation

Near-term feasibility is not the same as long-term likelihood. The historical pattern (mechanical · broadcast · cable) suggests Shape E — statutory compulsory licensing — is where these gaps eventually settle, on a 5–15 year timeline. The near-term outcomes (Shape A or B) will set the precedent the statutory regime eventually formalises. Whoever drafts the first major Shape A or B contract has disproportionate influence on what Shape E ends up codifying a decade later. This is the contract-precedent dynamic the parties at the table understand but the discourse mostly doesn’t.

VI · The four-party standoff · who structurally doesn’t want this contract written

The structural-incentive crystallization. The reason raw-feed licensing has no contract yet is that no party currently at the table wants to write one. Four parties. Four distinct refusal patterns. The standoff is structural.

Party 1 · The AI labs · prefer training-and-display licensing

The incentive: both training-data and display licensing are bulk and one-shot from the AI lab’s perspective · neither scales variable cost with usage · neither creates a line item that grows as the model is used more.

The contracting state: OpenAI · Anthropic · Google · Mistral · Meta have all paid eight- and nine-figure sums for training and display licensing. None has accepted a per-rewrite raw-feed structure publicly.

The refusal pattern: a per-rewrite royalty (or any usage-indexed raw-feed contract) creates an unbounded variable cost that the AI lab’s financial planning — currently structured around fixed compute and fixed licensing expenditures — is hostile to. The AI labs prefer the status quo because the status quo is fixed-cost.

Party 2 · The brand-strong publishers · prefer display licensing because the dollars accrue to them

The incentive: the existing display-licensing dollar volume flows to the brands with strongest demand-side recognition inside AI assistants · News Corp · the Murdoch titles · the FT · Axel Springer · the Springer-tier nationals · these brands capture the current dollars without revenue-sharing.

The contracting state: News Corp’s $250M / 5-year + Meta $150M / 3-year + Apple “significant” + FT $5–10M/year + Axel Springer ~$13M/year · these flow to the brand-strong, not to the wire cooperatives whose original reporting underpins many of those brand-strong stories.

The refusal pattern: a raw-feed licensing standard would route some of those dollars to the cooperatives, which is a reduction in the brand-strong publishers’ net take. The publishers most willing to advocate publicly for raw-feed licensing are the ones currently capturing the least display-licensing revenue — which is also the ones with least negotiating leverage.

Party 3 · The wire cooperatives · need the contract category most, worst-positioned to draft it

The structural constraint: AP is a not-for-profit member cooperative whose members are the publishers · its negotiating posture is constrained by the fact that its members are simultaneously its customers and the parties downstream of any raw-feed contract.

Reuters’ constraint: owned by Thomson Reuters · publicly traded subsidiary inside a broader information-services business · its negotiating posture is shaped by the Thomson terminal-revenue business model · structurally different from selling raw feeds to AI companies.

AFP’s constraint: state-supported French agency with a different governance constraint again · Mistral–AFP 2025 deal is suggestive but isn’t structured as raw-feed-rewrite.

The coordination gap: none of the three has the structural position the music industry’s RIAA had when it pushed for the 1909 Act — a unified, well-funded rights-holder coalition acting against the technology party. The parties who need a raw-feed standard most are also the parties least able to coordinate on one.

Party 4 · The search engines (Google in particular) · prefer derivation opacity

The incentive: a raw-feed royalty regime would force per-source accounting in a way that current undisclosed-derivation models do not. Google has paid AP for Gemini-display licensing; what it has not done is signed a structure that requires it to report the derivation share of AI-generated answers back to the wire agency.

The refusal pattern: a raw-feed contract by definition forces this disclosure. Google’s posture is, predictably, to prefer the display structure that doesn’t require the disclosure. The Penske Media v. Google suit (September 2025) — the first major US publisher to sue Google over AI summaries — is the visible pressure on this preference.

The four-party standoff observation

The near-term equilibrium produced by these four parties’ preferences is the current standoff: training-data licensing is contracted · display licensing is contracted at brand-tier rates · raw-feed-for-rewrite happens unlicensed in the gap between the categories. This is not a stable equilibrium — the lawsuits described in Piece 01 are the visible pressure on it — but it is, in mid-2026, the equilibrium that is holding.

VII · The shape of a standard · how this resolves

The historical-precedent crystallization. The post-wire era needs a raw-feed licensing standard the way music needed mechanical royalty rates after the player-piano fight of 1908 and broadcast needed compulsory licensing after the 1976 Act. The mechanism that has historically resolved these gaps is not industry self-organisation — it is statutory intervention.

The historical pattern · technology outruns licensing, statutory intervention follows

1908 · White-Smith v. Apollo: the Supreme Court rules piano rolls are not “copies” of sheet music because humans can’t read them. Songwriters lose at the Court · mechanical reproduction unregulated.

1909 · Copyright Act: Congress overrides the Court · creates the first compulsory mechanical license at 2¢ per unit · the original statutory rate-setting precedent.

1976 · Copyright Act revision: rate raised from 2¢ to 2.75¢ after 67 years frozen · Section 115 framework retained · compulsory licensing extended to new media.

1995 · Digital Performance Right in Sound Recordings Act: extends mechanical licensing to digital downloads · acknowledges new technology forms.

2018 · Music Modernization Act: establishes the Mechanical Licensing Collective · blanket licensing for digital streaming · centralised collection infrastructure.

2023–2027 · Phonorecords IV (CRB): sets all-in mechanical streaming royalty rate at 15.1% → 15.35% of platform revenue · current statutory mechanical rate 12.7¢ per track.

The pattern across 117 years: technology outruns licensing · lawsuit fails to protect rights-holders · Congress intervenes statutorily · rate-setting body resolves per-unit pricing · collective handles administration. News raw-feed licensing is currently at the “technology outruns licensing” step. The intervening steps will, on historical pattern, eventually follow — but they take decades.

The political question for the next 24 months

Which path does the news industry take? The wire cooperatives (AP · Reuters · AFP · the second-tier nationals like dpa and ANSA) could coordinate on a raw-feed licensing standard that the AI labs can sign into. The Murdoch and Springer-tier publishers could preempt them with a brand-led licensing standard that does not fund the cooperatives’ bureau infrastructure.

The first path preserves the cooperative wire model. The second extends the post-wire era’s value capture toward brand-strong publishers and away from original-reporting funders. Neither is preordained.

The structural-inevitability observation

What is preordained, structurally, is that raw-feed licensing as a category will not stay un-contracted. The economic pressure produced by the cost inversion described in Piece 01 — per-rewrite inference falling below the cost of identical-paragraph distribution — guarantees the AI fan-out model will keep growing. The lawsuits will produce some form of legal forcing-function. The infrastructure platforms (TollBit · Skyfire · Cloudflare AI Audit · the proposed llms.txt standard · schema.org’s expanded provenance vocabulary) will keep building the metering and attribution rails. The contract will, eventually, be written.

The question is who writes it, who pays into it, and where the dollars route. Those are political and economic questions that the parties currently in the room have not yet been forced to answer. They will be. The contract that does not exist yet will exist, and it will look like something. What it looks like determines whether the bureau in Kyiv stays funded or doesn’t.

That is the structural editorial question raw-feed licensing is sitting on top of. It does not have a single answer, and anyone offering one is selling something.

Piece 02 of the post-wire track closes here. The empirical-evidence foundation is complete: three categories accounted for, six specifications surfaced, the cost collision quantified, the deployed infrastructure mapped, the five contract shapes scored, the four-party standoff structurally explained, the historical-precedent pattern named. Piece 03 picks up the attribution-standard question — the provenance layer raw-feed licensing depends on — that Specification 2 in Section II flagged but did not resolve.

About the Author

Thorsten Meyer is a Munich-based futurist, post-labor economist, and recipient of OpenAI’s 10 Billion Token Award. He spent two decades managing €1B+ portfolios in enterprise ICT before deciding that writing about the transition was more useful than managing quarterly slides through it. He runs StrongMocha News Group, a network of more than 450 niche WordPress magazines built on the DojoClaw editorial engine — the same operator-side context that produces the per-rewrite inference-cost figures used as the empirical baseline in this piece. More at ThorstenMeyerAI.com.

Related Reading · the Post-Wire track

The post-wire track · contract and economics

- Post-Wire Piece 01 · The death of the identical paragraph · the structural-economics account of the wire’s collapse · the three-category licensing framework · the cost inversion that produces the post-wire era · structural-slate register

- This piece · Post-Wire Piece 02 · Raw-feed licensing · the contract-forensic analysis of the missing third category · empirical-clay register

- Forthcoming · Post-Wire Piece 03 · the attribution-standard layer · provenance infrastructure raw-feed licensing depends on (C2PA · Content Credentials · schema.org · llms.txt · EU AI Act Article 50) · transition-bronze register

- Forthcoming · Post-Wire Piece 04 · the labour-economics piece · who pays for the bureau in Kyiv when the raw-feed dollars don’t flow back · labor-rose register

- Forthcoming · Post-Wire Piece 05 · what the wire got right · the cooperative-model pre-mortem · synthesis-deep register

The operator-side companion · published

- Read the world, then publish · Inside the DojoClaw + Stenvrik loop · the operator-side technical account of the per-site rewrite engine · top-N matcher · Readability fail-soft · attribution preservation · status truth-source rule · the empirical baseline for the per-rewrite inference-cost figures used in Section III of this piece

Cross-franchise links

- DojoClaw · the editorial engine itself · 78,000+ articles · 361M+ words · 450+ WordPress magazines

- Stenvrik · the upstream news globe · 227 RSS sources · 24 topics · 49 cities · refreshed every ten minutes

- StrongMocha News Group · the publisher portfolio that the post-wire economics described here are actually running through

Sources

Music-streaming royalty rates and Phonorecords IV framework

- Unchained Music · Spotify Royalty Calculator · Spotify $0.003–0.005/stream · Apple Music $0.006–0.01 · YouTube $0.001 · current 2025 averages

- MusicDemo · Music Streaming Payouts Ranked 2025 · pro-rata pool mechanics · platform-by-platform breakdown · Tidal $0.01284 highest

- Orphiq · Apple Music per-stream rate · ~30% Apple platform cut · 70% to rights-holders pro-rata

- Musicstax · Royalty Calculator · pro-rata-pooling per-country revenue allocation · $1,000 takes ~300,000 Spotify streams / 125,000 Apple Music streams

- Royalty Exchange · Mechanical Royalties · Phonorecords IV 15.1% (2023) → 15.35% (2027) all-in streaming rate · MLC $3B+ payouts since 2021 · current 12.7¢/track statutory rate

- Groover · Spotify Royalty Calculator 2026 · 1 million Spotify streams = $3,000–4,000 · current 2025–2026 averages

Mechanical license history and statutory framework

- 17 U.S. Code § 115 · Cornell Legal Information Institute · statutory text governing music compulsory licensing · the legal scaffolding raw-feed licensing currently lacks

- Mechanical License · Wikipedia · 1909 Copyright Act · Section 115 framework · White-Smith v. Apollo 1908 precedent · 2¢ → 12.7¢ rate history

- Fair Trade Music International · Mechanical Rate · 1909 (2¢) → 1976 (2.75¢) → 1989 (5.7¢) → 2006 (9.1¢) → 2025 (12.7¢) rate evolution · 67 years frozen at 2¢

- Pay for Play · Mechanical Rights · Phonorecords IV CRB private-negotiation settlement August 2022 · 15.1%/15.2%/15.25%/15.3%/15.35% phase-in 2023–2027

- UpCounsel · Compulsory Mechanical License · Section 115 NOI procedures · statutory royalty calculation methodology

- Royalty Exchange · Mechanical Royalties · Music Modernization Act 2018 · MLC creation · digital streaming blanket licensing

TollBit and emerging publisher-AI infrastructure

- TollBit Publisher Marketplace documentation · Summarization + Full Display license types · per-1,000-pages pricing · publisher keeps 100% · transaction fee on top

- TollBit · MCP-server integration · agent-mediated raw access via tollbit.yoursite.com/mcp · move toward agent-protocol licensing infrastructure

- Media Copilot · Why publishers choose TollBit · ChatGPT 87.8% of AI-bot traffic at Digital Trends · 3.6M monthly scrapes

- Reviews.thewindowsclub.com · TollBit review · ~7,000 publisher sites · 20% earning revenue · $24M Lightspeed Series A · $31M total funding · 730% Q4 2024 → Q1 2025 bot-paywall growth

- Playwire · Washington Post Arc XP × TollBit · 2,000+ Arc XP publisher properties added to TollBit marketplace · January 2025 integration

- Monetizationworks · TollBit analysis · publisher rate-card mechanics · marketplace operations

- Media Copilot · Digital Trends TollBit deployment · bot-paywall implementation · revenue-realisation patterns

AI-publisher licensing deal economics

- PR News · AI Licensing Tracker · ~$2B cumulative publisher-side deal volume · News Corp–OpenAI $250M/5yr · News Corp–Meta $150M/3yr · Reddit–Google $60M/yr · Axel Springer–OpenAI ~$13M/yr · FT–OpenAI $5–10M/yr

- Digiday · 2025 AI-deals timeline · OpenAI / Google / Meta / Mistral / Apple chronology · Axios · AP · Guardian · AFP · Schibsted · Hearst · News Corp deals

- Digiday · 2024 AI-deals timeline · News Corp–OpenAI $250M deal documentation · WSJ source reporting

- VCPost · News Corp–OpenAI deal · Robert Thomson / Sam Altman framing · Factiva and HarperCollins exclusions

- Axios · AP–OpenAI deal · July 13 2023 · first major news-AI deal · two-year archive license back to 1985

- MediaAndTheMachine Substack · The 7 Deal Points of AI Content Licensing · contract-structure analysis · News Corp $250M deal components · Curiosity Stream $19.6M projection 2025

Wire-agency pricing and structure

- Journalism.co.uk · AP Member Choice pricing · AP Breaking News + AP Complete tiers · circulation-indexed since 1984 · $21M annual member assessments returned 2009

- CBS News · AP To Charge For Web Content · early online-licensing rationale · ~300 commercial web buyers including Yahoo · AOL · MSN at the time

- Sports Journalists Forum · What does AP cost · small daily ~$400/week historical baseline · AP photo archive ~$40-60 per photo

- Vendr · Thomson Reuters software pricing analysis 2026 · opaque negotiated contracts · named-user licensing · add-ons 20–50% over base · annual maintenance 15–22% of license cost

- Wikipedia · Associated Press · revenue mix (US newspapers 30% → 10%, 2007 → 2024) · 235 bureaus / 94 countries · 128M monthly visits

- Wikipedia · Reuters · 2,500 journalists / 200 locations · 105M monthly readers · founded 1851

Companion-piece source backbone

- Post-Wire Piece 01 · The Death of the Identical Paragraph · Thorsten Meyer · structural-economics account · the three-category framework this piece extends · NYT v. Perplexity citation · Bartz v. Anthropic $1.5B settlement · 96% TollBit referral-traffic finding

- Read the World, Then Publish · Thorsten Meyer · DojoClaw + Stenvrik operator-side technical account · 78,000+ articles · 361M+ words · 450+ WordPress magazines · per-rewrite inference economics baseline

Key Piece 02 reference figures crystallized

- Three license categories · training-data + display (both contracted) + raw-feed-for-rewrite (uncontracted)

- Six contract specifications missing · pricing unit + attribution requirement + derivative-work scope + right-to-ingest + audit/reporting + modification scope

- Cost-collision band · music streaming $0.003–$0.013 / per-rewrite inference $0.003–$0.020 · same numerical neighbourhood

- Music-licensing legal scaffolding age · 117 years (1909 → 2026) · 4 major Acts · 1 federal rate-setting body · 1 centralised collection collective · $3B+ payouts

- TollBit operational scale · 7,000 publisher sites · 20% earning · $24M Series A · 730% growth · 2 license types · 0 covering raw-feed-rewrite

- Five contract shapes · per-rewrite royalty + per-source flat fee + per-endpoint subscription + revenue-share + statutory compulsory · feasibility med/high/med/low/low-slow

- Four-party standoff · AI labs + brand-strong publishers + wire cooperatives + search engines · all preferring the current mis-pricing

- Historical-precedent timeline · 1908 White-Smith → 1909 Act → 1976 revision → 1995 DPRA → 2018 MMA → 2023–27 Phonorecords IV · the pattern raw-feed licensing has not yet entered